Business Finance Report: Cash Flow and Ratio Analysis of Two Firms

VerifiedAdded on 2020/10/05

|12

|3523

|153

Report

AI Summary

This report provides a detailed analysis of the financial performance of Modern Garden Designs Ltd and GlowSheets Ltd. It begins by defining and explaining key concepts such as profit, cash flow, working capital, receivables, inventory, and payables, including how alterations in working capital impact cash flow. The report then applies these concepts to Modern Garden Designs Ltd, examining its financial results and recommending steps to improve cash flow through better working capital management. Part 2 focuses on GlowSheets Ltd, calculating and analyzing financial ratios, including sales growth, gross profit margin, operating profit margin, and gearing ratio. The analysis reveals trends in financial performance from 20X9 to 20X1, highlighting areas of concern and providing recommendations for improvement. The report concludes by summarizing the key findings and offering insights into the financial health and management strategies of both companies.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Business finance is termed as money and credit which is directly employed in business as

it engages utilization and procurement of funds where various business entities which might be

capable for carrying its operations in efficient aspect. The present report will give brief

discussion about Modern Garden Designs Limited and GlowSheets Ltd on basis of financial

statements and appropriate ratio analysis. By considering Modern Garden Designs Ltd, it has

been suggested that cash flow could be managed easily with reference to better working capital.

In the similar aspect GlowSheets Ltd has to control its operating expense which is giving direct

impact on profitability.

Business finance is termed as money and credit which is directly employed in business as

it engages utilization and procurement of funds where various business entities which might be

capable for carrying its operations in efficient aspect. The present report will give brief

discussion about Modern Garden Designs Limited and GlowSheets Ltd on basis of financial

statements and appropriate ratio analysis. By considering Modern Garden Designs Ltd, it has

been suggested that cash flow could be managed easily with reference to better working capital.

In the similar aspect GlowSheets Ltd has to control its operating expense which is giving direct

impact on profitability.

TABLE OF CONTENTS

PART 1 Modern Garden Designs Ltd.............................................................................................1

1.a Explaining meaning of profit and cash flow with its variations............................................1

1.b Explaining working capital, Receivables, Inventory and payables.......................................1

1.c Explaining how alterations in working capital impact cash flow..........................................2

2. Explaining above concepts in Modern Garden Designs Ltd for managing its financial results

......................................................................................................................................................3

3. Analysing and recommending steps for improving cash flow of organization with better

working capital management.......................................................................................................3

PART 2 GlowSheets Ltd.................................................................................................................4

A. Explaining elements of financial performance of each...........................................................4

B. Calculating ratio and changes from year 20X9 to 20X1.........................................................4

C. Analysing changes from year 20X9 to 20X1..........................................................................7

Analysis and recommendation.....................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

PART 1 Modern Garden Designs Ltd.............................................................................................1

1.a Explaining meaning of profit and cash flow with its variations............................................1

1.b Explaining working capital, Receivables, Inventory and payables.......................................1

1.c Explaining how alterations in working capital impact cash flow..........................................2

2. Explaining above concepts in Modern Garden Designs Ltd for managing its financial results

......................................................................................................................................................3

3. Analysing and recommending steps for improving cash flow of organization with better

working capital management.......................................................................................................3

PART 2 GlowSheets Ltd.................................................................................................................4

A. Explaining elements of financial performance of each...........................................................4

B. Calculating ratio and changes from year 20X9 to 20X1.........................................................4

C. Analysing changes from year 20X9 to 20X1..........................................................................7

Analysis and recommendation.....................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 1 Modern Garden Designs Ltd

1.a Explaining meaning of profit and cash flow with its variations

Cash flow is replicated as money which flows out and in to business entity through

financing and operating activities. This is money which is used for accomplishing present and

near term obligations but it must always consider that:

The business could be profitable enough but still with absence of adequate cash flow as

well.

There could be increment in sales simultaneously money could be poured which does not

signifies that profit is created.

Profit is also replicated as net income or what is remained through sales revenue after

deducting each expense of business. It is considered as obvious principal where business could

not sustain unless it is profitable but it could be with context of cash flow, the products' success

could increase its expenses. It might be not apparent on immediate aspect as it is issue. In various

cases, problems could be easily extracted but by decreasing cost of production will help in

restoring profitability for avoiding crisis. Consequently, without appropriate understanding of

relevant data about cost it might not perform effectively and prompt for making business entity

as profitable before it goes out of money (The Critical Differences Between Cash Flow and

Profit, 2018).

1.b Explaining working capital, Receivables, Inventory and payables

Working capital: It is also replicated as net working capital which is difference among

current assets and current liabilities where current assets considers cash, accounts receivables,

inventories of finished goods and raw materials and current liabilities considers accounts payable

and all. It is measure of both organization's short term financial health along with operational

efficiency. If difference is higher on what it own and owe for short term then business is

healthier. If working capital is negative then it is close for being out from business (Yusuf and

Sani, 2018).

Receivables: These are replicated as accounts receivable as well as debts which are

owned through business entity for services and goods which are used or delivered but payment

has been not paid. It is formed through extending credit line to its customers and reported in form

of current assets and in term of required payments which are due with relatively short duration

with range of few days to financial or calendar year. In similar aspect, they are considered as

1

1.a Explaining meaning of profit and cash flow with its variations

Cash flow is replicated as money which flows out and in to business entity through

financing and operating activities. This is money which is used for accomplishing present and

near term obligations but it must always consider that:

The business could be profitable enough but still with absence of adequate cash flow as

well.

There could be increment in sales simultaneously money could be poured which does not

signifies that profit is created.

Profit is also replicated as net income or what is remained through sales revenue after

deducting each expense of business. It is considered as obvious principal where business could

not sustain unless it is profitable but it could be with context of cash flow, the products' success

could increase its expenses. It might be not apparent on immediate aspect as it is issue. In various

cases, problems could be easily extracted but by decreasing cost of production will help in

restoring profitability for avoiding crisis. Consequently, without appropriate understanding of

relevant data about cost it might not perform effectively and prompt for making business entity

as profitable before it goes out of money (The Critical Differences Between Cash Flow and

Profit, 2018).

1.b Explaining working capital, Receivables, Inventory and payables

Working capital: It is also replicated as net working capital which is difference among

current assets and current liabilities where current assets considers cash, accounts receivables,

inventories of finished goods and raw materials and current liabilities considers accounts payable

and all. It is measure of both organization's short term financial health along with operational

efficiency. If difference is higher on what it own and owe for short term then business is

healthier. If working capital is negative then it is close for being out from business (Yusuf and

Sani, 2018).

Receivables: These are replicated as accounts receivable as well as debts which are

owned through business entity for services and goods which are used or delivered but payment

has been not paid. It is formed through extending credit line to its customers and reported in form

of current assets and in term of required payments which are due with relatively short duration

with range of few days to financial or calendar year. In similar aspect, they are considered as

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

liquid asset as they can be used for purpose of collateral for securing loan to accomplish short

term obligations.

Inventories: It is referred as term for availability of goods for raw materials and sales

which are used for producing goods. Inventory is represented as very important for assets of

business due to its turnover on basis of inventory is termed as primary source for producing

revenue along with subsequent earning for shareholders of organization. It is array of various

finished goods which are used for production which are held through business entity. Generally,

it is classified in balance sheet as current asset. In the similar series, it serves buffer among

manufacturing and fulfilment of order.

Payables: It is an accounting entry which shows obligation of business entity for

repaying its short term debt to its suppliers and creditors. It will appear in balance sheet with

context to current liabilities and its common use has been referred to specific business

department along with division which is responsible for payments which are owned through

company to its suppliers and creditors. These are debit which should be paid within specific

duration for avoiding default. For example at corporate level it refers to short term debt payment

to its suppliers and payable is mandatory for short term informal document through business to

any other organisation (Enow and Kamala, 2018).

1.c Explaining how alterations in working capital impact cash flow

The alteration in working capital would be directly reflected in cash flow statement of

business entity. If there is increment in transactions then current assets and liabilities would raise

by similar amount, so it will not impact working capital. In case organization will purchase fixed

asset like building then cash flow of organization will decrease. In the similar aspect, working

capital of business entity will reduce as portion of cash with context of current assets will be

decreased. However, its current liabilities will not change as it would be long term debt.

Simultaneously, if selling of fixed asset would directly boost working capital along with cash

flow. If organization will purchase inventory through cash then there will be no alteration in

working capital due to cash and inventory both are considered in category of current asset. On

the contrary, cash flow would decrease by inventory purchases (Uwuigbe and et.al., 2018).

In a nutshell, boost in working capital and cash flow might be not good if business entity

will undertake long term debt as it will not generate sufficient cash flow for repaying it.

Consequently, huge decrease in cash flow and working capital which is not bad if company will

2

term obligations.

Inventories: It is referred as term for availability of goods for raw materials and sales

which are used for producing goods. Inventory is represented as very important for assets of

business due to its turnover on basis of inventory is termed as primary source for producing

revenue along with subsequent earning for shareholders of organization. It is array of various

finished goods which are used for production which are held through business entity. Generally,

it is classified in balance sheet as current asset. In the similar series, it serves buffer among

manufacturing and fulfilment of order.

Payables: It is an accounting entry which shows obligation of business entity for

repaying its short term debt to its suppliers and creditors. It will appear in balance sheet with

context to current liabilities and its common use has been referred to specific business

department along with division which is responsible for payments which are owned through

company to its suppliers and creditors. These are debit which should be paid within specific

duration for avoiding default. For example at corporate level it refers to short term debt payment

to its suppliers and payable is mandatory for short term informal document through business to

any other organisation (Enow and Kamala, 2018).

1.c Explaining how alterations in working capital impact cash flow

The alteration in working capital would be directly reflected in cash flow statement of

business entity. If there is increment in transactions then current assets and liabilities would raise

by similar amount, so it will not impact working capital. In case organization will purchase fixed

asset like building then cash flow of organization will decrease. In the similar aspect, working

capital of business entity will reduce as portion of cash with context of current assets will be

decreased. However, its current liabilities will not change as it would be long term debt.

Simultaneously, if selling of fixed asset would directly boost working capital along with cash

flow. If organization will purchase inventory through cash then there will be no alteration in

working capital due to cash and inventory both are considered in category of current asset. On

the contrary, cash flow would decrease by inventory purchases (Uwuigbe and et.al., 2018).

In a nutshell, boost in working capital and cash flow might be not good if business entity

will undertake long term debt as it will not generate sufficient cash flow for repaying it.

Consequently, huge decrease in cash flow and working capital which is not bad if company will

2

be using proceeds for investment in fixed assets for long term which will produce earnings in

coming year.

2. Explaining above concepts in Modern Garden Designs Ltd for managing its financial results

The Modern Garden designs limited will be managing its financial outcome as it has

profit of £18 million against sales of £220 million. It has presence of accounts payable with

consignment of £20 million for Brico France which will complete in year 2017 which is not yet

paid as it will led to payment which is withheld during continuation of negotiation among its

lawyers and technical suppliers. With reference to accounts receivable as £8 million as advance

fee through Eastern Fires. Furthermore, on basis of inventory there is requirement with presence

of stock level when dispute is sorted and reluctant to press his key consumers for hard payment.

3. Analysing and recommending steps for improving cash flow of organization with better

working capital management

The steps for improving cash flow with managing its working capital are stated below:

Assessing current position Determining pattern with outgoing and

incoming receivables and assets and align it with

specific level of working capital.

The baseline will be continuously monitored and

alteration in metrics as key for developing

strategy of working capital management.

Tracking performance Developing management reports along with

dashboards for monitoring and tracking

compliance across business entity both

horizontally and laterally.

Creating action plan Strategic initiative as managing working capital

Streamline for manufacturing along with supply

chain

close collaboration

Appropriate coordination

Improvement in cash collection and billing

Implementation of risk of supply chain to

3

coming year.

2. Explaining above concepts in Modern Garden Designs Ltd for managing its financial results

The Modern Garden designs limited will be managing its financial outcome as it has

profit of £18 million against sales of £220 million. It has presence of accounts payable with

consignment of £20 million for Brico France which will complete in year 2017 which is not yet

paid as it will led to payment which is withheld during continuation of negotiation among its

lawyers and technical suppliers. With reference to accounts receivable as £8 million as advance

fee through Eastern Fires. Furthermore, on basis of inventory there is requirement with presence

of stock level when dispute is sorted and reluctant to press his key consumers for hard payment.

3. Analysing and recommending steps for improving cash flow of organization with better

working capital management

The steps for improving cash flow with managing its working capital are stated below:

Assessing current position Determining pattern with outgoing and

incoming receivables and assets and align it with

specific level of working capital.

The baseline will be continuously monitored and

alteration in metrics as key for developing

strategy of working capital management.

Tracking performance Developing management reports along with

dashboards for monitoring and tracking

compliance across business entity both

horizontally and laterally.

Creating action plan Strategic initiative as managing working capital

Streamline for manufacturing along with supply

chain

close collaboration

Appropriate coordination

Improvement in cash collection and billing

Implementation of risk of supply chain to

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manage its policies

Continual for improvement Initiative should be sustainable

Continual analysis along with collaboration

PART 2 GlowSheets Ltd

A. Explaining elements of financial performance of each

The elements of financial performance are referred with financial statements which are

stated below:

Revenue: It is referred as income which is earned by business through it normal activities

of business. It is considered as inflow of assets whose outcome is increment in owner's

equity.

Expenses: These are replicated as gross outflow which is incurred through business

entity for producing revenues as it is always charged in Income statement.

Assets: It is legal rights or property which is owned through business by which money

value be directly attached as it is item of economic value which is directly expected for

yield a benefit in coming future. It comprises current and non current assets whereas

current assets could be convertible in cash and non current assets are vice versa.

Liabilities: It is referred as present obligation of business entity which has been arisen

through past events along with settlement which is expected to outcome in outflow

through business entity of its resources for economic benefits. It consists of current and

non current liabilities which are repayable in current financial year and others are due for

payment for long term duration respectively (Zeng and Wudhikarn, 2018).

Equity: It reflects ownership interest in business entity with stock form. In simple words,

it is variation among cost of liabilities and assets value of something owned. Generally,

its residual amount is adjusted through assets against liabilities.

B. Calculating ratio and changes from year 20X9 to 20X1

Formula 20X9 20X0 20X1

Sales 250 275 319

Sales growth

(Sales Y2 – Sales

Y1)/ Sales Y1 10.00% 16.00%

4

Continual for improvement Initiative should be sustainable

Continual analysis along with collaboration

PART 2 GlowSheets Ltd

A. Explaining elements of financial performance of each

The elements of financial performance are referred with financial statements which are

stated below:

Revenue: It is referred as income which is earned by business through it normal activities

of business. It is considered as inflow of assets whose outcome is increment in owner's

equity.

Expenses: These are replicated as gross outflow which is incurred through business

entity for producing revenues as it is always charged in Income statement.

Assets: It is legal rights or property which is owned through business by which money

value be directly attached as it is item of economic value which is directly expected for

yield a benefit in coming future. It comprises current and non current assets whereas

current assets could be convertible in cash and non current assets are vice versa.

Liabilities: It is referred as present obligation of business entity which has been arisen

through past events along with settlement which is expected to outcome in outflow

through business entity of its resources for economic benefits. It consists of current and

non current liabilities which are repayable in current financial year and others are due for

payment for long term duration respectively (Zeng and Wudhikarn, 2018).

Equity: It reflects ownership interest in business entity with stock form. In simple words,

it is variation among cost of liabilities and assets value of something owned. Generally,

its residual amount is adjusted through assets against liabilities.

B. Calculating ratio and changes from year 20X9 to 20X1

Formula 20X9 20X0 20X1

Sales 250 275 319

Sales growth

(Sales Y2 – Sales

Y1)/ Sales Y1 10.00% 16.00%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

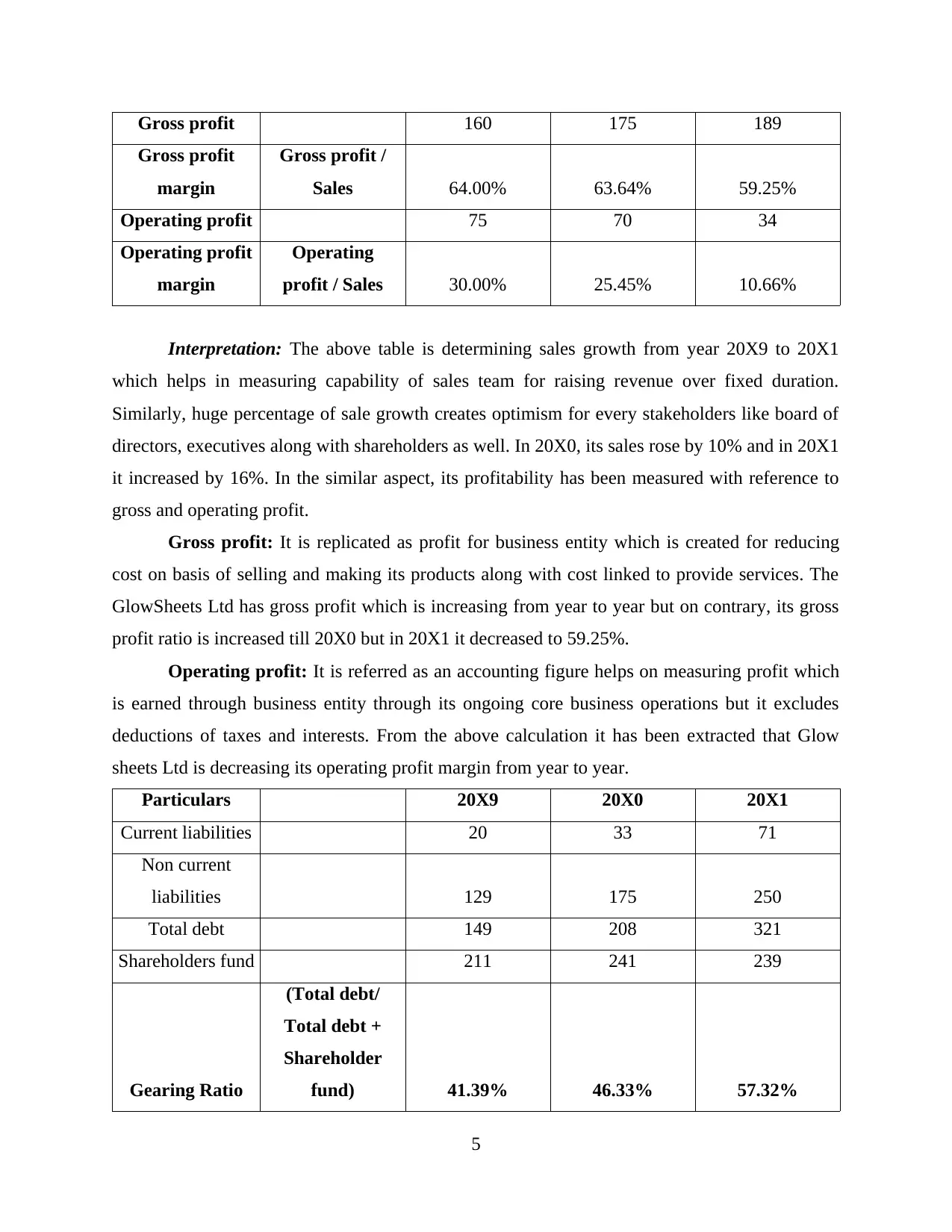

Gross profit 160 175 189

Gross profit

margin

Gross profit /

Sales 64.00% 63.64% 59.25%

Operating profit 75 70 34

Operating profit

margin

Operating

profit / Sales 30.00% 25.45% 10.66%

Interpretation: The above table is determining sales growth from year 20X9 to 20X1

which helps in measuring capability of sales team for raising revenue over fixed duration.

Similarly, huge percentage of sale growth creates optimism for every stakeholders like board of

directors, executives along with shareholders as well. In 20X0, its sales rose by 10% and in 20X1

it increased by 16%. In the similar aspect, its profitability has been measured with reference to

gross and operating profit.

Gross profit: It is replicated as profit for business entity which is created for reducing

cost on basis of selling and making its products along with cost linked to provide services. The

GlowSheets Ltd has gross profit which is increasing from year to year but on contrary, its gross

profit ratio is increased till 20X0 but in 20X1 it decreased to 59.25%.

Operating profit: It is referred as an accounting figure helps on measuring profit which

is earned through business entity through its ongoing core business operations but it excludes

deductions of taxes and interests. From the above calculation it has been extracted that Glow

sheets Ltd is decreasing its operating profit margin from year to year.

Particulars 20X9 20X0 20X1

Current liabilities 20 33 71

Non current

liabilities 129 175 250

Total debt 149 208 321

Shareholders fund 211 241 239

Gearing Ratio

(Total debt/

Total debt +

Shareholder

fund) 41.39% 46.33% 57.32%

5

Gross profit

margin

Gross profit /

Sales 64.00% 63.64% 59.25%

Operating profit 75 70 34

Operating profit

margin

Operating

profit / Sales 30.00% 25.45% 10.66%

Interpretation: The above table is determining sales growth from year 20X9 to 20X1

which helps in measuring capability of sales team for raising revenue over fixed duration.

Similarly, huge percentage of sale growth creates optimism for every stakeholders like board of

directors, executives along with shareholders as well. In 20X0, its sales rose by 10% and in 20X1

it increased by 16%. In the similar aspect, its profitability has been measured with reference to

gross and operating profit.

Gross profit: It is replicated as profit for business entity which is created for reducing

cost on basis of selling and making its products along with cost linked to provide services. The

GlowSheets Ltd has gross profit which is increasing from year to year but on contrary, its gross

profit ratio is increased till 20X0 but in 20X1 it decreased to 59.25%.

Operating profit: It is referred as an accounting figure helps on measuring profit which

is earned through business entity through its ongoing core business operations but it excludes

deductions of taxes and interests. From the above calculation it has been extracted that Glow

sheets Ltd is decreasing its operating profit margin from year to year.

Particulars 20X9 20X0 20X1

Current liabilities 20 33 71

Non current

liabilities 129 175 250

Total debt 149 208 321

Shareholders fund 211 241 239

Gearing Ratio

(Total debt/

Total debt +

Shareholder

fund) 41.39% 46.33% 57.32%

5

Gearing ratio: This is replicated as general classification for giving description of

financial ratio which helps in comparing for of owner's equity to particular funds which are

borrowed by organization. The gearing is increasing from year to year whereas high gearing

reflects huge proportion of debt to equity while low gearing is vice versa. Generally, gearing

between 25% to 50% belongs to optimal or normal for companies which are well established as

in year 20X9 and 20X0 it was 41.39% and 46.33% respectively but in 20X1 it was more than

50% as 57.32% which signifies that it would be at huge financial risk through both lenders and

investors as well.

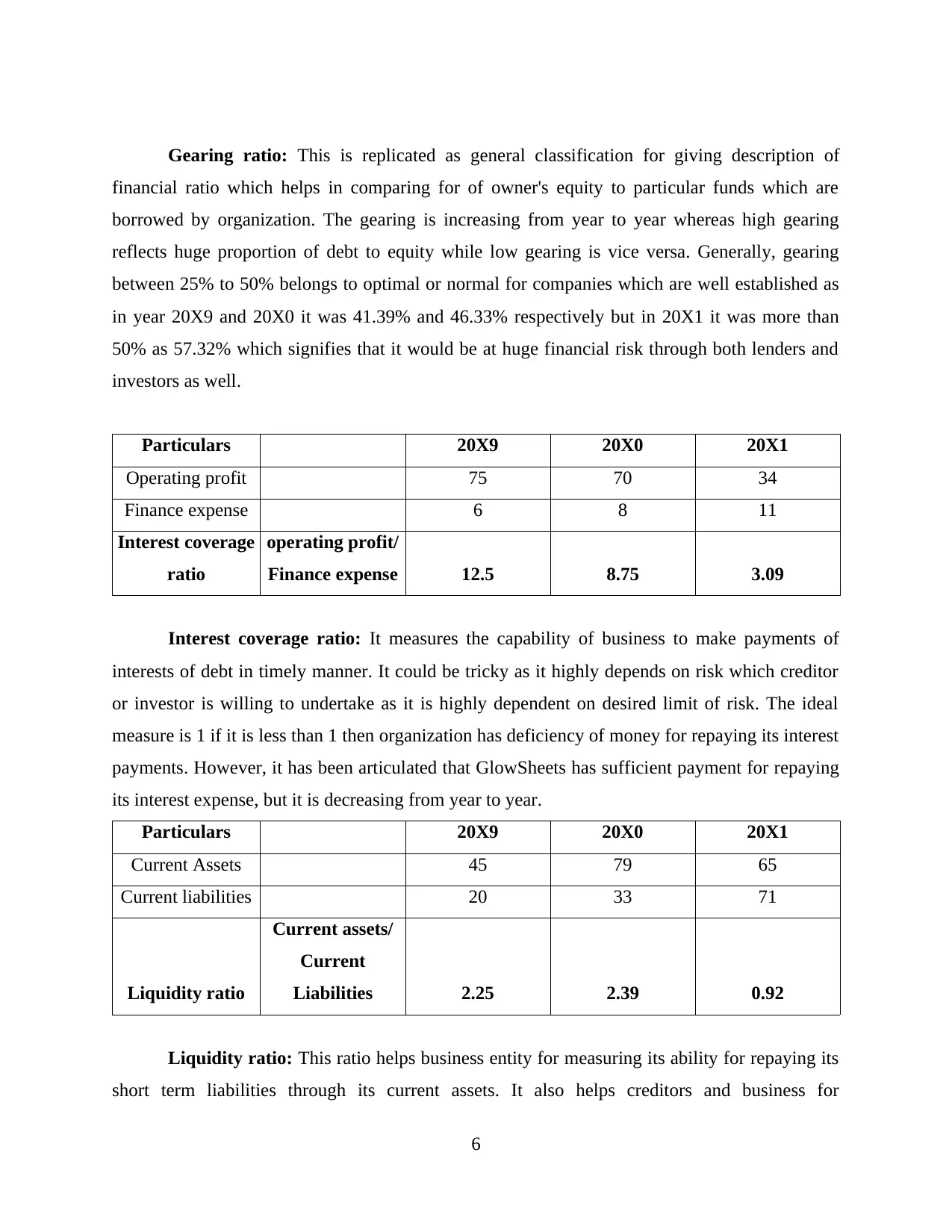

Particulars 20X9 20X0 20X1

Operating profit 75 70 34

Finance expense 6 8 11

Interest coverage

ratio

operating profit/

Finance expense 12.5 8.75 3.09

Interest coverage ratio: It measures the capability of business to make payments of

interests of debt in timely manner. It could be tricky as it highly depends on risk which creditor

or investor is willing to undertake as it is highly dependent on desired limit of risk. The ideal

measure is 1 if it is less than 1 then organization has deficiency of money for repaying its interest

payments. However, it has been articulated that GlowSheets has sufficient payment for repaying

its interest expense, but it is decreasing from year to year.

Particulars 20X9 20X0 20X1

Current Assets 45 79 65

Current liabilities 20 33 71

Liquidity ratio

Current assets/

Current

Liabilities 2.25 2.39 0.92

Liquidity ratio: This ratio helps business entity for measuring its ability for repaying its

short term liabilities through its current assets. It also helps creditors and business for

6

financial ratio which helps in comparing for of owner's equity to particular funds which are

borrowed by organization. The gearing is increasing from year to year whereas high gearing

reflects huge proportion of debt to equity while low gearing is vice versa. Generally, gearing

between 25% to 50% belongs to optimal or normal for companies which are well established as

in year 20X9 and 20X0 it was 41.39% and 46.33% respectively but in 20X1 it was more than

50% as 57.32% which signifies that it would be at huge financial risk through both lenders and

investors as well.

Particulars 20X9 20X0 20X1

Operating profit 75 70 34

Finance expense 6 8 11

Interest coverage

ratio

operating profit/

Finance expense 12.5 8.75 3.09

Interest coverage ratio: It measures the capability of business to make payments of

interests of debt in timely manner. It could be tricky as it highly depends on risk which creditor

or investor is willing to undertake as it is highly dependent on desired limit of risk. The ideal

measure is 1 if it is less than 1 then organization has deficiency of money for repaying its interest

payments. However, it has been articulated that GlowSheets has sufficient payment for repaying

its interest expense, but it is decreasing from year to year.

Particulars 20X9 20X0 20X1

Current Assets 45 79 65

Current liabilities 20 33 71

Liquidity ratio

Current assets/

Current

Liabilities 2.25 2.39 0.92

Liquidity ratio: This ratio helps business entity for measuring its ability for repaying its

short term liabilities through its current assets. It also helps creditors and business for

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

understanding company's liquidity as high current ratio is highly preferable. In 20X9 and 20X0

GlowSheets Ltd has 2 times more current assets as compared to current liabilities which was

good indicator. However, in 20X1 it was less than 1 which shows that GlowSheets Ltd is not

making sufficient through its operations for supporting its activities.

Particulars 20X9 20X0 20X1

Net profit 55 50 18

Shareholders fund 211 241 239

Return on Equity

Net profit/

Shareholders

fund 26.07% 20.75% 7.53%

Return on Equity: It is profitability measure along with capability of business entity for

generating its margin through shareholders' investment. In simple words, it shows return on

equity which shows margin of each amount of common stockholders' equity produced. The

GlpwSheets Ltd return with reference to equity was decreasing from year to year in huge

proportion as it is not growing because of decreasing net profit with huge proportion

(Subalakshmi, Grahalakshmi and Manikandan, 2018).

Particulars 20X9 20X0 20X1

Operating profit 75 70 34

Total debt 149 208 321

Shareholders fund 211 241 239

Return on capital

employed

operating profit/

(total debt +

Shareholders

fund) 20.83% 15.59% 6.07%

Return on capital employed: It is profitability ratio which measure that how

organization is efficiently producing margin through its capital employed as compare to net

operating profit from capital employed. In this measure, higher ratio is preferable but by

observing GlowSheet performance, it returns on capital employed is decreasing with huge

7

GlowSheets Ltd has 2 times more current assets as compared to current liabilities which was

good indicator. However, in 20X1 it was less than 1 which shows that GlowSheets Ltd is not

making sufficient through its operations for supporting its activities.

Particulars 20X9 20X0 20X1

Net profit 55 50 18

Shareholders fund 211 241 239

Return on Equity

Net profit/

Shareholders

fund 26.07% 20.75% 7.53%

Return on Equity: It is profitability measure along with capability of business entity for

generating its margin through shareholders' investment. In simple words, it shows return on

equity which shows margin of each amount of common stockholders' equity produced. The

GlpwSheets Ltd return with reference to equity was decreasing from year to year in huge

proportion as it is not growing because of decreasing net profit with huge proportion

(Subalakshmi, Grahalakshmi and Manikandan, 2018).

Particulars 20X9 20X0 20X1

Operating profit 75 70 34

Total debt 149 208 321

Shareholders fund 211 241 239

Return on capital

employed

operating profit/

(total debt +

Shareholders

fund) 20.83% 15.59% 6.07%

Return on capital employed: It is profitability ratio which measure that how

organization is efficiently producing margin through its capital employed as compare to net

operating profit from capital employed. In this measure, higher ratio is preferable but by

observing GlowSheet performance, it returns on capital employed is decreasing with huge

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

proportion as its total debt and shareholders fund is in appropriate position but its operating

profit has decreased from 70 to 34 which is impacting the returns.

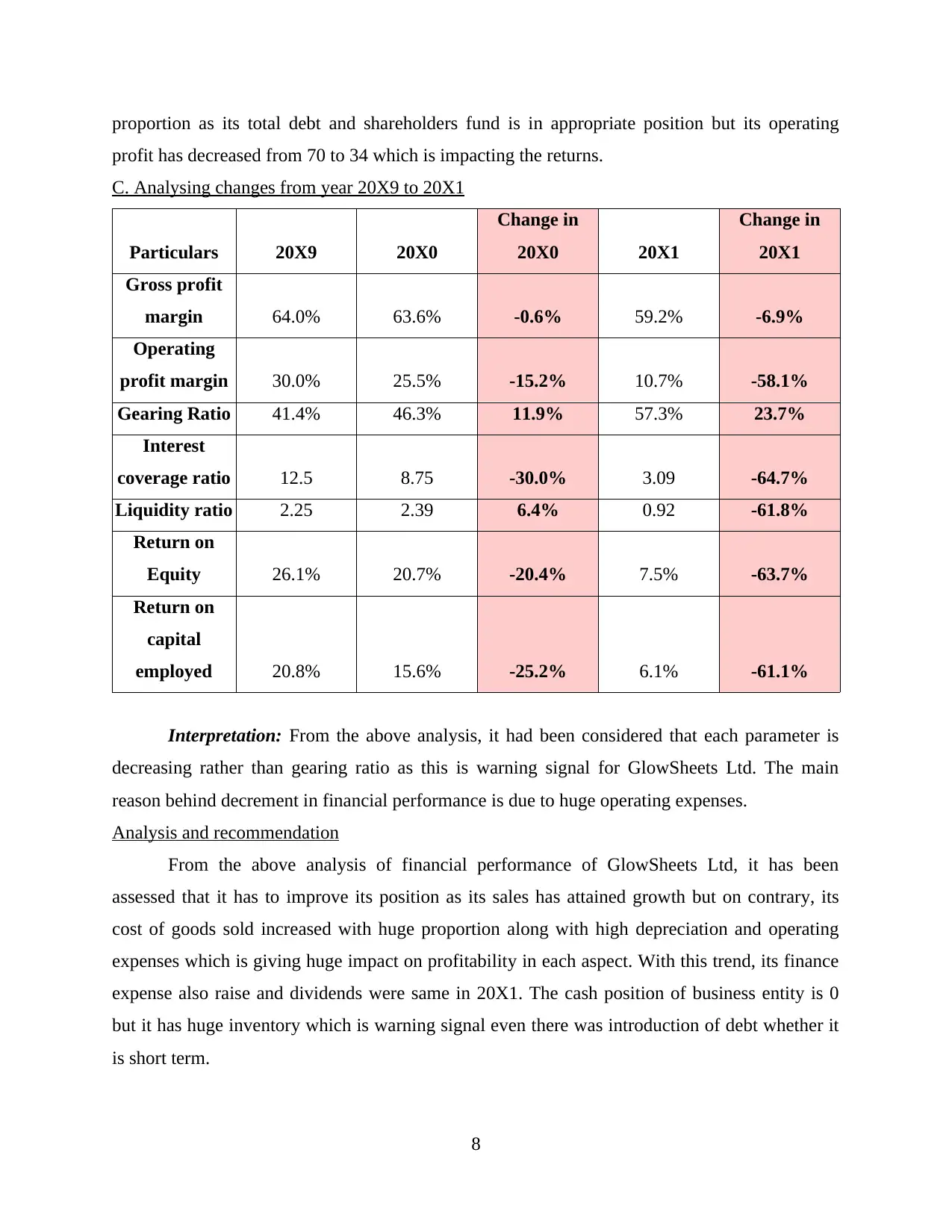

C. Analysing changes from year 20X9 to 20X1

Particulars 20X9 20X0

Change in

20X0 20X1

Change in

20X1

Gross profit

margin 64.0% 63.6% -0.6% 59.2% -6.9%

Operating

profit margin 30.0% 25.5% -15.2% 10.7% -58.1%

Gearing Ratio 41.4% 46.3% 11.9% 57.3% 23.7%

Interest

coverage ratio 12.5 8.75 -30.0% 3.09 -64.7%

Liquidity ratio 2.25 2.39 6.4% 0.92 -61.8%

Return on

Equity 26.1% 20.7% -20.4% 7.5% -63.7%

Return on

capital

employed 20.8% 15.6% -25.2% 6.1% -61.1%

Interpretation: From the above analysis, it had been considered that each parameter is

decreasing rather than gearing ratio as this is warning signal for GlowSheets Ltd. The main

reason behind decrement in financial performance is due to huge operating expenses.

Analysis and recommendation

From the above analysis of financial performance of GlowSheets Ltd, it has been

assessed that it has to improve its position as its sales has attained growth but on contrary, its

cost of goods sold increased with huge proportion along with high depreciation and operating

expenses which is giving huge impact on profitability in each aspect. With this trend, its finance

expense also raise and dividends were same in 20X1. The cash position of business entity is 0

but it has huge inventory which is warning signal even there was introduction of debt whether it

is short term.

8

profit has decreased from 70 to 34 which is impacting the returns.

C. Analysing changes from year 20X9 to 20X1

Particulars 20X9 20X0

Change in

20X0 20X1

Change in

20X1

Gross profit

margin 64.0% 63.6% -0.6% 59.2% -6.9%

Operating

profit margin 30.0% 25.5% -15.2% 10.7% -58.1%

Gearing Ratio 41.4% 46.3% 11.9% 57.3% 23.7%

Interest

coverage ratio 12.5 8.75 -30.0% 3.09 -64.7%

Liquidity ratio 2.25 2.39 6.4% 0.92 -61.8%

Return on

Equity 26.1% 20.7% -20.4% 7.5% -63.7%

Return on

capital

employed 20.8% 15.6% -25.2% 6.1% -61.1%

Interpretation: From the above analysis, it had been considered that each parameter is

decreasing rather than gearing ratio as this is warning signal for GlowSheets Ltd. The main

reason behind decrement in financial performance is due to huge operating expenses.

Analysis and recommendation

From the above analysis of financial performance of GlowSheets Ltd, it has been

assessed that it has to improve its position as its sales has attained growth but on contrary, its

cost of goods sold increased with huge proportion along with high depreciation and operating

expenses which is giving huge impact on profitability in each aspect. With this trend, its finance

expense also raise and dividends were same in 20X1. The cash position of business entity is 0

but it has huge inventory which is warning signal even there was introduction of debt whether it

is short term.

8

Further, it has been recommended that GlowSheets Ltd must control its expenditure

which are incurred with involvement of any activity which is directly linked with productions of

services and goods as they are similar to general, administrative and selling expenses. This action

will give positive impact to the financial performance of GlowSheets Ltd.

CONCLUSION

From the above study it had been concluded that financial statements are very important

for monitoring the performance and to articulate its trends as well. By considering Modern

Garden Designs Ltd, it has been suggested that cash flow could be managed easily with reference

to better working capital. In the similar aspect GlowSheets Ltd has to control its operating

expense which is giving direct impact on profitability.

9

which are incurred with involvement of any activity which is directly linked with productions of

services and goods as they are similar to general, administrative and selling expenses. This action

will give positive impact to the financial performance of GlowSheets Ltd.

CONCLUSION

From the above study it had been concluded that financial statements are very important

for monitoring the performance and to articulate its trends as well. By considering Modern

Garden Designs Ltd, it has been suggested that cash flow could be managed easily with reference

to better working capital. In the similar aspect GlowSheets Ltd has to control its operating

expense which is giving direct impact on profitability.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.