Finance Project: Capital Acquisition, Project Evaluation, WACC

VerifiedAdded on 2020/07/22

|13

|2153

|283

Report

AI Summary

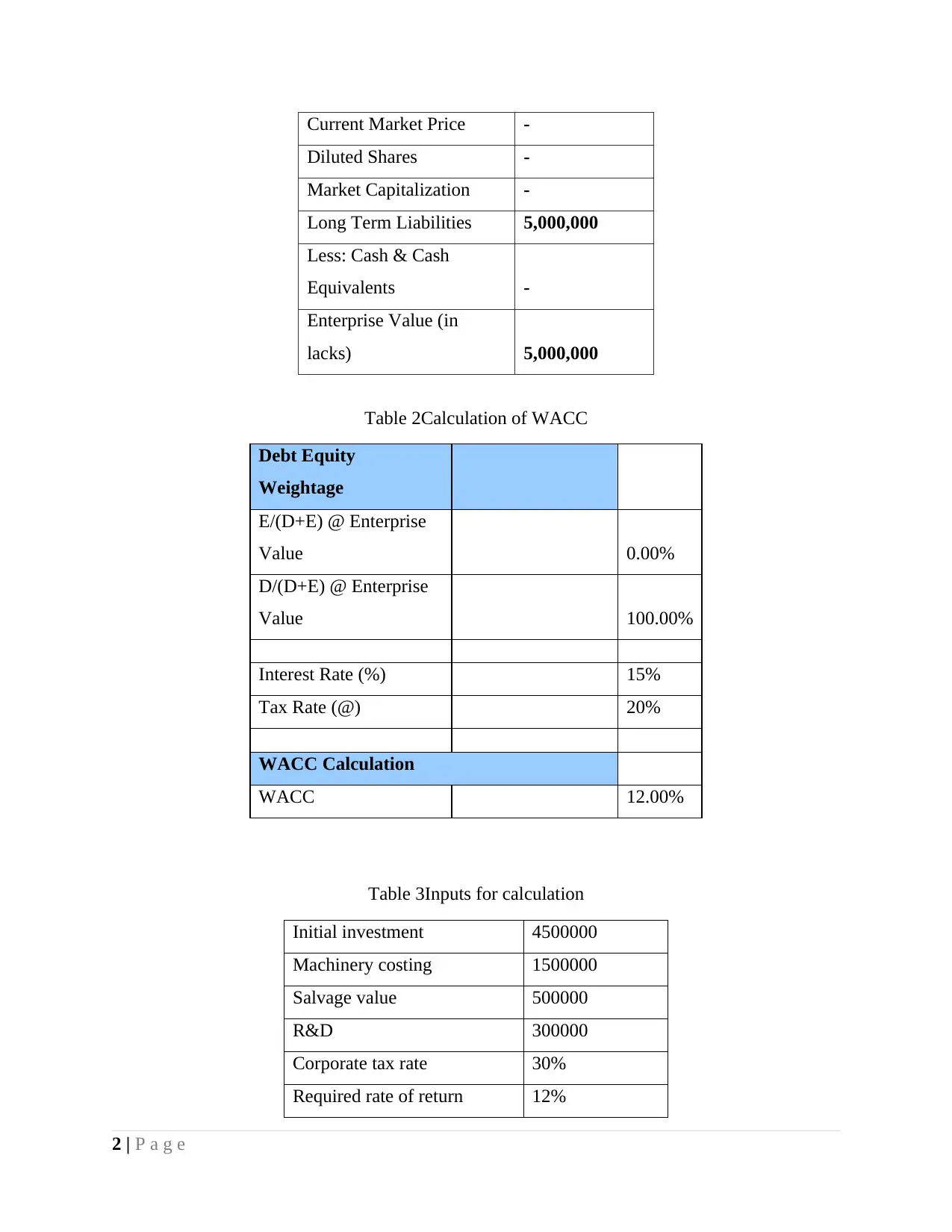

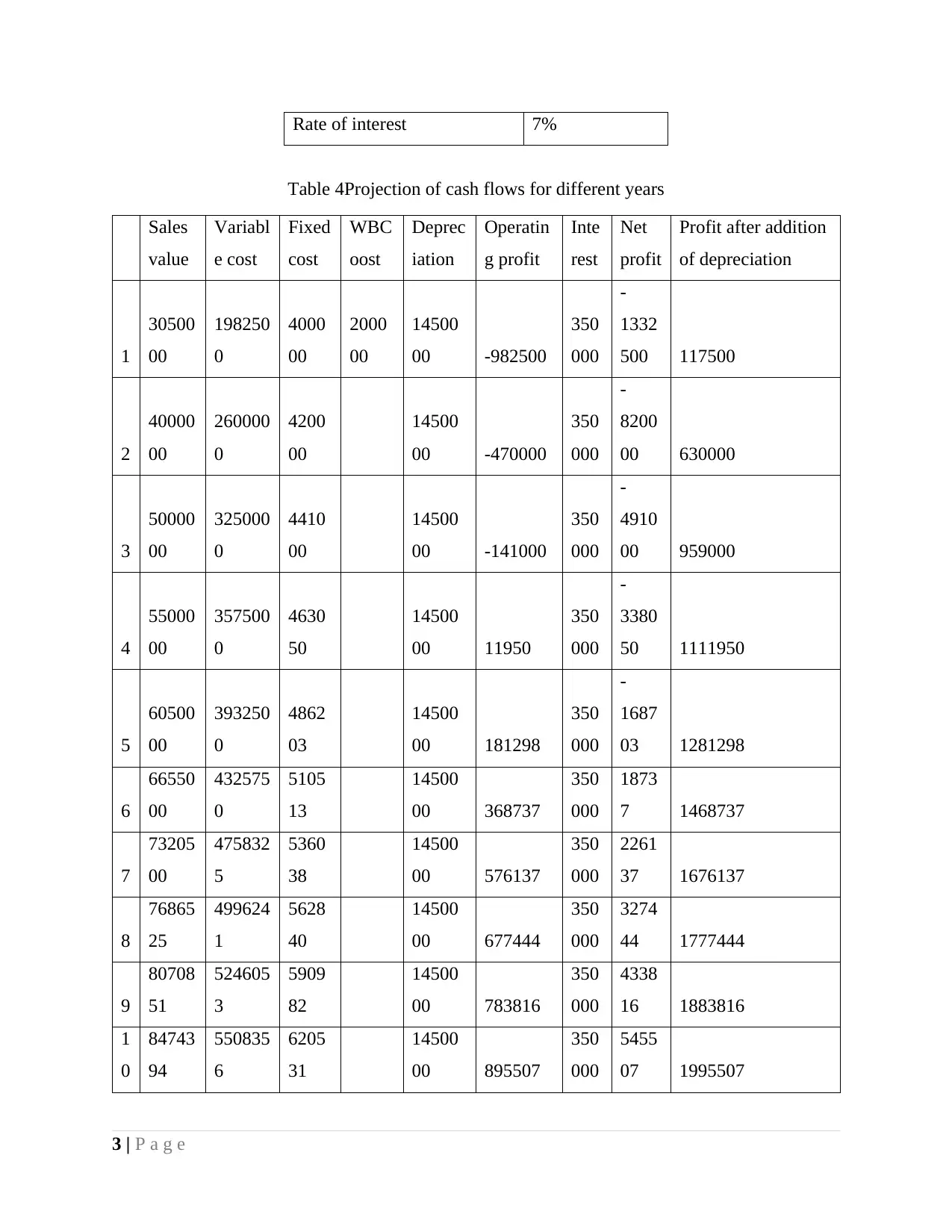

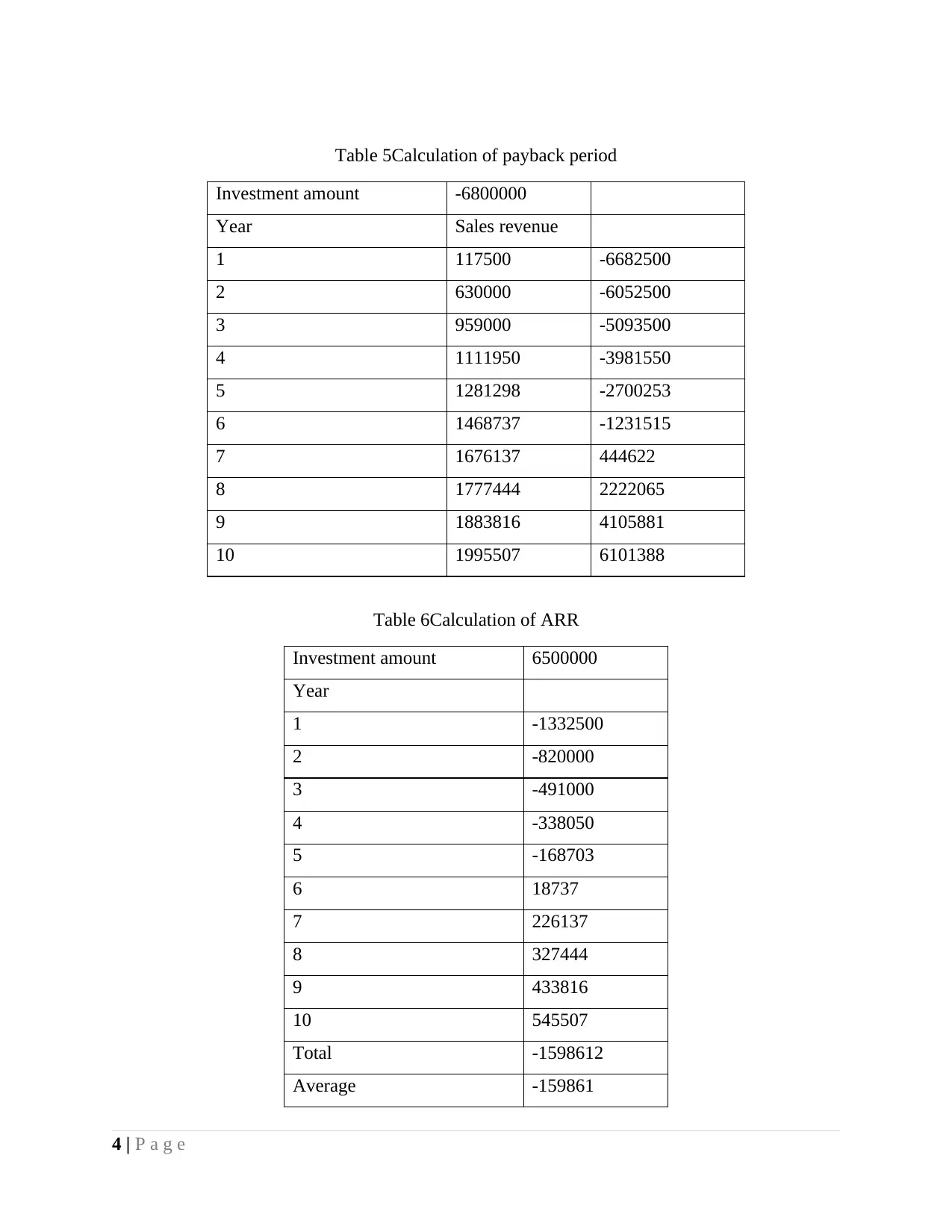

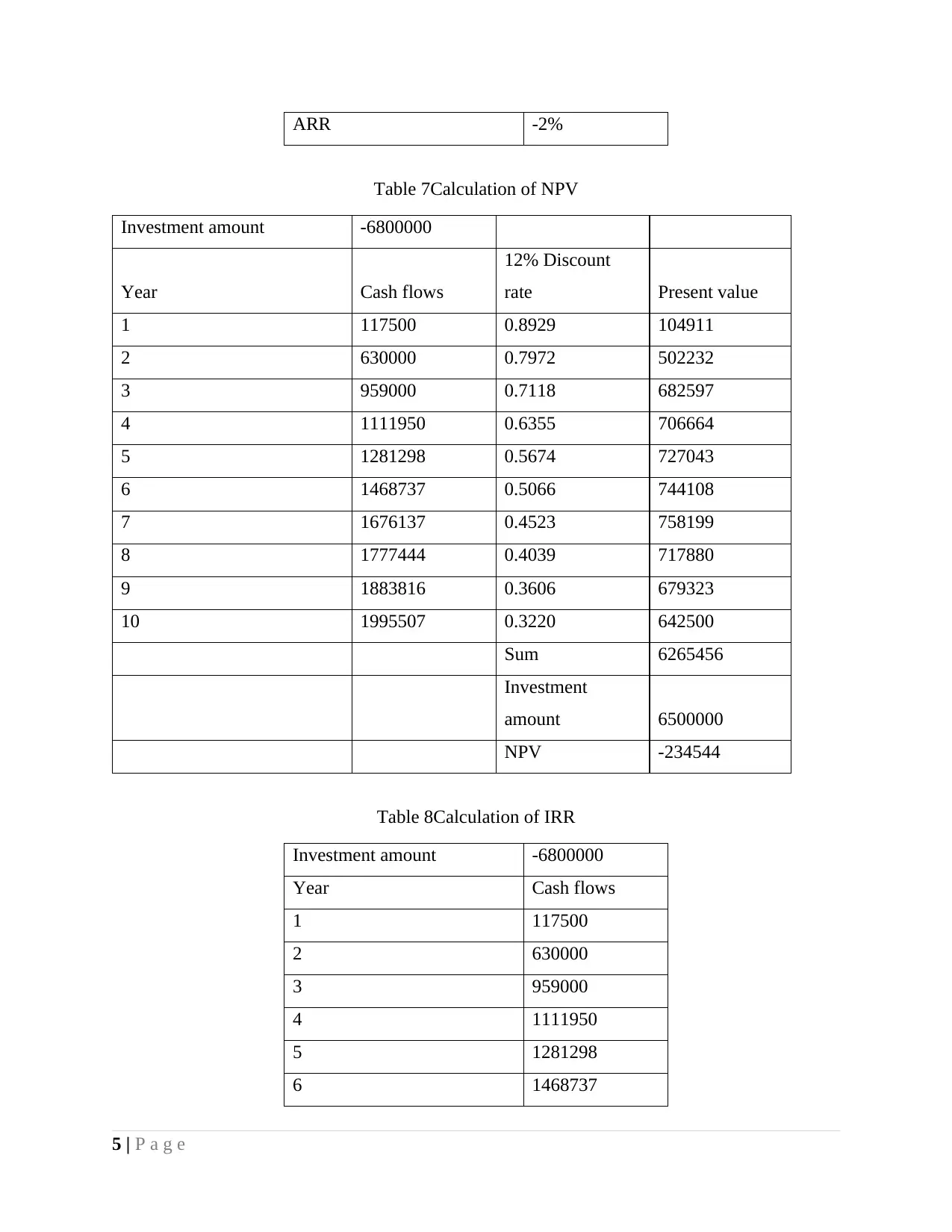

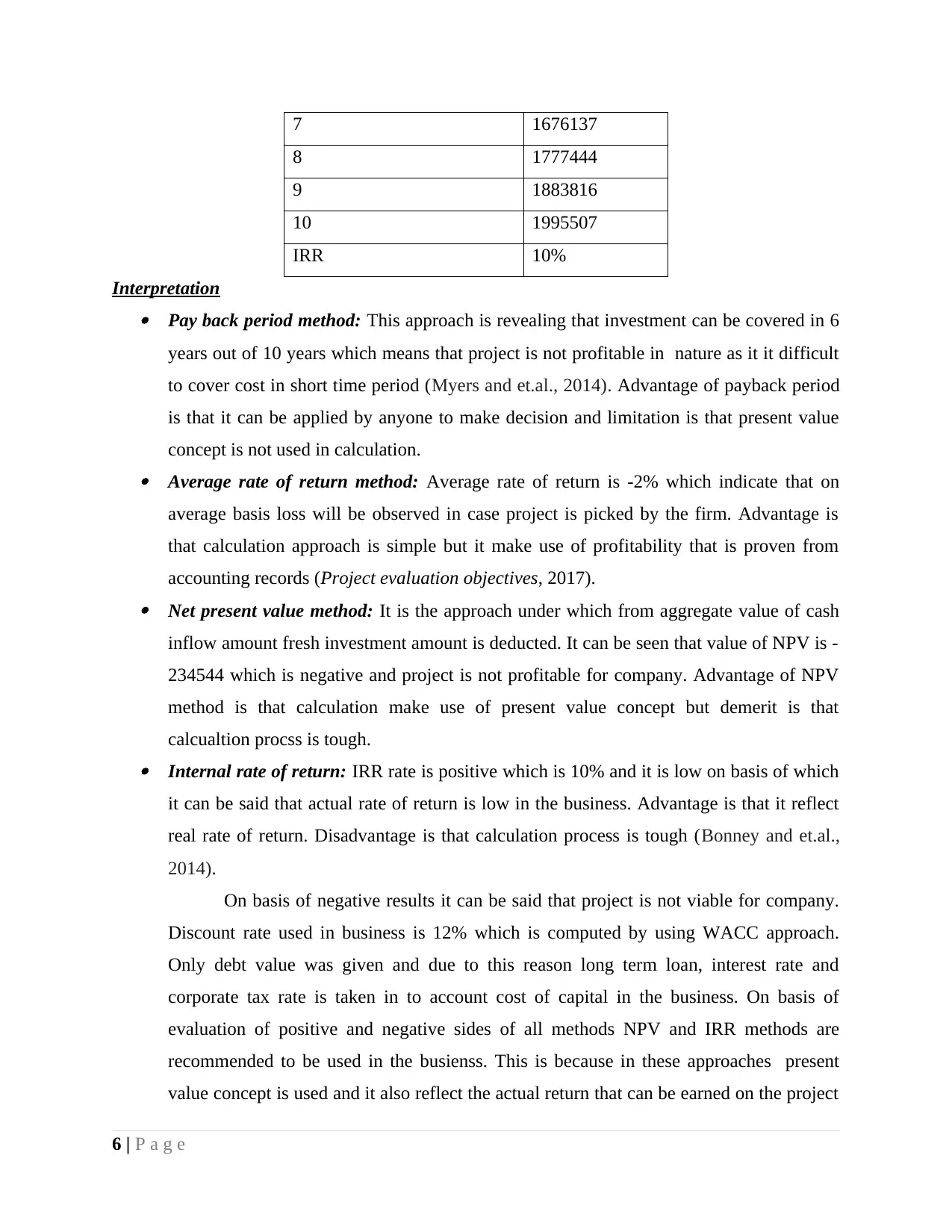

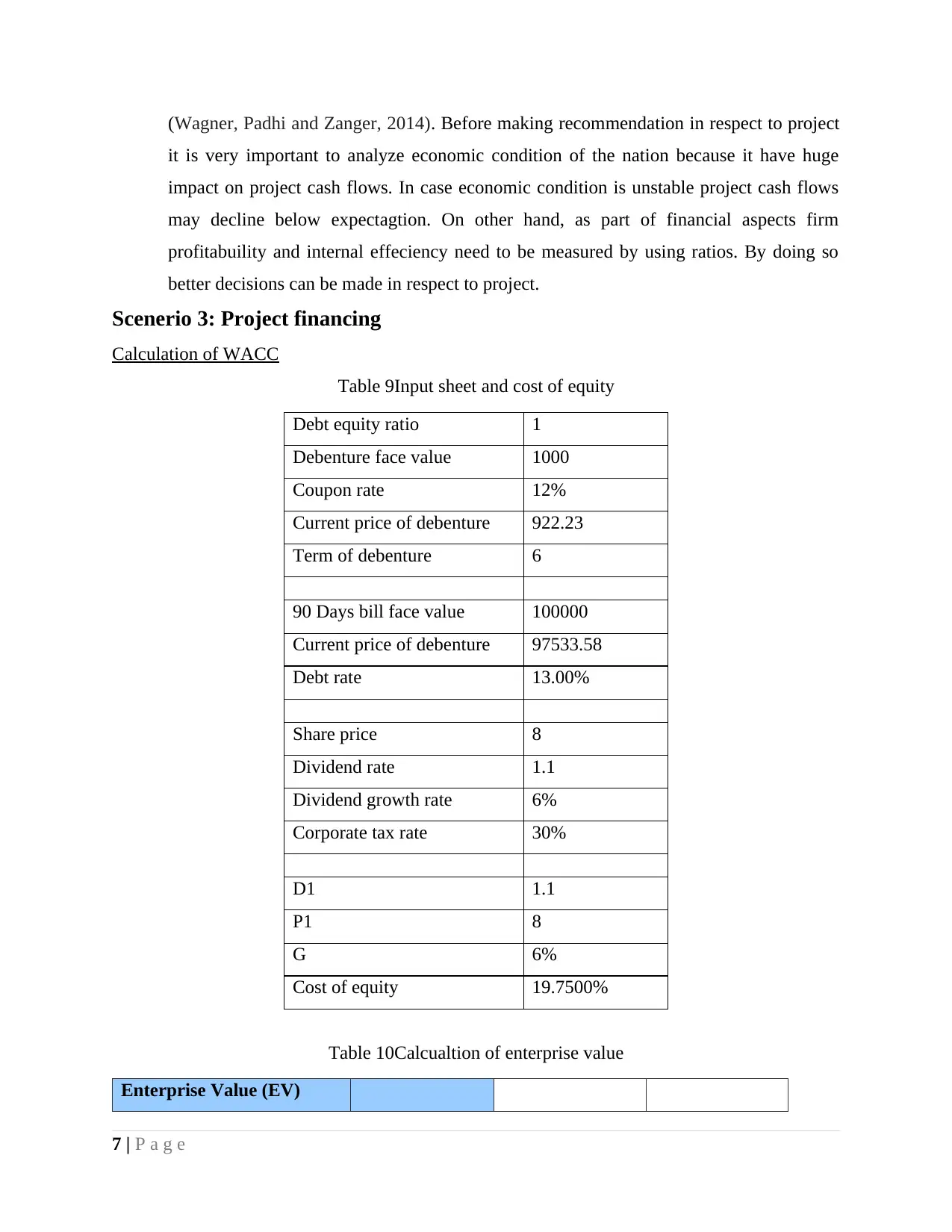

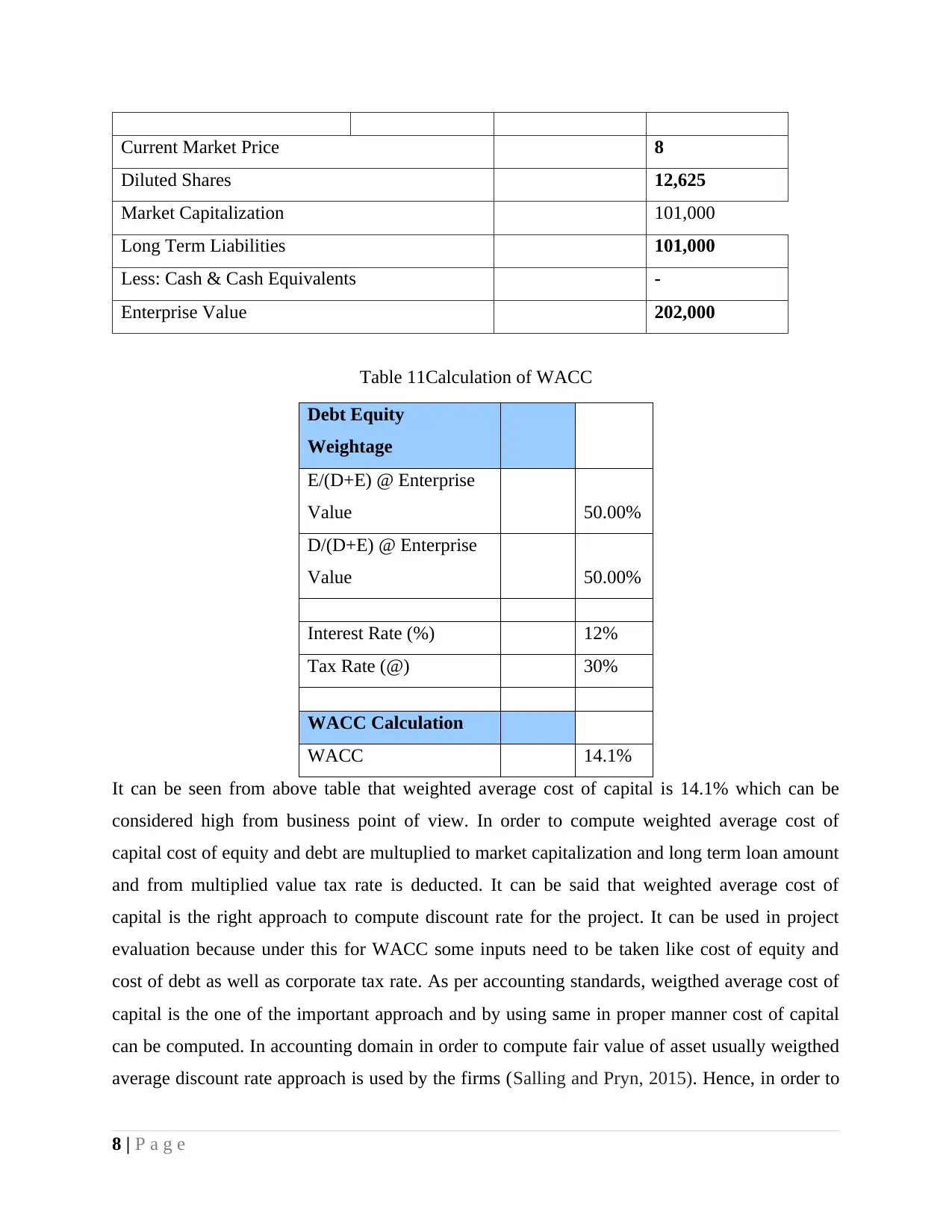

The report provides an executive summary of a business finance project, focusing on project evaluation methods and the calculation of Weighted Average Cost of Capital (WACC). It explores capital acquisition strategies, emphasizing the importance of replacing tools and machines for improved efficiency and the factors influencing investment decisions, such as technology, cost, and budget considerations. The report includes detailed calculations of Enterprise Value, WACC, and cash flow projections, along with analyses using methods like Payback Period, Average Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR). The interpretation of these methods highlights the project's financial viability, concluding with a recommendation to use NPV and IRR for project assessment, and a discussion on the impact of economic conditions on project cash flows and the importance of measuring profitability and efficiency ratios. The report also includes a scenario on project financing, calculating WACC with detailed inputs and the limitations of the WACC method, emphasizing the need for stable capital structure.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.