Business Finance Report: Cash Budgeting and Working Capital Management

VerifiedAdded on 2022/12/27

|12

|3357

|99

Report

AI Summary

This report delves into key aspects of business finance, beginning with an executive summary that defines business finance and its importance. Part A explores the concepts of profit and cash flow, differentiating between them, and explaining the components of working capital, trade receivables, payables, and inventory. It also examines how changes in working capital affect cash flow and how company management can influence financial results, including profit, cash flow, payables, and working capital. Recommendations for effective working capital management are provided. Part B focuses on preparing a monthly cash budget for four months for Thorne Estates Limited and offers observations and recommendations for the company's cash management. The report includes a detailed cash budget table and working notes, with the goal of improving financial decision-making and overall financial health.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

PART A...........................................................................................................................................1

1) A) Meaning of profit and cash flow and description of their difference................................1

B) Explanation of working capital, receivables, payables and inventory...................................2

C) Explanation of changes in working capital effect cash flow..................................................3

2) Company is being managed might affect its financial results................................................3

3) Recommendation related to effective working capital management......................................4

EXECUTIVE SUMMARY.............................................................................................................5

PART B............................................................................................................................................5

1. Prepare a monthly cash budget for four months.....................................................................5

2. Any observations or recommendations that you would make to the management of Thorne

Estates.........................................................................................................................................7

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................1

PART A...........................................................................................................................................1

1) A) Meaning of profit and cash flow and description of their difference................................1

B) Explanation of working capital, receivables, payables and inventory...................................2

C) Explanation of changes in working capital effect cash flow..................................................3

2) Company is being managed might affect its financial results................................................3

3) Recommendation related to effective working capital management......................................4

EXECUTIVE SUMMARY.............................................................................................................5

PART B............................................................................................................................................5

1. Prepare a monthly cash budget for four months.....................................................................5

2. Any observations or recommendations that you would make to the management of Thorne

Estates.........................................................................................................................................7

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY

Business Finance defined as external monetary assistance utilize whenever an

organization runs short of capital. The funds enable individual to manage routine operational

activities, expand market reach, obtain raw material, invest in infrastructure and many similar

necessities (Beekes and et.al., 2016). It provide funds for business working capital requirement,

capital requirement and also provide diversification of funds. In this report covers meaning of

profit and cash flow their difference, changes in working capital, meanings of receivables,

inventory and payables. Moreover, provide suggestions for the improvement of cash flow for

better working capital.

PART A

1) A) Meaning of profit and cash flow and description of their difference

Profit: The term of profit defined as financial benefit that realised when revenue

generated from business activity exceeds the expenditure, costs and taxes consist of in sustaining

the activity in question. It is mainly used by the business to present business activity and reward

to business owners for investing. In the other words, when incomes are greater than expenditure

so it is known as profit and it is essential part of any business that presents growth and strong

performance.

Cash flow: It is net amount of cash that an entity acquire and pay out in certain period of

time. A positive cash flow presents good management of cash and maintain liquidity in business

and a negative cash flow indicates higher cash out flow. Cash flow mainly represents the money

coming and going out of an entity in particular period time. It is providing relevant cash flow to

analysis the quality of income (Boschmans and Pissareva, 2018).

Difference between profit and cash flow

Particular Profit Cash flow

Meaning It is a overall amount in which

producers generate after deducting

the production costs.

It is defined as net amount of cash

and cash equivalents being

transferred into as well as out of

business.

Time For the calculation of profit not This statement is developed by the

1

Business Finance defined as external monetary assistance utilize whenever an

organization runs short of capital. The funds enable individual to manage routine operational

activities, expand market reach, obtain raw material, invest in infrastructure and many similar

necessities (Beekes and et.al., 2016). It provide funds for business working capital requirement,

capital requirement and also provide diversification of funds. In this report covers meaning of

profit and cash flow their difference, changes in working capital, meanings of receivables,

inventory and payables. Moreover, provide suggestions for the improvement of cash flow for

better working capital.

PART A

1) A) Meaning of profit and cash flow and description of their difference

Profit: The term of profit defined as financial benefit that realised when revenue

generated from business activity exceeds the expenditure, costs and taxes consist of in sustaining

the activity in question. It is mainly used by the business to present business activity and reward

to business owners for investing. In the other words, when incomes are greater than expenditure

so it is known as profit and it is essential part of any business that presents growth and strong

performance.

Cash flow: It is net amount of cash that an entity acquire and pay out in certain period of

time. A positive cash flow presents good management of cash and maintain liquidity in business

and a negative cash flow indicates higher cash out flow. Cash flow mainly represents the money

coming and going out of an entity in particular period time. It is providing relevant cash flow to

analysis the quality of income (Boschmans and Pissareva, 2018).

Difference between profit and cash flow

Particular Profit Cash flow

Meaning It is a overall amount in which

producers generate after deducting

the production costs.

It is defined as net amount of cash

and cash equivalents being

transferred into as well as out of

business.

Time For the calculation of profit not This statement is developed by the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

required particular time period. It

is calculating by the organisation

on monthly, weekly and yearly

basis.

business at the end of fiscal year that

present actual situation of cash flow

in business.

Calculation It is calculating by various

methods by using managerial and

accounting techniques. Along

with it is calculated by profit and

loss statement in which mention

all the income and expenses

(Cowling, Liu and Zhang, 2016).

It is calculated by record each item

in cash flow statement and

categorised different activities into

different functions like operation,

financial and investment. By this

statement manager recognise net

cash flow activity.

Purpose The main purpose of profit to

maintain sustainability in business

entity and present financial health

effectively.

The main reason to identify actual

financial performance of an entity

that supports to generate cash

appropriately.

B) Explanation of working capital, receivables, payables and inventory

Working Capital: It is the amount invested in short term asset of an entity that is

represented by stocks, short term receivables and cash balances in which deduct short term

liabilities. It is defined as differences of current assets and current liabilities. In current assets

consist of cash, stock of raw material, accounts receivables and in current liabilities, bills

payable, bank and many others. Working capital is a measurement tool which is utilised to

present liquidity of business and presents the differences between operating current assets and

current liabilities.

Trade receivables: These are amounts billed by a business its customers when its

delivers goods and services them in ordinary course of business. This is commonly used by

collections staff to collect overdue payment from customers. For an invoice to be added trade

receivables, full payment must be expected within one year. It is total amount owing by company

for goods or services it has sold, which are reflected in invoices that company has issued its

clients, but has not yet received payment (Heil, 2017).

2

is calculating by the organisation

on monthly, weekly and yearly

basis.

business at the end of fiscal year that

present actual situation of cash flow

in business.

Calculation It is calculating by various

methods by using managerial and

accounting techniques. Along

with it is calculated by profit and

loss statement in which mention

all the income and expenses

(Cowling, Liu and Zhang, 2016).

It is calculated by record each item

in cash flow statement and

categorised different activities into

different functions like operation,

financial and investment. By this

statement manager recognise net

cash flow activity.

Purpose The main purpose of profit to

maintain sustainability in business

entity and present financial health

effectively.

The main reason to identify actual

financial performance of an entity

that supports to generate cash

appropriately.

B) Explanation of working capital, receivables, payables and inventory

Working Capital: It is the amount invested in short term asset of an entity that is

represented by stocks, short term receivables and cash balances in which deduct short term

liabilities. It is defined as differences of current assets and current liabilities. In current assets

consist of cash, stock of raw material, accounts receivables and in current liabilities, bills

payable, bank and many others. Working capital is a measurement tool which is utilised to

present liquidity of business and presents the differences between operating current assets and

current liabilities.

Trade receivables: These are amounts billed by a business its customers when its

delivers goods and services them in ordinary course of business. This is commonly used by

collections staff to collect overdue payment from customers. For an invoice to be added trade

receivables, full payment must be expected within one year. It is total amount owing by company

for goods or services it has sold, which are reflected in invoices that company has issued its

clients, but has not yet received payment (Heil, 2017).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory: Inventory is a term for goods available for sale and raw materials used

produce goods available for sale. It represents one of the primary sources of revenue generation

and subsequent earnings for company shareholders. It is an accounting term that refers goods

that are in various stages of being made ready for sale, including finished goods, raw material

and work in progress.

Trade payable: It is an obligations, to pay for goods or services that have been acquired

from suppliers in a ordinary course of business. These billed amounts, if paid on credit, are

entered in the account payable module of a company's accounting software, after which they

appear in a accounts payable aging report until they are paid.

C) Explanation of changes in working capital effect cash flow

Working capital represents the difference between a firms's current assets and current

liability. Working capital, also called net working capital, it the amount of money a company has

available to pay its short term expenses. Positive working capital is when a company has more

current assets than current liabiltity, then it means it has a positive impact on the cash flow

statements. When negative working capital is there then current liability is more than current

assets then it means it has a negative impact on the cash flow statements (Kennickell, Kwast and

Pogach, 2016). For ex. If a company purchased a fixed asset such as building, the company cash

flow would decreases and when the company selling the fixed assets then the there is a boost in

the cash flow statements.

2) Company is being managed might affect its financial results

Trends Ltd is manufacturing company that product different types of gym cloth and

footwear. Moreover it design for various organisation under their own brands. The overall

turnover of the business is excess of 300 Pound dollar. There are mentioning various changes in

financial results that can be managed by the business such as:

Profit: Trend Ltd has been generated profitability of 60 Million Pound last year that

render the effective situation of an entity. On the basis of profit company liabile for the

tax liability and interest payable on borrowings accountable that supports the business

entity to achieve better profit in future.

Cash flow: An organisation can produce their cash flow on basis of the new policies and

regulations like providing discount price to its clients and utilising efficient bill paying.

3

produce goods available for sale. It represents one of the primary sources of revenue generation

and subsequent earnings for company shareholders. It is an accounting term that refers goods

that are in various stages of being made ready for sale, including finished goods, raw material

and work in progress.

Trade payable: It is an obligations, to pay for goods or services that have been acquired

from suppliers in a ordinary course of business. These billed amounts, if paid on credit, are

entered in the account payable module of a company's accounting software, after which they

appear in a accounts payable aging report until they are paid.

C) Explanation of changes in working capital effect cash flow

Working capital represents the difference between a firms's current assets and current

liability. Working capital, also called net working capital, it the amount of money a company has

available to pay its short term expenses. Positive working capital is when a company has more

current assets than current liabiltity, then it means it has a positive impact on the cash flow

statements. When negative working capital is there then current liability is more than current

assets then it means it has a negative impact on the cash flow statements (Kennickell, Kwast and

Pogach, 2016). For ex. If a company purchased a fixed asset such as building, the company cash

flow would decreases and when the company selling the fixed assets then the there is a boost in

the cash flow statements.

2) Company is being managed might affect its financial results

Trends Ltd is manufacturing company that product different types of gym cloth and

footwear. Moreover it design for various organisation under their own brands. The overall

turnover of the business is excess of 300 Pound dollar. There are mentioning various changes in

financial results that can be managed by the business such as:

Profit: Trend Ltd has been generated profitability of 60 Million Pound last year that

render the effective situation of an entity. On the basis of profit company liabile for the

tax liability and interest payable on borrowings accountable that supports the business

entity to achieve better profit in future.

Cash flow: An organisation can produce their cash flow on basis of the new policies and

regulations like providing discount price to its clients and utilising efficient bill paying.

3

An organisation clear out its debts quickly and manage the better cash flow activities to

present actual flow of cash in front of adminstration (Ketterer, 2017).

Payable: An entity require to enahnce the value of current assets that consist of

expenditure of current liabilities and required to pay obligation on time. There are

analysed the position of company that time identified that debt of business enahnce by 95

million Pounds from 60 Million Pounds year before that presents organisation is more

accountable to pay its debt on time.

Working capital: The working capital of company present changes in current assets as

well as current liabilities. These changes direct impact on the profitability and reduce

potential clients and less supply in raw material to its suppliers. The working cpaitla

managed by the Trend Ltd effectively and deliver products on time and payment to their

supplier on time that help in manage working capital (Kraemer-Eis and et.al., 2019).

3) Recommendation related to effective working capital management

Working capital management is effective tool which is mainly utilised by business to

present use of current assets and liabilities in proper manner. It is supporting organizations to

manage cash position in proper manner and meet with business objectives. For the cash flow

statement required to use this method for the analysis of cash activities. Trend Ltd can use

particular way to maintained cash flow are:

Predicting of cash flow: It is good method that helps in estimation of cash flows like

receiables as well as payables when an organization will faciliates in effective decision making

in the context of the investment and other activities.

Analysis of accounts receivable: It is useful act in which an organisation analysis all

accounts receiables properly and assure about the clients pay due payments on time. This

necessary to change the credit policies that will enahnce the early payment as well as effectively

analysis the financial health of business. Along with it will increase the cash flows of business

entity for proper management of cash position effectively.

Review of supply and stocks: It is recommended that analysis of the supply as well as

stock of the business to enahnce cash flow in proper way that enahnce the effectiveness of entity.

As a result it will assure about the Trend Ltd is effectively supply stock on time that he;ping to

manage working capital properly.

4

present actual flow of cash in front of adminstration (Ketterer, 2017).

Payable: An entity require to enahnce the value of current assets that consist of

expenditure of current liabilities and required to pay obligation on time. There are

analysed the position of company that time identified that debt of business enahnce by 95

million Pounds from 60 Million Pounds year before that presents organisation is more

accountable to pay its debt on time.

Working capital: The working capital of company present changes in current assets as

well as current liabilities. These changes direct impact on the profitability and reduce

potential clients and less supply in raw material to its suppliers. The working cpaitla

managed by the Trend Ltd effectively and deliver products on time and payment to their

supplier on time that help in manage working capital (Kraemer-Eis and et.al., 2019).

3) Recommendation related to effective working capital management

Working capital management is effective tool which is mainly utilised by business to

present use of current assets and liabilities in proper manner. It is supporting organizations to

manage cash position in proper manner and meet with business objectives. For the cash flow

statement required to use this method for the analysis of cash activities. Trend Ltd can use

particular way to maintained cash flow are:

Predicting of cash flow: It is good method that helps in estimation of cash flows like

receiables as well as payables when an organization will faciliates in effective decision making

in the context of the investment and other activities.

Analysis of accounts receivable: It is useful act in which an organisation analysis all

accounts receiables properly and assure about the clients pay due payments on time. This

necessary to change the credit policies that will enahnce the early payment as well as effectively

analysis the financial health of business. Along with it will increase the cash flows of business

entity for proper management of cash position effectively.

Review of supply and stocks: It is recommended that analysis of the supply as well as

stock of the business to enahnce cash flow in proper way that enahnce the effectiveness of entity.

As a result it will assure about the Trend Ltd is effectively supply stock on time that he;ping to

manage working capital properly.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

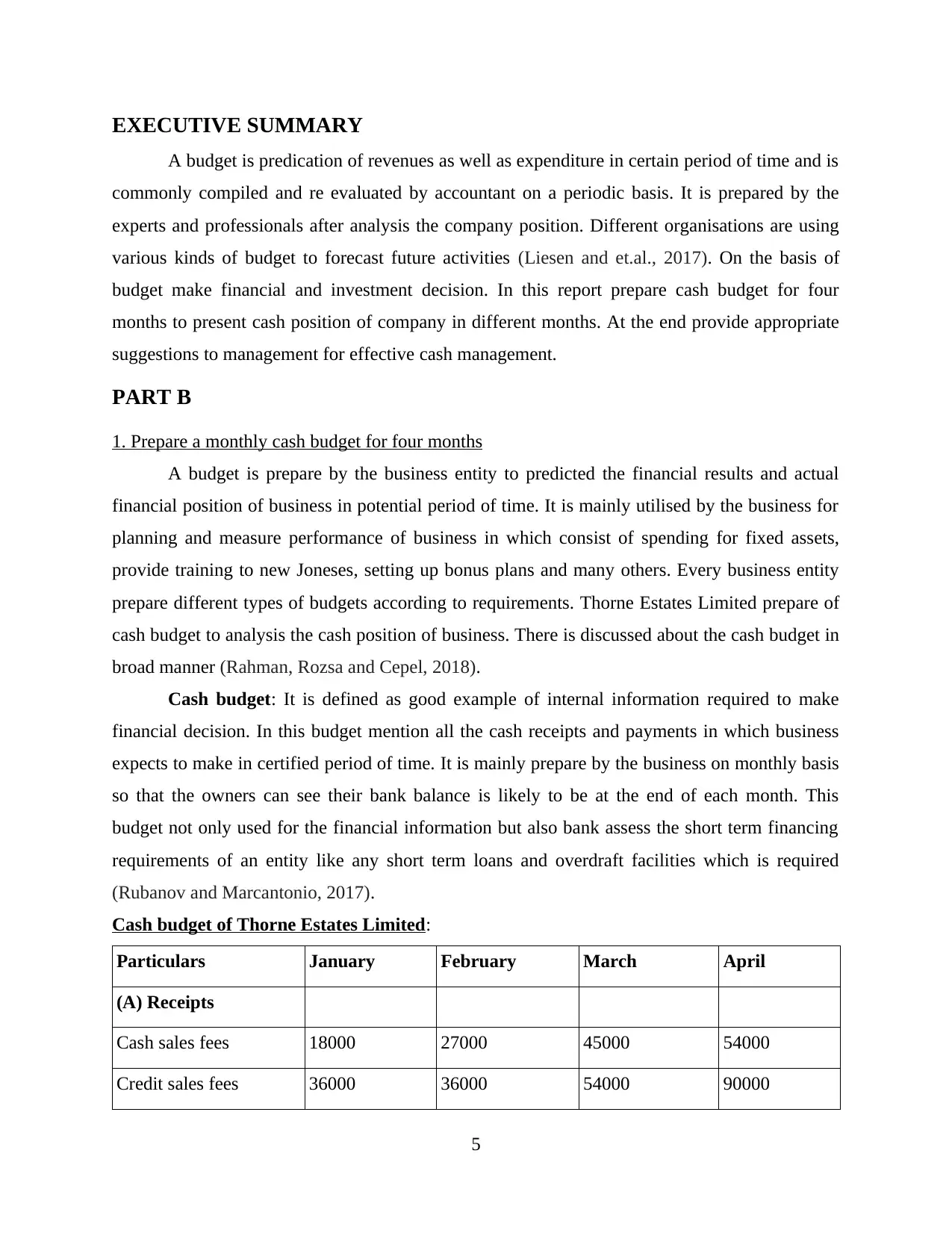

EXECUTIVE SUMMARY

A budget is predication of revenues as well as expenditure in certain period of time and is

commonly compiled and re evaluated by accountant on a periodic basis. It is prepared by the

experts and professionals after analysis the company position. Different organisations are using

various kinds of budget to forecast future activities (Liesen and et.al., 2017). On the basis of

budget make financial and investment decision. In this report prepare cash budget for four

months to present cash position of company in different months. At the end provide appropriate

suggestions to management for effective cash management.

PART B

1. Prepare a monthly cash budget for four months

A budget is prepare by the business entity to predicted the financial results and actual

financial position of business in potential period of time. It is mainly utilised by the business for

planning and measure performance of business in which consist of spending for fixed assets,

provide training to new Joneses, setting up bonus plans and many others. Every business entity

prepare different types of budgets according to requirements. Thorne Estates Limited prepare of

cash budget to analysis the cash position of business. There is discussed about the cash budget in

broad manner (Rahman, Rozsa and Cepel, 2018).

Cash budget: It is defined as good example of internal information required to make

financial decision. In this budget mention all the cash receipts and payments in which business

expects to make in certified period of time. It is mainly prepare by the business on monthly basis

so that the owners can see their bank balance is likely to be at the end of each month. This

budget not only used for the financial information but also bank assess the short term financing

requirements of an entity like any short term loans and overdraft facilities which is required

(Rubanov and Marcantonio, 2017).

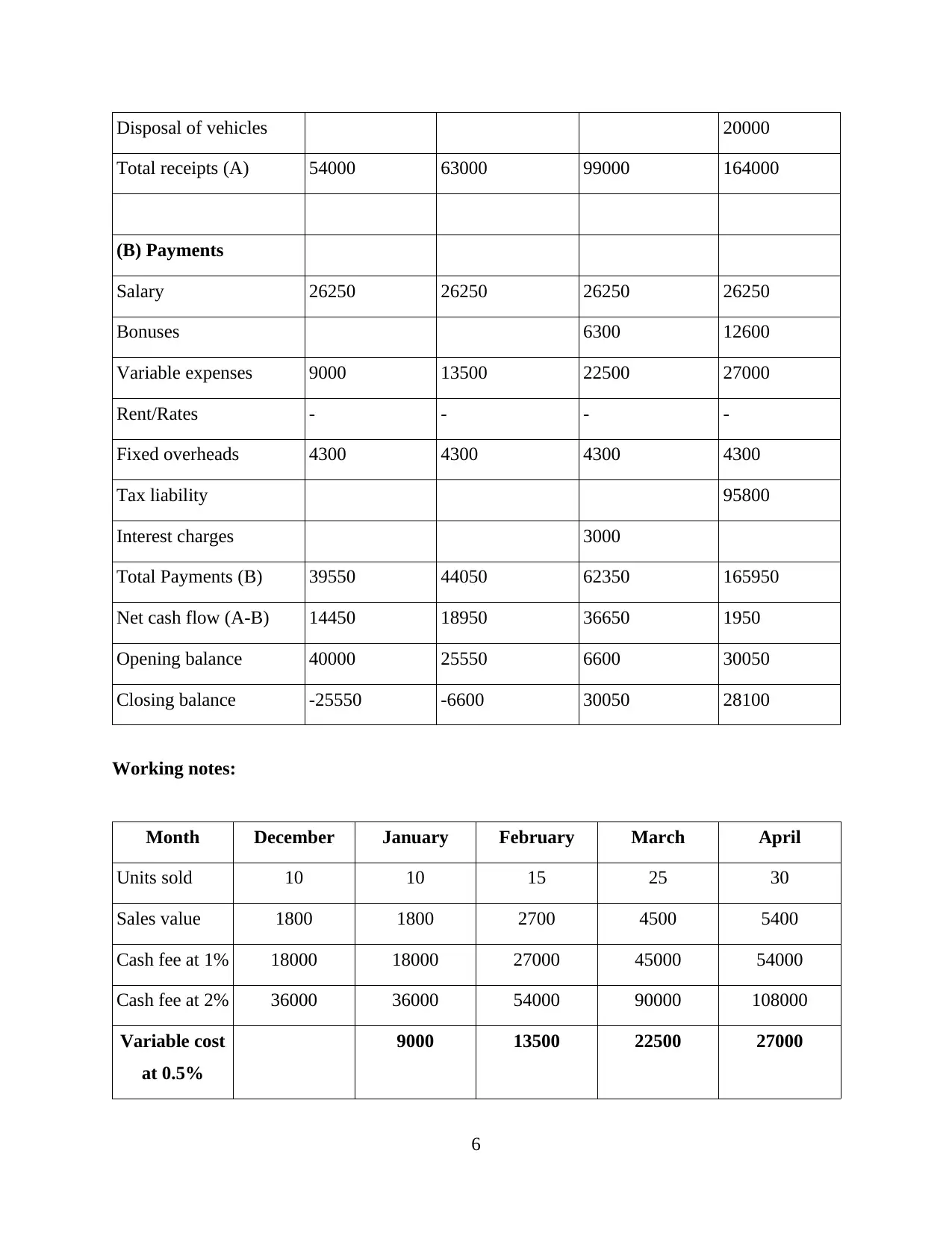

Cash budget of Thorne Estates Limited:

Particulars January February March April

(A) Receipts

Cash sales fees 18000 27000 45000 54000

Credit sales fees 36000 36000 54000 90000

5

A budget is predication of revenues as well as expenditure in certain period of time and is

commonly compiled and re evaluated by accountant on a periodic basis. It is prepared by the

experts and professionals after analysis the company position. Different organisations are using

various kinds of budget to forecast future activities (Liesen and et.al., 2017). On the basis of

budget make financial and investment decision. In this report prepare cash budget for four

months to present cash position of company in different months. At the end provide appropriate

suggestions to management for effective cash management.

PART B

1. Prepare a monthly cash budget for four months

A budget is prepare by the business entity to predicted the financial results and actual

financial position of business in potential period of time. It is mainly utilised by the business for

planning and measure performance of business in which consist of spending for fixed assets,

provide training to new Joneses, setting up bonus plans and many others. Every business entity

prepare different types of budgets according to requirements. Thorne Estates Limited prepare of

cash budget to analysis the cash position of business. There is discussed about the cash budget in

broad manner (Rahman, Rozsa and Cepel, 2018).

Cash budget: It is defined as good example of internal information required to make

financial decision. In this budget mention all the cash receipts and payments in which business

expects to make in certified period of time. It is mainly prepare by the business on monthly basis

so that the owners can see their bank balance is likely to be at the end of each month. This

budget not only used for the financial information but also bank assess the short term financing

requirements of an entity like any short term loans and overdraft facilities which is required

(Rubanov and Marcantonio, 2017).

Cash budget of Thorne Estates Limited:

Particulars January February March April

(A) Receipts

Cash sales fees 18000 27000 45000 54000

Credit sales fees 36000 36000 54000 90000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disposal of vehicles 20000

Total receipts (A) 54000 63000 99000 164000

(B) Payments

Salary 26250 26250 26250 26250

Bonuses 6300 12600

Variable expenses 9000 13500 22500 27000

Rent/Rates - - - -

Fixed overheads 4300 4300 4300 4300

Tax liability 95800

Interest charges 3000

Total Payments (B) 39550 44050 62350 165950

Net cash flow (A-B) 14450 18950 36650 1950

Opening balance 40000 25550 6600 30050

Closing balance -25550 -6600 30050 28100

Working notes:

Month December January February March April

Units sold 10 10 15 25 30

Sales value 1800 1800 2700 4500 5400

Cash fee at 1% 18000 18000 27000 45000 54000

Cash fee at 2% 36000 36000 54000 90000 108000

Variable cost

at 0.5%

9000 13500 22500 27000

6

Total receipts (A) 54000 63000 99000 164000

(B) Payments

Salary 26250 26250 26250 26250

Bonuses 6300 12600

Variable expenses 9000 13500 22500 27000

Rent/Rates - - - -

Fixed overheads 4300 4300 4300 4300

Tax liability 95800

Interest charges 3000

Total Payments (B) 39550 44050 62350 165950

Net cash flow (A-B) 14450 18950 36650 1950

Opening balance 40000 25550 6600 30050

Closing balance -25550 -6600 30050 28100

Working notes:

Month December January February March April

Units sold 10 10 15 25 30

Sales value 1800 1800 2700 4500 5400

Cash fee at 1% 18000 18000 27000 45000 54000

Cash fee at 2% 36000 36000 54000 90000 108000

Variable cost

at 0.5%

9000 13500 22500 27000

6

Monthly salary cost= (35000*9)/12=26250

Bonus for March= (25*20)*140*9=6300

Bonus for April= (30*20)*140*9=12600

Interpretation: As per the above report it has been interpreted that Throne Estate limited

prepare cash budget from January to April to present actual cash situation in the business. It is

changing as per the situation and impact on the profitability in direct manner. At the starting of

the budget calculation presents total receipt of the company in which consist of cash fees, credit

fees which is 2% of sale and sale of assets. The company receive 15 cash sales in same month

and remaining 2% receive after 2 months. In the month of January to April total receipt were

54000, 63000, 99000 and 164000 respectively. From the total receipt of the company less

amount of payment in which consist of salary, bonus, expenses, taxation, interest and fixed

overhead. The average salary per employee is 35000 per year so accordingly divide by 12

months and multiply by 9 employees. The variable expenditure rate 0.5% apply on each property

that sale out by company. After all the calculation Cash outflow is 14450 after that it is increased

and reached on 18950 in the month of February. In the month of March identify growth in

outflow 36650 and again fall down in April 1950 that presents major changes in the amount of

net cash flow. The closing balance in January (-25550) because of company liquidity position is

not good and do not able to conduct business activities in proper manner. Same procedure follow

in other months and get negative closing balance in February due to less liquidity position but in

March company get positive balance because of able to maintain cash as per the requirement.

There are requirement of analysis of overall procedure are changes done by business entity to

enhance cash flow the lower down of expenditure. Moreover, increment in the expenditure

impact on the cash situation that concentrating on paying the expenditure amount that deduct the

cash position.

2. Any observations or recommendations that you would make to the management of Thorne

Estates

As per the observation of cash budget it is analysed that Thorne Estate has not been able

to maintain effective cash balance at the end of each month. It is clearly presented that

internal management of company is not able to manage a decent policy in these months

because of less cash balances are changing in different months.

7

Bonus for March= (25*20)*140*9=6300

Bonus for April= (30*20)*140*9=12600

Interpretation: As per the above report it has been interpreted that Throne Estate limited

prepare cash budget from January to April to present actual cash situation in the business. It is

changing as per the situation and impact on the profitability in direct manner. At the starting of

the budget calculation presents total receipt of the company in which consist of cash fees, credit

fees which is 2% of sale and sale of assets. The company receive 15 cash sales in same month

and remaining 2% receive after 2 months. In the month of January to April total receipt were

54000, 63000, 99000 and 164000 respectively. From the total receipt of the company less

amount of payment in which consist of salary, bonus, expenses, taxation, interest and fixed

overhead. The average salary per employee is 35000 per year so accordingly divide by 12

months and multiply by 9 employees. The variable expenditure rate 0.5% apply on each property

that sale out by company. After all the calculation Cash outflow is 14450 after that it is increased

and reached on 18950 in the month of February. In the month of March identify growth in

outflow 36650 and again fall down in April 1950 that presents major changes in the amount of

net cash flow. The closing balance in January (-25550) because of company liquidity position is

not good and do not able to conduct business activities in proper manner. Same procedure follow

in other months and get negative closing balance in February due to less liquidity position but in

March company get positive balance because of able to maintain cash as per the requirement.

There are requirement of analysis of overall procedure are changes done by business entity to

enhance cash flow the lower down of expenditure. Moreover, increment in the expenditure

impact on the cash situation that concentrating on paying the expenditure amount that deduct the

cash position.

2. Any observations or recommendations that you would make to the management of Thorne

Estates

As per the observation of cash budget it is analysed that Thorne Estate has not been able

to maintain effective cash balance at the end of each month. It is clearly presented that

internal management of company is not able to manage a decent policy in these months

because of less cash balances are changing in different months.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finally, it is suggested that manager of Throne Estate is really designed once time in a

year that is depended on the business entity. It is set up as per the monthly, yearly and

quarterly level.

Sales are the primary kind of funds of a firm that is based on the reliability of the

financial statement is also based on the accuration of outlook of revenues (Young and

Pagliari, 2017). It is suggested to Thorne to sell out product in the market in broad

manner and manage liquidity position in effective manner.

Moreover, The administration will predict the volume of revenues in regard of cash and

also credits that depend on the past experience. It is advised that the manager should use

effective strategies for payment to the creditors on time and analysis all the accounts

receivables in the business entity.

There are required to applied some modification of Thorne in various operational

activities and apply on different functions for collect fund for an entity. For this require to

proper planning and manage cash position effectively. The proper payment by the

supplier in supply right time will also supports business entity to enhance their cash

position and set up good relationship with them in order to accomplishing effective net

cash flow (Zherlitsyn and Kravchenko, 2016).

It is advised to Thorne Estates limited that when the duration of credit is permitted by

borrowers in one month so amount will be paid in month of Feb for various payment

activities that has done in January. The manager try to maintain effective liquidity

position by the proper movement of cash inflow and out flow. It supports to conduct

business activities in proper manner.

8

year that is depended on the business entity. It is set up as per the monthly, yearly and

quarterly level.

Sales are the primary kind of funds of a firm that is based on the reliability of the

financial statement is also based on the accuration of outlook of revenues (Young and

Pagliari, 2017). It is suggested to Thorne to sell out product in the market in broad

manner and manage liquidity position in effective manner.

Moreover, The administration will predict the volume of revenues in regard of cash and

also credits that depend on the past experience. It is advised that the manager should use

effective strategies for payment to the creditors on time and analysis all the accounts

receivables in the business entity.

There are required to applied some modification of Thorne in various operational

activities and apply on different functions for collect fund for an entity. For this require to

proper planning and manage cash position effectively. The proper payment by the

supplier in supply right time will also supports business entity to enhance their cash

position and set up good relationship with them in order to accomplishing effective net

cash flow (Zherlitsyn and Kravchenko, 2016).

It is advised to Thorne Estates limited that when the duration of credit is permitted by

borrowers in one month so amount will be paid in month of Feb for various payment

activities that has done in January. The manager try to maintain effective liquidity

position by the proper movement of cash inflow and out flow. It supports to conduct

business activities in proper manner.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

REFERENCES

Books and Journals

Beekes, W. and et.al., 2016. Corporate governance, companies’ disclosure practices and market

transparency: A cross country study. Journal of Business Finance & Accounting. 43(3-

4). pp.263-297.

Boschmans, K. and Pissareva, L., 2018. Fostering Markets for SME Finance: Matching Business

and Investor Needs.

Cowling, M., Liu, W. and Zhang, N., 2016. Access to bank finance for UK SMEs in the wake of

the recent financial crisis. International Journal of Entrepreneurial Behavior &

Research.

Heil, M., 2017. Finance and productivity: A literature review.

Kennickell, A. B., Kwast, M. L. and Pogach, J., 2016. Small businesses and small business

finance during the financial crisis and the great recession: New evidence from the

survey of consumer finances. In Measuring Entrepreneurial Businesses: Current

Knowledge and Challenges (pp. 291-349). University of Chicago Press.

Ketterer, J. A., 2017. Digital finance: New times, new challenges, new opportunities. IDB-Inter

American Development Bank.

Kraemer-Eis, H. and et.al., 2019. European Small Business Finance Outlook: June 2019 (No.

2019/57). EIF Working Paper.

Liesen, A. and et.al., 2017. Climate change and asset prices: are corporate carbon disclosure and

performance priced appropriately?. Journal of Business Finance & Accounting. 44(1-2).

pp.35-62.

Rahman, A., Rozsa, Z. and Cepel, M., 2018. Trade credit and bank finance–evidence from the

Visegrad Group. Journal of Competitiveness.

Rubanov, P. M. and Marcantonio, A., 2017. Alternative finance business-models: Online

platforms.

Young, K. and Pagliari, S., 2017. Capital united? Business unity in regulatory politics and the

special place of finance. Regulation & Governance. 11(1). pp.3-23.

Zherlitsyn, D. and Kravchenko, V., 2016. Supply Chain Resilience Through Operations and

Finance Management. Scientific Letters of Academic Society of Michal Baludansky.

4(1).

10

Books and Journals

Beekes, W. and et.al., 2016. Corporate governance, companies’ disclosure practices and market

transparency: A cross country study. Journal of Business Finance & Accounting. 43(3-

4). pp.263-297.

Boschmans, K. and Pissareva, L., 2018. Fostering Markets for SME Finance: Matching Business

and Investor Needs.

Cowling, M., Liu, W. and Zhang, N., 2016. Access to bank finance for UK SMEs in the wake of

the recent financial crisis. International Journal of Entrepreneurial Behavior &

Research.

Heil, M., 2017. Finance and productivity: A literature review.

Kennickell, A. B., Kwast, M. L. and Pogach, J., 2016. Small businesses and small business

finance during the financial crisis and the great recession: New evidence from the

survey of consumer finances. In Measuring Entrepreneurial Businesses: Current

Knowledge and Challenges (pp. 291-349). University of Chicago Press.

Ketterer, J. A., 2017. Digital finance: New times, new challenges, new opportunities. IDB-Inter

American Development Bank.

Kraemer-Eis, H. and et.al., 2019. European Small Business Finance Outlook: June 2019 (No.

2019/57). EIF Working Paper.

Liesen, A. and et.al., 2017. Climate change and asset prices: are corporate carbon disclosure and

performance priced appropriately?. Journal of Business Finance & Accounting. 44(1-2).

pp.35-62.

Rahman, A., Rozsa, Z. and Cepel, M., 2018. Trade credit and bank finance–evidence from the

Visegrad Group. Journal of Competitiveness.

Rubanov, P. M. and Marcantonio, A., 2017. Alternative finance business-models: Online

platforms.

Young, K. and Pagliari, S., 2017. Capital united? Business unity in regulatory politics and the

special place of finance. Regulation & Governance. 11(1). pp.3-23.

Zherlitsyn, D. and Kravchenko, V., 2016. Supply Chain Resilience Through Operations and

Finance Management. Scientific Letters of Academic Society of Michal Baludansky.

4(1).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.