Group Report: WACC Calculation, Investment Selection, and Analysis

VerifiedAdded on 2020/09/17

|28

|5086

|31

Report

AI Summary

This group report delves into the financial analysis of a parent company, focusing on the calculation of the Weighted Average Cost of Capital (WACC) and its adjustment for country-specific risks. The report begins by identifying the risk-free rate and calculating the WACC using data such as share prices, beta, tax rates, and interest rates for various debt instruments. The market value of each component (equity and debt) is calculated, and the weight of each item is determined to compute the WACC. The Capital Asset Pricing Model (CAPM) is applied to calculate the cost of equity. The report then addresses the need to adjust the WACC to account for the Country Risk Premium (CRP) when considering investments in Vietnam. This includes an analysis of factors contributing to the CRP, such as land clearance delays, currency fluctuations, sovereign debt, and unclear government regulations. The CRP is calculated using a specific formula, incorporating sovereign debt yields and market volatility data. The final WACC is adjusted by incorporating the CRP to reflect the increased risk associated with investments in Vietnam. The report provides a detailed breakdown of all calculations and assumptions, including the effective annual rates and weighted costs of each component, providing a comprehensive financial analysis.

Business Finance – Group Report May 12, 2019

WACC Calculation, Investment Selection and Asset Pricing Model analysis

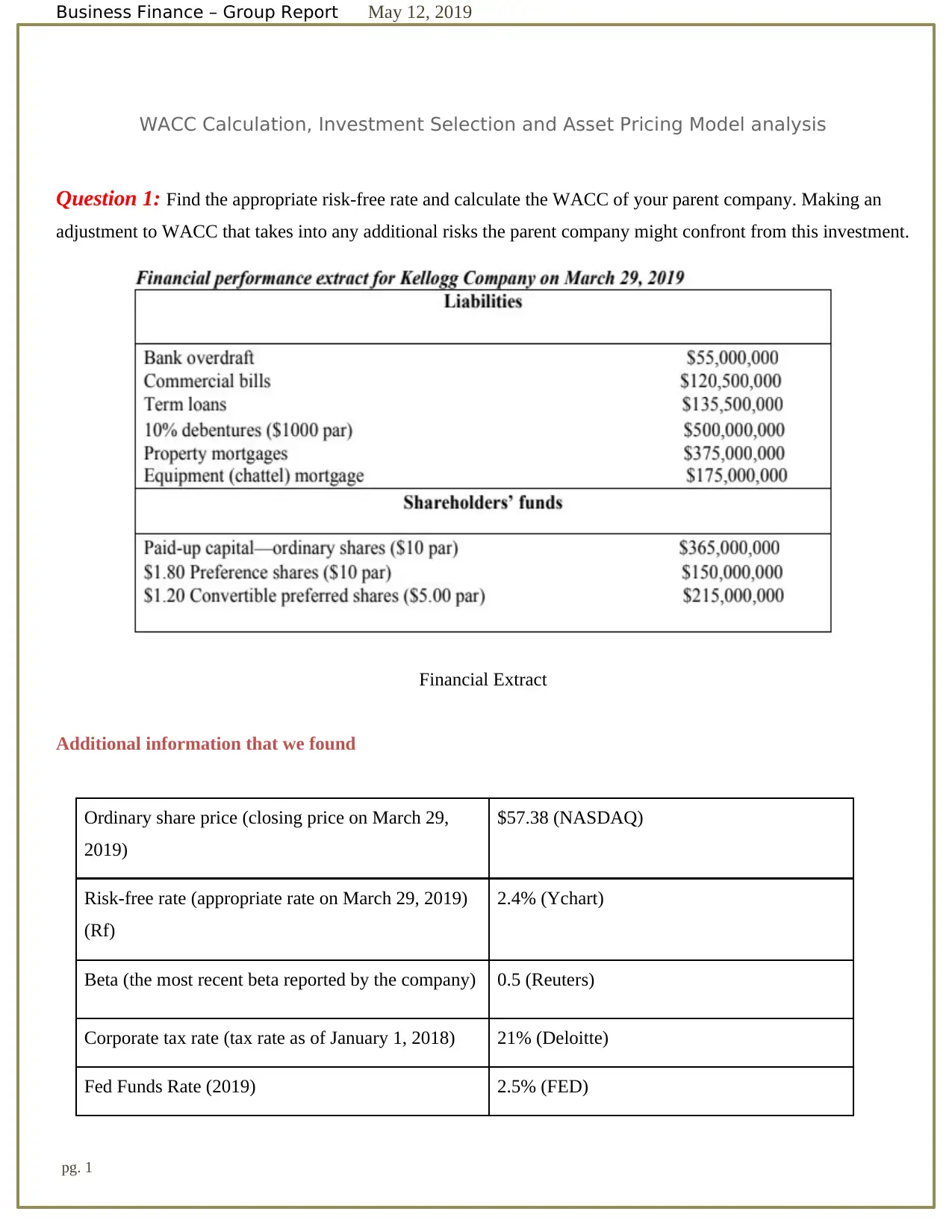

Question 1: Find the appropriate risk-free rate and calculate the WACC of your parent company. Making an

adjustment to WACC that takes into any additional risks the parent company might confront from this investment.

Financial Extract

Additional information that we found

Ordinary share price (closing price on March 29,

2019)

$57.38 (NASDAQ)

Risk-free rate (appropriate rate on March 29, 2019)

(Rf)

2.4% (Ychart)

Beta (the most recent beta reported by the company) 0.5 (Reuters)

Corporate tax rate (tax rate as of January 1, 2018) 21% (Deloitte)

Fed Funds Rate (2019) 2.5% (FED)

pg. 1

WACC Calculation, Investment Selection and Asset Pricing Model analysis

Question 1: Find the appropriate risk-free rate and calculate the WACC of your parent company. Making an

adjustment to WACC that takes into any additional risks the parent company might confront from this investment.

Financial Extract

Additional information that we found

Ordinary share price (closing price on March 29,

2019)

$57.38 (NASDAQ)

Risk-free rate (appropriate rate on March 29, 2019)

(Rf)

2.4% (Ychart)

Beta (the most recent beta reported by the company) 0.5 (Reuters)

Corporate tax rate (tax rate as of January 1, 2018) 21% (Deloitte)

Fed Funds Rate (2019) 2.5% (FED)

pg. 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance – Group Report May 12, 2019

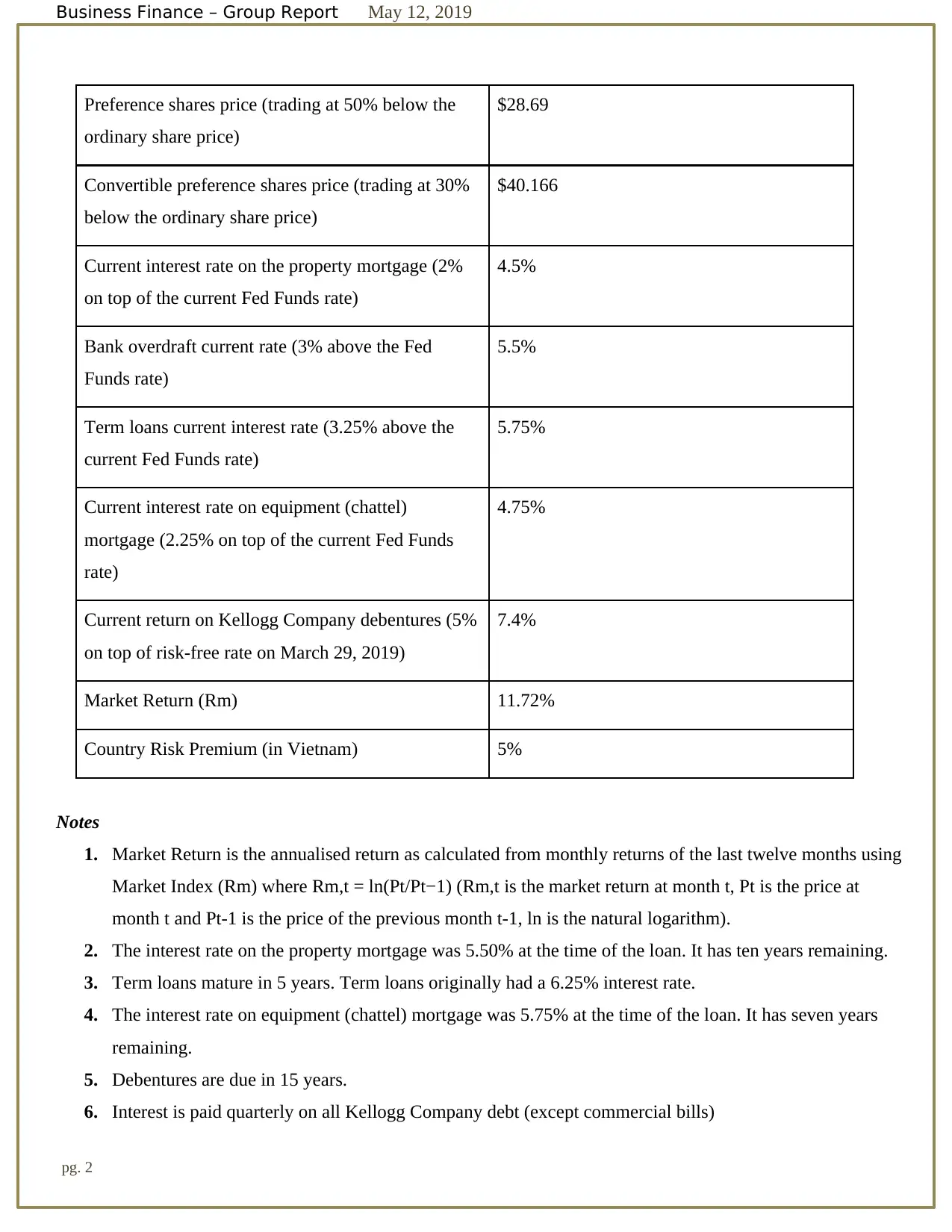

Preference shares price (trading at 50% below the

ordinary share price)

$28.69

Convertible preference shares price (trading at 30%

below the ordinary share price)

$40.166

Current interest rate on the property mortgage (2%

on top of the current Fed Funds rate)

4.5%

Bank overdraft current rate (3% above the Fed

Funds rate)

5.5%

Term loans current interest rate (3.25% above the

current Fed Funds rate)

5.75%

Current interest rate on equipment (chattel)

mortgage (2.25% on top of the current Fed Funds

rate)

4.75%

Current return on Kellogg Company debentures (5%

on top of risk-free rate on March 29, 2019)

7.4%

Market Return (Rm) 11.72%

Country Risk Premium (in Vietnam) 5%

Notes

1. Market Return is the annualised return as calculated from monthly returns of the last twelve months using

Market Index (Rm) where Rm,t = ln(Pt/Pt−1) (Rm,t is the market return at month t, Pt is the price at

month t and Pt-1 is the price of the previous month t-1, ln is the natural logarithm).

2. The interest rate on the property mortgage was 5.50% at the time of the loan. It has ten years remaining.

3. Term loans mature in 5 years. Term loans originally had a 6.25% interest rate.

4. The interest rate on equipment (chattel) mortgage was 5.75% at the time of the loan. It has seven years

remaining.

5. Debentures are due in 15 years.

6. Interest is paid quarterly on all Kellogg Company debt (except commercial bills)

pg. 2

Preference shares price (trading at 50% below the

ordinary share price)

$28.69

Convertible preference shares price (trading at 30%

below the ordinary share price)

$40.166

Current interest rate on the property mortgage (2%

on top of the current Fed Funds rate)

4.5%

Bank overdraft current rate (3% above the Fed

Funds rate)

5.5%

Term loans current interest rate (3.25% above the

current Fed Funds rate)

5.75%

Current interest rate on equipment (chattel)

mortgage (2.25% on top of the current Fed Funds

rate)

4.75%

Current return on Kellogg Company debentures (5%

on top of risk-free rate on March 29, 2019)

7.4%

Market Return (Rm) 11.72%

Country Risk Premium (in Vietnam) 5%

Notes

1. Market Return is the annualised return as calculated from monthly returns of the last twelve months using

Market Index (Rm) where Rm,t = ln(Pt/Pt−1) (Rm,t is the market return at month t, Pt is the price at

month t and Pt-1 is the price of the previous month t-1, ln is the natural logarithm).

2. The interest rate on the property mortgage was 5.50% at the time of the loan. It has ten years remaining.

3. Term loans mature in 5 years. Term loans originally had a 6.25% interest rate.

4. The interest rate on equipment (chattel) mortgage was 5.75% at the time of the loan. It has seven years

remaining.

5. Debentures are due in 15 years.

6. Interest is paid quarterly on all Kellogg Company debt (except commercial bills)

pg. 2

Business Finance – Group Report May 12, 2019

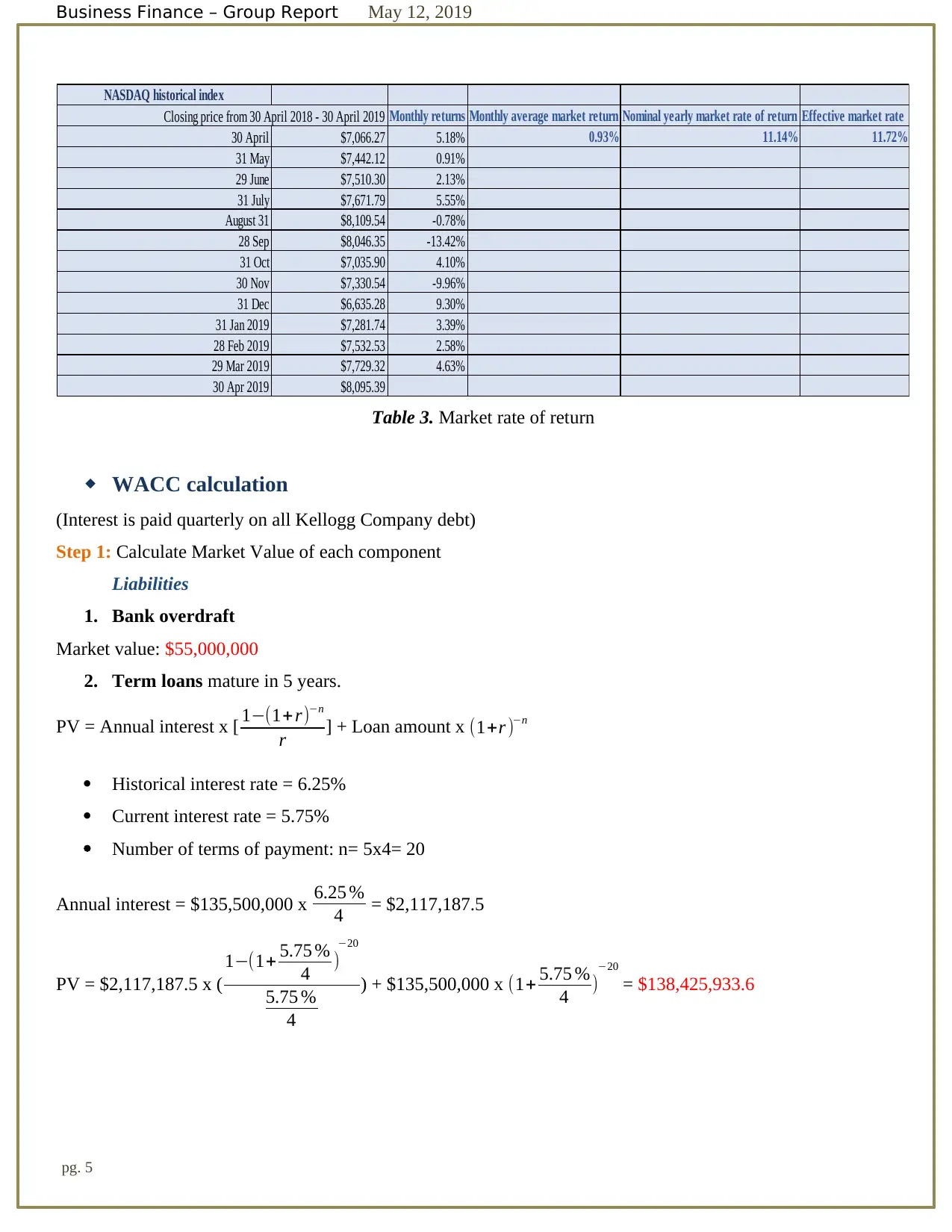

★ Market Return Calculation

We select the closing price of stocks on NASDAQ stock market for 1 year (from 30 April 2018 to 30 April

2019) (Yahoo Finance)

NASDAQ historical index

30 April $7,066.27

31 May $7,442.12

29 June $7,510.30

31 July $7,671.79

August 31 $8,109.54

28 Sep $8,046.35

31 Oct $7,035.90

30 Nov $7,330.54

31 Dec $6,635.28

31 Jan 2019 $7,281.74

28 Feb 2019 $7,532.53

29 Mar 2019 $7,729.32

30 Apr 2019 $8,095.39

Closing price from 30 April 2018 - 30 April 2019

Table 1. Closing price of stocks on NASDAQ stock market for 1 year

- Formula of Log Return to calculate monthly returns

pg. 3

★ Market Return Calculation

We select the closing price of stocks on NASDAQ stock market for 1 year (from 30 April 2018 to 30 April

2019) (Yahoo Finance)

NASDAQ historical index

30 April $7,066.27

31 May $7,442.12

29 June $7,510.30

31 July $7,671.79

August 31 $8,109.54

28 Sep $8,046.35

31 Oct $7,035.90

30 Nov $7,330.54

31 Dec $6,635.28

31 Jan 2019 $7,281.74

28 Feb 2019 $7,532.53

29 Mar 2019 $7,729.32

30 Apr 2019 $8,095.39

Closing price from 30 April 2018 - 30 April 2019

Table 1. Closing price of stocks on NASDAQ stock market for 1 year

- Formula of Log Return to calculate monthly returns

pg. 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Finance – Group Report May 12, 2019

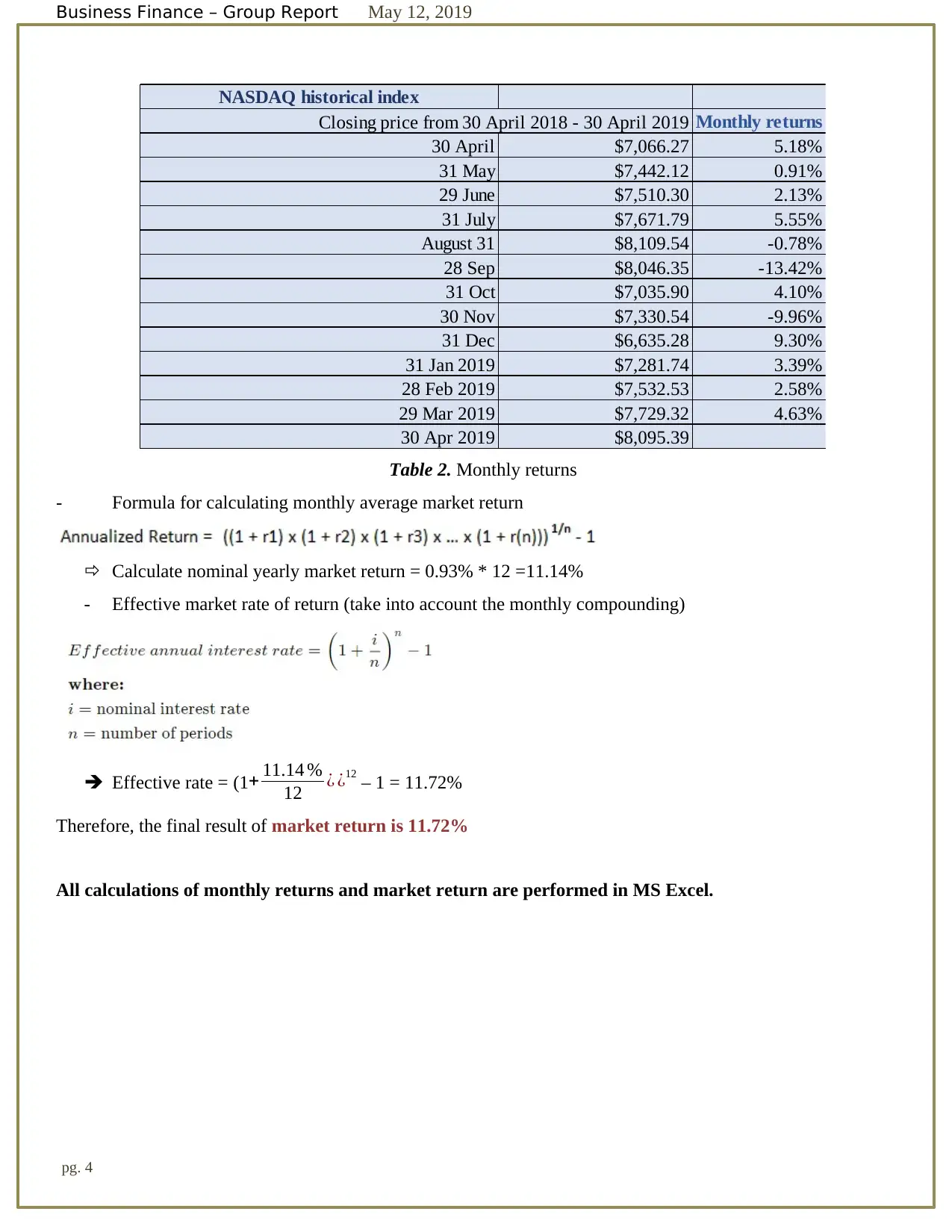

NASDAQ historical index

Monthly returns

30 April $7,066.27 5.18%

31 May $7,442.12 0.91%

29 June $7,510.30 2.13%

31 July $7,671.79 5.55%

August 31 $8,109.54 -0.78%

28 Sep $8,046.35 -13.42%

31 Oct $7,035.90 4.10%

30 Nov $7,330.54 -9.96%

31 Dec $6,635.28 9.30%

31 Jan 2019 $7,281.74 3.39%

28 Feb 2019 $7,532.53 2.58%

29 Mar 2019 $7,729.32 4.63%

30 Apr 2019 $8,095.39

Closing price from 30 April 2018 - 30 April 2019

Table 2. Monthly returns

- Formula for calculating monthly average market return

Calculate nominal yearly market return = 0.93% * 12 =11.14%

- Effective market rate of return (take into account the monthly compounding)

Effective rate = (1+ 11.14 %

12 ¿ ¿12

– 1 = 11.72%

Therefore, the final result of market return is 11.72%

All calculations of monthly returns and market return are performed in MS Excel.

pg. 4

NASDAQ historical index

Monthly returns

30 April $7,066.27 5.18%

31 May $7,442.12 0.91%

29 June $7,510.30 2.13%

31 July $7,671.79 5.55%

August 31 $8,109.54 -0.78%

28 Sep $8,046.35 -13.42%

31 Oct $7,035.90 4.10%

30 Nov $7,330.54 -9.96%

31 Dec $6,635.28 9.30%

31 Jan 2019 $7,281.74 3.39%

28 Feb 2019 $7,532.53 2.58%

29 Mar 2019 $7,729.32 4.63%

30 Apr 2019 $8,095.39

Closing price from 30 April 2018 - 30 April 2019

Table 2. Monthly returns

- Formula for calculating monthly average market return

Calculate nominal yearly market return = 0.93% * 12 =11.14%

- Effective market rate of return (take into account the monthly compounding)

Effective rate = (1+ 11.14 %

12 ¿ ¿12

– 1 = 11.72%

Therefore, the final result of market return is 11.72%

All calculations of monthly returns and market return are performed in MS Excel.

pg. 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance – Group Report May 12, 2019

NASDAQ historical index

Monthly returns Monthly average market return Nominal yearly market rate of return Effective market rate

30 April $7,066.27 5.18% 0.93% 11.14% 11.72%

31 May $7,442.12 0.91%

29 June $7,510.30 2.13%

31 July $7,671.79 5.55%

August 31 $8,109.54 -0.78%

28 Sep $8,046.35 -13.42%

31 Oct $7,035.90 4.10%

30 Nov $7,330.54 -9.96%

31 Dec $6,635.28 9.30%

31 Jan 2019 $7,281.74 3.39%

28 Feb 2019 $7,532.53 2.58%

29 Mar 2019 $7,729.32 4.63%

30 Apr 2019 $8,095.39

Closing price from 30 April 2018 - 30 April 2019

Table 3. Market rate of return

WACC calculation

(Interest is paid quarterly on all Kellogg Company debt)

Step 1: Calculate Market Value of each component

Liabilities

1. Bank overdraft

Market value: $55,000,000

2. Term loans mature in 5 years.

PV = Annual interest x [ 1−(1+ r)−n

r ] + Loan amount x (1+r )−n

Historical interest rate = 6.25%

Current interest rate = 5.75%

Number of terms of payment: n= 5x4= 20

Annual interest = $135,500,000 x 6.25 %

4 = $2,117,187.5

PV = $2,117,187.5 x (

1−(1+ 5.75 %

4 )

−20

5.75 %

4

) + $135,500,000 x (1+ 5.75 %

4 )

−20

= $138,425,933.6

pg. 5

NASDAQ historical index

Monthly returns Monthly average market return Nominal yearly market rate of return Effective market rate

30 April $7,066.27 5.18% 0.93% 11.14% 11.72%

31 May $7,442.12 0.91%

29 June $7,510.30 2.13%

31 July $7,671.79 5.55%

August 31 $8,109.54 -0.78%

28 Sep $8,046.35 -13.42%

31 Oct $7,035.90 4.10%

30 Nov $7,330.54 -9.96%

31 Dec $6,635.28 9.30%

31 Jan 2019 $7,281.74 3.39%

28 Feb 2019 $7,532.53 2.58%

29 Mar 2019 $7,729.32 4.63%

30 Apr 2019 $8,095.39

Closing price from 30 April 2018 - 30 April 2019

Table 3. Market rate of return

WACC calculation

(Interest is paid quarterly on all Kellogg Company debt)

Step 1: Calculate Market Value of each component

Liabilities

1. Bank overdraft

Market value: $55,000,000

2. Term loans mature in 5 years.

PV = Annual interest x [ 1−(1+ r)−n

r ] + Loan amount x (1+r )−n

Historical interest rate = 6.25%

Current interest rate = 5.75%

Number of terms of payment: n= 5x4= 20

Annual interest = $135,500,000 x 6.25 %

4 = $2,117,187.5

PV = $2,117,187.5 x (

1−(1+ 5.75 %

4 )

−20

5.75 %

4

) + $135,500,000 x (1+ 5.75 %

4 )

−20

= $138,425,933.6

pg. 5

Business Finance – Group Report May 12, 2019

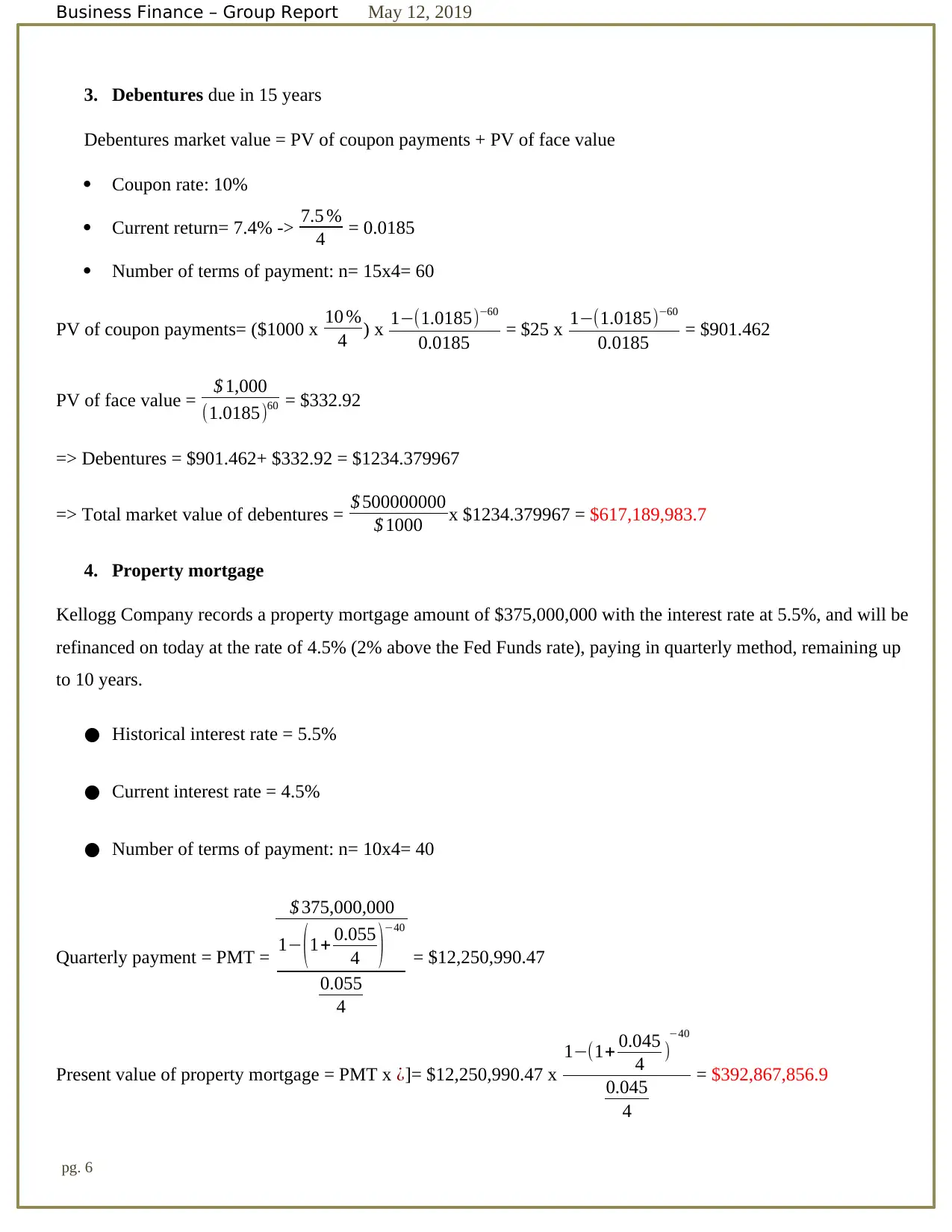

3. Debentures due in 15 years

Debentures market value = PV of coupon payments + PV of face value

Coupon rate: 10%

Current return= 7.4% -> 7.5 %

4 = 0.0185

Number of terms of payment: n= 15x4= 60

PV of coupon payments= ($1000 x 10 %

4 ) x 1−(1.0185)−60

0.0185 = $25 x 1−(1.0185)−60

0.0185 = $901.462

PV of face value = $ 1,000

(1.0185)60 = $332.92

=> Debentures = $901.462+ $332.92 = $1234.379967

=> Total market value of debentures = $ 500000000

$ 1000 x $1234.379967 = $617,189,983.7

4. Property mortgage

Kellogg Company records a property mortgage amount of $375,000,000 with the interest rate at 5.5%, and will be

refinanced on today at the rate of 4.5% (2% above the Fed Funds rate), paying in quarterly method, remaining up

to 10 years.

● Historical interest rate = 5.5%

● Current interest rate = 4.5%

● Number of terms of payment: n= 10x4= 40

Quarterly payment = PMT =

$ 375,000,000

1− ( 1+ 0.055

4 )

−40

0.055

4

= $12,250,990.47

Present value of property mortgage = PMT x ¿]= $12,250,990.47 x

1−(1+ 0.045

4 )

−40

0.045

4

= $392,867,856.9

pg. 6

3. Debentures due in 15 years

Debentures market value = PV of coupon payments + PV of face value

Coupon rate: 10%

Current return= 7.4% -> 7.5 %

4 = 0.0185

Number of terms of payment: n= 15x4= 60

PV of coupon payments= ($1000 x 10 %

4 ) x 1−(1.0185)−60

0.0185 = $25 x 1−(1.0185)−60

0.0185 = $901.462

PV of face value = $ 1,000

(1.0185)60 = $332.92

=> Debentures = $901.462+ $332.92 = $1234.379967

=> Total market value of debentures = $ 500000000

$ 1000 x $1234.379967 = $617,189,983.7

4. Property mortgage

Kellogg Company records a property mortgage amount of $375,000,000 with the interest rate at 5.5%, and will be

refinanced on today at the rate of 4.5% (2% above the Fed Funds rate), paying in quarterly method, remaining up

to 10 years.

● Historical interest rate = 5.5%

● Current interest rate = 4.5%

● Number of terms of payment: n= 10x4= 40

Quarterly payment = PMT =

$ 375,000,000

1− ( 1+ 0.055

4 )

−40

0.055

4

= $12,250,990.47

Present value of property mortgage = PMT x ¿]= $12,250,990.47 x

1−(1+ 0.045

4 )

−40

0.045

4

= $392,867,856.9

pg. 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Finance – Group Report May 12, 2019

pg. 7

pg. 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance – Group Report May 12, 2019

5. Equipment mortgage

Kellogg Company records an equipment mortgage amount of $175,000,000 with the interest rate at 5.75%, and

will be refinanced on today at the rate of 4.75% (2.25% above the Fed Funds rate), paying in quarterly method,

remaining up to 7 years.

● Historical interest rate = 5.75%

● Current interest rate = 4.75%

● Number of terms of payment: n= 7x4= 28

Quarterly payment = PMT =

$ 175,000,000

1−(1+ 0.05755

4 )

−28

0.0575

4

= $7,636,182.89

Present value of equipment mortgage = PMT x ¿] = $7,636,182.89 x

1−(1+ 0.0475

4 )

−28

0.0475

4

= $180,995,408.2

Equity

Ordinary shares = $ 365,000,000

10 x $57.38 = $2,094,370,000

Preference shares = $ 150,000,000

10 x $ 57.38

2 = $430,350,000

Convertible preferred shares = $ 215,0000,000

5 x ($57.38 x 70%) = $1,727,138,000

Step 2: Calculate total value of those items

- Total market value = Total market value of equity + Total market value of debt

= ($2,094,370,000.00 + $430,350,000.00 + $1,727,138,000.00) + ($55,000,000.00 + $138,425,933.60 +

$617,189,983.70 + $392,867,856.90 + $180,995,408.20)

= $5,636,337,182.40

pg. 8

5. Equipment mortgage

Kellogg Company records an equipment mortgage amount of $175,000,000 with the interest rate at 5.75%, and

will be refinanced on today at the rate of 4.75% (2.25% above the Fed Funds rate), paying in quarterly method,

remaining up to 7 years.

● Historical interest rate = 5.75%

● Current interest rate = 4.75%

● Number of terms of payment: n= 7x4= 28

Quarterly payment = PMT =

$ 175,000,000

1−(1+ 0.05755

4 )

−28

0.0575

4

= $7,636,182.89

Present value of equipment mortgage = PMT x ¿] = $7,636,182.89 x

1−(1+ 0.0475

4 )

−28

0.0475

4

= $180,995,408.2

Equity

Ordinary shares = $ 365,000,000

10 x $57.38 = $2,094,370,000

Preference shares = $ 150,000,000

10 x $ 57.38

2 = $430,350,000

Convertible preferred shares = $ 215,0000,000

5 x ($57.38 x 70%) = $1,727,138,000

Step 2: Calculate total value of those items

- Total market value = Total market value of equity + Total market value of debt

= ($2,094,370,000.00 + $430,350,000.00 + $1,727,138,000.00) + ($55,000,000.00 + $138,425,933.60 +

$617,189,983.70 + $392,867,856.90 + $180,995,408.20)

= $5,636,337,182.40

pg. 8

Business Finance – Group Report May 12, 2019

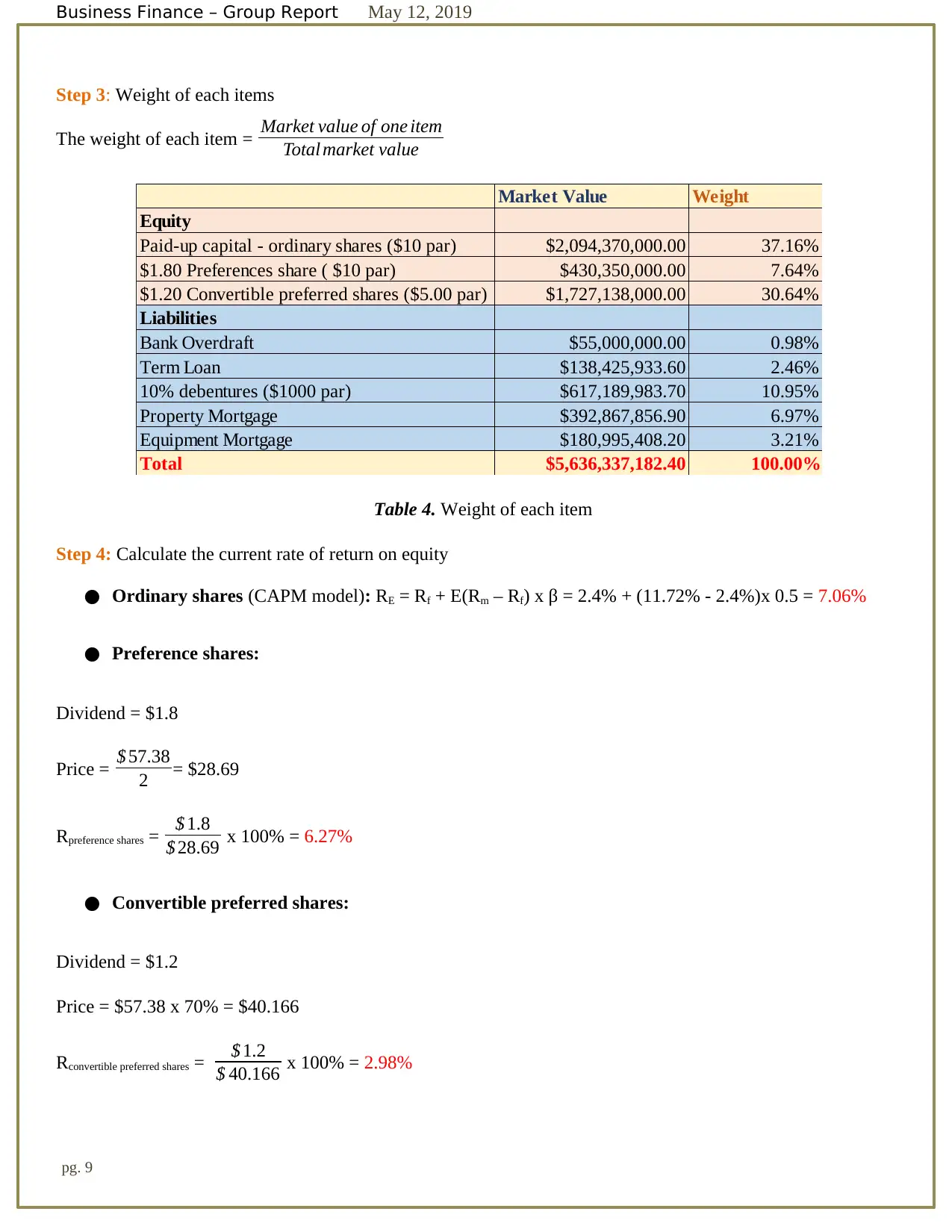

Step 3: Weight of each items

The weight of each item = Market value of one item

Total market value

Market Value Weight

Equity

Paid-up capital - ordinary shares ($10 par) $2,094,370,000.00 37.16%

$1.80 Preferences share ( $10 par) $430,350,000.00 7.64%

$1.20 Convertible preferred shares ($5.00 par) $1,727,138,000.00 30.64%

Liabilities

Bank Overdraft $55,000,000.00 0.98%

Term Loan $138,425,933.60 2.46%

10% debentures ($1000 par) $617,189,983.70 10.95%

Property Mortgage $392,867,856.90 6.97%

Equipment Mortgage $180,995,408.20 3.21%

Total $5,636,337,182.40 100.00%

Table 4. Weight of each item

Step 4: Calculate the current rate of return on equity

● Ordinary shares (CAPM model): RE = Rf + E(Rm – Rf) x β = 2.4% + (11.72% - 2.4%)x 0.5 = 7.06%

● Preference shares:

Dividend = $1.8

Price = $ 57.38

2 = $28.69

Rpreference shares = $ 1.8

$ 28.69 x 100% = 6.27%

● Convertible preferred shares:

Dividend = $1.2

Price = $57.38 x 70% = $40.166

Rconvertible preferred shares = $ 1.2

$ 40.166 x 100% = 2.98%

pg. 9

Step 3: Weight of each items

The weight of each item = Market value of one item

Total market value

Market Value Weight

Equity

Paid-up capital - ordinary shares ($10 par) $2,094,370,000.00 37.16%

$1.80 Preferences share ( $10 par) $430,350,000.00 7.64%

$1.20 Convertible preferred shares ($5.00 par) $1,727,138,000.00 30.64%

Liabilities

Bank Overdraft $55,000,000.00 0.98%

Term Loan $138,425,933.60 2.46%

10% debentures ($1000 par) $617,189,983.70 10.95%

Property Mortgage $392,867,856.90 6.97%

Equipment Mortgage $180,995,408.20 3.21%

Total $5,636,337,182.40 100.00%

Table 4. Weight of each item

Step 4: Calculate the current rate of return on equity

● Ordinary shares (CAPM model): RE = Rf + E(Rm – Rf) x β = 2.4% + (11.72% - 2.4%)x 0.5 = 7.06%

● Preference shares:

Dividend = $1.8

Price = $ 57.38

2 = $28.69

Rpreference shares = $ 1.8

$ 28.69 x 100% = 6.27%

● Convertible preferred shares:

Dividend = $1.2

Price = $57.38 x 70% = $40.166

Rconvertible preferred shares = $ 1.2

$ 40.166 x 100% = 2.98%

pg. 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business Finance – Group Report May 12, 2019

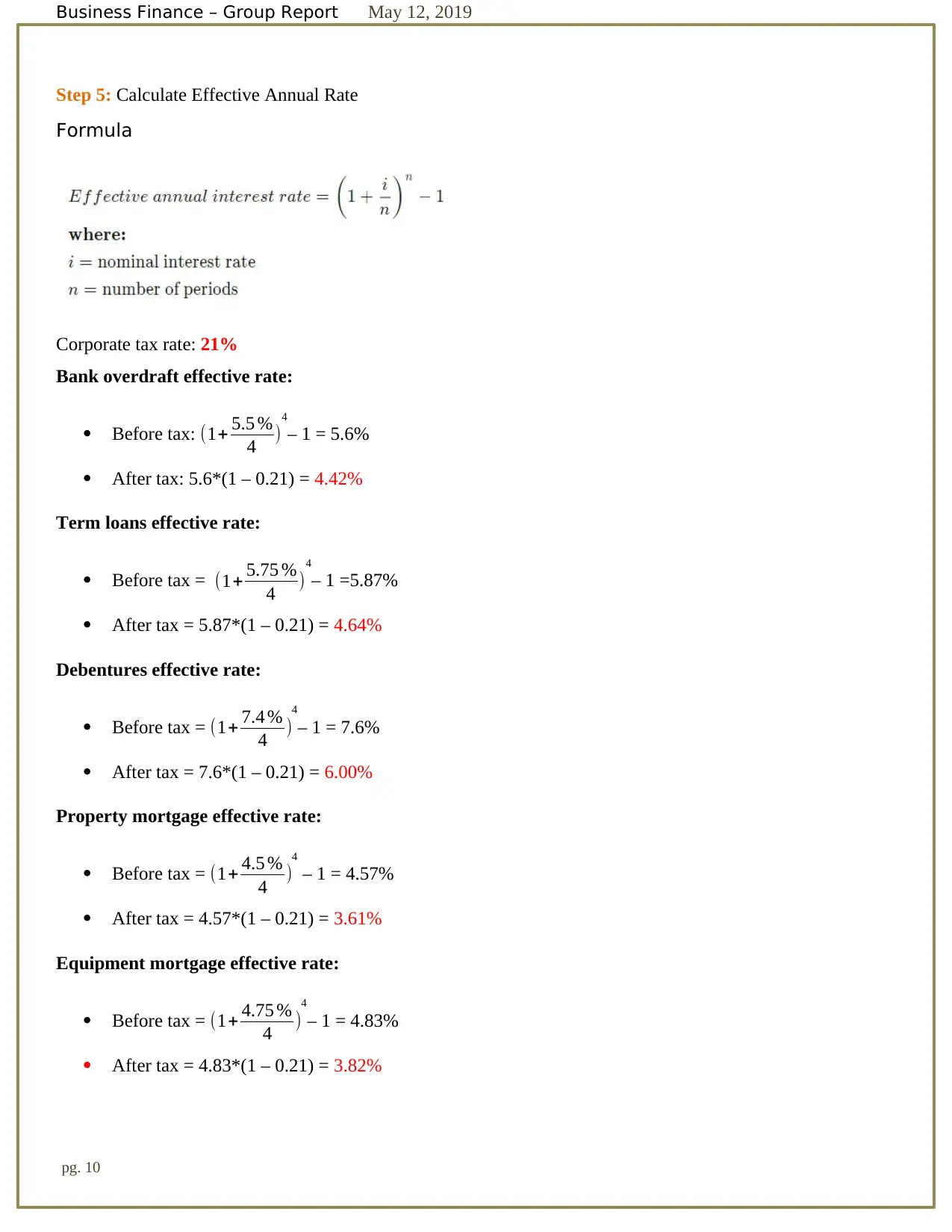

Step 5: Calculate Effective Annual Rate

Formula

Corporate tax rate: 21%

Bank overdraft effective rate:

Before tax: (1+ 5.5 %

4 )

4

– 1 = 5.6%

After tax: 5.6*(1 – 0.21) = 4.42%

Term loans effective rate:

Before tax = (1+ 5.75 %

4 )

4

– 1 =5.87%

After tax = 5.87*(1 – 0.21) = 4.64%

Debentures effective rate:

Before tax = (1+ 7.4 %

4 )

4

– 1 = 7.6%

After tax = 7.6*(1 – 0.21) = 6.00%

Property mortgage effective rate:

Before tax = (1+ 4.5 %

4 )

4

– 1 = 4.57%

After tax = 4.57*(1 – 0.21) = 3.61%

Equipment mortgage effective rate:

Before tax = (1+ 4.75 %

4 )

4

– 1 = 4.83%

After tax = 4.83*(1 – 0.21) = 3.82%

pg. 10

Step 5: Calculate Effective Annual Rate

Formula

Corporate tax rate: 21%

Bank overdraft effective rate:

Before tax: (1+ 5.5 %

4 )

4

– 1 = 5.6%

After tax: 5.6*(1 – 0.21) = 4.42%

Term loans effective rate:

Before tax = (1+ 5.75 %

4 )

4

– 1 =5.87%

After tax = 5.87*(1 – 0.21) = 4.64%

Debentures effective rate:

Before tax = (1+ 7.4 %

4 )

4

– 1 = 7.6%

After tax = 7.6*(1 – 0.21) = 6.00%

Property mortgage effective rate:

Before tax = (1+ 4.5 %

4 )

4

– 1 = 4.57%

After tax = 4.57*(1 – 0.21) = 3.61%

Equipment mortgage effective rate:

Before tax = (1+ 4.75 %

4 )

4

– 1 = 4.83%

After tax = 4.83*(1 – 0.21) = 3.82%

pg. 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business Finance – Group Report May 12, 2019

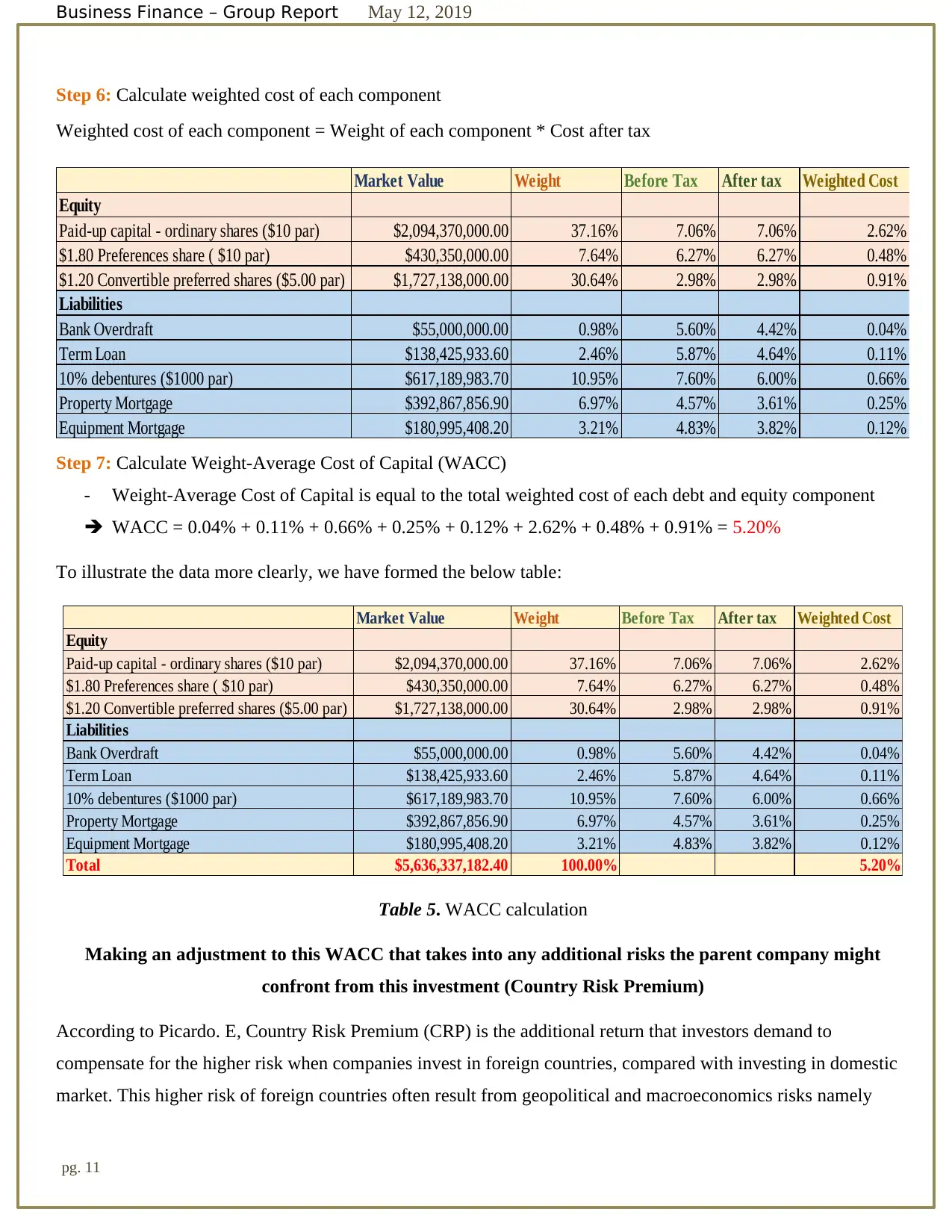

Step 6: Calculate weighted cost of each component

Weighted cost of each component = Weight of each component * Cost after tax

Market Value Weight Before Tax After tax Weighted Cost

Equity

Paid-up capital - ordinary shares ($10 par) $2,094,370,000.00 37.16% 7.06% 7.06% 2.62%

$1.80 Preferences share ( $10 par) $430,350,000.00 7.64% 6.27% 6.27% 0.48%

$1.20 Convertible preferred shares ($5.00 par) $1,727,138,000.00 30.64% 2.98% 2.98% 0.91%

Liabilities

Bank Overdraft $55,000,000.00 0.98% 5.60% 4.42% 0.04%

Term Loan $138,425,933.60 2.46% 5.87% 4.64% 0.11%

10% debentures ($1000 par) $617,189,983.70 10.95% 7.60% 6.00% 0.66%

Property Mortgage $392,867,856.90 6.97% 4.57% 3.61% 0.25%

Equipment Mortgage $180,995,408.20 3.21% 4.83% 3.82% 0.12%

Step 7: Calculate Weight-Average Cost of Capital (WACC)

- Weight-Average Cost of Capital is equal to the total weighted cost of each debt and equity component

WACC = 0.04% + 0.11% + 0.66% + 0.25% + 0.12% + 2.62% + 0.48% + 0.91% = 5.20%

To illustrate the data more clearly, we have formed the below table:

Market Value Weight Before Tax After tax Weighted Cost

Equity

Paid-up capital - ordinary shares ($10 par) $2,094,370,000.00 37.16% 7.06% 7.06% 2.62%

$1.80 Preferences share ( $10 par) $430,350,000.00 7.64% 6.27% 6.27% 0.48%

$1.20 Convertible preferred shares ($5.00 par) $1,727,138,000.00 30.64% 2.98% 2.98% 0.91%

Liabilities

Bank Overdraft $55,000,000.00 0.98% 5.60% 4.42% 0.04%

Term Loan $138,425,933.60 2.46% 5.87% 4.64% 0.11%

10% debentures ($1000 par) $617,189,983.70 10.95% 7.60% 6.00% 0.66%

Property Mortgage $392,867,856.90 6.97% 4.57% 3.61% 0.25%

Equipment Mortgage $180,995,408.20 3.21% 4.83% 3.82% 0.12%

Total $5,636,337,182.40 100.00% 5.20%

Table 5. WACC calculation

Making an adjustment to this WACC that takes into any additional risks the parent company might

confront from this investment (Country Risk Premium)

According to Picardo. E, Country Risk Premium (CRP) is the additional return that investors demand to

compensate for the higher risk when companies invest in foreign countries, compared with investing in domestic

market. This higher risk of foreign countries often result from geopolitical and macroeconomics risks namely

pg. 11

Step 6: Calculate weighted cost of each component

Weighted cost of each component = Weight of each component * Cost after tax

Market Value Weight Before Tax After tax Weighted Cost

Equity

Paid-up capital - ordinary shares ($10 par) $2,094,370,000.00 37.16% 7.06% 7.06% 2.62%

$1.80 Preferences share ( $10 par) $430,350,000.00 7.64% 6.27% 6.27% 0.48%

$1.20 Convertible preferred shares ($5.00 par) $1,727,138,000.00 30.64% 2.98% 2.98% 0.91%

Liabilities

Bank Overdraft $55,000,000.00 0.98% 5.60% 4.42% 0.04%

Term Loan $138,425,933.60 2.46% 5.87% 4.64% 0.11%

10% debentures ($1000 par) $617,189,983.70 10.95% 7.60% 6.00% 0.66%

Property Mortgage $392,867,856.90 6.97% 4.57% 3.61% 0.25%

Equipment Mortgage $180,995,408.20 3.21% 4.83% 3.82% 0.12%

Step 7: Calculate Weight-Average Cost of Capital (WACC)

- Weight-Average Cost of Capital is equal to the total weighted cost of each debt and equity component

WACC = 0.04% + 0.11% + 0.66% + 0.25% + 0.12% + 2.62% + 0.48% + 0.91% = 5.20%

To illustrate the data more clearly, we have formed the below table:

Market Value Weight Before Tax After tax Weighted Cost

Equity

Paid-up capital - ordinary shares ($10 par) $2,094,370,000.00 37.16% 7.06% 7.06% 2.62%

$1.80 Preferences share ( $10 par) $430,350,000.00 7.64% 6.27% 6.27% 0.48%

$1.20 Convertible preferred shares ($5.00 par) $1,727,138,000.00 30.64% 2.98% 2.98% 0.91%

Liabilities

Bank Overdraft $55,000,000.00 0.98% 5.60% 4.42% 0.04%

Term Loan $138,425,933.60 2.46% 5.87% 4.64% 0.11%

10% debentures ($1000 par) $617,189,983.70 10.95% 7.60% 6.00% 0.66%

Property Mortgage $392,867,856.90 6.97% 4.57% 3.61% 0.25%

Equipment Mortgage $180,995,408.20 3.21% 4.83% 3.82% 0.12%

Total $5,636,337,182.40 100.00% 5.20%

Table 5. WACC calculation

Making an adjustment to this WACC that takes into any additional risks the parent company might

confront from this investment (Country Risk Premium)

According to Picardo. E, Country Risk Premium (CRP) is the additional return that investors demand to

compensate for the higher risk when companies invest in foreign countries, compared with investing in domestic

market. This higher risk of foreign countries often result from geopolitical and macroeconomics risks namely

pg. 11

Business Finance – Group Report May 12, 2019

political instability, currency fluctuations, government regulations and so on. In the case of Vietnam, there are

some factors that contribute to the country risk premium.

The first risk is about land clearance in Vietnam. In Hanoi, there are about 383 projects that are behind-

schedule because of the delay in land clearance whereas the number is 215 projects in Ho Chi Minh city

(Duong. P, 2018). Dr. Le Xuan Nghia - Former Deputy Chairman of National Financial Supervisory

Commission sees this risk as the biggest blockage for foreign investors in Viet Nam. As some projects had

been delayed for nearly a decade due to some difficulty in clearance, firms had to bear the cost of cash

flows that aren’t generated during the time plus the cost of maintaining the projects.

Dr. Nghia also points out that currency fluctuation is the problem in Vietnam. Although exchange rate is

just a macroeconomics components which varies below 1% everyday but when considering about a

projects that last more than a decade then it becomes a real problem. The data from XE.inc shows that

throughout 10 year period, the value of 1 $USD increases from 17,785.00VND in 2009 to 23,371.73VND

in 2019. This means that the profit a company earns in Vietnam might lose its value when returning to

USA.

Another difficulty for any corporation to invest in Vietnam is the country’s huge sovereign debt or its

national debt. The data from Parliamentary Financial Budget committee indicates that in 2017 the total

foreign debt occupied for 45.2% of the country’s GDP, in 2018, the number was 49.7% and it is expected

to be 49.9% in 2019 (RFA, 2018). The huge debt reduces Vietnam’s liabilities for international investors,

which proves to be a big risk for Kellogg. However, Fitch Ratings, one of the biggest credits rating

companies, had increased Vietnam’s ratings due to its effort to minimize the public debt in 2018 (Ha.N,

2018). Therefore, Vietnam is still a proper place to invest.

Last but not least, an unclear point in the government’s law for foreign investment becomes a big risk. For

specific, every investment from other countries will operate under the Public- Private Partner (PPP)

module. This module means that the government and companies will collaborate in monitoring the project

since the government will set the standards and firms can follow that standard during their operation

(Tam. N, nd). PPP module seems to be the optimal way to benefit both sides but, there is one unclear point

in the standards that can causes trouble. PPP module forces the profit to stay at 14% but in case the profit

reaches 30%, will the government take the exceeded profit and in case the profit is under 14%, will the

pg. 12

political instability, currency fluctuations, government regulations and so on. In the case of Vietnam, there are

some factors that contribute to the country risk premium.

The first risk is about land clearance in Vietnam. In Hanoi, there are about 383 projects that are behind-

schedule because of the delay in land clearance whereas the number is 215 projects in Ho Chi Minh city

(Duong. P, 2018). Dr. Le Xuan Nghia - Former Deputy Chairman of National Financial Supervisory

Commission sees this risk as the biggest blockage for foreign investors in Viet Nam. As some projects had

been delayed for nearly a decade due to some difficulty in clearance, firms had to bear the cost of cash

flows that aren’t generated during the time plus the cost of maintaining the projects.

Dr. Nghia also points out that currency fluctuation is the problem in Vietnam. Although exchange rate is

just a macroeconomics components which varies below 1% everyday but when considering about a

projects that last more than a decade then it becomes a real problem. The data from XE.inc shows that

throughout 10 year period, the value of 1 $USD increases from 17,785.00VND in 2009 to 23,371.73VND

in 2019. This means that the profit a company earns in Vietnam might lose its value when returning to

USA.

Another difficulty for any corporation to invest in Vietnam is the country’s huge sovereign debt or its

national debt. The data from Parliamentary Financial Budget committee indicates that in 2017 the total

foreign debt occupied for 45.2% of the country’s GDP, in 2018, the number was 49.7% and it is expected

to be 49.9% in 2019 (RFA, 2018). The huge debt reduces Vietnam’s liabilities for international investors,

which proves to be a big risk for Kellogg. However, Fitch Ratings, one of the biggest credits rating

companies, had increased Vietnam’s ratings due to its effort to minimize the public debt in 2018 (Ha.N,

2018). Therefore, Vietnam is still a proper place to invest.

Last but not least, an unclear point in the government’s law for foreign investment becomes a big risk. For

specific, every investment from other countries will operate under the Public- Private Partner (PPP)

module. This module means that the government and companies will collaborate in monitoring the project

since the government will set the standards and firms can follow that standard during their operation

(Tam. N, nd). PPP module seems to be the optimal way to benefit both sides but, there is one unclear point

in the standards that can causes trouble. PPP module forces the profit to stay at 14% but in case the profit

reaches 30%, will the government take the exceeded profit and in case the profit is under 14%, will the

pg. 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.