Business Finance Report: Finance Concepts and Budgeting Analysis

VerifiedAdded on 2023/01/12

|13

|3181

|30

Report

AI Summary

This report is a comprehensive analysis of key business finance concepts. It begins by defining profit and cashflow, differentiating between them, and discussing the impact of working capital on an organization's cash flow. The report then delves into the components of working capital, including receivables, inventory, and payables, illustrating how changes in these areas affect cash flow. A case study on MDL (a fictitious company) is presented, analyzing its financial situation, particularly concerning its cash flow and working capital management, and suggesting steps to improve its financial performance. The second part of the report shifts focus to budgeting, explaining the purpose of budgeting and detailing various methods such as traditional, rolling, zero-based, and activity-based budgeting. The report then demonstrates the applicability of budgeting methods in cost management, specifically for Second Sight Plc, and concludes by recommending the most suitable budgeting approach for its new facility planning, which is activity-based budgeting.

Business finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................3

Part-1................................................................................................................................................4

a. Meaning of profit and cashflow...............................................................................................4

b. Working capital, receivables, inventory and payables.............................................................4

c. How changes in working capital affect the cashflow...............................................................5

How the MDL is managed which might affect its financial results............................................5

Steps to improve the company's cashflow through working capital management......................6

EXECUTIVE SUMMARY.............................................................................................................1

Part-2................................................................................................................................................2

Purpose of preparing the budget and its different types..............................................................2

Demonstrating the applicability of budgeting methods to pan future cost management.............4

Analysing which method is appropriate for Second Sight Plc....................................................5

REFERENCES................................................................................................................................6

EXECUTIVE SUMMARY.............................................................................................................3

Part-1................................................................................................................................................4

a. Meaning of profit and cashflow...............................................................................................4

b. Working capital, receivables, inventory and payables.............................................................4

c. How changes in working capital affect the cashflow...............................................................5

How the MDL is managed which might affect its financial results............................................5

Steps to improve the company's cashflow through working capital management......................6

EXECUTIVE SUMMARY.............................................................................................................1

Part-2................................................................................................................................................2

Purpose of preparing the budget and its different types..............................................................2

Demonstrating the applicability of budgeting methods to pan future cost management.............4

Analysing which method is appropriate for Second Sight Plc....................................................5

REFERENCES................................................................................................................................6

EXECUTIVE SUMMARY

This report represents the introduction to basic finance terms like profits, cashflow,

working capital, account receivables, payables and inventory. It also presents the impact of

changes in working capital on the cash flow of the organization. After complete analysis, the key

steps that MDL should take in order to improve its cashflow are stated.

This report represents the introduction to basic finance terms like profits, cashflow,

working capital, account receivables, payables and inventory. It also presents the impact of

changes in working capital on the cash flow of the organization. After complete analysis, the key

steps that MDL should take in order to improve its cashflow are stated.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part-1

I.

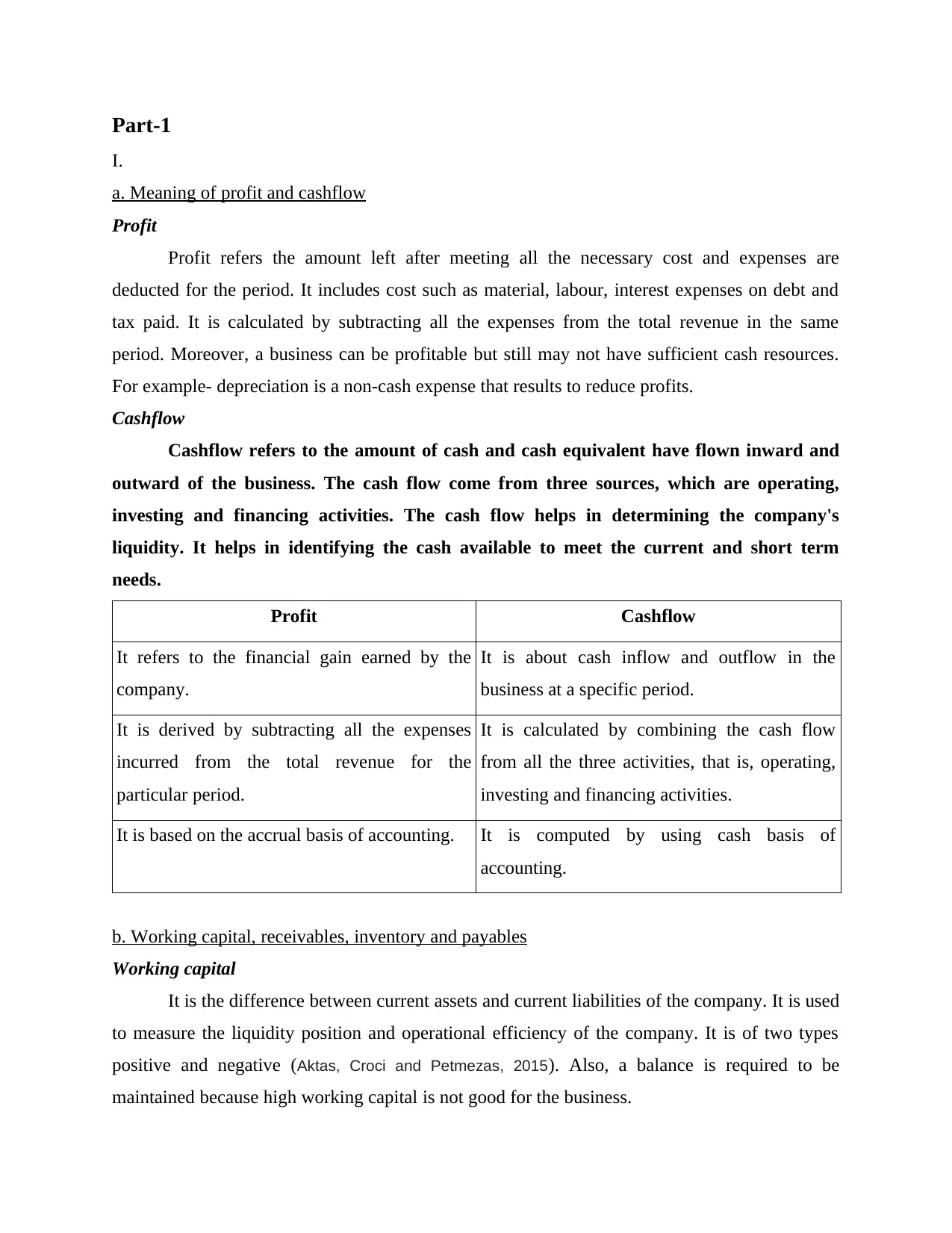

a. Meaning of profit and cashflow

Profit

Profit refers the amount left after meeting all the necessary cost and expenses are

deducted for the period. It includes cost such as material, labour, interest expenses on debt and

tax paid. It is calculated by subtracting all the expenses from the total revenue in the same

period. Moreover, a business can be profitable but still may not have sufficient cash resources.

For example- depreciation is a non-cash expense that results to reduce profits.

Cashflow

Cashflow refers to the amount of cash and cash equivalent have flown inward and

outward of the business. The cash flow come from three sources, which are operating,

investing and financing activities. The cash flow helps in determining the company's

liquidity. It helps in identifying the cash available to meet the current and short term

needs.

Profit Cashflow

It refers to the financial gain earned by the

company.

It is about cash inflow and outflow in the

business at a specific period.

It is derived by subtracting all the expenses

incurred from the total revenue for the

particular period.

It is calculated by combining the cash flow

from all the three activities, that is, operating,

investing and financing activities.

It is based on the accrual basis of accounting. It is computed by using cash basis of

accounting.

b. Working capital, receivables, inventory and payables

Working capital

It is the difference between current assets and current liabilities of the company. It is used

to measure the liquidity position and operational efficiency of the company. It is of two types

positive and negative (Aktas, Croci and Petmezas, 2015). Also, a balance is required to be

maintained because high working capital is not good for the business.

I.

a. Meaning of profit and cashflow

Profit

Profit refers the amount left after meeting all the necessary cost and expenses are

deducted for the period. It includes cost such as material, labour, interest expenses on debt and

tax paid. It is calculated by subtracting all the expenses from the total revenue in the same

period. Moreover, a business can be profitable but still may not have sufficient cash resources.

For example- depreciation is a non-cash expense that results to reduce profits.

Cashflow

Cashflow refers to the amount of cash and cash equivalent have flown inward and

outward of the business. The cash flow come from three sources, which are operating,

investing and financing activities. The cash flow helps in determining the company's

liquidity. It helps in identifying the cash available to meet the current and short term

needs.

Profit Cashflow

It refers to the financial gain earned by the

company.

It is about cash inflow and outflow in the

business at a specific period.

It is derived by subtracting all the expenses

incurred from the total revenue for the

particular period.

It is calculated by combining the cash flow

from all the three activities, that is, operating,

investing and financing activities.

It is based on the accrual basis of accounting. It is computed by using cash basis of

accounting.

b. Working capital, receivables, inventory and payables

Working capital

It is the difference between current assets and current liabilities of the company. It is used

to measure the liquidity position and operational efficiency of the company. It is of two types

positive and negative (Aktas, Croci and Petmezas, 2015). Also, a balance is required to be

maintained because high working capital is not good for the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Receivables

It is also termed as account receivables, in which debts are owed by the customers to be

paid to the company for the goods and services received. Company sell their products on credit

to customers which are shown in the balance sheet as receivables. For example, a company sells

goods of £1000 to customer for 60 days which will be shown as reduction in inventory and

increase in accounts receivables by £1000.

Inventory

Inventory refers to material and the finished products that is used by the business for the

selling and production purpose. It is the crucial and essential part of the business. It categorized

as the current asset of the business (Watson, Head, 2010). It includes raw material, work in

progress and finished goods. Companies maintain inventory to meet the unanticipated increase in

demand or to take the advantage of price breaks by placing orders in bulk. It is the important

component for calculating cost of goods sold and deriving the profits.

Payables

It is that part of the balance sheet which represents the company's obligation to pay its

debts. Sometime big organizations also have a separate department for making payment to the

company's suppliers. The sum of all this amount is shown as accounts payable on the liability

side of balance sheet.

c. How changes in working capital affect the cashflow

There is a direct impact of change in working capital on the business cash flow which is

increases the demand to maintain a balanced working capital. A positive working capital will

mean that cash has flowed in whereas negative working capital will mean company has spent

more cash in the specific period (Atrill and Mclaney, 2014). For example, if the company

purchases fixed asset then it will cause decrease in cashflow which will lead to decrease in

working capital as cash is a part of current asset. Another example, if company purchases

inventory for cash then there will be no change in the working capital as both are the part of

current assets. Thus, working capital is the core part of the company which is required to be

analysed regularly.

ii.

It is also termed as account receivables, in which debts are owed by the customers to be

paid to the company for the goods and services received. Company sell their products on credit

to customers which are shown in the balance sheet as receivables. For example, a company sells

goods of £1000 to customer for 60 days which will be shown as reduction in inventory and

increase in accounts receivables by £1000.

Inventory

Inventory refers to material and the finished products that is used by the business for the

selling and production purpose. It is the crucial and essential part of the business. It categorized

as the current asset of the business (Watson, Head, 2010). It includes raw material, work in

progress and finished goods. Companies maintain inventory to meet the unanticipated increase in

demand or to take the advantage of price breaks by placing orders in bulk. It is the important

component for calculating cost of goods sold and deriving the profits.

Payables

It is that part of the balance sheet which represents the company's obligation to pay its

debts. Sometime big organizations also have a separate department for making payment to the

company's suppliers. The sum of all this amount is shown as accounts payable on the liability

side of balance sheet.

c. How changes in working capital affect the cashflow

There is a direct impact of change in working capital on the business cash flow which is

increases the demand to maintain a balanced working capital. A positive working capital will

mean that cash has flowed in whereas negative working capital will mean company has spent

more cash in the specific period (Atrill and Mclaney, 2014). For example, if the company

purchases fixed asset then it will cause decrease in cashflow which will lead to decrease in

working capital as cash is a part of current asset. Another example, if company purchases

inventory for cash then there will be no change in the working capital as both are the part of

current assets. Thus, working capital is the core part of the company which is required to be

analysed regularly.

ii.

How the MDL is managed which might affect its financial results

MDL has a wide spread business throughout the South of England, Last year, it has

turnover of over £50 million. MDL has acquired 40% stake in Italian company and has also

invested £10 million to acquire the shares. But on the other hand, the company owes £1.5 million

pounds to Delios. Also, it is facing a dispute of about £2 million in respect to delivery to San

Pedro in 2017. Apart from this, there are the chances that a legal action can be taken by Valetta

for non payment of dues by MDL. The company is also having the large stock of inventory in its

warehouse and company thinks that it will be of use after all the issues are sorted. So, based on

the current situation of the company, it should for now stop further investment and look for the

ways to pay its debt as soon as possible. Also, it should sell all its inventory as it may cause a

huge loss if waited for the dispute to be resolved. Otherwise, there are the chances that the

company might face liquidity crisis and may go bankrupt.

As all these things will make the situation more complicated. It will directly affect the

cash flow and profits of the organization. Also, it will increase the liability of the MDL because

of increase in debt which is required to repaid along with interest. MDL needs to recover its

money blocked by the customers by forcing them to pay back as quickly as possible.

iii.

Steps to improve the company's cashflow through working capital management

There are number of steps that can be taken by the organization in order to improve its

cash flow by effectively managing the working capital. Some important measures are stated

below.

The company should review its expenses regularly which will help in maintaining the

proper record of it.

MDL needs to make sure to met its obligation on time by using electronic payment

system which will help in ensuring timely payments and also helps in avoiding the

situation of delay payments.

MDL can also postpone the current capital expenditure plan in order to meet its current

cash needs.

The company should contact vendors and suppliers to offer better discounts which will

help in saving the finances. And it is also required to maintain a cordial relationship with

the vendors which will help in at the time of crisis in overcoming the situation.

MDL has a wide spread business throughout the South of England, Last year, it has

turnover of over £50 million. MDL has acquired 40% stake in Italian company and has also

invested £10 million to acquire the shares. But on the other hand, the company owes £1.5 million

pounds to Delios. Also, it is facing a dispute of about £2 million in respect to delivery to San

Pedro in 2017. Apart from this, there are the chances that a legal action can be taken by Valetta

for non payment of dues by MDL. The company is also having the large stock of inventory in its

warehouse and company thinks that it will be of use after all the issues are sorted. So, based on

the current situation of the company, it should for now stop further investment and look for the

ways to pay its debt as soon as possible. Also, it should sell all its inventory as it may cause a

huge loss if waited for the dispute to be resolved. Otherwise, there are the chances that the

company might face liquidity crisis and may go bankrupt.

As all these things will make the situation more complicated. It will directly affect the

cash flow and profits of the organization. Also, it will increase the liability of the MDL because

of increase in debt which is required to repaid along with interest. MDL needs to recover its

money blocked by the customers by forcing them to pay back as quickly as possible.

iii.

Steps to improve the company's cashflow through working capital management

There are number of steps that can be taken by the organization in order to improve its

cash flow by effectively managing the working capital. Some important measures are stated

below.

The company should review its expenses regularly which will help in maintaining the

proper record of it.

MDL needs to make sure to met its obligation on time by using electronic payment

system which will help in ensuring timely payments and also helps in avoiding the

situation of delay payments.

MDL can also postpone the current capital expenditure plan in order to meet its current

cash needs.

The company should contact vendors and suppliers to offer better discounts which will

help in saving the finances. And it is also required to maintain a cordial relationship with

the vendors which will help in at the time of crisis in overcoming the situation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

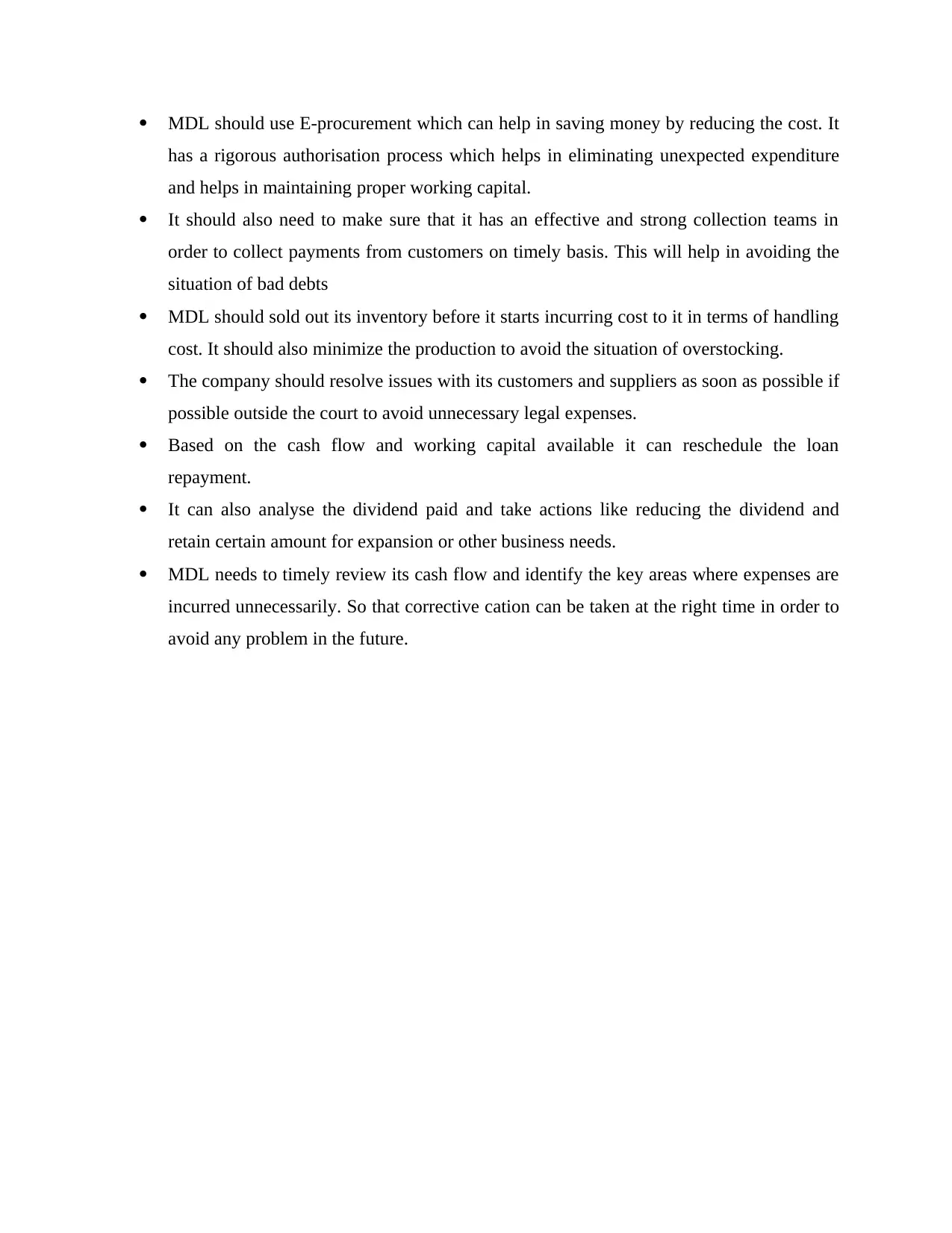

MDL should use E-procurement which can help in saving money by reducing the cost. It

has a rigorous authorisation process which helps in eliminating unexpected expenditure

and helps in maintaining proper working capital.

It should also need to make sure that it has an effective and strong collection teams in

order to collect payments from customers on timely basis. This will help in avoiding the

situation of bad debts

MDL should sold out its inventory before it starts incurring cost to it in terms of handling

cost. It should also minimize the production to avoid the situation of overstocking.

The company should resolve issues with its customers and suppliers as soon as possible if

possible outside the court to avoid unnecessary legal expenses.

Based on the cash flow and working capital available it can reschedule the loan

repayment.

It can also analyse the dividend paid and take actions like reducing the dividend and

retain certain amount for expansion or other business needs.

MDL needs to timely review its cash flow and identify the key areas where expenses are

incurred unnecessarily. So that corrective cation can be taken at the right time in order to

avoid any problem in the future.

has a rigorous authorisation process which helps in eliminating unexpected expenditure

and helps in maintaining proper working capital.

It should also need to make sure that it has an effective and strong collection teams in

order to collect payments from customers on timely basis. This will help in avoiding the

situation of bad debts

MDL should sold out its inventory before it starts incurring cost to it in terms of handling

cost. It should also minimize the production to avoid the situation of overstocking.

The company should resolve issues with its customers and suppliers as soon as possible if

possible outside the court to avoid unnecessary legal expenses.

Based on the cash flow and working capital available it can reschedule the loan

repayment.

It can also analyse the dividend paid and take actions like reducing the dividend and

retain certain amount for expansion or other business needs.

MDL needs to timely review its cash flow and identify the key areas where expenses are

incurred unnecessarily. So that corrective cation can be taken at the right time in order to

avoid any problem in the future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report presents the different methods of budgeting that can be used by the

organization as per the need. It includes traditional method of budgeting and other alternative

methods of budgeting like activity and zero based budgeting, rolling budget etc. Based on the

findings, the activity based budgeting method is best suited to the Second Sight Plc for its new

facility planning.

1

This report presents the different methods of budgeting that can be used by the

organization as per the need. It includes traditional method of budgeting and other alternative

methods of budgeting like activity and zero based budgeting, rolling budget etc. Based on the

findings, the activity based budgeting method is best suited to the Second Sight Plc for its new

facility planning.

1

Part-2

I.

Purpose of preparing the budget and its different types

Budget is the report which is prepared for implementing new project or plan into action.

It provides a structure based on which the planning and controlling process is done. It is an

essential part of long term planning (Atrill & McLaney, 2009). It is prepared based on previous

year's data with an increment in the amount in the new budget, also known as incremental

budget. There are different types of budgets which are stated below.

Traditional budgeting approach

It is the method of preparing budget by taking into consideration the budget prepared for

previous year based on which current year budget is prepared. It is depends exactly on the

previous years spending and then adding or subtracting the inflation rate and the changing

market situation. Only those items are required to be justified which are beyond the previous

year's budget. It's easy to use framework has made it easy for organization to manage its

activities because they are use to it.

Strengths:

It is easy to set up and implement as it relies on the past data.

This method helps in better decision making. It brings stability in the organization as everyone is aware of what is required to be done.

Weaknesses:

It is rigid in nature.

It can cause budget slack as managers can easily change the numbers as per the

requirement.

Chances of getting errors is high as it completely depends on past year data.

Other alternative budget reports

Rolling budgets

It is also known as continuous budget. This budget is updated by the adding further

period when the previous one is completed. Companies prepare these budgets in different

intervals such as monthly, quarterly etc. It requires a lot of time and efforts to prepare but once it

is prepared then extending it further is very easy.

Strengths:

2

I.

Purpose of preparing the budget and its different types

Budget is the report which is prepared for implementing new project or plan into action.

It provides a structure based on which the planning and controlling process is done. It is an

essential part of long term planning (Atrill & McLaney, 2009). It is prepared based on previous

year's data with an increment in the amount in the new budget, also known as incremental

budget. There are different types of budgets which are stated below.

Traditional budgeting approach

It is the method of preparing budget by taking into consideration the budget prepared for

previous year based on which current year budget is prepared. It is depends exactly on the

previous years spending and then adding or subtracting the inflation rate and the changing

market situation. Only those items are required to be justified which are beyond the previous

year's budget. It's easy to use framework has made it easy for organization to manage its

activities because they are use to it.

Strengths:

It is easy to set up and implement as it relies on the past data.

This method helps in better decision making. It brings stability in the organization as everyone is aware of what is required to be done.

Weaknesses:

It is rigid in nature.

It can cause budget slack as managers can easily change the numbers as per the

requirement.

Chances of getting errors is high as it completely depends on past year data.

Other alternative budget reports

Rolling budgets

It is also known as continuous budget. This budget is updated by the adding further

period when the previous one is completed. Companies prepare these budgets in different

intervals such as monthly, quarterly etc. It requires a lot of time and efforts to prepare but once it

is prepared then extending it further is very easy.

Strengths:

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps in effective planning and controlling which helps in reducing uncertainty.

This method is flexible enough to make changes in between. It takes into consideration long term planning.

Weaknesses:

It is a time consuming process.

Frequent changes in the budget target may lead to demoralizing the employees of the

organization.

It is not suited for the organizations where the working business conditions does not

change.

Zero based budgets

In this method, budget is prepared from the base level or the zero level. Under this,

proper justification is required before adding it to the actual budget. The major objective of this

budget is to identify unnecessary expenses so that it can be eliminated. Organizations adopt this

method of budgeting when there are frequent changes in the business conditions.

Strengths:

It helps in effective allocation of resources department wise.

This method is accurate and helps in reducing the unwanted cost. It involves better communication within departments which assists in better decision

making.

Weaknesses:

It requires large number of people in order to prepare budget.

It is a time consuming approach.

This approach requires highly skilled personnels.

Activity based budget

This budget is prepared after considering the relevant cost, that is, overhead cost. In this

method, past year's data is not used by the budget is prepared by deeply analysing the cost. Based

on which resources are allocated (Weetman, 2006). It separately evaluates different activities and

processes undertaken. The objective is to bring efficiency in the business. It is activity oriented.

Strengths:

It is practical in approach and is easy for employees to communicate.

3

This method is flexible enough to make changes in between. It takes into consideration long term planning.

Weaknesses:

It is a time consuming process.

Frequent changes in the budget target may lead to demoralizing the employees of the

organization.

It is not suited for the organizations where the working business conditions does not

change.

Zero based budgets

In this method, budget is prepared from the base level or the zero level. Under this,

proper justification is required before adding it to the actual budget. The major objective of this

budget is to identify unnecessary expenses so that it can be eliminated. Organizations adopt this

method of budgeting when there are frequent changes in the business conditions.

Strengths:

It helps in effective allocation of resources department wise.

This method is accurate and helps in reducing the unwanted cost. It involves better communication within departments which assists in better decision

making.

Weaknesses:

It requires large number of people in order to prepare budget.

It is a time consuming approach.

This approach requires highly skilled personnels.

Activity based budget

This budget is prepared after considering the relevant cost, that is, overhead cost. In this

method, past year's data is not used by the budget is prepared by deeply analysing the cost. Based

on which resources are allocated (Weetman, 2006). It separately evaluates different activities and

processes undertaken. The objective is to bring efficiency in the business. It is activity oriented.

Strengths:

It is practical in approach and is easy for employees to communicate.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It provides a better insight on inefficient processes and helps in identifying the area of

improvement. This method helps in exercising control over the expenses.

Weaknesses:

It is very costly to implement.

This method focusses on short term needs of the business.

It also requires highly professional employees.

ii.

Demonstrating the applicability of budgeting methods to pan future cost management

A detailed analysis of the usage budgeting methods on Second Sight Plc is described

below.

Traditional method

The organization Second Sight Plc is currently using traditional method of budgeting.

This approach has been used over many years. The organization is having various department

and this method of budgeting has been very simple and has form a coordination across all the

functional units (Drury, 2005). This method of budgeting can be used by Second Sight Plc if the

change is no major change in the budget and the business goes the same. For example, in the

previous year the budget for expenses was £3 million and for the current year also, the budget

remains the same with minor changes so this can be used by the organization.

Rolling budget

The rolling budget if used by Second Sight Plc, it will be beneficial in terms of planning

and controlling. Also, it is very flexible as changes can be made in it in between. For example,

company with 12 months planning from January to December. After the completion of January it

will add the another month from the next year because of which plan will still be of 12 months

but it will be from February to next year's January.

Zero based budgets

This budget if adopted by Second Sight Plc, then it will help in effective allocation of

resources. As budget is prepared from the scratch, it evaluates each and every expenses of every

department and after identifying the result it will allocate the resources as per the requirement.

The only problem with this method is that it is time consuming.

Activity based budget

4

improvement. This method helps in exercising control over the expenses.

Weaknesses:

It is very costly to implement.

This method focusses on short term needs of the business.

It also requires highly professional employees.

ii.

Demonstrating the applicability of budgeting methods to pan future cost management

A detailed analysis of the usage budgeting methods on Second Sight Plc is described

below.

Traditional method

The organization Second Sight Plc is currently using traditional method of budgeting.

This approach has been used over many years. The organization is having various department

and this method of budgeting has been very simple and has form a coordination across all the

functional units (Drury, 2005). This method of budgeting can be used by Second Sight Plc if the

change is no major change in the budget and the business goes the same. For example, in the

previous year the budget for expenses was £3 million and for the current year also, the budget

remains the same with minor changes so this can be used by the organization.

Rolling budget

The rolling budget if used by Second Sight Plc, it will be beneficial in terms of planning

and controlling. Also, it is very flexible as changes can be made in it in between. For example,

company with 12 months planning from January to December. After the completion of January it

will add the another month from the next year because of which plan will still be of 12 months

but it will be from February to next year's January.

Zero based budgets

This budget if adopted by Second Sight Plc, then it will help in effective allocation of

resources. As budget is prepared from the scratch, it evaluates each and every expenses of every

department and after identifying the result it will allocate the resources as per the requirement.

The only problem with this method is that it is time consuming.

Activity based budget

4

This method of budgeting will help in evaluating the cost separately for each and every

activity. Second sight Plc can use this method which will help it in determining the cost

associated with different activities. This will help in identifying the unnecessary cost so that r

necessary actions can be taken for reducing the cost. For example, company has estimated the

sales order of 20000 in the next year with each order cost £5, thus, based on this method,

expenses pertaining to the sales order for the next year is £100,000. If this budget is compared to

traditional method, then if last year's sales budget was £80000 and is expected to grow at 10%,

then only £88000 is budgeted.

iii.

Analysing which method is appropriate for Second Sight Plc

For the very long time the Second Sight Plc is using traditional budgeting method which

has been working very well for it. But with the emerging changes, the idea to implement any

new method is right. Other than the traditional method, other alternative methods are rolling out

budget, zero based and activity based budget. The objective of Second Sight Plc is to identify

any hidden cost or errors in the previous budget which can be determined in the new one. So,

that timely actions can be taken before the company can move ahead with other significant

changes. According to the Second Sight Plc business, the best and appropriate method will be

activity based budgeting. It will help the company in identifying the cost associated with

different activities or tasks undertaken by it. It will also provide more improved information

about the activities and processes which in turn help in identifying the unnecessary cost and

processes so that it can be eliminated. Apart from this, this method will also help in exercising

control over the activities in order to reduce cost. The major weakness in relation to this method

is that it is very costly and requires highly skilled and knowledgeable professionals. Second

Sight Plc for its new facility in Netherlands and Chennai, should implement activity based

budgeting method.

5

activity. Second sight Plc can use this method which will help it in determining the cost

associated with different activities. This will help in identifying the unnecessary cost so that r

necessary actions can be taken for reducing the cost. For example, company has estimated the

sales order of 20000 in the next year with each order cost £5, thus, based on this method,

expenses pertaining to the sales order for the next year is £100,000. If this budget is compared to

traditional method, then if last year's sales budget was £80000 and is expected to grow at 10%,

then only £88000 is budgeted.

iii.

Analysing which method is appropriate for Second Sight Plc

For the very long time the Second Sight Plc is using traditional budgeting method which

has been working very well for it. But with the emerging changes, the idea to implement any

new method is right. Other than the traditional method, other alternative methods are rolling out

budget, zero based and activity based budget. The objective of Second Sight Plc is to identify

any hidden cost or errors in the previous budget which can be determined in the new one. So,

that timely actions can be taken before the company can move ahead with other significant

changes. According to the Second Sight Plc business, the best and appropriate method will be

activity based budgeting. It will help the company in identifying the cost associated with

different activities or tasks undertaken by it. It will also provide more improved information

about the activities and processes which in turn help in identifying the unnecessary cost and

processes so that it can be eliminated. Apart from this, this method will also help in exercising

control over the activities in order to reduce cost. The major weakness in relation to this method

is that it is very costly and requires highly skilled and knowledgeable professionals. Second

Sight Plc for its new facility in Netherlands and Chennai, should implement activity based

budgeting method.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.