Business Finance Report: Financial Analysis for Root and Cook Ltd

VerifiedAdded on 2020/06/03

|15

|3671

|215

Report

AI Summary

This report provides a comprehensive analysis of business finance, focusing on the financial performance of Root and Cook Ltd. It begins by defining key financial terms like profit, cash flow, and working capital, highlighting their differences and impacts. The report then delves into the financial position of the company by examining its cash flow statement, income statement, and balance sheet from 2016 to 2020. Based on the financial outcomes, the report recommends steps to control cash flow through effective working capital management, including improvements in debtor collection, creditor payments, supplier negotiations, expense reduction, and tax opportunity review. Furthermore, the report evaluates capital budgeting processes and investment appraisal methods, discussing their advantages and disadvantages to aid in strategic financial decision-making. The analysis provides recommendations for professionals involved in project evaluation and expansion.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

1. Explaining various terms.........................................................................................................3

2. Determining the financial position of the business as per the outcomes of various financial

results..........................................................................................................................................4

3. Recommending the steps to control the cash flow through working capital management.....8

PART 2............................................................................................................................................8

1. Evaluating the terms................................................................................................................8

2. Illustrating the various terms of investment operations........................................................11

3. Recommending the professionals to pursue the project........................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

1. Explaining various terms.........................................................................................................3

2. Determining the financial position of the business as per the outcomes of various financial

results..........................................................................................................................................4

3. Recommending the steps to control the cash flow through working capital management.....8

PART 2............................................................................................................................................8

1. Evaluating the terms................................................................................................................8

2. Illustrating the various terms of investment operations........................................................11

3. Recommending the professionals to pursue the project........................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

To make the strategic decisions in terms with designing the operational activities of the

business there is need to have better financial management. It determines the financial statements

of the business which will be helpful for execution of operations and profits. In the present report

there will be study over the various financial terms such as profit, cash flow and working

statement on which Root and Cook Ltd. The report is also consists of outcomes of the investment

appraisals which are helping in having the appropriate information regarding the profitability of

the proposed project. Therefore, in relation with such measurements the professionals will have

sufficient details regarding the expansion of business operations.

PART 1

1. Explaining various terms

a. Analysing the profit and cash flow and determining the differences among them

The terms profit and cash flow are different from each other in accordance with analysing

the financial health of the business. However, in accordance with the business requirements there

is need to manage the cash flows and various transactions of the business which in turn will be

helpful to the entity to have profitable growth.

Profit: It is a surplus amount which will be helpful to the business in terms of analysing

the expenses and gains over the operational made by them. Thus, with the help of such amount

the business will become able to perform the operational activities (Campbell, 2017). Purchase

raw material, pay salaries to the employees, dividend payments to the shareholders as well as it

can plan for the expansion of the business criteria.

Cash flow: The inflows and outflows of the cash balance in the business which will be

helpful in analysing the liquidity. However, the level of cash balance determine the ability of the

entity in meeting the expenses as well as making the adequate payments to the operations

(Kumar, Sivashanmugam and Vennela, 2018). It ascertains the requirement of the cash has been

met and analysed by the business professionals.

Determining the difference between profit and cash flow:

Profit Cash flow

To make the strategic decisions in terms with designing the operational activities of the

business there is need to have better financial management. It determines the financial statements

of the business which will be helpful for execution of operations and profits. In the present report

there will be study over the various financial terms such as profit, cash flow and working

statement on which Root and Cook Ltd. The report is also consists of outcomes of the investment

appraisals which are helping in having the appropriate information regarding the profitability of

the proposed project. Therefore, in relation with such measurements the professionals will have

sufficient details regarding the expansion of business operations.

PART 1

1. Explaining various terms

a. Analysing the profit and cash flow and determining the differences among them

The terms profit and cash flow are different from each other in accordance with analysing

the financial health of the business. However, in accordance with the business requirements there

is need to manage the cash flows and various transactions of the business which in turn will be

helpful to the entity to have profitable growth.

Profit: It is a surplus amount which will be helpful to the business in terms of analysing

the expenses and gains over the operational made by them. Thus, with the help of such amount

the business will become able to perform the operational activities (Campbell, 2017). Purchase

raw material, pay salaries to the employees, dividend payments to the shareholders as well as it

can plan for the expansion of the business criteria.

Cash flow: The inflows and outflows of the cash balance in the business which will be

helpful in analysing the liquidity. However, the level of cash balance determine the ability of the

entity in meeting the expenses as well as making the adequate payments to the operations

(Kumar, Sivashanmugam and Vennela, 2018). It ascertains the requirement of the cash has been

met and analysed by the business professionals.

Determining the difference between profit and cash flow:

Profit Cash flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is the method of analysing the

surplus amount over all the income and

expenditures made by the business in a

financial year. These are the amount on

which the firm will make payments to

the shareholder's dividends, operational

investment as well as make payments

of the taxes.

The determination of the daily tasks and

operations of the business which in turn

helps in analysing the inflows and

outflows of the total cash (Young and

Pagliari, 2017). However, it helps in

managing the daily financial activities

such as taxation, purchase of

inventories, employee salaries as well

as paying off the costs incurred in

various operations.

b. Ascertaining the concept of working capital:

This is the technique which helps in determining the efficiency of the business in day to

day operations. This ascertains the ability of the firm in meeting the short terms requirements

such as analysing the current liabilities and current assets of the firm (Block and et.al., 2018). It

facilitates the information to the professionals that the firm is having enough short term assets

which will be helpful in meeting to pay off the short term debts.

c. Analysing the impacts of working capital over cash flow

2. Determining the financial position of the business as per the outcomes of various financial

results

To ascertains the appropriate financial health of the entity there are analysis of the 5 years

financials which will be helpful in suggesting the adequate changes in the operations of Root and

Cook Ltd. Thus, there are analysis of cash flow statement, income statement and balance sheet of

the entity which will indicate the operational transactions held during the period and which will

be beneficial in ascertaining the liquidity and efficiency of the business.

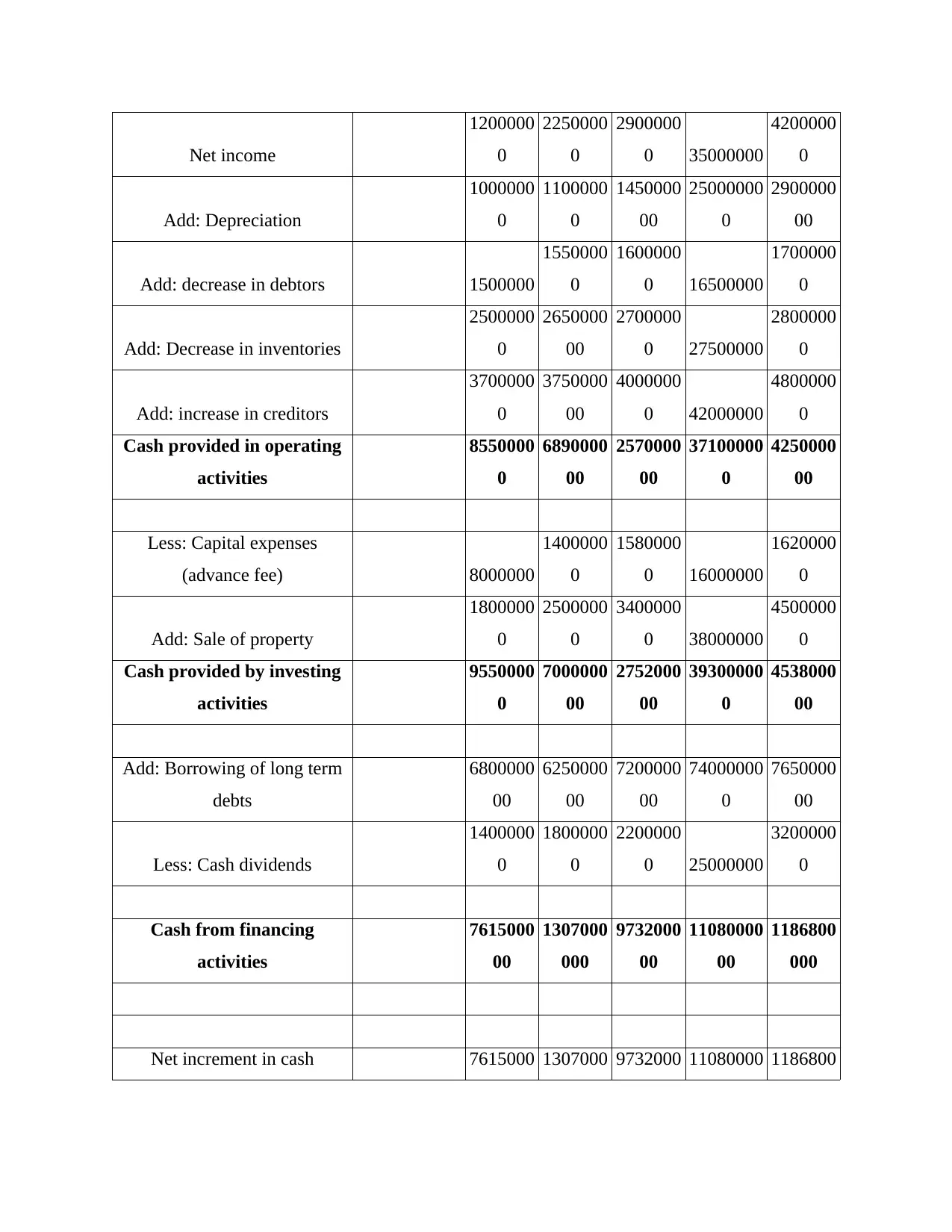

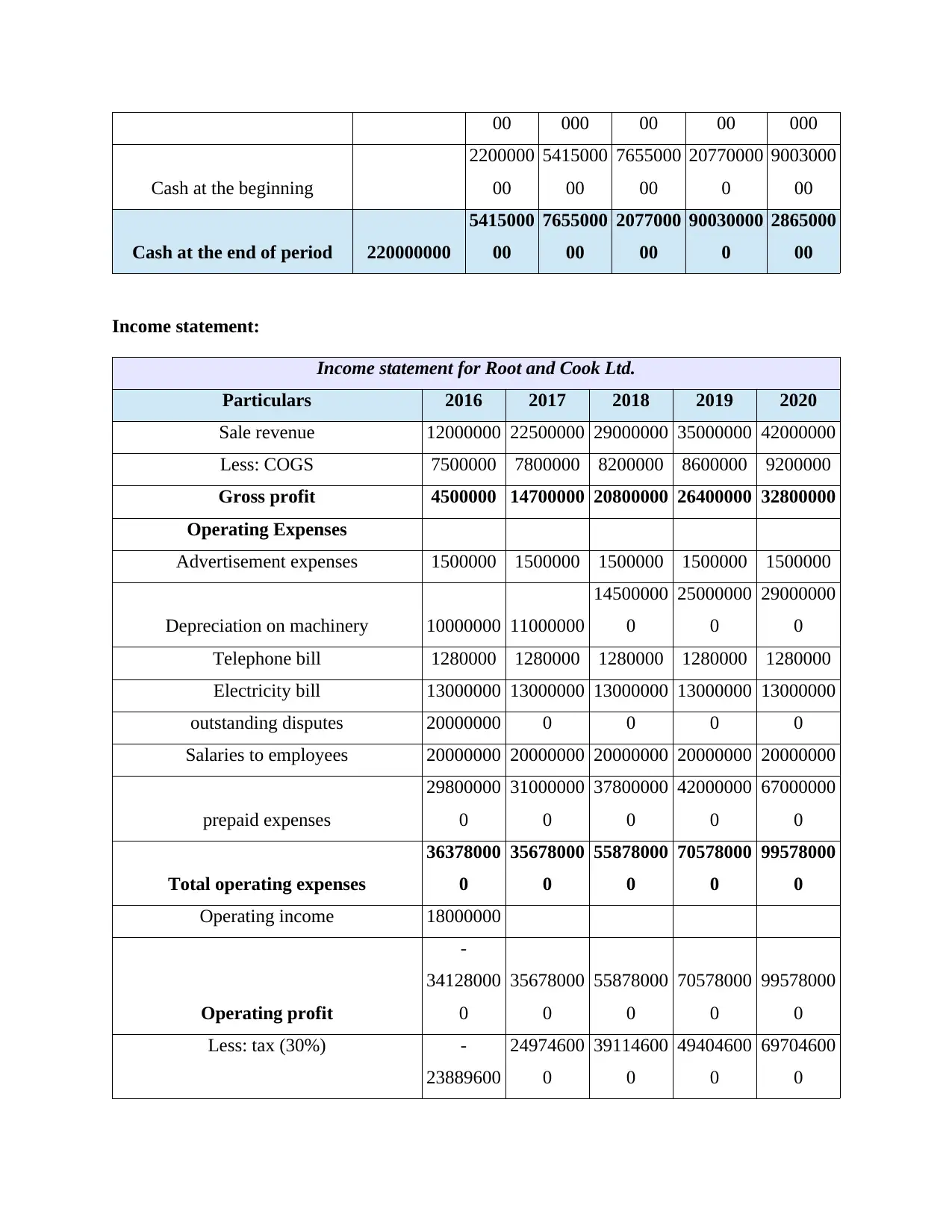

Cash Flow statement:

Cash flow statement of Root and Cook Ltd.

Particulars

Initial

investment 2016 2017 2018 2019 2020

surplus amount over all the income and

expenditures made by the business in a

financial year. These are the amount on

which the firm will make payments to

the shareholder's dividends, operational

investment as well as make payments

of the taxes.

The determination of the daily tasks and

operations of the business which in turn

helps in analysing the inflows and

outflows of the total cash (Young and

Pagliari, 2017). However, it helps in

managing the daily financial activities

such as taxation, purchase of

inventories, employee salaries as well

as paying off the costs incurred in

various operations.

b. Ascertaining the concept of working capital:

This is the technique which helps in determining the efficiency of the business in day to

day operations. This ascertains the ability of the firm in meeting the short terms requirements

such as analysing the current liabilities and current assets of the firm (Block and et.al., 2018). It

facilitates the information to the professionals that the firm is having enough short term assets

which will be helpful in meeting to pay off the short term debts.

c. Analysing the impacts of working capital over cash flow

2. Determining the financial position of the business as per the outcomes of various financial

results

To ascertains the appropriate financial health of the entity there are analysis of the 5 years

financials which will be helpful in suggesting the adequate changes in the operations of Root and

Cook Ltd. Thus, there are analysis of cash flow statement, income statement and balance sheet of

the entity which will indicate the operational transactions held during the period and which will

be beneficial in ascertaining the liquidity and efficiency of the business.

Cash Flow statement:

Cash flow statement of Root and Cook Ltd.

Particulars

Initial

investment 2016 2017 2018 2019 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net income

1200000

0

2250000

0

2900000

0 35000000

4200000

0

Add: Depreciation

1000000

0

1100000

0

1450000

00

25000000

0

2900000

00

Add: decrease in debtors 1500000

1550000

0

1600000

0 16500000

1700000

0

Add: Decrease in inventories

2500000

0

2650000

00

2700000

0 27500000

2800000

0

Add: increase in creditors

3700000

0

3750000

00

4000000

0 42000000

4800000

0

Cash provided in operating

activities

8550000

0

6890000

00

2570000

00

37100000

0

4250000

00

Less: Capital expenses

(advance fee) 8000000

1400000

0

1580000

0 16000000

1620000

0

Add: Sale of property

1800000

0

2500000

0

3400000

0 38000000

4500000

0

Cash provided by investing

activities

9550000

0

7000000

00

2752000

00

39300000

0

4538000

00

Add: Borrowing of long term

debts

6800000

00

6250000

00

7200000

00

74000000

0

7650000

00

Less: Cash dividends

1400000

0

1800000

0

2200000

0 25000000

3200000

0

Cash from financing

activities

7615000

00

1307000

000

9732000

00

11080000

00

1186800

000

Net increment in cash 7615000 1307000 9732000 11080000 1186800

1200000

0

2250000

0

2900000

0 35000000

4200000

0

Add: Depreciation

1000000

0

1100000

0

1450000

00

25000000

0

2900000

00

Add: decrease in debtors 1500000

1550000

0

1600000

0 16500000

1700000

0

Add: Decrease in inventories

2500000

0

2650000

00

2700000

0 27500000

2800000

0

Add: increase in creditors

3700000

0

3750000

00

4000000

0 42000000

4800000

0

Cash provided in operating

activities

8550000

0

6890000

00

2570000

00

37100000

0

4250000

00

Less: Capital expenses

(advance fee) 8000000

1400000

0

1580000

0 16000000

1620000

0

Add: Sale of property

1800000

0

2500000

0

3400000

0 38000000

4500000

0

Cash provided by investing

activities

9550000

0

7000000

00

2752000

00

39300000

0

4538000

00

Add: Borrowing of long term

debts

6800000

00

6250000

00

7200000

00

74000000

0

7650000

00

Less: Cash dividends

1400000

0

1800000

0

2200000

0 25000000

3200000

0

Cash from financing

activities

7615000

00

1307000

000

9732000

00

11080000

00

1186800

000

Net increment in cash 7615000 1307000 9732000 11080000 1186800

00 000 00 00 000

Cash at the beginning

2200000

00

5415000

00

7655000

00

20770000

0

9003000

00

Cash at the end of period 220000000

5415000

00

7655000

00

2077000

00

90030000

0

2865000

00

Income statement:

Income statement for Root and Cook Ltd.

Particulars 2016 2017 2018 2019 2020

Sale revenue 12000000 22500000 29000000 35000000 42000000

Less: COGS 7500000 7800000 8200000 8600000 9200000

Gross profit 4500000 14700000 20800000 26400000 32800000

Operating Expenses

Advertisement expenses 1500000 1500000 1500000 1500000 1500000

Depreciation on machinery 10000000 11000000

14500000

0

25000000

0

29000000

0

Telephone bill 1280000 1280000 1280000 1280000 1280000

Electricity bill 13000000 13000000 13000000 13000000 13000000

outstanding disputes 20000000 0 0 0 0

Salaries to employees 20000000 20000000 20000000 20000000 20000000

prepaid expenses

29800000

0

31000000

0

37800000

0

42000000

0

67000000

0

Total operating expenses

36378000

0

35678000

0

55878000

0

70578000

0

99578000

0

Operating income 18000000

Operating profit

-

34128000

0

35678000

0

55878000

0

70578000

0

99578000

0

Less: tax (30%) -

23889600

24974600

0

39114600

0

49404600

0

69704600

0

Cash at the beginning

2200000

00

5415000

00

7655000

00

20770000

0

9003000

00

Cash at the end of period 220000000

5415000

00

7655000

00

2077000

00

90030000

0

2865000

00

Income statement:

Income statement for Root and Cook Ltd.

Particulars 2016 2017 2018 2019 2020

Sale revenue 12000000 22500000 29000000 35000000 42000000

Less: COGS 7500000 7800000 8200000 8600000 9200000

Gross profit 4500000 14700000 20800000 26400000 32800000

Operating Expenses

Advertisement expenses 1500000 1500000 1500000 1500000 1500000

Depreciation on machinery 10000000 11000000

14500000

0

25000000

0

29000000

0

Telephone bill 1280000 1280000 1280000 1280000 1280000

Electricity bill 13000000 13000000 13000000 13000000 13000000

outstanding disputes 20000000 0 0 0 0

Salaries to employees 20000000 20000000 20000000 20000000 20000000

prepaid expenses

29800000

0

31000000

0

37800000

0

42000000

0

67000000

0

Total operating expenses

36378000

0

35678000

0

55878000

0

70578000

0

99578000

0

Operating income 18000000

Operating profit

-

34128000

0

35678000

0

55878000

0

70578000

0

99578000

0

Less: tax (30%) -

23889600

24974600

0

39114600

0

49404600

0

69704600

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

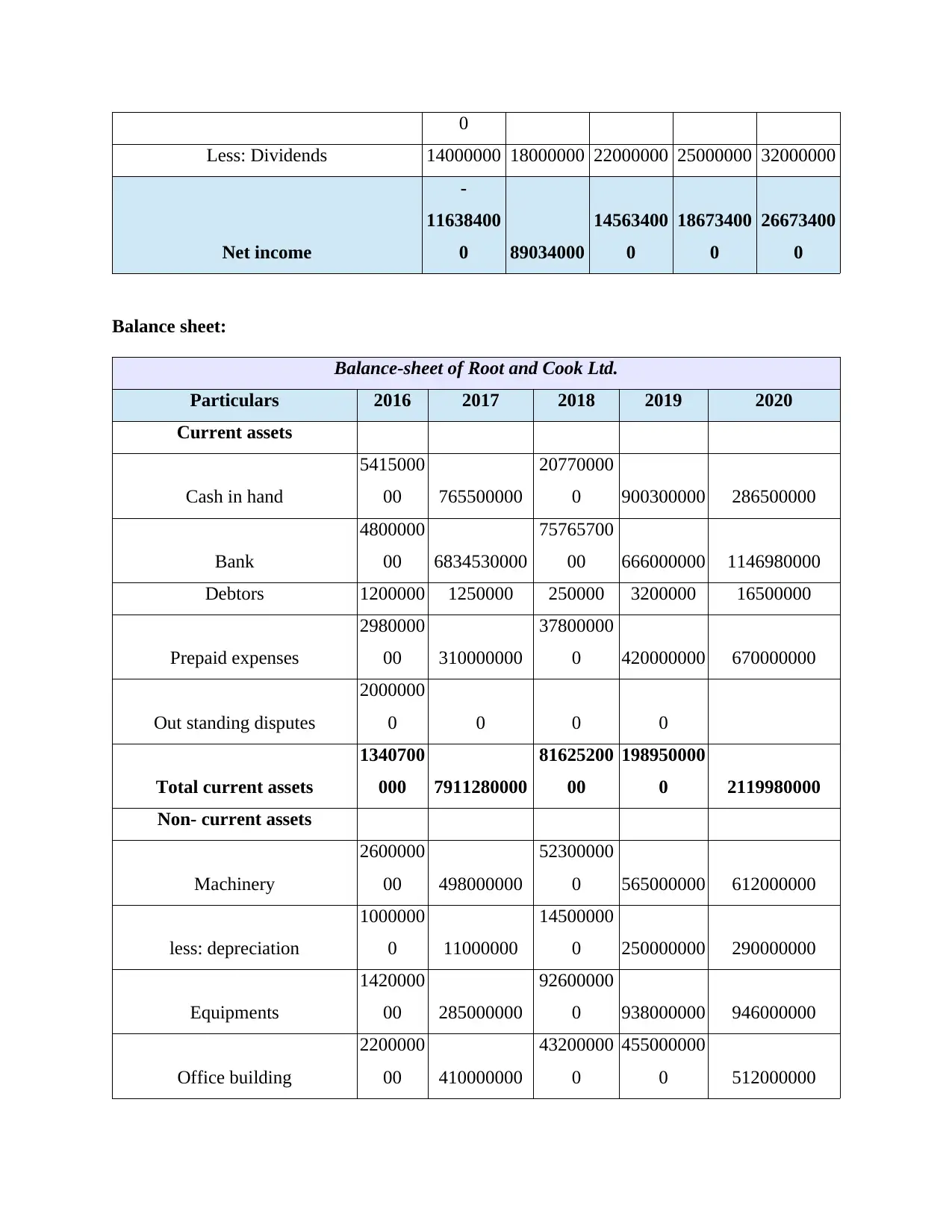

0

Less: Dividends 14000000 18000000 22000000 25000000 32000000

Net income

-

11638400

0 89034000

14563400

0

18673400

0

26673400

0

Balance sheet:

Balance-sheet of Root and Cook Ltd.

Particulars 2016 2017 2018 2019 2020

Current assets

Cash in hand

5415000

00 765500000

20770000

0 900300000 286500000

Bank

4800000

00 6834530000

75765700

00 666000000 1146980000

Debtors 1200000 1250000 250000 3200000 16500000

Prepaid expenses

2980000

00 310000000

37800000

0 420000000 670000000

Out standing disputes

2000000

0 0 0 0

Total current assets

1340700

000 7911280000

81625200

00

198950000

0 2119980000

Non- current assets

Machinery

2600000

00 498000000

52300000

0 565000000 612000000

less: depreciation

1000000

0 11000000

14500000

0 250000000 290000000

Equipments

1420000

00 285000000

92600000

0 938000000 946000000

Office building

2200000

00 410000000

43200000

0

455000000

0 512000000

Less: Dividends 14000000 18000000 22000000 25000000 32000000

Net income

-

11638400

0 89034000

14563400

0

18673400

0

26673400

0

Balance sheet:

Balance-sheet of Root and Cook Ltd.

Particulars 2016 2017 2018 2019 2020

Current assets

Cash in hand

5415000

00 765500000

20770000

0 900300000 286500000

Bank

4800000

00 6834530000

75765700

00 666000000 1146980000

Debtors 1200000 1250000 250000 3200000 16500000

Prepaid expenses

2980000

00 310000000

37800000

0 420000000 670000000

Out standing disputes

2000000

0 0 0 0

Total current assets

1340700

000 7911280000

81625200

00

198950000

0 2119980000

Non- current assets

Machinery

2600000

00 498000000

52300000

0 565000000 612000000

less: depreciation

1000000

0 11000000

14500000

0 250000000 290000000

Equipments

1420000

00 285000000

92600000

0 938000000 946000000

Office building

2200000

00 410000000

43200000

0

455000000

0 512000000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

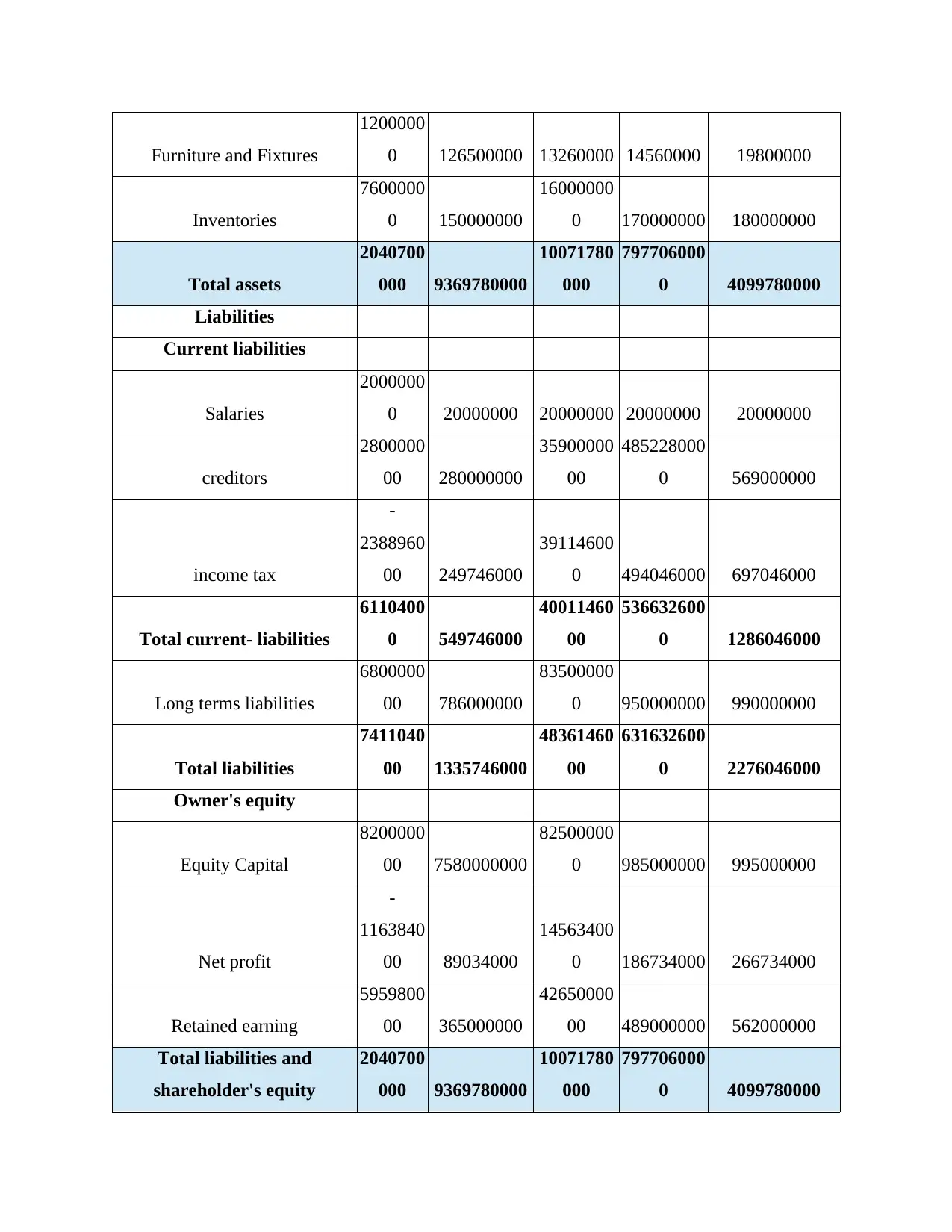

Furniture and Fixtures

1200000

0 126500000 13260000 14560000 19800000

Inventories

7600000

0 150000000

16000000

0 170000000 180000000

Total assets

2040700

000 9369780000

10071780

000

797706000

0 4099780000

Liabilities

Current liabilities

Salaries

2000000

0 20000000 20000000 20000000 20000000

creditors

2800000

00 280000000

35900000

00

485228000

0 569000000

income tax

-

2388960

00 249746000

39114600

0 494046000 697046000

Total current- liabilities

6110400

0 549746000

40011460

00

536632600

0 1286046000

Long terms liabilities

6800000

00 786000000

83500000

0 950000000 990000000

Total liabilities

7411040

00 1335746000

48361460

00

631632600

0 2276046000

Owner's equity

Equity Capital

8200000

00 7580000000

82500000

0 985000000 995000000

Net profit

-

1163840

00 89034000

14563400

0 186734000 266734000

Retained earning

5959800

00 365000000

42650000

00 489000000 562000000

Total liabilities and

shareholder's equity

2040700

000 9369780000

10071780

000

797706000

0 4099780000

1200000

0 126500000 13260000 14560000 19800000

Inventories

7600000

0 150000000

16000000

0 170000000 180000000

Total assets

2040700

000 9369780000

10071780

000

797706000

0 4099780000

Liabilities

Current liabilities

Salaries

2000000

0 20000000 20000000 20000000 20000000

creditors

2800000

00 280000000

35900000

00

485228000

0 569000000

income tax

-

2388960

00 249746000

39114600

0 494046000 697046000

Total current- liabilities

6110400

0 549746000

40011460

00

536632600

0 1286046000

Long terms liabilities

6800000

00 786000000

83500000

0 950000000 990000000

Total liabilities

7411040

00 1335746000

48361460

00

631632600

0 2276046000

Owner's equity

Equity Capital

8200000

00 7580000000

82500000

0 985000000 995000000

Net profit

-

1163840

00 89034000

14563400

0 186734000 266734000

Retained earning

5959800

00 365000000

42650000

00 489000000 562000000

Total liabilities and

shareholder's equity

2040700

000 9369780000

10071780

000

797706000

0 4099780000

3. Recommending the steps to control the cash flow through working capital management

On the basis of above determination and the findings in the financial statements of the

business it can be said that there is need to improve the funding process for the business which

will be helpful in managing the operational activities. Ion the year 2016 there has large amount

of debts which are need to be pay off as per having the appropriate investments in the company.

Thus, the professionals at Root and Cook Ltd will be suggested to have the adequate

improvement in the probability and balancing the working capital in appropriate way by

implicating several techniques such as:

There is need to have appropriate improvement in the debtor collection.

It is essential to have the satisfactory control over the creditor payments of the business.

To have the better negotiation and adequate prices with suppliers and distributors.

There should be appropriate reduction in the expenses of business (Castellucci and et.al.,

2017).

There is need to have adequate review over the tax opportunities.

PART 2

1. Evaluating the terms

Capital Budgeting process and steps

To have the satisfactory control over the financial transactions in the business there is

need to have proper capital budgeting (Alkhamis and et.al., 2017). It will be beneficial in terms

of having the effective financial management of the expensive assets as well as executing the

long term operations. However, the process of preparing the fruitful capital budgeting will be

analysed as follows:

Proposing the idea: The decision must be made and proposed by the professionals which

is need to be in good quality and must be accurate as to attain the fruitful growth.

However, the ideas will be generated through senior mangers, employees, departmental

heads etc.

On the basis of above determination and the findings in the financial statements of the

business it can be said that there is need to improve the funding process for the business which

will be helpful in managing the operational activities. Ion the year 2016 there has large amount

of debts which are need to be pay off as per having the appropriate investments in the company.

Thus, the professionals at Root and Cook Ltd will be suggested to have the adequate

improvement in the probability and balancing the working capital in appropriate way by

implicating several techniques such as:

There is need to have appropriate improvement in the debtor collection.

It is essential to have the satisfactory control over the creditor payments of the business.

To have the better negotiation and adequate prices with suppliers and distributors.

There should be appropriate reduction in the expenses of business (Castellucci and et.al.,

2017).

There is need to have adequate review over the tax opportunities.

PART 2

1. Evaluating the terms

Capital Budgeting process and steps

To have the satisfactory control over the financial transactions in the business there is

need to have proper capital budgeting (Alkhamis and et.al., 2017). It will be beneficial in terms

of having the effective financial management of the expensive assets as well as executing the

long term operations. However, the process of preparing the fruitful capital budgeting will be

analysed as follows:

Proposing the idea: The decision must be made and proposed by the professionals which

is need to be in good quality and must be accurate as to attain the fruitful growth.

However, the ideas will be generated through senior mangers, employees, departmental

heads etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Determining the proposed idea: After having the ideas there is need to have research

over it as well as need to generate the appropriate information. This will be helpful in

ascertaining the profitability of such plan and the professionals will analyse the returns

they will have from such investments (Adiwibowo, Lestari and Manalu, 2018).

Developing the capital budget: To proceed the plan after analysing the collected

information there is need to draw a capital budget on which the expected investment will

be mentioned. There will be presence of various financial statements such as forecasted

cash flows, income statements and balance sheet. It helps the professionals in strategic

planning and decision making.

Post audit and execution: After preparing such budgets, it is essentially required to

make the adequate analysis over the operations as well as actual results of such activities.

There will be comparison of such budgeted plan and actual result and the variance result

will help the professionals to plan for further changes (Malek and et.al., 2017). It

promotes the better internal control as the costs incurred in each activities will be

managed and have the adequate control over it.

Advantages and disadvantages of the investment appraisal methods

Payback period: This is the time on which the initially invested cash amount will be

recovered in the upcoming time. To identify when the company will recover such invested

capital there are several operations and analysis will be made which in turn helps in determining

the profitability of the projects (Campbell, 2017). However, there will be various advantages and

disadvantages of this technique such as:

Advantages:

This is the easiest and convenient way of determining the outcomes.

It will be beneficial in identifying the risks involved in such projects and determines the

profitably of the cash inflows.

It helps the organisation which are facing the liquidity problems with providing the

information about early return of the money (Block and et.al., 2018).

Disadvantages

over it as well as need to generate the appropriate information. This will be helpful in

ascertaining the profitability of such plan and the professionals will analyse the returns

they will have from such investments (Adiwibowo, Lestari and Manalu, 2018).

Developing the capital budget: To proceed the plan after analysing the collected

information there is need to draw a capital budget on which the expected investment will

be mentioned. There will be presence of various financial statements such as forecasted

cash flows, income statements and balance sheet. It helps the professionals in strategic

planning and decision making.

Post audit and execution: After preparing such budgets, it is essentially required to

make the adequate analysis over the operations as well as actual results of such activities.

There will be comparison of such budgeted plan and actual result and the variance result

will help the professionals to plan for further changes (Malek and et.al., 2017). It

promotes the better internal control as the costs incurred in each activities will be

managed and have the adequate control over it.

Advantages and disadvantages of the investment appraisal methods

Payback period: This is the time on which the initially invested cash amount will be

recovered in the upcoming time. To identify when the company will recover such invested

capital there are several operations and analysis will be made which in turn helps in determining

the profitability of the projects (Campbell, 2017). However, there will be various advantages and

disadvantages of this technique such as:

Advantages:

This is the easiest and convenient way of determining the outcomes.

It will be beneficial in identifying the risks involved in such projects and determines the

profitably of the cash inflows.

It helps the organisation which are facing the liquidity problems with providing the

information about early return of the money (Block and et.al., 2018).

Disadvantages

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It does not consider the time value of money as it did not consider the discounting factors

which examining the data set.

It did not consider the amount of cash flows which incurred after the measurements of the

payback period (Payback Period, 2013).

Net present value: This ascertains the present value of the future cash flows which helps

the managers in analysing the profitability of such projects. It facilitates the accurate information

regarding the profitability of the projects and help the business to have modification in the plan

(Castellucci and et.al., 2017). It is the accurate way of determining the fruitfulness of the projects

in the development and growth of the entities.

Advantages

It is the easiest way of identifying the profitability over such projects and investments

planned by the professionals.

It considers the time value of money as there has been influence of the discounting factor

which will be fruitful in determining the accurate outcomes (Alkhamis and et.al., 2017).

It provokes the investors by the outcomes to make the investment decisions in the

business.

Disadvantages

It considers the guesswork in measuring the cash flows for the planned period which in

turn does not bring the surety of having the accurate results.

The results brought from two or more projects does not bring the adequate information

about the investments to be made or not as all the invested plan belongs to the different

time scale and it will be inaccurate in analysing the profitability ion the basis of same

discounting factors (Adiwibowo, Lestari and Manalu, 2018).

Internal rate of return: To ascertain the returns a firm will acquire through its invested

projects on the basis of the proposed period this technique is most required. It identifies the rate

on which the firm will have the profitable returns over the period. Therefore, there are several

advantages and disadvantages of this method plan which are as follows:

Advantages

which examining the data set.

It did not consider the amount of cash flows which incurred after the measurements of the

payback period (Payback Period, 2013).

Net present value: This ascertains the present value of the future cash flows which helps

the managers in analysing the profitability of such projects. It facilitates the accurate information

regarding the profitability of the projects and help the business to have modification in the plan

(Castellucci and et.al., 2017). It is the accurate way of determining the fruitfulness of the projects

in the development and growth of the entities.

Advantages

It is the easiest way of identifying the profitability over such projects and investments

planned by the professionals.

It considers the time value of money as there has been influence of the discounting factor

which will be fruitful in determining the accurate outcomes (Alkhamis and et.al., 2017).

It provokes the investors by the outcomes to make the investment decisions in the

business.

Disadvantages

It considers the guesswork in measuring the cash flows for the planned period which in

turn does not bring the surety of having the accurate results.

The results brought from two or more projects does not bring the adequate information

about the investments to be made or not as all the invested plan belongs to the different

time scale and it will be inaccurate in analysing the profitability ion the basis of same

discounting factors (Adiwibowo, Lestari and Manalu, 2018).

Internal rate of return: To ascertain the returns a firm will acquire through its invested

projects on the basis of the proposed period this technique is most required. It identifies the rate

on which the firm will have the profitable returns over the period. Therefore, there are several

advantages and disadvantages of this method plan which are as follows:

Advantages

The estimation of the projected cash flows will be based on considering the time value of

money.

There will be no influence of any hurdle rate to identify the rate of return.

Disadvantages

It considers only the cash flows as it ignore the other factors such as economies of scale.

The analysis is based on several assumptions and estimations which does not bring the

reliability over the outcomes (Malek and et.al., 2017).

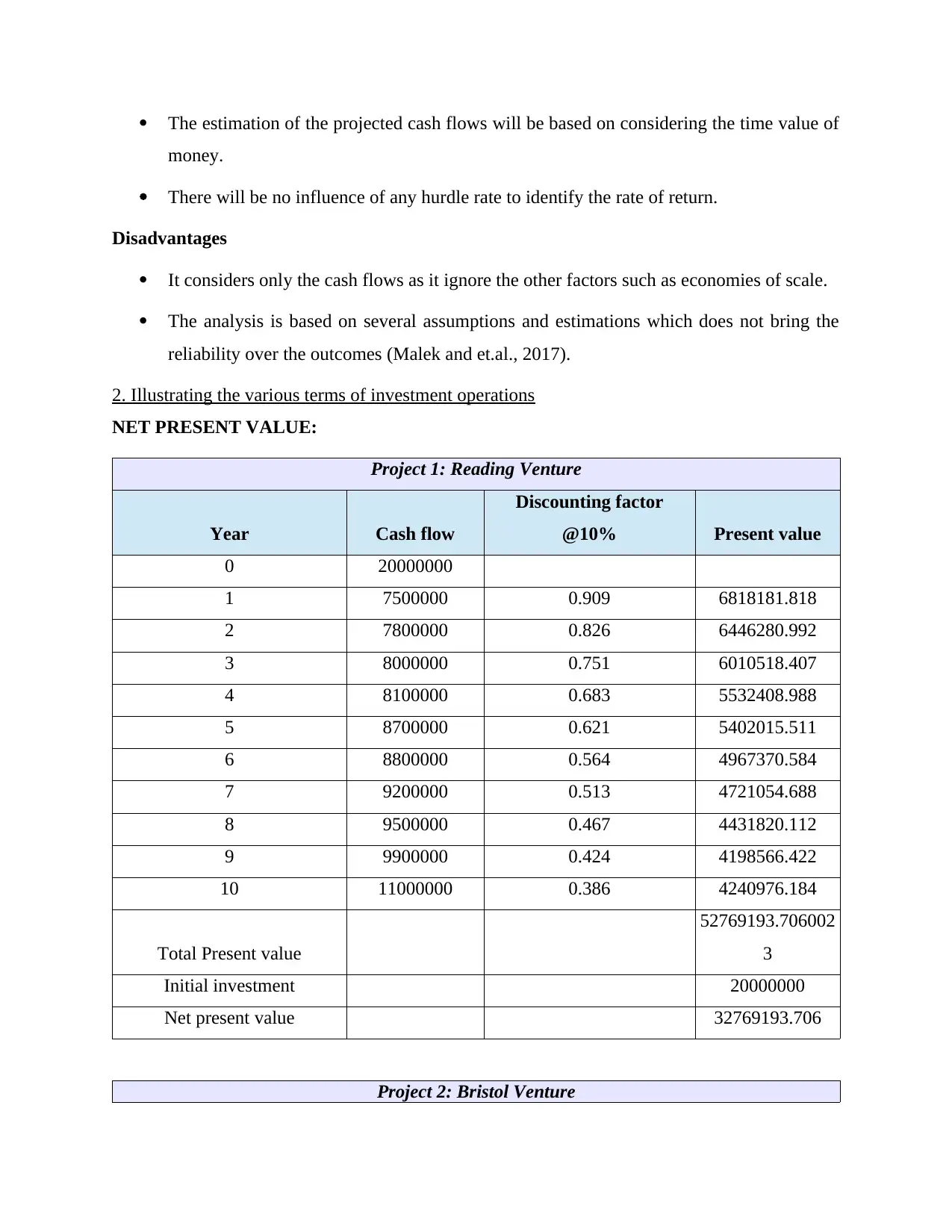

2. Illustrating the various terms of investment operations

NET PRESENT VALUE:

Project 1: Reading Venture

Year Cash flow

Discounting factor

@10% Present value

0 20000000

1 7500000 0.909 6818181.818

2 7800000 0.826 6446280.992

3 8000000 0.751 6010518.407

4 8100000 0.683 5532408.988

5 8700000 0.621 5402015.511

6 8800000 0.564 4967370.584

7 9200000 0.513 4721054.688

8 9500000 0.467 4431820.112

9 9900000 0.424 4198566.422

10 11000000 0.386 4240976.184

Total Present value

52769193.706002

3

Initial investment 20000000

Net present value 32769193.706

Project 2: Bristol Venture

money.

There will be no influence of any hurdle rate to identify the rate of return.

Disadvantages

It considers only the cash flows as it ignore the other factors such as economies of scale.

The analysis is based on several assumptions and estimations which does not bring the

reliability over the outcomes (Malek and et.al., 2017).

2. Illustrating the various terms of investment operations

NET PRESENT VALUE:

Project 1: Reading Venture

Year Cash flow

Discounting factor

@10% Present value

0 20000000

1 7500000 0.909 6818181.818

2 7800000 0.826 6446280.992

3 8000000 0.751 6010518.407

4 8100000 0.683 5532408.988

5 8700000 0.621 5402015.511

6 8800000 0.564 4967370.584

7 9200000 0.513 4721054.688

8 9500000 0.467 4431820.112

9 9900000 0.424 4198566.422

10 11000000 0.386 4240976.184

Total Present value

52769193.706002

3

Initial investment 20000000

Net present value 32769193.706

Project 2: Bristol Venture

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.