Financial Management Report: Financial Statement Analysis and Methods

VerifiedAdded on 2022/11/24

|13

|2838

|494

Report

AI Summary

This report provides an in-depth analysis of financial management, beginning with an introduction to the core concepts and its importance within a business context. It then delves into the preparation and significance of financial statements, including income statements, cash flow statements, balance sheets, and statements of shareholders' equity. The report emphasizes the use of financial ratios, such as profitability, liquidity, and solvency ratios, to evaluate a company's financial health and performance. Practical templates and examples are incorporated to demonstrate the application of these concepts. Furthermore, the report offers recommendations on methods to improve financial performance, including strategies to enhance customer relationships, optimize cash flow, and boost profitability through expense control and revenue generation. The conclusion summarizes the key findings and underscores the crucial role of financial management in achieving business objectives.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Section 1: Financial management and its importance.................................................................3

Section 2: Financial statements and use of ratios........................................................................4

Section 3: Templates....................................................................................................................6

Section 4: Methods of improving financial performance............................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Section 1: Financial management and its importance.................................................................3

Section 2: Financial statements and use of ratios........................................................................4

Section 3: Templates....................................................................................................................6

Section 4: Methods of improving financial performance............................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................2

INTRODUCTION

Finance refers to the blood the company that will lead to the running and operation of the

company's operation. It is the major aspect with regard to company that will lead to have actual

performance of business operation. Financial management refers to a process of finance

management that will ensure availability and utilization of finance. This report will discuss about

the concept of financial management, its importance along with financial statement preparation

and ratio analysis. A practical approach is also presented within this report regarding financial

statement's preparation.

MAIN BODY

Section 1: Financial management and its importance

Financial management:

It refers to a process under which various activities related with planning, organizing,

directing and controlling related with financial activities are undertaken. This will lead to

efficiently utilization of funds (Brigham and Houston, 2021). It would also be right to said that

under the concept of financial management various concepts and aspects of management are

applied so that better utilization of finance will take place.

In orders words financial management means the management and utilization of finance

with the involvement of decision-making concept so that organization will be directed towards

the direction of its objectives in terms of the better grabbing of profits and revenues.

Importance:

Financial planning:

Financial management will lead to have a making of appropriate financial plan. Under

this necessary financial activities with respect to company's finance are undertaken.\

Fund allocation:

This is also a major importance of financial management. This concept will lead to have

adequate allocation of finance among various assets and parts of business (Siekelova and et.al.,

2017). This will further lead to growth enhancement.

Financial decision:

As the financial management involves the preparation of financial statement so with the

help of those statements, company's position can be determined and as a result most appropriate

Finance refers to the blood the company that will lead to the running and operation of the

company's operation. It is the major aspect with regard to company that will lead to have actual

performance of business operation. Financial management refers to a process of finance

management that will ensure availability and utilization of finance. This report will discuss about

the concept of financial management, its importance along with financial statement preparation

and ratio analysis. A practical approach is also presented within this report regarding financial

statement's preparation.

MAIN BODY

Section 1: Financial management and its importance

Financial management:

It refers to a process under which various activities related with planning, organizing,

directing and controlling related with financial activities are undertaken. This will lead to

efficiently utilization of funds (Brigham and Houston, 2021). It would also be right to said that

under the concept of financial management various concepts and aspects of management are

applied so that better utilization of finance will take place.

In orders words financial management means the management and utilization of finance

with the involvement of decision-making concept so that organization will be directed towards

the direction of its objectives in terms of the better grabbing of profits and revenues.

Importance:

Financial planning:

Financial management will lead to have a making of appropriate financial plan. Under

this necessary financial activities with respect to company's finance are undertaken.\

Fund allocation:

This is also a major importance of financial management. This concept will lead to have

adequate allocation of finance among various assets and parts of business (Siekelova and et.al.,

2017). This will further lead to growth enhancement.

Financial decision:

As the financial management involves the preparation of financial statement so with the

help of those statements, company's position can be determined and as a result most appropriate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and better decision with respect to company betterment will be taken (Damayanti, Murtaqi and

Pradana, 2018).

Utilization of funds:

As financial management involves decision-making so it will lead to have a better

utilization of funds that will direct the company towards the direction of its goal

accomplishment.

Importance to public:

As these statements are the reflection of the company's financial performance so it will

play an important role with regard to public. This is because through these statements public can

know the company and its financial efficiency.

Section 2: Financial statements and use of ratios

Financial statements:

These are the statements that depicts the financial position of the company. It includes

those statements and activities that will lead to have depiction of the financial performance of the

company (Osadchy and et.al., 2018).

Importance:

Important to stakeholders:

Financial statements plays an important role with respect to stakeholders. This will assist

them to take adequate decision with respect to company. As these statements depict the financial

position so with the help of these statements financial and various other decisions are taken by

concerned stakeholders.

Analyse company's performance:

With the use of financial statements the company's performance in terms of financial

condition can be analysed easily. This will assist the management to determine whether they are

moving in right direction towards company's goal or not.

Controlling and monitoring:

Financial statements also act as a base that will lead to have monitoring of the company's

financial performance. Also, these statements enable the management to take adequate decisions

so that loopholes and deviation with respect to financial performance of the company can be

improvised.

Pradana, 2018).

Utilization of funds:

As financial management involves decision-making so it will lead to have a better

utilization of funds that will direct the company towards the direction of its goal

accomplishment.

Importance to public:

As these statements are the reflection of the company's financial performance so it will

play an important role with regard to public. This is because through these statements public can

know the company and its financial efficiency.

Section 2: Financial statements and use of ratios

Financial statements:

These are the statements that depicts the financial position of the company. It includes

those statements and activities that will lead to have depiction of the financial performance of the

company (Osadchy and et.al., 2018).

Importance:

Important to stakeholders:

Financial statements plays an important role with respect to stakeholders. This will assist

them to take adequate decision with respect to company. As these statements depict the financial

position so with the help of these statements financial and various other decisions are taken by

concerned stakeholders.

Analyse company's performance:

With the use of financial statements the company's performance in terms of financial

condition can be analysed easily. This will assist the management to determine whether they are

moving in right direction towards company's goal or not.

Controlling and monitoring:

Financial statements also act as a base that will lead to have monitoring of the company's

financial performance. Also, these statements enable the management to take adequate decisions

so that loopholes and deviation with respect to financial performance of the company can be

improvised.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Types of financial statements:

Income statement:

It is an important statement which shows the income and expenditure associated with the

company (Statements, 2020). Through this statement company can analyse that whether it is

making profit or loss. In short financial health of the company can be determined with these

statements.

Statement of cash flow:

This statement is used to analyse the company's cash flow position. This means that

through this statement company can determine its cash inflows and outflows.

Balance sheet:

It refers to that statement by which adequate reporting related with company's assets,

liabilities and shareholder equity related details can be analysed. It is usually prepared at the end

of the financial year (Daniel, Marioara and Isabela, 2017).

Statements of shareholders' equity:

It is part of balance sheet which shows changes in the share value of stockholders and the

equity shareholders. Changes in ownership interest will also be analysed with this statements.

Financial ratio:

These are the ratio which are financially evolved and related. These ratios are the

depiction of the company financial performance. Ratios are calculated on the basis of analysis of

the financial statements.

Importance:

Financial ratios are very important with respect to company and analysis of its

performance. These can also be used as benchmark with respect to measurement of company's

performance. As there are various kinds of financial ratio including profitability, liquidity,

solvency and various other so with the analysis of these ratios financial position of the company

can be determined easily (Kadim, Sunardi and Husain, 2020). As liquidity ratio including current

and quick ratio enable the company to determine its liquidity in terms of payment of short term

obligations will be determined. Likewise, with the calculation of profitability ratio including net

or gross profit, company's capability in terms of profitability will be analysed. However, with the

calculation of solvency ratio like debt to equity, interest coverage and various others, company

can determine its capacity with respect to the repayment of its long term obligations. In addition,

Income statement:

It is an important statement which shows the income and expenditure associated with the

company (Statements, 2020). Through this statement company can analyse that whether it is

making profit or loss. In short financial health of the company can be determined with these

statements.

Statement of cash flow:

This statement is used to analyse the company's cash flow position. This means that

through this statement company can determine its cash inflows and outflows.

Balance sheet:

It refers to that statement by which adequate reporting related with company's assets,

liabilities and shareholder equity related details can be analysed. It is usually prepared at the end

of the financial year (Daniel, Marioara and Isabela, 2017).

Statements of shareholders' equity:

It is part of balance sheet which shows changes in the share value of stockholders and the

equity shareholders. Changes in ownership interest will also be analysed with this statements.

Financial ratio:

These are the ratio which are financially evolved and related. These ratios are the

depiction of the company financial performance. Ratios are calculated on the basis of analysis of

the financial statements.

Importance:

Financial ratios are very important with respect to company and analysis of its

performance. These can also be used as benchmark with respect to measurement of company's

performance. As there are various kinds of financial ratio including profitability, liquidity,

solvency and various other so with the analysis of these ratios financial position of the company

can be determined easily (Kadim, Sunardi and Husain, 2020). As liquidity ratio including current

and quick ratio enable the company to determine its liquidity in terms of payment of short term

obligations will be determined. Likewise, with the calculation of profitability ratio including net

or gross profit, company's capability in terms of profitability will be analysed. However, with the

calculation of solvency ratio like debt to equity, interest coverage and various others, company

can determine its capacity with respect to the repayment of its long term obligations. In addition,

of this with the help of ratio analysis, company can make measurement of its performance with

regard to other companies and in case of any discrepancies corrective actions will be taken.

Thus, it would not be wrong to said that the financial ratios plays an important role with

respect to financial management. This is because it will act as base that will lead to have

financial planning and management of finance as per derived outcome of the financial ratio.

Section 3: Templates

(iv) Analysis:

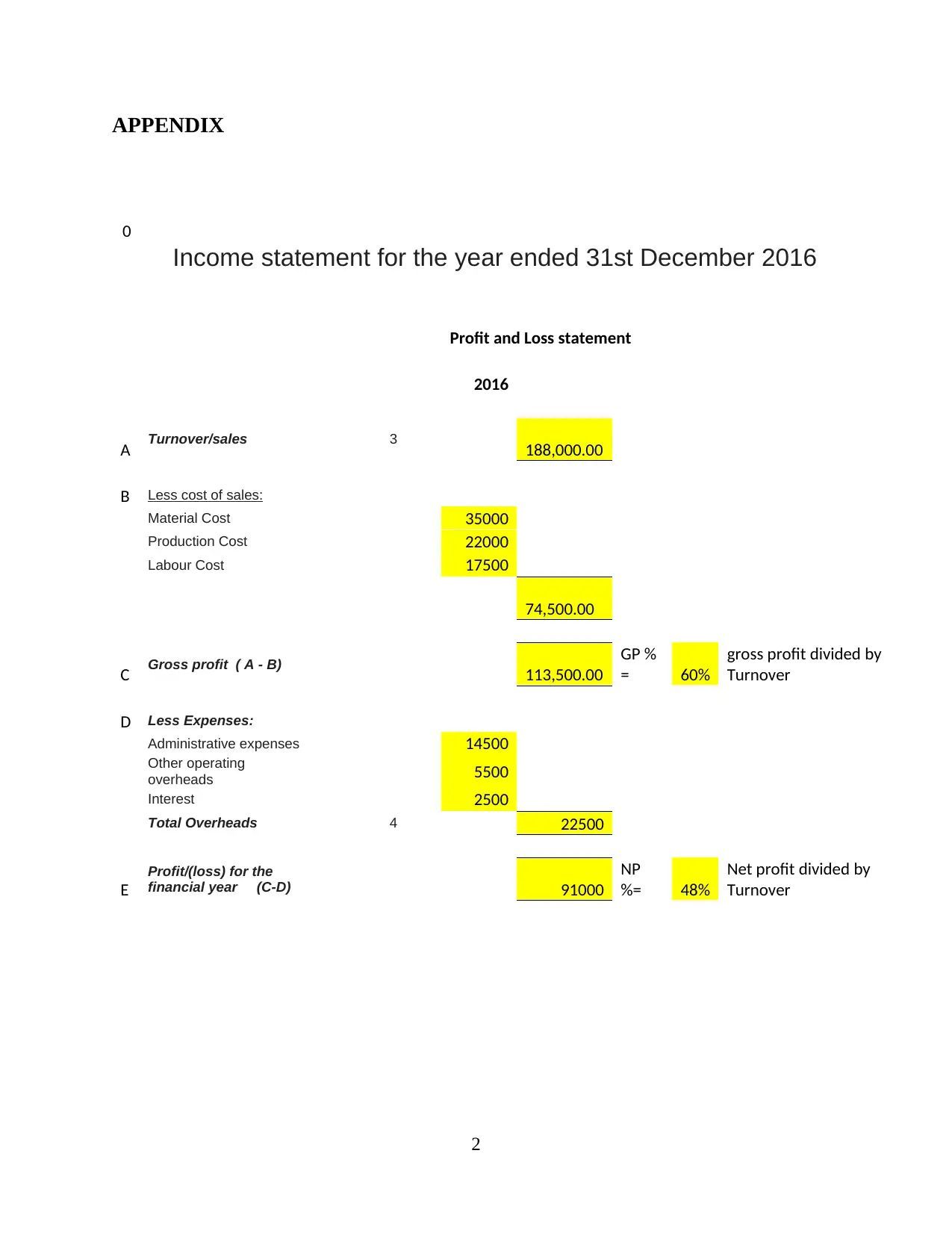

Profitability:

It is an important aspect with regard to company and its performance. A company with a

good percentage of profitability and profit percentage would indicate efficient performance. This

means that the company is running its business in profitability state. As the main objective of

every company is to earn profits and if the company's profitability state is showing a rising phase

then it means that the company is grabbing and directing towards its objectives. This can further

be understood with the profitability ratio that may include the gross profit and net profit ratio. As

the gross profit is the ratio of gross profit and turnover which shows that the amount of money

which is being left after having a deduction of cost of production. However, in case of net profit,

it is an indication of the actual and net profit which is being left after having a deduction of all

the expenses.

From the information and analysis of the case study it is being found that the gross profit of the

company is 60% while its net profit is 48%. This means that the profitability of the company is

showing a positive indication.

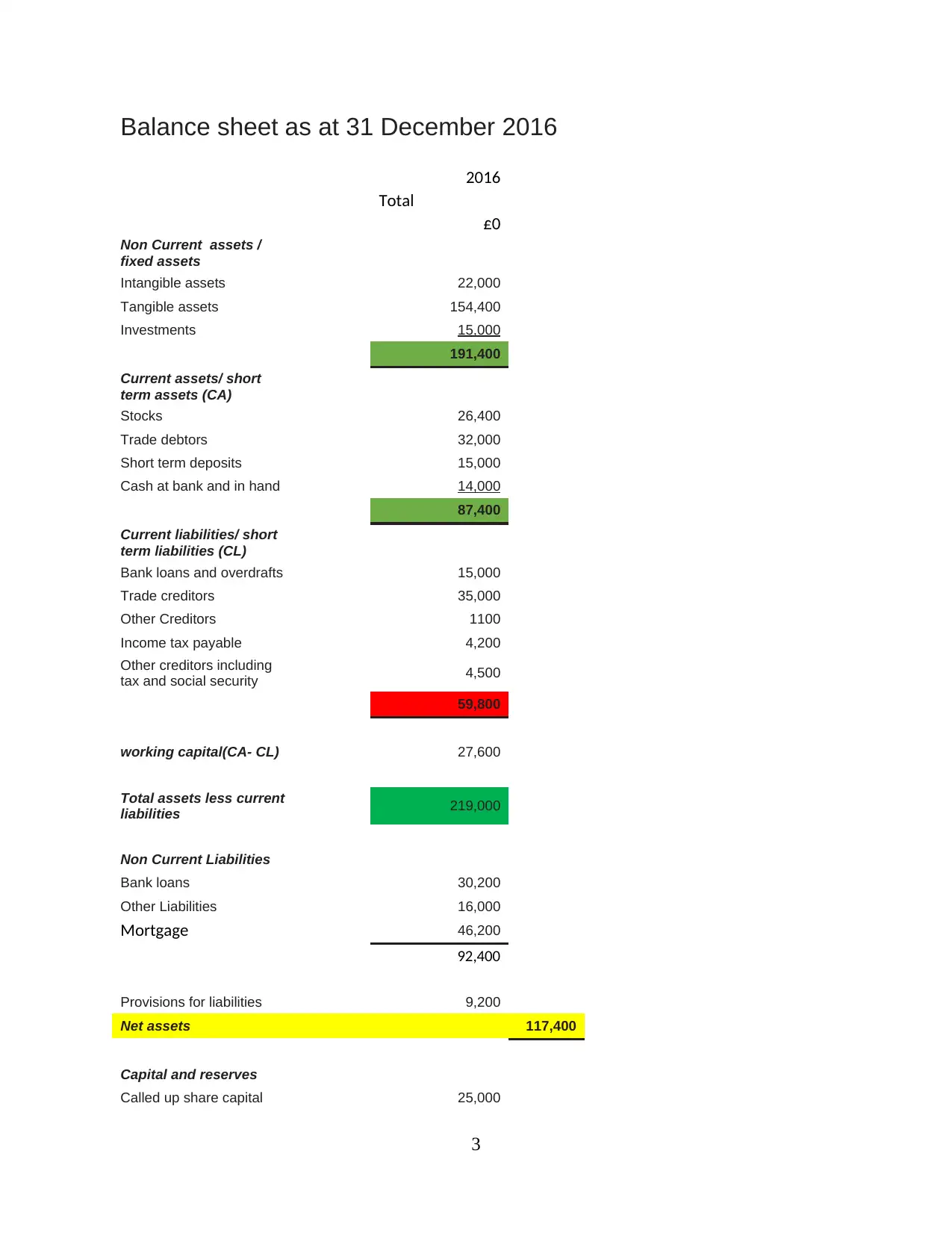

Liquidity:

This is also an important aspect with regard to company. This aspect shows the amount of

cash and cash condition which is possessed by the company. Existence of cash enable the

company to have a capacity of meeting short term obligations. It is usually determined by

working capital efficiency amount. Working capital shows the amount of money which is

required in daily operation and business. the liquidity of the company will be determined with

the help of current ratio which is a percentage of current asset by current liabilities (Nuryani and

Sunarsi, 2020). In current case it is 1.46 (87400/59800). As the ideal ratio is 1 and the current

regard to other companies and in case of any discrepancies corrective actions will be taken.

Thus, it would not be wrong to said that the financial ratios plays an important role with

respect to financial management. This is because it will act as base that will lead to have

financial planning and management of finance as per derived outcome of the financial ratio.

Section 3: Templates

(iv) Analysis:

Profitability:

It is an important aspect with regard to company and its performance. A company with a

good percentage of profitability and profit percentage would indicate efficient performance. This

means that the company is running its business in profitability state. As the main objective of

every company is to earn profits and if the company's profitability state is showing a rising phase

then it means that the company is grabbing and directing towards its objectives. This can further

be understood with the profitability ratio that may include the gross profit and net profit ratio. As

the gross profit is the ratio of gross profit and turnover which shows that the amount of money

which is being left after having a deduction of cost of production. However, in case of net profit,

it is an indication of the actual and net profit which is being left after having a deduction of all

the expenses.

From the information and analysis of the case study it is being found that the gross profit of the

company is 60% while its net profit is 48%. This means that the profitability of the company is

showing a positive indication.

Liquidity:

This is also an important aspect with regard to company. This aspect shows the amount of

cash and cash condition which is possessed by the company. Existence of cash enable the

company to have a capacity of meeting short term obligations. It is usually determined by

working capital efficiency amount. Working capital shows the amount of money which is

required in daily operation and business. the liquidity of the company will be determined with

the help of current ratio which is a percentage of current asset by current liabilities (Nuryani and

Sunarsi, 2020). In current case it is 1.46 (87400/59800). As the ideal ratio is 1 and the current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

case shows 1.46 this means that the company has enough cash with regard to meeting its short-

term obligations.

Efficiency:

In order to determine the efficiency, various ratio related with efficiency are determined.

These ratio shows the company’s ability towards the use of assets with regard to income

generation. This means that how efficiently company may use its assets in order to generate

income. It can be best determined with the use of asset turnover ratio which shows the

company’s sales and revenue with company’s total assets. The higher the ratio would be it will

be indicating that the company is generating efficient revenue from its asset. In the current case

the value of this ratio is 1.34 (188000/139400). As the ideal ratio shows that its value must be

more than 2.5 in case of retail sector, however, in case of other companies it lies between 0.25 to

0.5. and in the current case as it is 1.34 which itself shows quite good. This means that the

company is efficiently utilizing its assets with respect to revenue generation.

Likewise, the efficiency of the company can also be determined through the accounts

receivable turnover ratio. As this ratio indicate the efficiency of the company with respect to

collection of debts from the market (Wajo, 2021). It can be calculated by net credit sales divided

by accounts receivable for a period by. In the current case this ratio is 5.87 (188000/32000). As

the ratio shows high values this means that the company efficiency with regard to debt collection

is not good and need to be improved.

Section 4: Methods of improving financial performance

As the financial performance with regard to company is is moderate and in declining state so in

order to improve its financial performance and the concerned ratio following aspects need to be

considered.

Well directed focus towards the improvement of relationship with the customers,

enabling early payment discounts and policies, improving efficiency related with billing,

inculcation of system related with reminders are some methods that will assist the

company to improve its performance and accounts receivable ratio. As this is a ratio

related with company's efficiency so with an improvised ratio, company can also puts a

positive brand image in the market.

term obligations.

Efficiency:

In order to determine the efficiency, various ratio related with efficiency are determined.

These ratio shows the company’s ability towards the use of assets with regard to income

generation. This means that how efficiently company may use its assets in order to generate

income. It can be best determined with the use of asset turnover ratio which shows the

company’s sales and revenue with company’s total assets. The higher the ratio would be it will

be indicating that the company is generating efficient revenue from its asset. In the current case

the value of this ratio is 1.34 (188000/139400). As the ideal ratio shows that its value must be

more than 2.5 in case of retail sector, however, in case of other companies it lies between 0.25 to

0.5. and in the current case as it is 1.34 which itself shows quite good. This means that the

company is efficiently utilizing its assets with respect to revenue generation.

Likewise, the efficiency of the company can also be determined through the accounts

receivable turnover ratio. As this ratio indicate the efficiency of the company with respect to

collection of debts from the market (Wajo, 2021). It can be calculated by net credit sales divided

by accounts receivable for a period by. In the current case this ratio is 5.87 (188000/32000). As

the ratio shows high values this means that the company efficiency with regard to debt collection

is not good and need to be improved.

Section 4: Methods of improving financial performance

As the financial performance with regard to company is is moderate and in declining state so in

order to improve its financial performance and the concerned ratio following aspects need to be

considered.

Well directed focus towards the improvement of relationship with the customers,

enabling early payment discounts and policies, improving efficiency related with billing,

inculcation of system related with reminders are some methods that will assist the

company to improve its performance and accounts receivable ratio. As this is a ratio

related with company's efficiency so with an improvised ratio, company can also puts a

positive brand image in the market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As it is analysed that the current ratio of company is more than 1, which means excess of

cash available for business will need to be improved and rectified with the making of

investment in the best available option. As when the funds will be invested in the best

alternatives then it will not only lead to improvement in ratio but it will further assist the

company to raise its earnings.

This means that with the improvement in current ratio and cash efficiency the company's

efficiency with regard to profitability will also be raised. Since the profitability of the

company is determining good indicators but with the controlling over expenses and

increasing the source of earning profits, the profitability situation and its net profit ratio

will be improvised.

In addition to this, with regard to improving the net profit percentage of the company, it

may focus over either raising of sales of its products or increasing the existing prices.

This means that with a raise in its sales volume company may earn more profit margin

while an increase in prices will also offer a good percentage of profits.

Along with the above steps adoption of certain strategies including making of correct

invoicing while making purchase, collection of debts as soon as possible, reduction of

expenses that are not required will also lead to have an improvement in financial

performance (Karami, Samimi and Jafari, 2020). Likewise, availing raw material,

consolidation of debts at better rate, availing periodic payments will further lead to have

an improvement in its performance.

CONCLUSION

From the above report it is analysed that the financial management and its implication

along with preparation of financial statement's plays an important role with respect to company

and its directed activities towards its objectives. With the preparation of financial statement's,

financial ability and position of the company will be determined and accordingly most

appropriate actions with respect tom raising and improvising the company existing position will

be taken. Like the preparation of financial statements, ratio analysis also enable the company to

have an analysis of its financial performance.

cash available for business will need to be improved and rectified with the making of

investment in the best available option. As when the funds will be invested in the best

alternatives then it will not only lead to improvement in ratio but it will further assist the

company to raise its earnings.

This means that with the improvement in current ratio and cash efficiency the company's

efficiency with regard to profitability will also be raised. Since the profitability of the

company is determining good indicators but with the controlling over expenses and

increasing the source of earning profits, the profitability situation and its net profit ratio

will be improvised.

In addition to this, with regard to improving the net profit percentage of the company, it

may focus over either raising of sales of its products or increasing the existing prices.

This means that with a raise in its sales volume company may earn more profit margin

while an increase in prices will also offer a good percentage of profits.

Along with the above steps adoption of certain strategies including making of correct

invoicing while making purchase, collection of debts as soon as possible, reduction of

expenses that are not required will also lead to have an improvement in financial

performance (Karami, Samimi and Jafari, 2020). Likewise, availing raw material,

consolidation of debts at better rate, availing periodic payments will further lead to have

an improvement in its performance.

CONCLUSION

From the above report it is analysed that the financial management and its implication

along with preparation of financial statement's plays an important role with respect to company

and its directed activities towards its objectives. With the preparation of financial statement's,

financial ability and position of the company will be determined and accordingly most

appropriate actions with respect tom raising and improvising the company existing position will

be taken. Like the preparation of financial statements, ratio analysis also enable the company to

have an analysis of its financial performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Brigham, E.F. and Houston, J.F., 2021. Fundamentals of financial management. Cengage

Learning.

Damayanti, S.M., Murtaqi, I. and Pradana, H.A., 2018. The importance of financial literacy in a

global economic era. The Business & Management Review. 9(3). pp.435-441.

Daniel, A.C., Marioara, A. and Isabela, D., 2017. Annual Financial Statements as a Financial

Communication Support. Ovidius University Annals, Economic Sciences Series. 17(1).

pp.403-406.

Kadim, A., Sunardi, N. and Husain, T., 2020. The modeling firm's value based on financial

ratios, intellectual capital and dividend policy. Accounting. 6(5). pp.859-870.

Karami, M., Samimi, A. and Jafari, M., 2020. The impact of effective risk management on

corporate financial performance. Advanced Journal of Chemistry-Section B. 2(3).

pp.144-150.

Nuryani, Y. and Sunarsi, D., 2020. The Effect of Current Ratio and Debt to Equity Ratio on

Deviding Growth. JASa (Jurnal Akuntansi, Audit dan Sistem Informasi Akuntansi). 4(2).

pp.304-312.

Osadchy, and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

Siekelova, and et.al., 2017. Receivables management: the importance of financial indicators in

assessing the creditworthiness. Polish Journal of Management Studies. 15.

Statements, W.F., 2020. Introduction to Financial Statements Analysis.

Wajo, A.R., 2021. Effect of Cash Turnover, Receivable Turnover, Inventory Turnover and

Growth Opportunity on Profitability. ATESTASI: Jurnal Ilmiah Akuntansi. 4(1). pp.61-

69.

1

Books and journals

Brigham, E.F. and Houston, J.F., 2021. Fundamentals of financial management. Cengage

Learning.

Damayanti, S.M., Murtaqi, I. and Pradana, H.A., 2018. The importance of financial literacy in a

global economic era. The Business & Management Review. 9(3). pp.435-441.

Daniel, A.C., Marioara, A. and Isabela, D., 2017. Annual Financial Statements as a Financial

Communication Support. Ovidius University Annals, Economic Sciences Series. 17(1).

pp.403-406.

Kadim, A., Sunardi, N. and Husain, T., 2020. The modeling firm's value based on financial

ratios, intellectual capital and dividend policy. Accounting. 6(5). pp.859-870.

Karami, M., Samimi, A. and Jafari, M., 2020. The impact of effective risk management on

corporate financial performance. Advanced Journal of Chemistry-Section B. 2(3).

pp.144-150.

Nuryani, Y. and Sunarsi, D., 2020. The Effect of Current Ratio and Debt to Equity Ratio on

Deviding Growth. JASa (Jurnal Akuntansi, Audit dan Sistem Informasi Akuntansi). 4(2).

pp.304-312.

Osadchy, and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

Siekelova, and et.al., 2017. Receivables management: the importance of financial indicators in

assessing the creditworthiness. Polish Journal of Management Studies. 15.

Statements, W.F., 2020. Introduction to Financial Statements Analysis.

Wajo, A.R., 2021. Effect of Cash Turnover, Receivable Turnover, Inventory Turnover and

Growth Opportunity on Profitability. ATESTASI: Jurnal Ilmiah Akuntansi. 4(1). pp.61-

69.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

0

Income statement for the year ended 31st December 2016

Profit and Loss statement

2016

A Turnover/sales 3 188,000.00

B Less cost of sales:

Material Cost 35000

Production Cost 22000

Labour Cost 17500

74,500.00

C Gross profit ( A - B) 113,500.00

GP %

= 60%

gross profit divided by

Turnover

D Less Expenses:

Administrative expenses 14500

Other operating

overheads 5500

Interest 2500

Total Overheads 4 22500

E

Profit/(loss) for the

financial year (C-D) 91000

NP

%= 48%

Net profit divided by

Turnover

2

0

Income statement for the year ended 31st December 2016

Profit and Loss statement

2016

A Turnover/sales 3 188,000.00

B Less cost of sales:

Material Cost 35000

Production Cost 22000

Labour Cost 17500

74,500.00

C Gross profit ( A - B) 113,500.00

GP %

= 60%

gross profit divided by

Turnover

D Less Expenses:

Administrative expenses 14500

Other operating

overheads 5500

Interest 2500

Total Overheads 4 22500

E

Profit/(loss) for the

financial year (C-D) 91000

NP

%= 48%

Net profit divided by

Turnover

2

Balance sheet as at 31 December 2016

2016

Total

£0

Non Current assets /

fixed assets

Intangible assets 22,000

Tangible assets 154,400

Investments 15,000

191,400

Current assets/ short

term assets (CA)

Stocks 26,400

Trade debtors 32,000

Short term deposits 15,000

Cash at bank and in hand 14,000

87,400

Current liabilities/ short

term liabilities (CL)

Bank loans and overdrafts 15,000

Trade creditors 35,000

Other Creditors 1100

Income tax payable 4,200

Other creditors including

tax and social security 4,500

59,800

working capital(CA- CL) 27,600

Total assets less current

liabilities 219,000

Non Current Liabilities

Bank loans 30,200

Other Liabilities 16,000

Mortgage 46,200

92,400

Provisions for liabilities 9,200

Net assets 117,400

Capital and reserves

Called up share capital 25,000

3

2016

Total

£0

Non Current assets /

fixed assets

Intangible assets 22,000

Tangible assets 154,400

Investments 15,000

191,400

Current assets/ short

term assets (CA)

Stocks 26,400

Trade debtors 32,000

Short term deposits 15,000

Cash at bank and in hand 14,000

87,400

Current liabilities/ short

term liabilities (CL)

Bank loans and overdrafts 15,000

Trade creditors 35,000

Other Creditors 1100

Income tax payable 4,200

Other creditors including

tax and social security 4,500

59,800

working capital(CA- CL) 27,600

Total assets less current

liabilities 219,000

Non Current Liabilities

Bank loans 30,200

Other Liabilities 16,000

Mortgage 46,200

92,400

Provisions for liabilities 9,200

Net assets 117,400

Capital and reserves

Called up share capital 25,000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.