Analysis of Business Finance: Performance and Strategies

VerifiedAdded on 2023/01/06

|13

|3654

|29

Report

AI Summary

This comprehensive report analyzes the financial performance of a business, focusing on key areas such as statement of profit or loss, statement of financial position, and ratio analysis. It delves into the understanding of financial information, contrasting accrual and cash accounting methods, and explaining the significance of profit versus cash flow. The report further examines budgeting processes and their purpose within an organization. Through detailed analysis of financial ratios like current ratio, quick ratio, gross profit margin, and debt-to-equity ratio, the report provides insights into the company's liquidity, profitability, and solvency. The report also covers efficiency ratios like asset turnover and inventory turnover, offering a holistic view of the business's financial health and operational effectiveness. The analysis includes practical examples and case studies, offering valuable insights for students and professionals in the field of finance. The report concludes with an assessment of the overall financial position of the company and proposes corrective actions.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1: BUSINESS PERFORMANCE ANALYSIS....................................................................1

1.1 Analysis of Statement of Profit or Loss...........................................................................1

1.2 Statement of Financial Position........................................................................................2

PART 2: UNDERSTANDING FINANCIAL INFORMATION & MANAGEMENT OF CASH.3

2.1 Concept of accrual accounting vs cash accounting..........................................................3

2.2 Presenting meaning and differences of profit and Cash flow...........................................5

PART 3............................................................................................................................................5

3.1 Budget and purpose of preparing a budget.......................................................................5

3.2 Benefits of forming a limited company and listing it on a stock exchange.....................6

REFERENCES................................................................................................................................8

APPENDIX....................................................................................................................................10

PART 1: BUSINESS PERFORMANCE ANALYSIS....................................................................1

1.1 Analysis of Statement of Profit or Loss...........................................................................1

1.2 Statement of Financial Position........................................................................................2

PART 2: UNDERSTANDING FINANCIAL INFORMATION & MANAGEMENT OF CASH.3

2.1 Concept of accrual accounting vs cash accounting..........................................................3

2.2 Presenting meaning and differences of profit and Cash flow...........................................5

PART 3............................................................................................................................................5

3.1 Budget and purpose of preparing a budget.......................................................................5

3.2 Benefits of forming a limited company and listing it on a stock exchange.....................6

REFERENCES................................................................................................................................8

APPENDIX....................................................................................................................................10

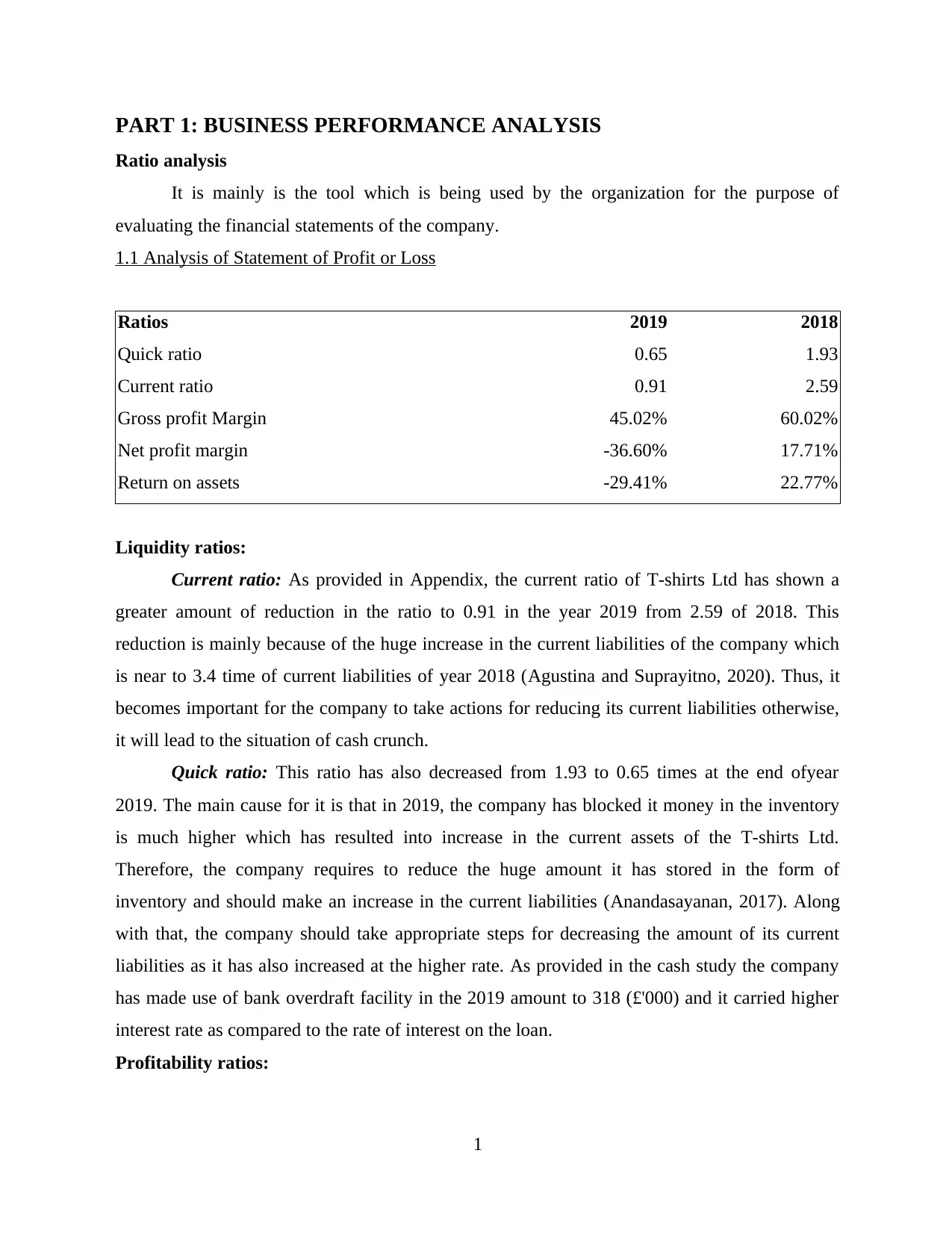

PART 1: BUSINESS PERFORMANCE ANALYSIS

Ratio analysis

It is mainly is the tool which is being used by the organization for the purpose of

evaluating the financial statements of the company.

1.1 Analysis of Statement of Profit or Loss

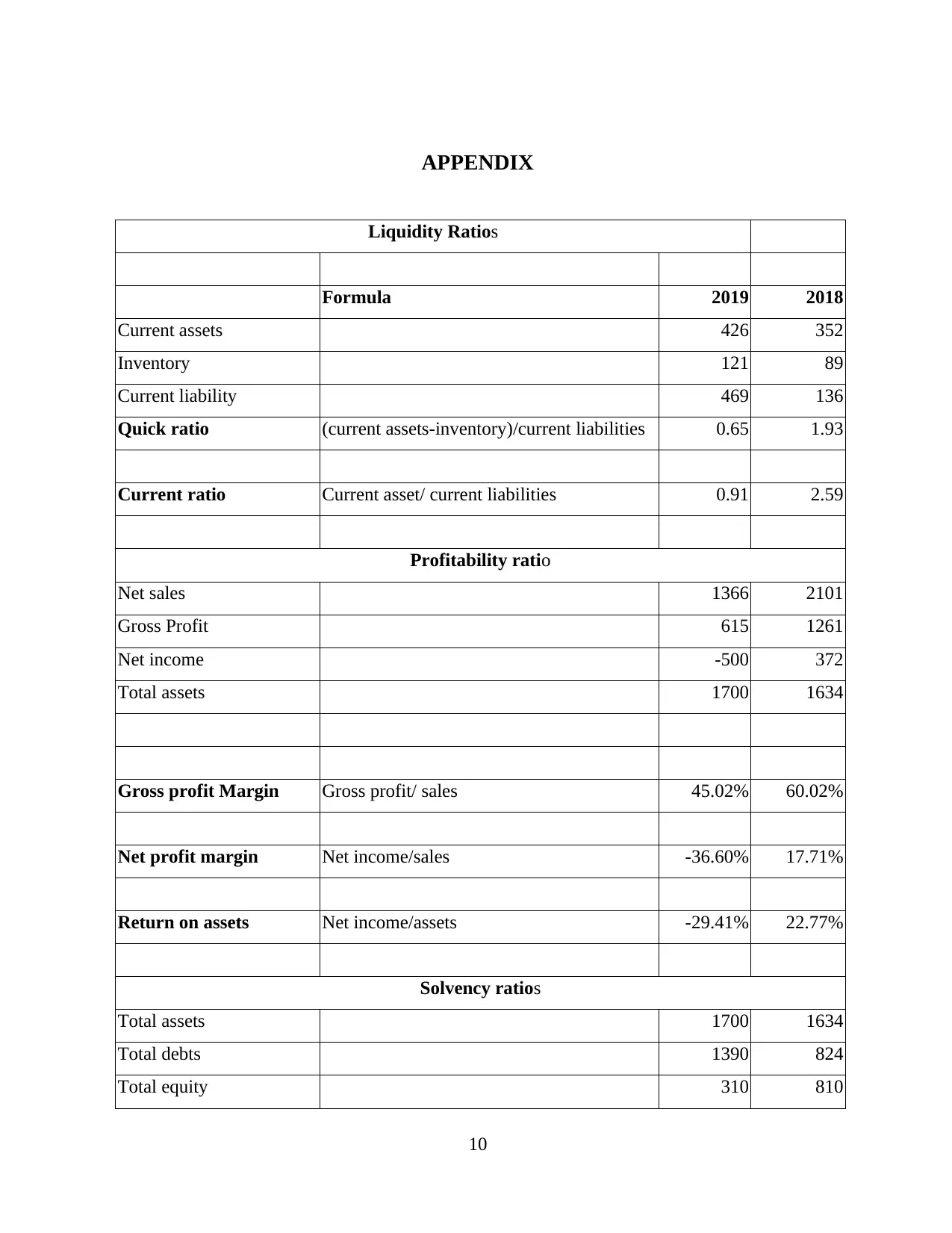

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

Gross profit Margin 45.02% 60.02%

Net profit margin -36.60% 17.71%

Return on assets -29.41% 22.77%

Liquidity ratios:

Current ratio: As provided in Appendix, the current ratio of T-shirts Ltd has shown a

greater amount of reduction in the ratio to 0.91 in the year 2019 from 2.59 of 2018. This

reduction is mainly because of the huge increase in the current liabilities of the company which

is near to 3.4 time of current liabilities of year 2018 (Agustina and Suprayitno, 2020). Thus, it

becomes important for the company to take actions for reducing its current liabilities otherwise,

it will lead to the situation of cash crunch.

Quick ratio: This ratio has also decreased from 1.93 to 0.65 times at the end ofyear

2019. The main cause for it is that in 2019, the company has blocked it money in the inventory

is much higher which has resulted into increase in the current assets of the T-shirts Ltd.

Therefore, the company requires to reduce the huge amount it has stored in the form of

inventory and should make an increase in the current liabilities (Anandasayanan, 2017). Along

with that, the company should take appropriate steps for decreasing the amount of its current

liabilities as it has also increased at the higher rate. As provided in the cash study the company

has made use of bank overdraft facility in the 2019 amount to 318 (£'000) and it carried higher

interest rate as compared to the rate of interest on the loan.

Profitability ratios:

1

Ratio analysis

It is mainly is the tool which is being used by the organization for the purpose of

evaluating the financial statements of the company.

1.1 Analysis of Statement of Profit or Loss

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

Gross profit Margin 45.02% 60.02%

Net profit margin -36.60% 17.71%

Return on assets -29.41% 22.77%

Liquidity ratios:

Current ratio: As provided in Appendix, the current ratio of T-shirts Ltd has shown a

greater amount of reduction in the ratio to 0.91 in the year 2019 from 2.59 of 2018. This

reduction is mainly because of the huge increase in the current liabilities of the company which

is near to 3.4 time of current liabilities of year 2018 (Agustina and Suprayitno, 2020). Thus, it

becomes important for the company to take actions for reducing its current liabilities otherwise,

it will lead to the situation of cash crunch.

Quick ratio: This ratio has also decreased from 1.93 to 0.65 times at the end ofyear

2019. The main cause for it is that in 2019, the company has blocked it money in the inventory

is much higher which has resulted into increase in the current assets of the T-shirts Ltd.

Therefore, the company requires to reduce the huge amount it has stored in the form of

inventory and should make an increase in the current liabilities (Anandasayanan, 2017). Along

with that, the company should take appropriate steps for decreasing the amount of its current

liabilities as it has also increased at the higher rate. As provided in the cash study the company

has made use of bank overdraft facility in the 2019 amount to 318 (£'000) and it carried higher

interest rate as compared to the rate of interest on the loan.

Profitability ratios:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross profit ratio: In this profitability ratio, the T-shirts Ltd has shown a fall in its GP

ratio which is mainly because of the bigger fall in the net sales of the company. This has resulted

into reduction in the gross profit as well as the GP ratio (Laitinen and Laitinen, 2018). Earlier, it

was 60.02% which decreased to 45.02% in 2019, thus, the company has taken step for

increasing its sales by the way of providing an increase in the credit terms to its customers. As it

has been increased to 60 days from 30 days which will help in attracting more customers

resulting into increase in sales.

Net profit margin: This ratio of T-shirts Ltd has shown a downward trend as the ratio

has decreased to -36.60% from 17.71%. The main reason behind this increase is the reduction in

revenue and the increase in the other expenses of the company (Bondoc and Dumitru, 2018).

Also, there was an increase in interest obligation as well affecting the profitability of the

company. Therefore, company requires to reduce its operating expenses and interest burden.

Return on asset ratio: It can be seen that the company is not able to effectively make use

of its assets in generating higher profits since the ratio has become negative which indicates that

the T-shirts Ltd is not effective enough in making proper and optimum utilization of its assets

(Rahman, Ibrahim and Ahmad, 2017). There has been an increase in the assets but a reduction in

the sales of the company.

1.2 Statement of Financial Position

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

Solvency ratios:

Debt to equity ratio: This is the solvency ratio for the purpose of measuring the capital

structure of the company. T-shirts Ltd in the year 2019 has shown a rise in the ratio as compared

to the previous year which is mainly because of the increase in the debt in the capital structure

(BRÎNDESCU–OLARIU, 2016). This indicates the risky situation for the company as it is

having greater proportion of debt against the equity financing. This might mean that the

investors are least interested in funding the business operation as the company is not performing

good which is why T-shirts Ltd is seeking additional debt financing.

2

ratio which is mainly because of the bigger fall in the net sales of the company. This has resulted

into reduction in the gross profit as well as the GP ratio (Laitinen and Laitinen, 2018). Earlier, it

was 60.02% which decreased to 45.02% in 2019, thus, the company has taken step for

increasing its sales by the way of providing an increase in the credit terms to its customers. As it

has been increased to 60 days from 30 days which will help in attracting more customers

resulting into increase in sales.

Net profit margin: This ratio of T-shirts Ltd has shown a downward trend as the ratio

has decreased to -36.60% from 17.71%. The main reason behind this increase is the reduction in

revenue and the increase in the other expenses of the company (Bondoc and Dumitru, 2018).

Also, there was an increase in interest obligation as well affecting the profitability of the

company. Therefore, company requires to reduce its operating expenses and interest burden.

Return on asset ratio: It can be seen that the company is not able to effectively make use

of its assets in generating higher profits since the ratio has become negative which indicates that

the T-shirts Ltd is not effective enough in making proper and optimum utilization of its assets

(Rahman, Ibrahim and Ahmad, 2017). There has been an increase in the assets but a reduction in

the sales of the company.

1.2 Statement of Financial Position

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

Solvency ratios:

Debt to equity ratio: This is the solvency ratio for the purpose of measuring the capital

structure of the company. T-shirts Ltd in the year 2019 has shown a rise in the ratio as compared

to the previous year which is mainly because of the increase in the debt in the capital structure

(BRÎNDESCU–OLARIU, 2016). This indicates the risky situation for the company as it is

having greater proportion of debt against the equity financing. This might mean that the

investors are least interested in funding the business operation as the company is not performing

good which is why T-shirts Ltd is seeking additional debt financing.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Proprietary ratio: This ratio of the company highlights that in the year 2018 the

company has nearly 49.57% of the funds being contributed by the shareholders and the

remaining amount has been funded through creditors (Fatihudin and Mochklas, 2018). On the

other hand, in 2019 it reduced to 18.24% which shows that the company has made use of the

debt in its financing other than the expensive equity. The company requires to maintain a

balance between the high and low ratio.

Efficiency ratios

Asset turnover ratio: This ratio of the company is very low which indicates that the

company is not having ability to effectively make use of its assets in order to generate revenue

for the company. This highlights that the company is not working productively in utilizing its

assets to its full capacity (Patin, Rahman and Mustafa, 2020). The ratio was 1.29 in 2018 which

further reduced to 0.82 in 2019. It is favourable to have higher ratio and as the company is

having lower ratio which indicates that the company is not utilizing its assets efficiently which

might be because of the problem pertaining to the management or the production.

Inventory turnover ratio: In the year 2018, the company was having the inventory

turnover ratio of 9.44 times which depicts the efficiency of the company in selling out its

inventory which is not so high but manageable. In contrast to it, in 2019, the ratio reduced to

1.93 times which states that the company is going through time as the company is overspending

the amount in buying large amount of inventory and wasting the resources by making the

storage for the non-saleable inventory (Kwak, 2019). Therefore, the company requires to review

its inventory management system and implement policies for effectively managing its inventory

leading improving its liquidity position as well.

Therefore, based on the financial statement analysis of the T-shirts Ltd it can be stated

that the current position and performance of the company is very poor and the company requires

undertaking corrective actions on an immediate basis in order to take control of the current

situation of the company and work on improving it. In case, if the instant decision are not made

there are chances that the company might go bankrupt. Thus, the over financial situation of the

company is not good.

3

company has nearly 49.57% of the funds being contributed by the shareholders and the

remaining amount has been funded through creditors (Fatihudin and Mochklas, 2018). On the

other hand, in 2019 it reduced to 18.24% which shows that the company has made use of the

debt in its financing other than the expensive equity. The company requires to maintain a

balance between the high and low ratio.

Efficiency ratios

Asset turnover ratio: This ratio of the company is very low which indicates that the

company is not having ability to effectively make use of its assets in order to generate revenue

for the company. This highlights that the company is not working productively in utilizing its

assets to its full capacity (Patin, Rahman and Mustafa, 2020). The ratio was 1.29 in 2018 which

further reduced to 0.82 in 2019. It is favourable to have higher ratio and as the company is

having lower ratio which indicates that the company is not utilizing its assets efficiently which

might be because of the problem pertaining to the management or the production.

Inventory turnover ratio: In the year 2018, the company was having the inventory

turnover ratio of 9.44 times which depicts the efficiency of the company in selling out its

inventory which is not so high but manageable. In contrast to it, in 2019, the ratio reduced to

1.93 times which states that the company is going through time as the company is overspending

the amount in buying large amount of inventory and wasting the resources by making the

storage for the non-saleable inventory (Kwak, 2019). Therefore, the company requires to review

its inventory management system and implement policies for effectively managing its inventory

leading improving its liquidity position as well.

Therefore, based on the financial statement analysis of the T-shirts Ltd it can be stated

that the current position and performance of the company is very poor and the company requires

undertaking corrective actions on an immediate basis in order to take control of the current

situation of the company and work on improving it. In case, if the instant decision are not made

there are chances that the company might go bankrupt. Thus, the over financial situation of the

company is not good.

3

PART 2: UNDERSTANDING FINANCIAL INFORMATION &

MANAGEMENT OF CASH

2.1 Concept of accrual accounting vs cash accounting

Accrual Accounting: This helps to measure the performance as well as position of

company. Also, when transaction is recorded within books of accounts, if payment are not

received then it is known as accrual accounting (Goel, 2016). Further, it is also based upon

revenue recognition principle and matching principle, the nature of this accounting is complex

while preferred to large business.

Benefits:

Accrual Accounting is considered as one of the most useful business analysis

It also assists to creates budget for the expenses and further predict sales as well.

This method allows for financial statement that unaffected by cash timing within

business negotiation.

Limitations:

If company uses this method then it is complicated to follow the rules of revenue and

expenses.

Business may have misused this method to hide weakness and mistakes within financial

reports (Difference between cash and accrual cash accounting, 2020).

Example: As per the case study, T shirts Ltd increase the credit terms from 30 to 60 days and

once the transaction takes place, company recorded under accrual, even though there is no cash

received by customer side.

Cash Accounting (CA): It is that accounting method in which all payment receipt is

recorded during each period whenever they received (NGUYEN and NGUYEN, 2020). On the

other side, it can be said that cash accounting is used when both revenue and expenses are

recorded, whenever cash is received or paid. The nature of this method is easy and mostly used

by small businesses.

Benefits:

This method is simple to use because it do not require any experts knowledge and

consumes less time as compared to other.

Cheaper as compared to accrual accounting method and does not conform to GAAP

provision.

4

MANAGEMENT OF CASH

2.1 Concept of accrual accounting vs cash accounting

Accrual Accounting: This helps to measure the performance as well as position of

company. Also, when transaction is recorded within books of accounts, if payment are not

received then it is known as accrual accounting (Goel, 2016). Further, it is also based upon

revenue recognition principle and matching principle, the nature of this accounting is complex

while preferred to large business.

Benefits:

Accrual Accounting is considered as one of the most useful business analysis

It also assists to creates budget for the expenses and further predict sales as well.

This method allows for financial statement that unaffected by cash timing within

business negotiation.

Limitations:

If company uses this method then it is complicated to follow the rules of revenue and

expenses.

Business may have misused this method to hide weakness and mistakes within financial

reports (Difference between cash and accrual cash accounting, 2020).

Example: As per the case study, T shirts Ltd increase the credit terms from 30 to 60 days and

once the transaction takes place, company recorded under accrual, even though there is no cash

received by customer side.

Cash Accounting (CA): It is that accounting method in which all payment receipt is

recorded during each period whenever they received (NGUYEN and NGUYEN, 2020). On the

other side, it can be said that cash accounting is used when both revenue and expenses are

recorded, whenever cash is received or paid. The nature of this method is easy and mostly used

by small businesses.

Benefits:

This method is simple to use because it do not require any experts knowledge and

consumes less time as compared to other.

Cheaper as compared to accrual accounting method and does not conform to GAAP

provision.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Limitations:

CA helps to analyze financial health of company but do not provide clear picture.

If a firm approve Audited Financial Statements, then accounts prepared under cash basis

are not consider.

Example: In accordance with the case study, even though the transaction has been proceeding

but within the credit limits, when customer paid the amount of purchased product. At that time,

cash based accounting is performed in which transaction are recorded once the amount is

received by company.

2.2 Presenting meaning and differences of profit and Cash flow

Profit: It is also known as net income which is collected after subtracting all the revenue

from expenses. Also, a business cannot survive unless it is profitable and it assists in analyzing

the financial health of a firm. In profit and loss account, company consider net profit which

reflect the business's profitability.

Cash flow: It means the net balance of cash that moves into and out of business within a

specific tenure. It can be positive or negative, but does not include credit from suppliers, money

owned from debtors. It is also used to track the cash flow which in turn helps in assessing

deficiencies that takes place in operations (Eulner and Waldbauer, 2018).

Difference between profit and cash flow

Cash flow is the money that flows in and out within a business throughout a define time

period, while profit remains from a revenue after deduction of a cost. Moreover, profit helps to

analyze immediate success of a business while cash flow provides long term financial prospect

of a business. Also, both profit and cash flow are considered as two important aspects. Such that

for short term, cash flow is used while in long term, profit is considered (Cash flow vs profit,

2020). Moreover, a company have a positive cash flow while having no profit, but this type of

transaction is not considered as an income.

Thus, it is stated that both method have their own unique ways of assessing the

performance which in turn helps to present the financial picture of a business. For example, T

shirt Ltd sell the product £10 and making profit of £1 after all-expenses paid. Then could be

consider raising its price to £12 by lowering its production cost. Thus, if business review its

profit vs cash flow, then low cash flow can restrict a profitable business limiting further growth

5

CA helps to analyze financial health of company but do not provide clear picture.

If a firm approve Audited Financial Statements, then accounts prepared under cash basis

are not consider.

Example: In accordance with the case study, even though the transaction has been proceeding

but within the credit limits, when customer paid the amount of purchased product. At that time,

cash based accounting is performed in which transaction are recorded once the amount is

received by company.

2.2 Presenting meaning and differences of profit and Cash flow

Profit: It is also known as net income which is collected after subtracting all the revenue

from expenses. Also, a business cannot survive unless it is profitable and it assists in analyzing

the financial health of a firm. In profit and loss account, company consider net profit which

reflect the business's profitability.

Cash flow: It means the net balance of cash that moves into and out of business within a

specific tenure. It can be positive or negative, but does not include credit from suppliers, money

owned from debtors. It is also used to track the cash flow which in turn helps in assessing

deficiencies that takes place in operations (Eulner and Waldbauer, 2018).

Difference between profit and cash flow

Cash flow is the money that flows in and out within a business throughout a define time

period, while profit remains from a revenue after deduction of a cost. Moreover, profit helps to

analyze immediate success of a business while cash flow provides long term financial prospect

of a business. Also, both profit and cash flow are considered as two important aspects. Such that

for short term, cash flow is used while in long term, profit is considered (Cash flow vs profit,

2020). Moreover, a company have a positive cash flow while having no profit, but this type of

transaction is not considered as an income.

Thus, it is stated that both method have their own unique ways of assessing the

performance which in turn helps to present the financial picture of a business. For example, T

shirt Ltd sell the product £10 and making profit of £1 after all-expenses paid. Then could be

consider raising its price to £12 by lowering its production cost. Thus, if business review its

profit vs cash flow, then low cash flow can restrict a profitable business limiting further growth

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

options. It is so because it may not be able to pay bills or take advantage of further opportunities

that come its way.

PART 3

3.1 Budget and purpose of preparing a budget

Budget is mainly referred to as a plan which is expressed in a quantitative terms for a

specific period of time which is mainly one year. It describes all the activities which the

company is required to undertake in that period in order to attain its desired goals and profits. In

simple words, budgeting is the process of designing, implementing and operating budgets

(Laitinen, Länsiluoto and Salonen, 2016). Thus, it is an estimation of revenue and expenses for a

specific time period. Budgeting is very useful in taking meaningful decisions and its purpose is

immense. The main purpose of budget is detailed out below.

Forecast of incomes and expenses: The main purpose of budgeting is to provide a

model in respect to how the business might perform or undertake the business operation in the

situation where certain strategies are carried out. Therefore, before starting a new project a

complete budget is created in involves the forecasted income and expenditure and the profit

associated with it.

Tool for decision-making: Budgeting provides financial framework within which the

business organization is required to make decisions like the proposed action is planned or not.

For the business to carried out in a responsible way, the expenditure is needed to be controlled.

For example, budget for advertising is completely exhausted and now the decision for making

additional expenditure on the same will be most likely “no”.

Monitoring and measuring business performance: Budgeting helps the business

organization in effectively measuring and monitoring the performance of the business in against

the forecasted outcomes of the business performance which helps in determining whether the

business is moving as per the expectation or not (Bužinskienė, 2019). Based on this, corrective

actions can be taken in respect to the variance incurred between the actual or the budgeted one.

Providing benchmark: Budgeting provides a benchmark based on which the current

activities of the organization can be easily managed and controlled with the help of the set

benchmark. Thus resulting into undertaking right decision in order to achieve the desired

objectives.

6

that come its way.

PART 3

3.1 Budget and purpose of preparing a budget

Budget is mainly referred to as a plan which is expressed in a quantitative terms for a

specific period of time which is mainly one year. It describes all the activities which the

company is required to undertake in that period in order to attain its desired goals and profits. In

simple words, budgeting is the process of designing, implementing and operating budgets

(Laitinen, Länsiluoto and Salonen, 2016). Thus, it is an estimation of revenue and expenses for a

specific time period. Budgeting is very useful in taking meaningful decisions and its purpose is

immense. The main purpose of budget is detailed out below.

Forecast of incomes and expenses: The main purpose of budgeting is to provide a

model in respect to how the business might perform or undertake the business operation in the

situation where certain strategies are carried out. Therefore, before starting a new project a

complete budget is created in involves the forecasted income and expenditure and the profit

associated with it.

Tool for decision-making: Budgeting provides financial framework within which the

business organization is required to make decisions like the proposed action is planned or not.

For the business to carried out in a responsible way, the expenditure is needed to be controlled.

For example, budget for advertising is completely exhausted and now the decision for making

additional expenditure on the same will be most likely “no”.

Monitoring and measuring business performance: Budgeting helps the business

organization in effectively measuring and monitoring the performance of the business in against

the forecasted outcomes of the business performance which helps in determining whether the

business is moving as per the expectation or not (Bužinskienė, 2019). Based on this, corrective

actions can be taken in respect to the variance incurred between the actual or the budgeted one.

Providing benchmark: Budgeting provides a benchmark based on which the current

activities of the organization can be easily managed and controlled with the help of the set

benchmark. Thus resulting into undertaking right decision in order to achieve the desired

objectives.

6

3.2 Benefits of forming a limited company and listing it on a stock exchange

Forming a limited company increases the ways of acquiring funds and contributing

towards the growth and development of the organization. Listing a company on a stock

exchange enables it to raise capital from the public which will help in further strengthening of

the organizational structure and reputation (Benefits of Listing / Going Public. 2020). Listing

helps in offering liquidity to the investors and in ensuring effective compliance with the issuer

and working in the interest of the investors. There are various benefits associated with the listing

a company on a stock exchange which are stated below.

Gathering capital for further growth: Companies reaches a level in which the additional

capital is required to be injected which helps in company's growth and business expansion plans.

Thus, going public is a way through which these constraints can be easily mitigated. In this, the

company increases the shareholders base and enhances the credibility.

Enhanced Visibility: This will help in improving the company's visibility and credibility

all across the other institutions and the public who are willing to invest which is because of

complying with the different regulatory requirement and ensuring transparency while

undertaking the business operations.

Liquidity: Going public stimulates liquidity providing the shareholders the opportunity

for realizing the value they have invested in the company (James, 2018). It provides opportunity

to the investors to transact in the stocks of the organization and sharing risks and along with the

same benefiting the investors with the increase in the organizational value.

Increase in employee morale: Listing of the company increases the visibility and

enhances the perception of the public towards the business organization, thereby, resulting into

increase in the employee value and boosting of their morale. There are chances of recruiting new

staff and providing them the stock based payments like ESOPs etc.

Transparency and efficiency: Going public brings the efficiency on the business

operation of the organization. The board members and the management team of the listed entity

are accountable to the shareholders. Along with that, the entity is required to comply with the all

the regulation on timely basis by providing and disclosing all the relevant information to the

exchange and the shareholders in accordance with the terms listed in the listed agreement.

7

Forming a limited company increases the ways of acquiring funds and contributing

towards the growth and development of the organization. Listing a company on a stock

exchange enables it to raise capital from the public which will help in further strengthening of

the organizational structure and reputation (Benefits of Listing / Going Public. 2020). Listing

helps in offering liquidity to the investors and in ensuring effective compliance with the issuer

and working in the interest of the investors. There are various benefits associated with the listing

a company on a stock exchange which are stated below.

Gathering capital for further growth: Companies reaches a level in which the additional

capital is required to be injected which helps in company's growth and business expansion plans.

Thus, going public is a way through which these constraints can be easily mitigated. In this, the

company increases the shareholders base and enhances the credibility.

Enhanced Visibility: This will help in improving the company's visibility and credibility

all across the other institutions and the public who are willing to invest which is because of

complying with the different regulatory requirement and ensuring transparency while

undertaking the business operations.

Liquidity: Going public stimulates liquidity providing the shareholders the opportunity

for realizing the value they have invested in the company (James, 2018). It provides opportunity

to the investors to transact in the stocks of the organization and sharing risks and along with the

same benefiting the investors with the increase in the organizational value.

Increase in employee morale: Listing of the company increases the visibility and

enhances the perception of the public towards the business organization, thereby, resulting into

increase in the employee value and boosting of their morale. There are chances of recruiting new

staff and providing them the stock based payments like ESOPs etc.

Transparency and efficiency: Going public brings the efficiency on the business

operation of the organization. The board members and the management team of the listed entity

are accountable to the shareholders. Along with that, the entity is required to comply with the all

the regulation on timely basis by providing and disclosing all the relevant information to the

exchange and the shareholders in accordance with the terms listed in the listed agreement.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Agustina, Y. N. and Suprayitno, H., 2020. ANALYSIS OF FINANCIAL STATEMENTS

USING LIQUIDITY RATIO TO MEASURE FINANCIAL PERFORMANCE IN

2017-2019. JOSAR (Journal of Students Academic Research). 5(2). pp.32-39.

Anandasayanan, S., 2017. The effects of liquidity management on firm profitability: Evidence

from Sri Lankan listed companies. TRANS Asian Journal of Marketing & Management

Research (TAJMMR). 6(2and3). pp.32-41.

Bondoc, M. D. and Dumitru, M. I., 2018. Comparative Study Of Financial Profitability Of

Romanian Tourism Companies. Scientific Bulletin-Economic Sciences. 17(3). pp.169-

176.

BRÎNDESCU–OLARIU, D., 2016. Solvency ratio as a tool for bankruptcy prediction. Ecoforum

Journal. 5(2).

Bužinskienė, R., 2019. MASTER BUDGET FORMATION IN PRIVATE

COMPANIES. Professional Studies: Theory & Practice/Profesines Studijos: Teorija ir

Praktika. (21).

Eulner, V. and Waldbauer, G., 2018. New development: Cash versus accrual accounting for the

public sector—EPSAS. Public Money & Management, pp.1-4.

Fatihudin, D. and Mochklas, M., 2018. How Measuring Financial Performance. International

Journal of Civil Engineering and Technology (IJCIET). 6(9). pp.553-557.

Goel, D., 2016. The earnings management motivation: Accrual accounting vs. cash

accounting. Australasian Accounting, Business and Finance Journal.10(3). pp.48-66.

Kwak, J. K., 2019. Analysis of Inventory Turnover as a Performance Measure in Manufacturing

Industry. Processes. 7(10). p.760.

Laitinen, E. K. and Laitinen, T., 2018. Financial reporting: profitability ratios in the different

stages of life cycle. Archives of Business Research, 6(11).

Laitinen, E. K., Länsiluoto, A. and Salonen, S., 2016. Interactive budgeting, product innovation,

and firm performance: empirical evidence from Finnish firms. Journal of Management

Control. 27(4). pp.293-322.

NGUYEN, D.D. and NGUYEN, A.H., 2020. The impact of cash flow statement on lending

decision of commercial banks: evidence from Vietnam. The Journal of Asian Finance,

Economics, and Business.7(6). pp.85-93.

Patin, J. C., Rahman, M. and Mustafa, M., 2020. Impact of Total Asset Turnover Ratios on

Equity Returns: Dynamic Panel Data Analyses. Journal of Accounting, Business and

Management (JABM). 27(1). pp.19-29.

Rahman, M. H. U., Ibrahim, M. Y. and Ahmad, A. C., 2017. Accounting Profitability and Firm

Market Valuation: A Panel Data Analysis. Global Business and Management

Research: An International Journal. 9. pp.679-689.

Online

Difference between cash and accrual cash accounting. 2020. [Online]. Available through:

<https://smartbooks.com/resources/articles/cash-vs-accrual-accounting-pros-cons/>

Cash flow vs profit. 2020. [Online]. Available through: <https://online.hbs.edu/blog/post/cash-

flow-vs-profit>.

8

Books and Journals

Agustina, Y. N. and Suprayitno, H., 2020. ANALYSIS OF FINANCIAL STATEMENTS

USING LIQUIDITY RATIO TO MEASURE FINANCIAL PERFORMANCE IN

2017-2019. JOSAR (Journal of Students Academic Research). 5(2). pp.32-39.

Anandasayanan, S., 2017. The effects of liquidity management on firm profitability: Evidence

from Sri Lankan listed companies. TRANS Asian Journal of Marketing & Management

Research (TAJMMR). 6(2and3). pp.32-41.

Bondoc, M. D. and Dumitru, M. I., 2018. Comparative Study Of Financial Profitability Of

Romanian Tourism Companies. Scientific Bulletin-Economic Sciences. 17(3). pp.169-

176.

BRÎNDESCU–OLARIU, D., 2016. Solvency ratio as a tool for bankruptcy prediction. Ecoforum

Journal. 5(2).

Bužinskienė, R., 2019. MASTER BUDGET FORMATION IN PRIVATE

COMPANIES. Professional Studies: Theory & Practice/Profesines Studijos: Teorija ir

Praktika. (21).

Eulner, V. and Waldbauer, G., 2018. New development: Cash versus accrual accounting for the

public sector—EPSAS. Public Money & Management, pp.1-4.

Fatihudin, D. and Mochklas, M., 2018. How Measuring Financial Performance. International

Journal of Civil Engineering and Technology (IJCIET). 6(9). pp.553-557.

Goel, D., 2016. The earnings management motivation: Accrual accounting vs. cash

accounting. Australasian Accounting, Business and Finance Journal.10(3). pp.48-66.

Kwak, J. K., 2019. Analysis of Inventory Turnover as a Performance Measure in Manufacturing

Industry. Processes. 7(10). p.760.

Laitinen, E. K. and Laitinen, T., 2018. Financial reporting: profitability ratios in the different

stages of life cycle. Archives of Business Research, 6(11).

Laitinen, E. K., Länsiluoto, A. and Salonen, S., 2016. Interactive budgeting, product innovation,

and firm performance: empirical evidence from Finnish firms. Journal of Management

Control. 27(4). pp.293-322.

NGUYEN, D.D. and NGUYEN, A.H., 2020. The impact of cash flow statement on lending

decision of commercial banks: evidence from Vietnam. The Journal of Asian Finance,

Economics, and Business.7(6). pp.85-93.

Patin, J. C., Rahman, M. and Mustafa, M., 2020. Impact of Total Asset Turnover Ratios on

Equity Returns: Dynamic Panel Data Analyses. Journal of Accounting, Business and

Management (JABM). 27(1). pp.19-29.

Rahman, M. H. U., Ibrahim, M. Y. and Ahmad, A. C., 2017. Accounting Profitability and Firm

Market Valuation: A Panel Data Analysis. Global Business and Management

Research: An International Journal. 9. pp.679-689.

Online

Difference between cash and accrual cash accounting. 2020. [Online]. Available through:

<https://smartbooks.com/resources/articles/cash-vs-accrual-accounting-pros-cons/>

Cash flow vs profit. 2020. [Online]. Available through: <https://online.hbs.edu/blog/post/cash-

flow-vs-profit>.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Benefits of Listing / Going Public. 2020. [Online]. Available

Through:<https://www.msei.in/Corporates/benefits-of-listing>.

James, H., 2018. BENEFITS OF STOCK EXCHANGE FOR THE COMPANY. [Online].

Available Through:<https://www.omniamerican.com/benefits-of-stock-exchange-for-

the-company/>.

9

Through:<https://www.msei.in/Corporates/benefits-of-listing>.

James, H., 2018. BENEFITS OF STOCK EXCHANGE FOR THE COMPANY. [Online].

Available Through:<https://www.omniamerican.com/benefits-of-stock-exchange-for-

the-company/>.

9

APPENDIX

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Return on assets Net income/assets -29.41% 22.77%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

10

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Return on assets Net income/assets -29.41% 22.77%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.