Business Finance Report: Differences Between FA and MA and Importance

VerifiedAdded on 2023/01/11

|7

|1301

|90

Report

AI Summary

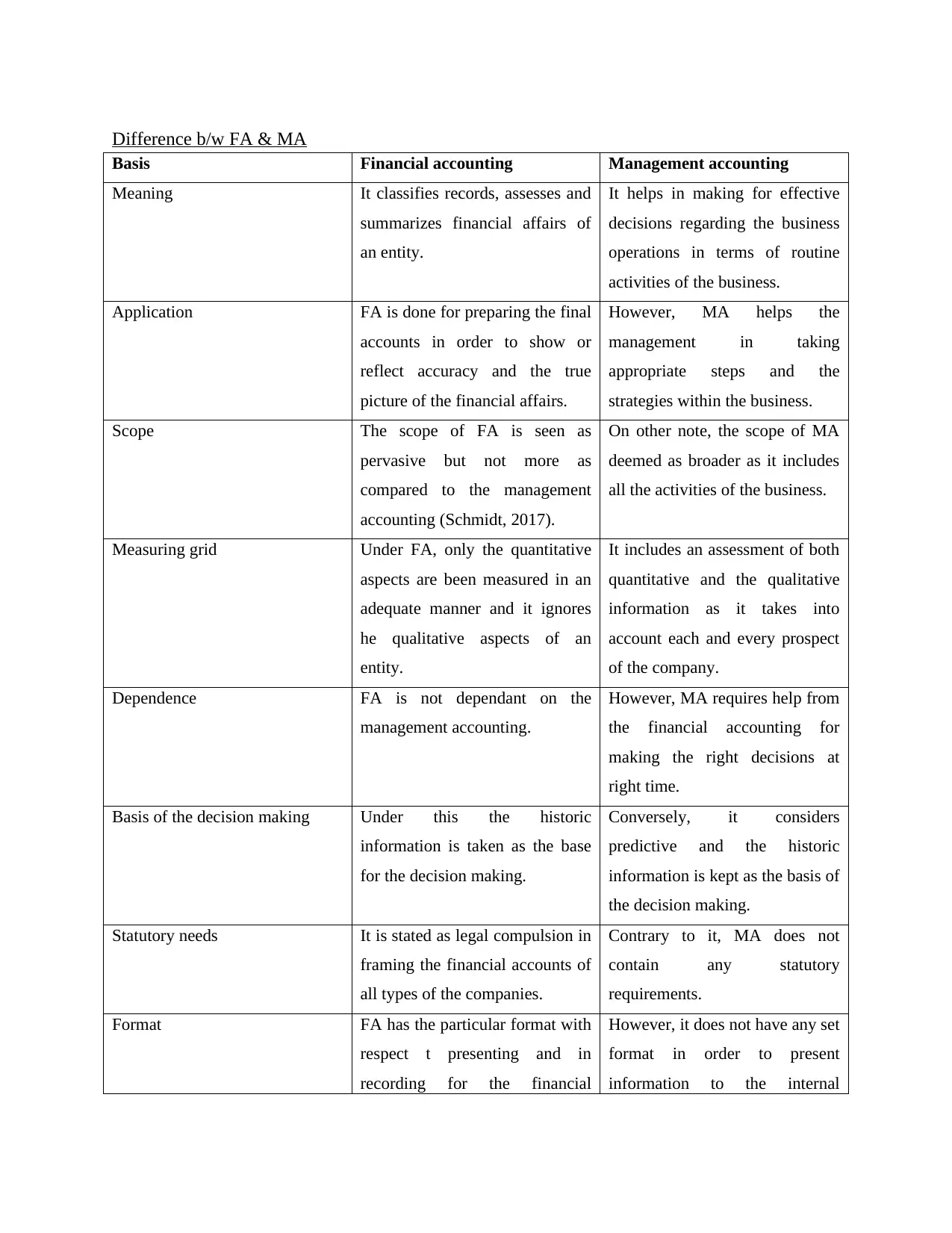

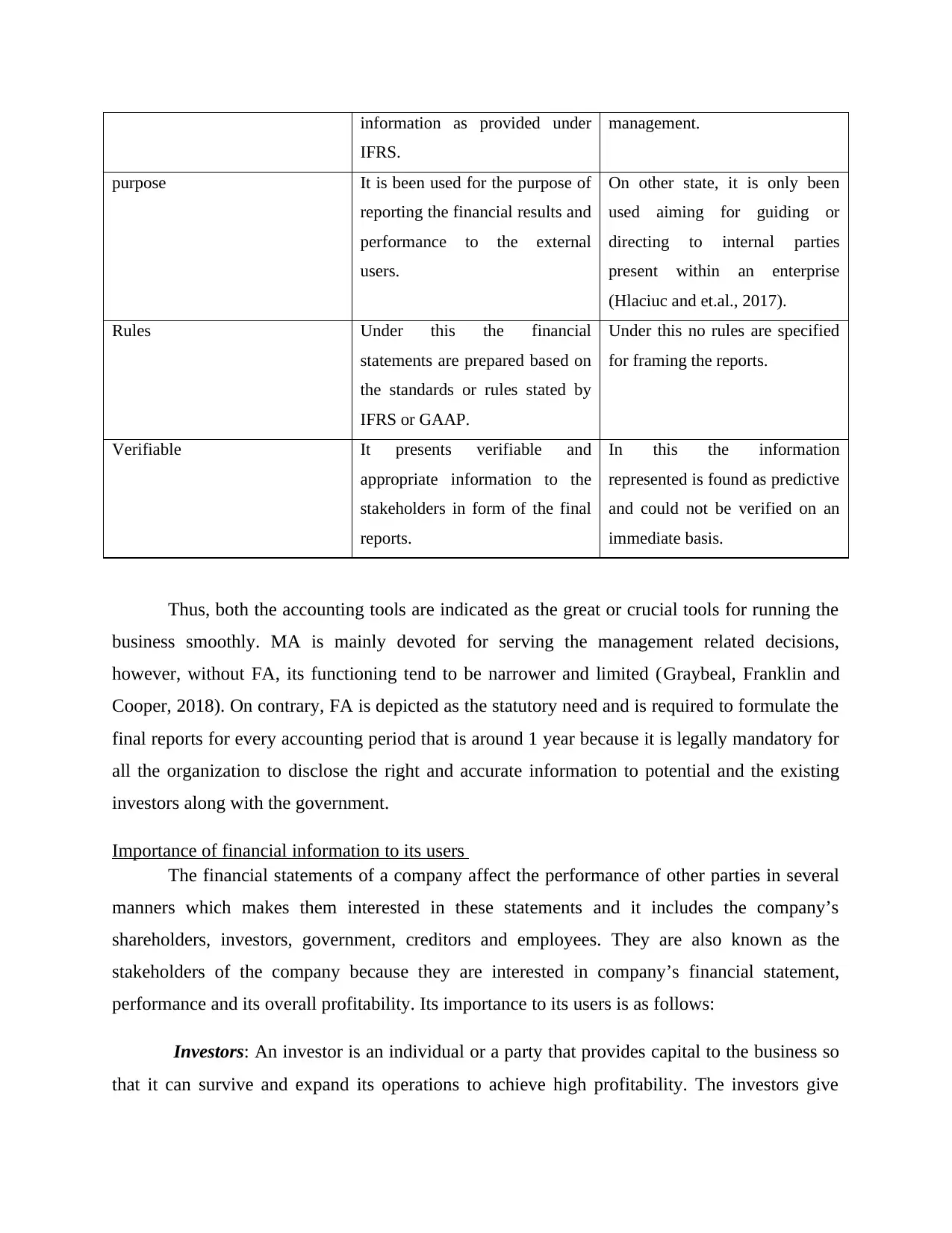

This report provides a comparative analysis of Financial Accounting (FA) and Management Accounting (MA). It details the key differences between them, including their basis, scope, and application. FA focuses on recording and reporting financial information for external users, adhering to specific standards, while MA supports internal decision-making with a broader scope. The report also emphasizes the importance of financial information to various stakeholders, such as investors, management, creditors, employees, and the government, highlighting how financial statements influence their decisions and actions. The document is a solution to a business finance assignment, offering a clear understanding of both accounting methods and their significance in the business environment.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.