Business Finance Report: Budgeting and Financial Analysis

VerifiedAdded on 2020/10/04

|14

|3256

|143

Report

AI Summary

This report provides a comprehensive analysis of business finance, focusing on budgeting and its role in developing a business model. It examines the purpose of budgeting, its process, and how it aids in decision-making, forecasting, and performance monitoring, using Snappy Drinks Plc as a case study. The report delves into traditional budgeting approaches, including incremental budgeting, and assesses their appropriateness for different organizational departments. Furthermore, it explores various budgeting methods like rolling budgets and analyzes their application, advantages, and suitability for the company. The report also covers the importance of strategic planning, revenue projections, and cost management, providing a detailed understanding of financial planning within a business context.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

..........................................................................................................................................................3

EXECUTIVE SUMMARY.............................................................................................................4

PART 1 ...........................................................................................................................................4

. Purpose of preparing budget, its process and how it helps in the development of business

model...........................................................................................................................................4

. Application of traditional budgeting approaches for planning future cost management..........7

. Analysing whether traditional budgetary system is appropriate to all or any part of

organisation's future plan ...........................................................................................................8

PART 2............................................................................................................................................9

.V Different types of budget methods.........................................................................................9

.V Application of these methods to the company through specific examples..........................10

.VI Analysing the methods which is best suited to the organisation........................................14

CONCLUSION..............................................................................................................................14

REFERENCES\.............................................................................................................................15

..........................................................................................................................................................3

EXECUTIVE SUMMARY.............................................................................................................4

PART 1 ...........................................................................................................................................4

. Purpose of preparing budget, its process and how it helps in the development of business

model...........................................................................................................................................4

. Application of traditional budgeting approaches for planning future cost management..........7

. Analysing whether traditional budgetary system is appropriate to all or any part of

organisation's future plan ...........................................................................................................8

PART 2............................................................................................................................................9

.V Different types of budget methods.........................................................................................9

.V Application of these methods to the company through specific examples..........................10

.VI Analysing the methods which is best suited to the organisation........................................14

CONCLUSION..............................................................................................................................14

REFERENCES\.............................................................................................................................15

EXECUTIVE SUMMARY

Business finance can be defined as the money and credit which is employed in the

business. It basically involves acquisition of funds and utilising those funds in the most

productive way. The various activities are related with the business finance such as allocating the

resources, preparing forecasts and continuously reviewing the opportunities for debt and equity

financing. The present report is going to discuss about Snappy Drinks Plc, an energy drink

manufacturing company situated at Nottingham. It is listed on LSE. The report will highlight the

concept of budget, why it is prepared and its process. Further, different types of budgeting

methods will be analysed in the project report.

PART 1

Purpose of preparing budget, its process and how it helps in the development of business model

Budget in the simpler terms, means a short term plan that states out the expenditure that

will be incurred by the organisation. Preparing budgets is necessary for the Snappy Drinks

because of the following reasons:

It forecasts the income and expenditure of organisation: Budgeting is said to be one of

the crucial part of business planning process. Managers continuously put their efforts in

predicting whether the expenses that are incurred could be recovered by the income generated by

incurring them. This is done by the way of preparing budgets.

It helps in decision making: Another purpose of preparing budget is to render a financial

framework that leads to better decision making. For example, when budgets are prepared by

Snappy Drinks, it knows where its money is used and how productively it is used. Also,

preparing budget leads to tight control on the expenses of the company that again leads to

attainment of company's objective of being cost effective organisation.

Monitors and review business performance: The basic objective of budget is to find the

deviation between the actual performance and standard performance of Snappy Drinks by

comparing them against each other. This results in taking corrective actions that eventually leads

to better business performance of the company (Miller, 2018.).

Business finance can be defined as the money and credit which is employed in the

business. It basically involves acquisition of funds and utilising those funds in the most

productive way. The various activities are related with the business finance such as allocating the

resources, preparing forecasts and continuously reviewing the opportunities for debt and equity

financing. The present report is going to discuss about Snappy Drinks Plc, an energy drink

manufacturing company situated at Nottingham. It is listed on LSE. The report will highlight the

concept of budget, why it is prepared and its process. Further, different types of budgeting

methods will be analysed in the project report.

PART 1

Purpose of preparing budget, its process and how it helps in the development of business model

Budget in the simpler terms, means a short term plan that states out the expenditure that

will be incurred by the organisation. Preparing budgets is necessary for the Snappy Drinks

because of the following reasons:

It forecasts the income and expenditure of organisation: Budgeting is said to be one of

the crucial part of business planning process. Managers continuously put their efforts in

predicting whether the expenses that are incurred could be recovered by the income generated by

incurring them. This is done by the way of preparing budgets.

It helps in decision making: Another purpose of preparing budget is to render a financial

framework that leads to better decision making. For example, when budgets are prepared by

Snappy Drinks, it knows where its money is used and how productively it is used. Also,

preparing budget leads to tight control on the expenses of the company that again leads to

attainment of company's objective of being cost effective organisation.

Monitors and review business performance: The basic objective of budget is to find the

deviation between the actual performance and standard performance of Snappy Drinks by

comparing them against each other. This results in taking corrective actions that eventually leads

to better business performance of the company (Miller, 2018.).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Process of budgeting: The process of budgeting which Snappy Drinks could follow is

described below:

Strategic planning process: The very step in the preparation of budget is writing down

the things Snappy Drinks wants. Every company comes into existence for a specific

purpose that it desires to fulfil. Thus, this is done by witting down the mission and vision

of the company that continuously guides them it has to achieve its objectives and goals

for which it has been formed.

The budgeting process involves strategic planning to ensure that organisation uses its

resources in the most optimum way for supporting the strategic goals of the company and paves

the way for its development. This means that budgeting moves towards vision. Goals of business: There are certain business goals which the Snappy Drinks wishes to

achieve for implementing its strategic plan. It is these goals which are funded by budget

or it can be said that the expenses are forecasted in the form of budget that helps in

fulfilling those goals. It is mainly the responsibility of management team of entity.

Projections of revenue: The next step in budgeting process is to project or estimate the

income that will be generated by incurring the expenses for meeting the business goals,

For instance, for meeting the goal of increasing the sales of Snappy Drinks by 2%,

income that would be generated is projected for the year concerned (Dudin and et.al.,2015). Projection of fixed cost: Preparing budget involves estimating the expenses that will not

change due to any reason. Examples are employees' salary, interest expenses, rent, utility

expenses etc. Projection of variable cost: Budget also include variable cost that fluctuates with time or

other factor. These expenses should be controlled by management of Snappy Drinks by

the way of budgets. Annual goal expenses: Budgets should be prepared I such a way that helps in

accomplishing goals. Each initiative must have estimation of cost that is related to a

annual specific goal. Thus, it is place where annual goals or targets are integrated in

departmental budgets.

described below:

Strategic planning process: The very step in the preparation of budget is writing down

the things Snappy Drinks wants. Every company comes into existence for a specific

purpose that it desires to fulfil. Thus, this is done by witting down the mission and vision

of the company that continuously guides them it has to achieve its objectives and goals

for which it has been formed.

The budgeting process involves strategic planning to ensure that organisation uses its

resources in the most optimum way for supporting the strategic goals of the company and paves

the way for its development. This means that budgeting moves towards vision. Goals of business: There are certain business goals which the Snappy Drinks wishes to

achieve for implementing its strategic plan. It is these goals which are funded by budget

or it can be said that the expenses are forecasted in the form of budget that helps in

fulfilling those goals. It is mainly the responsibility of management team of entity.

Projections of revenue: The next step in budgeting process is to project or estimate the

income that will be generated by incurring the expenses for meeting the business goals,

For instance, for meeting the goal of increasing the sales of Snappy Drinks by 2%,

income that would be generated is projected for the year concerned (Dudin and et.al.,2015). Projection of fixed cost: Preparing budget involves estimating the expenses that will not

change due to any reason. Examples are employees' salary, interest expenses, rent, utility

expenses etc. Projection of variable cost: Budget also include variable cost that fluctuates with time or

other factor. These expenses should be controlled by management of Snappy Drinks by

the way of budgets. Annual goal expenses: Budgets should be prepared I such a way that helps in

accomplishing goals. Each initiative must have estimation of cost that is related to a

annual specific goal. Thus, it is place where annual goals or targets are integrated in

departmental budgets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Targeting profit margin: Every company wants to earn profit by undertaking business

activity. Profits are crucial because this shows the financial soundness of the company in

the market. Approval of board: Budgets have to approved by the board or any concerned authority

for putting the budget into effect. Reviewing budget: Prepared budgets shall be reviewed by the management monthly for

maintaining its effectiveness and to make sure that it does not deviate from its track.

Handling the variations: When the actual performance deviates from the standard

performance, variation is said to have occurred. These variances should be reviewed by

the concerned manager and shall look into the reasons that created variances (Popesko

and et.al., 2015).

Budget process helps in the development of business model of Snappy Drinks in the

following manner:

A business model is a plan that lays out the operations of company will be carried out

along with identification of sources of revenues, target customer base and intense finance

detailing. Innovation and differentiation process of company: Snappy Drinks is intending to

launch healthy drinks with low sugar content in its product line. Preparing budgets will

help the managers in estimating the total expenditure that would be incurred for

launching new product. Marketing campaign planning: The business model involves detailed structure of how

company will generate its profits. In it, it also includes planning of marketing campaign

that rolls out the structure regarding how the new product is to be marketed in the target

market. Process of budgeting will help in determining the cost of marketing the products.

Business expansion: Snappy Drinks is intending to expand its business in the Gulf

countries, Asian countries etc. This requires the management to draw a proper strategic

plan where the cost and benefits of the expansion plan will be evaluated and analysed.

Such a forecast will throw light on the viability of expansion proposal of the enterprise

(Argenti, 2018).

activity. Profits are crucial because this shows the financial soundness of the company in

the market. Approval of board: Budgets have to approved by the board or any concerned authority

for putting the budget into effect. Reviewing budget: Prepared budgets shall be reviewed by the management monthly for

maintaining its effectiveness and to make sure that it does not deviate from its track.

Handling the variations: When the actual performance deviates from the standard

performance, variation is said to have occurred. These variances should be reviewed by

the concerned manager and shall look into the reasons that created variances (Popesko

and et.al., 2015).

Budget process helps in the development of business model of Snappy Drinks in the

following manner:

A business model is a plan that lays out the operations of company will be carried out

along with identification of sources of revenues, target customer base and intense finance

detailing. Innovation and differentiation process of company: Snappy Drinks is intending to

launch healthy drinks with low sugar content in its product line. Preparing budgets will

help the managers in estimating the total expenditure that would be incurred for

launching new product. Marketing campaign planning: The business model involves detailed structure of how

company will generate its profits. In it, it also includes planning of marketing campaign

that rolls out the structure regarding how the new product is to be marketed in the target

market. Process of budgeting will help in determining the cost of marketing the products.

Business expansion: Snappy Drinks is intending to expand its business in the Gulf

countries, Asian countries etc. This requires the management to draw a proper strategic

plan where the cost and benefits of the expansion plan will be evaluated and analysed.

Such a forecast will throw light on the viability of expansion proposal of the enterprise

(Argenti, 2018).

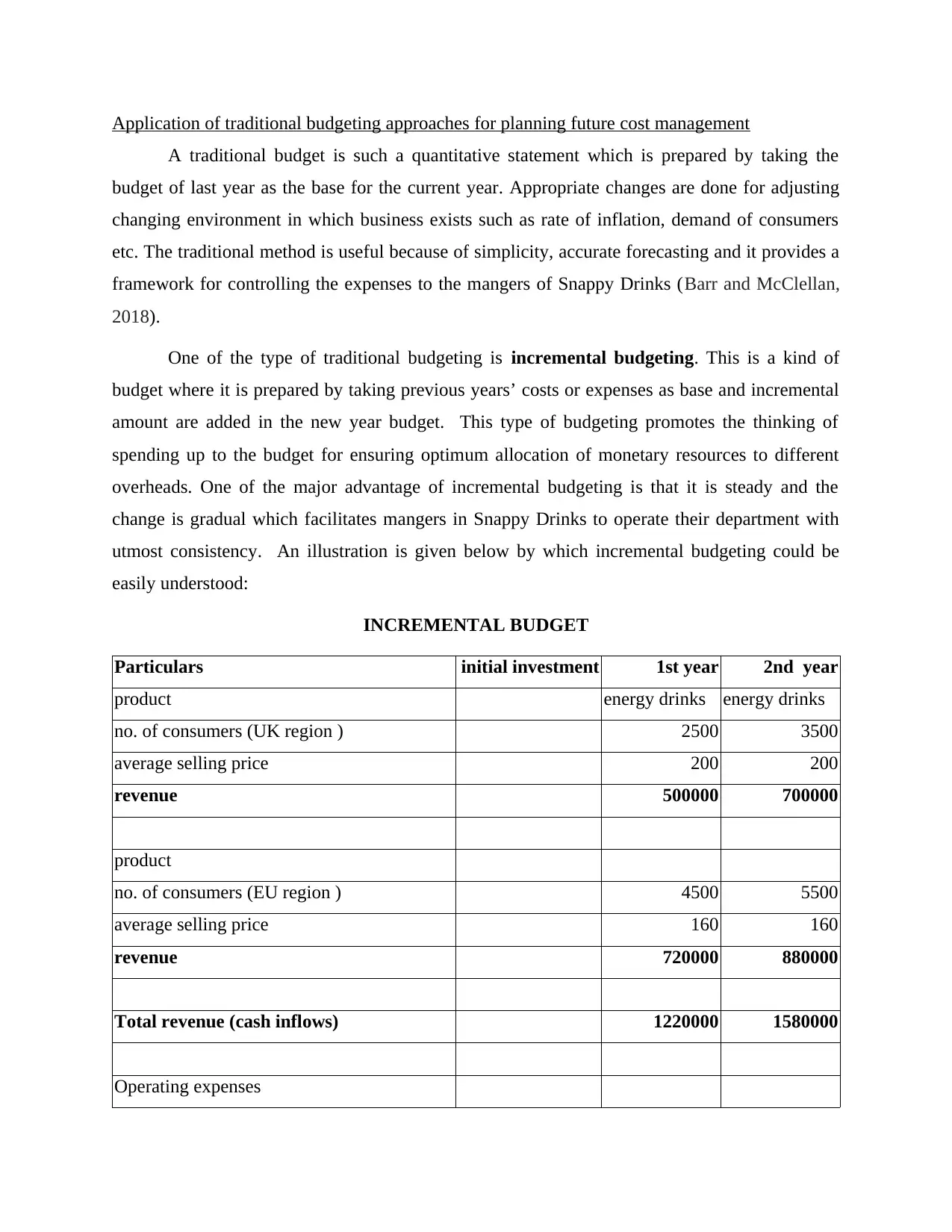

Application of traditional budgeting approaches for planning future cost management

A traditional budget is such a quantitative statement which is prepared by taking the

budget of last year as the base for the current year. Appropriate changes are done for adjusting

changing environment in which business exists such as rate of inflation, demand of consumers

etc. The traditional method is useful because of simplicity, accurate forecasting and it provides a

framework for controlling the expenses to the mangers of Snappy Drinks (Barr and McClellan,

2018).

One of the type of traditional budgeting is incremental budgeting. This is a kind of

budget where it is prepared by taking previous years’ costs or expenses as base and incremental

amount are added in the new year budget. This type of budgeting promotes the thinking of

spending up to the budget for ensuring optimum allocation of monetary resources to different

overheads. One of the major advantage of incremental budgeting is that it is steady and the

change is gradual which facilitates mangers in Snappy Drinks to operate their department with

utmost consistency. An illustration is given below by which incremental budgeting could be

easily understood:

INCREMENTAL BUDGET

Particulars initial investment 1st year 2nd year

product energy drinks energy drinks

no. of consumers (UK region ) 2500 3500

average selling price 200 200

revenue 500000 700000

product

no. of consumers (EU region ) 4500 5500

average selling price 160 160

revenue 720000 880000

Total revenue (cash inflows) 1220000 1580000

Operating expenses

A traditional budget is such a quantitative statement which is prepared by taking the

budget of last year as the base for the current year. Appropriate changes are done for adjusting

changing environment in which business exists such as rate of inflation, demand of consumers

etc. The traditional method is useful because of simplicity, accurate forecasting and it provides a

framework for controlling the expenses to the mangers of Snappy Drinks (Barr and McClellan,

2018).

One of the type of traditional budgeting is incremental budgeting. This is a kind of

budget where it is prepared by taking previous years’ costs or expenses as base and incremental

amount are added in the new year budget. This type of budgeting promotes the thinking of

spending up to the budget for ensuring optimum allocation of monetary resources to different

overheads. One of the major advantage of incremental budgeting is that it is steady and the

change is gradual which facilitates mangers in Snappy Drinks to operate their department with

utmost consistency. An illustration is given below by which incremental budgeting could be

easily understood:

INCREMENTAL BUDGET

Particulars initial investment 1st year 2nd year

product energy drinks energy drinks

no. of consumers (UK region ) 2500 3500

average selling price 200 200

revenue 500000 700000

product

no. of consumers (EU region ) 4500 5500

average selling price 160 160

revenue 720000 880000

Total revenue (cash inflows) 1220000 1580000

Operating expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

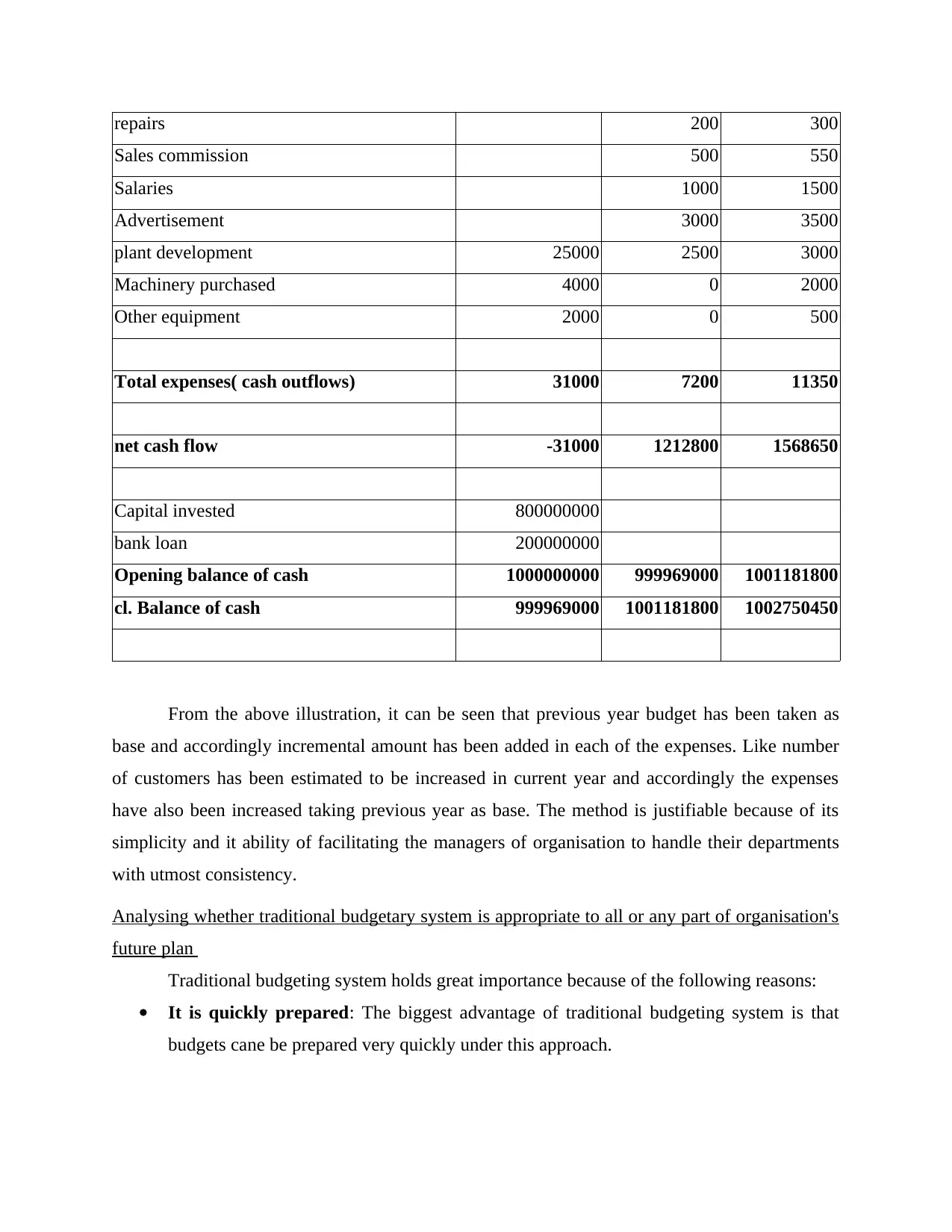

repairs 200 300

Sales commission 500 550

Salaries 1000 1500

Advertisement 3000 3500

plant development 25000 2500 3000

Machinery purchased 4000 0 2000

Other equipment 2000 0 500

Total expenses( cash outflows) 31000 7200 11350

net cash flow -31000 1212800 1568650

Capital invested 800000000

bank loan 200000000

Opening balance of cash 1000000000 999969000 1001181800

cl. Balance of cash 999969000 1001181800 1002750450

From the above illustration, it can be seen that previous year budget has been taken as

base and accordingly incremental amount has been added in each of the expenses. Like number

of customers has been estimated to be increased in current year and accordingly the expenses

have also been increased taking previous year as base. The method is justifiable because of its

simplicity and it ability of facilitating the managers of organisation to handle their departments

with utmost consistency.

Analysing whether traditional budgetary system is appropriate to all or any part of organisation's

future plan

Traditional budgeting system holds great importance because of the following reasons:

It is quickly prepared: The biggest advantage of traditional budgeting system is that

budgets cane be prepared very quickly under this approach.

Sales commission 500 550

Salaries 1000 1500

Advertisement 3000 3500

plant development 25000 2500 3000

Machinery purchased 4000 0 2000

Other equipment 2000 0 500

Total expenses( cash outflows) 31000 7200 11350

net cash flow -31000 1212800 1568650

Capital invested 800000000

bank loan 200000000

Opening balance of cash 1000000000 999969000 1001181800

cl. Balance of cash 999969000 1001181800 1002750450

From the above illustration, it can be seen that previous year budget has been taken as

base and accordingly incremental amount has been added in each of the expenses. Like number

of customers has been estimated to be increased in current year and accordingly the expenses

have also been increased taking previous year as base. The method is justifiable because of its

simplicity and it ability of facilitating the managers of organisation to handle their departments

with utmost consistency.

Analysing whether traditional budgetary system is appropriate to all or any part of organisation's

future plan

Traditional budgeting system holds great importance because of the following reasons:

It is quickly prepared: The biggest advantage of traditional budgeting system is that

budgets cane be prepared very quickly under this approach.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Simpler method: Its importance lies in the fact that it is simple in nature and rules out

the possibility of complications in drawing out a budget. This leads to better and more

accurate forecasting of the expenses and revenue.

It facilitates a framework for control: It leads to better control of the business activities

as deviation is found out by comparing the actual expenses with estimated costs and the

reasons for such variance is found out by managers and are minutely analysed by them.

This lead to better control over the activities of an organisation (Rogulenko and et.al.,

2016).

Appropriateness of traditional system in Snappy Drinks company

Operations department: The traditional budgeting system could be effectively used by

Snappy Drinks. The managers can use previous year's data and can accordingly prepare their

current year budget with the incremental amount. This will help them in estimating the cost more

accurately by taking into factors such as inflation, market demand etc., into consideration.

Marketing department: The marketing department of Snappy Drinks Plc could use

traditional budgeting system as it can take the budget of last year and make new one by making

some adjustments. For example, cost of promotional activities, marketing campaigns etc., of the

current year could be determined by analysing the expenses incurred in the last year.

Finance department: It is one of the most useful technique which could be efficiently

used by finance department of company to prepare the finance budget that shows how assets are

managed, cash flow, income and expenditures takes place in the organisation. Finance manager

can use previous year budget for estimating the revenue and profits for the next year (Mahal and

Hossain, 2015).

PART 2

Different types of budget methods

There are different types of budget methods which are discussed below:

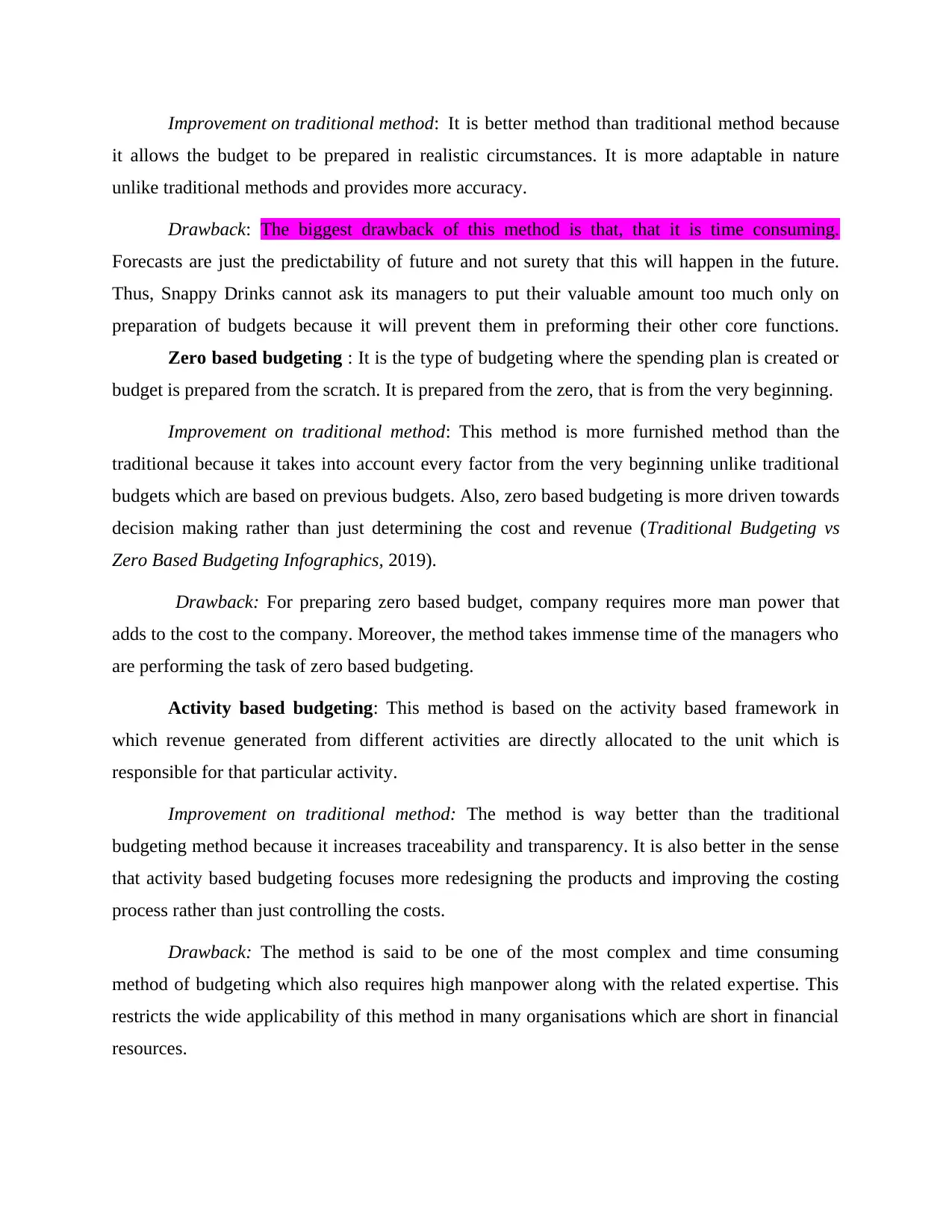

Rolling budget method: In this type of budgeting system, a budget is prepared in the

beginning of the accounting period and is continually monitored and amended for reflecting the

deviation that occurred because of different changing circumstances. Rolling budgets would

allow the Snappy Drinks to forecast the future with more reliability as the budget is based o

updated revenue and expense or actual results (Mahieu, Vroman and Calluy, 2015).

the possibility of complications in drawing out a budget. This leads to better and more

accurate forecasting of the expenses and revenue.

It facilitates a framework for control: It leads to better control of the business activities

as deviation is found out by comparing the actual expenses with estimated costs and the

reasons for such variance is found out by managers and are minutely analysed by them.

This lead to better control over the activities of an organisation (Rogulenko and et.al.,

2016).

Appropriateness of traditional system in Snappy Drinks company

Operations department: The traditional budgeting system could be effectively used by

Snappy Drinks. The managers can use previous year's data and can accordingly prepare their

current year budget with the incremental amount. This will help them in estimating the cost more

accurately by taking into factors such as inflation, market demand etc., into consideration.

Marketing department: The marketing department of Snappy Drinks Plc could use

traditional budgeting system as it can take the budget of last year and make new one by making

some adjustments. For example, cost of promotional activities, marketing campaigns etc., of the

current year could be determined by analysing the expenses incurred in the last year.

Finance department: It is one of the most useful technique which could be efficiently

used by finance department of company to prepare the finance budget that shows how assets are

managed, cash flow, income and expenditures takes place in the organisation. Finance manager

can use previous year budget for estimating the revenue and profits for the next year (Mahal and

Hossain, 2015).

PART 2

Different types of budget methods

There are different types of budget methods which are discussed below:

Rolling budget method: In this type of budgeting system, a budget is prepared in the

beginning of the accounting period and is continually monitored and amended for reflecting the

deviation that occurred because of different changing circumstances. Rolling budgets would

allow the Snappy Drinks to forecast the future with more reliability as the budget is based o

updated revenue and expense or actual results (Mahieu, Vroman and Calluy, 2015).

Improvement on traditional method: It is better method than traditional method because

it allows the budget to be prepared in realistic circumstances. It is more adaptable in nature

unlike traditional methods and provides more accuracy.

Drawback: The biggest drawback of this method is that, that it is time consuming.

Forecasts are just the predictability of future and not surety that this will happen in the future.

Thus, Snappy Drinks cannot ask its managers to put their valuable amount too much only on

preparation of budgets because it will prevent them in preforming their other core functions.

Zero based budgeting : It is the type of budgeting where the spending plan is created or

budget is prepared from the scratch. It is prepared from the zero, that is from the very beginning.

Improvement on traditional method: This method is more furnished method than the

traditional because it takes into account every factor from the very beginning unlike traditional

budgets which are based on previous budgets. Also, zero based budgeting is more driven towards

decision making rather than just determining the cost and revenue (Traditional Budgeting vs

Zero Based Budgeting Infographics, 2019).

Drawback: For preparing zero based budget, company requires more man power that

adds to the cost to the company. Moreover, the method takes immense time of the managers who

are performing the task of zero based budgeting.

Activity based budgeting: This method is based on the activity based framework in

which revenue generated from different activities are directly allocated to the unit which is

responsible for that particular activity.

Improvement on traditional method: The method is way better than the traditional

budgeting method because it increases traceability and transparency. It is also better in the sense

that activity based budgeting focuses more redesigning the products and improving the costing

process rather than just controlling the costs.

Drawback: The method is said to be one of the most complex and time consuming

method of budgeting which also requires high manpower along with the related expertise. This

restricts the wide applicability of this method in many organisations which are short in financial

resources.

it allows the budget to be prepared in realistic circumstances. It is more adaptable in nature

unlike traditional methods and provides more accuracy.

Drawback: The biggest drawback of this method is that, that it is time consuming.

Forecasts are just the predictability of future and not surety that this will happen in the future.

Thus, Snappy Drinks cannot ask its managers to put their valuable amount too much only on

preparation of budgets because it will prevent them in preforming their other core functions.

Zero based budgeting : It is the type of budgeting where the spending plan is created or

budget is prepared from the scratch. It is prepared from the zero, that is from the very beginning.

Improvement on traditional method: This method is more furnished method than the

traditional because it takes into account every factor from the very beginning unlike traditional

budgets which are based on previous budgets. Also, zero based budgeting is more driven towards

decision making rather than just determining the cost and revenue (Traditional Budgeting vs

Zero Based Budgeting Infographics, 2019).

Drawback: For preparing zero based budget, company requires more man power that

adds to the cost to the company. Moreover, the method takes immense time of the managers who

are performing the task of zero based budgeting.

Activity based budgeting: This method is based on the activity based framework in

which revenue generated from different activities are directly allocated to the unit which is

responsible for that particular activity.

Improvement on traditional method: The method is way better than the traditional

budgeting method because it increases traceability and transparency. It is also better in the sense

that activity based budgeting focuses more redesigning the products and improving the costing

process rather than just controlling the costs.

Drawback: The method is said to be one of the most complex and time consuming

method of budgeting which also requires high manpower along with the related expertise. This

restricts the wide applicability of this method in many organisations which are short in financial

resources.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Application of these methods to the company through specific examples

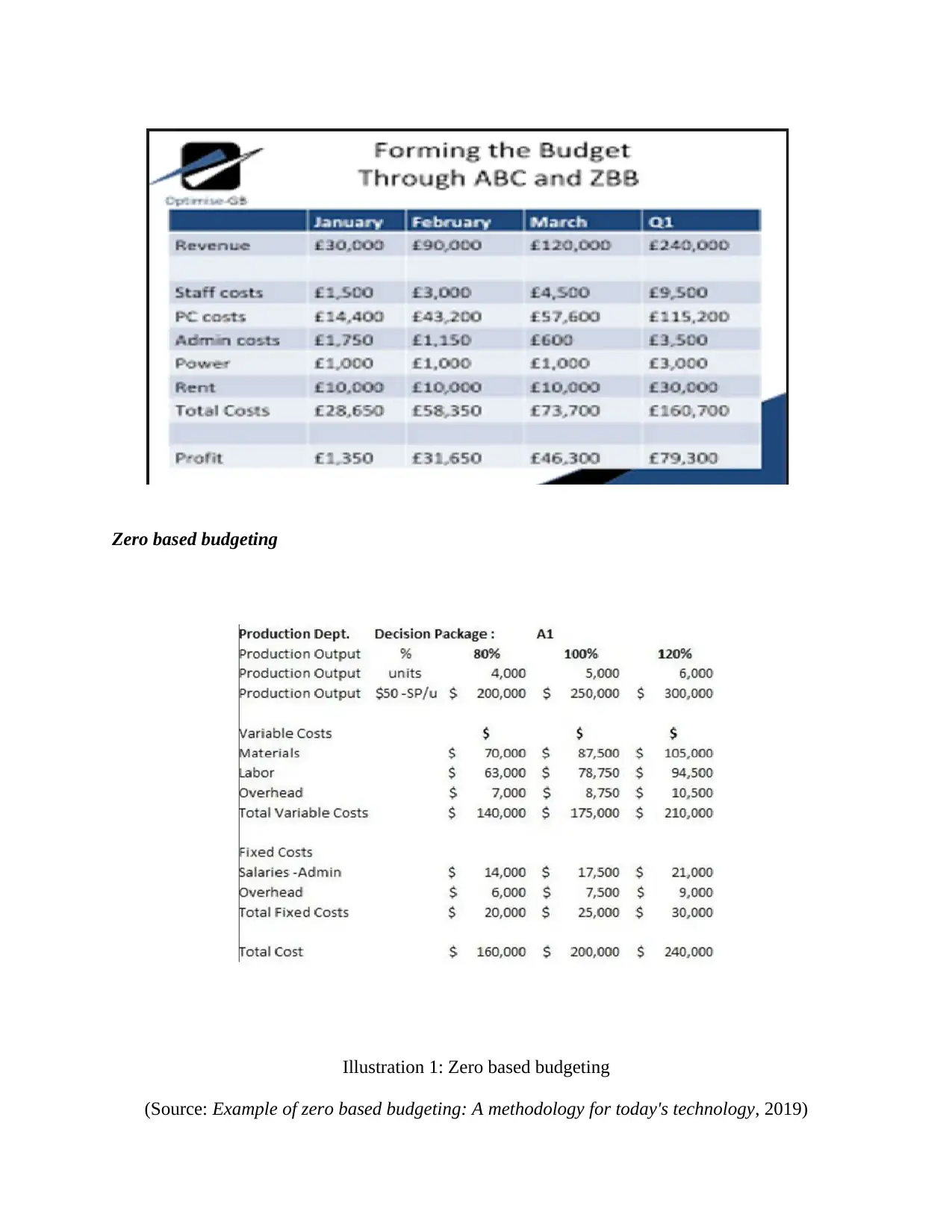

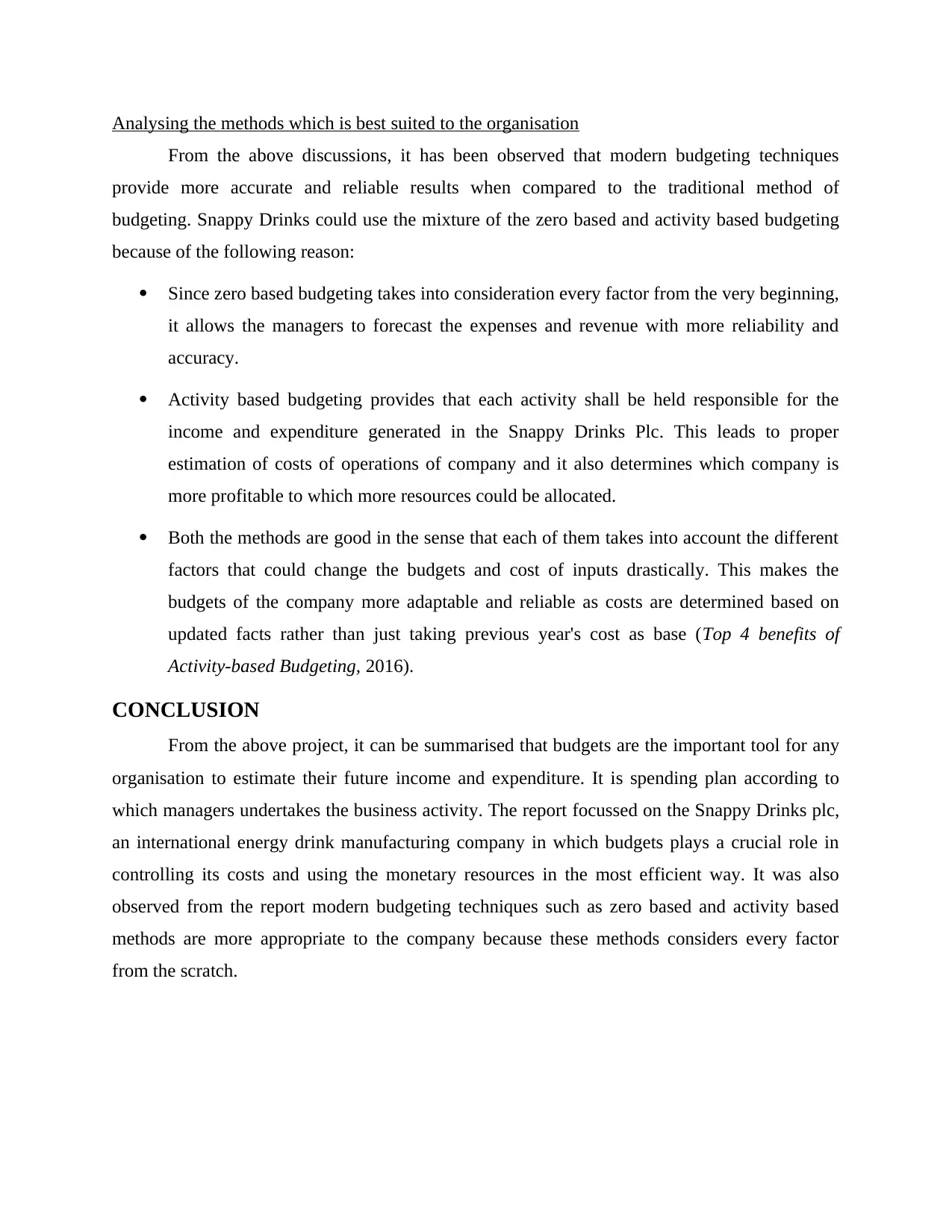

An illustration of rolling out budget:

An illustration of zero based and activity based budget:

An illustration of rolling out budget:

An illustration of zero based and activity based budget:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero based budgeting

Illustration 1: Zero based budgeting

(Source: Example of zero based budgeting: A methodology for today's technology, 2019)

Illustration 1: Zero based budgeting

(Source: Example of zero based budgeting: A methodology for today's technology, 2019)

Analysing the methods which is best suited to the organisation

From the above discussions, it has been observed that modern budgeting techniques

provide more accurate and reliable results when compared to the traditional method of

budgeting. Snappy Drinks could use the mixture of the zero based and activity based budgeting

because of the following reason:

Since zero based budgeting takes into consideration every factor from the very beginning,

it allows the managers to forecast the expenses and revenue with more reliability and

accuracy.

Activity based budgeting provides that each activity shall be held responsible for the

income and expenditure generated in the Snappy Drinks Plc. This leads to proper

estimation of costs of operations of company and it also determines which company is

more profitable to which more resources could be allocated.

Both the methods are good in the sense that each of them takes into account the different

factors that could change the budgets and cost of inputs drastically. This makes the

budgets of the company more adaptable and reliable as costs are determined based on

updated facts rather than just taking previous year's cost as base (Top 4 benefits of

Activity-based Budgeting, 2016).

CONCLUSION

From the above project, it can be summarised that budgets are the important tool for any

organisation to estimate their future income and expenditure. It is spending plan according to

which managers undertakes the business activity. The report focussed on the Snappy Drinks plc,

an international energy drink manufacturing company in which budgets plays a crucial role in

controlling its costs and using the monetary resources in the most efficient way. It was also

observed from the report modern budgeting techniques such as zero based and activity based

methods are more appropriate to the company because these methods considers every factor

from the scratch.

From the above discussions, it has been observed that modern budgeting techniques

provide more accurate and reliable results when compared to the traditional method of

budgeting. Snappy Drinks could use the mixture of the zero based and activity based budgeting

because of the following reason:

Since zero based budgeting takes into consideration every factor from the very beginning,

it allows the managers to forecast the expenses and revenue with more reliability and

accuracy.

Activity based budgeting provides that each activity shall be held responsible for the

income and expenditure generated in the Snappy Drinks Plc. This leads to proper

estimation of costs of operations of company and it also determines which company is

more profitable to which more resources could be allocated.

Both the methods are good in the sense that each of them takes into account the different

factors that could change the budgets and cost of inputs drastically. This makes the

budgets of the company more adaptable and reliable as costs are determined based on

updated facts rather than just taking previous year's cost as base (Top 4 benefits of

Activity-based Budgeting, 2016).

CONCLUSION

From the above project, it can be summarised that budgets are the important tool for any

organisation to estimate their future income and expenditure. It is spending plan according to

which managers undertakes the business activity. The report focussed on the Snappy Drinks plc,

an international energy drink manufacturing company in which budgets plays a crucial role in

controlling its costs and using the monetary resources in the most efficient way. It was also

observed from the report modern budgeting techniques such as zero based and activity based

methods are more appropriate to the company because these methods considers every factor

from the scratch.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.