Comprehensive Financial Report: Profit, Cash Flow, Ratio Analysis

VerifiedAdded on 2023/01/19

|14

|3357

|96

Report

AI Summary

This report provides a comprehensive analysis of business finance concepts, focusing on profit, cash flow, and working capital management. It begins by differentiating between profit and cash flow, highlighting the importance of working capital components such as receivables, inventory, and payables. The report then examines the impact of working capital changes on cash flow, emphasizing strategies for effective financial position management. It also includes a detailed discussion on improving cash flow through efficient working capital management. Furthermore, the report analyzes financial ratios, including sales growth, gross profit ratio, operating profit ratio, gearing ratio, interest coverage ratio, liquidity ratio, return on equity, and return on capital employed, to assess the financial performance of an entity. The analysis includes computations of these ratios for a three-year period, interpretations of the results, and recommendations for enhancing financial performance. Desklib offers a variety of solved assignments and past papers for students seeking additional resources.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

I...............................................................................................................................................3

a. Presenting meaning of Profit and cash flow and explaining their differences...................3

b. Presenting meaning of working capital and receivables, inventory and payables.............4

c. The effects of working capital changes over cash flow......................................................4

2. Financial position management by the different concepts.................................................5

3. Ways to improve the cash flow by working capital management......................................6

PART-2............................................................................................................................................6

1.a Explaining the component that each of the ratio depicts in relation to financial

performance............................................................................................................................6

1.b. Computing the ratios for 3 years.....................................................................................7

1.c. Interpreting the results by showing the reasons for the change in each of the ratio over the

years........................................................................................................................................9

2. Assessment and the recommendations in respect of the financial performance of an entity10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

I...............................................................................................................................................3

a. Presenting meaning of Profit and cash flow and explaining their differences...................3

b. Presenting meaning of working capital and receivables, inventory and payables.............4

c. The effects of working capital changes over cash flow......................................................4

2. Financial position management by the different concepts.................................................5

3. Ways to improve the cash flow by working capital management......................................6

PART-2............................................................................................................................................6

1.a Explaining the component that each of the ratio depicts in relation to financial

performance............................................................................................................................6

1.b. Computing the ratios for 3 years.....................................................................................7

1.c. Interpreting the results by showing the reasons for the change in each of the ratio over the

years........................................................................................................................................9

2. Assessment and the recommendations in respect of the financial performance of an entity10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Business finance refers to money and credit invested in business for the effective and

efficient growth of the company. The report is conducted in 2 parts. In 1 part Flashy product Ltd

company is taken which is a manufacturer company produce sport equipment. They manufacture

the products in UK & China and sell in different countries such as UK, south Asia and Australia.

The report highlights the importance of financial statements in management company financial

results. In the second part of the report it explains the different financial ratio and their changing

trend of Farringdon Pharma Ltd. Company.

MAIN BODY

PART 1

I.

a. Presenting meaning of Profit and cash flow and explaining their differences

Profit:for na organisation can be understood as financial gain which is earned by

company which is basically the difference between the amount earned and expenditure made for

generating such revenues. The profits are the real earning of a firm which is reached after

deducting all operation and financial expenses for the overall activities of business.

Cash flow: of a business is the total inflow and out flow of the cash within business

operation for a specific time period (Cash Flows from Operating Activities, 2019). This is

basically the incoming and outgoing of the cash from the operating, financing and investing

activities of the business. The cash flow depicts the changes in holding of cash over an income

year through the incoming and outgoings of cash form company within same period.

Difference between profit and cash flow:

Cash and profits are both crucial aspects of a business and required for successful

operations in the long term. A company is required to generate profits while operating with

positive cash flow. Cash flow is inflow and outflow of cash form the business which is required

to meet daily expenses of the business such as purchase of inventory, taxes, paying employees

and others. On the other had profits are the surplus after all the expenses are met and the total is

deducted from the overall revenues earned (Are a Firm's Cash Flow and Profit Different, 2019).

Cash flow is basically the way through which cash flows in business and company can have a

positive cash flow with having no profits. On other others hand a company can have negative

cash floes while having large profits, so the one of the major difference between both profits

Business finance refers to money and credit invested in business for the effective and

efficient growth of the company. The report is conducted in 2 parts. In 1 part Flashy product Ltd

company is taken which is a manufacturer company produce sport equipment. They manufacture

the products in UK & China and sell in different countries such as UK, south Asia and Australia.

The report highlights the importance of financial statements in management company financial

results. In the second part of the report it explains the different financial ratio and their changing

trend of Farringdon Pharma Ltd. Company.

MAIN BODY

PART 1

I.

a. Presenting meaning of Profit and cash flow and explaining their differences

Profit:for na organisation can be understood as financial gain which is earned by

company which is basically the difference between the amount earned and expenditure made for

generating such revenues. The profits are the real earning of a firm which is reached after

deducting all operation and financial expenses for the overall activities of business.

Cash flow: of a business is the total inflow and out flow of the cash within business

operation for a specific time period (Cash Flows from Operating Activities, 2019). This is

basically the incoming and outgoing of the cash from the operating, financing and investing

activities of the business. The cash flow depicts the changes in holding of cash over an income

year through the incoming and outgoings of cash form company within same period.

Difference between profit and cash flow:

Cash and profits are both crucial aspects of a business and required for successful

operations in the long term. A company is required to generate profits while operating with

positive cash flow. Cash flow is inflow and outflow of cash form the business which is required

to meet daily expenses of the business such as purchase of inventory, taxes, paying employees

and others. On the other had profits are the surplus after all the expenses are met and the total is

deducted from the overall revenues earned (Are a Firm's Cash Flow and Profit Different, 2019).

Cash flow is basically the way through which cash flows in business and company can have a

positive cash flow with having no profits. On other others hand a company can have negative

cash floes while having large profits, so the one of the major difference between both profits

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

realization depends on accounting basis while cash flow depends on sources of the cash

transactions.

b. Presenting meaning of working capital and receivables, inventory and payables

Working capital: for a business is a financial metrics representing operating liquidity of

company which depicts the ability of firm in meeting short term obligations of organisation. WC

is calculated as deducting current liabilities from current assets. Under normal trade cycle

working capital is equals to working assets.

Receivables: or account receivables reflecting at asset side of balance sheet depicts the

balance of money due to the firm for the goods and services delivers to its consumers which is

not yet paid by the users. This is the money owned by consumers to the organisation and the

quantum of amount and its rotation shows the credit sales made by company also the capacity of

organisation in realising the dues form consumers.

Payables: or account payables reflects of liability side of balance sheet of a company and

this shows the amount that is owed by the company to its suppliers and creditors. This quantum

shows the credit purchase of goods and services made by company. This is short term debt of the

company classified under current liability of organisation.

Inventory: for a business includes raw material used for production of goods, work in

progress and the finished goods. This is basically the merchandise, goods and material held by

the business for selling to consumer (finished goods), or make the final products after processing

(raw material and work in progress) in order to generate profits.

c. The effects of working capital changes over cash flow

Working capital of a business is represented as difference between current asset and

current liability of the business (Working capital finance,2019). Changes in the working capital

are reflected in the cash flow statement of company, which can be explained with some

examples:

When a transaction reflects an increase in current asset and current liability with same

amount there is no change in the working capital.

In case of decrease in assets, cash floe from operations will increase while reducing the

working capital.

Also, an increase in account receivables shows that there is less collection by company

and this effects the cash flow negatively while increasing the working capital.

transactions.

b. Presenting meaning of working capital and receivables, inventory and payables

Working capital: for a business is a financial metrics representing operating liquidity of

company which depicts the ability of firm in meeting short term obligations of organisation. WC

is calculated as deducting current liabilities from current assets. Under normal trade cycle

working capital is equals to working assets.

Receivables: or account receivables reflecting at asset side of balance sheet depicts the

balance of money due to the firm for the goods and services delivers to its consumers which is

not yet paid by the users. This is the money owned by consumers to the organisation and the

quantum of amount and its rotation shows the credit sales made by company also the capacity of

organisation in realising the dues form consumers.

Payables: or account payables reflects of liability side of balance sheet of a company and

this shows the amount that is owed by the company to its suppliers and creditors. This quantum

shows the credit purchase of goods and services made by company. This is short term debt of the

company classified under current liability of organisation.

Inventory: for a business includes raw material used for production of goods, work in

progress and the finished goods. This is basically the merchandise, goods and material held by

the business for selling to consumer (finished goods), or make the final products after processing

(raw material and work in progress) in order to generate profits.

c. The effects of working capital changes over cash flow

Working capital of a business is represented as difference between current asset and

current liability of the business (Working capital finance,2019). Changes in the working capital

are reflected in the cash flow statement of company, which can be explained with some

examples:

When a transaction reflects an increase in current asset and current liability with same

amount there is no change in the working capital.

In case of decrease in assets, cash floe from operations will increase while reducing the

working capital.

Also, an increase in account receivables shows that there is less collection by company

and this effects the cash flow negatively while increasing the working capital.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above examples it can be stated that changes in the working capital have a

direct impact on the cash flow which can be both in negative and positive way.

2. Financial position management by the different concepts

The profit of the company helps to manage the various financial activity. The operating

profit of Flashy product Ltd. Company is £4 million and the average turnover of the company in

last 5 year is £50 million which present that company is able to manage the performance in

market. But from the internal reorganisation it has been reflected that they did not control the

credit, manage inventory and purchases in the organisation which increases the wastage.

The working capital management help the Flashy product Ltd. Company to improve the

cash flow position. To manage the working capital they have to control the inventory level by

using the various software to regulate the inventory level and only order the quantity when they

required (Muhammad, Rehman and Waqas, 2016). The management of inventory also reduces

the maintenance cost and increases the working capital to meet day to day short term expenses.

The mismanagement of working capital increases the cost and debt of the company which

ultimately decreases their profit.

The formulation of budget help the company to regulate the cost involve in each activity

and manage the activities according to the differences arise in expected and actual budget of

particular accounting period. They have to use the electronic payments to manage the cash flow

in the organisation for fulfilling the daily requirement of cash (Robinson and Sensoy, 2016).

Flashy product Ltd. Company has to control the credit and reduces the time period of collecting

payment from the debtor. It increases the cash level and present the positive cash flow. The

management of working capital by regulating inventory, receivables, payables etc. and cash flow

provide the support to improve the financial results.

The financial position of Flashy product Ltd. Company reflect the £5 million overdraft

which shows that in compare to the last year company's overdraft is increases. The overdraft of

the company increases the current liability and show the negative working capital. It also

increases the debt of the company because a long term negative working capital reflect that

company is struggled to manage current liabilities. The different financial tools help the

company to manage financial position and improve the profit in the market.

direct impact on the cash flow which can be both in negative and positive way.

2. Financial position management by the different concepts

The profit of the company helps to manage the various financial activity. The operating

profit of Flashy product Ltd. Company is £4 million and the average turnover of the company in

last 5 year is £50 million which present that company is able to manage the performance in

market. But from the internal reorganisation it has been reflected that they did not control the

credit, manage inventory and purchases in the organisation which increases the wastage.

The working capital management help the Flashy product Ltd. Company to improve the

cash flow position. To manage the working capital they have to control the inventory level by

using the various software to regulate the inventory level and only order the quantity when they

required (Muhammad, Rehman and Waqas, 2016). The management of inventory also reduces

the maintenance cost and increases the working capital to meet day to day short term expenses.

The mismanagement of working capital increases the cost and debt of the company which

ultimately decreases their profit.

The formulation of budget help the company to regulate the cost involve in each activity

and manage the activities according to the differences arise in expected and actual budget of

particular accounting period. They have to use the electronic payments to manage the cash flow

in the organisation for fulfilling the daily requirement of cash (Robinson and Sensoy, 2016).

Flashy product Ltd. Company has to control the credit and reduces the time period of collecting

payment from the debtor. It increases the cash level and present the positive cash flow. The

management of working capital by regulating inventory, receivables, payables etc. and cash flow

provide the support to improve the financial results.

The financial position of Flashy product Ltd. Company reflect the £5 million overdraft

which shows that in compare to the last year company's overdraft is increases. The overdraft of

the company increases the current liability and show the negative working capital. It also

increases the debt of the company because a long term negative working capital reflect that

company is struggled to manage current liabilities. The different financial tools help the

company to manage financial position and improve the profit in the market.

3. Ways to improve the cash flow by working capital management

The current position of Flashy product Ltd. Company reflect that they never focus on

working capital management. They have to manage the working capital by regulating the current

assets and current liability (Mathuva, 2015). Working capital reflect the difference between

current assets and current liability. The excess of current assets reflect positive working capital

and excess of current liability reflect negative working capital. Due to the mismanagement of

credit control and inventory level the working capital cycle is increases 4 times.

It can be recommend that Flashy product Ltd. Company has to control the credit and

regulate the time period of collecting the payment from the debtors which help to reduce the

liabilities and increases the cash inflow by collecting payments on time. They have to use the

credit card rather than to pay in cash. The usage of credit card in purchasing the inventory and

other current assets increases the current asset level and does not reduce the cash inflow which

also reflect positive cash flow.

It also recommends that Flashy product Ltd. Company has to control the inventory level

and regulate the inventory in fixed time interval. It helps them to reduce the maintenance cost of

the company which ultimately increases the cash flow. The control of trade receivables and trade

payables also help the organisation to reflect positive working capital and pay the short term

expenses on time and increases the cash level in organisation.

PART-2

1.a Explaining the component that each of the ratio depicts in relation to financial performance

Sales growth- It refers to the increase or the decrease in the sales of an entity from one

period to another (Choi and et.al., 2018). It reflects the percentage of the revenue growth that is

been gained by Flashy products Ltd. It helps in determining the revenue trend of the business

over the time. Higher the percentage of the sales growth, reflects more profitability within the

business.

Gross profit ratio- It refers to the profitability ratio which indicates the relationship in

between the net sales and the gross profit. It is the most useful tool in evaluating the operational

efficiency of Flashy products Ltd.

Operating profit ratio- It indicates the amount of the profits that is been earned by the

company after making the payment of its variable cost. This ratio states the percentage of the

The current position of Flashy product Ltd. Company reflect that they never focus on

working capital management. They have to manage the working capital by regulating the current

assets and current liability (Mathuva, 2015). Working capital reflect the difference between

current assets and current liability. The excess of current assets reflect positive working capital

and excess of current liability reflect negative working capital. Due to the mismanagement of

credit control and inventory level the working capital cycle is increases 4 times.

It can be recommend that Flashy product Ltd. Company has to control the credit and

regulate the time period of collecting the payment from the debtors which help to reduce the

liabilities and increases the cash inflow by collecting payments on time. They have to use the

credit card rather than to pay in cash. The usage of credit card in purchasing the inventory and

other current assets increases the current asset level and does not reduce the cash inflow which

also reflect positive cash flow.

It also recommends that Flashy product Ltd. Company has to control the inventory level

and regulate the inventory in fixed time interval. It helps them to reduce the maintenance cost of

the company which ultimately increases the cash flow. The control of trade receivables and trade

payables also help the organisation to reflect positive working capital and pay the short term

expenses on time and increases the cash level in organisation.

PART-2

1.a Explaining the component that each of the ratio depicts in relation to financial performance

Sales growth- It refers to the increase or the decrease in the sales of an entity from one

period to another (Choi and et.al., 2018). It reflects the percentage of the revenue growth that is

been gained by Flashy products Ltd. It helps in determining the revenue trend of the business

over the time. Higher the percentage of the sales growth, reflects more profitability within the

business.

Gross profit ratio- It refers to the profitability ratio which indicates the relationship in

between the net sales and the gross profit. It is the most useful tool in evaluating the operational

efficiency of Flashy products Ltd.

Operating profit ratio- It indicates the amount of the profits that is been earned by the

company after making the payment of its variable cost. This ratio states the percentage of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profits earned by Flashy products Ltd by keeping the control over the expenses and the cost with

respect to the business operations.

Gearing ratio- It is a kind of the financial ratio which focuses on comparing the debts of

the company with that of its equity (DeBord and et.al., 2017). Gearing ratio represent the

leverage position of the company.

Interest coverage ratio- It referred as the ratio that helps in determining the interest

obligation of Flashy products against its net income. It also depicts the leverage position of an

enterprise. This ratio is used to identify the risk that is associated relating to the current debt and

the future borrowings of an organization.

Liquidity ratio- This ratio reflects the liquidity position of the firm and act as the

financial metric in respect of determining the ability of Flashy products in meeting their current

obligations.

Return on equity- It is the measure of the financial performance that reflects the extent to

which the management of Flashy products is making use of its assets in order to generate profits.

This ratio depicts the income generated against shareholders funds of an organization

(Fallahpour, Lakvan and Zadeh, 2017).

Return on capital employed- It is the profitability ratio which measures the profits that

are been earned by the firm through the use of its capital employed.

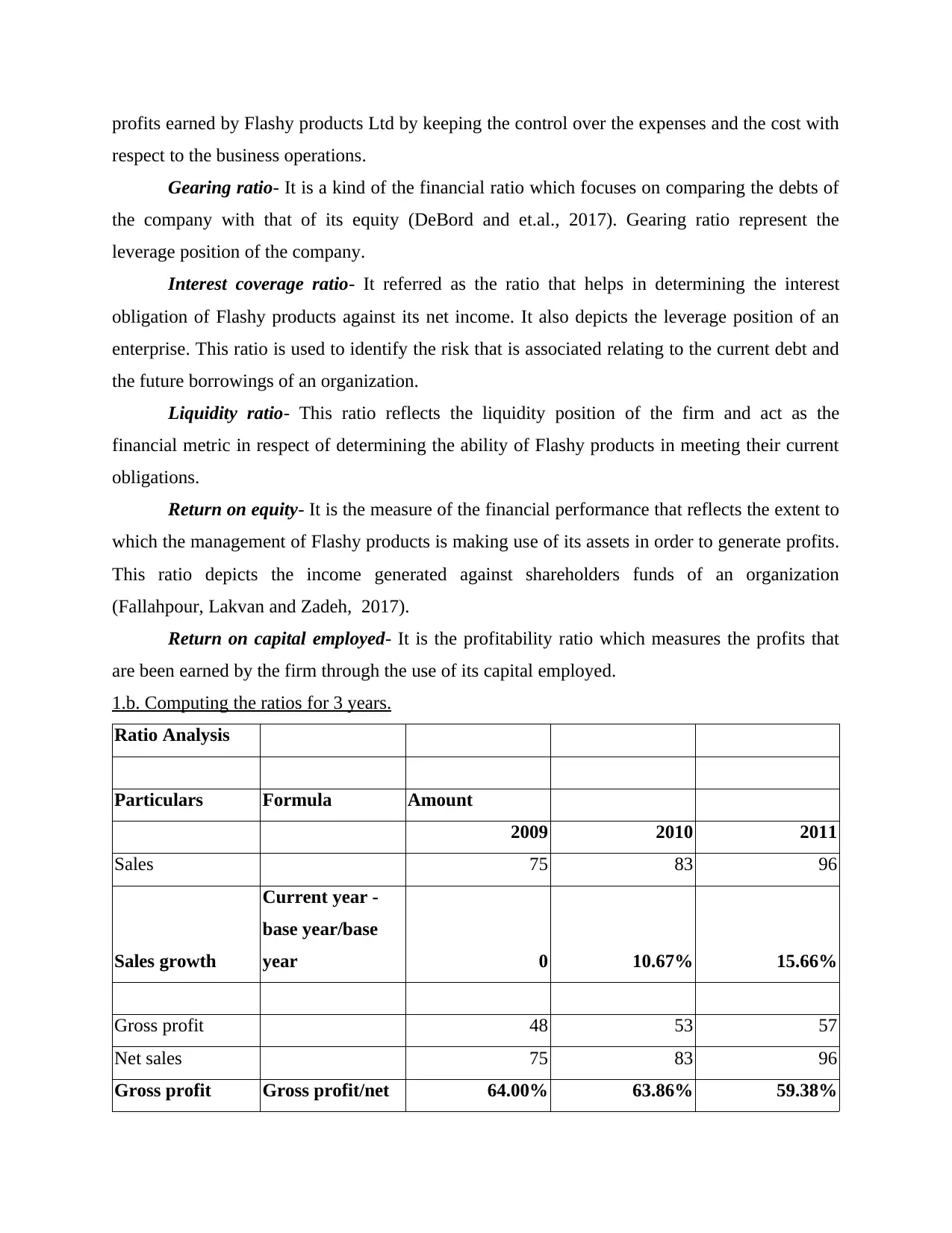

1.b. Computing the ratios for 3 years.

Ratio Analysis

Particulars Formula Amount

2009 2010 2011

Sales 75 83 96

Sales growth

Current year -

base year/base

year 0 10.67% 15.66%

Gross profit 48 53 57

Net sales 75 83 96

Gross profit Gross profit/net 64.00% 63.86% 59.38%

respect to the business operations.

Gearing ratio- It is a kind of the financial ratio which focuses on comparing the debts of

the company with that of its equity (DeBord and et.al., 2017). Gearing ratio represent the

leverage position of the company.

Interest coverage ratio- It referred as the ratio that helps in determining the interest

obligation of Flashy products against its net income. It also depicts the leverage position of an

enterprise. This ratio is used to identify the risk that is associated relating to the current debt and

the future borrowings of an organization.

Liquidity ratio- This ratio reflects the liquidity position of the firm and act as the

financial metric in respect of determining the ability of Flashy products in meeting their current

obligations.

Return on equity- It is the measure of the financial performance that reflects the extent to

which the management of Flashy products is making use of its assets in order to generate profits.

This ratio depicts the income generated against shareholders funds of an organization

(Fallahpour, Lakvan and Zadeh, 2017).

Return on capital employed- It is the profitability ratio which measures the profits that

are been earned by the firm through the use of its capital employed.

1.b. Computing the ratios for 3 years.

Ratio Analysis

Particulars Formula Amount

2009 2010 2011

Sales 75 83 96

Sales growth

Current year -

base year/base

year 0 10.67% 15.66%

Gross profit 48 53 57

Net sales 75 83 96

Gross profit Gross profit/net 64.00% 63.86% 59.38%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

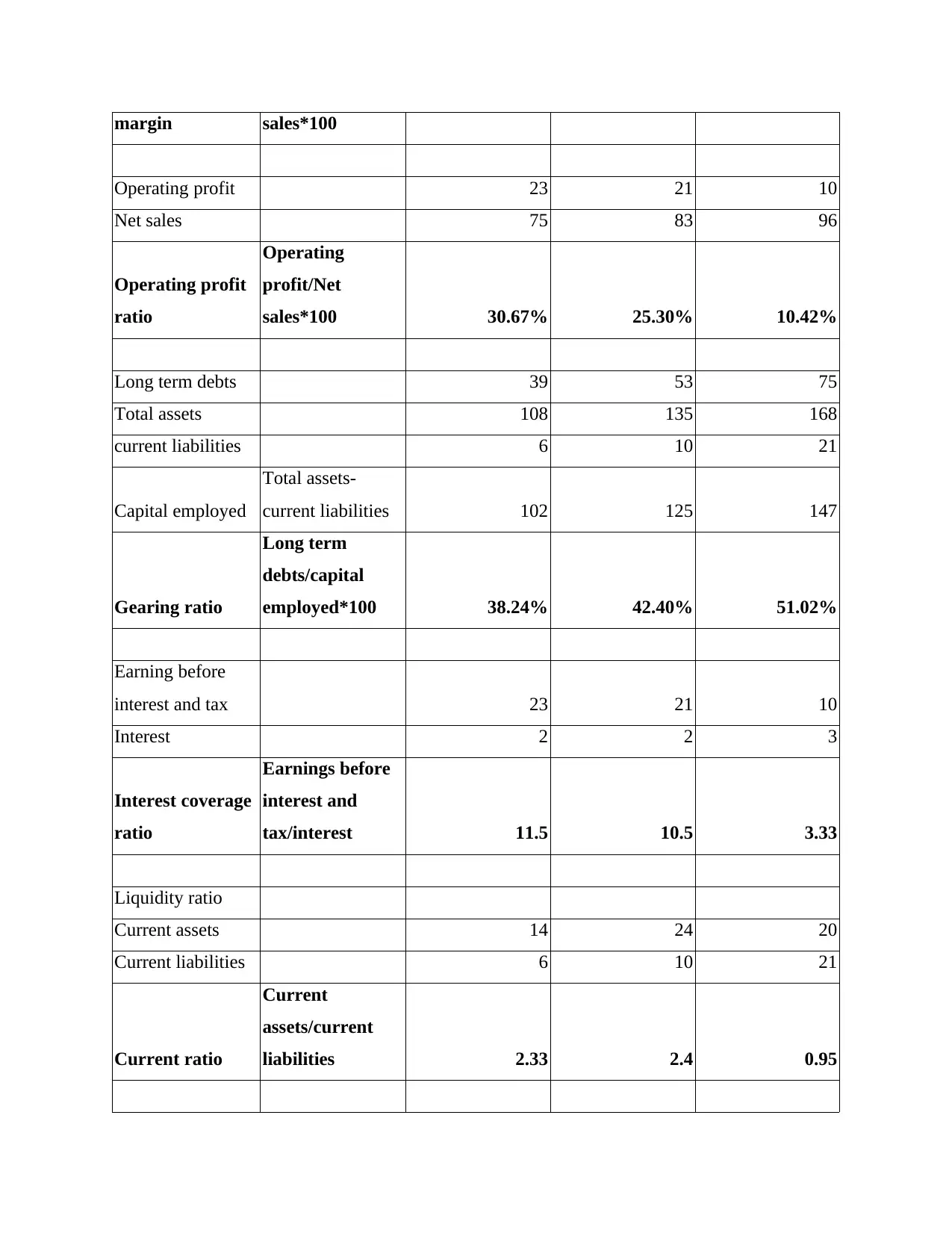

margin sales*100

Operating profit 23 21 10

Net sales 75 83 96

Operating profit

ratio

Operating

profit/Net

sales*100 30.67% 25.30% 10.42%

Long term debts 39 53 75

Total assets 108 135 168

current liabilities 6 10 21

Capital employed

Total assets-

current liabilities 102 125 147

Gearing ratio

Long term

debts/capital

employed*100 38.24% 42.40% 51.02%

Earning before

interest and tax 23 21 10

Interest 2 2 3

Interest coverage

ratio

Earnings before

interest and

tax/interest 11.5 10.5 3.33

Liquidity ratio

Current assets 14 24 20

Current liabilities 6 10 21

Current ratio

Current

assets/current

liabilities 2.33 2.4 0.95

Operating profit 23 21 10

Net sales 75 83 96

Operating profit

ratio

Operating

profit/Net

sales*100 30.67% 25.30% 10.42%

Long term debts 39 53 75

Total assets 108 135 168

current liabilities 6 10 21

Capital employed

Total assets-

current liabilities 102 125 147

Gearing ratio

Long term

debts/capital

employed*100 38.24% 42.40% 51.02%

Earning before

interest and tax 23 21 10

Interest 2 2 3

Interest coverage

ratio

Earnings before

interest and

tax/interest 11.5 10.5 3.33

Liquidity ratio

Current assets 14 24 20

Current liabilities 6 10 21

Current ratio

Current

assets/current

liabilities 2.33 2.4 0.95

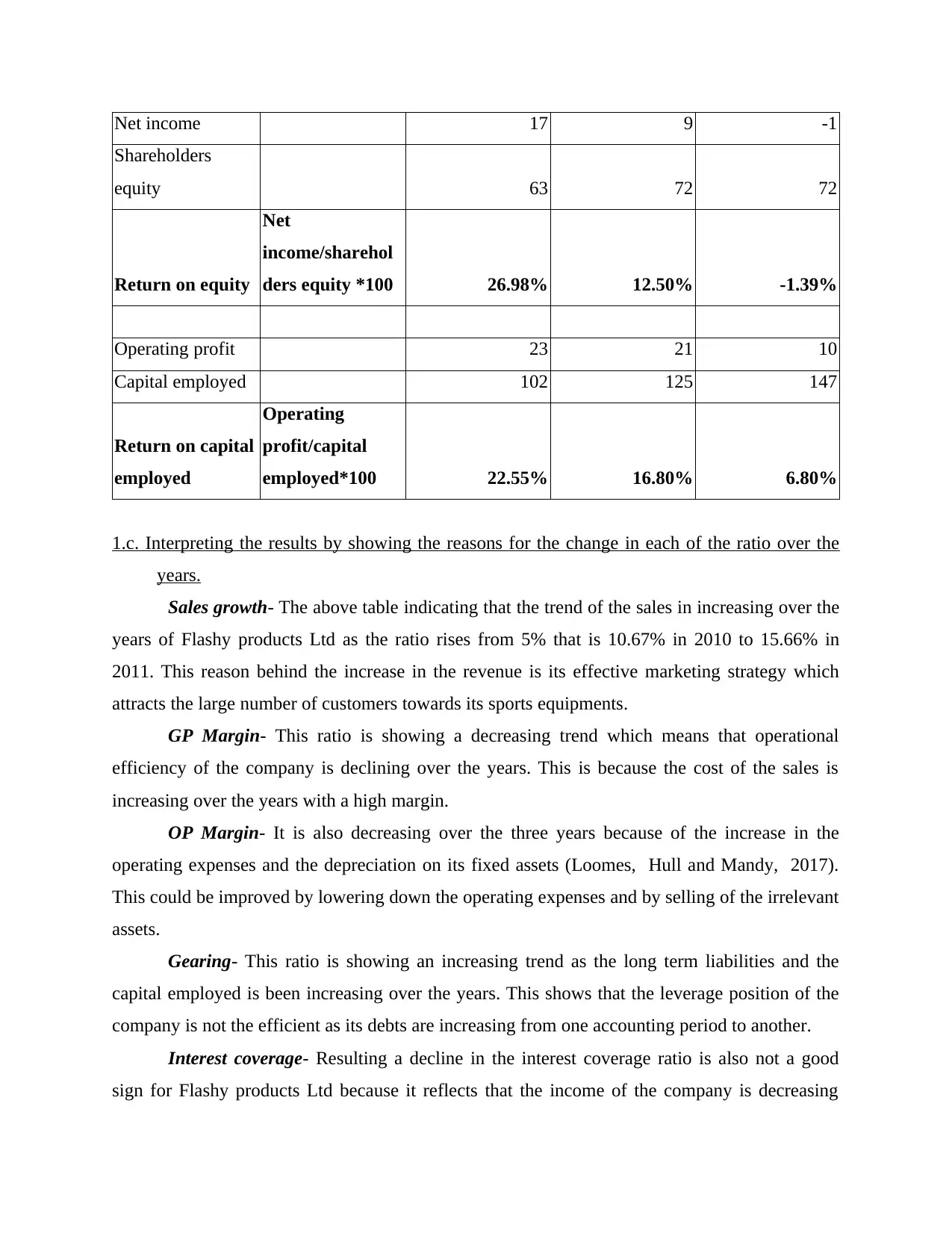

Net income 17 9 -1

Shareholders

equity 63 72 72

Return on equity

Net

income/sharehol

ders equity *100 26.98% 12.50% -1.39%

Operating profit 23 21 10

Capital employed 102 125 147

Return on capital

employed

Operating

profit/capital

employed*100 22.55% 16.80% 6.80%

1.c. Interpreting the results by showing the reasons for the change in each of the ratio over the

years.

Sales growth- The above table indicating that the trend of the sales in increasing over the

years of Flashy products Ltd as the ratio rises from 5% that is 10.67% in 2010 to 15.66% in

2011. This reason behind the increase in the revenue is its effective marketing strategy which

attracts the large number of customers towards its sports equipments.

GP Margin- This ratio is showing a decreasing trend which means that operational

efficiency of the company is declining over the years. This is because the cost of the sales is

increasing over the years with a high margin.

OP Margin- It is also decreasing over the three years because of the increase in the

operating expenses and the depreciation on its fixed assets (Loomes, Hull and Mandy, 2017).

This could be improved by lowering down the operating expenses and by selling of the irrelevant

assets.

Gearing- This ratio is showing an increasing trend as the long term liabilities and the

capital employed is been increasing over the years. This shows that the leverage position of the

company is not the efficient as its debts are increasing from one accounting period to another.

Interest coverage- Resulting a decline in the interest coverage ratio is also not a good

sign for Flashy products Ltd because it reflects that the income of the company is decreasing

Shareholders

equity 63 72 72

Return on equity

Net

income/sharehol

ders equity *100 26.98% 12.50% -1.39%

Operating profit 23 21 10

Capital employed 102 125 147

Return on capital

employed

Operating

profit/capital

employed*100 22.55% 16.80% 6.80%

1.c. Interpreting the results by showing the reasons for the change in each of the ratio over the

years.

Sales growth- The above table indicating that the trend of the sales in increasing over the

years of Flashy products Ltd as the ratio rises from 5% that is 10.67% in 2010 to 15.66% in

2011. This reason behind the increase in the revenue is its effective marketing strategy which

attracts the large number of customers towards its sports equipments.

GP Margin- This ratio is showing a decreasing trend which means that operational

efficiency of the company is declining over the years. This is because the cost of the sales is

increasing over the years with a high margin.

OP Margin- It is also decreasing over the three years because of the increase in the

operating expenses and the depreciation on its fixed assets (Loomes, Hull and Mandy, 2017).

This could be improved by lowering down the operating expenses and by selling of the irrelevant

assets.

Gearing- This ratio is showing an increasing trend as the long term liabilities and the

capital employed is been increasing over the years. This shows that the leverage position of the

company is not the efficient as its debts are increasing from one accounting period to another.

Interest coverage- Resulting a decline in the interest coverage ratio is also not a good

sign for Flashy products Ltd because it reflects that the income of the company is decreasing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

over its interest obligation is increasing (Uechi and et.al., 2015). This indicates that the leverage

position of the firm is not better.

Liquidity ratio- In the year 2009 and 2010, the liquidity position of Flashy products is

depicting an ideal results which means that company is effectively managing its current assets

and has the capability in meeting its short term liabilities. However, in the year 2011, its current

ratio is declining which affects the liquidity of the company.

ROE- Higher the return on equity ratio, better is the performance of the firm but the ROE

of Flashy products is reducing and reaching to negative results in the year 2011 (Yeh and et.al.,

2016). This clearly states that the net income of an organization is declining towards negative

outcome against the increase in the shareholders funds.

ROC- It is also decreasing over the years due to the decline in the operating profits as the

expenses are greater than revenue.

2. Assessment and the recommendations in respect of the financial performance of an entity

Overall the financial performance of Flashy product is not good because its net profits

and the operating profits are declining from one period to another. Its liquidity and the leverage

position is also not reflected as sound because its debts are increasing and its interest expenses

are also increasing with decrease in its earnings. Flashy products must take corrective measures

in order to improve its financial performance by eliminating the activities that are unprofitable,

looking for the new customers, reducing the expenses and the cost, reviewing the present pricing

structure and maintaining appropriate inventory for better working capital.

CONCLUSION

The report summarizes the various financial reports and their importance in company

decision making process. It can be concluded from that the evaluation of financial statement help

the organisation to manage the inventory, purchasing and credit. It also helps to minimize the

waste and maintain the performance of the firm. Different financial ratio such as liquidity ratio,

profitability, solvency etc. help the company to analyse the financial position. The growth in

sales, operating profit margin, ROE etc. are the reason behind the changing ratio.

position of the firm is not better.

Liquidity ratio- In the year 2009 and 2010, the liquidity position of Flashy products is

depicting an ideal results which means that company is effectively managing its current assets

and has the capability in meeting its short term liabilities. However, in the year 2011, its current

ratio is declining which affects the liquidity of the company.

ROE- Higher the return on equity ratio, better is the performance of the firm but the ROE

of Flashy products is reducing and reaching to negative results in the year 2011 (Yeh and et.al.,

2016). This clearly states that the net income of an organization is declining towards negative

outcome against the increase in the shareholders funds.

ROC- It is also decreasing over the years due to the decline in the operating profits as the

expenses are greater than revenue.

2. Assessment and the recommendations in respect of the financial performance of an entity

Overall the financial performance of Flashy product is not good because its net profits

and the operating profits are declining from one period to another. Its liquidity and the leverage

position is also not reflected as sound because its debts are increasing and its interest expenses

are also increasing with decrease in its earnings. Flashy products must take corrective measures

in order to improve its financial performance by eliminating the activities that are unprofitable,

looking for the new customers, reducing the expenses and the cost, reviewing the present pricing

structure and maintaining appropriate inventory for better working capital.

CONCLUSION

The report summarizes the various financial reports and their importance in company

decision making process. It can be concluded from that the evaluation of financial statement help

the organisation to manage the inventory, purchasing and credit. It also helps to minimize the

waste and maintain the performance of the firm. Different financial ratio such as liquidity ratio,

profitability, solvency etc. help the company to analyse the financial position. The growth in

sales, operating profit margin, ROE etc. are the reason behind the changing ratio.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Muhammad, H., Rehman, A.U. and Waqas, M., 2016. The relationship between working capital

management and profitability: A case study of tobacco industry of Pakistan. The

Journal of Asian Finance, Economics and Business (JAFEB), 3(2). pp.13-20.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and cash flow

liquidity in private equity. Journal of Financial Economics, 122(3). pp.521-543.

Choi, K.B. and et.al., 2018. Amplification ratio analysis of a bridge-type mechanical

amplification mechanism based on a fully compliant model. Mechanism and Machine

Theory. 121,. pp.355-372.

DeBord, J. and et.al., 2017. Profiling of heroin and assignment of provenance by 87Sr/86Sr

isotope ratio analysis. Inorganica Chimica Acta.468. pp.294-299.

Fallahpour, S., Lakvan, E. N. and Zadeh, M. H., 2017. Using an ensemble classifier based on

sequential floating forward selection for financial distress prediction problem. Journal of

Retailing and Consumer Services. 34. pp.159-167.

Loomes, R., Hull, L. and Mandy, W. P. L., 2017. What is the male-to-female ratio in autism

spectrum disorder? A systematic review and meta-analysis. Journal of the American

Academy of Child & Adolescent Psychiatry. 56(6). pp.466-474.

Uechi, L. and et.al., 2015. Sector dominance ratio analysis of financial markets. Physica A:

Statistical Mechanics and its Applications. 421. pp.488-509.

Yeh, C.C. and et.al., 2016. A hybrid detecting fraudulent financial statements model using rough

set theory and support vector machines. Cybernetics and Systems. 47(4). pp.261-276.

Books and journals

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Muhammad, H., Rehman, A.U. and Waqas, M., 2016. The relationship between working capital

management and profitability: A case study of tobacco industry of Pakistan. The

Journal of Asian Finance, Economics and Business (JAFEB), 3(2). pp.13-20.

Robinson, D.T. and Sensoy, B.A., 2016. Cyclicality, performance measurement, and cash flow

liquidity in private equity. Journal of Financial Economics, 122(3). pp.521-543.

Choi, K.B. and et.al., 2018. Amplification ratio analysis of a bridge-type mechanical

amplification mechanism based on a fully compliant model. Mechanism and Machine

Theory. 121,. pp.355-372.

DeBord, J. and et.al., 2017. Profiling of heroin and assignment of provenance by 87Sr/86Sr

isotope ratio analysis. Inorganica Chimica Acta.468. pp.294-299.

Fallahpour, S., Lakvan, E. N. and Zadeh, M. H., 2017. Using an ensemble classifier based on

sequential floating forward selection for financial distress prediction problem. Journal of

Retailing and Consumer Services. 34. pp.159-167.

Loomes, R., Hull, L. and Mandy, W. P. L., 2017. What is the male-to-female ratio in autism

spectrum disorder? A systematic review and meta-analysis. Journal of the American

Academy of Child & Adolescent Psychiatry. 56(6). pp.466-474.

Uechi, L. and et.al., 2015. Sector dominance ratio analysis of financial markets. Physica A:

Statistical Mechanics and its Applications. 421. pp.488-509.

Yeh, C.C. and et.al., 2016. A hybrid detecting fraudulent financial statements model using rough

set theory and support vector machines. Cybernetics and Systems. 47(4). pp.261-276.

Online

Cash Flows from Operating Activities. 2019. [online]. Available through

:<http://news.morningstar.com/classroom2/course.asp?

docId=145092&page=3&CN=COM>.

Are a Firm's Cash Flow and Profit Different. 2019. [online]. Available through

:<https://www.thebalancesmb.com/are-a-firm-s-cash-flow-and-profit-different-393585>.

Working capital finance. 2019. [online]. Available through

:<https://www.fundingoptions.com/knowledge/working-capital-finance/>.

Cash Flows from Operating Activities. 2019. [online]. Available through

:<http://news.morningstar.com/classroom2/course.asp?

docId=145092&page=3&CN=COM>.

Are a Firm's Cash Flow and Profit Different. 2019. [online]. Available through

:<https://www.thebalancesmb.com/are-a-firm-s-cash-flow-and-profit-different-393585>.

Working capital finance. 2019. [online]. Available through

:<https://www.fundingoptions.com/knowledge/working-capital-finance/>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.