Business Finance Report: Analysis of Cash Flow and Budgetary Systems

VerifiedAdded on 2023/01/19

|10

|3155

|71

Report

AI Summary

This report provides a comprehensive analysis of key business finance concepts. It begins by defining and differentiating between profit and cash flow, and then explores the components of working capital, including receivables, inventory, and payables, and how changes in working capital affect cash flow. The report applies these concepts to the case of Bright Lawns Ltd., identifying issues related to working capital management and offering recommendations for improvement. The second part of the report focuses on budgeting, explaining the purposes of preparing a budget and comparing traditional and alternative budgetary systems, such as rolling budgets, zero-based budgets, and activity-based budgets. The application of these methods in cost management is demonstrated, and an analysis is provided on the appropriateness of each system for different business contexts, using Boat World Plc. as a case study.

Business

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Explanation of different components...........................................................................................1

Application of concepts...............................................................................................................3

Analysis and recommendation about the steps which should be taken to improve company's

cash flow through working capital management.........................................................................3

PART 2............................................................................................................................................4

Understanding of purposes of preparing a budget and explanation of tradition and alternative

budgetary systems........................................................................................................................4

Demonstration of the application of the methods to show their use in planning future cost

management.................................................................................................................................6

Analysis of whether traditional or alternative budgetary system is appropriate to all or any

parts of the business.....................................................................................................................6

CONCLUSION................................................................................................................................7

REFERNCES...................................................................................................................................8

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

Explanation of different components...........................................................................................1

Application of concepts...............................................................................................................3

Analysis and recommendation about the steps which should be taken to improve company's

cash flow through working capital management.........................................................................3

PART 2............................................................................................................................................4

Understanding of purposes of preparing a budget and explanation of tradition and alternative

budgetary systems........................................................................................................................4

Demonstration of the application of the methods to show their use in planning future cost

management.................................................................................................................................6

Analysis of whether traditional or alternative budgetary system is appropriate to all or any

parts of the business.....................................................................................................................6

CONCLUSION................................................................................................................................7

REFERNCES...................................................................................................................................8

INTRODUCTION

Business finance can be defined as the money which is used by organisations for the

purpose of running all the operational activities. If there is lack of it then it may affect the

efficiency of carrying out operations (Burns and Dewhurst, 2016). This assignment is divided in

two parts, first one is based upon Bright Lawns Ltd. which is operating its business in London,

Birmingham and Manchester. Second one is based on Boat World Plc which is an international

leisure company that rents boats to the holiday makers and operates in France and United

Kingdom. This project covers various topics such as profit, cash flow and their differences,

working capital, receivables, inventory, payables and the way in which working capital changes

affect cash flow. Along with this, application of concepts, steps to be taken to improve cash

slow, purpose of preparing budget, different methods for their preparation and application and

discussion regarding appropriateness of traditional and alternative budgetary system are also

covered in this report.

PART 1

Explanation of different components

Profit: It can be defined as financial gain which is generated by an organisation by

selling its products and services to clients. While calculating it the accounting professionals are

required to deduct costs from the amount which is received from selling activities. All the

incomes which are generated by an organisation after deduction the expenses is known as profit.

It is mainly analysed by shareholders for the purpose of measuring success and ability of a

company to generate profits.

Cash flow: It is the total of monetary resources which are transferred in and out of a

business for the purpose of facilitating the process of carrying out operational activities. In other

words, it can be defined as the procedure in which money flows inward and outward of a

company. It is the total amount of cash and other cash equivalents that are available to an

enterprise (Canales, 2016).

Difference between profit and cash flow: There are various differences between cash

flow and profits. All of them are described below:

Cash flow Profit

1

Business finance can be defined as the money which is used by organisations for the

purpose of running all the operational activities. If there is lack of it then it may affect the

efficiency of carrying out operations (Burns and Dewhurst, 2016). This assignment is divided in

two parts, first one is based upon Bright Lawns Ltd. which is operating its business in London,

Birmingham and Manchester. Second one is based on Boat World Plc which is an international

leisure company that rents boats to the holiday makers and operates in France and United

Kingdom. This project covers various topics such as profit, cash flow and their differences,

working capital, receivables, inventory, payables and the way in which working capital changes

affect cash flow. Along with this, application of concepts, steps to be taken to improve cash

slow, purpose of preparing budget, different methods for their preparation and application and

discussion regarding appropriateness of traditional and alternative budgetary system are also

covered in this report.

PART 1

Explanation of different components

Profit: It can be defined as financial gain which is generated by an organisation by

selling its products and services to clients. While calculating it the accounting professionals are

required to deduct costs from the amount which is received from selling activities. All the

incomes which are generated by an organisation after deduction the expenses is known as profit.

It is mainly analysed by shareholders for the purpose of measuring success and ability of a

company to generate profits.

Cash flow: It is the total of monetary resources which are transferred in and out of a

business for the purpose of facilitating the process of carrying out operational activities. In other

words, it can be defined as the procedure in which money flows inward and outward of a

company. It is the total amount of cash and other cash equivalents that are available to an

enterprise (Canales, 2016).

Difference between profit and cash flow: There are various differences between cash

flow and profits. All of them are described below:

Cash flow Profit

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

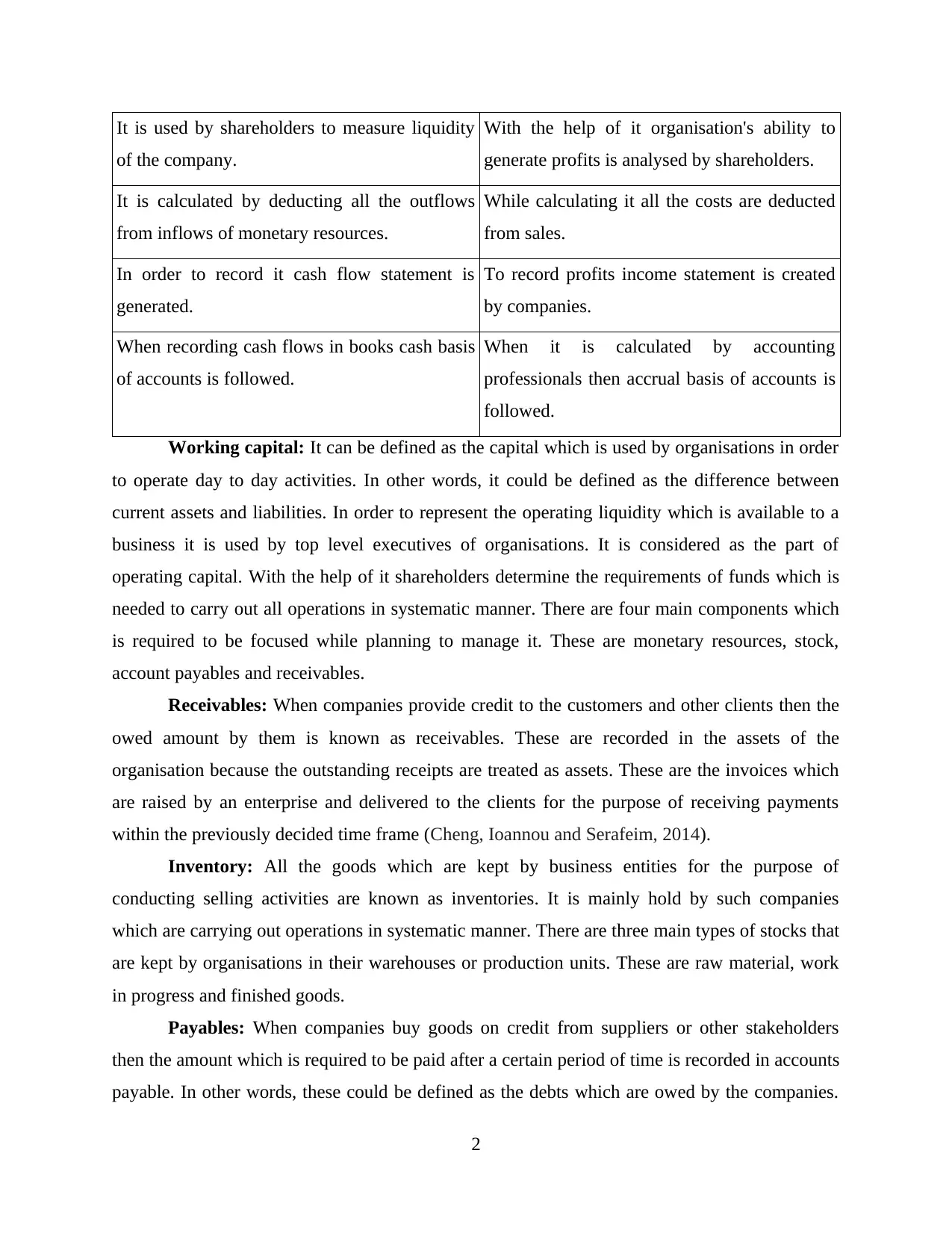

It is used by shareholders to measure liquidity

of the company.

With the help of it organisation's ability to

generate profits is analysed by shareholders.

It is calculated by deducting all the outflows

from inflows of monetary resources.

While calculating it all the costs are deducted

from sales.

In order to record it cash flow statement is

generated.

To record profits income statement is created

by companies.

When recording cash flows in books cash basis

of accounts is followed.

When it is calculated by accounting

professionals then accrual basis of accounts is

followed.

Working capital: It can be defined as the capital which is used by organisations in order

to operate day to day activities. In other words, it could be defined as the difference between

current assets and liabilities. In order to represent the operating liquidity which is available to a

business it is used by top level executives of organisations. It is considered as the part of

operating capital. With the help of it shareholders determine the requirements of funds which is

needed to carry out all operations in systematic manner. There are four main components which

is required to be focused while planning to manage it. These are monetary resources, stock,

account payables and receivables.

Receivables: When companies provide credit to the customers and other clients then the

owed amount by them is known as receivables. These are recorded in the assets of the

organisation because the outstanding receipts are treated as assets. These are the invoices which

are raised by an enterprise and delivered to the clients for the purpose of receiving payments

within the previously decided time frame (Cheng, Ioannou and Serafeim, 2014).

Inventory: All the goods which are kept by business entities for the purpose of

conducting selling activities are known as inventories. It is mainly hold by such companies

which are carrying out operations in systematic manner. There are three main types of stocks that

are kept by organisations in their warehouses or production units. These are raw material, work

in progress and finished goods.

Payables: When companies buy goods on credit from suppliers or other stakeholders

then the amount which is required to be paid after a certain period of time is recorded in accounts

payable. In other words, these could be defined as the debts which are owed by the companies.

2

of the company.

With the help of it organisation's ability to

generate profits is analysed by shareholders.

It is calculated by deducting all the outflows

from inflows of monetary resources.

While calculating it all the costs are deducted

from sales.

In order to record it cash flow statement is

generated.

To record profits income statement is created

by companies.

When recording cash flows in books cash basis

of accounts is followed.

When it is calculated by accounting

professionals then accrual basis of accounts is

followed.

Working capital: It can be defined as the capital which is used by organisations in order

to operate day to day activities. In other words, it could be defined as the difference between

current assets and liabilities. In order to represent the operating liquidity which is available to a

business it is used by top level executives of organisations. It is considered as the part of

operating capital. With the help of it shareholders determine the requirements of funds which is

needed to carry out all operations in systematic manner. There are four main components which

is required to be focused while planning to manage it. These are monetary resources, stock,

account payables and receivables.

Receivables: When companies provide credit to the customers and other clients then the

owed amount by them is known as receivables. These are recorded in the assets of the

organisation because the outstanding receipts are treated as assets. These are the invoices which

are raised by an enterprise and delivered to the clients for the purpose of receiving payments

within the previously decided time frame (Cheng, Ioannou and Serafeim, 2014).

Inventory: All the goods which are kept by business entities for the purpose of

conducting selling activities are known as inventories. It is mainly hold by such companies

which are carrying out operations in systematic manner. There are three main types of stocks that

are kept by organisations in their warehouses or production units. These are raw material, work

in progress and finished goods.

Payables: When companies buy goods on credit from suppliers or other stakeholders

then the amount which is required to be paid after a certain period of time is recorded in accounts

payable. In other words, these could be defined as the debts which are owed by the companies.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The amount which will be paid in future is recorded in liabilities side because it is a

responsibility of the company to pay the amount to creditors.

The way in which changes in working capital affect cash flow: If there are end

number of changes in working capital then it may affect the cash flow because if the debtors are

not paying the amount then it will decrease the amount of current assets. Due to this working

capital will be affected that will also leave impact upon cash flow because the organisation will

have to write off the amount of bad debts from its available funds (Haeger, 2017).

Application of concepts

All the concepts which are described in the above questions are applied in the Bright

Lawns Ltd. First one which is analysed is profit before interest and tax which is 5 Million

Pounds. Payables for the company are 1.5 million pounds and outstanding dispute is costing

around 2 million pound. Due to all these figures the working capital of the company may get

affected as fluctuation in all of them may result in decrement of increment of it. Cash flow

concept is also applied within the organisation because inflow and outflow of funds results in it.

The company is not managed by management properly because the additional outstanding

amount of 2 million pound consignment was completed in year 2017 which has led to payment

being withheld while negotiations. Another issue which has taken place is that Simmo believes

that Brico France problem of 2 million pound is faced by the company due to faulty

workmanship of contractor and the payment for the work is being stopped. All these issues are

affecting financial results of the company because due to this organisation is not able to analyse

its actual profits for the business.

Analysis and recommendation about the steps which should be taken to improve company's cash

flow through working capital management

There are various steps could be taken by the company to improve cash flow through

better working capital management. All of them are as follows:

Organisation can reduce the credit period which is offered to the debtors it can help to

acquire funds earlier and maintain cash flow (Jordà, Schularick and Taylor, 2016).

The managers can cut costs for future period which can help to improve the cash flow.

In order to manage the working capital organisation can reduce the expenses which may

help to improve cash flow.

3

responsibility of the company to pay the amount to creditors.

The way in which changes in working capital affect cash flow: If there are end

number of changes in working capital then it may affect the cash flow because if the debtors are

not paying the amount then it will decrease the amount of current assets. Due to this working

capital will be affected that will also leave impact upon cash flow because the organisation will

have to write off the amount of bad debts from its available funds (Haeger, 2017).

Application of concepts

All the concepts which are described in the above questions are applied in the Bright

Lawns Ltd. First one which is analysed is profit before interest and tax which is 5 Million

Pounds. Payables for the company are 1.5 million pounds and outstanding dispute is costing

around 2 million pound. Due to all these figures the working capital of the company may get

affected as fluctuation in all of them may result in decrement of increment of it. Cash flow

concept is also applied within the organisation because inflow and outflow of funds results in it.

The company is not managed by management properly because the additional outstanding

amount of 2 million pound consignment was completed in year 2017 which has led to payment

being withheld while negotiations. Another issue which has taken place is that Simmo believes

that Brico France problem of 2 million pound is faced by the company due to faulty

workmanship of contractor and the payment for the work is being stopped. All these issues are

affecting financial results of the company because due to this organisation is not able to analyse

its actual profits for the business.

Analysis and recommendation about the steps which should be taken to improve company's cash

flow through working capital management

There are various steps could be taken by the company to improve cash flow through

better working capital management. All of them are as follows:

Organisation can reduce the credit period which is offered to the debtors it can help to

acquire funds earlier and maintain cash flow (Jordà, Schularick and Taylor, 2016).

The managers can cut costs for future period which can help to improve the cash flow.

In order to manage the working capital organisation can reduce the expenses which may

help to improve cash flow.

3

PART 2

Understanding of purposes of preparing a budget and explanation of tradition and alternative

budgetary systems

Budget: It can be defined as a financial plan which is formed by organisations so that all

operational activities could be performed appropriately. With the help of it future incomes and

expenses could be estimated by management. It is mainly generated on yearly, half yearly and

quarterly basis.

Purposes of preparing a budget: In all the companies budgets are prepared for different

purposes. All of them could be understood with the help of following pointers:

Budget is prepared for the purpose of taking control over all overspending of financial

resources.

Another purpose of formulating budget is to making sure that organisations is having

sufficient funds to perform operations in future (McLean and Zhao, 2014).

Traditional budgeting approaches: These are the budgets in which last year's financial

information is used as a basis for current year. All the approaches of it are as follows with their

strengths and weaknesses:

Incremental budget: It is a traditional approach of budgeting in which previous year's

data is used to create budget of current year. Main purpose of it is to determine actual

performance of business. The amounts which are recorded in it include adjustment for different

elements such as inflation, increase in selling price or cost etc. All the strengths and weaknesses

of it are as follows:

Strengths: It is an easy to prepare and understand method for budgeting which takes less

time and results in lower cost for company. With the help of it conflicts amount different

departments could be ignored because a consistent approach is followed within the

organisation.

Weaknesses: In this method all the costs are not justified by the organisation that create

issues to analyse the actual performance of the company.

Alternative budget methods:

Rolling budget: This is a budget which is updated continuously for the purpose of being

updated about the latest changes in the financial position of the company. With the help of it up

to date decisions could be formulated by the managers of companies such as Boat World Plc

4

Understanding of purposes of preparing a budget and explanation of tradition and alternative

budgetary systems

Budget: It can be defined as a financial plan which is formed by organisations so that all

operational activities could be performed appropriately. With the help of it future incomes and

expenses could be estimated by management. It is mainly generated on yearly, half yearly and

quarterly basis.

Purposes of preparing a budget: In all the companies budgets are prepared for different

purposes. All of them could be understood with the help of following pointers:

Budget is prepared for the purpose of taking control over all overspending of financial

resources.

Another purpose of formulating budget is to making sure that organisations is having

sufficient funds to perform operations in future (McLean and Zhao, 2014).

Traditional budgeting approaches: These are the budgets in which last year's financial

information is used as a basis for current year. All the approaches of it are as follows with their

strengths and weaknesses:

Incremental budget: It is a traditional approach of budgeting in which previous year's

data is used to create budget of current year. Main purpose of it is to determine actual

performance of business. The amounts which are recorded in it include adjustment for different

elements such as inflation, increase in selling price or cost etc. All the strengths and weaknesses

of it are as follows:

Strengths: It is an easy to prepare and understand method for budgeting which takes less

time and results in lower cost for company. With the help of it conflicts amount different

departments could be ignored because a consistent approach is followed within the

organisation.

Weaknesses: In this method all the costs are not justified by the organisation that create

issues to analyse the actual performance of the company.

Alternative budget methods:

Rolling budget: This is a budget which is updated continuously for the purpose of being

updated about the latest changes in the financial position of the company. With the help of it up

to date decisions could be formulated by the managers of companies such as Boat World Plc

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

because it helps them to to get detailed and latest information regarding modifications which are

made in the budgets (Rolling budget, 2019). Following are its strengths and weaknesses:

Strengths: It helps companies and managers to be more responsive to the unforeseen

changes in the reports as it keeps up to date information. There is high level of flexibility

in this budget because it could be updated any time.

Weaknesses: One of the main weakness of it is that it is similar to the process of

preparing a budget again and again that may result in lack of focus of managers. The time

required to prepare it is very high.

Zero based budget: This budget is prepared with a zero base in which a new financial

plan for each year is generated. While using this method of budgeting it is very important for

companies such as Boat World Plc to justify all the incomes and expenses which are recorded in

the books. Previous year's data is not used while formulating it as it is prepared for the purpose

of analysing performance of all the year's performance separately. All the strengths and

weaknesses of it are as follows:

Strengths: It guides managers to justify all the incomes and expenses which is beneficial

for the company to determine actual performance for the current accounting year. With

the help of it efficiency of resource allocation could be enhanced (Mian and Sufi, 2018).

Weaknesses: It could not be used for long term purposes because it covers information

of single year. The process of formulating it is very rigid as managers may face confusion

while recording prepaid or outstanding amounts in the books.

Activity based budget: It is a budgeting method in which organisations such as Boat

World Plc formulate budget according to different activities which are performed for business

execution. Main purpose of it is to record and analyse different operations so that funds could be

allocated according to their requirements. All the strengths and weaknesses of it are as follows:

Strengths: It can help the managers to analyse cost per unit in accurate manner. With the

help of it pricing, sales strategy, management and performance related decisions could be

formed in systematic manner.

Weaknesses: The process which is followed to collect and prepare records is time

consuming. The sources that are required to gather data are not always available to form

decisions which create difficulties for the process of decision making (Roberts, 2015).

5

made in the budgets (Rolling budget, 2019). Following are its strengths and weaknesses:

Strengths: It helps companies and managers to be more responsive to the unforeseen

changes in the reports as it keeps up to date information. There is high level of flexibility

in this budget because it could be updated any time.

Weaknesses: One of the main weakness of it is that it is similar to the process of

preparing a budget again and again that may result in lack of focus of managers. The time

required to prepare it is very high.

Zero based budget: This budget is prepared with a zero base in which a new financial

plan for each year is generated. While using this method of budgeting it is very important for

companies such as Boat World Plc to justify all the incomes and expenses which are recorded in

the books. Previous year's data is not used while formulating it as it is prepared for the purpose

of analysing performance of all the year's performance separately. All the strengths and

weaknesses of it are as follows:

Strengths: It guides managers to justify all the incomes and expenses which is beneficial

for the company to determine actual performance for the current accounting year. With

the help of it efficiency of resource allocation could be enhanced (Mian and Sufi, 2018).

Weaknesses: It could not be used for long term purposes because it covers information

of single year. The process of formulating it is very rigid as managers may face confusion

while recording prepaid or outstanding amounts in the books.

Activity based budget: It is a budgeting method in which organisations such as Boat

World Plc formulate budget according to different activities which are performed for business

execution. Main purpose of it is to record and analyse different operations so that funds could be

allocated according to their requirements. All the strengths and weaknesses of it are as follows:

Strengths: It can help the managers to analyse cost per unit in accurate manner. With the

help of it pricing, sales strategy, management and performance related decisions could be

formed in systematic manner.

Weaknesses: The process which is followed to collect and prepare records is time

consuming. The sources that are required to gather data are not always available to form

decisions which create difficulties for the process of decision making (Roberts, 2015).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Demonstration of the application of the methods to show their use in planning future cost

management

The management in Boat World Plc is using tradition budgeting since last few years and

now it can use different alternative methods for the purpose of planning future cost management

for the company. For example, in traditional approach the company can budget the plan of

opening new out let in Netherlands and Germany with the help of previous year's data. The rates

for them could be set according to the old one's which are used for renting boats in existing

places.

In alternative methods of budgeting the management of the organisation can create a

budget with the help of zero based budget in which a new plan could be formed with a zero

balance. It will be beneficial for the company because here the strategy will be made on the basis

of new areas where business will be operated (Rogers and Makonnen, 2014).

Activity based budget could be used by Boat World Plc to allocate funds to different

activities such as marketing, selling etc. With the help of this technique organisation will be able

to perform all the operations in systematic manner because costs for all of them will be

determined in advance.

Rolling budget is mainly used to make timely upgradation in the budgets so that accurate

results could be determined. By using it in the new business expansion plan the managers in Boat

World Plc will be able to make modifications in the records according to market situations of the

new locations. It will help to manage the cost in future in systematic manner because it makes

modifications according to the changing situations of market (Storey, 2016).

Analysis of whether traditional or alternative budgetary system is appropriate to all or any parts

of the business

Traditional and alternative budgetary systems both are used for different purposes by

business entities. In first method previous year's data is used to formulate decision for future but

in another framework different ways are used to make strategy for future perspective. From both

of them the alternative budgetary system will be the best suitable option for Boat World Plc for

its planned future form because while operating business in a new location it is very important

for a company to make sure that it is paying attention towards different elements such as market

situations. There are three main types of budgets which could be formed by the company under

this system. These are zero based, rolling and activity based (Ylhäinen, 2017). With the help of

6

management

The management in Boat World Plc is using tradition budgeting since last few years and

now it can use different alternative methods for the purpose of planning future cost management

for the company. For example, in traditional approach the company can budget the plan of

opening new out let in Netherlands and Germany with the help of previous year's data. The rates

for them could be set according to the old one's which are used for renting boats in existing

places.

In alternative methods of budgeting the management of the organisation can create a

budget with the help of zero based budget in which a new plan could be formed with a zero

balance. It will be beneficial for the company because here the strategy will be made on the basis

of new areas where business will be operated (Rogers and Makonnen, 2014).

Activity based budget could be used by Boat World Plc to allocate funds to different

activities such as marketing, selling etc. With the help of this technique organisation will be able

to perform all the operations in systematic manner because costs for all of them will be

determined in advance.

Rolling budget is mainly used to make timely upgradation in the budgets so that accurate

results could be determined. By using it in the new business expansion plan the managers in Boat

World Plc will be able to make modifications in the records according to market situations of the

new locations. It will help to manage the cost in future in systematic manner because it makes

modifications according to the changing situations of market (Storey, 2016).

Analysis of whether traditional or alternative budgetary system is appropriate to all or any parts

of the business

Traditional and alternative budgetary systems both are used for different purposes by

business entities. In first method previous year's data is used to formulate decision for future but

in another framework different ways are used to make strategy for future perspective. From both

of them the alternative budgetary system will be the best suitable option for Boat World Plc for

its planned future form because while operating business in a new location it is very important

for a company to make sure that it is paying attention towards different elements such as market

situations. There are three main types of budgets which could be formed by the company under

this system. These are zero based, rolling and activity based (Ylhäinen, 2017). With the help of

6

all of them the bugs can be ironed out before the organisation goes through more significant

changes in upcoming years because all of them do not use information of prior years.

CONCLUSION

From the above project report it has been concluded that business finance is the

combination of all the monetary resources which are used by organisations for the purpose of

carrying out operations in systematic manner. While planning to satisfy shareholders it is very

important for companies to provide them detailed information of different elements. These are

profit, cash flow, working capital, receivables, payables and stock. With the help of their analysis

steps which are required to be take for working capital management could be taken. All the

companies prepare budgets for various purposes such as reducing overspending, running

operations appropriately etc. Different methods of preparing them are rolling, zero based and

activity based. While preparing them it is very important for accounting professional to be aware

of appropriateness of tradition and alternative budgetary system.

7

changes in upcoming years because all of them do not use information of prior years.

CONCLUSION

From the above project report it has been concluded that business finance is the

combination of all the monetary resources which are used by organisations for the purpose of

carrying out operations in systematic manner. While planning to satisfy shareholders it is very

important for companies to provide them detailed information of different elements. These are

profit, cash flow, working capital, receivables, payables and stock. With the help of their analysis

steps which are required to be take for working capital management could be taken. All the

companies prepare budgets for various purposes such as reducing overspending, running

operations appropriately etc. Different methods of preparing them are rolling, zero based and

activity based. While preparing them it is very important for accounting professional to be aware

of appropriateness of tradition and alternative budgetary system.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERNCES

Books and Journals:

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Canales, R., 2016. From ideals to institutions: Institutional entrepreneurship and the growth of

Mexican small business finance. Organization Science. 27(6). pp.1548-1573.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic management journal. 35(1). pp.1-23.

Haeger, J. D., 2017. John Jacob Astor: Business and Finance in the Early Republic. Wayne State

University Press.

Jordà, Ò., Schularick, M. and Taylor, A. M., 2016. The great mortgaging: housing finance, crises

and business cycles. Economic Policy. 31(85). pp.107-152.

McLean, R. D. and Zhao, M., 2014. The business cycle, investor sentiment, and costly external

finance. The Journal of Finance. 69(3). pp.1377-1409.

Mian, A. and Sufi, A., 2018. Finance and business cycles: the credit-driven household demand

channel. Journal of Economic Perspectives. 32(3). pp.31-58.

Roberts, R., 2015. Finance for small and entrepreneurial business. Routledge.

Rogers, S. and Makonnen, R., 2014. Entrepreneurial finance: Finance and business strategies for

the serious entrepreneur.

Storey, D. J., 2016. Understanding the small business sector. Routledge.

Ylhäinen, I., 2017. Life-cycle effects in small business finance. Journal of Banking & Finance.

77. pp.176-196.

Online

Rolling budget. 2019. [Online]. Available through:

<https://yourbusiness.azcentral.com/advantages-disadvantages-rolling-budget-

1728.html>

8

Books and Journals:

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Canales, R., 2016. From ideals to institutions: Institutional entrepreneurship and the growth of

Mexican small business finance. Organization Science. 27(6). pp.1548-1573.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic management journal. 35(1). pp.1-23.

Haeger, J. D., 2017. John Jacob Astor: Business and Finance in the Early Republic. Wayne State

University Press.

Jordà, Ò., Schularick, M. and Taylor, A. M., 2016. The great mortgaging: housing finance, crises

and business cycles. Economic Policy. 31(85). pp.107-152.

McLean, R. D. and Zhao, M., 2014. The business cycle, investor sentiment, and costly external

finance. The Journal of Finance. 69(3). pp.1377-1409.

Mian, A. and Sufi, A., 2018. Finance and business cycles: the credit-driven household demand

channel. Journal of Economic Perspectives. 32(3). pp.31-58.

Roberts, R., 2015. Finance for small and entrepreneurial business. Routledge.

Rogers, S. and Makonnen, R., 2014. Entrepreneurial finance: Finance and business strategies for

the serious entrepreneur.

Storey, D. J., 2016. Understanding the small business sector. Routledge.

Ylhäinen, I., 2017. Life-cycle effects in small business finance. Journal of Banking & Finance.

77. pp.176-196.

Online

Rolling budget. 2019. [Online]. Available through:

<https://yourbusiness.azcentral.com/advantages-disadvantages-rolling-budget-

1728.html>

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.