Business Finance Report: Financial Ratio Analysis of Browns PLC

VerifiedAdded on 2022/11/25

|13

|3770

|458

Report

AI Summary

This report provides a comprehensive financial analysis of Browns PLC, focusing on key financial ratios and cash flow management. The analysis includes calculations and interpretations of the gross profit margin, operating profit margin, current ratio, quick ratio, inventory holding period, and payables payment period for the years 2018 and 2019. The report highlights the company's operational efficiency, liquidity position, and working capital cycle. Furthermore, it differentiates between profit and cash flow, explaining their roles and importance in assessing a company's financial health. The report also discusses the relevance of calculating certain financial metrics, such as the receivables collection period, in the context of Browns PLC's operations. Finally, the report addresses the understanding of financial information and the management of cash, including working capital, receivables, inventory, and payables, and their impact on cash flows.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

PART- 1: FINANCIAL RATIO ANALYSIS.................................................................................1

Ratio Analysis..............................................................................................................................1

Interpretation................................................................................................................................2

Irrelevance of calculating the receivables collection period in this scenario..............................4

PART- 2: UNDERSTANDING FINANCIAL INFORMATION AND MANAGEMENT OF

CASH...............................................................................................................................................5

2.1 Explaining profit & cash flow and their differentiation........................................................5

2.2 Explaining working capital, receivables, inventory and payables.........................................7

2.3 Reasons for changes in the working capital affecting the cash flows...................................7

2.4 Appropriateness of the traditional and the alternative budgetary system for the business....9

REFERENCES..............................................................................................................................11

TABLE OF CONTENTS................................................................................................................2

PART- 1: FINANCIAL RATIO ANALYSIS.................................................................................1

Ratio Analysis..............................................................................................................................1

Interpretation................................................................................................................................2

Irrelevance of calculating the receivables collection period in this scenario..............................4

PART- 2: UNDERSTANDING FINANCIAL INFORMATION AND MANAGEMENT OF

CASH...............................................................................................................................................5

2.1 Explaining profit & cash flow and their differentiation........................................................5

2.2 Explaining working capital, receivables, inventory and payables.........................................7

2.3 Reasons for changes in the working capital affecting the cash flows...................................7

2.4 Appropriateness of the traditional and the alternative budgetary system for the business....9

REFERENCES..............................................................................................................................11

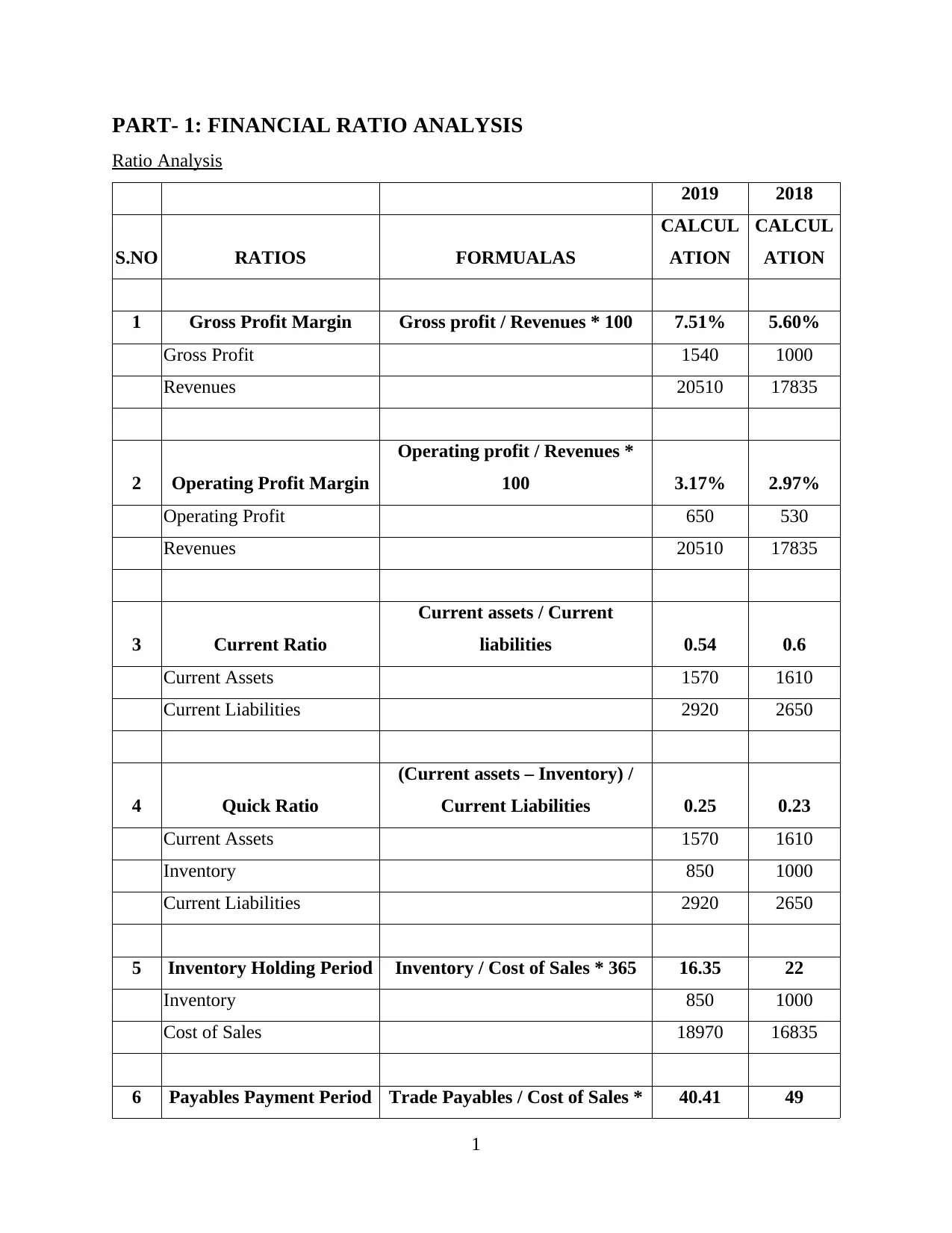

PART- 1: FINANCIAL RATIO ANALYSIS

Ratio Analysis

2019 2018

S.NO RATIOS FORMUALAS

CALCUL

ATION

CALCUL

ATION

1 Gross Profit Margin Gross profit / Revenues * 100 7.51% 5.60%

Gross Profit 1540 1000

Revenues 20510 17835

2 Operating Profit Margin

Operating profit / Revenues *

100 3.17% 2.97%

Operating Profit 650 530

Revenues 20510 17835

3 Current Ratio

Current assets / Current

liabilities 0.54 0.6

Current Assets 1570 1610

Current Liabilities 2920 2650

4 Quick Ratio

(Current assets – Inventory) /

Current Liabilities 0.25 0.23

Current Assets 1570 1610

Inventory 850 1000

Current Liabilities 2920 2650

5 Inventory Holding Period Inventory / Cost of Sales * 365 16.35 22

Inventory 850 1000

Cost of Sales 18970 16835

6 Payables Payment Period Trade Payables / Cost of Sales * 40.41 49

1

Ratio Analysis

2019 2018

S.NO RATIOS FORMUALAS

CALCUL

ATION

CALCUL

ATION

1 Gross Profit Margin Gross profit / Revenues * 100 7.51% 5.60%

Gross Profit 1540 1000

Revenues 20510 17835

2 Operating Profit Margin

Operating profit / Revenues *

100 3.17% 2.97%

Operating Profit 650 530

Revenues 20510 17835

3 Current Ratio

Current assets / Current

liabilities 0.54 0.6

Current Assets 1570 1610

Current Liabilities 2920 2650

4 Quick Ratio

(Current assets – Inventory) /

Current Liabilities 0.25 0.23

Current Assets 1570 1610

Inventory 850 1000

Current Liabilities 2920 2650

5 Inventory Holding Period Inventory / Cost of Sales * 365 16.35 22

Inventory 850 1000

Cost of Sales 18970 16835

6 Payables Payment Period Trade Payables / Cost of Sales * 40.41 49

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

365

Trade Payables 2100 2280

Cost of Sales 18970 16835

Interpretation

Gross profit margin- The gross profit margin of the company shall be representing the

operational efficiency through conducting the routine business transactions in the company.

It is depicted in the percentage form wherein the gross profits that are earned are divided by

the revenues that are generated over the period for the organization. The higher is such ratio

the better it is for the profitability position of the business showing the lesser costs of

production. From the above table it can be represented that for Browns plc the gross profit

margin has increased from 5.60% in the previous 2018 to 7.51% in the current year 2019

(Agustina and Suprayitno, 2020). This reflects the significant increase which can be due to

the increased operational efficiency pertaining to the increased sales of the online food

delivery and the clothing business. The reason behind interpreting the gross profit’s ratio

increase is due to inclination of online food home delivery that has increased present year

GP than previous

Operating profit margin- The operating profit margin of the company shall be showing

the performance that is generated through the routine operations that are undertaken by

the business. It is calculated by dividing the operating income to the sales of the company

and the operating income is identified post the deduction of all the operating expenses

that are incurred. As inferred by the above tabular representations the operating profit

margin of the Browns plc has also improved as compared with the previous year when it

was 2.97% and in the current year 2019 it has increased to 3.17%. The major reason for

this can be the strong and the aggressive marketing campaign that is being undertaken to

attract the larger portions of the market to the products and the services that are offered. Current ratio- The current ratio of the company shows the availability of the liquid assets

to meet the short term liabilities and obligations of the business. This shall be reflecting

the liquidity position and the maintenance of the credibility in the organization and

2

Trade Payables 2100 2280

Cost of Sales 18970 16835

Interpretation

Gross profit margin- The gross profit margin of the company shall be representing the

operational efficiency through conducting the routine business transactions in the company.

It is depicted in the percentage form wherein the gross profits that are earned are divided by

the revenues that are generated over the period for the organization. The higher is such ratio

the better it is for the profitability position of the business showing the lesser costs of

production. From the above table it can be represented that for Browns plc the gross profit

margin has increased from 5.60% in the previous 2018 to 7.51% in the current year 2019

(Agustina and Suprayitno, 2020). This reflects the significant increase which can be due to

the increased operational efficiency pertaining to the increased sales of the online food

delivery and the clothing business. The reason behind interpreting the gross profit’s ratio

increase is due to inclination of online food home delivery that has increased present year

GP than previous

Operating profit margin- The operating profit margin of the company shall be showing

the performance that is generated through the routine operations that are undertaken by

the business. It is calculated by dividing the operating income to the sales of the company

and the operating income is identified post the deduction of all the operating expenses

that are incurred. As inferred by the above tabular representations the operating profit

margin of the Browns plc has also improved as compared with the previous year when it

was 2.97% and in the current year 2019 it has increased to 3.17%. The major reason for

this can be the strong and the aggressive marketing campaign that is being undertaken to

attract the larger portions of the market to the products and the services that are offered. Current ratio- The current ratio of the company shows the availability of the liquid assets

to meet the short term liabilities and obligations of the business. This shall be reflecting

the liquidity position and the maintenance of the credibility in the organization and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

simultaneously fulfilling the company objectives. Apart from that it shows the

availability of the funds for the payment of the liabilities that arise within the period of

one year that are categorized as the short term liabilities. The ratio analysis that is being

conducted above from the financials available of the Browns plc shows that the current

ratio of the company decreases as compared to the past year and this shows the

deterioration in the liquidity position of the company. In the year 2018 the ratio was 0.6

which has now decreased to 0.54 in the year 2019 which is the red signal for the company

as they have the insufficient balances to meet the liabilities. The major reason for the

change occurred in current year performance regarding this particular matrix is that

number of store has grow that has reduced available liquidity as part of fund has been

invested for this purpose, Quick ratio- The quick ratio of the company shows the availability of the highly liquid

assets in the company to fulfil the short term debt obligations of the company. The highly

liquid assets are the ones that can be easily converted to cash and equivalents. This does

not include the inventory and the prepaid expenses of the company as they are readily

available as cash (Easton and et.al., 2018). The above table that is formed for the Browns

plc shows that the quick ratio of the company has increased as compared from the

financial statements. As it can be evidently be noticed that in the year 2018 the ratio was

0.23 which increased to 0.25 in the year 2019 which is the positive signal for the

company and its liquidity position. This is because the calculations of the quick ratio are

not impacted by the closing balance of the inventory and that is the reason the increasing

trend is visible. The reason behind alternation in present outcome is change in customer

buying behaviour which has increased for 20% as compared to previous that has resulted

into little change of capacity to meet with short term obligation.

Inventory holding period- The inventory holding period of the company highlights the

average number of days the inventory is hold by the business organization. This is found

out by dividing the average inventory by cost of sales and then multiplying it by 365

days, the result must not be too high showing that the funds are unnecessarily blocked

and the loss of the opportunity costs is taking place in the year. It can be analysed that in

comparison with the previous year the inventory holding period this year has reduced

significantly and the major reason for this is that the turnover of the company has

3

availability of the funds for the payment of the liabilities that arise within the period of

one year that are categorized as the short term liabilities. The ratio analysis that is being

conducted above from the financials available of the Browns plc shows that the current

ratio of the company decreases as compared to the past year and this shows the

deterioration in the liquidity position of the company. In the year 2018 the ratio was 0.6

which has now decreased to 0.54 in the year 2019 which is the red signal for the company

as they have the insufficient balances to meet the liabilities. The major reason for the

change occurred in current year performance regarding this particular matrix is that

number of store has grow that has reduced available liquidity as part of fund has been

invested for this purpose, Quick ratio- The quick ratio of the company shows the availability of the highly liquid

assets in the company to fulfil the short term debt obligations of the company. The highly

liquid assets are the ones that can be easily converted to cash and equivalents. This does

not include the inventory and the prepaid expenses of the company as they are readily

available as cash (Easton and et.al., 2018). The above table that is formed for the Browns

plc shows that the quick ratio of the company has increased as compared from the

financial statements. As it can be evidently be noticed that in the year 2018 the ratio was

0.23 which increased to 0.25 in the year 2019 which is the positive signal for the

company and its liquidity position. This is because the calculations of the quick ratio are

not impacted by the closing balance of the inventory and that is the reason the increasing

trend is visible. The reason behind alternation in present outcome is change in customer

buying behaviour which has increased for 20% as compared to previous that has resulted

into little change of capacity to meet with short term obligation.

Inventory holding period- The inventory holding period of the company highlights the

average number of days the inventory is hold by the business organization. This is found

out by dividing the average inventory by cost of sales and then multiplying it by 365

days, the result must not be too high showing that the funds are unnecessarily blocked

and the loss of the opportunity costs is taking place in the year. It can be analysed that in

comparison with the previous year the inventory holding period this year has reduced

significantly and the major reason for this is that the turnover of the company has

3

increased in terms of online food delivery and the sale of the clothing and apart the

aggressive marketing has also contributed to the maximization of the revenues. The other

fact is that since Browns plc has the supermarket business and the food products have

closer expiry that is the reason that the inventory holding period shall be shorter. The

reason can be considered that online delivery ahs increased which has impacted in same

manner. Payables payment period- The payables payment period reflects the average number of

days it takes the company to make the payments that are due to its suppliers and the

creditors. For the smooth conduction of the working capital cycle by the company it can

be assessed that the payables ratio must be in sync with the receivables ratio so that the

liquidity flow can be maintained (Heriyanto and et.al., 2021). It can be assessed that

earlier in the year 2018 it took averagely 49 days to pay the due amounts but now in the

year 2019 it approximately takes 40 days to do the same. This means that with the ratio

the credibility of the company has improved. Since the long term borrowings have been

taken so it can be identified that the company has the sufficient availability of the funds.

Major reason behind is that new strengthened Grocery Supplier Code of Practice came

into force to improve grocery retailers’ treatment of suppliers in terms of fairer prices. It

has helped to pay debts in lesser time.

Irrelevance of calculating the receivables collection period in this scenario

It can be assessed that the calculation of the receivables collection period is not relevant

for the company Browns plc as 100% of its operations are in cash and so the matter of the

collection of the credit does arise for the company (Basuki, Hidayat and Budiwitjaksono, 2020).

Apart from that it can also be analysed that since major proportion of the sales are being

conducted online for the company that is the reason either the payments are made through online

modes of payment or it can be through the physical payments on delivery. So in this case the

scope for the credit transactions decrease. Further the retail business of the supermarkets are also

undertaking the operations in the full cash system.

4

aggressive marketing has also contributed to the maximization of the revenues. The other

fact is that since Browns plc has the supermarket business and the food products have

closer expiry that is the reason that the inventory holding period shall be shorter. The

reason can be considered that online delivery ahs increased which has impacted in same

manner. Payables payment period- The payables payment period reflects the average number of

days it takes the company to make the payments that are due to its suppliers and the

creditors. For the smooth conduction of the working capital cycle by the company it can

be assessed that the payables ratio must be in sync with the receivables ratio so that the

liquidity flow can be maintained (Heriyanto and et.al., 2021). It can be assessed that

earlier in the year 2018 it took averagely 49 days to pay the due amounts but now in the

year 2019 it approximately takes 40 days to do the same. This means that with the ratio

the credibility of the company has improved. Since the long term borrowings have been

taken so it can be identified that the company has the sufficient availability of the funds.

Major reason behind is that new strengthened Grocery Supplier Code of Practice came

into force to improve grocery retailers’ treatment of suppliers in terms of fairer prices. It

has helped to pay debts in lesser time.

Irrelevance of calculating the receivables collection period in this scenario

It can be assessed that the calculation of the receivables collection period is not relevant

for the company Browns plc as 100% of its operations are in cash and so the matter of the

collection of the credit does arise for the company (Basuki, Hidayat and Budiwitjaksono, 2020).

Apart from that it can also be analysed that since major proportion of the sales are being

conducted online for the company that is the reason either the payments are made through online

modes of payment or it can be through the physical payments on delivery. So in this case the

scope for the credit transactions decrease. Further the retail business of the supermarkets are also

undertaking the operations in the full cash system.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART- 2: UNDERSTANDING FINANCIAL INFORMATION AND

MANAGEMENT OF CASH

2.1 Explaining profit & cash flow and their differentiation

Profit refers to gain company is earning from executing business transaction through

deducting expenses from revenue generated. It is one of the crucial objective of organization for

which is incurred to earn gain in terms of money. Achieving financial benefits are as well

referred as having profitability in company that tends to meet business goals. This is considered

to be one of the crucial aspects of measurement regarding company’s financial health (Laguecir,

Chapman and Kern, 2019). The margin taken into consideration for evaluating organization’s

success differs from industry to sector. Higher profit indicates good liquidity position and lower

signs poor position in industry. Several types of stakeholders highly give emphasis on

profitability for decision making. There are various situations in firm which indicates profitable

but posses lower cash balances as they include accrual principle while estimating the same. Non

monetary transaction such as depreciation, amortization, etc are taken into action while deterring

profits which creates differentiation in actual & estimated.

Cash Flow (CF) is real movement of money in and out of organization which is obtained

from three categories. It comprises operating, investing and financing which play important role

in deciding stability of organization. Operating cash flow includes money generated from main

business practices, financing are concerned with activities regarding capital assets & investment

and equivalents gained from debt, equity, etc. These are the forms which are utilized by

organization to have smooth functioning through maintaining liquidity. If the money is coming

due to implementation of entity activities it’s known as cash inflow. The cash and equivalent

incurred for practices are considered as outflow. Positive CF indicates firm is having stable and

sustainable liquidity position and recovering obligations via optimum utilization of resources.

Differentiation between profit and cash flow

Purpose

Profitability helps in identifying that organization is going in right direction or not. For

example- it helps in identifying profitability through including sales credit as well to get

appropriate knowledge

This provides guidance in evaluating capability in terms of monetary resources for reaching

the desirable position by evaluating the impact of depreciation, etc

5

MANAGEMENT OF CASH

2.1 Explaining profit & cash flow and their differentiation

Profit refers to gain company is earning from executing business transaction through

deducting expenses from revenue generated. It is one of the crucial objective of organization for

which is incurred to earn gain in terms of money. Achieving financial benefits are as well

referred as having profitability in company that tends to meet business goals. This is considered

to be one of the crucial aspects of measurement regarding company’s financial health (Laguecir,

Chapman and Kern, 2019). The margin taken into consideration for evaluating organization’s

success differs from industry to sector. Higher profit indicates good liquidity position and lower

signs poor position in industry. Several types of stakeholders highly give emphasis on

profitability for decision making. There are various situations in firm which indicates profitable

but posses lower cash balances as they include accrual principle while estimating the same. Non

monetary transaction such as depreciation, amortization, etc are taken into action while deterring

profits which creates differentiation in actual & estimated.

Cash Flow (CF) is real movement of money in and out of organization which is obtained

from three categories. It comprises operating, investing and financing which play important role

in deciding stability of organization. Operating cash flow includes money generated from main

business practices, financing are concerned with activities regarding capital assets & investment

and equivalents gained from debt, equity, etc. These are the forms which are utilized by

organization to have smooth functioning through maintaining liquidity. If the money is coming

due to implementation of entity activities it’s known as cash inflow. The cash and equivalent

incurred for practices are considered as outflow. Positive CF indicates firm is having stable and

sustainable liquidity position and recovering obligations via optimum utilization of resources.

Differentiation between profit and cash flow

Purpose

Profitability helps in identifying that organization is going in right direction or not. For

example- it helps in identifying profitability through including sales credit as well to get

appropriate knowledge

This provides guidance in evaluating capability in terms of monetary resources for reaching

the desirable position by evaluating the impact of depreciation, etc

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Basis of Outcome

It can be estimated in terms of value creation. This provides helps in measuring firm’s

financial health and sustainability. It basically highlights gain remaining after all cash and

non monetary activity

CF can be thought about in form of time like month, week or yearly operation depending

upon enterprise requirement. CFS is prepared for each period to get appropriate knowledge

of specific duration avail resources through removing irrelevant manipulation of non

monetary transaction

Procedure

It is procedure of formulating cash for smooth functioning of organization (Profit vs. Cash

flow: What is difference? 2021). Various practices like selling on credit, holding inventory ,

etc to generate revenue to gain financial benefit.

CF is crucial source material for generating profitability. It helps in having enough capacity

for reach position of higher liquidity through gaining financial advantages through.

Life span

Company can survive in industry for particular span of time in absence of profitability

It becomes difficult to have processing in company in non presence of cash flow. It leads to

closing of business operational practices.

Consideration

This aids in making assessment regarding business activities for knowing longer run cash

flows in business.

It is concerned with managing actions timely in respect to maximize profitability.

Pattern to gain

Sale made beyond the breakeven point brings profitability in organization. Treatment of

depreciation is here exerted as cost

It is affected by the timings of payments into & out of the firm as profits can be manipulated

but not cash.

Timeliness

Cash must be currently available in order to replenish supplies , pay employees, etc. But

profit comes when firm has become successful after bearing all these expenses.

6

It can be estimated in terms of value creation. This provides helps in measuring firm’s

financial health and sustainability. It basically highlights gain remaining after all cash and

non monetary activity

CF can be thought about in form of time like month, week or yearly operation depending

upon enterprise requirement. CFS is prepared for each period to get appropriate knowledge

of specific duration avail resources through removing irrelevant manipulation of non

monetary transaction

Procedure

It is procedure of formulating cash for smooth functioning of organization (Profit vs. Cash

flow: What is difference? 2021). Various practices like selling on credit, holding inventory ,

etc to generate revenue to gain financial benefit.

CF is crucial source material for generating profitability. It helps in having enough capacity

for reach position of higher liquidity through gaining financial advantages through.

Life span

Company can survive in industry for particular span of time in absence of profitability

It becomes difficult to have processing in company in non presence of cash flow. It leads to

closing of business operational practices.

Consideration

This aids in making assessment regarding business activities for knowing longer run cash

flows in business.

It is concerned with managing actions timely in respect to maximize profitability.

Pattern to gain

Sale made beyond the breakeven point brings profitability in organization. Treatment of

depreciation is here exerted as cost

It is affected by the timings of payments into & out of the firm as profits can be manipulated

but not cash.

Timeliness

Cash must be currently available in order to replenish supplies , pay employees, etc. But

profit comes when firm has become successful after bearing all these expenses.

6

2.2 Explaining working capital, receivables, inventory and payables

Working Capital

WC is the amount of money which is utilized in day to day practices by organization. It helps in

meeting short term expenses that due within year and it is obtained from the difference between

current assets and liabilities. Good WC ensures smooth processing of enterprise that lead to

attain sustainability.

Formula:

WC= Current assets – current liabilities

Receivables

Receivables are referred as amount payable by customers to company as goods are sold

on credit. It is legally enforceable claim for payment held by business for goods supplied or

services rendered to customer but not paid. It aids in building good relationship with customers

and increases market share.

Payables

It is created any time when money is owed by a firm for services rendered or products

provided that has not yet been paid by organization.

Inventory

This is important term that is used for finished goods, raw material and work in progress

for the purpose of production . It is taken into practice for determining organizational efficiency

of manufacturing process (Dagnall and et.al., 2018). Stock decides firm’s capability of meeting

market forces which contributes in increasing market share to generate more revenue.

2.3 Reasons for changes in the working capital affecting the cash flows

The changes in the working capital of the company shall be affecting the cash flows in

case they are cash transactions as associated with the current assets and the current liabilities and

are resulting in the movements of cash (How changes in working capital affect your net cash

flow in business valuation, 2021). If there is an increase in the working capital of the company

then it shall lead to the drainage of the cash flows which is the indication that the management of

7

Working Capital

WC is the amount of money which is utilized in day to day practices by organization. It helps in

meeting short term expenses that due within year and it is obtained from the difference between

current assets and liabilities. Good WC ensures smooth processing of enterprise that lead to

attain sustainability.

Formula:

WC= Current assets – current liabilities

Receivables

Receivables are referred as amount payable by customers to company as goods are sold

on credit. It is legally enforceable claim for payment held by business for goods supplied or

services rendered to customer but not paid. It aids in building good relationship with customers

and increases market share.

Payables

It is created any time when money is owed by a firm for services rendered or products

provided that has not yet been paid by organization.

Inventory

This is important term that is used for finished goods, raw material and work in progress

for the purpose of production . It is taken into practice for determining organizational efficiency

of manufacturing process (Dagnall and et.al., 2018). Stock decides firm’s capability of meeting

market forces which contributes in increasing market share to generate more revenue.

2.3 Reasons for changes in the working capital affecting the cash flows

The changes in the working capital of the company shall be affecting the cash flows in

case they are cash transactions as associated with the current assets and the current liabilities and

are resulting in the movements of cash (How changes in working capital affect your net cash

flow in business valuation, 2021). If there is an increase in the working capital of the company

then it shall lead to the drainage of the cash flows which is the indication that the management of

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the company is investing the resources for the short term. On the other hand if the working

capital of the company is negatively impacted then it means that there are cash inflows in the

form of short term borrowings to finance the operations of the business.

Receivables is important part of working capital which are recorded at the time of sale, it

decreases when payments are made by customers that is included in current assets par of balance

sheet. In order to have effective functioning of organization it becomes important for company to

formulate appropriate receivable collection period. Payables are recorded as liability side of

balance sheet as these are due to pay. Overcoming debt on time brings trustworthiness and

credibility which makes raising funds easier as compared to previous. Receivables and payables

are important part of working capital as it play role of increasing and decreasing cash flow of

company. Inventory contributes in reducing cash available within company.

Cash operating cycle is helps in measuring effective availability of cash tied up

with WC. Having effectual pattern of COC aids in gaining knowledge how much tiem firm

requires to convert out flows into inflows. Good WC is obtained through quick operating cycle

that signs lower amount of investment is needed to increase profitability and bring cash in

company. Offering credit can be risky for company s there is possibilities of occurring bad debt

which decline liquidity. The inventory holding decreases the ability of generating revenues and

results in unnecessary cost. It impacts the current assets side of WC which largely influence CF.

Company receives benefits from longer payable time as it gets ability to hold some cash for

utilizing in order to obtain smooth functioning. The benefits includes increasing efficiency of

operational practices, time to arrange funds for paying debt, capacity of meeting unforeseen

circumstances, etc. Appropriate availability of cash flow helps in removing situation of

bankruptcy via meeting payments on proper time.

There are different types of the transactions related to these both elements like if the

current asset increases keeping others constant then the working capital shall increase and the

free cash flows will decrease. In the similar way current liabilities increase then the working

capital decrease and the free cash flows increase. Lastly if the increase in the current assets is

higher than that of the current liabilities then again working capital will increase and the cash

flows shall be decreasing. These shall be important in the valuations of the company.

8

capital of the company is negatively impacted then it means that there are cash inflows in the

form of short term borrowings to finance the operations of the business.

Receivables is important part of working capital which are recorded at the time of sale, it

decreases when payments are made by customers that is included in current assets par of balance

sheet. In order to have effective functioning of organization it becomes important for company to

formulate appropriate receivable collection period. Payables are recorded as liability side of

balance sheet as these are due to pay. Overcoming debt on time brings trustworthiness and

credibility which makes raising funds easier as compared to previous. Receivables and payables

are important part of working capital as it play role of increasing and decreasing cash flow of

company. Inventory contributes in reducing cash available within company.

Cash operating cycle is helps in measuring effective availability of cash tied up

with WC. Having effectual pattern of COC aids in gaining knowledge how much tiem firm

requires to convert out flows into inflows. Good WC is obtained through quick operating cycle

that signs lower amount of investment is needed to increase profitability and bring cash in

company. Offering credit can be risky for company s there is possibilities of occurring bad debt

which decline liquidity. The inventory holding decreases the ability of generating revenues and

results in unnecessary cost. It impacts the current assets side of WC which largely influence CF.

Company receives benefits from longer payable time as it gets ability to hold some cash for

utilizing in order to obtain smooth functioning. The benefits includes increasing efficiency of

operational practices, time to arrange funds for paying debt, capacity of meeting unforeseen

circumstances, etc. Appropriate availability of cash flow helps in removing situation of

bankruptcy via meeting payments on proper time.

There are different types of the transactions related to these both elements like if the

current asset increases keeping others constant then the working capital shall increase and the

free cash flows will decrease. In the similar way current liabilities increase then the working

capital decrease and the free cash flows increase. Lastly if the increase in the current assets is

higher than that of the current liabilities then again working capital will increase and the cash

flows shall be decreasing. These shall be important in the valuations of the company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.4 Appropriateness of the traditional and the alternative budgetary system for the business

The traditional budgetary system for the company can be the method of incremental

budgeting. In this the management of the company shall be making the future projections based

on the past data and making the necessary adjustments as proposed in the future. The figures of

the past budget are only adjusted with the future changes like inflation, change in the demand

and supply forces and the level of the capacity at which the business shall be working. These

figures are then communicated to the employees so that the targets of the business are fulfilled.

Advantages of this system is easy to implement, promotion of decentralization, stability in

organizational function, etc. The related limitations are fixe & rigid nature, reliance on historial

data, improper allocation of resources, etc

Zero Based Budgeting

On the contrary the modern budgetary system involves zero based budgeting technique

wherein the budgets showing the future operations of the company are prepared from the zero or

scratch and accordingly every line of item that is involved shall be justified for the business. It’s

advantages includes that this does not consider the past figures rather accumulate all the

information based on the current trends of the business (Karmańska and Wiśniewska, 2020). It

can be assessed that the modern budgetary system is more appropriate for the businesses as this

shall provide with the accurate data after the analysis, the chances of the achievement of the

organizational objectives shall be higher, it will involve the optimum allocation as well as the

utilization of the resources. It is superior to the traditional methods as all the expenses are

justified and accordingly the profitability and the revenues of the Browns plc shall be boosted.

Disadvantages comprises the process of zero based budgeting is time-consuming and requires the

specialized staff that can enquire about each and every figure pertaining to the budgets.

Incremental budgeting

This prepared by making marginal changes in current budget for gaining competitive

advantages. As compared to traditional budgeting it is most simple to make some changes as per

the current scenario. With help of saving efforts through implementing alteration to current

budget fir can get operational and consistency stability. There is possibility of declining internal

rivalry as clarity regarding roles responsibility can be obtained. Drawback of it is includes leads

to extra spending, budgetary slack, waste of resources, based on unreal assumption, etc. It can be

9

The traditional budgetary system for the company can be the method of incremental

budgeting. In this the management of the company shall be making the future projections based

on the past data and making the necessary adjustments as proposed in the future. The figures of

the past budget are only adjusted with the future changes like inflation, change in the demand

and supply forces and the level of the capacity at which the business shall be working. These

figures are then communicated to the employees so that the targets of the business are fulfilled.

Advantages of this system is easy to implement, promotion of decentralization, stability in

organizational function, etc. The related limitations are fixe & rigid nature, reliance on historial

data, improper allocation of resources, etc

Zero Based Budgeting

On the contrary the modern budgetary system involves zero based budgeting technique

wherein the budgets showing the future operations of the company are prepared from the zero or

scratch and accordingly every line of item that is involved shall be justified for the business. It’s

advantages includes that this does not consider the past figures rather accumulate all the

information based on the current trends of the business (Karmańska and Wiśniewska, 2020). It

can be assessed that the modern budgetary system is more appropriate for the businesses as this

shall provide with the accurate data after the analysis, the chances of the achievement of the

organizational objectives shall be higher, it will involve the optimum allocation as well as the

utilization of the resources. It is superior to the traditional methods as all the expenses are

justified and accordingly the profitability and the revenues of the Browns plc shall be boosted.

Disadvantages comprises the process of zero based budgeting is time-consuming and requires the

specialized staff that can enquire about each and every figure pertaining to the budgets.

Incremental budgeting

This prepared by making marginal changes in current budget for gaining competitive

advantages. As compared to traditional budgeting it is most simple to make some changes as per

the current scenario. With help of saving efforts through implementing alteration to current

budget fir can get operational and consistency stability. There is possibility of declining internal

rivalry as clarity regarding roles responsibility can be obtained. Drawback of it is includes leads

to extra spending, budgetary slack, waste of resources, based on unreal assumption, etc. It can be

9

concluded that this is one of the most appropriate technique to gain efficiency and flexibility in

operational practices at all levels.

10

operational practices at all levels.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.