Business Finance Report: Financial Performance and Analysis 2020/21

VerifiedAdded on 2023/01/04

|10

|3192

|75

Report

AI Summary

This report provides a comprehensive analysis of business finance, focusing on the financial performance of a company and its competitor. It begins with an introduction to business finance and then delves into the analysis of the statement of profit and loss and the statement of financial position. The report then explains the concepts of accrual and cash accounting, outlining their benefits and limitations, and clarifies the differences between profit and cash flow. Furthermore, the report defines budgeting and explains its purpose, and it also discusses the benefits of forming a limited company and listing it on a stock exchange. The analysis includes the calculation of financial ratios such as gross profit margin, net profit margin, interest cover ratio, current ratio, quick ratio, and debt-equity ratio. The report concludes by summarizing the key findings and insights gained from the financial analysis.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1.1 Statement of profit and loss...................................................................................................1

1.2 Statement of financial position..............................................................................................2

PART 2............................................................................................................................................4

2.1 Explanation of concept of accrual accounting vs cash accounting that includes the benefits

and limitations of each.................................................................................................................4

2.2 What are profit and cash flow and difference between all of them.......................................5

PART 3............................................................................................................................................6

3.1 Definition of budget and explanation or purpose of preparing a budget...............................6

3.2 Benefits of forming a limited company and listing it on a stock exchange...........................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1.1 Statement of profit and loss...................................................................................................1

1.2 Statement of financial position..............................................................................................2

PART 2............................................................................................................................................4

2.1 Explanation of concept of accrual accounting vs cash accounting that includes the benefits

and limitations of each.................................................................................................................4

2.2 What are profit and cash flow and difference between all of them.......................................5

PART 3............................................................................................................................................6

3.1 Definition of budget and explanation or purpose of preparing a budget...............................6

3.2 Benefits of forming a limited company and listing it on a stock exchange...........................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Business finance is the funding which is required by an organisation for the purpose of

carrying out all the operational activities in systematic manner. If an entity will not be able to

manage the funding systematically then it may leave negative impacts upon functionality of

business. Proper arrangement and management of funding is very important as it can help to

carry out all the operational activities in systematic manner (Bezemer and Hudson, 2016).

Present report is based upon analysis of financial performance of Vests Plc and the finance

trainee of the company is asked to analyse the financial position of competitor which is T-Shirt

Plc. This assignment covers various topics such as assessment of business performance,

understanding of financial information and management of cash. Apart from this, discussion of

budget techniques and company finance are also covered in this project.

PART 1

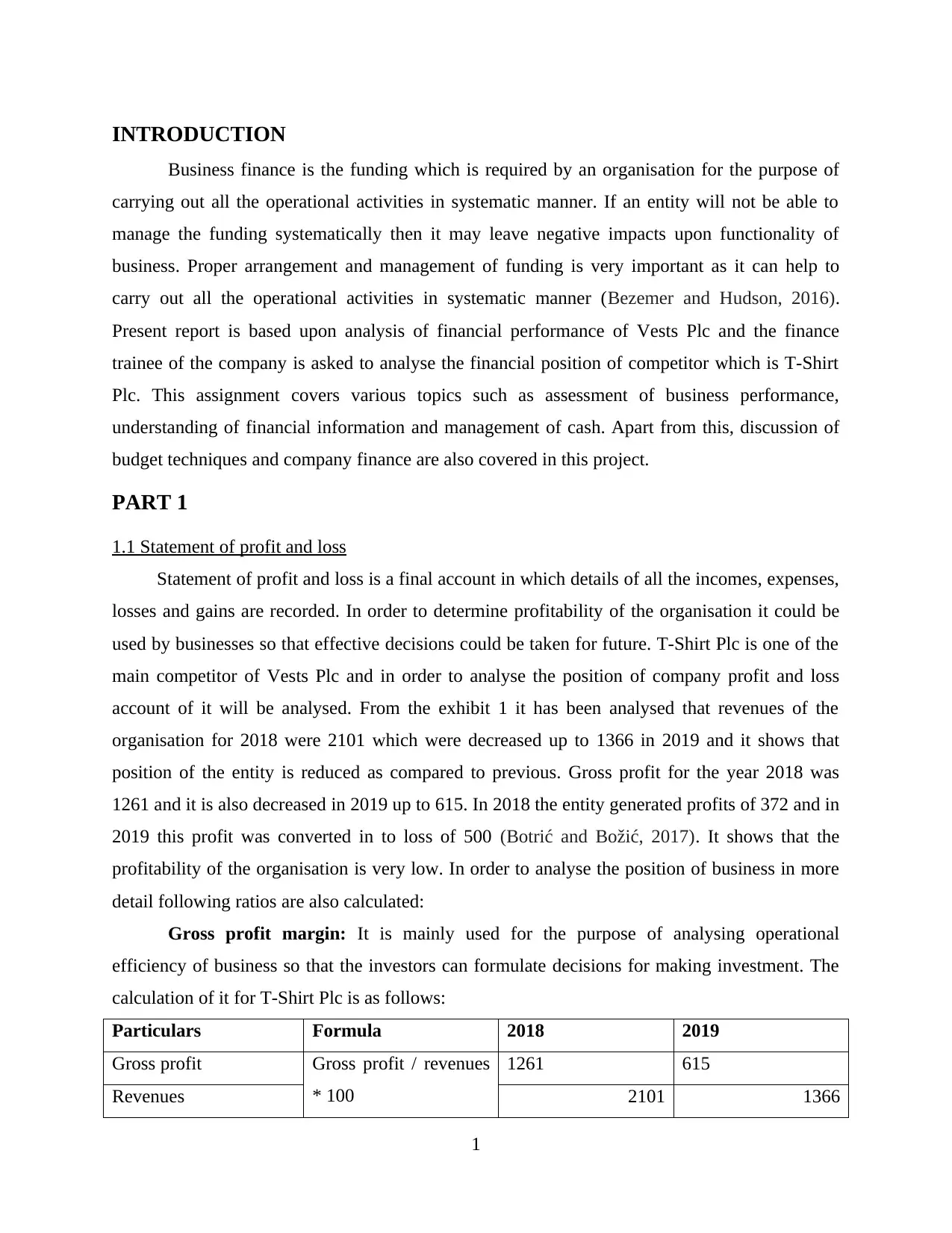

1.1 Statement of profit and loss

Statement of profit and loss is a final account in which details of all the incomes, expenses,

losses and gains are recorded. In order to determine profitability of the organisation it could be

used by businesses so that effective decisions could be taken for future. T-Shirt Plc is one of the

main competitor of Vests Plc and in order to analyse the position of company profit and loss

account of it will be analysed. From the exhibit 1 it has been analysed that revenues of the

organisation for 2018 were 2101 which were decreased up to 1366 in 2019 and it shows that

position of the entity is reduced as compared to previous. Gross profit for the year 2018 was

1261 and it is also decreased in 2019 up to 615. In 2018 the entity generated profits of 372 and in

2019 this profit was converted in to loss of 500 (Botrić and Božić, 2017). It shows that the

profitability of the organisation is very low. In order to analyse the position of business in more

detail following ratios are also calculated:

Gross profit margin: It is mainly used for the purpose of analysing operational

efficiency of business so that the investors can formulate decisions for making investment. The

calculation of it for T-Shirt Plc is as follows:

Particulars Formula 2018 2019

Gross profit Gross profit / revenues

* 100

1261 615

Revenues 2101 1366

1

Business finance is the funding which is required by an organisation for the purpose of

carrying out all the operational activities in systematic manner. If an entity will not be able to

manage the funding systematically then it may leave negative impacts upon functionality of

business. Proper arrangement and management of funding is very important as it can help to

carry out all the operational activities in systematic manner (Bezemer and Hudson, 2016).

Present report is based upon analysis of financial performance of Vests Plc and the finance

trainee of the company is asked to analyse the financial position of competitor which is T-Shirt

Plc. This assignment covers various topics such as assessment of business performance,

understanding of financial information and management of cash. Apart from this, discussion of

budget techniques and company finance are also covered in this project.

PART 1

1.1 Statement of profit and loss

Statement of profit and loss is a final account in which details of all the incomes, expenses,

losses and gains are recorded. In order to determine profitability of the organisation it could be

used by businesses so that effective decisions could be taken for future. T-Shirt Plc is one of the

main competitor of Vests Plc and in order to analyse the position of company profit and loss

account of it will be analysed. From the exhibit 1 it has been analysed that revenues of the

organisation for 2018 were 2101 which were decreased up to 1366 in 2019 and it shows that

position of the entity is reduced as compared to previous. Gross profit for the year 2018 was

1261 and it is also decreased in 2019 up to 615. In 2018 the entity generated profits of 372 and in

2019 this profit was converted in to loss of 500 (Botrić and Božić, 2017). It shows that the

profitability of the organisation is very low. In order to analyse the position of business in more

detail following ratios are also calculated:

Gross profit margin: It is mainly used for the purpose of analysing operational

efficiency of business so that the investors can formulate decisions for making investment. The

calculation of it for T-Shirt Plc is as follows:

Particulars Formula 2018 2019

Gross profit Gross profit / revenues

* 100

1261 615

Revenues 2101 1366

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

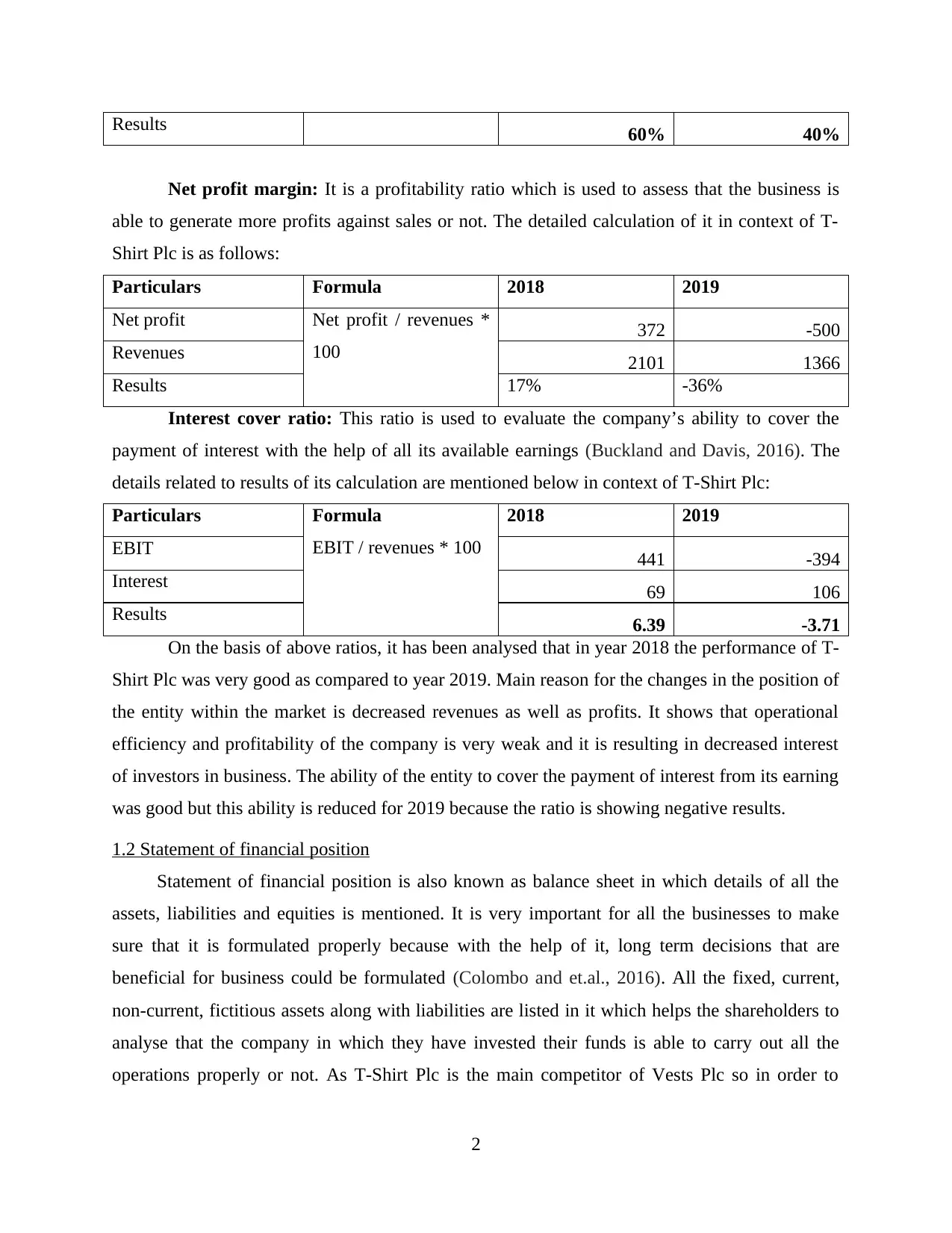

Results 60% 40%

Net profit margin: It is a profitability ratio which is used to assess that the business is

able to generate more profits against sales or not. The detailed calculation of it in context of T-

Shirt Plc is as follows:

Particulars Formula 2018 2019

Net profit Net profit / revenues *

100

372 -500

Revenues 2101 1366

Results 17% -36%

Interest cover ratio: This ratio is used to evaluate the company’s ability to cover the

payment of interest with the help of all its available earnings (Buckland and Davis, 2016). The

details related to results of its calculation are mentioned below in context of T-Shirt Plc:

Particulars Formula

EBIT / revenues * 100

2018 2019

EBIT 441 -394

Interest 69 106

Results 6.39 -3.71

On the basis of above ratios, it has been analysed that in year 2018 the performance of T-

Shirt Plc was very good as compared to year 2019. Main reason for the changes in the position of

the entity within the market is decreased revenues as well as profits. It shows that operational

efficiency and profitability of the company is very weak and it is resulting in decreased interest

of investors in business. The ability of the entity to cover the payment of interest from its earning

was good but this ability is reduced for 2019 because the ratio is showing negative results.

1.2 Statement of financial position

Statement of financial position is also known as balance sheet in which details of all the

assets, liabilities and equities is mentioned. It is very important for all the businesses to make

sure that it is formulated properly because with the help of it, long term decisions that are

beneficial for business could be formulated (Colombo and et.al., 2016). All the fixed, current,

non-current, fictitious assets along with liabilities are listed in it which helps the shareholders to

analyse that the company in which they have invested their funds is able to carry out all the

operations properly or not. As T-Shirt Plc is the main competitor of Vests Plc so in order to

2

Net profit margin: It is a profitability ratio which is used to assess that the business is

able to generate more profits against sales or not. The detailed calculation of it in context of T-

Shirt Plc is as follows:

Particulars Formula 2018 2019

Net profit Net profit / revenues *

100

372 -500

Revenues 2101 1366

Results 17% -36%

Interest cover ratio: This ratio is used to evaluate the company’s ability to cover the

payment of interest with the help of all its available earnings (Buckland and Davis, 2016). The

details related to results of its calculation are mentioned below in context of T-Shirt Plc:

Particulars Formula

EBIT / revenues * 100

2018 2019

EBIT 441 -394

Interest 69 106

Results 6.39 -3.71

On the basis of above ratios, it has been analysed that in year 2018 the performance of T-

Shirt Plc was very good as compared to year 2019. Main reason for the changes in the position of

the entity within the market is decreased revenues as well as profits. It shows that operational

efficiency and profitability of the company is very weak and it is resulting in decreased interest

of investors in business. The ability of the entity to cover the payment of interest from its earning

was good but this ability is reduced for 2019 because the ratio is showing negative results.

1.2 Statement of financial position

Statement of financial position is also known as balance sheet in which details of all the

assets, liabilities and equities is mentioned. It is very important for all the businesses to make

sure that it is formulated properly because with the help of it, long term decisions that are

beneficial for business could be formulated (Colombo and et.al., 2016). All the fixed, current,

non-current, fictitious assets along with liabilities are listed in it which helps the shareholders to

analyse that the company in which they have invested their funds is able to carry out all the

operations properly or not. As T-Shirt Plc is the main competitor of Vests Plc so in order to

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

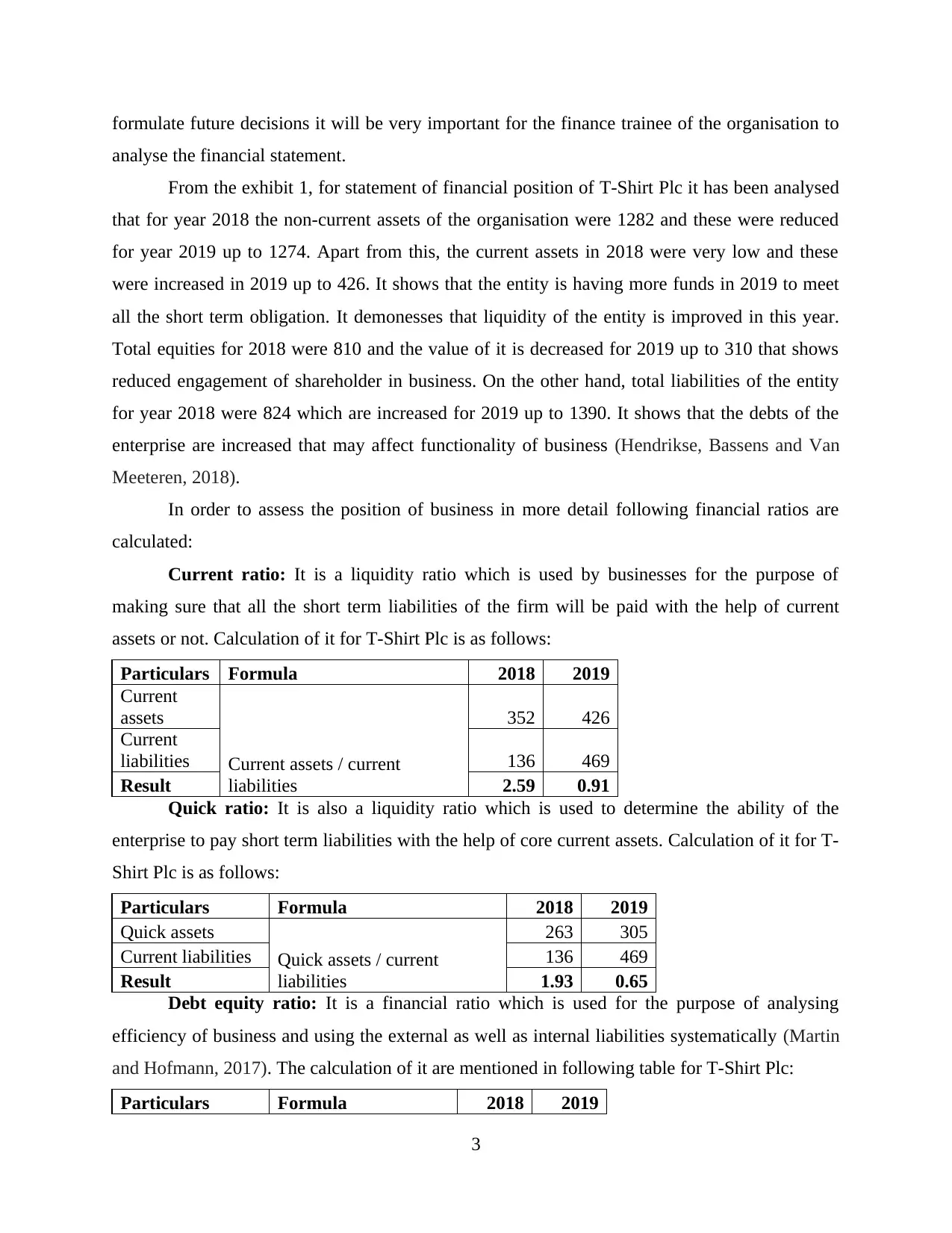

formulate future decisions it will be very important for the finance trainee of the organisation to

analyse the financial statement.

From the exhibit 1, for statement of financial position of T-Shirt Plc it has been analysed

that for year 2018 the non-current assets of the organisation were 1282 and these were reduced

for year 2019 up to 1274. Apart from this, the current assets in 2018 were very low and these

were increased in 2019 up to 426. It shows that the entity is having more funds in 2019 to meet

all the short term obligation. It demonesses that liquidity of the entity is improved in this year.

Total equities for 2018 were 810 and the value of it is decreased for 2019 up to 310 that shows

reduced engagement of shareholder in business. On the other hand, total liabilities of the entity

for year 2018 were 824 which are increased for 2019 up to 1390. It shows that the debts of the

enterprise are increased that may affect functionality of business (Hendrikse, Bassens and Van

Meeteren, 2018).

In order to assess the position of business in more detail following financial ratios are

calculated:

Current ratio: It is a liquidity ratio which is used by businesses for the purpose of

making sure that all the short term liabilities of the firm will be paid with the help of current

assets or not. Calculation of it for T-Shirt Plc is as follows:

Particulars Formula 2018 2019

Current

assets

Current assets / current

liabilities

352 426

Current

liabilities 136 469

Result 2.59 0.91

Quick ratio: It is also a liquidity ratio which is used to determine the ability of the

enterprise to pay short term liabilities with the help of core current assets. Calculation of it for T-

Shirt Plc is as follows:

Particulars Formula 2018 2019

Quick assets

Quick assets / current

liabilities

263 305

Current liabilities 136 469

Result 1.93 0.65

Debt equity ratio: It is a financial ratio which is used for the purpose of analysing

efficiency of business and using the external as well as internal liabilities systematically (Martin

and Hofmann, 2017). The calculation of it are mentioned in following table for T-Shirt Plc:

Particulars Formula 2018 2019

3

analyse the financial statement.

From the exhibit 1, for statement of financial position of T-Shirt Plc it has been analysed

that for year 2018 the non-current assets of the organisation were 1282 and these were reduced

for year 2019 up to 1274. Apart from this, the current assets in 2018 were very low and these

were increased in 2019 up to 426. It shows that the entity is having more funds in 2019 to meet

all the short term obligation. It demonesses that liquidity of the entity is improved in this year.

Total equities for 2018 were 810 and the value of it is decreased for 2019 up to 310 that shows

reduced engagement of shareholder in business. On the other hand, total liabilities of the entity

for year 2018 were 824 which are increased for 2019 up to 1390. It shows that the debts of the

enterprise are increased that may affect functionality of business (Hendrikse, Bassens and Van

Meeteren, 2018).

In order to assess the position of business in more detail following financial ratios are

calculated:

Current ratio: It is a liquidity ratio which is used by businesses for the purpose of

making sure that all the short term liabilities of the firm will be paid with the help of current

assets or not. Calculation of it for T-Shirt Plc is as follows:

Particulars Formula 2018 2019

Current

assets

Current assets / current

liabilities

352 426

Current

liabilities 136 469

Result 2.59 0.91

Quick ratio: It is also a liquidity ratio which is used to determine the ability of the

enterprise to pay short term liabilities with the help of core current assets. Calculation of it for T-

Shirt Plc is as follows:

Particulars Formula 2018 2019

Quick assets

Quick assets / current

liabilities

263 305

Current liabilities 136 469

Result 1.93 0.65

Debt equity ratio: It is a financial ratio which is used for the purpose of analysing

efficiency of business and using the external as well as internal liabilities systematically (Martin

and Hofmann, 2017). The calculation of it are mentioned in following table for T-Shirt Plc:

Particulars Formula 2018 2019

3

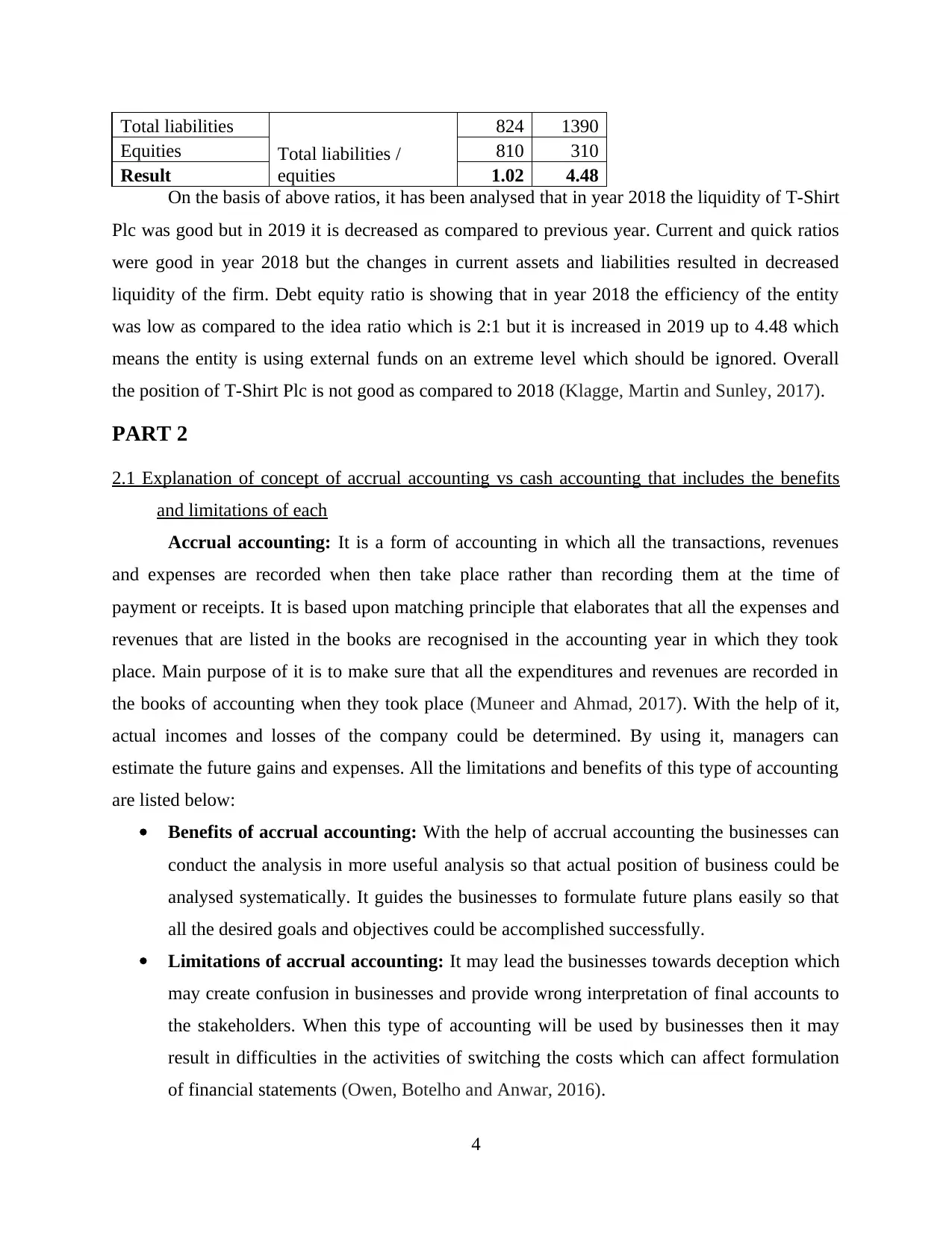

Total liabilities

Total liabilities /

equities

824 1390

Equities 810 310

Result 1.02 4.48

On the basis of above ratios, it has been analysed that in year 2018 the liquidity of T-Shirt

Plc was good but in 2019 it is decreased as compared to previous year. Current and quick ratios

were good in year 2018 but the changes in current assets and liabilities resulted in decreased

liquidity of the firm. Debt equity ratio is showing that in year 2018 the efficiency of the entity

was low as compared to the idea ratio which is 2:1 but it is increased in 2019 up to 4.48 which

means the entity is using external funds on an extreme level which should be ignored. Overall

the position of T-Shirt Plc is not good as compared to 2018 (Klagge, Martin and Sunley, 2017).

PART 2

2.1 Explanation of concept of accrual accounting vs cash accounting that includes the benefits

and limitations of each

Accrual accounting: It is a form of accounting in which all the transactions, revenues

and expenses are recorded when then take place rather than recording them at the time of

payment or receipts. It is based upon matching principle that elaborates that all the expenses and

revenues that are listed in the books are recognised in the accounting year in which they took

place. Main purpose of it is to make sure that all the expenditures and revenues are recorded in

the books of accounting when they took place (Muneer and Ahmad, 2017). With the help of it,

actual incomes and losses of the company could be determined. By using it, managers can

estimate the future gains and expenses. All the limitations and benefits of this type of accounting

are listed below:

Benefits of accrual accounting: With the help of accrual accounting the businesses can

conduct the analysis in more useful analysis so that actual position of business could be

analysed systematically. It guides the businesses to formulate future plans easily so that

all the desired goals and objectives could be accomplished successfully.

Limitations of accrual accounting: It may lead the businesses towards deception which

may create confusion in businesses and provide wrong interpretation of final accounts to

the stakeholders. When this type of accounting will be used by businesses then it may

result in difficulties in the activities of switching the costs which can affect formulation

of financial statements (Owen, Botelho and Anwar, 2016).

4

Total liabilities /

equities

824 1390

Equities 810 310

Result 1.02 4.48

On the basis of above ratios, it has been analysed that in year 2018 the liquidity of T-Shirt

Plc was good but in 2019 it is decreased as compared to previous year. Current and quick ratios

were good in year 2018 but the changes in current assets and liabilities resulted in decreased

liquidity of the firm. Debt equity ratio is showing that in year 2018 the efficiency of the entity

was low as compared to the idea ratio which is 2:1 but it is increased in 2019 up to 4.48 which

means the entity is using external funds on an extreme level which should be ignored. Overall

the position of T-Shirt Plc is not good as compared to 2018 (Klagge, Martin and Sunley, 2017).

PART 2

2.1 Explanation of concept of accrual accounting vs cash accounting that includes the benefits

and limitations of each

Accrual accounting: It is a form of accounting in which all the transactions, revenues

and expenses are recorded when then take place rather than recording them at the time of

payment or receipts. It is based upon matching principle that elaborates that all the expenses and

revenues that are listed in the books are recognised in the accounting year in which they took

place. Main purpose of it is to make sure that all the expenditures and revenues are recorded in

the books of accounting when they took place (Muneer and Ahmad, 2017). With the help of it,

actual incomes and losses of the company could be determined. By using it, managers can

estimate the future gains and expenses. All the limitations and benefits of this type of accounting

are listed below:

Benefits of accrual accounting: With the help of accrual accounting the businesses can

conduct the analysis in more useful analysis so that actual position of business could be

analysed systematically. It guides the businesses to formulate future plans easily so that

all the desired goals and objectives could be accomplished successfully.

Limitations of accrual accounting: It may lead the businesses towards deception which

may create confusion in businesses and provide wrong interpretation of final accounts to

the stakeholders. When this type of accounting will be used by businesses then it may

result in difficulties in the activities of switching the costs which can affect formulation

of financial statements (Owen, Botelho and Anwar, 2016).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash accounting: Under this type of accounting all the payments and receipts are

recorded in the books in the accounting period when they are received and paid. All the revenues

and expenses are listed in the books when cash related to them is received or paid. If the entity

will not make payment in the accounting year for the expenses which took place during the year

then it will not be recorded in the books. It will be listed in the accounts when cash of it will be

paid. In other words, it is a type of accounting in which only cash payments are recorded in the

books whether they are related to current accounting year or not.

Benefits of cash accounting: It helps to analyse the actual liquid position of business by

recording information of only cash transactions rather than accruals, advances etc. It

works as a short term indicator of profits of business that can help to formulate future

decisions regarding spending.

Limitations of cash accounting: The use of it is restricted as most of the businesses are

carried out on credit so use of it may result in negative interpretation of position of

business. When it will be used by a business then the entity may face difficulty to switch

from cash to accrual accounting because some expenses or incomes could be missed out

to record in books (Schmidt, Seibel and Thomes, 2016).

2.2 What are profit and cash flow and difference between all of them

Profit: It could be defined as the amount which is generated by a business on the sales

which is made during the year. The difference of sales and cost is known as profit. In financial

terms it could be described as the financial benefit which is created by business by performing all

the operations. Net profits for the year is calculated after deducting all the expenses, losses,

payments and taxes.

Cash flow: It is the difference between total cash inflows and outflows of a company

which have taken place during the accounting year. It is the total value of all the cash and cash

equivalents that are available to a business for carrying out all the future operations. By using it,

the investors and other stakeholders can analyse liquidity of business so that decision regarding

investment could be taken.

Difference between cash and profit:

Profit Cash flow

5

recorded in the books in the accounting period when they are received and paid. All the revenues

and expenses are listed in the books when cash related to them is received or paid. If the entity

will not make payment in the accounting year for the expenses which took place during the year

then it will not be recorded in the books. It will be listed in the accounts when cash of it will be

paid. In other words, it is a type of accounting in which only cash payments are recorded in the

books whether they are related to current accounting year or not.

Benefits of cash accounting: It helps to analyse the actual liquid position of business by

recording information of only cash transactions rather than accruals, advances etc. It

works as a short term indicator of profits of business that can help to formulate future

decisions regarding spending.

Limitations of cash accounting: The use of it is restricted as most of the businesses are

carried out on credit so use of it may result in negative interpretation of position of

business. When it will be used by a business then the entity may face difficulty to switch

from cash to accrual accounting because some expenses or incomes could be missed out

to record in books (Schmidt, Seibel and Thomes, 2016).

2.2 What are profit and cash flow and difference between all of them

Profit: It could be defined as the amount which is generated by a business on the sales

which is made during the year. The difference of sales and cost is known as profit. In financial

terms it could be described as the financial benefit which is created by business by performing all

the operations. Net profits for the year is calculated after deducting all the expenses, losses,

payments and taxes.

Cash flow: It is the difference between total cash inflows and outflows of a company

which have taken place during the accounting year. It is the total value of all the cash and cash

equivalents that are available to a business for carrying out all the future operations. By using it,

the investors and other stakeholders can analyse liquidity of business so that decision regarding

investment could be taken.

Difference between cash and profit:

Profit Cash flow

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

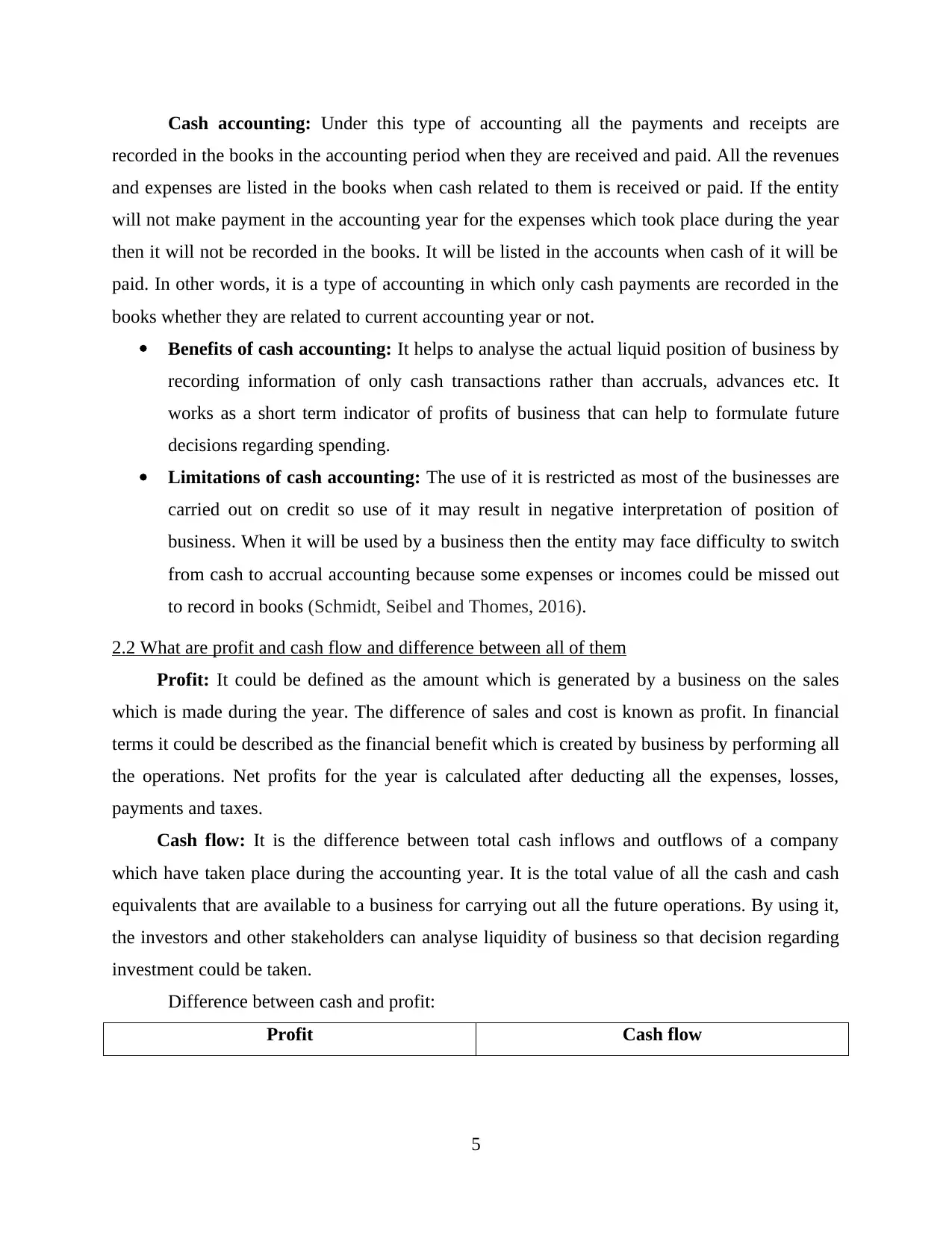

It is difference of total sales generated during

the year and cost of products.

The variation between total cash inflows and

outflows is known as cash flow.

It is reflected in the income statement or profit

and loss account of the company.

Cash flow statement is used to reflect the

actual value of cash flow.

With the help of it, profitability of entity could

be determined.

By using it actual liquidity of the enterprise can

be assessed.

All the incomes and gains are added in it and

all the losses and expenses are deducted from

it.

All the core current assets, cash and cash

equivalents are included in it.

PART 3

3.1 Definition of budget and explanation or purpose of preparing a budget

Budget: It could be described as the financial plan which is formulated for the purpose of

estimating the future incomes and expenses so that the desired goals and objectives could be met.

With the help of it, managers can analyse that the future expenses which may take place in

upcoming period could be dealt systematically or not. Main purpose due to which budget is

generated by entities is that it facilitates the entities to reduce possibility of overspending of

funds so that the liquidity of business could be maintained. Apart from this, another reason for

preparing budget is to estimate the future expenses and incomes so that plans according to it

could be formulated and funds could be arranged (Susan Parcells CPA, 2016).

3.2 Benefits of forming a limited company and listing it on a stock exchange

Limited company: It is type of corporation in which the liability of shareholders is

limited. It assures that the responsibilities of all the members of company as well as subscribers

is limited to an extent or their stake within the company. It is very beneficial for a firm to

become limited because with the help of it all the shareholders will get benefits for their share

within the company and their liabilities will be limited to the same. In the case of losses, they

will not be responsible to make payment of all the amount. Some of the key benefits of forming

and listing as a limited company are as follows:

It provides protection to the shareholders and other stakeholders through limited

liabilities within the organisation.

6

the year and cost of products.

The variation between total cash inflows and

outflows is known as cash flow.

It is reflected in the income statement or profit

and loss account of the company.

Cash flow statement is used to reflect the

actual value of cash flow.

With the help of it, profitability of entity could

be determined.

By using it actual liquidity of the enterprise can

be assessed.

All the incomes and gains are added in it and

all the losses and expenses are deducted from

it.

All the core current assets, cash and cash

equivalents are included in it.

PART 3

3.1 Definition of budget and explanation or purpose of preparing a budget

Budget: It could be described as the financial plan which is formulated for the purpose of

estimating the future incomes and expenses so that the desired goals and objectives could be met.

With the help of it, managers can analyse that the future expenses which may take place in

upcoming period could be dealt systematically or not. Main purpose due to which budget is

generated by entities is that it facilitates the entities to reduce possibility of overspending of

funds so that the liquidity of business could be maintained. Apart from this, another reason for

preparing budget is to estimate the future expenses and incomes so that plans according to it

could be formulated and funds could be arranged (Susan Parcells CPA, 2016).

3.2 Benefits of forming a limited company and listing it on a stock exchange

Limited company: It is type of corporation in which the liability of shareholders is

limited. It assures that the responsibilities of all the members of company as well as subscribers

is limited to an extent or their stake within the company. It is very beneficial for a firm to

become limited because with the help of it all the shareholders will get benefits for their share

within the company and their liabilities will be limited to the same. In the case of losses, they

will not be responsible to make payment of all the amount. Some of the key benefits of forming

and listing as a limited company are as follows:

It provides protection to the shareholders and other stakeholders through limited

liabilities within the organisation.

6

Forming a limited company provides tax and national insurance efficiency to the

business.

The credibility and reputation of a limited company in the market is very high so listing a

corporation as limited company can create a good market image (Torfs, 2018).

CONCLUSION

From the above project report it has been concluded that business finance could be

described as the financial resources that are required by a business to carry out all the operations

in systematic manner. While planning to analyse the competitiveness within the industry the

businesses can analyse financial position of competitors. For this purpose, ratio analysis could be

conducted and some of the ratios are gross and net margin, interest cover, quick, current and debt

equity ratio. There are two different types of accountings which could be used by businesses to

formulate the final accounts. These are cash and accrual accounting. Apart from this, there are

various types of budgets which could be used by entities for the purpose of meeting all the long

term objectives. On the other hand, if a company will be listed as limited company then it will

result in various benefits such as limited liabilities towards business.

7

business.

The credibility and reputation of a limited company in the market is very high so listing a

corporation as limited company can create a good market image (Torfs, 2018).

CONCLUSION

From the above project report it has been concluded that business finance could be

described as the financial resources that are required by a business to carry out all the operations

in systematic manner. While planning to analyse the competitiveness within the industry the

businesses can analyse financial position of competitors. For this purpose, ratio analysis could be

conducted and some of the ratios are gross and net margin, interest cover, quick, current and debt

equity ratio. There are two different types of accountings which could be used by businesses to

formulate the final accounts. These are cash and accrual accounting. Apart from this, there are

various types of budgets which could be used by entities for the purpose of meeting all the long

term objectives. On the other hand, if a company will be listed as limited company then it will

result in various benefits such as limited liabilities towards business.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Bezemer, D. and Hudson, M., 2016. Finance is not the economy: Reviving the conceptual

distinction. Journal of Economic Issues. 50(3). pp.745-768.

Botrić, V. and Božić, L., 2017. Access to finance–innovation relationship in post-transition. KnE

Social Sciences, pp.28-41.

Buckland, R. and Davis, E. W. eds., 2016. Finance for growing Enterprises. Routledge.

Colombo, M. G. and et.al., 2016. Open business models and venture capital finance. Industrial

and Corporate Change. 25(2). pp.353-370.

Hendrikse, R., Bassens, D. and Van Meeteren, M., 2018. The Appleization of finance: Charting

incumbent finance’s embrace of FinTech. Finance and society. 4(2). pp.159-80.

Klagge, B., Martin, R. and Sunley, P., 2017. The spatial structure of the financial system and the

funding of regional business: a comparison of Britain and Germany. In Handbook on

the Geographies of Money and Finance. Edward Elgar Publishing.

Martin, J. and Hofmann, E., 2017. Involving financial service providers in supply chain finance

practices. Journal of Applied Accounting Research.

Muneer, S. and Ahmad, R. A., 2017. Impact of Financing on Small and Medium Enterprises

(SMEs) Profitability with Moderating Role of Islamic Finance. Information

Management and Business Review. 9(2). pp.25-32.

Owen, R., Botelho, T. and Anwar, O., 2016. Exploring the success and barriers to SME access to

finance and its potential role in achieving growth. Research Paper. (53).

Schmidt, R. H., Seibel, H. D. and Thomes, P., 2016. From microfinance to inclusive finance:

Why local banking works. John Wiley & Sons.

Susan Parcells CPA, C. G. M. A., 2016. The power of finance automation. Strategic Finance.

98(6). p.40.

Torfs, W., 2018. EIF SME Access to Finance Index-June 2018 update (No. 2018/49). EIF

Working Paper.

8

Books and Journals:

Bezemer, D. and Hudson, M., 2016. Finance is not the economy: Reviving the conceptual

distinction. Journal of Economic Issues. 50(3). pp.745-768.

Botrić, V. and Božić, L., 2017. Access to finance–innovation relationship in post-transition. KnE

Social Sciences, pp.28-41.

Buckland, R. and Davis, E. W. eds., 2016. Finance for growing Enterprises. Routledge.

Colombo, M. G. and et.al., 2016. Open business models and venture capital finance. Industrial

and Corporate Change. 25(2). pp.353-370.

Hendrikse, R., Bassens, D. and Van Meeteren, M., 2018. The Appleization of finance: Charting

incumbent finance’s embrace of FinTech. Finance and society. 4(2). pp.159-80.

Klagge, B., Martin, R. and Sunley, P., 2017. The spatial structure of the financial system and the

funding of regional business: a comparison of Britain and Germany. In Handbook on

the Geographies of Money and Finance. Edward Elgar Publishing.

Martin, J. and Hofmann, E., 2017. Involving financial service providers in supply chain finance

practices. Journal of Applied Accounting Research.

Muneer, S. and Ahmad, R. A., 2017. Impact of Financing on Small and Medium Enterprises

(SMEs) Profitability with Moderating Role of Islamic Finance. Information

Management and Business Review. 9(2). pp.25-32.

Owen, R., Botelho, T. and Anwar, O., 2016. Exploring the success and barriers to SME access to

finance and its potential role in achieving growth. Research Paper. (53).

Schmidt, R. H., Seibel, H. D. and Thomes, P., 2016. From microfinance to inclusive finance:

Why local banking works. John Wiley & Sons.

Susan Parcells CPA, C. G. M. A., 2016. The power of finance automation. Strategic Finance.

98(6). p.40.

Torfs, W., 2018. EIF SME Access to Finance Index-June 2018 update (No. 2018/49). EIF

Working Paper.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.