Business Finance Report: Profit, Cash Flow and Working Capital

VerifiedAdded on 2022/12/14

|11

|3146

|99

Report

AI Summary

This report delves into the core concepts of business finance, focusing on profit, cash flow, and working capital. The first part of the report explains the differences between profit and cash flow, the definition of working capital, and how changes in working capital impact cash flow. It also provides an application of these concepts to a specific company, analyzing its financial challenges and suggesting improvements. The second part of the report presents a monthly cash budget for four months, explaining different types of cash flow and their importance. The report offers an in-depth analysis of the company's financial situation, including recommendations for improving its cash flow management and overall financial health, such as improving receivables collection and managing payables effectively.

Business finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Business financing implies the money and credit used in the corporation. Funding is the

corporate base. Acquisitions of land, commodities, manufactured goods and other economic

operations are needed under financial requirements. The term Business Finance represents the

amount of money spent on a company. Financing is important for a company, and it is necessary

to buy assets, raw materials, maintain the business and manage all related to business financial

operations. The report is divided into two parts in which part one summarizes about concept of

profit, receivables, payables and role of cash flow in management of working capital. In addition

to this part two of report summarizes about role of cash flow as well as calculation of cash flow

is also done in accordance of given scenario. In addition to this, recommendation is also

provided to respective company as per the analysis of cash flow in a significant manner.

Business financing implies the money and credit used in the corporation. Funding is the

corporate base. Acquisitions of land, commodities, manufactured goods and other economic

operations are needed under financial requirements. The term Business Finance represents the

amount of money spent on a company. Financing is important for a company, and it is necessary

to buy assets, raw materials, maintain the business and manage all related to business financial

operations. The report is divided into two parts in which part one summarizes about concept of

profit, receivables, payables and role of cash flow in management of working capital. In addition

to this part two of report summarizes about role of cash flow as well as calculation of cash flow

is also done in accordance of given scenario. In addition to this, recommendation is also

provided to respective company as per the analysis of cash flow in a significant manner.

Contents

EXECUTIVE SUMMARY.........................................................................................................................2

TASK 1.......................................................................................................................................................4

TASK 2.......................................................................................................................................................6

REFERENCES..........................................................................................................................................11

EXECUTIVE SUMMARY.........................................................................................................................2

TASK 1.......................................................................................................................................................4

TASK 2.......................................................................................................................................................6

REFERENCES..........................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

Explain:

a. what is meant by Profit and Cash flow and how they are different

The profit is based exclusively on the accounting concept used to exclude revenue, including

depletion and taxation, after sales costs have been deducted (Klopotan, Zoroja and Meško 2018).

Cash flow, as its name implies, either payment or collection is the transfer of cash. Non-

Financial investments including depreciation are the main differences in cash flow and profit.

Operating expenses and financial income or loss. The profit accounts for these non-cash costs,

but they are ignored by the cash flow strategy. Cash flow is none but is not widely used for

capital budgeting and financial reporting.

CF is a big concern for investors and businesses, since it is corporate lifeblood. "How does the

CF vary from the revenues of a corporation?" Income and benefit are built on the concepts of

accrual accounting that smooth out costs and balance profit as product lines are provided. In fact,

a corporation's own operating income or net benefit could vary significantly from CAF based on

profit means of a systematic and the corresponding concept.

b. what is meant by Working Capital

Working capital is classified as net work capital (NWC) and differs from existing assets of the

Business, for example currency, receivable accounts (unpaid consumer bills) and inventory of

commodities and final inventory and their interest expense, for instance, cash management (Mia

and Sufi, 2018). Net operating capital is a liquidity measurement of a business that refers to the

discrepancy between actual operating assets and total revenues liabilities. The calculations are

often identical and come from business cash plus receivable accounts and stock, less payable

accounts and less expenditure. Working capital refers to the disparity between existing and

current assets. This is done to see just how many outstanding liabilities Current Assets Company

has to pay. That is called the liquidity method, where lenders lock it in to see if the enterprise is

sufficiently solvent to pay its short-term commitments. Current assets include accounts or

commercial debts and are clients of the business who have to compensate the goods or services

that they receive. The stock applies to the products that the company buys and holds to sell to its

Explain:

a. what is meant by Profit and Cash flow and how they are different

The profit is based exclusively on the accounting concept used to exclude revenue, including

depletion and taxation, after sales costs have been deducted (Klopotan, Zoroja and Meško 2018).

Cash flow, as its name implies, either payment or collection is the transfer of cash. Non-

Financial investments including depreciation are the main differences in cash flow and profit.

Operating expenses and financial income or loss. The profit accounts for these non-cash costs,

but they are ignored by the cash flow strategy. Cash flow is none but is not widely used for

capital budgeting and financial reporting.

CF is a big concern for investors and businesses, since it is corporate lifeblood. "How does the

CF vary from the revenues of a corporation?" Income and benefit are built on the concepts of

accrual accounting that smooth out costs and balance profit as product lines are provided. In fact,

a corporation's own operating income or net benefit could vary significantly from CAF based on

profit means of a systematic and the corresponding concept.

b. what is meant by Working Capital

Working capital is classified as net work capital (NWC) and differs from existing assets of the

Business, for example currency, receivable accounts (unpaid consumer bills) and inventory of

commodities and final inventory and their interest expense, for instance, cash management (Mia

and Sufi, 2018). Net operating capital is a liquidity measurement of a business that refers to the

discrepancy between actual operating assets and total revenues liabilities. The calculations are

often identical and come from business cash plus receivable accounts and stock, less payable

accounts and less expenditure. Working capital refers to the disparity between existing and

current assets. This is done to see just how many outstanding liabilities Current Assets Company

has to pay. That is called the liquidity method, where lenders lock it in to see if the enterprise is

sufficiently solvent to pay its short-term commitments. Current assets include accounts or

commercial debts and are clients of the business who have to compensate the goods or services

that they receive. The stock applies to the products that the company buys and holds to sell to its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

clients. Payable implies the liabilities due the corporation for the products it has purchased or

purchased.

The inventory relates to the products that the company purchases and holds to sell its clients. The

liability due by the corporation for products that it has purchased or other costs such as charges

for taxes, insurance and leasing costs.

c. how changes in Working Capital affect Cash flow

The increases in working capital have the greatest effect on the cash flow. Cash flows are often

contrasted to each other with comparable accounts of existing properties (Anderson, Chandy and

Zia, 2018). When the existing assets are higher than last year, the cash flows are considered as

outflow. This is that if present properties such as commercial receivables are not obtained, it

ensures that the cash of the firm is blocked. The same applies to stocks in which the actual

balance reaches the preceding year. The gap is considered a reduction in job capital when cash is

blocked in the company's stocks. Assume the firm has $100 million in exchange receivables this

year. Suppose the firm had $100 million in accounts receivable in the current year and said $90

million in the prior year. The $10 million gap is perceived to be a decline in working capital,

since accounts receivable have been raised because money is not earned, but the receivables have

grown. For existing liabilities, the same is valid. ii The firm takes longer to settle its existing

obligations. It ensures the cash is used and the working capital surplus is raised.

ii. Apply the concepts in (i) above to this company.

The firm has net operating revenue of this million, but it receives more loans as its loans have

risen from 60 million dollars to 95 million dollars. For big orders put the business is payable in

the amount of $10 million and thus saved cash and is seen as improved by the delayed use of

cash. The business disputes over the products sold to Sadidas, who are clients of the company

(Apollos, Stephen and Atunbi, 2018). Owing to the failure to recover customer duties, which

ensures commercial debts. In other words, because of a benefit not turned to currency, business

has problems in working capital. As a consequence, consumers do not pay and business takes

loans to operate. The business disputes over the products that are shipped to the company

purchased.

The inventory relates to the products that the company purchases and holds to sell its clients. The

liability due by the corporation for products that it has purchased or other costs such as charges

for taxes, insurance and leasing costs.

c. how changes in Working Capital affect Cash flow

The increases in working capital have the greatest effect on the cash flow. Cash flows are often

contrasted to each other with comparable accounts of existing properties (Anderson, Chandy and

Zia, 2018). When the existing assets are higher than last year, the cash flows are considered as

outflow. This is that if present properties such as commercial receivables are not obtained, it

ensures that the cash of the firm is blocked. The same applies to stocks in which the actual

balance reaches the preceding year. The gap is considered a reduction in job capital when cash is

blocked in the company's stocks. Assume the firm has $100 million in exchange receivables this

year. Suppose the firm had $100 million in accounts receivable in the current year and said $90

million in the prior year. The $10 million gap is perceived to be a decline in working capital,

since accounts receivable have been raised because money is not earned, but the receivables have

grown. For existing liabilities, the same is valid. ii The firm takes longer to settle its existing

obligations. It ensures the cash is used and the working capital surplus is raised.

ii. Apply the concepts in (i) above to this company.

The firm has net operating revenue of this million, but it receives more loans as its loans have

risen from 60 million dollars to 95 million dollars. For big orders put the business is payable in

the amount of $10 million and thus saved cash and is seen as improved by the delayed use of

cash. The business disputes over the products sold to Sadidas, who are clients of the company

(Apollos, Stephen and Atunbi, 2018). Owing to the failure to recover customer duties, which

ensures commercial debts. In other words, because of a benefit not turned to currency, business

has problems in working capital. As a consequence, consumers do not pay and business takes

loans to operate. The business disputes over the products that are shipped to the company

Sadidas. This means the commercial receivables due to the failure to recover consumer duties.

Thus, business operating capital problems are not turned into cash because of profit. As a

consequence, clients do not pay and the firm takes loans to run the place or to satisfy the

demands of working capital.

iii. Analyze and recommend what steps should now be taken to improve.

The business must resolve the problems with Sadidas. The fundraising of your corporate clients

will facilitate the inflow of working capital (Young, 2018). The firm relies exclusively on its two

clients. In order to be more effective in managing our working resources, the business can meet

more consumers and build a number of customers that reimburse it on time. It should really take

additional borrowing time from its vendors or decrease the credit cap for its consumers for the

debt load. If it wants to divide ownership, the corporation should sell new stock to the public.

This will cause the organization to lose power, but it definitely would alleviate the operating

capital restrictions.

TASK 2

1. A monthly cash budget for the FOUR months from 1st Jan to 30 April 2021.

Cash flow- The cash flow of a company, company or entity is the increase or decrease in the sum

of capital (Owen, Hussain and Botelho, 2019). The concept is used in finances to denote the

amount of cash produced or spent over the course of a period of time (currency). Many forms of

CFs with different essential applications for a corporation and financial analysis are available.

Everything will be discussed in depth in this guide.

Types of Cash Flow-

There are many forms of cash flow, so a thorough knowledge of each of them is necessary. If

someone is talking about CF, they can say either of the following types, so make sure to explain

the word used in cash flow (Block, Cumming and Vismara, 2018).

Operating cash – cash created by a key market activity of a firm – does not involve CF from

spending. The cash flow statement of the group (the first section). The cash obtained from a key

business activity of a company is defined. Cash inflows and operating outflow are reported in the

first section when compiling a cash flow statement. Cash inflows here include the money earned

Thus, business operating capital problems are not turned into cash because of profit. As a

consequence, clients do not pay and the firm takes loans to run the place or to satisfy the

demands of working capital.

iii. Analyze and recommend what steps should now be taken to improve.

The business must resolve the problems with Sadidas. The fundraising of your corporate clients

will facilitate the inflow of working capital (Young, 2018). The firm relies exclusively on its two

clients. In order to be more effective in managing our working resources, the business can meet

more consumers and build a number of customers that reimburse it on time. It should really take

additional borrowing time from its vendors or decrease the credit cap for its consumers for the

debt load. If it wants to divide ownership, the corporation should sell new stock to the public.

This will cause the organization to lose power, but it definitely would alleviate the operating

capital restrictions.

TASK 2

1. A monthly cash budget for the FOUR months from 1st Jan to 30 April 2021.

Cash flow- The cash flow of a company, company or entity is the increase or decrease in the sum

of capital (Owen, Hussain and Botelho, 2019). The concept is used in finances to denote the

amount of cash produced or spent over the course of a period of time (currency). Many forms of

CFs with different essential applications for a corporation and financial analysis are available.

Everything will be discussed in depth in this guide.

Types of Cash Flow-

There are many forms of cash flow, so a thorough knowledge of each of them is necessary. If

someone is talking about CF, they can say either of the following types, so make sure to explain

the word used in cash flow (Block, Cumming and Vismara, 2018).

Operating cash – cash created by a key market activity of a firm – does not involve CF from

spending. The cash flow statement of the group (the first section). The cash obtained from a key

business activity of a company is defined. Cash inflows and operating outflow are reported in the

first section when compiling a cash flow statement. Cash inflows here include the money earned

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

after goods or services have been sold. Cash outflows from activities include operating expenses

such as rental costs, product sold expenses etc.

Free Cash Flow to Equities (FCFE) — FCFE is the money remaining after the company is

reinvested (capital expenditures). This is every transition, that is to say the rise or decrease in a

company's long-term assets (Paltrinieri and Kutan, 2019). The acquisition of fixed assets, any

loans provided by the company, any income assumed in an investment account and the lovers

will be described.

Free Cash Flow to Business (FCFF) – This metric supposedly would not exploit an enterprise

(debt). It's being used to model and evaluate financially. Financing activity cash inflow or

outflow is registered as a longer-term increase or decrease is followed in the amount of debt,

liabilities, corporate capital or dividends. An illustration of cash flow from finance would include

interest or interest rates, repurchases of assets, issued dividends, accrued liabilities, and more.

For the cash flow analysis, different calculation metrics are used to define the company's

liquidity status and other business costs for the periodical balance measured for these kinds of

liquidity flows.

Net cash shift – The adjustment from one financial cycle to the next in the sum of cash flow. It's

at the edge of the report on cash flow (Shi, Sun and Zhang, 2018).

Cash flows may be positive or harmful as mentioned. The calculation is based on a deduction of

the amount of the cash at the start of a time also known as the account payable, the amount of

money at the end of the term (may be week, half or even year) or the equilibrium at the close.

The tangible improvement means that at the end of a certain time you have more currency. If the

differential is significant, it implies that, relative to the initial balance, at the end of the given

time you have much less cash. Cash balance accounts are applied to predict where the cash

comes from and goes out. It consists of three primary types of operational cash flows that include

daily transactions, cash flow investments that include transactions for growth and cash flow

finance, including transactions in respect of dividends paid to shareholders. The fund has three

major groups. Even so, the cash flow amount is not an optimal criterion for analyzing an

investment firm. In order to conclude, a company's balance sheet and revenue declarations

should be reviewed closely (Popescu and Popescu, 2019). The cash rate for an enterprise may

such as rental costs, product sold expenses etc.

Free Cash Flow to Equities (FCFE) — FCFE is the money remaining after the company is

reinvested (capital expenditures). This is every transition, that is to say the rise or decrease in a

company's long-term assets (Paltrinieri and Kutan, 2019). The acquisition of fixed assets, any

loans provided by the company, any income assumed in an investment account and the lovers

will be described.

Free Cash Flow to Business (FCFF) – This metric supposedly would not exploit an enterprise

(debt). It's being used to model and evaluate financially. Financing activity cash inflow or

outflow is registered as a longer-term increase or decrease is followed in the amount of debt,

liabilities, corporate capital or dividends. An illustration of cash flow from finance would include

interest or interest rates, repurchases of assets, issued dividends, accrued liabilities, and more.

For the cash flow analysis, different calculation metrics are used to define the company's

liquidity status and other business costs for the periodical balance measured for these kinds of

liquidity flows.

Net cash shift – The adjustment from one financial cycle to the next in the sum of cash flow. It's

at the edge of the report on cash flow (Shi, Sun and Zhang, 2018).

Cash flows may be positive or harmful as mentioned. The calculation is based on a deduction of

the amount of the cash at the start of a time also known as the account payable, the amount of

money at the end of the term (may be week, half or even year) or the equilibrium at the close.

The tangible improvement means that at the end of a certain time you have more currency. If the

differential is significant, it implies that, relative to the initial balance, at the end of the given

time you have much less cash. Cash balance accounts are applied to predict where the cash

comes from and goes out. It consists of three primary types of operational cash flows that include

daily transactions, cash flow investments that include transactions for growth and cash flow

finance, including transactions in respect of dividends paid to shareholders. The fund has three

major groups. Even so, the cash flow amount is not an optimal criterion for analyzing an

investment firm. In order to conclude, a company's balance sheet and revenue declarations

should be reviewed closely (Popescu and Popescu, 2019). The cash rate for an enterprise may

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increase, as some of its properties may have been sold, but profitability does not improve. If the

firm sells some of its properties to pay off the loan, this would be a bad signal and more clarity

should be sought. If the corporation does not spend profits, it is a bad sign that it does not take

the chance to diversify or expand revenue. Cash flow is the money which moves (flows) within

one month from and into the company. While it often seems that cash flow is only one direction

— it flows all directions out of business. Cash comes from vendors or customers who purchase

their services or goods. If at the time of payment consumers don't pay, these cash flows are

derived from the sale of receivables. Cash leaves the company in the form of expense transfers

such as rents or hypotheses, annual interest payments and other payables in payments for

taxation. Cash is very cash for some companies, such as cafes and retailers: money and paper

money. The company collects cash and also pays its accounts in cash. Cash companies have a

particular difficulty with tracking cash flow, particularly when they cannot monitor incomes until

invoices or other documents are available.

Cash balance is the sum of cash or its company counterparts in inflow and outflow. The amount

of cash spent or produced within a given time is determined. In its review, the current cash

streams and future inflows are also identified (Gordon, 2019). The current cash stream for a

particular period is determined by decreasing from the close balance the opening balance of a

particular period. Cash flows will lead to a negative or optimistic balance after it has been

measured. A positive balance means that the firm has enough cash to meet its imminent liquidity

needs, while a deficit means that the liquidity is limited. However, in order to assess the true

liquidity situation the cash flow of the firm should be evaluated along with the financial

statement as well as the accounting. In addition, an increasing cash flow can not necessarily be a

good signal and should be carefully analyzed in order to reach a final conclusion (Boschmans

and Pissareva, 2018).

Number of Employees 9

Month December January February March April

Units Sold 10 10 15 25 30

firm sells some of its properties to pay off the loan, this would be a bad signal and more clarity

should be sought. If the corporation does not spend profits, it is a bad sign that it does not take

the chance to diversify or expand revenue. Cash flow is the money which moves (flows) within

one month from and into the company. While it often seems that cash flow is only one direction

— it flows all directions out of business. Cash comes from vendors or customers who purchase

their services or goods. If at the time of payment consumers don't pay, these cash flows are

derived from the sale of receivables. Cash leaves the company in the form of expense transfers

such as rents or hypotheses, annual interest payments and other payables in payments for

taxation. Cash is very cash for some companies, such as cafes and retailers: money and paper

money. The company collects cash and also pays its accounts in cash. Cash companies have a

particular difficulty with tracking cash flow, particularly when they cannot monitor incomes until

invoices or other documents are available.

Cash balance is the sum of cash or its company counterparts in inflow and outflow. The amount

of cash spent or produced within a given time is determined. In its review, the current cash

streams and future inflows are also identified (Gordon, 2019). The current cash stream for a

particular period is determined by decreasing from the close balance the opening balance of a

particular period. Cash flows will lead to a negative or optimistic balance after it has been

measured. A positive balance means that the firm has enough cash to meet its imminent liquidity

needs, while a deficit means that the liquidity is limited. However, in order to assess the true

liquidity situation the cash flow of the firm should be evaluated along with the financial

statement as well as the accounting. In addition, an increasing cash flow can not necessarily be a

good signal and should be carefully analyzed in order to reach a final conclusion (Boschmans

and Pissareva, 2018).

Number of Employees 9

Month December January February March April

Units Sold 10 10 15 25 30

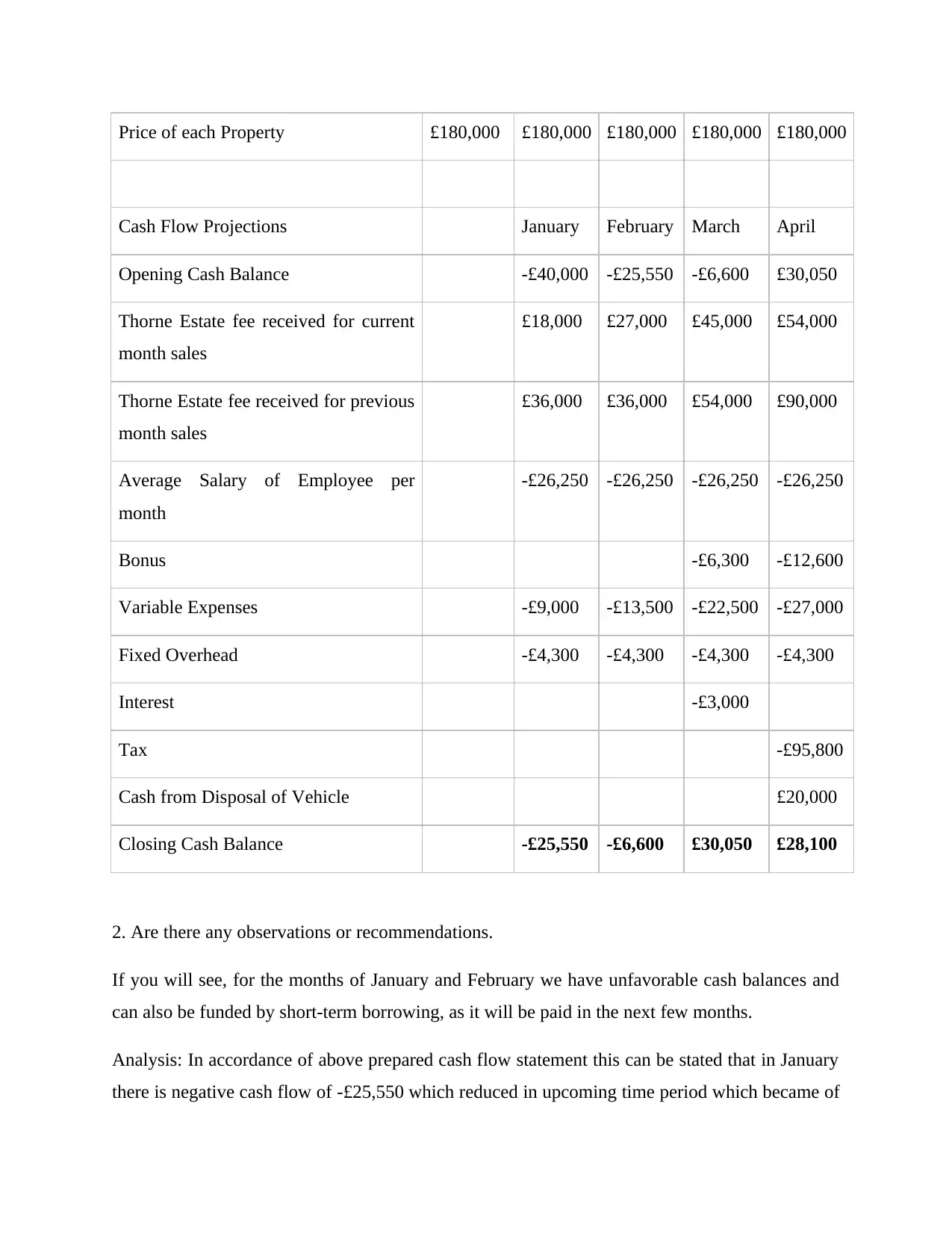

Price of each Property £180,000 £180,000 £180,000 £180,000 £180,000

Cash Flow Projections January February March April

Opening Cash Balance -£40,000 -£25,550 -£6,600 £30,050

Thorne Estate fee received for current

month sales

£18,000 £27,000 £45,000 £54,000

Thorne Estate fee received for previous

month sales

£36,000 £36,000 £54,000 £90,000

Average Salary of Employee per

month

-£26,250 -£26,250 -£26,250 -£26,250

Bonus -£6,300 -£12,600

Variable Expenses -£9,000 -£13,500 -£22,500 -£27,000

Fixed Overhead -£4,300 -£4,300 -£4,300 -£4,300

Interest -£3,000

Tax -£95,800

Cash from Disposal of Vehicle £20,000

Closing Cash Balance -£25,550 -£6,600 £30,050 £28,100

2. Are there any observations or recommendations.

If you will see, for the months of January and February we have unfavorable cash balances and

can also be funded by short-term borrowing, as it will be paid in the next few months.

Analysis: In accordance of above prepared cash flow statement this can be stated that in January

there is negative cash flow of -£25,550 which reduced in upcoming time period which became of

Cash Flow Projections January February March April

Opening Cash Balance -£40,000 -£25,550 -£6,600 £30,050

Thorne Estate fee received for current

month sales

£18,000 £27,000 £45,000 £54,000

Thorne Estate fee received for previous

month sales

£36,000 £36,000 £54,000 £90,000

Average Salary of Employee per

month

-£26,250 -£26,250 -£26,250 -£26,250

Bonus -£6,300 -£12,600

Variable Expenses -£9,000 -£13,500 -£22,500 -£27,000

Fixed Overhead -£4,300 -£4,300 -£4,300 -£4,300

Interest -£3,000

Tax -£95,800

Cash from Disposal of Vehicle £20,000

Closing Cash Balance -£25,550 -£6,600 £30,050 £28,100

2. Are there any observations or recommendations.

If you will see, for the months of January and February we have unfavorable cash balances and

can also be funded by short-term borrowing, as it will be paid in the next few months.

Analysis: In accordance of above prepared cash flow statement this can be stated that in January

there is negative cash flow of -£25,550 which reduced in upcoming time period which became of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

-£6,600. On the other hands, in March this became positive till £30,050. This is so because of

increased volume of cash receipts. In addition to this, in April this became of £28,100. This

shows that company’s cash flow is fluctuating in different month of accounting period.

Recommendation: In accordance of above project report this can be suggested that above

company should focus on those elements in which company’s cash expenses are increasing

because due to higher expenses there is negative cash flow in starting month of accounting

period. On the other hands, in last two months company’s cash flow is positive and this is so

because of higher cash receivables. Hence company needs to concentrate on those operations

which are leading to more number of cash receivables during the same accounting period.

increased volume of cash receipts. In addition to this, in April this became of £28,100. This

shows that company’s cash flow is fluctuating in different month of accounting period.

Recommendation: In accordance of above project report this can be suggested that above

company should focus on those elements in which company’s cash expenses are increasing

because due to higher expenses there is negative cash flow in starting month of accounting

period. On the other hands, in last two months company’s cash flow is positive and this is so

because of higher cash receivables. Hence company needs to concentrate on those operations

which are leading to more number of cash receivables during the same accounting period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering

Business Management, 10, p.1847979018797013.

Mian, A. and Sufi, A., 2018. Finance and business cycles: the credit-driven household demand

channel. Journal of Economic Perspectives, 32(3), pp.31-58.

Anderson, S.J., Chandy, R. and Zia, B., 2018. Pathways to profits: The impact of marketing vs.

finance skills on business performance. Management Science, 64(12), pp.5559-5583.

Young, C., 2018. Can women win on the obstacle course of business finance?.

Apollos, E.A., Stephen, O.O. and Atunbi, J.A., 2018. Venture Capital as Source of Business

Finance: Evaluation of the Awareness Level of Small and Medium Scale Enterprises in

Nigeria. International Journal of Economics and Business Management, 4(7), pp.104-

112.

Owen, R., Mac an Bhaird, C., Hussain, J. and Botelho, T., 2019. Blockchain and other

innovations in entrepreneurial finance: Implications for future policy. Strategic

Change, 28(1), p.5.

Block, J.H., Colombo, M.G., Cumming, D.J. and Vismara, S., 2018. New players in

entrepreneurial finance and why they are there. Small Business Economics, 50(2),

pp.239-250.

Paltrinieri, A. and Kutan, A., 2019. Islamic finance and business: an overview with directions for

further research. International Journal of Emerging Markets.

Shi, G., Sun, J. and Zhang, L., 2018. Product market competition and earnings management: A

firm‐level analysis. Journal of Business Finance & Accounting, 45(5-6), pp.604-624.

Popescu, C.R.G. and Popescu, G.N., 2019. An exploratory study based on a questionnaire

concerning green and sustainable finance, corporate social responsibility, and

performance: Evidence from the Romanian business environment. Journal of Risk and

Financial Management, 12(4), p.162.

Gordon, H., 2019. EMERGING TRENDS IN BUSINESS FINANCE: AFIA

PERSPECTIVE. AJAF, (2), pp.37-44.

Boschmans, K. and Pissareva, L., 2018. Fostering Markets for SME Finance: Matching Business

and Investor Needs.

Klopotan, I., Zoroja, J. and Meško, M., 2018. Early warning system in business, finance, and

economics: Bibliometric and topic analysis. International Journal of Engineering

Business Management, 10, p.1847979018797013.

Mian, A. and Sufi, A., 2018. Finance and business cycles: the credit-driven household demand

channel. Journal of Economic Perspectives, 32(3), pp.31-58.

Anderson, S.J., Chandy, R. and Zia, B., 2018. Pathways to profits: The impact of marketing vs.

finance skills on business performance. Management Science, 64(12), pp.5559-5583.

Young, C., 2018. Can women win on the obstacle course of business finance?.

Apollos, E.A., Stephen, O.O. and Atunbi, J.A., 2018. Venture Capital as Source of Business

Finance: Evaluation of the Awareness Level of Small and Medium Scale Enterprises in

Nigeria. International Journal of Economics and Business Management, 4(7), pp.104-

112.

Owen, R., Mac an Bhaird, C., Hussain, J. and Botelho, T., 2019. Blockchain and other

innovations in entrepreneurial finance: Implications for future policy. Strategic

Change, 28(1), p.5.

Block, J.H., Colombo, M.G., Cumming, D.J. and Vismara, S., 2018. New players in

entrepreneurial finance and why they are there. Small Business Economics, 50(2),

pp.239-250.

Paltrinieri, A. and Kutan, A., 2019. Islamic finance and business: an overview with directions for

further research. International Journal of Emerging Markets.

Shi, G., Sun, J. and Zhang, L., 2018. Product market competition and earnings management: A

firm‐level analysis. Journal of Business Finance & Accounting, 45(5-6), pp.604-624.

Popescu, C.R.G. and Popescu, G.N., 2019. An exploratory study based on a questionnaire

concerning green and sustainable finance, corporate social responsibility, and

performance: Evidence from the Romanian business environment. Journal of Risk and

Financial Management, 12(4), p.162.

Gordon, H., 2019. EMERGING TRENDS IN BUSINESS FINANCE: AFIA

PERSPECTIVE. AJAF, (2), pp.37-44.

Boschmans, K. and Pissareva, L., 2018. Fostering Markets for SME Finance: Matching Business

and Investor Needs.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.