Business Finance: Differences Between Accounting Types Explained

VerifiedAdded on 2023/01/12

|7

|1246

|48

Report

AI Summary

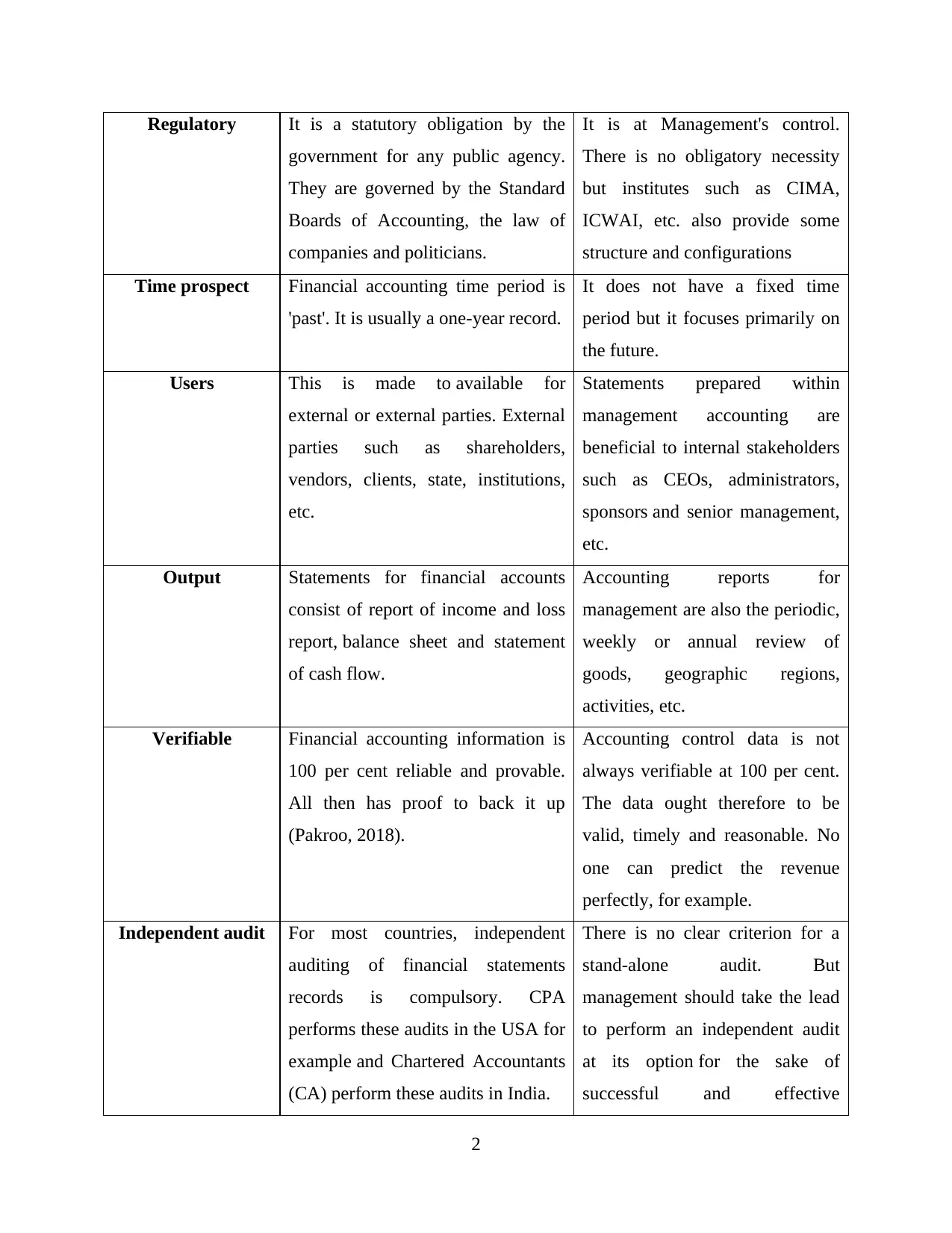

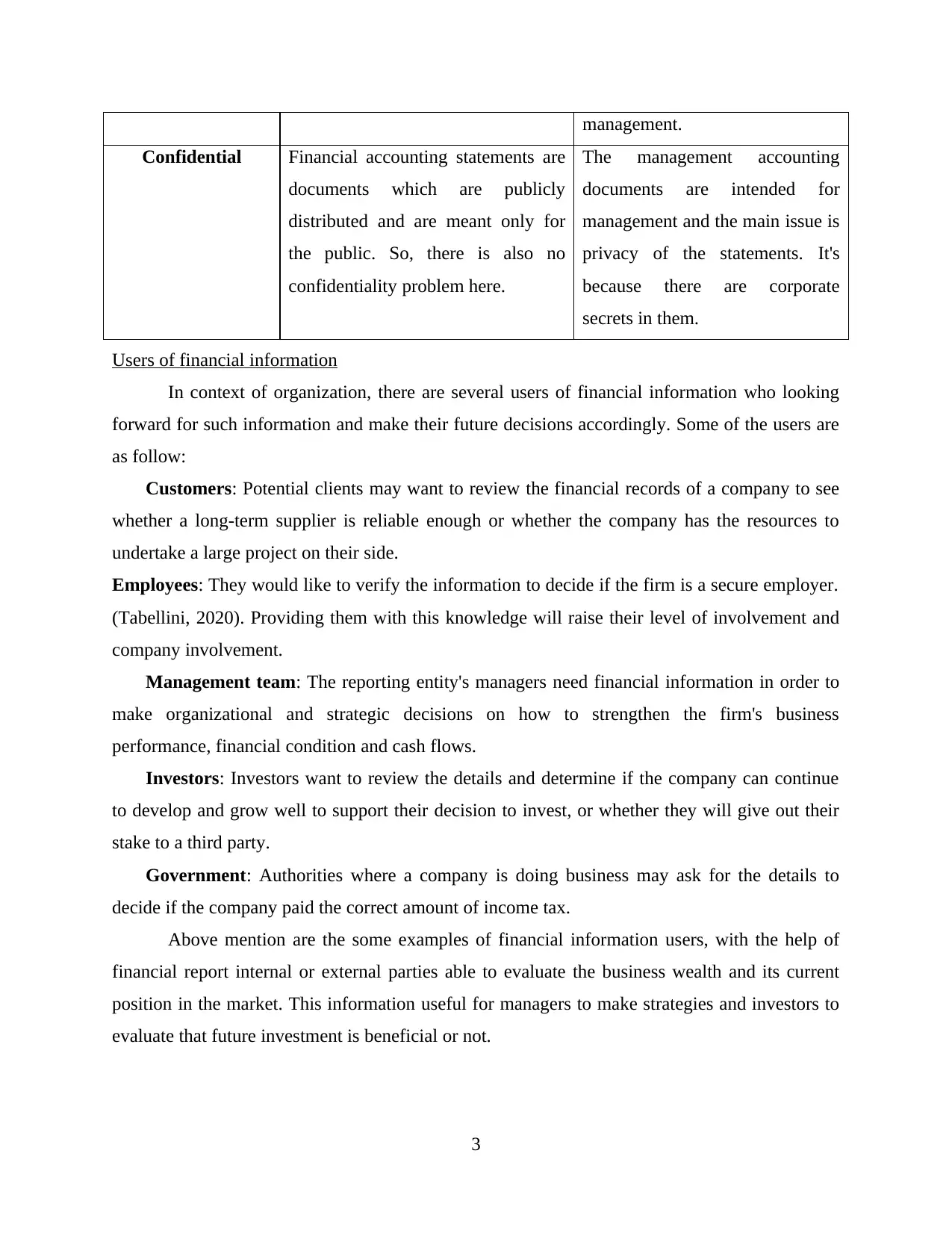

This report provides an overview of business finance, emphasizing the crucial role of finance in corporate operations. It delves into the core differences between financial accounting, which focuses on external stakeholders and regulatory compliance, and management accounting, which supports internal decision-making, performance evaluation, and strategic planning. The report highlights key distinctions such as the target audience, regulatory requirements, time perspective, and the nature of the information provided. Furthermore, it identifies various users of financial information, including customers, employees, management teams, investors, and government entities, illustrating how each group utilizes financial data to make informed decisions. The report concludes by underscoring the importance of both financial and management accounting in enabling organizations to assess performance, make strategic choices, and fulfill their operational needs. The references include books and journals that support the findings of the report.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.