Business Finance: Performance Analysis and Financial Statements Review

VerifiedAdded on 2022/12/30

|12

|3339

|66

Report

AI Summary

This report provides a comprehensive analysis of T-Shirt Ltd's financial performance for the years 2018 and 2019. It begins with an examination of the statement of profit or loss, utilizing ratio analysis to assess the company's liquidity, profitability, and efficiency. Key ratios such as current ratio, quick ratio, gross profit margin, net profit margin, and return on assets are calculated and interpreted, highlighting significant declines in several areas. The report then proceeds to analyze the statement of financial position, evaluating ratios like debt-to-equity, proprietary ratio, asset turnover, and inventory turnover, revealing further challenges in the company's financial health. Part 2 delves into the concepts of accrual accounting versus cash accounting, outlining their benefits and limitations, followed by a discussion on the differences between profit and cash flow. Finally, Part 3 defines the purpose of budgeting and the benefits of forming a limited company and listing it on the stock exchange. The report emphasizes the need for T-Shirt Ltd to implement strategies to improve its financial performance and sustain its brand image.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Part 1: Business Performance Analysis......................................................................................2

1.1 Statement of Profit or Loss..............................................................................................2

1.2 Statement of Financial Position.......................................................................................3

PART- 2.....................................................................................................................................5

2.1 Concept of accrual accounting versus cash accounting with benefits as well as

limitation................................................................................................................................5

2.2 Profit and cash Flow and the way they are different........................................................6

PART-3......................................................................................................................................7

3.1 Define budget and purpose of preparing a budget...........................................................7

3.2 Main benefits of forming a limited company and listing it on stock exchange...............7

REFERENCES...........................................................................................................................9

Appendix..............................................................................................................................10

Part 1: Business Performance Analysis......................................................................................2

1.1 Statement of Profit or Loss..............................................................................................2

1.2 Statement of Financial Position.......................................................................................3

PART- 2.....................................................................................................................................5

2.1 Concept of accrual accounting versus cash accounting with benefits as well as

limitation................................................................................................................................5

2.2 Profit and cash Flow and the way they are different........................................................6

PART-3......................................................................................................................................7

3.1 Define budget and purpose of preparing a budget...........................................................7

3.2 Main benefits of forming a limited company and listing it on stock exchange...............7

REFERENCES...........................................................................................................................9

Appendix..............................................................................................................................10

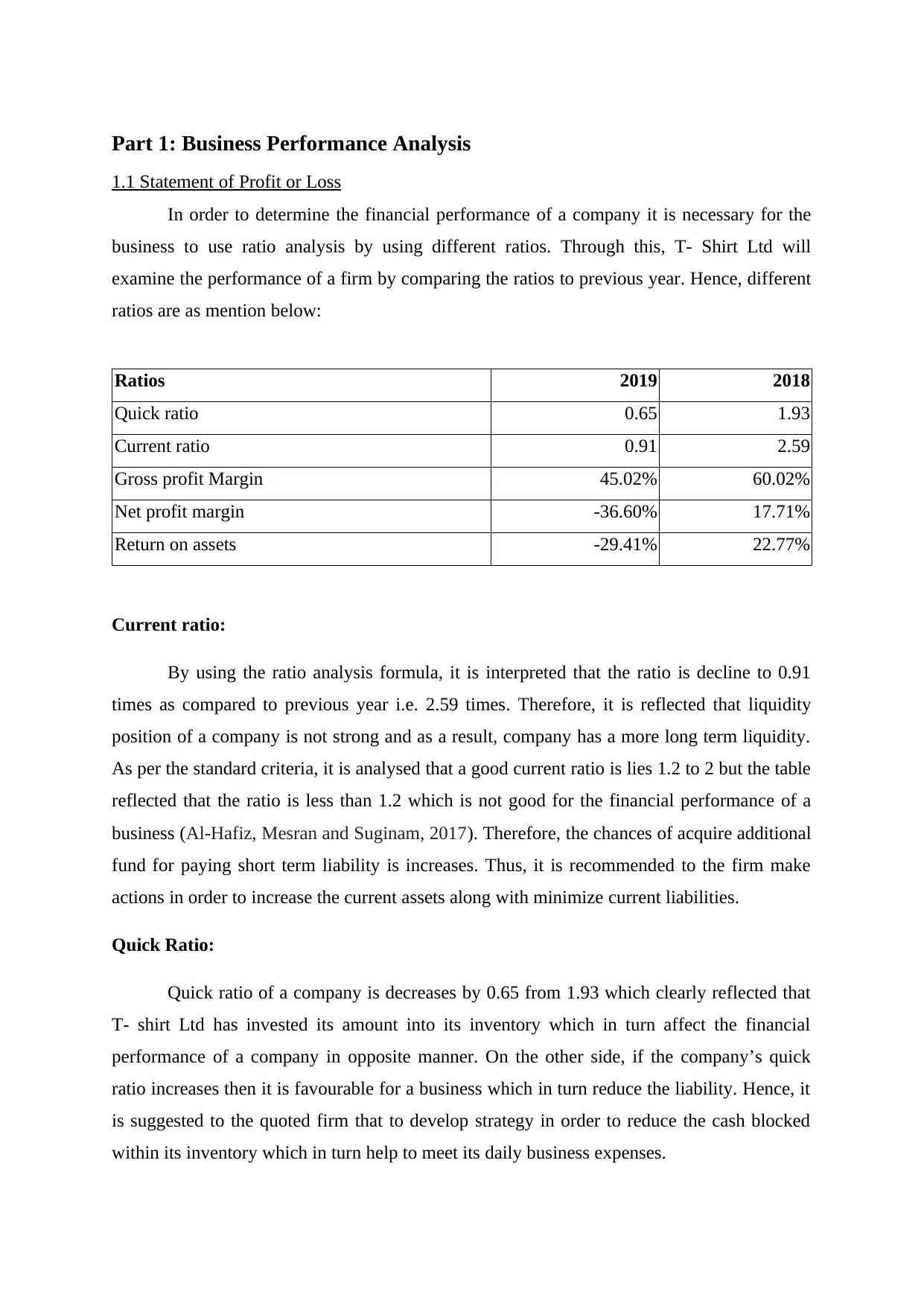

Part 1: Business Performance Analysis

1.1 Statement of Profit or Loss

In order to determine the financial performance of a company it is necessary for the

business to use ratio analysis by using different ratios. Through this, T- Shirt Ltd will

examine the performance of a firm by comparing the ratios to previous year. Hence, different

ratios are as mention below:

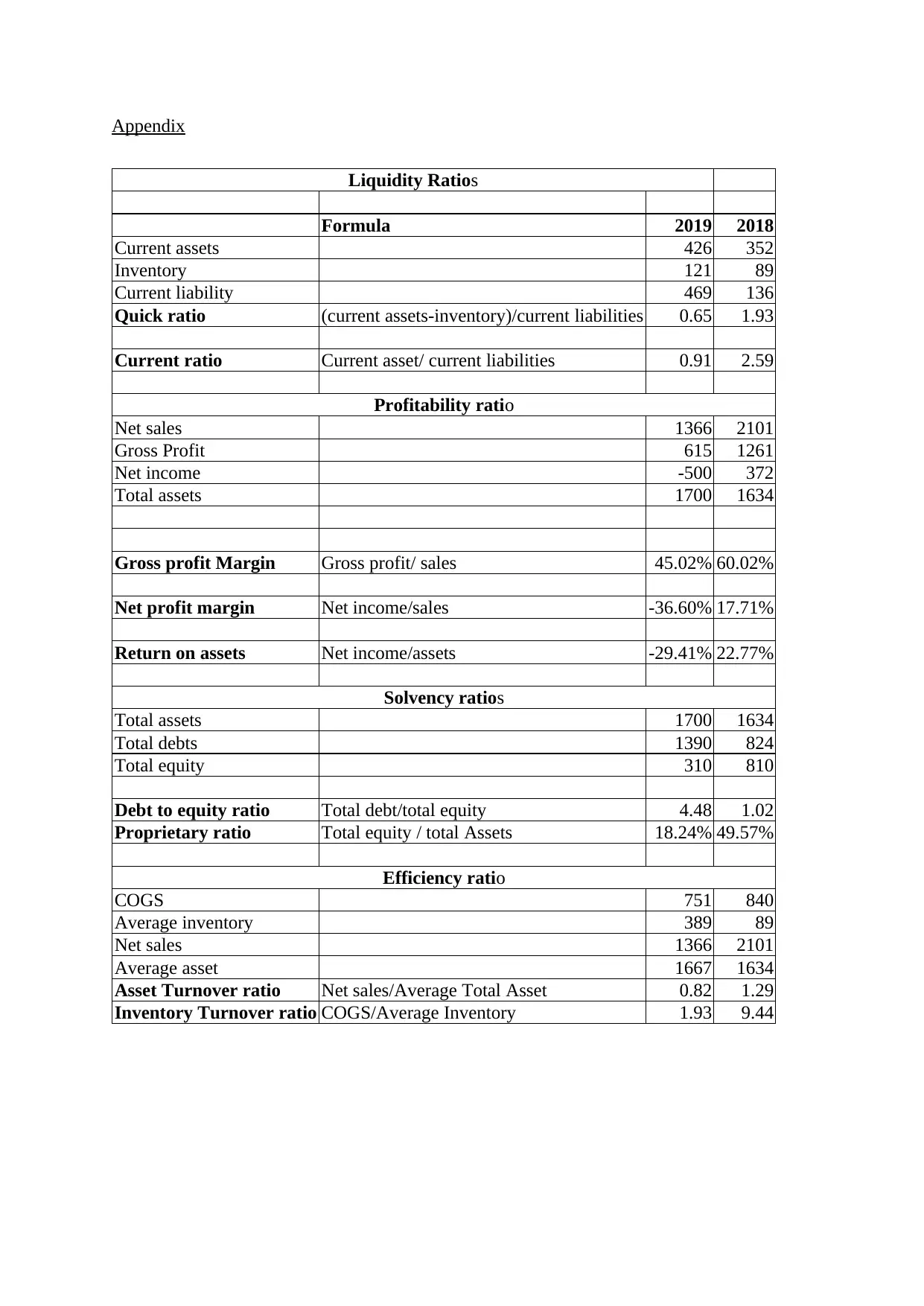

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

Gross profit Margin 45.02% 60.02%

Net profit margin -36.60% 17.71%

Return on assets -29.41% 22.77%

Current ratio:

By using the ratio analysis formula, it is interpreted that the ratio is decline to 0.91

times as compared to previous year i.e. 2.59 times. Therefore, it is reflected that liquidity

position of a company is not strong and as a result, company has a more long term liquidity.

As per the standard criteria, it is analysed that a good current ratio is lies 1.2 to 2 but the table

reflected that the ratio is less than 1.2 which is not good for the financial performance of a

business (Al-Hafiz, Mesran and Suginam, 2017). Therefore, the chances of acquire additional

fund for paying short term liability is increases. Thus, it is recommended to the firm make

actions in order to increase the current assets along with minimize current liabilities.

Quick Ratio:

Quick ratio of a company is decreases by 0.65 from 1.93 which clearly reflected that

T- shirt Ltd has invested its amount into its inventory which in turn affect the financial

performance of a company in opposite manner. On the other side, if the company’s quick

ratio increases then it is favourable for a business which in turn reduce the liability. Hence, it

is suggested to the quoted firm that to develop strategy in order to reduce the cash blocked

within its inventory which in turn help to meet its daily business expenses.

1.1 Statement of Profit or Loss

In order to determine the financial performance of a company it is necessary for the

business to use ratio analysis by using different ratios. Through this, T- Shirt Ltd will

examine the performance of a firm by comparing the ratios to previous year. Hence, different

ratios are as mention below:

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

Gross profit Margin 45.02% 60.02%

Net profit margin -36.60% 17.71%

Return on assets -29.41% 22.77%

Current ratio:

By using the ratio analysis formula, it is interpreted that the ratio is decline to 0.91

times as compared to previous year i.e. 2.59 times. Therefore, it is reflected that liquidity

position of a company is not strong and as a result, company has a more long term liquidity.

As per the standard criteria, it is analysed that a good current ratio is lies 1.2 to 2 but the table

reflected that the ratio is less than 1.2 which is not good for the financial performance of a

business (Al-Hafiz, Mesran and Suginam, 2017). Therefore, the chances of acquire additional

fund for paying short term liability is increases. Thus, it is recommended to the firm make

actions in order to increase the current assets along with minimize current liabilities.

Quick Ratio:

Quick ratio of a company is decreases by 0.65 from 1.93 which clearly reflected that

T- shirt Ltd has invested its amount into its inventory which in turn affect the financial

performance of a company in opposite manner. On the other side, if the company’s quick

ratio increases then it is favourable for a business which in turn reduce the liability. Hence, it

is suggested to the quoted firm that to develop strategy in order to reduce the cash blocked

within its inventory which in turn help to meet its daily business expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

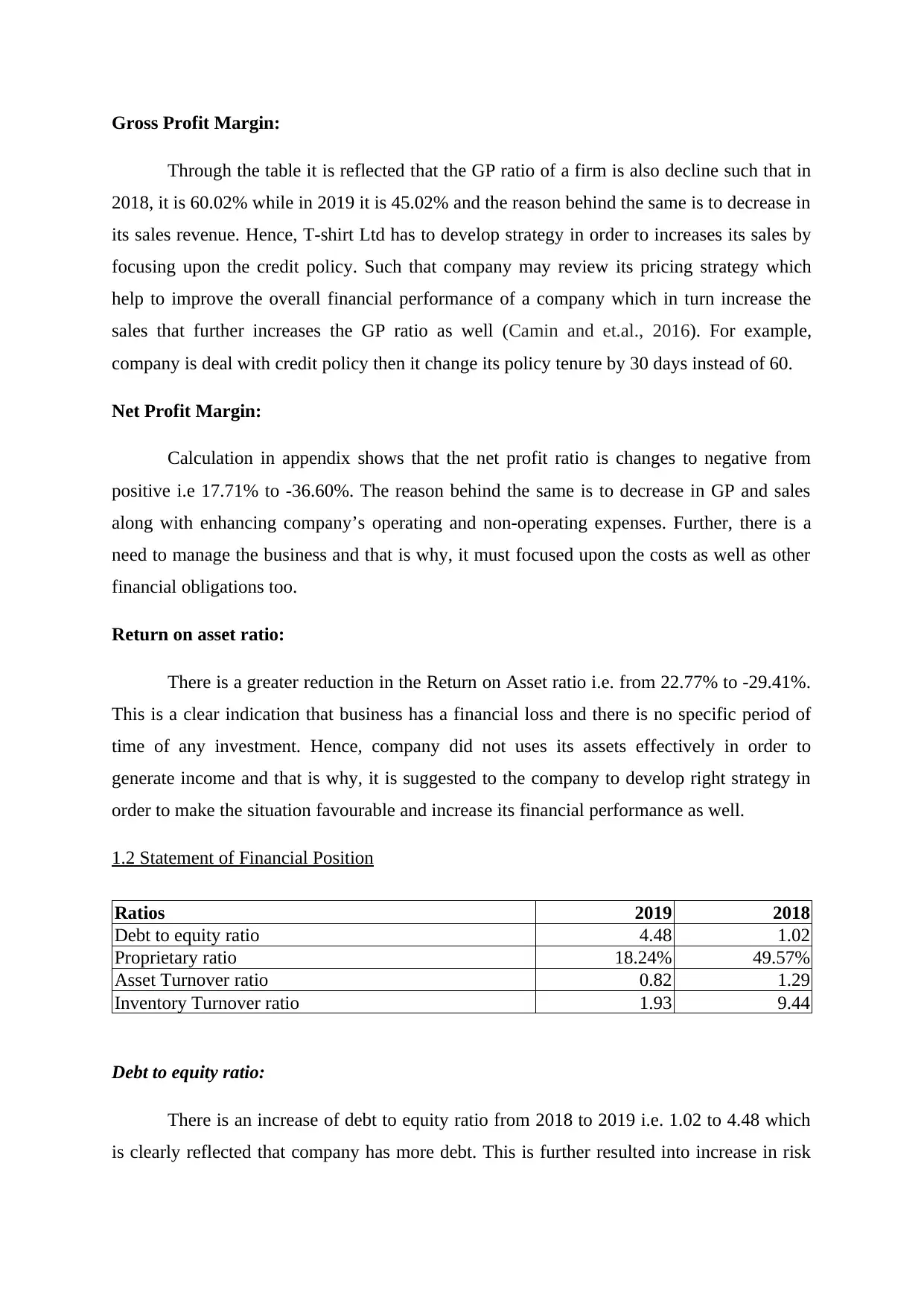

Gross Profit Margin:

Through the table it is reflected that the GP ratio of a firm is also decline such that in

2018, it is 60.02% while in 2019 it is 45.02% and the reason behind the same is to decrease in

its sales revenue. Hence, T-shirt Ltd has to develop strategy in order to increases its sales by

focusing upon the credit policy. Such that company may review its pricing strategy which

help to improve the overall financial performance of a company which in turn increase the

sales that further increases the GP ratio as well (Camin and et.al., 2016). For example,

company is deal with credit policy then it change its policy tenure by 30 days instead of 60.

Net Profit Margin:

Calculation in appendix shows that the net profit ratio is changes to negative from

positive i.e 17.71% to -36.60%. The reason behind the same is to decrease in GP and sales

along with enhancing company’s operating and non-operating expenses. Further, there is a

need to manage the business and that is why, it must focused upon the costs as well as other

financial obligations too.

Return on asset ratio:

There is a greater reduction in the Return on Asset ratio i.e. from 22.77% to -29.41%.

This is a clear indication that business has a financial loss and there is no specific period of

time of any investment. Hence, company did not uses its assets effectively in order to

generate income and that is why, it is suggested to the company to develop right strategy in

order to make the situation favourable and increase its financial performance as well.

1.2 Statement of Financial Position

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

Asset Turnover ratio 0.82 1.29

Inventory Turnover ratio 1.93 9.44

Debt to equity ratio:

There is an increase of debt to equity ratio from 2018 to 2019 i.e. 1.02 to 4.48 which

is clearly reflected that company has more debt. This is further resulted into increase in risk

Through the table it is reflected that the GP ratio of a firm is also decline such that in

2018, it is 60.02% while in 2019 it is 45.02% and the reason behind the same is to decrease in

its sales revenue. Hence, T-shirt Ltd has to develop strategy in order to increases its sales by

focusing upon the credit policy. Such that company may review its pricing strategy which

help to improve the overall financial performance of a company which in turn increase the

sales that further increases the GP ratio as well (Camin and et.al., 2016). For example,

company is deal with credit policy then it change its policy tenure by 30 days instead of 60.

Net Profit Margin:

Calculation in appendix shows that the net profit ratio is changes to negative from

positive i.e 17.71% to -36.60%. The reason behind the same is to decrease in GP and sales

along with enhancing company’s operating and non-operating expenses. Further, there is a

need to manage the business and that is why, it must focused upon the costs as well as other

financial obligations too.

Return on asset ratio:

There is a greater reduction in the Return on Asset ratio i.e. from 22.77% to -29.41%.

This is a clear indication that business has a financial loss and there is no specific period of

time of any investment. Hence, company did not uses its assets effectively in order to

generate income and that is why, it is suggested to the company to develop right strategy in

order to make the situation favourable and increase its financial performance as well.

1.2 Statement of Financial Position

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

Asset Turnover ratio 0.82 1.29

Inventory Turnover ratio 1.93 9.44

Debt to equity ratio:

There is an increase of debt to equity ratio from 2018 to 2019 i.e. 1.02 to 4.48 which

is clearly reflected that company has more debt. This is further resulted into increase in risk

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

factor that also increase the interest obligation along with timely payment of instalments.

Therefore, it is a sign of financing its growth with debt and that is why, it is suggested to the

company that by establishing the strategy in order to improve the business operations that

helps to minimize the error (Pasaribu and et.al., 2018).

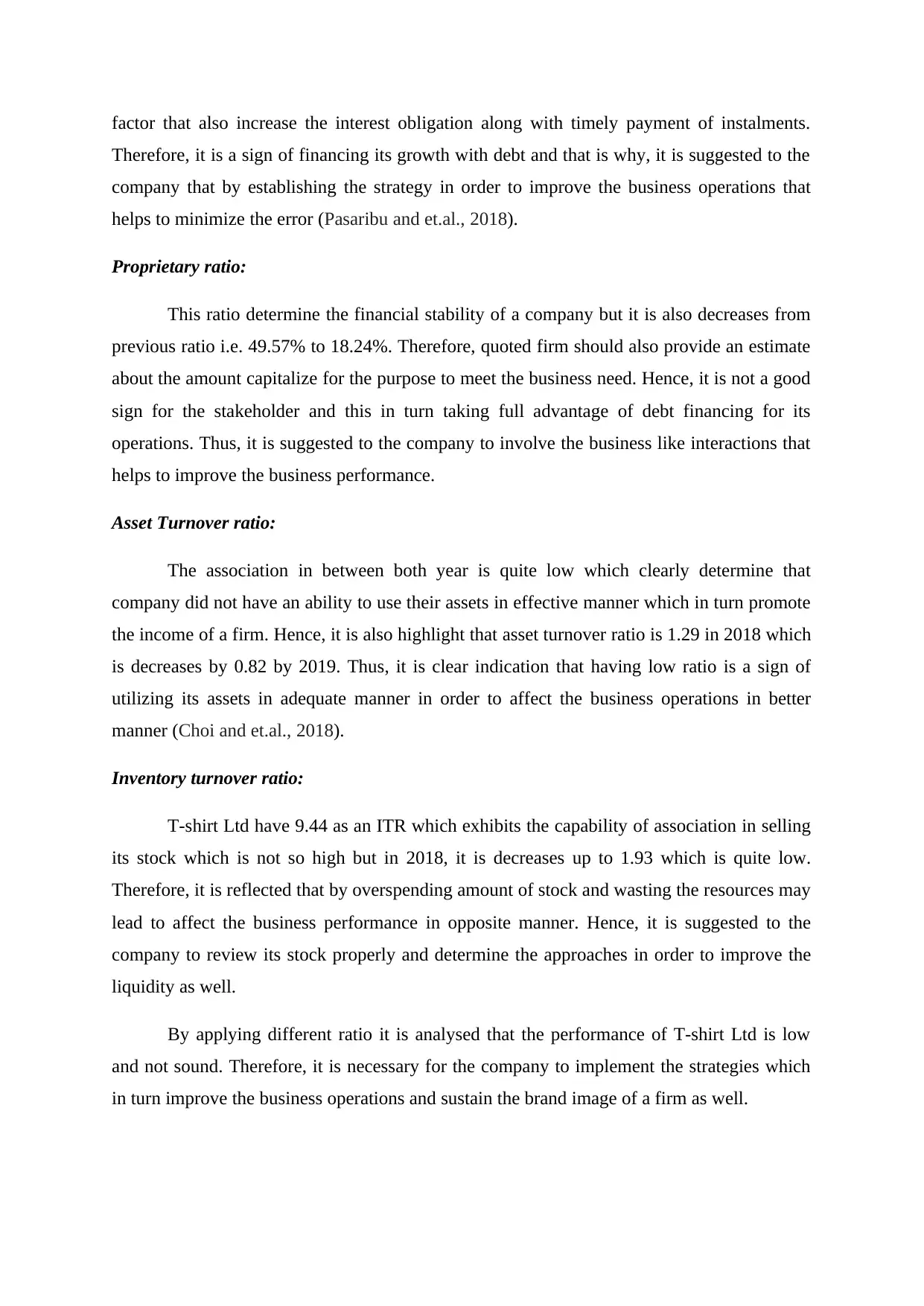

Proprietary ratio:

This ratio determine the financial stability of a company but it is also decreases from

previous ratio i.e. 49.57% to 18.24%. Therefore, quoted firm should also provide an estimate

about the amount capitalize for the purpose to meet the business need. Hence, it is not a good

sign for the stakeholder and this in turn taking full advantage of debt financing for its

operations. Thus, it is suggested to the company to involve the business like interactions that

helps to improve the business performance.

Asset Turnover ratio:

The association in between both year is quite low which clearly determine that

company did not have an ability to use their assets in effective manner which in turn promote

the income of a firm. Hence, it is also highlight that asset turnover ratio is 1.29 in 2018 which

is decreases by 0.82 by 2019. Thus, it is clear indication that having low ratio is a sign of

utilizing its assets in adequate manner in order to affect the business operations in better

manner (Choi and et.al., 2018).

Inventory turnover ratio:

T-shirt Ltd have 9.44 as an ITR which exhibits the capability of association in selling

its stock which is not so high but in 2018, it is decreases up to 1.93 which is quite low.

Therefore, it is reflected that by overspending amount of stock and wasting the resources may

lead to affect the business performance in opposite manner. Hence, it is suggested to the

company to review its stock properly and determine the approaches in order to improve the

liquidity as well.

By applying different ratio it is analysed that the performance of T-shirt Ltd is low

and not sound. Therefore, it is necessary for the company to implement the strategies which

in turn improve the business operations and sustain the brand image of a firm as well.

Therefore, it is a sign of financing its growth with debt and that is why, it is suggested to the

company that by establishing the strategy in order to improve the business operations that

helps to minimize the error (Pasaribu and et.al., 2018).

Proprietary ratio:

This ratio determine the financial stability of a company but it is also decreases from

previous ratio i.e. 49.57% to 18.24%. Therefore, quoted firm should also provide an estimate

about the amount capitalize for the purpose to meet the business need. Hence, it is not a good

sign for the stakeholder and this in turn taking full advantage of debt financing for its

operations. Thus, it is suggested to the company to involve the business like interactions that

helps to improve the business performance.

Asset Turnover ratio:

The association in between both year is quite low which clearly determine that

company did not have an ability to use their assets in effective manner which in turn promote

the income of a firm. Hence, it is also highlight that asset turnover ratio is 1.29 in 2018 which

is decreases by 0.82 by 2019. Thus, it is clear indication that having low ratio is a sign of

utilizing its assets in adequate manner in order to affect the business operations in better

manner (Choi and et.al., 2018).

Inventory turnover ratio:

T-shirt Ltd have 9.44 as an ITR which exhibits the capability of association in selling

its stock which is not so high but in 2018, it is decreases up to 1.93 which is quite low.

Therefore, it is reflected that by overspending amount of stock and wasting the resources may

lead to affect the business performance in opposite manner. Hence, it is suggested to the

company to review its stock properly and determine the approaches in order to improve the

liquidity as well.

By applying different ratio it is analysed that the performance of T-shirt Ltd is low

and not sound. Therefore, it is necessary for the company to implement the strategies which

in turn improve the business operations and sustain the brand image of a firm as well.

PART- 2

2.1 Concept of accrual accounting versus cash accounting with benefits as well as limitation

Accrual accounting is an fundamental principle of accounting that illustrated that company

needs to records all possible and existing loss while record revenue that are only earned

during the years. In another words it can be stated that entries or record are maintained in

books of accounts on the basis of transaction made rather than actual payment made or

received during particular year. Therefore, in order to understand the concept of accrual

accounting, first the meaning of word need to be understands “accrual” that means particular

transaction has occurred or accrual without any exchanged of payment or cash (Showalter,

2018). So, accrual concept of accounting is most suitable and fruitful for businesses that

have most of the transaction or sales on credit basis rather than on cash. In this concept it is

expected that money will be paid in future by customers so goods and services are delivered

to client on credit basis. On the other hand, in cash accounting concept, transaction are only

recorded when actual purchase of products and services has been made or expense are bear

by company. So, it include all relevant information related to the cash transaction rather than

credit as entry is only made when cash is received by the organisation (Semenova, 2018).

Therefore key difference between the both the term is that in accrual accounting entries are

made as products are sold or expense are made irrespective of cash received or paid while in

context of cash accounting, entries are specially made when actual cash in gained or paid by

company. For example: In the above case study, T-shirt Plc in order to attract more customers

range have extend its credit validity from 30 to 60 days. So, in this transaction has been made

30 or 60 days before but cash is paid to company afterwards so it is accrual transaction

concept. While if the company make entries at time customers make payment that is between

30 to 60 days that is known as cash accounting concept. Thus, Benefits and limitations of

both concept such as accrual accounting and cash accounting are discussed as follows:

Accrual accounting

Advantages

Shows accurate cash flow of business: There are huge numbers of business transaction in

particular month so it contributes in recording each transaction and transferring it to next

month or even longer.

2.1 Concept of accrual accounting versus cash accounting with benefits as well as limitation

Accrual accounting is an fundamental principle of accounting that illustrated that company

needs to records all possible and existing loss while record revenue that are only earned

during the years. In another words it can be stated that entries or record are maintained in

books of accounts on the basis of transaction made rather than actual payment made or

received during particular year. Therefore, in order to understand the concept of accrual

accounting, first the meaning of word need to be understands “accrual” that means particular

transaction has occurred or accrual without any exchanged of payment or cash (Showalter,

2018). So, accrual concept of accounting is most suitable and fruitful for businesses that

have most of the transaction or sales on credit basis rather than on cash. In this concept it is

expected that money will be paid in future by customers so goods and services are delivered

to client on credit basis. On the other hand, in cash accounting concept, transaction are only

recorded when actual purchase of products and services has been made or expense are bear

by company. So, it include all relevant information related to the cash transaction rather than

credit as entry is only made when cash is received by the organisation (Semenova, 2018).

Therefore key difference between the both the term is that in accrual accounting entries are

made as products are sold or expense are made irrespective of cash received or paid while in

context of cash accounting, entries are specially made when actual cash in gained or paid by

company. For example: In the above case study, T-shirt Plc in order to attract more customers

range have extend its credit validity from 30 to 60 days. So, in this transaction has been made

30 or 60 days before but cash is paid to company afterwards so it is accrual transaction

concept. While if the company make entries at time customers make payment that is between

30 to 60 days that is known as cash accounting concept. Thus, Benefits and limitations of

both concept such as accrual accounting and cash accounting are discussed as follows:

Accrual accounting

Advantages

Shows accurate cash flow of business: There are huge numbers of business transaction in

particular month so it contributes in recording each transaction and transferring it to next

month or even longer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Most of the investors prefer accrual accounting: Another advantage is that it is more

permanent and better method so investors prefer it most.

Limitation

Tax: Company needs to pay tax as it is record that income is earned but in reality no cash has

been received.

Cash accounting

Advantages

Single entry system: It is an easy process as involve single entry thus chance of errors and

mistake are minimised to large extend (Taskforce, 2018).

Limitation

Does not show the true picture: The biggest limitation of cash accounting system is that it

show limited looks at both expense and income of enterprise.

2.2 Profit and cash Flow and the way they are different

Profit and cash flow are two important financial metrics that have wide difference

between each others that need to be understood for effective decision making for good

financial health and business performance. Profit represents overall revenue earned by

company during particular year by selling products and services to end customers in best

possible manner. Or it state net income that company earned by subtracting total cost

incurred to manufacture products with that are sold to specific customers. While cash flow

represent in and out flow of money from different activities such as finance, operation and

investing (Heil, 2017). So, it is money or cash through which company is able to meet its

existing or future obligation by making their payments. Therefore, key difference between

cash flow and profit is that one indicates about the money which is left after meeting all

expenses related to sales of products and services. While the cash flow specific net cash flow

during particular years so that investors or other key stakeholders can take accurate and

correct decision to be part of firm or not in longer term.

permanent and better method so investors prefer it most.

Limitation

Tax: Company needs to pay tax as it is record that income is earned but in reality no cash has

been received.

Cash accounting

Advantages

Single entry system: It is an easy process as involve single entry thus chance of errors and

mistake are minimised to large extend (Taskforce, 2018).

Limitation

Does not show the true picture: The biggest limitation of cash accounting system is that it

show limited looks at both expense and income of enterprise.

2.2 Profit and cash Flow and the way they are different

Profit and cash flow are two important financial metrics that have wide difference

between each others that need to be understood for effective decision making for good

financial health and business performance. Profit represents overall revenue earned by

company during particular year by selling products and services to end customers in best

possible manner. Or it state net income that company earned by subtracting total cost

incurred to manufacture products with that are sold to specific customers. While cash flow

represent in and out flow of money from different activities such as finance, operation and

investing (Heil, 2017). So, it is money or cash through which company is able to meet its

existing or future obligation by making their payments. Therefore, key difference between

cash flow and profit is that one indicates about the money which is left after meeting all

expenses related to sales of products and services. While the cash flow specific net cash flow

during particular years so that investors or other key stakeholders can take accurate and

correct decision to be part of firm or not in longer term.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART-3

3.1 Define budget and purpose of preparing a budget

Budget refers to a specific amount decided to have revenue and expenses in a period of time.

This is the plan which can be estimated or framed for a person, groups, businesses,

institutions etc. which helps in spending the money. As planning is the first step which

everyone needs to perform and execute in appropriate manner to come over the positive

results in the work process. Purposes of preparing budget are as follows:

Increase savings: Budget plays a major role in savings of human life. As it is spend in a

planned manner in a particular period of time. Every budget set some saving as expenses and

revenues are being calculated and evaluated through experiences. This is done to increase the

saving and occur expenses in a desired manner.

Control over finance: It helps in controlling the feeling of spending Money on useless things

in the market. Budget has a control over the expenses which aren't necessary in the current

situations. As control over finance refers to check over the actual plan end planned plan. If

any diversion occurs then it needs to be rectified and work over the planned plan.

Achieving financial goals: Everyone starts budget with some financial goals keeping in mind

in order to achieve positive results in the work process (He, Jansen and Zarges, 2019).

Budget helps in achieving financial goals as it’s helped in controlling and monitoring over the

expenses and revenues occurred in day today time of life.

Debt free: Budget also helps in coming out from heavy debt which has been occurred during

a period of time. It helps in repayment of debt, rent, interests etc. through a specific financial

plan thus helped in attainment of end goals in limited time frame.

Reduce financial stress: It can be stated that preparation of budget in advance contributed in

reducing large amount of stress of business. It helps in resolving about issue related to

monthly expenses such as rent, wages to employees and fixed cost incurred in order to

delivered products and services to end customers. Therefore, budget in advance helps in

reducing all such financial stress and contributes in smooth achievements of company goals.

3.2 Main benefits of forming a limited company and listing it on stock exchange

Limited company is an type of organisation that has limited the amount of liability or its

shareholders, investors are limited liable to invested money so they cannot be forced to pay

3.1 Define budget and purpose of preparing a budget

Budget refers to a specific amount decided to have revenue and expenses in a period of time.

This is the plan which can be estimated or framed for a person, groups, businesses,

institutions etc. which helps in spending the money. As planning is the first step which

everyone needs to perform and execute in appropriate manner to come over the positive

results in the work process. Purposes of preparing budget are as follows:

Increase savings: Budget plays a major role in savings of human life. As it is spend in a

planned manner in a particular period of time. Every budget set some saving as expenses and

revenues are being calculated and evaluated through experiences. This is done to increase the

saving and occur expenses in a desired manner.

Control over finance: It helps in controlling the feeling of spending Money on useless things

in the market. Budget has a control over the expenses which aren't necessary in the current

situations. As control over finance refers to check over the actual plan end planned plan. If

any diversion occurs then it needs to be rectified and work over the planned plan.

Achieving financial goals: Everyone starts budget with some financial goals keeping in mind

in order to achieve positive results in the work process (He, Jansen and Zarges, 2019).

Budget helps in achieving financial goals as it’s helped in controlling and monitoring over the

expenses and revenues occurred in day today time of life.

Debt free: Budget also helps in coming out from heavy debt which has been occurred during

a period of time. It helps in repayment of debt, rent, interests etc. through a specific financial

plan thus helped in attainment of end goals in limited time frame.

Reduce financial stress: It can be stated that preparation of budget in advance contributed in

reducing large amount of stress of business. It helps in resolving about issue related to

monthly expenses such as rent, wages to employees and fixed cost incurred in order to

delivered products and services to end customers. Therefore, budget in advance helps in

reducing all such financial stress and contributes in smooth achievements of company goals.

3.2 Main benefits of forming a limited company and listing it on stock exchange

Limited company is an type of organisation that has limited the amount of liability or its

shareholders, investors are limited liable to invested money so they cannot be forced to pay

extra in case of more loss. Thus, their liability is limited to their stake in the organisation in

terms of total investment made thereby there are several benefits or advantages of forming

limited company which can be illustrated as follows:

Minimising personal liability: The greatest advantage of limited company is that personal is

not entitled to sells is personal asset or give money in order to pay liabilities or remaining

debt of organisation. It also stated that company is separate legal entity from individuals so it

has its personal rights on its assets thereby any type of losses is solely responsibility of

company rather than owner or stakeholders.

Professional status: Another benefit of limited company is that professional image and status

improved or enhanced as all function are effectively organised or well structured. All

operation are rigorously monitored and controlled so that no major loss can be caused in any

circumstances (Mancuso, 2019). At the same time there are more complex accounting

procedure, statutory compliance obligation and reporting requirements that need to be

fulfilled by company so that chance of loss can be minimised thus helps in attracting

investors.

Tax efficiency and planning: It can be stated that currently, company operating as Limited

liability in UK needs to pay 19% corporate tax on total profit earned as compared to other

sole trader that have to pay around 20-45%. Thus, Limited Liability Company also enjoys

flexibility of tax planning or saving as compared to other organisation.

There are numerous benefits of listing company in stock exchange

Access to capital for growth: Limited Company through listing on stock exchange can

easily increase number of shareholders base and its credibility in the external market.

Organisation always required capital or fund in order to further grow or diversify business

operation so listing contribute in effecting raising of funds.

Liquidity: Another benefits is that it give chance to shareholder to realise their value of

investment made and take active part in risk sharing or enjoying benefits of organisation.

Enhance visibility: It is also one of the major benefits of listing limited company on stock

exchanged as it helps in increasing visibility or awareness among maximum individuals.

Moreover it clearly show that company has complied to all legal regulators and norms thus it

is more transparent while performing its different function in order to attain end objectives.

terms of total investment made thereby there are several benefits or advantages of forming

limited company which can be illustrated as follows:

Minimising personal liability: The greatest advantage of limited company is that personal is

not entitled to sells is personal asset or give money in order to pay liabilities or remaining

debt of organisation. It also stated that company is separate legal entity from individuals so it

has its personal rights on its assets thereby any type of losses is solely responsibility of

company rather than owner or stakeholders.

Professional status: Another benefit of limited company is that professional image and status

improved or enhanced as all function are effectively organised or well structured. All

operation are rigorously monitored and controlled so that no major loss can be caused in any

circumstances (Mancuso, 2019). At the same time there are more complex accounting

procedure, statutory compliance obligation and reporting requirements that need to be

fulfilled by company so that chance of loss can be minimised thus helps in attracting

investors.

Tax efficiency and planning: It can be stated that currently, company operating as Limited

liability in UK needs to pay 19% corporate tax on total profit earned as compared to other

sole trader that have to pay around 20-45%. Thus, Limited Liability Company also enjoys

flexibility of tax planning or saving as compared to other organisation.

There are numerous benefits of listing company in stock exchange

Access to capital for growth: Limited Company through listing on stock exchange can

easily increase number of shareholders base and its credibility in the external market.

Organisation always required capital or fund in order to further grow or diversify business

operation so listing contribute in effecting raising of funds.

Liquidity: Another benefits is that it give chance to shareholder to realise their value of

investment made and take active part in risk sharing or enjoying benefits of organisation.

Enhance visibility: It is also one of the major benefits of listing limited company on stock

exchanged as it helps in increasing visibility or awareness among maximum individuals.

Moreover it clearly show that company has complied to all legal regulators and norms thus it

is more transparent while performing its different function in order to attain end objectives.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Chambost, I., Lenglet, M. and Tadjeddine, Y. eds., 2018. The Making of Finance:

Perspectives from the social sciences. Routledge.

Heil, M., 2017. Finance and productivity.

Mancuso, A., 2019. Your limited liability company: an operating manual. Nolo.

Semenova, S., 2018. Cash flow optimization and accounting in the enterprise. Social and

Legal Sciences, 1(2). pp.57-69.

Showalter, D. S., 2018. Increasing the Value of Accrual Accounting: Lessons from around

the World. The Journal of Government Financial Management, 67(3). p.56.

Taskforce, B. F., 2018. Better finance, better world. Consultation Paper.

Al-Hafiz, N.W., Mesran, M. and Suginam, S., 2017. Sistem Pendukung Keputusan

Penentukan Kredit Pemilikan Rumah Menerapkan Multi-Objective Optimization On

The Basis Of Ratio Analysis (Moora). KOMIK (Konferensi Nasional Teknologi

Informasi dan Komputer). 1(1).

Camin, F. and et.al., 2016. Stable isotope ratio analysis for assessing the authenticity of food

of animal origin. Comprehensive Reviews in Food Science and Food Safety. 15(5).

pp.868-877.

Pasaribu, S.W. and et.al., 2018. Implementasi Multi-Objective Optimization On The Basis Of

Ratio Analysis (MOORA) Untuk Menentukan Kualitas Buah Mangga

Terbaik. JURIKOM (Jurnal Riset Komputer). 5(1). pp.50-55.

Choi, K.B. and et.al., 2018. Amplification ratio analysis of a bridge-type mechanical

amplification mechanism based on a fully compliant model. Mechanism and Machine

Theory. 121. pp.355-372.

He, J., Jansen, T. and Zarges, C., 2019, July. Unlimited budget analysis. In Proceedings of the

Genetic and Evolutionary Computation Conference Companion (pp. 427-428).

Books and Journals

Chambost, I., Lenglet, M. and Tadjeddine, Y. eds., 2018. The Making of Finance:

Perspectives from the social sciences. Routledge.

Heil, M., 2017. Finance and productivity.

Mancuso, A., 2019. Your limited liability company: an operating manual. Nolo.

Semenova, S., 2018. Cash flow optimization and accounting in the enterprise. Social and

Legal Sciences, 1(2). pp.57-69.

Showalter, D. S., 2018. Increasing the Value of Accrual Accounting: Lessons from around

the World. The Journal of Government Financial Management, 67(3). p.56.

Taskforce, B. F., 2018. Better finance, better world. Consultation Paper.

Al-Hafiz, N.W., Mesran, M. and Suginam, S., 2017. Sistem Pendukung Keputusan

Penentukan Kredit Pemilikan Rumah Menerapkan Multi-Objective Optimization On

The Basis Of Ratio Analysis (Moora). KOMIK (Konferensi Nasional Teknologi

Informasi dan Komputer). 1(1).

Camin, F. and et.al., 2016. Stable isotope ratio analysis for assessing the authenticity of food

of animal origin. Comprehensive Reviews in Food Science and Food Safety. 15(5).

pp.868-877.

Pasaribu, S.W. and et.al., 2018. Implementasi Multi-Objective Optimization On The Basis Of

Ratio Analysis (MOORA) Untuk Menentukan Kualitas Buah Mangga

Terbaik. JURIKOM (Jurnal Riset Komputer). 5(1). pp.50-55.

Choi, K.B. and et.al., 2018. Amplification ratio analysis of a bridge-type mechanical

amplification mechanism based on a fully compliant model. Mechanism and Machine

Theory. 121. pp.355-372.

He, J., Jansen, T. and Zarges, C., 2019, July. Unlimited budget analysis. In Proceedings of the

Genetic and Evolutionary Computation Conference Companion (pp. 427-428).

Appendix

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Return on assets Net income/assets -29.41% 22.77%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

Debt to equity ratio Total debt/total equity 4.48 1.02

Proprietary ratio Total equity / total Assets 18.24% 49.57%

Efficiency ratio

COGS 751 840

Average inventory 389 89

Net sales 1366 2101

Average asset 1667 1634

Asset Turnover ratio Net sales/Average Total Asset 0.82 1.29

Inventory Turnover ratio COGS/Average Inventory 1.93 9.44

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Return on assets Net income/assets -29.41% 22.77%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

Debt to equity ratio Total debt/total equity 4.48 1.02

Proprietary ratio Total equity / total Assets 18.24% 49.57%

Efficiency ratio

COGS 751 840

Average inventory 389 89

Net sales 1366 2101

Average asset 1667 1634

Asset Turnover ratio Net sales/Average Total Asset 0.82 1.29

Inventory Turnover ratio COGS/Average Inventory 1.93 9.44

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.