Financing Business Initiatives Report - Finance, DCF and LBO Analysis

VerifiedAdded on 2020/02/12

|23

|5549

|88

Report

AI Summary

This report provides a comprehensive analysis of financing business initiatives, utilizing both the Discounted Cash Flow (DCF) and Leveraged Buyout (LBO) models. It begins with an overview of the finance domain, discussing the acquisition of firms and the importance of financial modeling tools. The report applies the Porter five forces model to the cloud computing industry, assessing the threats and opportunities for potential acquisitions. It then identifies and explains the characteristics of a good LBO candidate, followed by an examination of how a Private Equity (PE) firm can align its interests with the managers of a target company. The report details various debt structures and sources of finance, and includes a detailed DCF model with calculations to determine the intrinsic value of shares. Furthermore, an LBO model is applied to evaluate potential investments, covering exit strategies and private equity fund structures. The analysis includes tables illustrating financial data, such as free cash flow calculations, cost sheets, terminal values, equity values, and debt structures, providing a thorough understanding of the financial aspects of business initiatives.

FINANCING BUSINESS

INITIATIVES

INITIATIVES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1Porter five forces model on cloud computing industry.............................................1

Question 2 Identification and explanation of characteristics of good LBO candidate................2

Question 3 Ways in which PE firm 3M can align its interests to mangers of relevant company 2

Question 4Debt structures and sources of finance......................................................................3

Question 5DCF model and explanation on calculations ............................................................3

LBO model..................................................................................................................................6

Question 7 Exit strategies in LBO ...........................................................................................10

Question 8 Private equity fund structures, fund terms, economic terms and corporate governance terms used by PE firms 11

Reflective.......................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

Question 1Porter five forces model on cloud computing industry.............................................1

Question 2 Identification and explanation of characteristics of good LBO candidate................2

Question 3 Ways in which PE firm 3M can align its interests to mangers of relevant company 2

Question 4Debt structures and sources of finance......................................................................3

Question 5DCF model and explanation on calculations ............................................................3

LBO model..................................................................................................................................6

Question 7 Exit strategies in LBO ...........................................................................................10

Question 8 Private equity fund structures, fund terms, economic terms and corporate governance terms used by PE firms 11

Reflective.......................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Index of Tables

Table 1Calculation of free cash flow...............................................................................................6

Table 2Cost sheet.............................................................................................................................7

Table 3PV at 10% WACC...............................................................................................................7

Table 4Terminal values....................................................................................................................7

Table 5Equity value.........................................................................................................................8

Table 6Intrinsic value of shares.......................................................................................................8

Table 7Financing structure of LBO.................................................................................................9

Table 8Implied debt burden table....................................................................................................9

Table 9Debt split of overall debt amount across years....................................................................9

Table 10Interest rate......................................................................................................................10

Table 11Calculation.......................................................................................................................10

Table 12Calculation of free cash flow...........................................................................................10

Table 13Cash flows calculation.....................................................................................................11

Table 14Cash conversion table......................................................................................................11

Table 15EBITDA and FCF............................................................................................................11

Table 16Debt pay down table........................................................................................................11

Table 17Cash flow available for debt repayment..........................................................................12

Table 18IRR table..........................................................................................................................12

Table 1Calculation of free cash flow...............................................................................................6

Table 2Cost sheet.............................................................................................................................7

Table 3PV at 10% WACC...............................................................................................................7

Table 4Terminal values....................................................................................................................7

Table 5Equity value.........................................................................................................................8

Table 6Intrinsic value of shares.......................................................................................................8

Table 7Financing structure of LBO.................................................................................................9

Table 8Implied debt burden table....................................................................................................9

Table 9Debt split of overall debt amount across years....................................................................9

Table 10Interest rate......................................................................................................................10

Table 11Calculation.......................................................................................................................10

Table 12Calculation of free cash flow...........................................................................................10

Table 13Cash flows calculation.....................................................................................................11

Table 14Cash conversion table......................................................................................................11

Table 15EBITDA and FCF............................................................................................................11

Table 16Debt pay down table........................................................................................................11

Table 17Cash flow available for debt repayment..........................................................................12

Table 18IRR table..........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is the vast domain and number of things are performed under it. Every year number of firms acquired other one across

the globe. There are number of tools that are used by these firms to make decisions like discounted cash flow model and leverage

buyout model. There is great use of both models for the firms. In case of discounted cash flow model real value of shares is computed

and on that basis it is identified whether shares are available at higher or low price. Apart from this, in the report leverage buyout

model is applied on cash flows and on that basis it is identified whether investment must be made in the firm. It can be said that

complex calculations are performed and interpreted in current report.

Question 1Porter five forces model on cloud computing industry

Porter five forces model is the one of the important tool that is used for analysis of industry. There are some components of

this model and same are explained below. New market entrants: There is moderate threat of new entrants for Bottomline Technologies because usually in enter to this

industry one needs to make heavy capital investment. As every firm cannot arrange such amount of money. There are already

large number of giant firms in the mentioned industry and due to this reason it is very difficult for any firm to enter in to this

industry (Cloud computing, 2017). It can be said that if 3M acquired Bottomline technologies then in that case same will be

beneficial for it. This is because there is less threat of new entrants and if same is acquired then in that case firm will have to

compete with existing players only. Bargaining power of suppliers: There is less bargaining power of suppliers in the mentioned industry. There is very tight

competition among firms that are providing cloud related services. Hence, no firm can easily increase price of services in the

market. Hence, it can be said that there is less bargaining power of suppliers in the market. 3M if acquired Bottomline

technologies then it will have less bargaining power. Which means that by innovating existing technology base at rapid rate

firm can accelerate its growth rate.

Finance is the vast domain and number of things are performed under it. Every year number of firms acquired other one across

the globe. There are number of tools that are used by these firms to make decisions like discounted cash flow model and leverage

buyout model. There is great use of both models for the firms. In case of discounted cash flow model real value of shares is computed

and on that basis it is identified whether shares are available at higher or low price. Apart from this, in the report leverage buyout

model is applied on cash flows and on that basis it is identified whether investment must be made in the firm. It can be said that

complex calculations are performed and interpreted in current report.

Question 1Porter five forces model on cloud computing industry

Porter five forces model is the one of the important tool that is used for analysis of industry. There are some components of

this model and same are explained below. New market entrants: There is moderate threat of new entrants for Bottomline Technologies because usually in enter to this

industry one needs to make heavy capital investment. As every firm cannot arrange such amount of money. There are already

large number of giant firms in the mentioned industry and due to this reason it is very difficult for any firm to enter in to this

industry (Cloud computing, 2017). It can be said that if 3M acquired Bottomline technologies then in that case same will be

beneficial for it. This is because there is less threat of new entrants and if same is acquired then in that case firm will have to

compete with existing players only. Bargaining power of suppliers: There is less bargaining power of suppliers in the mentioned industry. There is very tight

competition among firms that are providing cloud related services. Hence, no firm can easily increase price of services in the

market. Hence, it can be said that there is less bargaining power of suppliers in the market. 3M if acquired Bottomline

technologies then it will have less bargaining power. Which means that by innovating existing technology base at rapid rate

firm can accelerate its growth rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bargaining power of buyers: There is high bargaining power of buyers because they have options and on the basis of quality

of service they can switch to any supplier of services. Hence, it can be said that there is high bargaining power of buyers in the

cloud computing market. There is risk in acquisition of Bottomline technologies as number of alternatives are available to the

customers and they can switch anytime to any product. It can be said that it will be very difficult task for the firm to retain its

customers. Threat from substitutes: There is less threat from substitutes in the market because alternatives of the product are not so

available in the market. Means that in large number alternatives of the product are not available in the market. It can be said

that varied firms are making available almost same services in the market. Technology is not changing at very fast rate and due

to this reason there is no substitute of the current services (Latham and Braun, 2011). This is positive point for 3M and by

considering this factor it can take decision to purchase Bottomline technologies.

Threat from new competitors: There is less competition to the existing firms from the newly entered company. This is because

firms that are operating from three or four years have strong infrastructure then those newly enter in the market. It is the

second risk that is associated with the acquisition of Bottomline technologies. In case rivals innovate their services it become

difficult for 3M to gain benefits from LBO deal.

Question 2 Identification and explanation of characteristics of good LBO candidate

Characteristics for good LBO candidate is given below. Consistency in cash flows: If firm to which any company wants to acquire have elevation in cash flows in previous years

consistently. Then in that case relevant firm is good candidate (Ivashina and Kovner 2011). Large amount of tangible assets: Bottomline technologies must be large amount of assets in its business to become best

candidate of LBO for 3M. Assets of purchased company are kept as collateral by 3M while taking loan from market. In case

of service they can switch to any supplier of services. Hence, it can be said that there is high bargaining power of buyers in the

cloud computing market. There is risk in acquisition of Bottomline technologies as number of alternatives are available to the

customers and they can switch anytime to any product. It can be said that it will be very difficult task for the firm to retain its

customers. Threat from substitutes: There is less threat from substitutes in the market because alternatives of the product are not so

available in the market. Means that in large number alternatives of the product are not available in the market. It can be said

that varied firms are making available almost same services in the market. Technology is not changing at very fast rate and due

to this reason there is no substitute of the current services (Latham and Braun, 2011). This is positive point for 3M and by

considering this factor it can take decision to purchase Bottomline technologies.

Threat from new competitors: There is less competition to the existing firms from the newly entered company. This is because

firms that are operating from three or four years have strong infrastructure then those newly enter in the market. It is the

second risk that is associated with the acquisition of Bottomline technologies. In case rivals innovate their services it become

difficult for 3M to gain benefits from LBO deal.

Question 2 Identification and explanation of characteristics of good LBO candidate

Characteristics for good LBO candidate is given below. Consistency in cash flows: If firm to which any company wants to acquire have elevation in cash flows in previous years

consistently. Then in that case relevant firm is good candidate (Ivashina and Kovner 2011). Large amount of tangible assets: Bottomline technologies must be large amount of assets in its business to become best

candidate of LBO for 3M. Assets of purchased company are kept as collateral by 3M while taking loan from market. In case

there are large assets then some of its portion will remain completely in hands of firm by selling which it can good amount of

revenue.

Limited working capital requirements: If in any business working capital requirement is less than it is best candidate because

with small amount same can be operated by any company.

Question 3 Ways in which PE firm 3M can align its interests to mangers of relevant company

There are many ways in which 3M can align its interest with managers of Bottomline technology and under this it can

communicate them that they wants to sale a firm stake so that money can be received for investment in the business. In order to

improve business performance firm needs intellectual capital that invest money in right way (Turco 2010). That capital can be

invested in prudent manner by receiving guidance from the PE firm. Thus, in this way 3M can align its interests with the Bottomline

technology. Apart from this providing a reasonable amount of money to firm in LBO is another incentive that can be provided to

target company managers.

Question 4Debt structures and sources of finance Revolving credit facility (Revolver): Under this approach firm can take debt up to certain limit as specified by the bank and

repay the debt amount when it have surplus cash in its business. This method is used to finance LBO deals at large scale by the

business firms. Bank debt: Debt is also taken from the banks and other financial institutions and under this at specific rate debt is available

which is used to purchase debt of the target bank under LBO deal (Kim and McCue 2012). It is the commonly used source of

finance under LBO deals.

Mezzanine: It is also known as subordinated debt and under this debt is raised from the market in conjunction to senior debt

and it have features of both debt and equity. Along with above it is third alternative that is quite popular among firms.

revenue.

Limited working capital requirements: If in any business working capital requirement is less than it is best candidate because

with small amount same can be operated by any company.

Question 3 Ways in which PE firm 3M can align its interests to mangers of relevant company

There are many ways in which 3M can align its interest with managers of Bottomline technology and under this it can

communicate them that they wants to sale a firm stake so that money can be received for investment in the business. In order to

improve business performance firm needs intellectual capital that invest money in right way (Turco 2010). That capital can be

invested in prudent manner by receiving guidance from the PE firm. Thus, in this way 3M can align its interests with the Bottomline

technology. Apart from this providing a reasonable amount of money to firm in LBO is another incentive that can be provided to

target company managers.

Question 4Debt structures and sources of finance Revolving credit facility (Revolver): Under this approach firm can take debt up to certain limit as specified by the bank and

repay the debt amount when it have surplus cash in its business. This method is used to finance LBO deals at large scale by the

business firms. Bank debt: Debt is also taken from the banks and other financial institutions and under this at specific rate debt is available

which is used to purchase debt of the target bank under LBO deal (Kim and McCue 2012). It is the commonly used source of

finance under LBO deals.

Mezzanine: It is also known as subordinated debt and under this debt is raised from the market in conjunction to senior debt

and it have features of both debt and equity. Along with above it is third alternative that is quite popular among firms.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

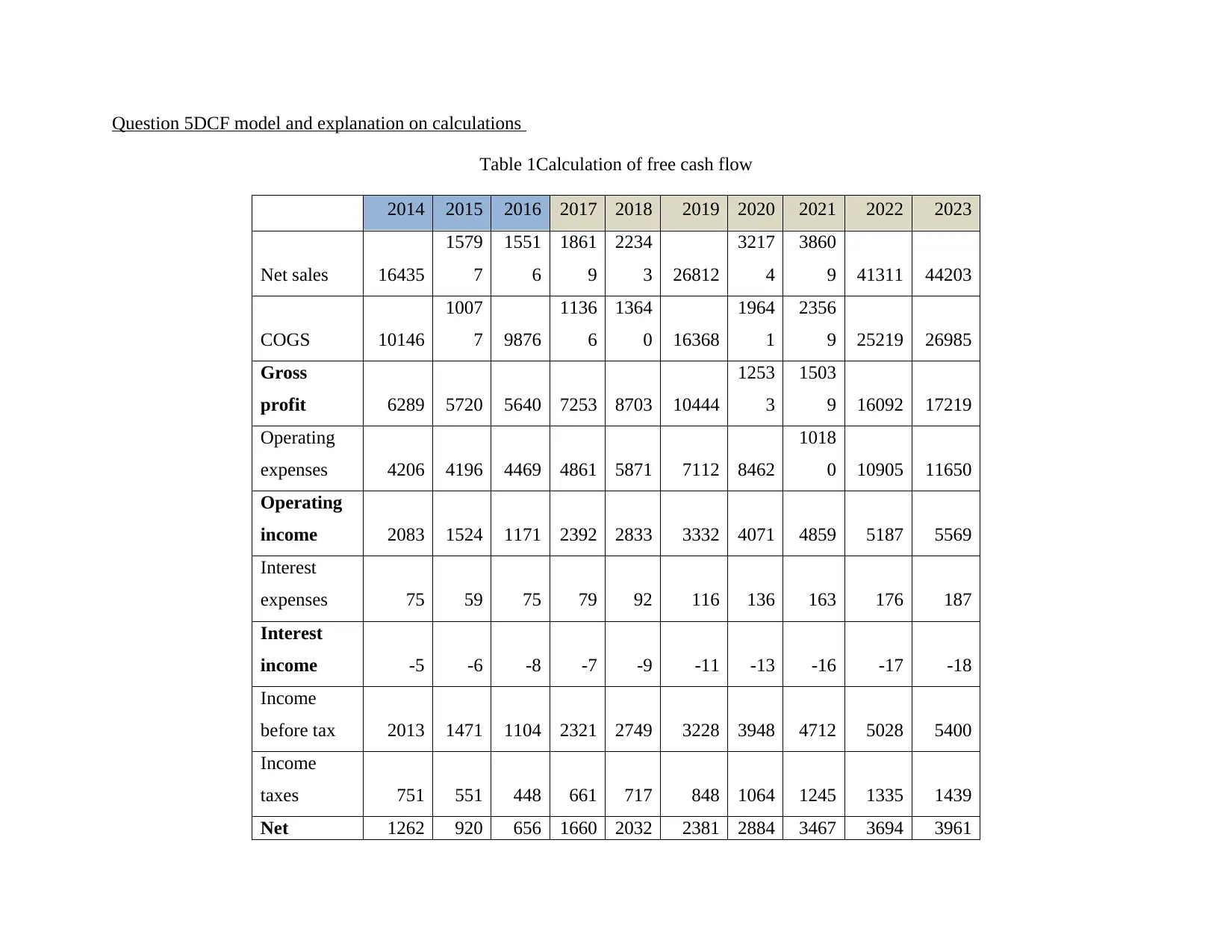

Question 5DCF model and explanation on calculations

Table 1Calculation of free cash flow

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Net sales 16435

1579

7

1551

6

1861

9

2234

3 26812

3217

4

3860

9 41311 44203

COGS 10146

1007

7 9876

1136

6

1364

0 16368

1964

1

2356

9 25219 26985

Gross

profit 6289 5720 5640 7253 8703 10444

1253

3

1503

9 16092 17219

Operating

expenses 4206 4196 4469 4861 5871 7112 8462

1018

0 10905 11650

Operating

income 2083 1524 1171 2392 2833 3332 4071 4859 5187 5569

Interest

expenses 75 59 75 79 92 116 136 163 176 187

Interest

income -5 -6 -8 -7 -9 -11 -13 -16 -17 -18

Income

before tax 2013 1471 1104 2321 2749 3228 3948 4712 5028 5400

Income

taxes 751 551 448 661 717 848 1064 1245 1335 1439

Net 1262 920 656 1660 2032 2381 2884 3467 3694 3961

Table 1Calculation of free cash flow

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Net sales 16435

1579

7

1551

6

1861

9

2234

3 26812

3217

4

3860

9 41311 44203

COGS 10146

1007

7 9876

1136

6

1364

0 16368

1964

1

2356

9 25219 26985

Gross

profit 6289 5720 5640 7253 8703 10444

1253

3

1503

9 16092 17219

Operating

expenses 4206 4196 4469 4861 5871 7112 8462

1018

0 10905 11650

Operating

income 2083 1524 1171 2392 2833 3332 4071 4859 5187 5569

Interest

expenses 75 59 75 79 92 116 136 163 176 187

Interest

income -5 -6 -8 -7 -9 -11 -13 -16 -17 -18

Income

before tax 2013 1471 1104 2321 2749 3228 3948 4712 5028 5400

Income

taxes 751 551 448 661 717 848 1064 1245 1335 1439

Net 1262 920 656 1660 2032 2381 2884 3467 3694 3961

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

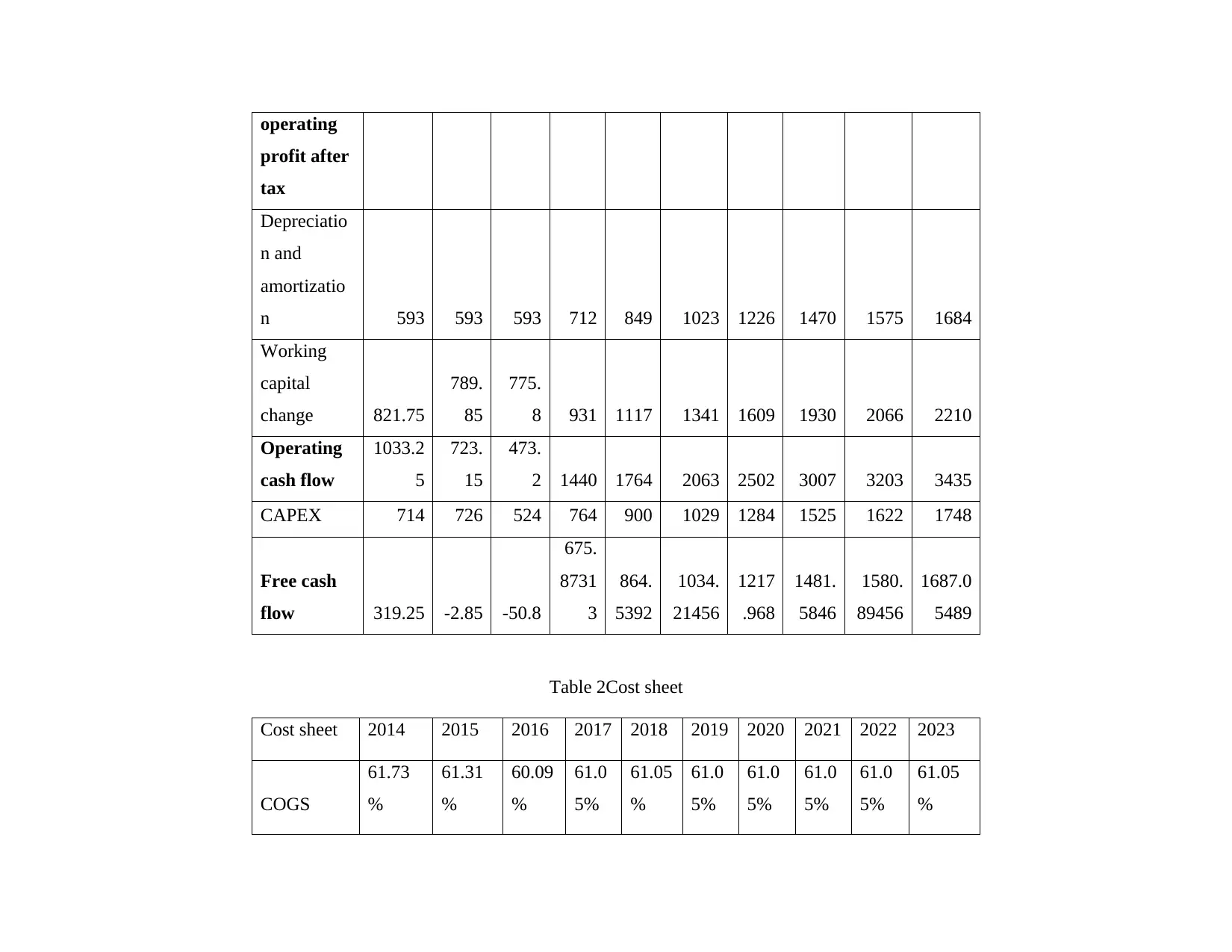

operating

profit after

tax

Depreciatio

n and

amortizatio

n 593 593 593 712 849 1023 1226 1470 1575 1684

Working

capital

change 821.75

789.

85

775.

8 931 1117 1341 1609 1930 2066 2210

Operating

cash flow

1033.2

5

723.

15

473.

2 1440 1764 2063 2502 3007 3203 3435

CAPEX 714 726 524 764 900 1029 1284 1525 1622 1748

Free cash

flow 319.25 -2.85 -50.8

675.

8731

3

864.

5392

1034.

21456

1217

.968

1481.

5846

1580.

89456

1687.0

5489

Table 2Cost sheet

Cost sheet 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

COGS

61.73

%

61.31

%

60.09

%

61.0

5%

61.05

%

61.0

5%

61.0

5%

61.0

5%

61.0

5%

61.05

%

profit after

tax

Depreciatio

n and

amortizatio

n 593 593 593 712 849 1023 1226 1470 1575 1684

Working

capital

change 821.75

789.

85

775.

8 931 1117 1341 1609 1930 2066 2210

Operating

cash flow

1033.2

5

723.

15

473.

2 1440 1764 2063 2502 3007 3203 3435

CAPEX 714 726 524 764 900 1029 1284 1525 1622 1748

Free cash

flow 319.25 -2.85 -50.8

675.

8731

3

864.

5392

1034.

21456

1217

.968

1481.

5846

1580.

89456

1687.0

5489

Table 2Cost sheet

Cost sheet 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

COGS

61.73

%

61.31

%

60.09

%

61.0

5%

61.05

%

61.0

5%

61.0

5%

61.0

5%

61.0

5%

61.05

%

Operating

expenses

25.59

%

25.53

%

27.19

%

26.1

0%

26.28

%

26.5

2%

26.3

0%

26.3

7%

26.4

0%

26.36

%

Interest

expenses 0.46% 0.36%

0.46

%

0.42

%

0.41

%

0.43

%

0.42

%

0.42

%

0.43

% 0.42%

Interest

income -0.03%

-

0.04%

-

0.05

%

-

0.04

%

-

0.04

%

-

0.04

%

-

0.04

%

-

0.04

%

-

0.04

%

-

0.04%

Income

taxes 4.57% 3.35%

2.73

%

3.55

%

3.21

%

3.16

%

3.31

%

3.23

%

3.23

% 3.25%

Depreciatio

n and

amortizatio

n 3.61% 3.75%

3.82

%

3.82

%

3.80

%

3.81

%

3.81

%

3.81

%

3.81

%

0.0381

0577

CAPEX 4.34% 4.60%

3.38

%

4.11

%

4.03

%

3.84

%

3.99

%

3.95

%

3.93

%

0.0395

5239

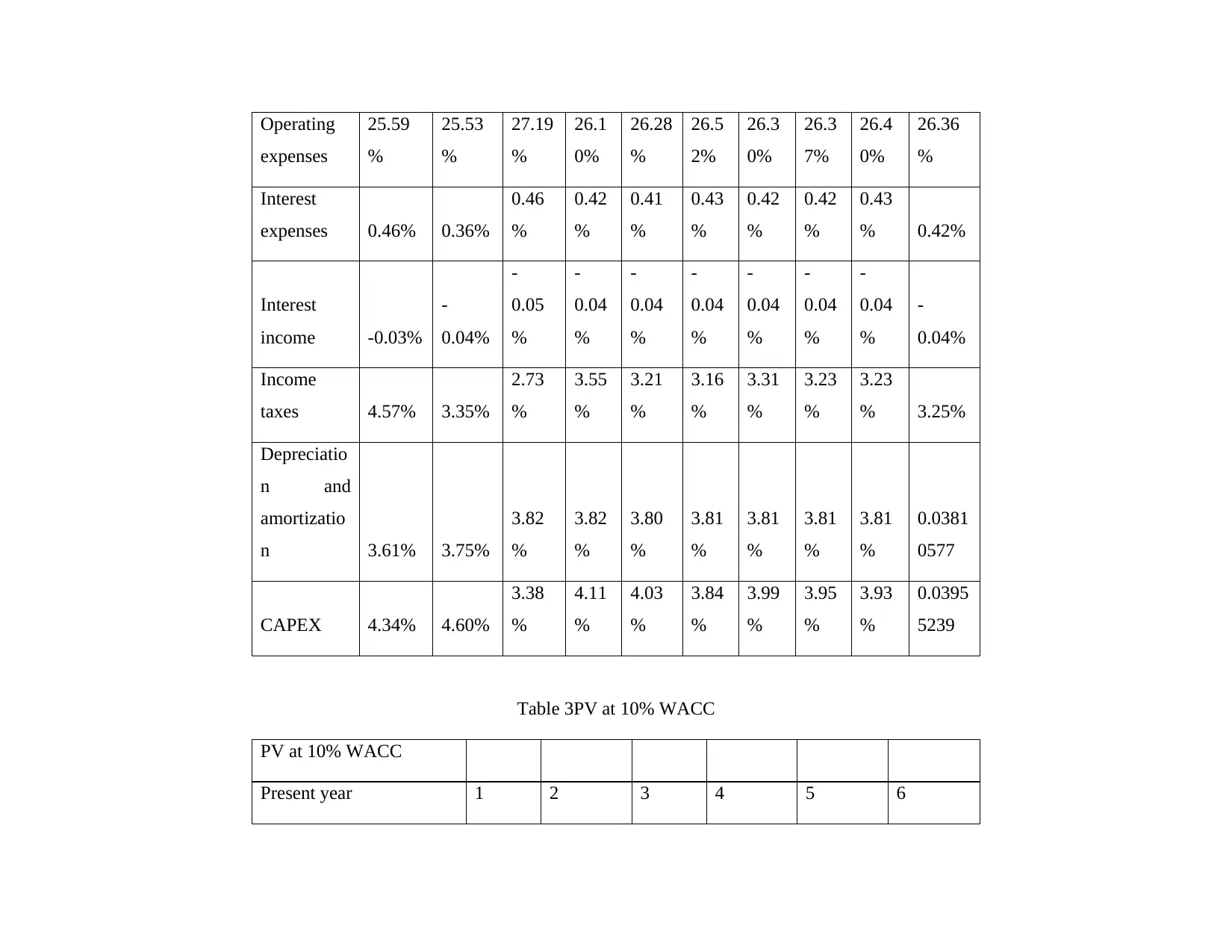

Table 3PV at 10% WACC

PV at 10% WACC

Present year 1 2 3 4 5 6

expenses

25.59

%

25.53

%

27.19

%

26.1

0%

26.28

%

26.5

2%

26.3

0%

26.3

7%

26.4

0%

26.36

%

Interest

expenses 0.46% 0.36%

0.46

%

0.42

%

0.41

%

0.43

%

0.42

%

0.42

%

0.43

% 0.42%

Interest

income -0.03%

-

0.04%

-

0.05

%

-

0.04

%

-

0.04

%

-

0.04

%

-

0.04

%

-

0.04

%

-

0.04

%

-

0.04%

Income

taxes 4.57% 3.35%

2.73

%

3.55

%

3.21

%

3.16

%

3.31

%

3.23

%

3.23

% 3.25%

Depreciatio

n and

amortizatio

n 3.61% 3.75%

3.82

%

3.82

%

3.80

%

3.81

%

3.81

%

3.81

%

3.81

%

0.0381

0577

CAPEX 4.34% 4.60%

3.38

%

4.11

%

4.03

%

3.84

%

3.99

%

3.95

%

3.93

%

0.0395

5239

Table 3PV at 10% WACC

PV at 10% WACC

Present year 1 2 3 4 5 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

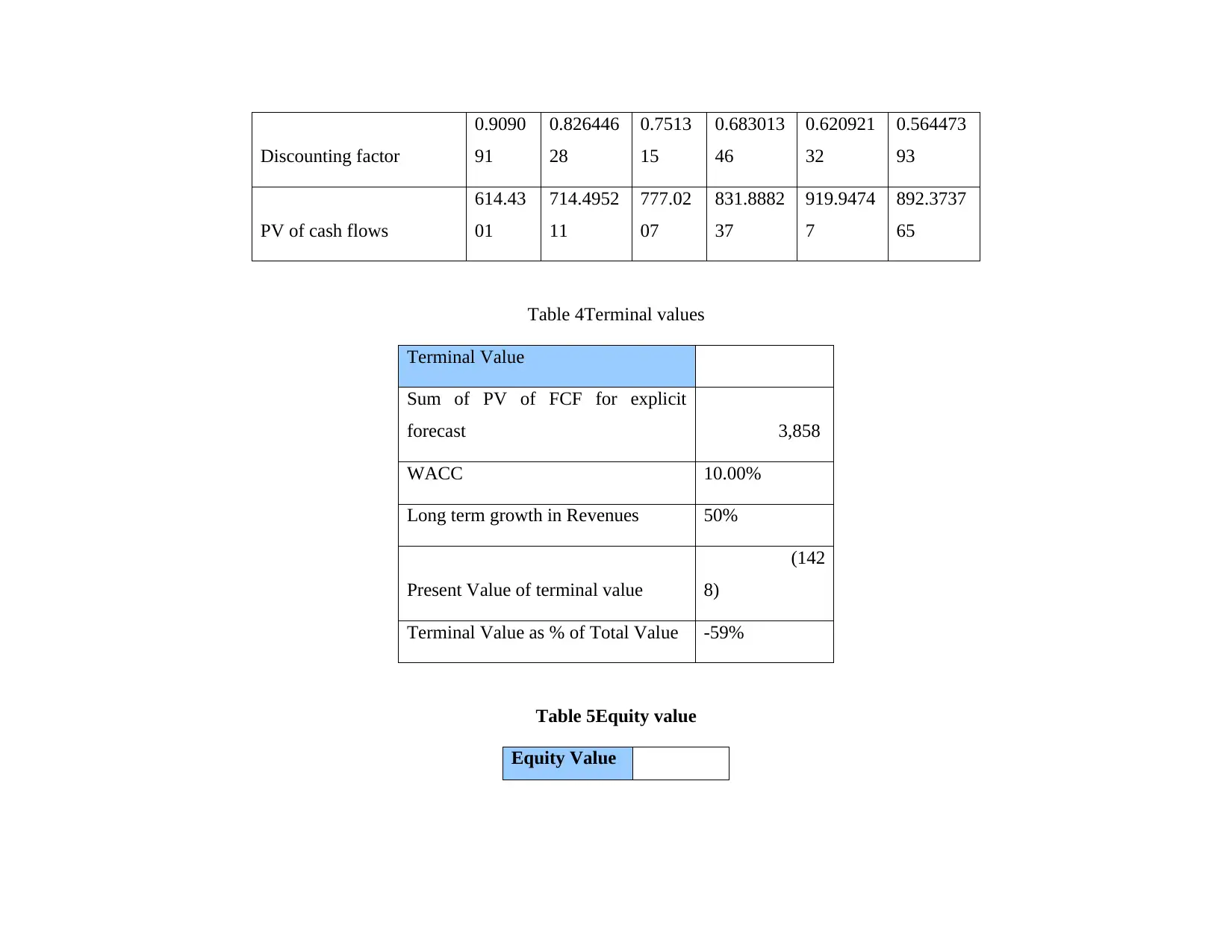

Discounting factor

0.9090

91

0.826446

28

0.7513

15

0.683013

46

0.620921

32

0.564473

93

PV of cash flows

614.43

01

714.4952

11

777.02

07

831.8882

37

919.9474

7

892.3737

65

Table 4Terminal values

Terminal Value

Sum of PV of FCF for explicit

forecast 3,858

WACC 10.00%

Long term growth in Revenues 50%

Present Value of terminal value

(142

8)

Terminal Value as % of Total Value -59%

Table 5Equity value

Equity Value

0.9090

91

0.826446

28

0.7513

15

0.683013

46

0.620921

32

0.564473

93

PV of cash flows

614.43

01

714.4952

11

777.02

07

831.8882

37

919.9474

7

892.3737

65

Table 4Terminal values

Terminal Value

Sum of PV of FCF for explicit

forecast 3,858

WACC 10.00%

Long term growth in Revenues 50%

Present Value of terminal value

(142

8)

Terminal Value as % of Total Value -59%

Table 5Equity value

Equity Value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

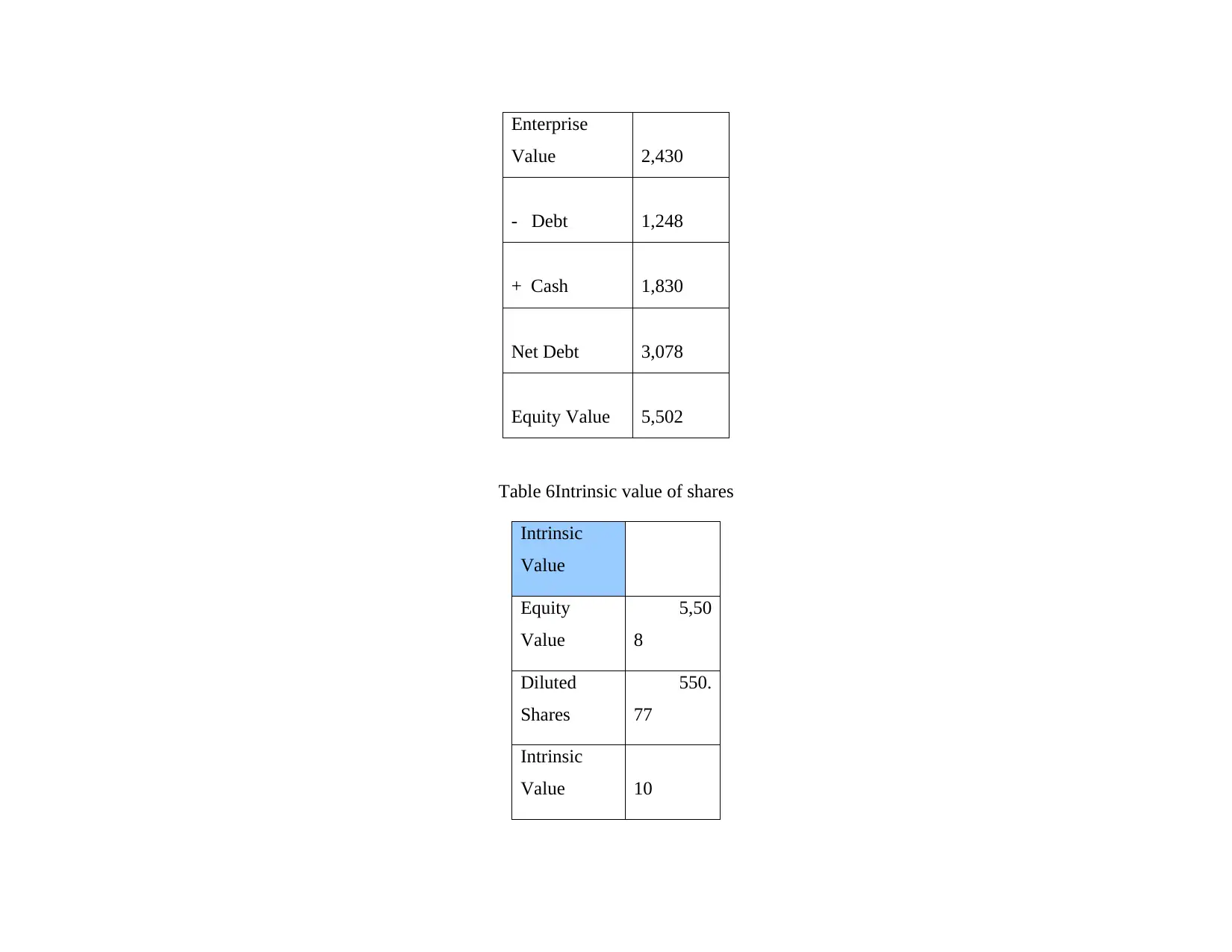

Enterprise

Value 2,430

- Debt 1,248

+ Cash 1,830

Net Debt 3,078

Equity Value 5,502

Table 6Intrinsic value of shares

Intrinsic

Value

Equity

Value

5,50

8

Diluted

Shares

550.

77

Intrinsic

Value 10

Value 2,430

- Debt 1,248

+ Cash 1,830

Net Debt 3,078

Equity Value 5,502

Table 6Intrinsic value of shares

Intrinsic

Value

Equity

Value

5,50

8

Diluted

Shares

550.

77

Intrinsic

Value 10

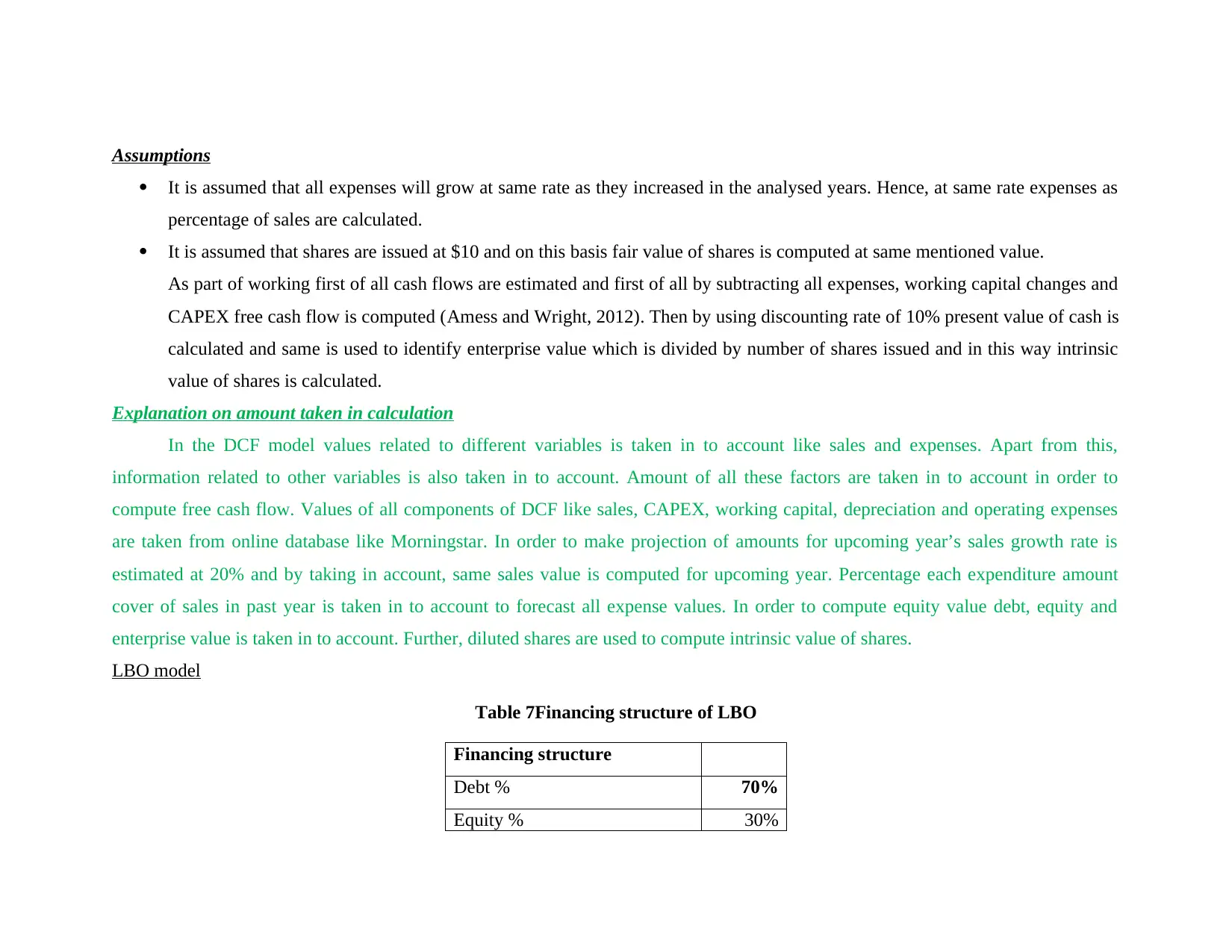

Assumptions

It is assumed that all expenses will grow at same rate as they increased in the analysed years. Hence, at same rate expenses as

percentage of sales are calculated.

It is assumed that shares are issued at $10 and on this basis fair value of shares is computed at same mentioned value.

As part of working first of all cash flows are estimated and first of all by subtracting all expenses, working capital changes and

CAPEX free cash flow is computed (Amess and Wright, 2012). Then by using discounting rate of 10% present value of cash is

calculated and same is used to identify enterprise value which is divided by number of shares issued and in this way intrinsic

value of shares is calculated.

Explanation on amount taken in calculation

In the DCF model values related to different variables is taken in to account like sales and expenses. Apart from this,

information related to other variables is also taken in to account. Amount of all these factors are taken in to account in order to

compute free cash flow. Values of all components of DCF like sales, CAPEX, working capital, depreciation and operating expenses

are taken from online database like Morningstar. In order to make projection of amounts for upcoming year’s sales growth rate is

estimated at 20% and by taking in account, same sales value is computed for upcoming year. Percentage each expenditure amount

cover of sales in past year is taken in to account to forecast all expense values. In order to compute equity value debt, equity and

enterprise value is taken in to account. Further, diluted shares are used to compute intrinsic value of shares.

LBO model

Table 7Financing structure of LBO

Financing structure

Debt % 70%

Equity % 30%

It is assumed that all expenses will grow at same rate as they increased in the analysed years. Hence, at same rate expenses as

percentage of sales are calculated.

It is assumed that shares are issued at $10 and on this basis fair value of shares is computed at same mentioned value.

As part of working first of all cash flows are estimated and first of all by subtracting all expenses, working capital changes and

CAPEX free cash flow is computed (Amess and Wright, 2012). Then by using discounting rate of 10% present value of cash is

calculated and same is used to identify enterprise value which is divided by number of shares issued and in this way intrinsic

value of shares is calculated.

Explanation on amount taken in calculation

In the DCF model values related to different variables is taken in to account like sales and expenses. Apart from this,

information related to other variables is also taken in to account. Amount of all these factors are taken in to account in order to

compute free cash flow. Values of all components of DCF like sales, CAPEX, working capital, depreciation and operating expenses

are taken from online database like Morningstar. In order to make projection of amounts for upcoming year’s sales growth rate is

estimated at 20% and by taking in account, same sales value is computed for upcoming year. Percentage each expenditure amount

cover of sales in past year is taken in to account to forecast all expense values. In order to compute equity value debt, equity and

enterprise value is taken in to account. Further, diluted shares are used to compute intrinsic value of shares.

LBO model

Table 7Financing structure of LBO

Financing structure

Debt % 70%

Equity % 30%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.