Business Finance Report: Project Evaluation and Analysis

VerifiedAdded on 2022/11/14

|9

|1323

|219

Report

AI Summary

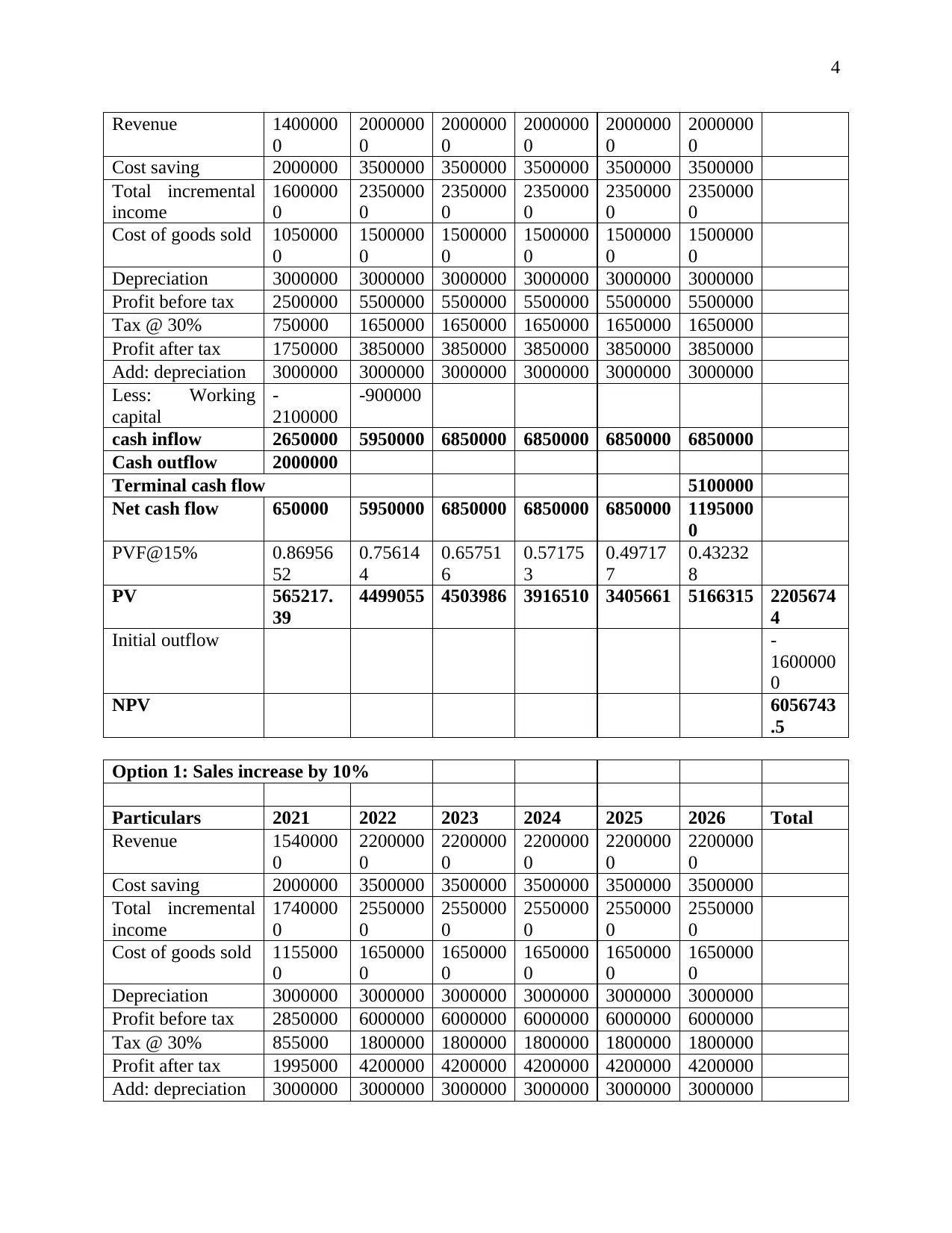

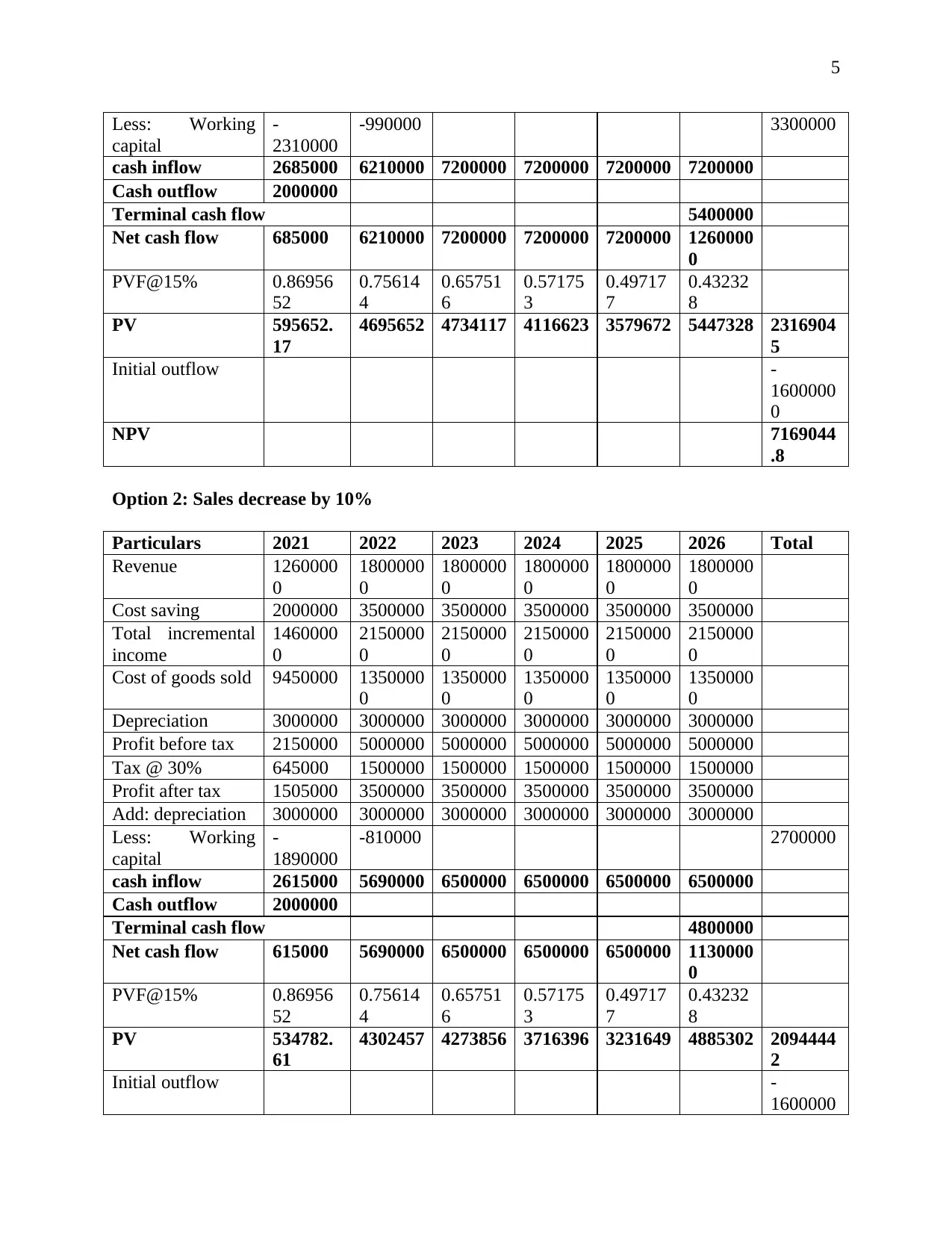

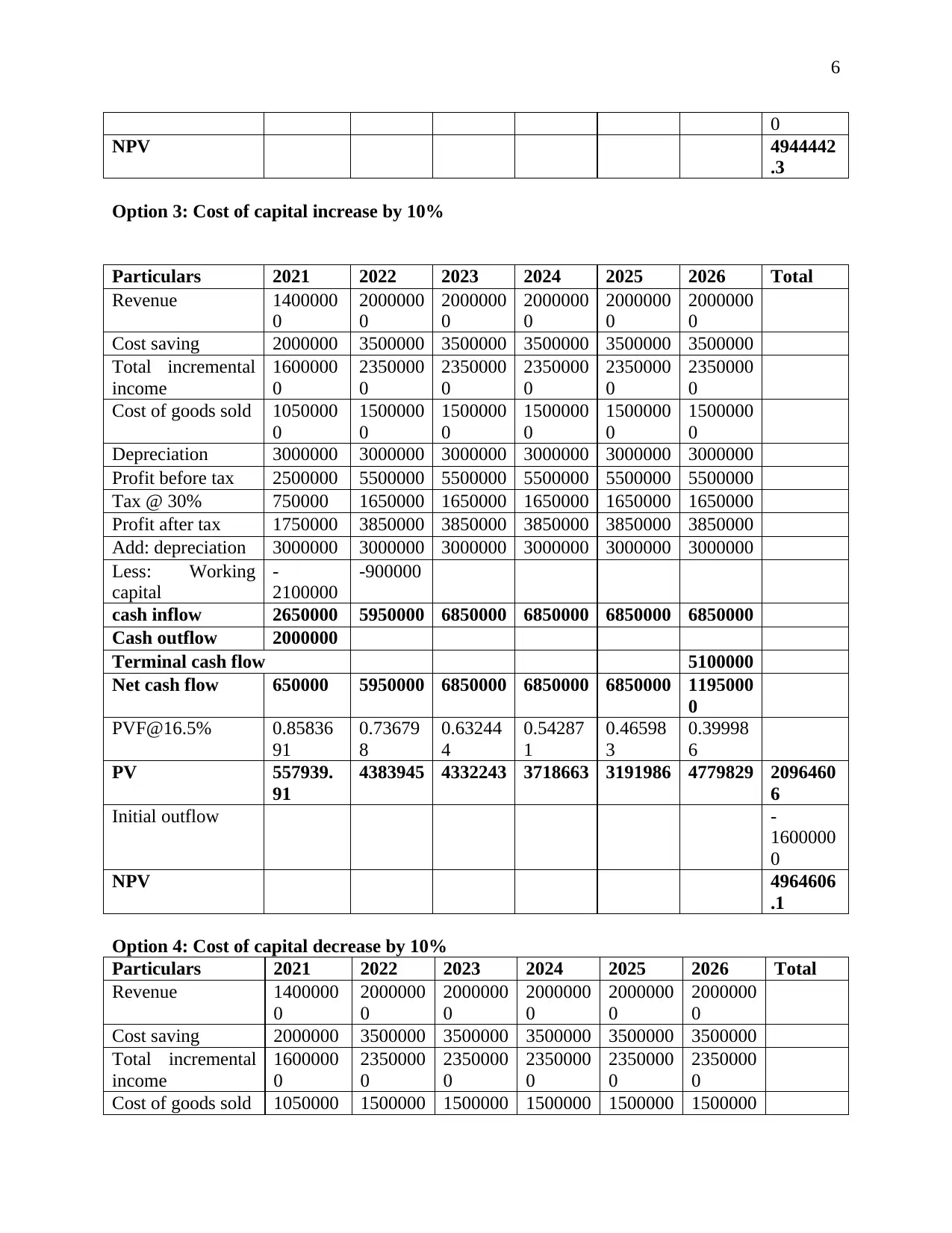

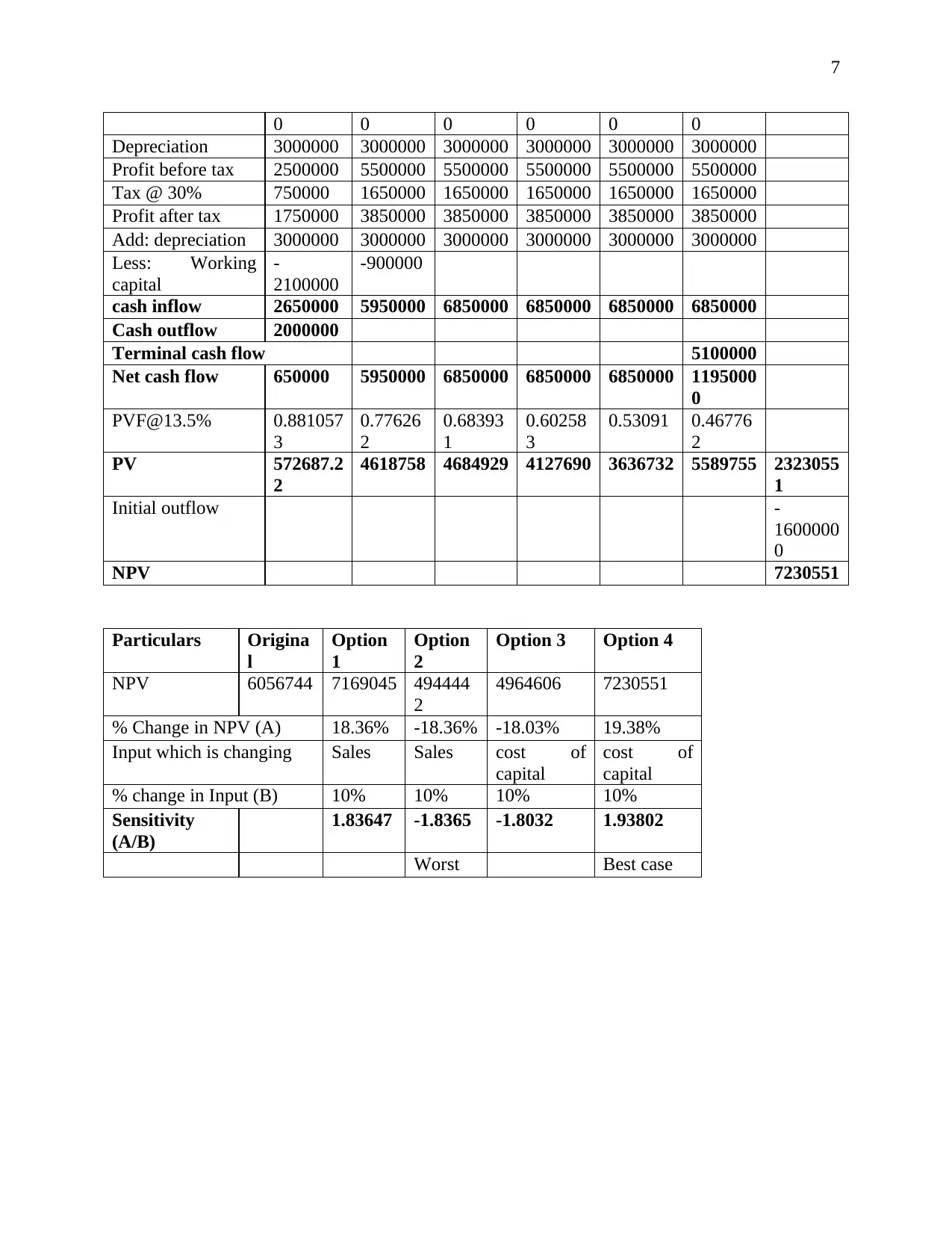

This report provides a detailed analysis of a business finance project, focusing on the evaluation of a project using the hurdle rate. It begins by explaining the concept of the hurdle rate and its limitations compared to the discount rate, highlighting why the company is hesitant to use it. The report then presents a comprehensive cash flow analysis, projecting revenues, costs, and profits over several years. It includes calculations for net present value (NPV) under various scenarios, such as changes in sales, cost of capital, and sensitivity analysis to assess the impact of these changes. The analysis includes detailed tables showing the impact of different scenarios on the project's financial performance. The report also includes references to academic literature supporting the financial concepts discussed.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.