Business Finance: Financial Ratio Analysis & Performance Review

VerifiedAdded on 2022/11/24

|24

|2884

|165

Report

AI Summary

This report explores financial management principles and their application in enhancing organizational performance. It emphasizes the importance of financial planning, decision-making, and capital management. The report delves into key financial statements—balance sheets, income statements, and cash flow statements—and their significance in evaluating a company's financial health. It discusses various financial ratios, including leverage, profitability, and asset management ratios, and how they reflect a company's performance. The report also analyzes a business review template, highlighting changes in profit, shareholder equity, and other key metrics. It concludes by suggesting strategies for improving financial performance, such as optimizing credit facilities, reducing overheads, and raising capital through market operations, all aimed at fostering sustainable growth and profitability. Desklib provides access to this assignment and other resources for students.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

SECTION 1.....................................................................................................................................3

Financial management and its importance..................................................................................3

SECTION 2.....................................................................................................................................4

Financial statements and significance of ratios...........................................................................4

SECTION 3.....................................................................................................................................6

Information given through business review template..................................................................6

Description of ratios....................................................................................................................6

SECTION 4.....................................................................................................................................7

Ways of improving financial performance..................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

Business review Template...............................................................................................................11

Notes to the financial statements..........................................................................................12

at 31 December 2016..................................................................................12

Excel sheet.................................................................................................................................14

INTRODUCTION...........................................................................................................................3

SECTION 1.....................................................................................................................................3

Financial management and its importance..................................................................................3

SECTION 2.....................................................................................................................................4

Financial statements and significance of ratios...........................................................................4

SECTION 3.....................................................................................................................................6

Information given through business review template..................................................................6

Description of ratios....................................................................................................................6

SECTION 4.....................................................................................................................................7

Ways of improving financial performance..................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

Business review Template...............................................................................................................11

Notes to the financial statements..........................................................................................12

at 31 December 2016..................................................................................12

Excel sheet.................................................................................................................................14

INTRODUCTION

The study is on financial management and its use in organisation. Financial management is the

planning and use of finance component in organisation in a manner which does optimum

utilisation of resources and tells the best method which will be suitable for investment. The study

discusses the concept of financial management, its use in organisation and how organisation can

find ways to improve the financial performance. The report discussed the main financial

statements used by the organisation and the ratios being used in financial management. The

ratios have been described how they reflect the company’s performance.

SECTION 1

Financial management and its importance

It is an important aspect in organisation and for doing business successfully, financial

management is of utmost importance. Finance management means planning strategically, giving

direction and control of undertaking of financial activities in an institute. Managing the financial

assets is also a role played by it in the organisation. Financial management has these objectives:

a) Maintenance of fund supply for the organisation

b) Assurance to organisation’s investors for getting returns which are beneficial on investment

made.

c) Usage of funds which is correct.

d) Creation of investment opportunities which are safe (Akan and Tevfik, 2020).

Financial management includes these elements:

a) Financial planning: The process of calculation of capital amount which is required for an

organisation and then defining its allocation. Financial plan shall include:

a) Determination of amount of capital to be needed for operations.

b) Determination of organising capital structure.

c) Financial policy making and framing regulations.

b) Financial making of decisions: It involves financing and investment talking of

organisation. Decision is taken by organisation of raising finance on when new shares

have to be sold and when profit distribution take place.

The study is on financial management and its use in organisation. Financial management is the

planning and use of finance component in organisation in a manner which does optimum

utilisation of resources and tells the best method which will be suitable for investment. The study

discusses the concept of financial management, its use in organisation and how organisation can

find ways to improve the financial performance. The report discussed the main financial

statements used by the organisation and the ratios being used in financial management. The

ratios have been described how they reflect the company’s performance.

SECTION 1

Financial management and its importance

It is an important aspect in organisation and for doing business successfully, financial

management is of utmost importance. Finance management means planning strategically, giving

direction and control of undertaking of financial activities in an institute. Managing the financial

assets is also a role played by it in the organisation. Financial management has these objectives:

a) Maintenance of fund supply for the organisation

b) Assurance to organisation’s investors for getting returns which are beneficial on investment

made.

c) Usage of funds which is correct.

d) Creation of investment opportunities which are safe (Akan and Tevfik, 2020).

Financial management includes these elements:

a) Financial planning: The process of calculation of capital amount which is required for an

organisation and then defining its allocation. Financial plan shall include:

a) Determination of amount of capital to be needed for operations.

b) Determination of organising capital structure.

c) Financial policy making and framing regulations.

b) Financial making of decisions: It involves financing and investment talking of

organisation. Decision is taken by organisation of raising finance on when new shares

have to be sold and when profit distribution take place.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

c) Calculation of capital: Financial manager calculate funds which will be required by the

various departments of the organisation and the amount estimation is done in a way

which also anticipates the increase in earnings of the organisation as time passes on.

d) Capital structure formation; As the amount of capital is estimated, the capital structure

requires formation. It has involvement of debt and equity in long as well as short term.

The amount required to be raised by sources of external finance is also decided in this

aspect (Bailey, 2017).

e) Investment of capital: Investment is required by every organisation to grow and make

profits. Thus, it is necessary to invest the company funds which go in right direction and

bring returns for the company and its investors.

f) Profit allocation: As the organisation gathers profits, financial management has to

allocate the same.

g) Effective money management: The money required in various functions like bill

payments, maintenance of stock and covering up current liabilities has to be performed

under financial management. Also, since time value of money concept is used in financial

management, techniques like NPV and IRR help in taking right decisions and save costs

thus managing money for operations (Akan and Tevfik, 2020).

SECTION 2

Financial statements and significance of ratios

The financial statements of use in organisation are Balance sheet, Income statement and Cash

flow statement. Balance sheet is also known as Statement of Financial position. It depicts the

assets on one side and liabilities on the other. Assets include long term as well as short term also

known as current assets. Liabilities include short term as well as long term liabilities which are

payable by the company. The accounting rule states that assets side has to match with liabilities

side. Assets are shown also of fixed assets like land and building, machinery which are

considered to be resources for organisation. Also are registered accounts receivables and

payables in the balance sheet which shows company’s credit due and self-credit returns owed.

Investors look for current assets and liabilities section in balance sheet of the past five years and

make mind for investment. This also gives information of dividends paid by the company.

various departments of the organisation and the amount estimation is done in a way

which also anticipates the increase in earnings of the organisation as time passes on.

d) Capital structure formation; As the amount of capital is estimated, the capital structure

requires formation. It has involvement of debt and equity in long as well as short term.

The amount required to be raised by sources of external finance is also decided in this

aspect (Bailey, 2017).

e) Investment of capital: Investment is required by every organisation to grow and make

profits. Thus, it is necessary to invest the company funds which go in right direction and

bring returns for the company and its investors.

f) Profit allocation: As the organisation gathers profits, financial management has to

allocate the same.

g) Effective money management: The money required in various functions like bill

payments, maintenance of stock and covering up current liabilities has to be performed

under financial management. Also, since time value of money concept is used in financial

management, techniques like NPV and IRR help in taking right decisions and save costs

thus managing money for operations (Akan and Tevfik, 2020).

SECTION 2

Financial statements and significance of ratios

The financial statements of use in organisation are Balance sheet, Income statement and Cash

flow statement. Balance sheet is also known as Statement of Financial position. It depicts the

assets on one side and liabilities on the other. Assets include long term as well as short term also

known as current assets. Liabilities include short term as well as long term liabilities which are

payable by the company. The accounting rule states that assets side has to match with liabilities

side. Assets are shown also of fixed assets like land and building, machinery which are

considered to be resources for organisation. Also are registered accounts receivables and

payables in the balance sheet which shows company’s credit due and self-credit returns owed.

Investors look for current assets and liabilities section in balance sheet of the past five years and

make mind for investment. This also gives information of dividends paid by the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income statement is the statement depicting profit and loss of the company. It gives an insight of

the revenue earned, cost of goods for the company, gross profit thus made. It gives insight of

variable and fixed expenses along with overhead costs and selling and administrative expenses. It

lastly gives the net income when all expenses have been deducted from revenues. This statement

is of utmost importance because of net profit which is the important factor regarding investment

and the efficiency of company in keeping check of operational costs.

Cash flow statement talks of cash inflows and cash outflows and tells about the sources of

income and source of expense that is where money comes in and goes out. It tells how

effectively organisation uses money and whether cash inflow is more than outflow which means

money is sufficient for operations. It also tells which projects have been generating investment as

returns and which projects are undergoing now which need money or cash outflow (Bailey,

2017).

The financial ratios depict the financial status of the company and thus are of importance for

investors and management to see how well the company is performing. The leverage ratios

indicate the financial health of the company. It tells whether the company has sufficient equity in

comparison to debt or not. This means company is able to manage its finances in a correct ratio

and can fulfil financial needs with mixture of both. Examples are debt to equity ratio and long-

term debt to capitalization ratio etc.

Profitability ratio gives indication of organisation to contain operational costs and generate

profits. The ratio is important as bottom line for investors to check on company’s profitability to

check on past five years whether it is able to pay the dividends by profit generation or not.

Examples of profitability ratios are gross profit, net profit, return on equity etc.

Asset management ratios help in determining how well company uses its assets for generating

sales. It helps having a check on credit policy whether it needs renewal or not and also how well

company is at inventory management (Schoenmaker and Schramade, 2018). For example,

inventory turnover, receivables collection period, account payables etc.

the revenue earned, cost of goods for the company, gross profit thus made. It gives insight of

variable and fixed expenses along with overhead costs and selling and administrative expenses. It

lastly gives the net income when all expenses have been deducted from revenues. This statement

is of utmost importance because of net profit which is the important factor regarding investment

and the efficiency of company in keeping check of operational costs.

Cash flow statement talks of cash inflows and cash outflows and tells about the sources of

income and source of expense that is where money comes in and goes out. It tells how

effectively organisation uses money and whether cash inflow is more than outflow which means

money is sufficient for operations. It also tells which projects have been generating investment as

returns and which projects are undergoing now which need money or cash outflow (Bailey,

2017).

The financial ratios depict the financial status of the company and thus are of importance for

investors and management to see how well the company is performing. The leverage ratios

indicate the financial health of the company. It tells whether the company has sufficient equity in

comparison to debt or not. This means company is able to manage its finances in a correct ratio

and can fulfil financial needs with mixture of both. Examples are debt to equity ratio and long-

term debt to capitalization ratio etc.

Profitability ratio gives indication of organisation to contain operational costs and generate

profits. The ratio is important as bottom line for investors to check on company’s profitability to

check on past five years whether it is able to pay the dividends by profit generation or not.

Examples of profitability ratios are gross profit, net profit, return on equity etc.

Asset management ratios help in determining how well company uses its assets for generating

sales. It helps having a check on credit policy whether it needs renewal or not and also how well

company is at inventory management (Schoenmaker and Schramade, 2018). For example,

inventory turnover, receivables collection period, account payables etc.

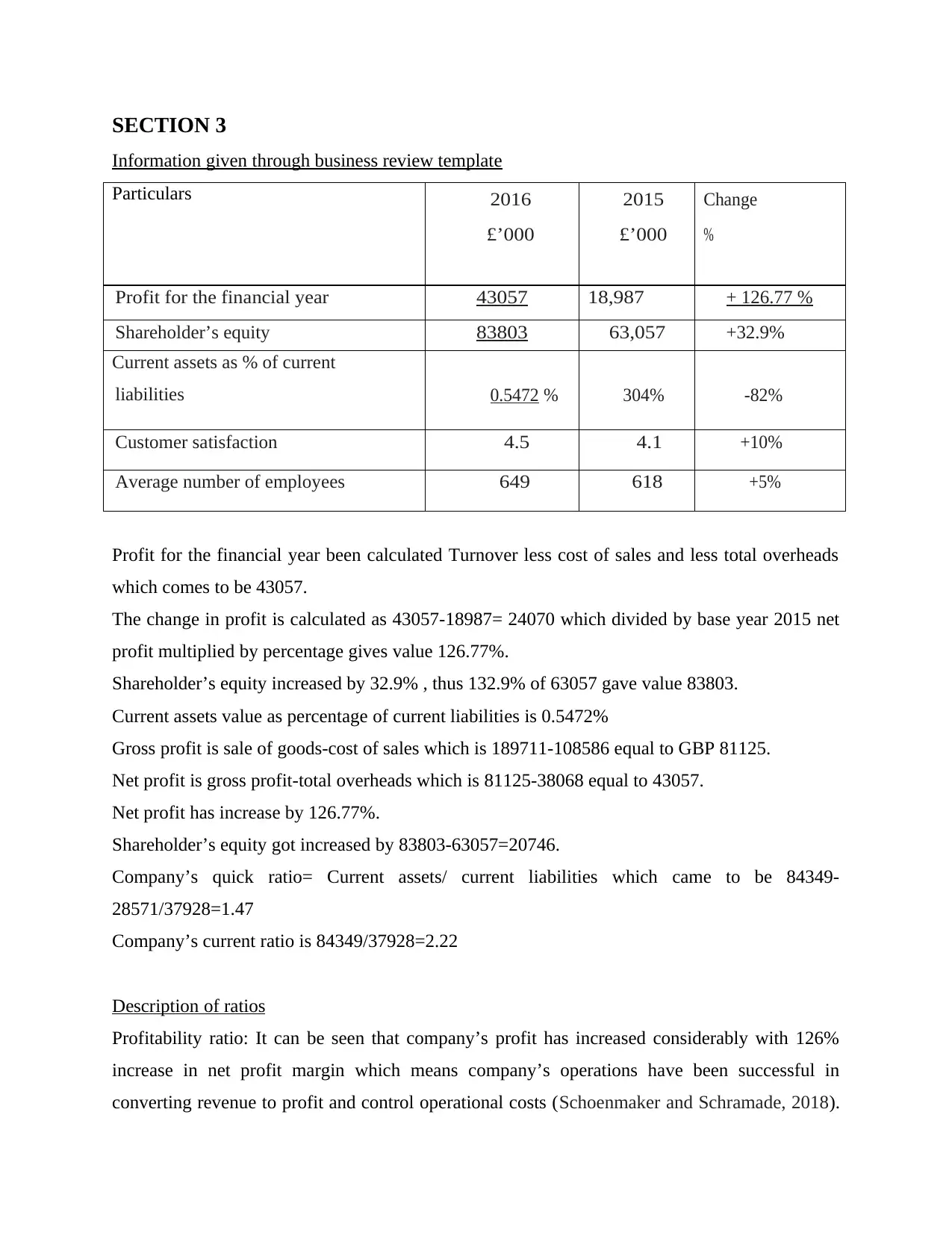

SECTION 3

Information given through business review template

Particulars 2016

£’000

2015

£’000

Change

%

Profit for the financial year 43057 18,987 + 126.77 %

Shareholder’s equity 83803 63,057 +32.9%

Current assets as % of current

liabilities 0.5472 % 304% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

Profit for the financial year been calculated Turnover less cost of sales and less total overheads

which comes to be 43057.

The change in profit is calculated as 43057-18987= 24070 which divided by base year 2015 net

profit multiplied by percentage gives value 126.77%.

Shareholder’s equity increased by 32.9% , thus 132.9% of 63057 gave value 83803.

Current assets value as percentage of current liabilities is 0.5472%

Gross profit is sale of goods-cost of sales which is 189711-108586 equal to GBP 81125.

Net profit is gross profit-total overheads which is 81125-38068 equal to 43057.

Net profit has increase by 126.77%.

Shareholder’s equity got increased by 83803-63057=20746.

Company’s quick ratio= Current assets/ current liabilities which came to be 84349-

28571/37928=1.47

Company’s current ratio is 84349/37928=2.22

Description of ratios

Profitability ratio: It can be seen that company’s profit has increased considerably with 126%

increase in net profit margin which means company’s operations have been successful in

converting revenue to profit and control operational costs (Schoenmaker and Schramade, 2018).

Information given through business review template

Particulars 2016

£’000

2015

£’000

Change

%

Profit for the financial year 43057 18,987 + 126.77 %

Shareholder’s equity 83803 63,057 +32.9%

Current assets as % of current

liabilities 0.5472 % 304% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

Profit for the financial year been calculated Turnover less cost of sales and less total overheads

which comes to be 43057.

The change in profit is calculated as 43057-18987= 24070 which divided by base year 2015 net

profit multiplied by percentage gives value 126.77%.

Shareholder’s equity increased by 32.9% , thus 132.9% of 63057 gave value 83803.

Current assets value as percentage of current liabilities is 0.5472%

Gross profit is sale of goods-cost of sales which is 189711-108586 equal to GBP 81125.

Net profit is gross profit-total overheads which is 81125-38068 equal to 43057.

Net profit has increase by 126.77%.

Shareholder’s equity got increased by 83803-63057=20746.

Company’s quick ratio= Current assets/ current liabilities which came to be 84349-

28571/37928=1.47

Company’s current ratio is 84349/37928=2.22

Description of ratios

Profitability ratio: It can be seen that company’s profit has increased considerably with 126%

increase in net profit margin which means company’s operations have been successful in

converting revenue to profit and control operational costs (Schoenmaker and Schramade, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales has increased too from the previous year and this has been effectively converted in profit

seen by gross profit and net profit margins. This is seen by investors as the bottom line of the

organisation as to how successfully company is able to control costs and get profits over a period

of time say, five years to assess financial performance.

Liquidity ratio

The company has quick and current ratio higher than 1 and less than 3 which signifies good

position in liquidity and use of assets for covering liabilities sufficiently. However, the ideal ratio

is 1:1. Company shall be able to pay current liabilities with help of current assets and this is seen

by investors as to how successfully company pays current liabilities and thus has liquidity

sufficient to pay them their dividends (Gupta and et.al., 2017).

Efficiency

The efficiency can be seen in how company has been able to manage operational costs and

increase profit which can be seen in net profit margin. In terms of efficiency, it can be noted that

operational and non-operating costs have fallen significantly from the previous year's high levels.

This impacts pricing and transaction costs for the product comes down. Efficiency can also be

seen how successful is organisation in maintaining inventory usage and account receivables

collection to check on the credit policy. This affects the working capital.

SECTION 4

Ways of improving financial performance

The aforementioned statistics clearly show that the company's gross profit ratio has been

constant over the past two years, with minimal fluctuation, which is a favourable indicator. That

is, the company's profit has increased over the prior year. Furthermore, it has been established

that the company's overall profit has increased from the previous year as a result of greater credit

facilities being made available to clients for the purchase of products and services. The credit

supplied must be utilised wisely in order to earn more money and enhance cash flow. Creditors

who have been engaged with the company for a long time can be given sufficient time. Getting

rid of unneeded overheads might also help you save money (Orus, Mugel and Lizaso, 2019).

seen by gross profit and net profit margins. This is seen by investors as the bottom line of the

organisation as to how successfully company is able to control costs and get profits over a period

of time say, five years to assess financial performance.

Liquidity ratio

The company has quick and current ratio higher than 1 and less than 3 which signifies good

position in liquidity and use of assets for covering liabilities sufficiently. However, the ideal ratio

is 1:1. Company shall be able to pay current liabilities with help of current assets and this is seen

by investors as to how successfully company pays current liabilities and thus has liquidity

sufficient to pay them their dividends (Gupta and et.al., 2017).

Efficiency

The efficiency can be seen in how company has been able to manage operational costs and

increase profit which can be seen in net profit margin. In terms of efficiency, it can be noted that

operational and non-operating costs have fallen significantly from the previous year's high levels.

This impacts pricing and transaction costs for the product comes down. Efficiency can also be

seen how successful is organisation in maintaining inventory usage and account receivables

collection to check on the credit policy. This affects the working capital.

SECTION 4

Ways of improving financial performance

The aforementioned statistics clearly show that the company's gross profit ratio has been

constant over the past two years, with minimal fluctuation, which is a favourable indicator. That

is, the company's profit has increased over the prior year. Furthermore, it has been established

that the company's overall profit has increased from the previous year as a result of greater credit

facilities being made available to clients for the purchase of products and services. The credit

supplied must be utilised wisely in order to earn more money and enhance cash flow. Creditors

who have been engaged with the company for a long time can be given sufficient time. Getting

rid of unneeded overheads might also help you save money (Orus, Mugel and Lizaso, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed assets that are just left idle, such as empty rooms in a building, can be used as warehouses

for inventory storage. This can assist save money on extra space while also increasing storage

throughout the holiday season. It can assist the company in raising funds by selling assets that

are no longer in use, such as old machinery. It will also lessen the company's reliance on interest-

bearing securities for capital generation.

To raise more capital, a company might engage in market operations such as investing in bonds

or conducting its own initial public offering (IPO), which allows it to raise funds from the

general public. This will grow capital as needed and generate enough revenue to continue

operations (Gupta and et.al., 2017).

Reduced product pricing can help to increase sales by attracting customers. On the purchase of

multiple products, offers and discounts may be granted. Customers are drawn to these schemes,

and higher prices can be maintained if premium products are being offered and operational costs

are high, allowing the money to be recovered without loss.

Raising equity while maintaining leverage can help a company's capital gearing. Friends and

fellow investors can help the company spend more in stock, allowing it to boost its gearing.

CONCLUSION

Finance management, it can be concluded, is a vital duty in recommending investments that are

beneficial to the firm, as well as reducing expenses and generating profits for the company. The

study explored the relevance of ratios and financial analysis, as well as the use of major financial

statements and their ramifications in business. The ratios' estimates reflected the company's

financial health and areas for improvement. The same was shown in a ratio study. Various

methods for improving a company's financial performance were considered.

for inventory storage. This can assist save money on extra space while also increasing storage

throughout the holiday season. It can assist the company in raising funds by selling assets that

are no longer in use, such as old machinery. It will also lessen the company's reliance on interest-

bearing securities for capital generation.

To raise more capital, a company might engage in market operations such as investing in bonds

or conducting its own initial public offering (IPO), which allows it to raise funds from the

general public. This will grow capital as needed and generate enough revenue to continue

operations (Gupta and et.al., 2017).

Reduced product pricing can help to increase sales by attracting customers. On the purchase of

multiple products, offers and discounts may be granted. Customers are drawn to these schemes,

and higher prices can be maintained if premium products are being offered and operational costs

are high, allowing the money to be recovered without loss.

Raising equity while maintaining leverage can help a company's capital gearing. Friends and

fellow investors can help the company spend more in stock, allowing it to boost its gearing.

CONCLUSION

Finance management, it can be concluded, is a vital duty in recommending investments that are

beneficial to the firm, as well as reducing expenses and generating profits for the company. The

study explored the relevance of ratios and financial analysis, as well as the use of major financial

statements and their ramifications in business. The ratios' estimates reflected the company's

financial health and areas for improvement. The same was shown in a ratio study. Various

methods for improving a company's financial performance were considered.

REFERENCES

Books and journals

Akan, M. and Tevfik, A.T., 2020. Fundamentals of finance. In Fundamentals of Finance. De

Gruyter.

Bailey, S.J., 2017. Strategic public finance. Macmillan International Higher Education.

Schoenmaker, D. and Schramade, W., 2018. Principles of sustainable finance. Oxford University

Press.

Gupta, M.S., Keen, M.M., Shah, M.A. and Verdier, M.G. eds., 2017. Digital revolutions in

public finance. International Monetary Fund.

Orus, R., Mugel, S. and Lizaso, E., 2019. Quantum computing for finance: Overview and

prospects. Reviews in Physics, 4, p.100028.

Bulturbayevich, M.B., Sharipdjanovna, S.G., Ibragimovich, A.S. and Gulnora, M., 2020. Modern

features of financial management in small businesses. International Engineering Journal

For Research & Development, 5(4), pp.5-5.

Books and journals

Akan, M. and Tevfik, A.T., 2020. Fundamentals of finance. In Fundamentals of Finance. De

Gruyter.

Bailey, S.J., 2017. Strategic public finance. Macmillan International Higher Education.

Schoenmaker, D. and Schramade, W., 2018. Principles of sustainable finance. Oxford University

Press.

Gupta, M.S., Keen, M.M., Shah, M.A. and Verdier, M.G. eds., 2017. Digital revolutions in

public finance. International Monetary Fund.

Orus, R., Mugel, S. and Lizaso, E., 2019. Quantum computing for finance: Overview and

prospects. Reviews in Physics, 4, p.100028.

Bulturbayevich, M.B., Sharipdjanovna, S.G., Ibragimovich, A.S. and Gulnora, M., 2020. Modern

features of financial management in small businesses. International Engineering Journal

For Research & Development, 5(4), pp.5-5.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

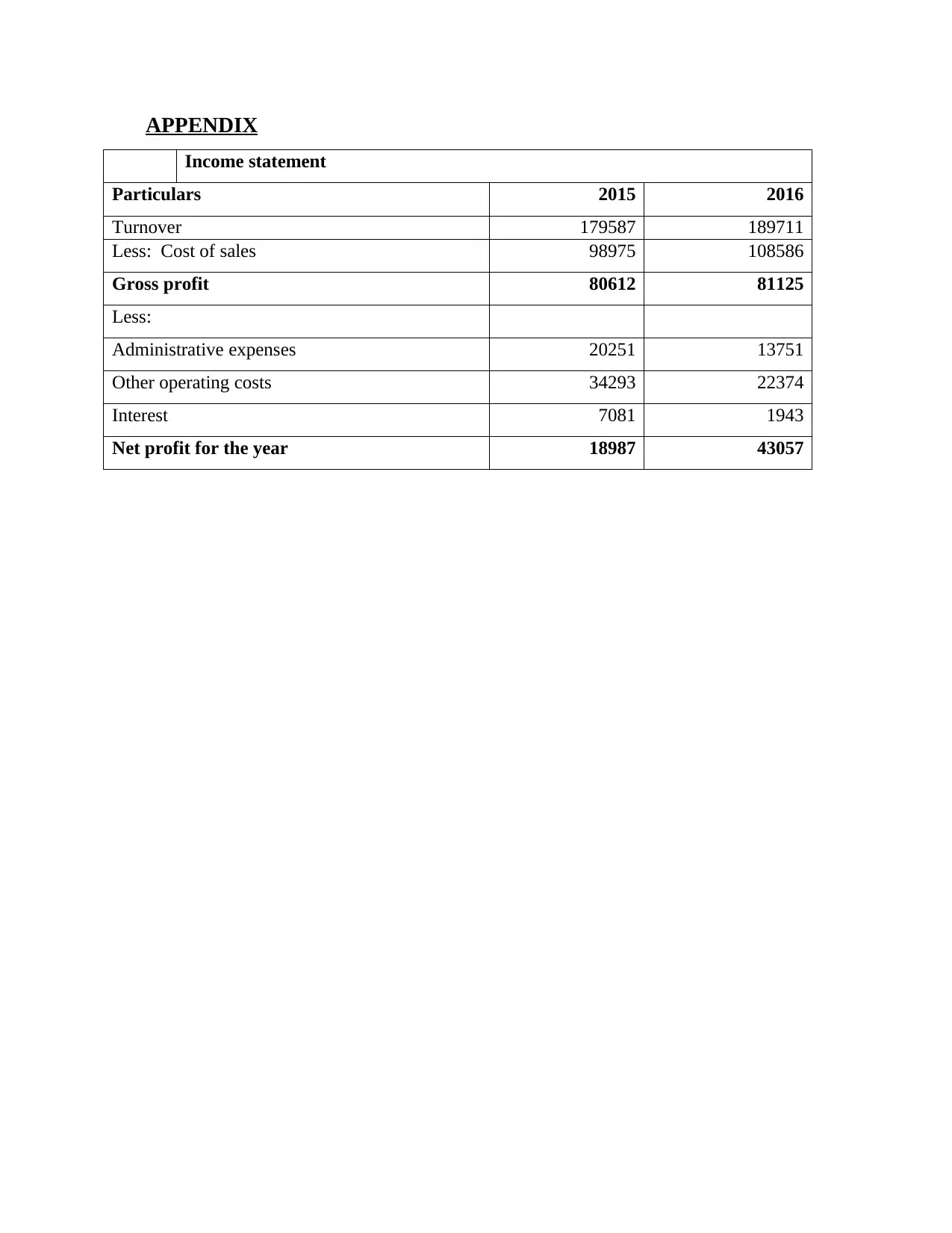

APPENDIX

Income statement

Particulars 2015 2016

Turnover 179587 189711

Less: Cost of sales 98975 108586

Gross profit 80612 81125

Less:

Administrative expenses 20251 13751

Other operating costs 34293 22374

Interest 7081 1943

Net profit for the year 18987 43057

Income statement

Particulars 2015 2016

Turnover 179587 189711

Less: Cost of sales 98975 108586

Gross profit 80612 81125

Less:

Administrative expenses 20251 13751

Other operating costs 34293 22374

Interest 7081 1943

Net profit for the year 18987 43057

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

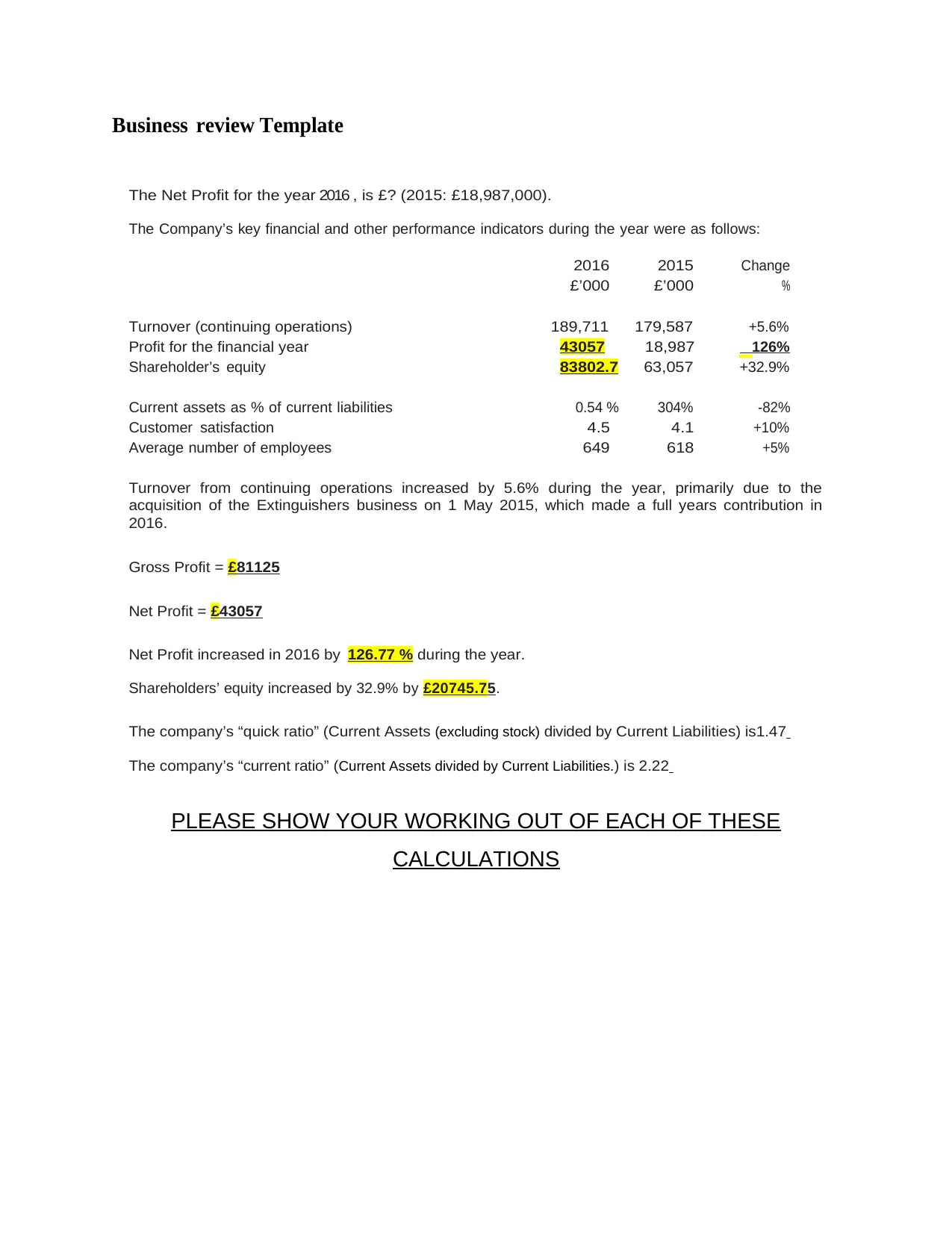

Business review Template

The Net Profit for the year 2016 , is £? (2015: £18,987,000).

The Company’s key financial and other performance indicators during the year were as follows:

2016

£’000

2015

£’000

Change

%

Turnover (continuing operations) 189,711 179,587 +5.6%

Profit for the financial year 43057 18,987 126%

%Shareholder’s equity 83802.7 63,057 +32.9%

Current assets as % of current liabilities 0.54 % 304% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

Turnover from continuing operations increased by 5.6% during the year, primarily due to the

acquisition of the Extinguishers business on 1 May 2015, which made a full years contribution in

2016.

Gross Profit = £81125

Net Profit = £43057

Net Profit increased in 2016 by 126.77 % during the year.

Shareholders’ equity increased by 32.9% by £20745.75.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current Liabilities) is1.47

The company’s “current ratio” (Current Assets divided by Current Liabilities. ) is 2.22

PLEASE SHOW YOUR WORKING OUT OF EACH OF THESE

CALCULATIONS

The Net Profit for the year 2016 , is £? (2015: £18,987,000).

The Company’s key financial and other performance indicators during the year were as follows:

2016

£’000

2015

£’000

Change

%

Turnover (continuing operations) 189,711 179,587 +5.6%

Profit for the financial year 43057 18,987 126%

%Shareholder’s equity 83802.7 63,057 +32.9%

Current assets as % of current liabilities 0.54 % 304% -82%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

Turnover from continuing operations increased by 5.6% during the year, primarily due to the

acquisition of the Extinguishers business on 1 May 2015, which made a full years contribution in

2016.

Gross Profit = £81125

Net Profit = £43057

Net Profit increased in 2016 by 126.77 % during the year.

Shareholders’ equity increased by 32.9% by £20745.75.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current Liabilities) is1.47

The company’s “current ratio” (Current Assets divided by Current Liabilities. ) is 2.22

PLEASE SHOW YOUR WORKING OUT OF EACH OF THESE

CALCULATIONS

Notes to the financial statements

at 31 December 2016

3. Turnover

Turnover recognised in the income statement is analysed as follows.

2016 2015

£000 £000

Sale of goods 189,711 179,587

Turnover from continuing operations 189,711 179,587

4. Cost of Sales

2016 2015

£000 £000

Material Cost 42,597 38.845

Production Cost 15,231 12,845

Labour Cost 50,758 47,285

Cost of Sales 108,586 98,975

5. Overheads

2016 2015

at 31 December 2016

3. Turnover

Turnover recognised in the income statement is analysed as follows.

2016 2015

£000 £000

Sale of goods 189,711 179,587

Turnover from continuing operations 189,711 179,587

4. Cost of Sales

2016 2015

£000 £000

Material Cost 42,597 38.845

Production Cost 15,231 12,845

Labour Cost 50,758 47,285

Cost of Sales 108,586 98,975

5. Overheads

2016 2015

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.