Applied Business Finance: Performance Analysis and Improvement

VerifiedAdded on 2023/06/13

|12

|2590

|182

Report

AI Summary

This report provides an analysis of applied business finance, focusing on financial statement interpretation and performance evaluation. It covers key aspects of financial management, including financial planning, resource allocation, and investment strategies. The report details the components of financial statements such as cash flow statements, balance sheets, income statements, and statements of shareholder equity. Ratio analysis is employed to assess the company's liquidity, profitability, and efficiency, using metrics like quick ratio, current ratio, and asset turnover ratio. A business review template is used to analyze turnover, profit, and shareholder equity. The report concludes with recommendations for improving liquidity by managing current assets and liabilities, and enhancing efficiency through better receivables management and cost control. The analysis underscores the importance of regular financial statement analysis for maintaining a healthy financial position and achieving business goals. Desklib provides various study tools and resources to help students with similar assignments.

APPLIED BUSSINESS

FINANCE.

FINANCE.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Section 1.......................................................................................................................................3

MAIN BODY...................................................................................................................................3

Section 2.......................................................................................................................................3

Section 3.......................................................................................................................................5

Section 4 ......................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................2

INTRODUCTION...........................................................................................................................3

Section 1.......................................................................................................................................3

MAIN BODY...................................................................................................................................3

Section 2.......................................................................................................................................3

Section 3.......................................................................................................................................5

Section 4 ......................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................2

INTRODUCTION.

Section 1

Financial management is defined as planning, organizing and controlling the activities

related to finances of the organization. It is useful in preparing short term and long term financial

plans of the organization (Brigham and Ehrhardt, 2019). It identifies where a firm should invest,

how much is the liquidity and profitability of the enterprise. Financial management has two basic

aspects' procurement of funds and utilization of funds.

Importance of Financial Management.

1. FM is important for the financial planning, it helps the organization in deciding the needs

and use of finances.

2. FM helps in managing the financial resources to achieve the goals of the business. To

avoid overspending and lack of finances it is necessary to manage and invest the funds

wisely.

3. It helps the organization in effective allocation of the funds. It decides the amount of

funds required for the projects thus enhancing the capital and minimizing the business

expenses.

4. It helps in ensuring tax planning to avoid loopholes and extra tax payments by the

organization.

5. Financial management helps in getting higher investment returns by investing funds in

the profitable ventures.

MAIN BODY

Section 2

Financial Statements are the records in written form which specifies the financial

activities and performance of the business or individual (Hasanaj and Kuqi,2019). These

statements are audited by accountant firms, government agencies or auditors to determine the

true and fair view of the statements. Financial Statements are of four types:

Cash Flow Statement : These statements are used by the organization the cash inflows

and outflows in a period. Cash flow statements are prepared to ascertain that company

have maintained the cash assets to pay off its liabilities and expenses. The statement is

prepared with the help of Balance sheet and income statement, it determines that whether

there is cash generation in the company or not. The three parts of the CFS determine the

Section 1

Financial management is defined as planning, organizing and controlling the activities

related to finances of the organization. It is useful in preparing short term and long term financial

plans of the organization (Brigham and Ehrhardt, 2019). It identifies where a firm should invest,

how much is the liquidity and profitability of the enterprise. Financial management has two basic

aspects' procurement of funds and utilization of funds.

Importance of Financial Management.

1. FM is important for the financial planning, it helps the organization in deciding the needs

and use of finances.

2. FM helps in managing the financial resources to achieve the goals of the business. To

avoid overspending and lack of finances it is necessary to manage and invest the funds

wisely.

3. It helps the organization in effective allocation of the funds. It decides the amount of

funds required for the projects thus enhancing the capital and minimizing the business

expenses.

4. It helps in ensuring tax planning to avoid loopholes and extra tax payments by the

organization.

5. Financial management helps in getting higher investment returns by investing funds in

the profitable ventures.

MAIN BODY

Section 2

Financial Statements are the records in written form which specifies the financial

activities and performance of the business or individual (Hasanaj and Kuqi,2019). These

statements are audited by accountant firms, government agencies or auditors to determine the

true and fair view of the statements. Financial Statements are of four types:

Cash Flow Statement : These statements are used by the organization the cash inflows

and outflows in a period. Cash flow statements are prepared to ascertain that company

have maintained the cash assets to pay off its liabilities and expenses. The statement is

prepared with the help of Balance sheet and income statement, it determines that whether

there is cash generation in the company or not. The three parts of the CFS determine the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company 's value for the investors. The activities of Cash Flow statements are divided

into three parts:

Operating Activities or Cash Flow from Operations : The first part of the statement

specifies outflow and inflow of cash from the operational activities of the business. In

these activities all non cash items are reconciled with the cash items with all the

operational activities, thus determining the net income of the company in cash form.

Investing activities : The second part of CFS determines the inflow and outflow of cash

from the investing activities, it determines the changes occurred in the capital expenditure

as if decrease in capital expenditure determines cash flow reduction which means either

company making investments or bearing loss and if cash flow increases it determines the

growth of companies.

Financing Activities: This part of CFS specifies the cash used by the business in

financing. The outflow or inflow of cash between the owners, company and its creditors

in way of debt or equity (Anyushenkova and Samorukova, 2019). These activities

determine the payment of dividends, buyback of shares, paying or borrowing of loans,

etc.

Balance Sheet: It is a financial statement prepared by the company to ascertain the

shareholder's equity, reserves, assets and liabilities of a specific period. Balance sheet is

used by to calculate the financial ratios and analyse the financial health of business.

It helps in determining the net worth of the company and identify whether a business has

enough cash and assets to pay off liabilities (CREȚU, Iova and Năstase, 2019). There are

three components in the balance sheet assets, liabilities and shareholder's equity.

Income Statement : It is a statement prepared to determine the income and expenditure

of the business. It shows that company is having profit or loss in that period. It is an

important financial statement used with the balance sheet and C FS to ascertain the

financial position of business. It is also known as earnings statements or profit or loss

statement. Income statement is used by the owners to determine the efficiency of business

strategies formulated for higher profits and cost reduction.

Statement of Shareholder's Equity:It is the financial statement which is prepared from

the balance sheet, it is termed as a part of balance sheet. It specifies the changes in equity

value of the shareholders from the beginning to the end of accounting period. Equity of

into three parts:

Operating Activities or Cash Flow from Operations : The first part of the statement

specifies outflow and inflow of cash from the operational activities of the business. In

these activities all non cash items are reconciled with the cash items with all the

operational activities, thus determining the net income of the company in cash form.

Investing activities : The second part of CFS determines the inflow and outflow of cash

from the investing activities, it determines the changes occurred in the capital expenditure

as if decrease in capital expenditure determines cash flow reduction which means either

company making investments or bearing loss and if cash flow increases it determines the

growth of companies.

Financing Activities: This part of CFS specifies the cash used by the business in

financing. The outflow or inflow of cash between the owners, company and its creditors

in way of debt or equity (Anyushenkova and Samorukova, 2019). These activities

determine the payment of dividends, buyback of shares, paying or borrowing of loans,

etc.

Balance Sheet: It is a financial statement prepared by the company to ascertain the

shareholder's equity, reserves, assets and liabilities of a specific period. Balance sheet is

used by to calculate the financial ratios and analyse the financial health of business.

It helps in determining the net worth of the company and identify whether a business has

enough cash and assets to pay off liabilities (CREȚU, Iova and Năstase, 2019). There are

three components in the balance sheet assets, liabilities and shareholder's equity.

Income Statement : It is a statement prepared to determine the income and expenditure

of the business. It shows that company is having profit or loss in that period. It is an

important financial statement used with the balance sheet and C FS to ascertain the

financial position of business. It is also known as earnings statements or profit or loss

statement. Income statement is used by the owners to determine the efficiency of business

strategies formulated for higher profits and cost reduction.

Statement of Shareholder's Equity:It is the financial statement which is prepared from

the balance sheet, it is termed as a part of balance sheet. It specifies the changes in equity

value of the shareholders from the beginning to the end of accounting period. Equity of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

shareholders is calculated as difference between the total assets and liabilities of the

company. SH's equity means the amount invested by the owners of the company.

Use of Ratios:

Ratio Analysis is used by the companies to analyse and interpret the financial statements.

There are various ratios which helps in determining the strength and weakness of the company

(Dance and Imade, 2019.). The ratios include current ratio, quick ratio, debtors turnover ratio,

operating margin ratio, net profit ratio, etc. The ratio analysis helps the financial management in

many ways :

Ratios help the management in planing and forecasting the financial needs of the

company.

It helps in coordinating the activities of the business, thus ensuring effective

communication of the needs and weaknesses of the company.

Ratios help in controlling he business activities. It is used to compare the expected results

with the actual results to avoid mismanagement of the finances.

Ratios help the investors to evaluate the financial and profitability position of the

business.

Section 3

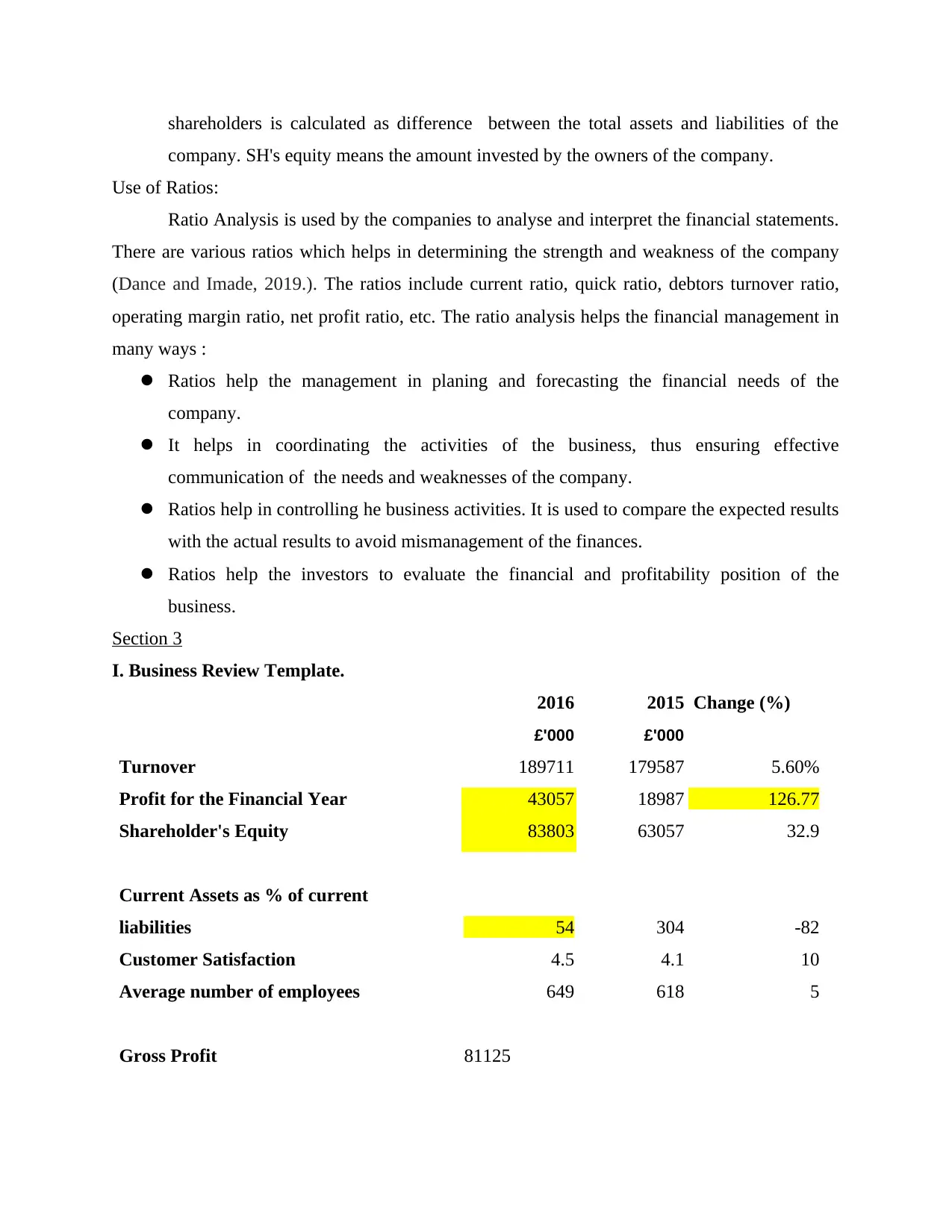

I. Business Review Template.

2016 2015 Change (%)

£'000 £'000

Turnover 189711 179587 5.60%

Profit for the Financial Year 43057 18987 126.77

Shareholder's Equity 83803 63057 32.9

Current Assets as % of current

liabilities 54 304 -82

Customer Satisfaction 4.5 4.1 10

Average number of employees 649 618 5

Gross Profit 81125

company. SH's equity means the amount invested by the owners of the company.

Use of Ratios:

Ratio Analysis is used by the companies to analyse and interpret the financial statements.

There are various ratios which helps in determining the strength and weakness of the company

(Dance and Imade, 2019.). The ratios include current ratio, quick ratio, debtors turnover ratio,

operating margin ratio, net profit ratio, etc. The ratio analysis helps the financial management in

many ways :

Ratios help the management in planing and forecasting the financial needs of the

company.

It helps in coordinating the activities of the business, thus ensuring effective

communication of the needs and weaknesses of the company.

Ratios help in controlling he business activities. It is used to compare the expected results

with the actual results to avoid mismanagement of the finances.

Ratios help the investors to evaluate the financial and profitability position of the

business.

Section 3

I. Business Review Template.

2016 2015 Change (%)

£'000 £'000

Turnover 189711 179587 5.60%

Profit for the Financial Year 43057 18987 126.77

Shareholder's Equity 83803 63057 32.9

Current Assets as % of current

liabilities 54 304 -82

Customer Satisfaction 4.5 4.1 10

Average number of employees 649 618 5

Gross Profit 81125

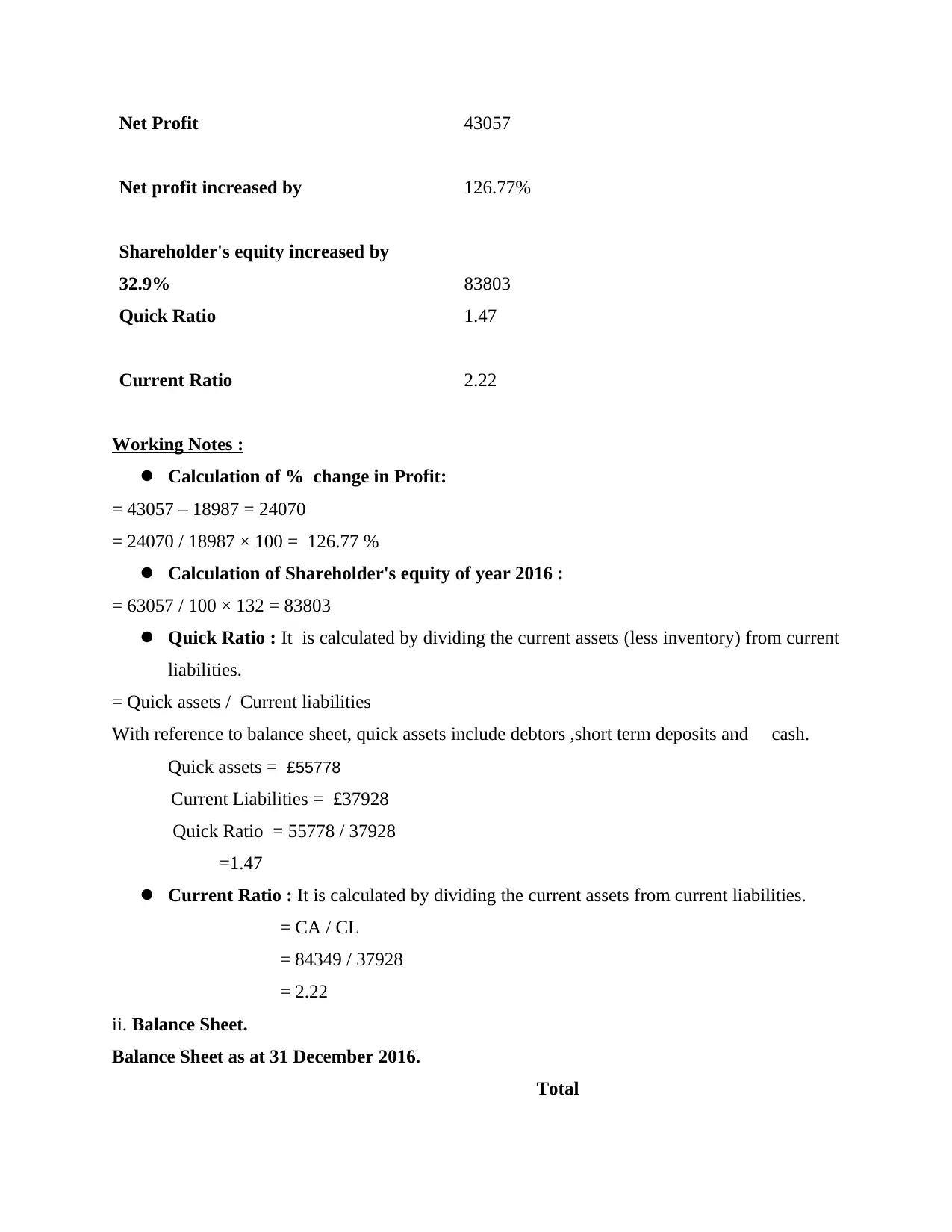

Net Profit 43057

Net profit increased by 126.77%

Shareholder's equity increased by

32.9% 83803

Quick Ratio 1.47

Current Ratio 2.22

Working Notes :

Calculation of % change in Profit:

= 43057 – 18987 = 24070

= 24070 / 18987 × 100 = 126.77 %

Calculation of Shareholder's equity of year 2016 :

= 63057 / 100 × 132 = 83803

Quick Ratio : It is calculated by dividing the current assets (less inventory) from current

liabilities.

= Quick assets / Current liabilities

With reference to balance sheet, quick assets include debtors ,short term deposits and cash.

Quick assets = £55778

Current Liabilities = £37928

Quick Ratio = 55778 / 37928

=1.47

Current Ratio : It is calculated by dividing the current assets from current liabilities.

= CA / CL

= 84349 / 37928

= 2.22

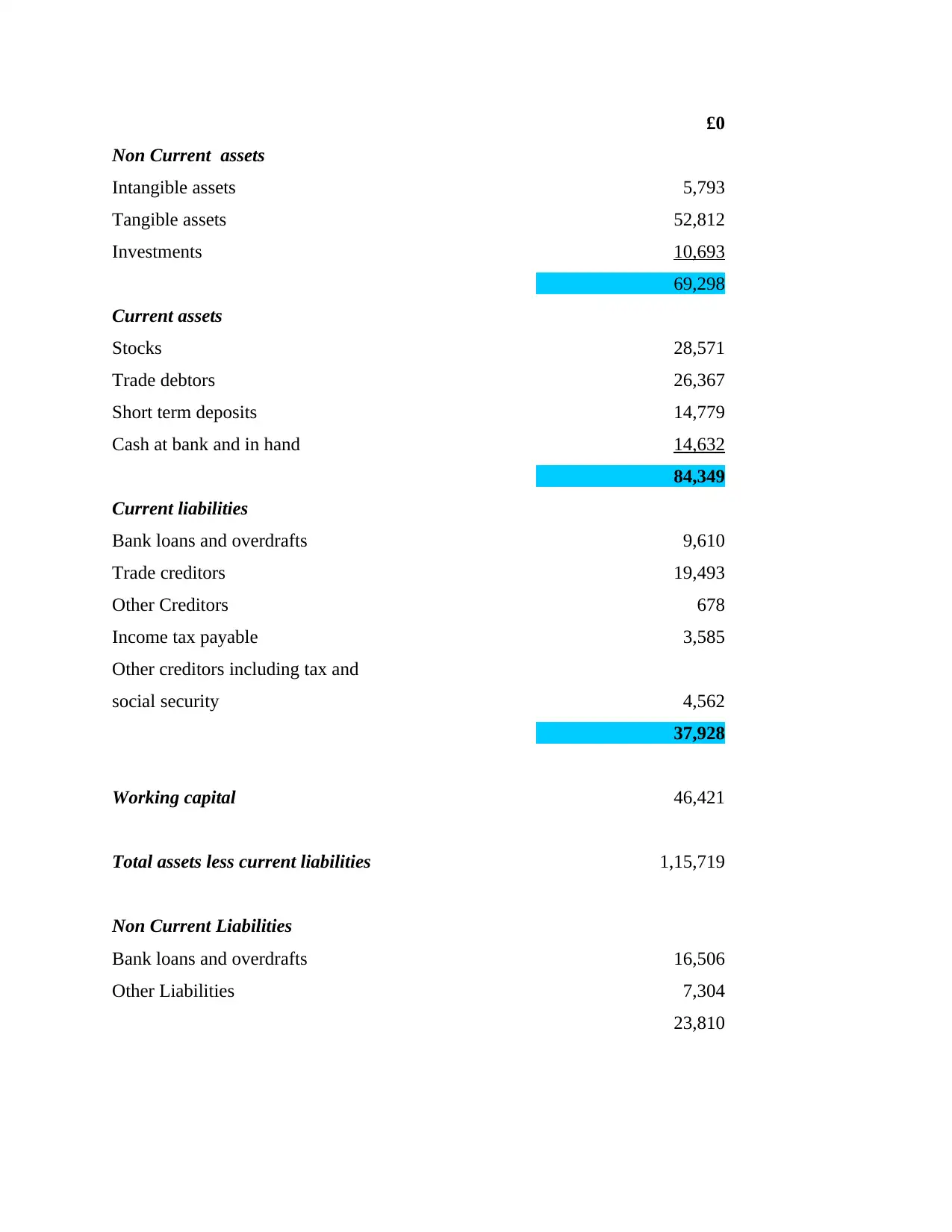

ii. Balance Sheet.

Balance Sheet as at 31 December 2016.

Total

Net profit increased by 126.77%

Shareholder's equity increased by

32.9% 83803

Quick Ratio 1.47

Current Ratio 2.22

Working Notes :

Calculation of % change in Profit:

= 43057 – 18987 = 24070

= 24070 / 18987 × 100 = 126.77 %

Calculation of Shareholder's equity of year 2016 :

= 63057 / 100 × 132 = 83803

Quick Ratio : It is calculated by dividing the current assets (less inventory) from current

liabilities.

= Quick assets / Current liabilities

With reference to balance sheet, quick assets include debtors ,short term deposits and cash.

Quick assets = £55778

Current Liabilities = £37928

Quick Ratio = 55778 / 37928

=1.47

Current Ratio : It is calculated by dividing the current assets from current liabilities.

= CA / CL

= 84349 / 37928

= 2.22

ii. Balance Sheet.

Balance Sheet as at 31 December 2016.

Total

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in hand 14,632

84,349

Current liabilities

Bank loans and overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors including tax and

social security 4,562

37,928

Working capital 46,421

Total assets less current liabilities 1,15,719

Non Current Liabilities

Bank loans and overdrafts 16,506

Other Liabilities 7,304

23,810

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in hand 14,632

84,349

Current liabilities

Bank loans and overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors including tax and

social security 4,562

37,928

Working capital 46,421

Total assets less current liabilities 1,15,719

Non Current Liabilities

Bank loans and overdrafts 16,506

Other Liabilities 7,304

23,810

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

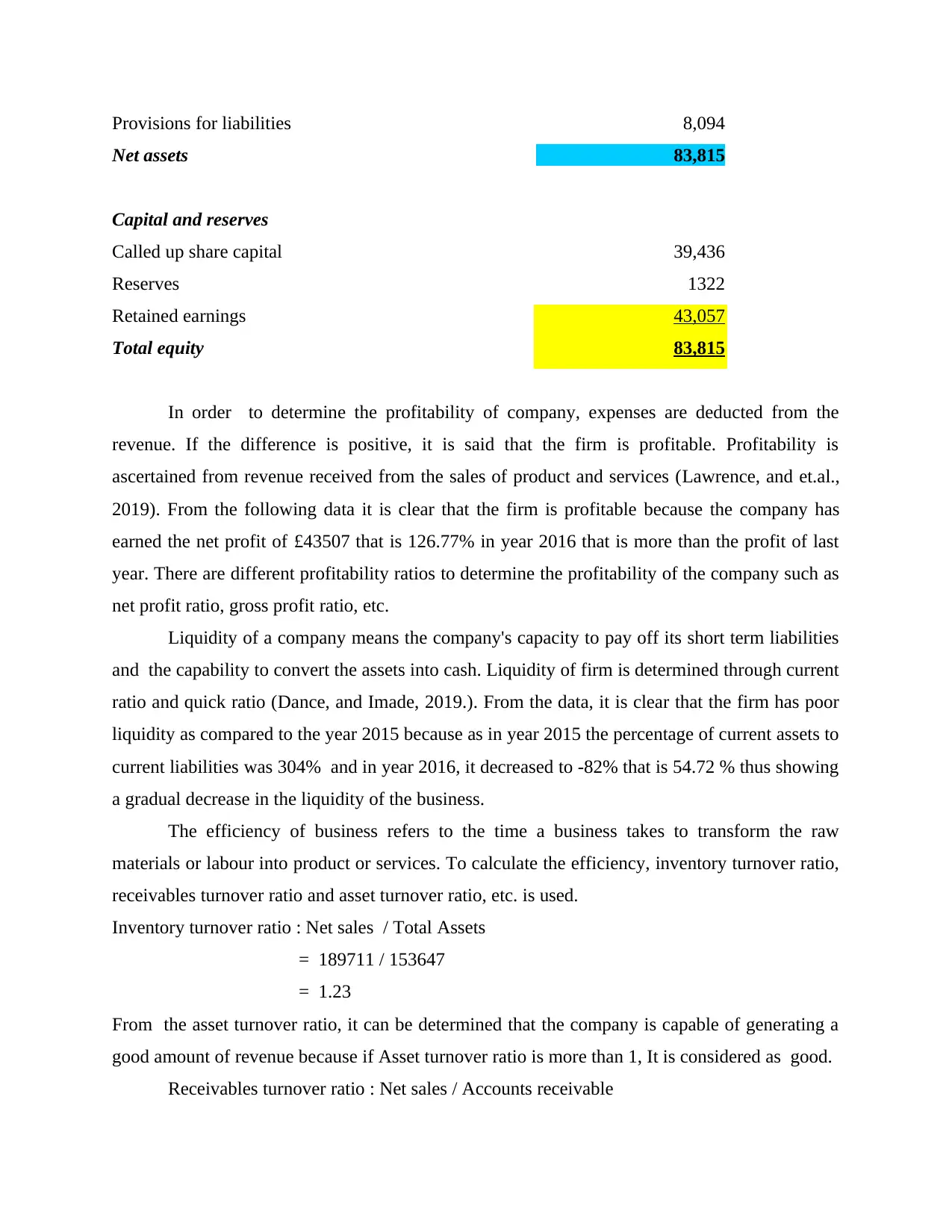

Provisions for liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Total equity 83,815

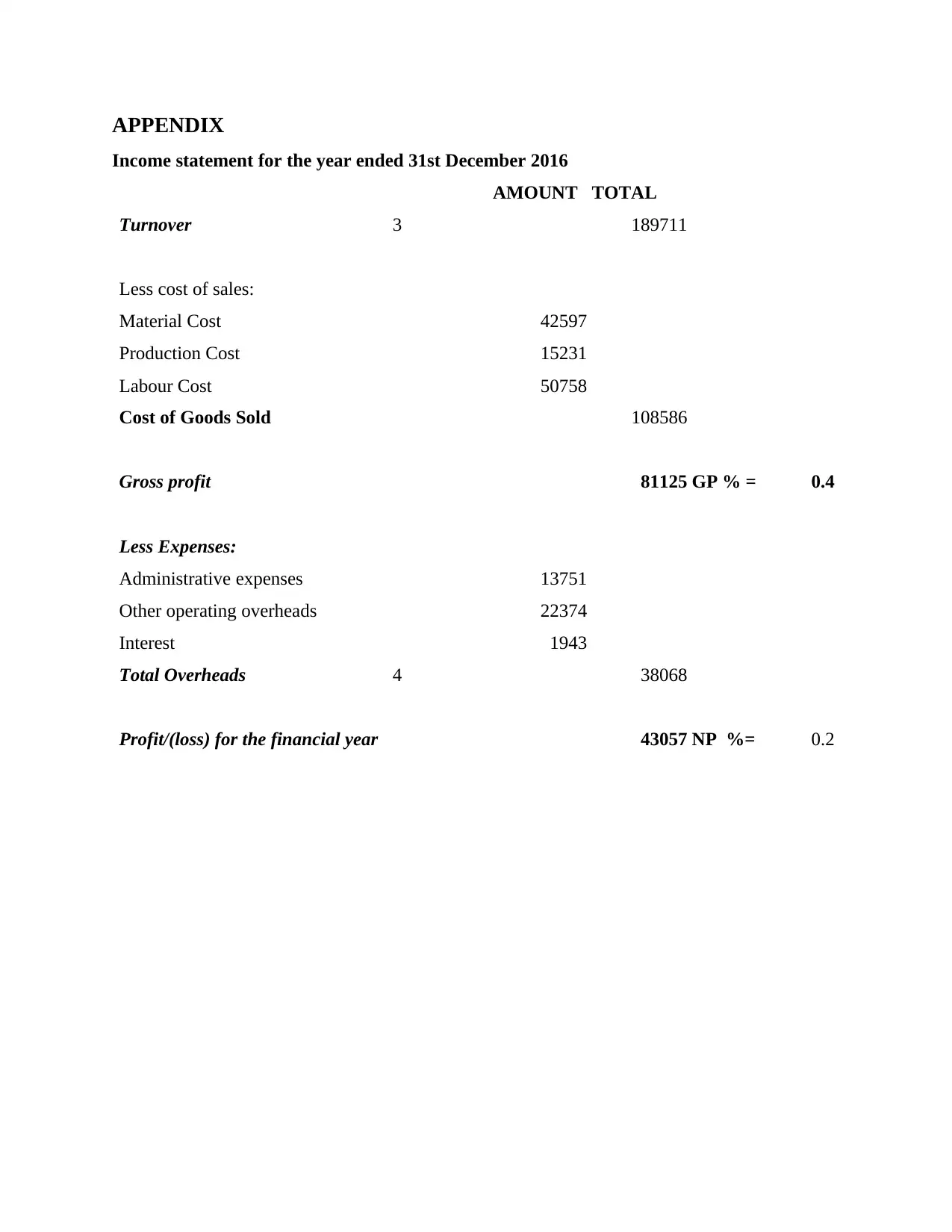

In order to determine the profitability of company, expenses are deducted from the

revenue. If the difference is positive, it is said that the firm is profitable. Profitability is

ascertained from revenue received from the sales of product and services (Lawrence, and et.al.,

2019). From the following data it is clear that the firm is profitable because the company has

earned the net profit of £43507 that is 126.77% in year 2016 that is more than the profit of last

year. There are different profitability ratios to determine the profitability of the company such as

net profit ratio, gross profit ratio, etc.

Liquidity of a company means the company's capacity to pay off its short term liabilities

and the capability to convert the assets into cash. Liquidity of firm is determined through current

ratio and quick ratio (Dance, and Imade, 2019.). From the data, it is clear that the firm has poor

liquidity as compared to the year 2015 because as in year 2015 the percentage of current assets to

current liabilities was 304% and in year 2016, it decreased to -82% that is 54.72 % thus showing

a gradual decrease in the liquidity of the business.

The efficiency of business refers to the time a business takes to transform the raw

materials or labour into product or services. To calculate the efficiency, inventory turnover ratio,

receivables turnover ratio and asset turnover ratio, etc. is used.

Inventory turnover ratio : Net sales / Total Assets

= 189711 / 153647

= 1.23

From the asset turnover ratio, it can be determined that the company is capable of generating a

good amount of revenue because if Asset turnover ratio is more than 1, It is considered as good.

Receivables turnover ratio : Net sales / Accounts receivable

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Total equity 83,815

In order to determine the profitability of company, expenses are deducted from the

revenue. If the difference is positive, it is said that the firm is profitable. Profitability is

ascertained from revenue received from the sales of product and services (Lawrence, and et.al.,

2019). From the following data it is clear that the firm is profitable because the company has

earned the net profit of £43507 that is 126.77% in year 2016 that is more than the profit of last

year. There are different profitability ratios to determine the profitability of the company such as

net profit ratio, gross profit ratio, etc.

Liquidity of a company means the company's capacity to pay off its short term liabilities

and the capability to convert the assets into cash. Liquidity of firm is determined through current

ratio and quick ratio (Dance, and Imade, 2019.). From the data, it is clear that the firm has poor

liquidity as compared to the year 2015 because as in year 2015 the percentage of current assets to

current liabilities was 304% and in year 2016, it decreased to -82% that is 54.72 % thus showing

a gradual decrease in the liquidity of the business.

The efficiency of business refers to the time a business takes to transform the raw

materials or labour into product or services. To calculate the efficiency, inventory turnover ratio,

receivables turnover ratio and asset turnover ratio, etc. is used.

Inventory turnover ratio : Net sales / Total Assets

= 189711 / 153647

= 1.23

From the asset turnover ratio, it can be determined that the company is capable of generating a

good amount of revenue because if Asset turnover ratio is more than 1, It is considered as good.

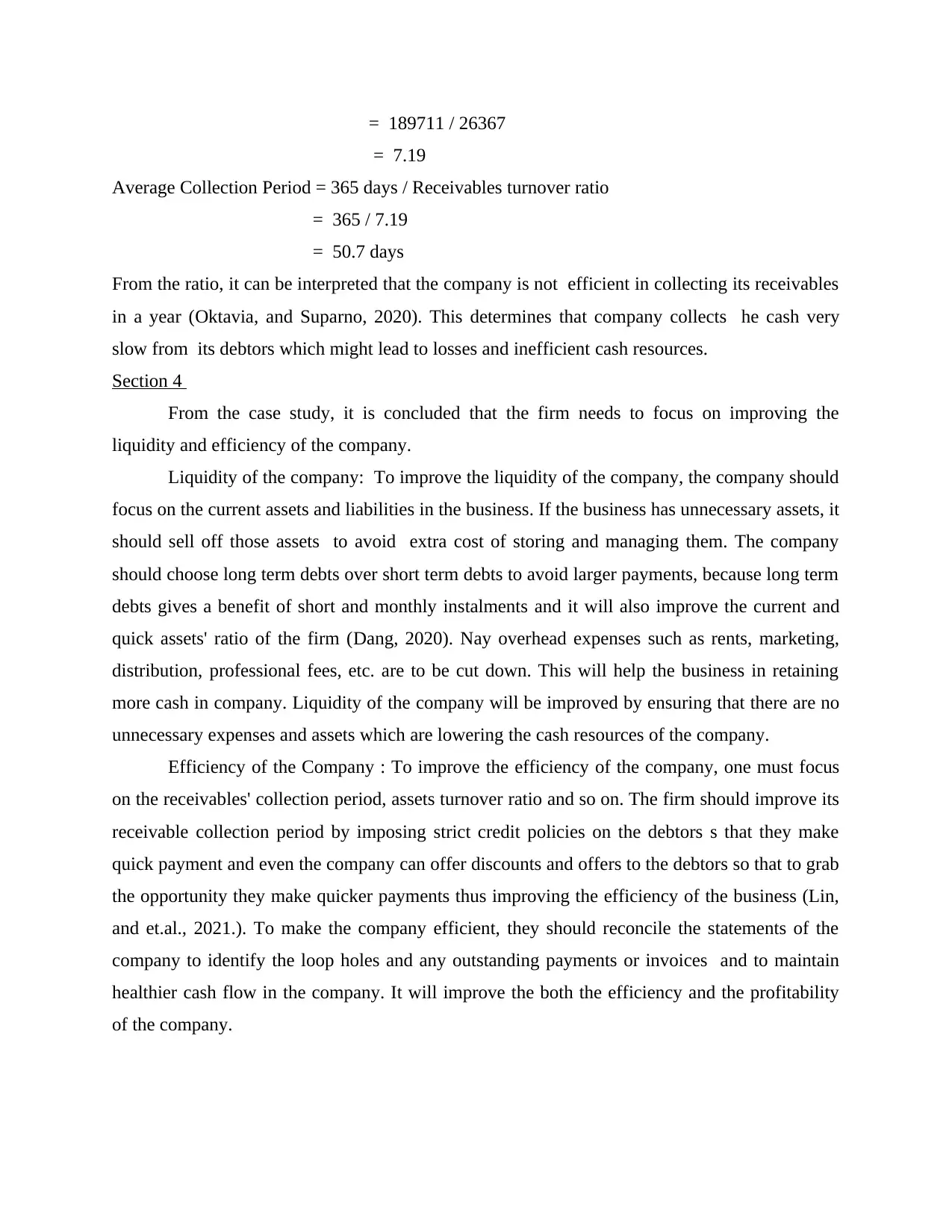

Receivables turnover ratio : Net sales / Accounts receivable

= 189711 / 26367

= 7.19

Average Collection Period = 365 days / Receivables turnover ratio

= 365 / 7.19

= 50.7 days

From the ratio, it can be interpreted that the company is not efficient in collecting its receivables

in a year (Oktavia, and Suparno, 2020). This determines that company collects he cash very

slow from its debtors which might lead to losses and inefficient cash resources.

Section 4

From the case study, it is concluded that the firm needs to focus on improving the

liquidity and efficiency of the company.

Liquidity of the company: To improve the liquidity of the company, the company should

focus on the current assets and liabilities in the business. If the business has unnecessary assets, it

should sell off those assets to avoid extra cost of storing and managing them. The company

should choose long term debts over short term debts to avoid larger payments, because long term

debts gives a benefit of short and monthly instalments and it will also improve the current and

quick assets' ratio of the firm (Dang, 2020). Nay overhead expenses such as rents, marketing,

distribution, professional fees, etc. are to be cut down. This will help the business in retaining

more cash in company. Liquidity of the company will be improved by ensuring that there are no

unnecessary expenses and assets which are lowering the cash resources of the company.

Efficiency of the Company : To improve the efficiency of the company, one must focus

on the receivables' collection period, assets turnover ratio and so on. The firm should improve its

receivable collection period by imposing strict credit policies on the debtors s that they make

quick payment and even the company can offer discounts and offers to the debtors so that to grab

the opportunity they make quicker payments thus improving the efficiency of the business (Lin,

and et.al., 2021.). To make the company efficient, they should reconcile the statements of the

company to identify the loop holes and any outstanding payments or invoices and to maintain

healthier cash flow in the company. It will improve the both the efficiency and the profitability

of the company.

= 7.19

Average Collection Period = 365 days / Receivables turnover ratio

= 365 / 7.19

= 50.7 days

From the ratio, it can be interpreted that the company is not efficient in collecting its receivables

in a year (Oktavia, and Suparno, 2020). This determines that company collects he cash very

slow from its debtors which might lead to losses and inefficient cash resources.

Section 4

From the case study, it is concluded that the firm needs to focus on improving the

liquidity and efficiency of the company.

Liquidity of the company: To improve the liquidity of the company, the company should

focus on the current assets and liabilities in the business. If the business has unnecessary assets, it

should sell off those assets to avoid extra cost of storing and managing them. The company

should choose long term debts over short term debts to avoid larger payments, because long term

debts gives a benefit of short and monthly instalments and it will also improve the current and

quick assets' ratio of the firm (Dang, 2020). Nay overhead expenses such as rents, marketing,

distribution, professional fees, etc. are to be cut down. This will help the business in retaining

more cash in company. Liquidity of the company will be improved by ensuring that there are no

unnecessary expenses and assets which are lowering the cash resources of the company.

Efficiency of the Company : To improve the efficiency of the company, one must focus

on the receivables' collection period, assets turnover ratio and so on. The firm should improve its

receivable collection period by imposing strict credit policies on the debtors s that they make

quick payment and even the company can offer discounts and offers to the debtors so that to grab

the opportunity they make quicker payments thus improving the efficiency of the business (Lin,

and et.al., 2021.). To make the company efficient, they should reconcile the statements of the

company to identify the loop holes and any outstanding payments or invoices and to maintain

healthier cash flow in the company. It will improve the both the efficiency and the profitability

of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the case study, it is concluded that to ascertain the financial performance of the business a

company have to interpret and analyse the financial statements after certain period. To

determine the financial performance the company my use ratio analysis to ascertain the liquidity,

profitability, efficiency and financial position of a business. There are many ways and strategies

that a business should adopt in order to improve its performance and financial health.

From the case study, it is concluded that to ascertain the financial performance of the business a

company have to interpret and analyse the financial statements after certain period. To

determine the financial performance the company my use ratio analysis to ascertain the liquidity,

profitability, efficiency and financial position of a business. There are many ways and strategies

that a business should adopt in order to improve its performance and financial health.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Brigham, E. F. and Ehrhardt, M. C., 2019. Financial management: Theory & practice. Cengage

Learning.

Hasanaj, P. and Kuqi, B., 2019. Analysis of financial statements. Humanities and Social Science

Research. 2(2). pp.p17-p17.

Anyushenkova, O. N. and Samorukova, N. N., 2019. The cash flow statement of a business

entity. Наука и образование: новое время. (1). pp.220-223.

CREȚU, D., Iova, A. R. and Năstase, M., 2019. Financial diagnosis of the company based on the

information derived from the balance sheet. Case study. Scientific Papers Series 溺

anagement, Economic Engineering in Agriculture and Rural Development. (19). p.2.

Dance, M. and Imade, S., 2019. Financial ratio analysis in predicting financial conditions distress

in indonesia stock exchange. Russian Journal of Agricultural and Socio-Economic

Sciences. 86(2).

Lawrence, J. M., and et.al., 2019. Multichannel strategies for managing the profitability of

business-to-business customers. Journal of Marketing Research. 56(3). pp.479-497.

Oktavia, S. and Suparno, S., 2020. THE EFFECT OF RECEIVABLES TURNOVER AND

INVENTORY TURNOVER ON PROFITABILITY IN AUTOMOTIVE AND

COMPONENT COMPANIES LISTED ON THE INDONESIA STOCK EXCHANGE

FOR THE 2010-2019 PERIOD. Jurnal Ekonomi Balance. 16(2). pp.184-193.

Dance, M. and Imade, S., 2019. Financial ratio analysis in predicting financial conditions distress

in indonesia stock exchange. Russian Journal of Agricultural and Socio-Economic

Sciences. 86(2).

Dang, H. T., 2020. Determinants of liquidity of listed enterprises: Evidence from Vietnam. The

Journal of Asian Finance, Economics, and Business. 7(11). pp.67-73.

Lin, Y.E., and et.al., 2021. Corporate social responsibility and investment efficiency: Does

business strategy matter?. International Review of Financial Analysis. 73. p.101585.

Books and journals

Brigham, E. F. and Ehrhardt, M. C., 2019. Financial management: Theory & practice. Cengage

Learning.

Hasanaj, P. and Kuqi, B., 2019. Analysis of financial statements. Humanities and Social Science

Research. 2(2). pp.p17-p17.

Anyushenkova, O. N. and Samorukova, N. N., 2019. The cash flow statement of a business

entity. Наука и образование: новое время. (1). pp.220-223.

CREȚU, D., Iova, A. R. and Năstase, M., 2019. Financial diagnosis of the company based on the

information derived from the balance sheet. Case study. Scientific Papers Series 溺

anagement, Economic Engineering in Agriculture and Rural Development. (19). p.2.

Dance, M. and Imade, S., 2019. Financial ratio analysis in predicting financial conditions distress

in indonesia stock exchange. Russian Journal of Agricultural and Socio-Economic

Sciences. 86(2).

Lawrence, J. M., and et.al., 2019. Multichannel strategies for managing the profitability of

business-to-business customers. Journal of Marketing Research. 56(3). pp.479-497.

Oktavia, S. and Suparno, S., 2020. THE EFFECT OF RECEIVABLES TURNOVER AND

INVENTORY TURNOVER ON PROFITABILITY IN AUTOMOTIVE AND

COMPONENT COMPANIES LISTED ON THE INDONESIA STOCK EXCHANGE

FOR THE 2010-2019 PERIOD. Jurnal Ekonomi Balance. 16(2). pp.184-193.

Dance, M. and Imade, S., 2019. Financial ratio analysis in predicting financial conditions distress

in indonesia stock exchange. Russian Journal of Agricultural and Socio-Economic

Sciences. 86(2).

Dang, H. T., 2020. Determinants of liquidity of listed enterprises: Evidence from Vietnam. The

Journal of Asian Finance, Economics, and Business. 7(11). pp.67-73.

Lin, Y.E., and et.al., 2021. Corporate social responsibility and investment efficiency: Does

business strategy matter?. International Review of Financial Analysis. 73. p.101585.

APPENDIX

Income statement for the year ended 31st December 2016

AMOUNT TOTAL

Turnover 3 189711

Less cost of sales:

Material Cost 42597

Production Cost 15231

Labour Cost 50758

Cost of Goods Sold 108586

Gross profit 81125 GP % = 0.4

Less Expenses:

Administrative expenses 13751

Other operating overheads 22374

Interest 1943

Total Overheads 4 38068

Profit/(loss) for the financial year 43057 NP %= 0.2

Income statement for the year ended 31st December 2016

AMOUNT TOTAL

Turnover 3 189711

Less cost of sales:

Material Cost 42597

Production Cost 15231

Labour Cost 50758

Cost of Goods Sold 108586

Gross profit 81125 GP % = 0.4

Less Expenses:

Administrative expenses 13751

Other operating overheads 22374

Interest 1943

Total Overheads 4 38068

Profit/(loss) for the financial year 43057 NP %= 0.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.