Business Finance Report: Financial Performance Analysis, Module 1

VerifiedAdded on 2022/12/27

|13

|3403

|96

Report

AI Summary

This report provides a detailed analysis of business finance, focusing on cash flow, profit, and working capital management. Task 1 examines the relationship between profit and cash flow, the impact of working capital changes, and the influence of company management on financial results. It offers recommendations for improving cash flow, such as reducing debt and optimizing working capital. Task 2 presents a monthly cash budget for Thorne Estate over four months, offering insights into cash needs and allocation. The report concludes with recommendations to enhance cash flow, including making realistic projections, managing receipts effectively, and consolidating predictable expenses. The analysis provides valuable insights for financial decision-making and business sustainability.

Business Finance

1 | P a g e

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Task 1...............................................................................................................................................3

Executive summary.....................................................................................................................3

i. Explain:.....................................................................................................................................3

a. Profit and cash flow.............................................................................................................3

b. Working capital.......................................................................................................................4

c. Effect of changes in Working Capital......................................................................................5

ii. Effect of company’s management on financial results............................................................6

iii. Recommendations..................................................................................................................6

Task 2...............................................................................................................................................8

Executive Summary.....................................................................................................................8

1. Monthly cash budget................................................................................................................8

2. Recommendation:....................................................................................................................9

References......................................................................................................................................13

2 | P a g e

Task 1...............................................................................................................................................3

Executive summary.....................................................................................................................3

i. Explain:.....................................................................................................................................3

a. Profit and cash flow.............................................................................................................3

b. Working capital.......................................................................................................................4

c. Effect of changes in Working Capital......................................................................................5

ii. Effect of company’s management on financial results............................................................6

iii. Recommendations..................................................................................................................6

Task 2...............................................................................................................................................8

Executive Summary.....................................................................................................................8

1. Monthly cash budget................................................................................................................8

2. Recommendation:....................................................................................................................9

References......................................................................................................................................13

2 | P a g e

Task 1

Executive summary

There is a maxim on business that "money is best" and, assuming so, it is the income from the

blood that keeps the heart of the filter in the kingdom. Turnover is perhaps the most fundamental

development segment for a small or medium-sized company. Without money, the benefits are

useless. Much productive activity on paper ended in Chapter 11 because the amount of money

coming in is no different and the amount of money going out. Companies that do not use large

sums of money will not be able to afford the expected profits or may have to pay more to get

money for the job. "Despite how money is the soul of a company - the fuel that keeps the engine

running - most entrepreneurs have no idea of their income, CPA and CFO first in some

organizations and creators of Never Run out of Unsupported Income advice are causing more

business frustration today than ever as a recent reminder.

i. Explain:

a. Profit and cash flow

Cashflow

It's basically developing resources across your business. Company should follow it week after

week, month by month or quarterly. There are of course two types of cash flows:

• Positive cash flow: This happens when the money from your business from contracts, sales

records, etc. exceeds the amount of money your organization leaves through liabilities creditors,

monthly expenses, compensation and so on.

• Negative cash flow: This happens when your cash flow is more important than your cash flow.

This usually means something bad for a business, but there are steps you can take to remedy the

situation and create or raise more money while maintaining or cutting costs.

3 | P a g e

Executive summary

There is a maxim on business that "money is best" and, assuming so, it is the income from the

blood that keeps the heart of the filter in the kingdom. Turnover is perhaps the most fundamental

development segment for a small or medium-sized company. Without money, the benefits are

useless. Much productive activity on paper ended in Chapter 11 because the amount of money

coming in is no different and the amount of money going out. Companies that do not use large

sums of money will not be able to afford the expected profits or may have to pay more to get

money for the job. "Despite how money is the soul of a company - the fuel that keeps the engine

running - most entrepreneurs have no idea of their income, CPA and CFO first in some

organizations and creators of Never Run out of Unsupported Income advice are causing more

business frustration today than ever as a recent reminder.

i. Explain:

a. Profit and cash flow

Cashflow

It's basically developing resources across your business. Company should follow it week after

week, month by month or quarterly. There are of course two types of cash flows:

• Positive cash flow: This happens when the money from your business from contracts, sales

records, etc. exceeds the amount of money your organization leaves through liabilities creditors,

monthly expenses, compensation and so on.

• Negative cash flow: This happens when your cash flow is more important than your cash flow.

This usually means something bad for a business, but there are steps you can take to remedy the

situation and create or raise more money while maintaining or cutting costs.

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit

Earnings reflect the cash benefit recognized when the income generated from the transfer of a

business exceeds the costs, expenses and costs involved in supporting the business. Any benefits

received will be donated to the entrepreneurs, who decide to return the money or return it to the

industry. The benefit is declared as total income excluding all expenses.

The owners and investors of the group can benefit, regularly as profit margins, or reinvest in the

group. Benefits, for example, can be used to buy new shares to sell a business or to finance

innovative work (R&D) for new items or administrations. Like income, profit can be expressed

as a positive or negative number. By the time this estimate gives a negative number, it is often

referred to as bad luck, as the organization was facing more financial work than it had the ability

to recover from these activities.

Profit vs. Cashflows

The important difference between Profit and Cashflows is that while an advantage shows the

amount of money remaining after all expenses have been paid, the income shows the net

progress of money in and out of the business.

Cash flow is the amount of money that flows through the entire business over a period of time

and is a benefit of whatever income is found after expenses. While it is beneficial to do business

quickly, revenue can also be a more effective way to determine an organization's cash flow

position. In this sense, time is the crucial difference between the two measurements.

b. Working capital

Working capital, also known as net working capital (NWC), is the difference between an

organization's current assets, such as cash, sales records (invoices neglected by customers), and

stocks of raw materials and finished goods, and its current liabilities, for example, the creditor's

liabilities. Net working capital is a percentage of an organization’s liquidity and refers to the

difference between current working resources and current workloads. These numbers are

generally the same and can be obtained from the organization's money as well as credits as well

as an inventory, fewer records to pay and fewer expenses collected.

4 | P a g e

Earnings reflect the cash benefit recognized when the income generated from the transfer of a

business exceeds the costs, expenses and costs involved in supporting the business. Any benefits

received will be donated to the entrepreneurs, who decide to return the money or return it to the

industry. The benefit is declared as total income excluding all expenses.

The owners and investors of the group can benefit, regularly as profit margins, or reinvest in the

group. Benefits, for example, can be used to buy new shares to sell a business or to finance

innovative work (R&D) for new items or administrations. Like income, profit can be expressed

as a positive or negative number. By the time this estimate gives a negative number, it is often

referred to as bad luck, as the organization was facing more financial work than it had the ability

to recover from these activities.

Profit vs. Cashflows

The important difference between Profit and Cashflows is that while an advantage shows the

amount of money remaining after all expenses have been paid, the income shows the net

progress of money in and out of the business.

Cash flow is the amount of money that flows through the entire business over a period of time

and is a benefit of whatever income is found after expenses. While it is beneficial to do business

quickly, revenue can also be a more effective way to determine an organization's cash flow

position. In this sense, time is the crucial difference between the two measurements.

b. Working capital

Working capital, also known as net working capital (NWC), is the difference between an

organization's current assets, such as cash, sales records (invoices neglected by customers), and

stocks of raw materials and finished goods, and its current liabilities, for example, the creditor's

liabilities. Net working capital is a percentage of an organization’s liquidity and refers to the

difference between current working resources and current workloads. These numbers are

generally the same and can be obtained from the organization's money as well as credits as well

as an inventory, fewer records to pay and fewer expenses collected.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working capital is part of the organization’s liquidity, operating productivity and financial well-

being. If an organization has good generous working capital, it should contribute to and improve.

With the current resources of an organization not exceeding its current responsibilities, it may

have difficulties in developing or caring for lenders, or even fail.

To work out working capital, compare an organization's current resources with its current

responsibilities. Current assets are recorded on an organization’s balance sheet including cash,

credits, stocks and miscellaneous assets that need to be sold or converted into cash in less than a

year. Current liabilities include posts payable, taxes, expenses payable and the current long-term

commitment period. Standard facilities are available within a year. Current responsibilities are

expected within a year.

Working capital that is at or above normal business for a similar group is considered satisfactory.

Low working capital can indicate a risk of distress or bankruptcy.

c. Effect of changes in Working Capital

Most new key initiatives, such as ongoing development or the introduction of new business

sectors, require an interest in working capital. This reduces cash flow. Be that as it may, money

will also decrease if money is raised too gradually or if contract volumes are decreasing, causing

credit to drop. Organizations that use working capital as waste can sustain revenue by crushing

suppliers and customers.

Changes in working capital are reflected in the definition of corporate income. Below are some

examples of how money and working capital are affected.

Since the stock exchanges do not accumulate current resources and current liabilities of a similar

amount, there would be no change in working capital. For example, if an organization received

money from a momentary payment obligation in 60 days, there would be an increase in the

definition of income. In any event, there would be no increase in working capital, as the credit

proceeds would be a normal asset or currency, and the pound would be payable as a current

liability as a progressive advance.

5 | P a g e

being. If an organization has good generous working capital, it should contribute to and improve.

With the current resources of an organization not exceeding its current responsibilities, it may

have difficulties in developing or caring for lenders, or even fail.

To work out working capital, compare an organization's current resources with its current

responsibilities. Current assets are recorded on an organization’s balance sheet including cash,

credits, stocks and miscellaneous assets that need to be sold or converted into cash in less than a

year. Current liabilities include posts payable, taxes, expenses payable and the current long-term

commitment period. Standard facilities are available within a year. Current responsibilities are

expected within a year.

Working capital that is at or above normal business for a similar group is considered satisfactory.

Low working capital can indicate a risk of distress or bankruptcy.

c. Effect of changes in Working Capital

Most new key initiatives, such as ongoing development or the introduction of new business

sectors, require an interest in working capital. This reduces cash flow. Be that as it may, money

will also decrease if money is raised too gradually or if contract volumes are decreasing, causing

credit to drop. Organizations that use working capital as waste can sustain revenue by crushing

suppliers and customers.

Changes in working capital are reflected in the definition of corporate income. Below are some

examples of how money and working capital are affected.

Since the stock exchanges do not accumulate current resources and current liabilities of a similar

amount, there would be no change in working capital. For example, if an organization received

money from a momentary payment obligation in 60 days, there would be an increase in the

definition of income. In any event, there would be no increase in working capital, as the credit

proceeds would be a normal asset or currency, and the pound would be payable as a current

liability as a progressive advance.

5 | P a g e

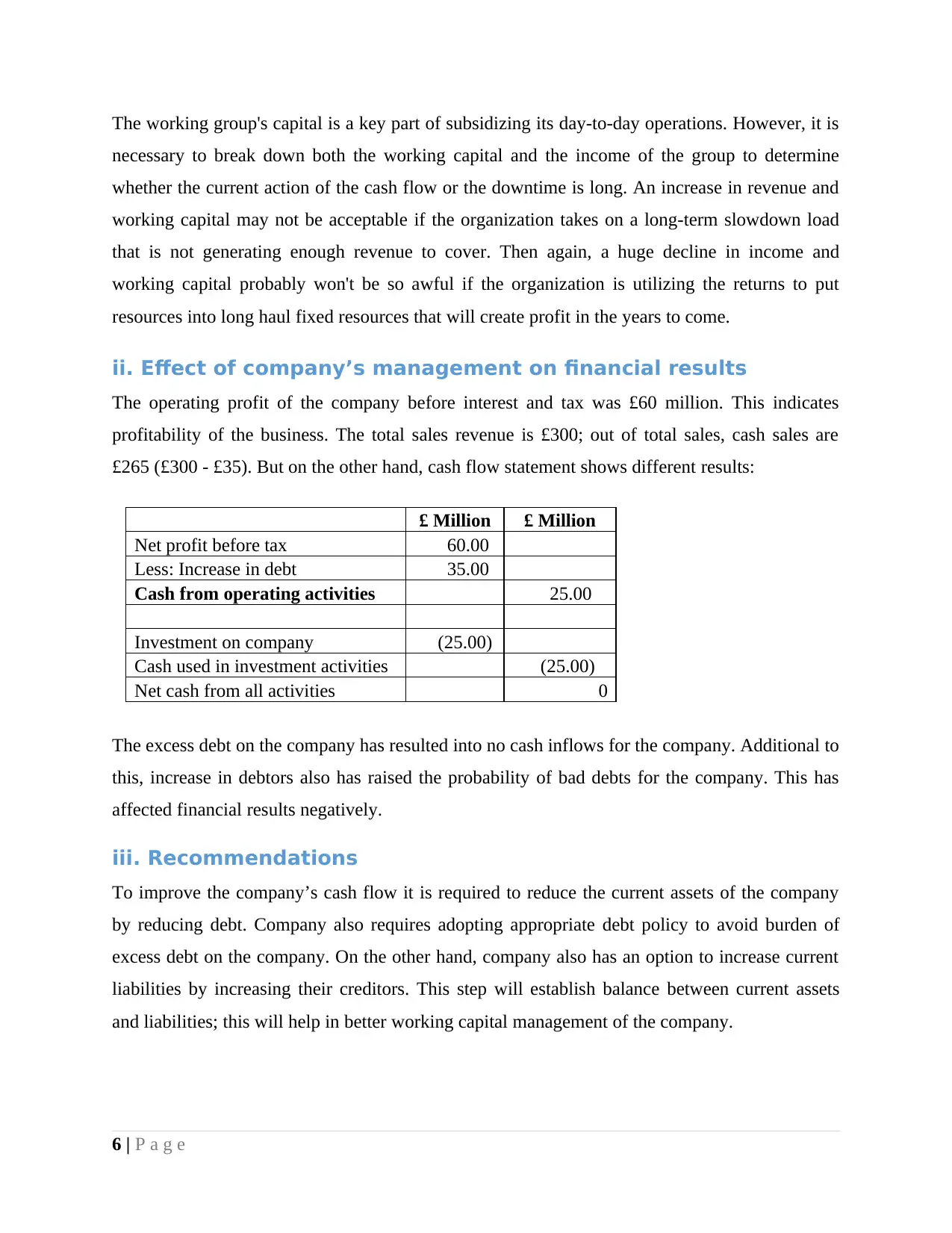

The working group's capital is a key part of subsidizing its day-to-day operations. However, it is

necessary to break down both the working capital and the income of the group to determine

whether the current action of the cash flow or the downtime is long. An increase in revenue and

working capital may not be acceptable if the organization takes on a long-term slowdown load

that is not generating enough revenue to cover. Then again, a huge decline in income and

working capital probably won't be so awful if the organization is utilizing the returns to put

resources into long haul fixed resources that will create profit in the years to come.

ii. Effect of company’s management on financial results

The operating profit of the company before interest and tax was £60 million. This indicates

profitability of the business. The total sales revenue is £300; out of total sales, cash sales are

£265 (£300 - £35). But on the other hand, cash flow statement shows different results:

£ Million £ Million

Net profit before tax 60.00

Less: Increase in debt 35.00

Cash from operating activities 25.00

Investment on company (25.00)

Cash used in investment activities (25.00)

Net cash from all activities 0

The excess debt on the company has resulted into no cash inflows for the company. Additional to

this, increase in debtors also has raised the probability of bad debts for the company. This has

affected financial results negatively.

iii. Recommendations

To improve the company’s cash flow it is required to reduce the current assets of the company

by reducing debt. Company also requires adopting appropriate debt policy to avoid burden of

excess debt on the company. On the other hand, company also has an option to increase current

liabilities by increasing their creditors. This step will establish balance between current assets

and liabilities; this will help in better working capital management of the company.

6 | P a g e

necessary to break down both the working capital and the income of the group to determine

whether the current action of the cash flow or the downtime is long. An increase in revenue and

working capital may not be acceptable if the organization takes on a long-term slowdown load

that is not generating enough revenue to cover. Then again, a huge decline in income and

working capital probably won't be so awful if the organization is utilizing the returns to put

resources into long haul fixed resources that will create profit in the years to come.

ii. Effect of company’s management on financial results

The operating profit of the company before interest and tax was £60 million. This indicates

profitability of the business. The total sales revenue is £300; out of total sales, cash sales are

£265 (£300 - £35). But on the other hand, cash flow statement shows different results:

£ Million £ Million

Net profit before tax 60.00

Less: Increase in debt 35.00

Cash from operating activities 25.00

Investment on company (25.00)

Cash used in investment activities (25.00)

Net cash from all activities 0

The excess debt on the company has resulted into no cash inflows for the company. Additional to

this, increase in debtors also has raised the probability of bad debts for the company. This has

affected financial results negatively.

iii. Recommendations

To improve the company’s cash flow it is required to reduce the current assets of the company

by reducing debt. Company also requires adopting appropriate debt policy to avoid burden of

excess debt on the company. On the other hand, company also has an option to increase current

liabilities by increasing their creditors. This step will establish balance between current assets

and liabilities; this will help in better working capital management of the company.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Increase in current liabilities will bring cash into the business, and will have positive working

capital effect on operating activities. Through this, the cash inflow from operating activities will

increase, and simultaneously fund from all over operations will also increase.

7 | P a g e

capital effect on operating activities. Through this, the cash inflow from operating activities will

increase, and simultaneously fund from all over operations will also increase.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

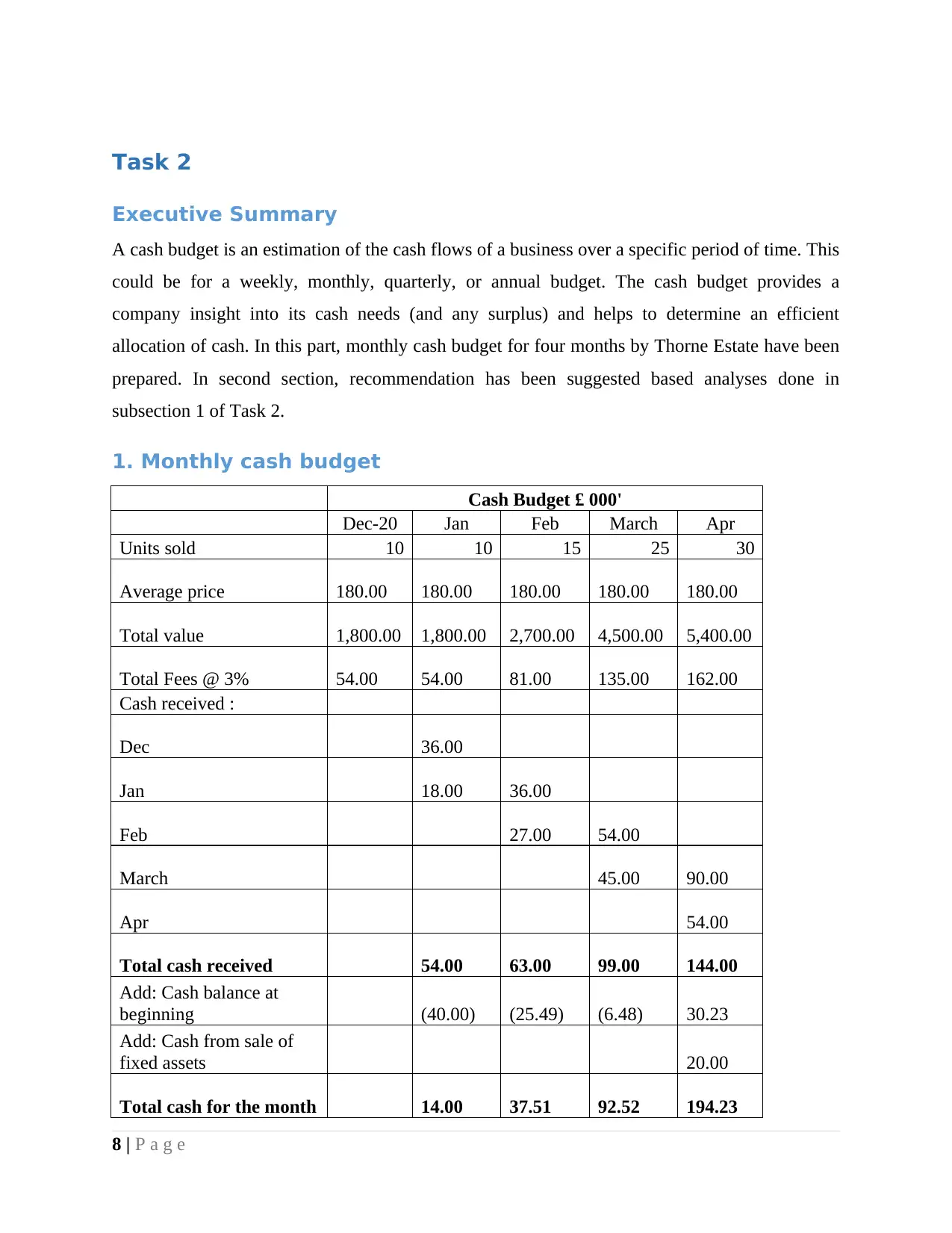

Task 2

Executive Summary

A cash budget is an estimation of the cash flows of a business over a specific period of time. This

could be for a weekly, monthly, quarterly, or annual budget. The cash budget provides a

company insight into its cash needs (and any surplus) and helps to determine an efficient

allocation of cash. In this part, monthly cash budget for four months by Thorne Estate have been

prepared. In second section, recommendation has been suggested based analyses done in

subsection 1 of Task 2.

1. Monthly cash budget

Cash Budget £ 000'

Dec-20 Jan Feb March Apr

Units sold 10 10 15 25 30

Average price 180.00 180.00 180.00 180.00 180.00

Total value 1,800.00 1,800.00 2,700.00 4,500.00 5,400.00

Total Fees @ 3% 54.00 54.00 81.00 135.00 162.00

Cash received :

Dec 36.00

Jan 18.00 36.00

Feb 27.00 54.00

March 45.00 90.00

Apr 54.00

Total cash received 54.00 63.00 99.00 144.00

Add: Cash balance at

beginning (40.00) (25.49) (6.48) 30.23

Add: Cash from sale of

fixed assets 20.00

Total cash for the month 14.00 37.51 92.52 194.23

8 | P a g e

Executive Summary

A cash budget is an estimation of the cash flows of a business over a specific period of time. This

could be for a weekly, monthly, quarterly, or annual budget. The cash budget provides a

company insight into its cash needs (and any surplus) and helps to determine an efficient

allocation of cash. In this part, monthly cash budget for four months by Thorne Estate have been

prepared. In second section, recommendation has been suggested based analyses done in

subsection 1 of Task 2.

1. Monthly cash budget

Cash Budget £ 000'

Dec-20 Jan Feb March Apr

Units sold 10 10 15 25 30

Average price 180.00 180.00 180.00 180.00 180.00

Total value 1,800.00 1,800.00 2,700.00 4,500.00 5,400.00

Total Fees @ 3% 54.00 54.00 81.00 135.00 162.00

Cash received :

Dec 36.00

Jan 18.00 36.00

Feb 27.00 54.00

March 45.00 90.00

Apr 54.00

Total cash received 54.00 63.00 99.00 144.00

Add: Cash balance at

beginning (40.00) (25.49) (6.48) 30.23

Add: Cash from sale of

fixed assets 20.00

Total cash for the month 14.00 37.51 92.52 194.23

8 | P a g e

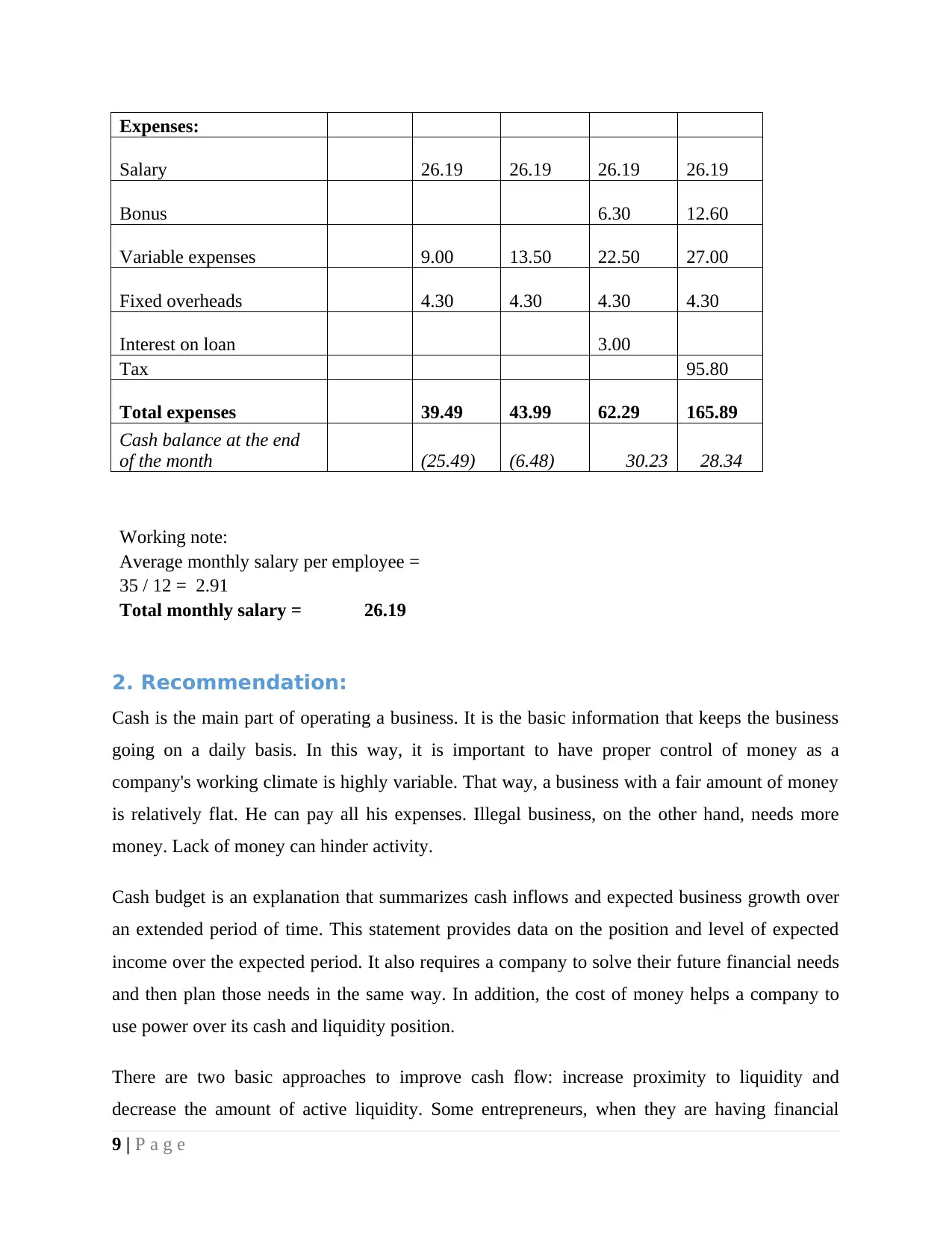

Expenses:

Salary 26.19 26.19 26.19 26.19

Bonus 6.30 12.60

Variable expenses 9.00 13.50 22.50 27.00

Fixed overheads 4.30 4.30 4.30 4.30

Interest on loan 3.00

Tax 95.80

Total expenses 39.49 43.99 62.29 165.89

Cash balance at the end

of the month (25.49) (6.48) 30.23 28.34

Working note:

Average monthly salary per employee =

35 / 12 = 2.91

Total monthly salary = 26.19

2. Recommendation:

Cash is the main part of operating a business. It is the basic information that keeps the business

going on a daily basis. In this way, it is important to have proper control of money as a

company's working climate is highly variable. That way, a business with a fair amount of money

is relatively flat. He can pay all his expenses. Illegal business, on the other hand, needs more

money. Lack of money can hinder activity.

Cash budget is an explanation that summarizes cash inflows and expected business growth over

an extended period of time. This statement provides data on the position and level of expected

income over the expected period. It also requires a company to solve their future financial needs

and then plan those needs in the same way. In addition, the cost of money helps a company to

use power over its cash and liquidity position.

There are two basic approaches to improve cash flow: increase proximity to liquidity and

decrease the amount of active liquidity. Some entrepreneurs, when they are having financial

9 | P a g e

Salary 26.19 26.19 26.19 26.19

Bonus 6.30 12.60

Variable expenses 9.00 13.50 22.50 27.00

Fixed overheads 4.30 4.30 4.30 4.30

Interest on loan 3.00

Tax 95.80

Total expenses 39.49 43.99 62.29 165.89

Cash balance at the end

of the month (25.49) (6.48) 30.23 28.34

Working note:

Average monthly salary per employee =

35 / 12 = 2.91

Total monthly salary = 26.19

2. Recommendation:

Cash is the main part of operating a business. It is the basic information that keeps the business

going on a daily basis. In this way, it is important to have proper control of money as a

company's working climate is highly variable. That way, a business with a fair amount of money

is relatively flat. He can pay all his expenses. Illegal business, on the other hand, needs more

money. Lack of money can hinder activity.

Cash budget is an explanation that summarizes cash inflows and expected business growth over

an extended period of time. This statement provides data on the position and level of expected

income over the expected period. It also requires a company to solve their future financial needs

and then plan those needs in the same way. In addition, the cost of money helps a company to

use power over its cash and liquidity position.

There are two basic approaches to improve cash flow: increase proximity to liquidity and

decrease the amount of active liquidity. Some entrepreneurs, when they are having financial

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

difficulties, use a debit card or open a credit extension. While a company may seem, by all

accounts, profitable, it can cause serious problems and even stop operations if the organization

develops beyond its capabilities. Some of the suggestions are as follows:

1. Make month-to-month projections (check your trust): When extending contracts for profit,

don't be overly optimistic. Best practice is to use the most compelling valuation marketing

predictions or mid-month-to-month points. Any marketing forecast should be used for revenue to

be practical and quickly accessible.

2. Recall Receipts: Only one out of every odd contract is equated in terms of money. Cash and

credit agreements for continuing operations are immediately available. However, contracts can

take 30, 60, or even 180 days or more to transform a usable asset. This factor is a key factor in

month-to-month income projections. Also, be aware of the expected impact on revenue before

extending terms to new entrants.

3. Unite unsurprising: Any business that has things that include things like a lease, financing, and

a reliable phone facility will have an average to a month's cash flow, which isn't surprising.

Combine these numbers into one labor cost figure. This will help financial experts identify the

amount of money required each month to cover operational costs. Since the organization may not

be able to manage them, there is a risk that they may run into funding problems and want to stay

in business for the long term.

4. Adaptation to development: it is fundamentally necessary to represent the capital required for

development. Many successful organizations are failing to have sufficient funds to subsidize

their development. New offers often require a new spend for hardware, staff and shop windows.

In general, there are costs that can be met before the agreement must be received in advance.

5. Plan for Contracts: Unforeseen circumstances should be considered in any revenue estimate to

ensure that, when the opportunity arises, the company will be able to join. An organization that

does not have another course of action in the event of an emergency does not have the capacity

to respond as an organization that has, for example, a financial facility or emergency shelter.

10 | P a g e

accounts, profitable, it can cause serious problems and even stop operations if the organization

develops beyond its capabilities. Some of the suggestions are as follows:

1. Make month-to-month projections (check your trust): When extending contracts for profit,

don't be overly optimistic. Best practice is to use the most compelling valuation marketing

predictions or mid-month-to-month points. Any marketing forecast should be used for revenue to

be practical and quickly accessible.

2. Recall Receipts: Only one out of every odd contract is equated in terms of money. Cash and

credit agreements for continuing operations are immediately available. However, contracts can

take 30, 60, or even 180 days or more to transform a usable asset. This factor is a key factor in

month-to-month income projections. Also, be aware of the expected impact on revenue before

extending terms to new entrants.

3. Unite unsurprising: Any business that has things that include things like a lease, financing, and

a reliable phone facility will have an average to a month's cash flow, which isn't surprising.

Combine these numbers into one labor cost figure. This will help financial experts identify the

amount of money required each month to cover operational costs. Since the organization may not

be able to manage them, there is a risk that they may run into funding problems and want to stay

in business for the long term.

4. Adaptation to development: it is fundamentally necessary to represent the capital required for

development. Many successful organizations are failing to have sufficient funds to subsidize

their development. New offers often require a new spend for hardware, staff and shop windows.

In general, there are costs that can be met before the agreement must be received in advance.

5. Plan for Contracts: Unforeseen circumstances should be considered in any revenue estimate to

ensure that, when the opportunity arises, the company will be able to join. An organization that

does not have another course of action in the event of an emergency does not have the capacity

to respond as an organization that has, for example, a financial facility or emergency shelter.

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Whether the contract is a contract or a development, any revenue outlook should include an

emergency policy or “mud investment” to address the new exemptions or problems that are

expected production.

It is recommended that company should maintain a full month-on-month income, minus labor

costs. Net minimum aggregate is the extra money needed to sustain the business or achieve a

business development goal.

In the event that this amount is not negative, it should already be accessible to the organization as

credit or equity so that the organization does not become bankrupt. When it comes to controlling

income, money will still be an important factor, but it will cease to be the most basic thing.

Based on above cash management analysis, it is recommended that company should maintain

minimum cash requirement at the end of each month. This cash requirement is nothing but

minimum working capital requirement by the business to meet its day to day business expenses.

Other recommendations:

1. Leasing rather than Buying: Since rent, hardware and land typically end up being more

expensive than buying, this might be strange for someone who only focuses on the primary

concern or pays after the expenses have been pay. However, if an organization is to fill with

money, an organization must maintain a cash flow for day to day activities. By getting the rent,

organizations are unable to make small contributions, which will improve their income. A

special reward is that rent installments are an operating expense, after which they can be

discounted.

2. Prepayment Discount: Everyone will love a promoter and if you offer a discount if they cover

their bills upfront, you are getting a deal that will be beneficial to both of them. Getting the

money up front will obviously help income.

3. Customer Credit Checks: Just assume that a customer doesn't want to pay you real money and

make sure you do a credit check, especially before signing up. If the customer has an unassisted

credit, you can confidently assume that will not receive the installments on schedule. With the

11 | P a g e

emergency policy or “mud investment” to address the new exemptions or problems that are

expected production.

It is recommended that company should maintain a full month-on-month income, minus labor

costs. Net minimum aggregate is the extra money needed to sustain the business or achieve a

business development goal.

In the event that this amount is not negative, it should already be accessible to the organization as

credit or equity so that the organization does not become bankrupt. When it comes to controlling

income, money will still be an important factor, but it will cease to be the most basic thing.

Based on above cash management analysis, it is recommended that company should maintain

minimum cash requirement at the end of each month. This cash requirement is nothing but

minimum working capital requirement by the business to meet its day to day business expenses.

Other recommendations:

1. Leasing rather than Buying: Since rent, hardware and land typically end up being more

expensive than buying, this might be strange for someone who only focuses on the primary

concern or pays after the expenses have been pay. However, if an organization is to fill with

money, an organization must maintain a cash flow for day to day activities. By getting the rent,

organizations are unable to make small contributions, which will improve their income. A

special reward is that rent installments are an operating expense, after which they can be

discounted.

2. Prepayment Discount: Everyone will love a promoter and if you offer a discount if they cover

their bills upfront, you are getting a deal that will be beneficial to both of them. Getting the

money up front will obviously help income.

3. Customer Credit Checks: Just assume that a customer doesn't want to pay you real money and

make sure you do a credit check, especially before signing up. If the customer has an unassisted

credit, you can confidently assume that will not receive the installments on schedule. With the

11 | P a g e

heaviness of the deal, overdue installments can hurt business's income. If company chooses a

contract despite sketch credit, be sure to set it up with a high loan cost.

4. Purchasing Collaboration: Structure Think of power in numbers and find other similar

organizations willing to raise their money to cut lower costs with suppliers, who usually place

big limits on large companies that buy in bulk.

4. Form a Buying Cooperative: Think power in numbers, and find other like-minded companies

willing to pool their cash in order to tackle lower prices with suppliers, who usually give big

discounts to large firms who buy in bulk.

12 | P a g e

contract despite sketch credit, be sure to set it up with a high loan cost.

4. Purchasing Collaboration: Structure Think of power in numbers and find other similar

organizations willing to raise their money to cut lower costs with suppliers, who usually place

big limits on large companies that buy in bulk.

4. Form a Buying Cooperative: Think power in numbers, and find other like-minded companies

willing to pool their cash in order to tackle lower prices with suppliers, who usually give big

discounts to large firms who buy in bulk.

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.