University Business Finance Report: Investment, Financing Decisions

VerifiedAdded on 2022/11/26

|10

|2197

|396

Report

AI Summary

This report provides a detailed analysis of business finance, focusing on investment decisions and financing strategies. Part A evaluates a project using techniques like Net Present Value (NPV), Internal Rate of Return (IRR), payback period, and profitability index, concluding the project is financially viable. Part B explores financing decisions, specifically dividend policy and capital structure, critiquing the Modigliani and Miller theorem. It discusses the theorem's propositions, assumptions, and limitations in the context of real-world factors such as taxes and bankruptcy, concluding that the theorem is not fully applicable in contemporary market conditions. The report includes a comprehensive financial analysis and references relevant literature to support its findings.

Running head: BUSINESS FINANCE

Business Finance

Name of the Student:

Name of the University:

Authors Note:

Business Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

1

Table of Contents

Part A: Investment Decision- Project evaluation.......................................................................2

Part B: Financing Decisions – Dividend policy and capital structure.......................................3

Reference and Bibliography:......................................................................................................8

1

Table of Contents

Part A: Investment Decision- Project evaluation.......................................................................2

Part B: Financing Decisions – Dividend policy and capital structure.......................................3

Reference and Bibliography:......................................................................................................8

BUSINESS FINANCE

2

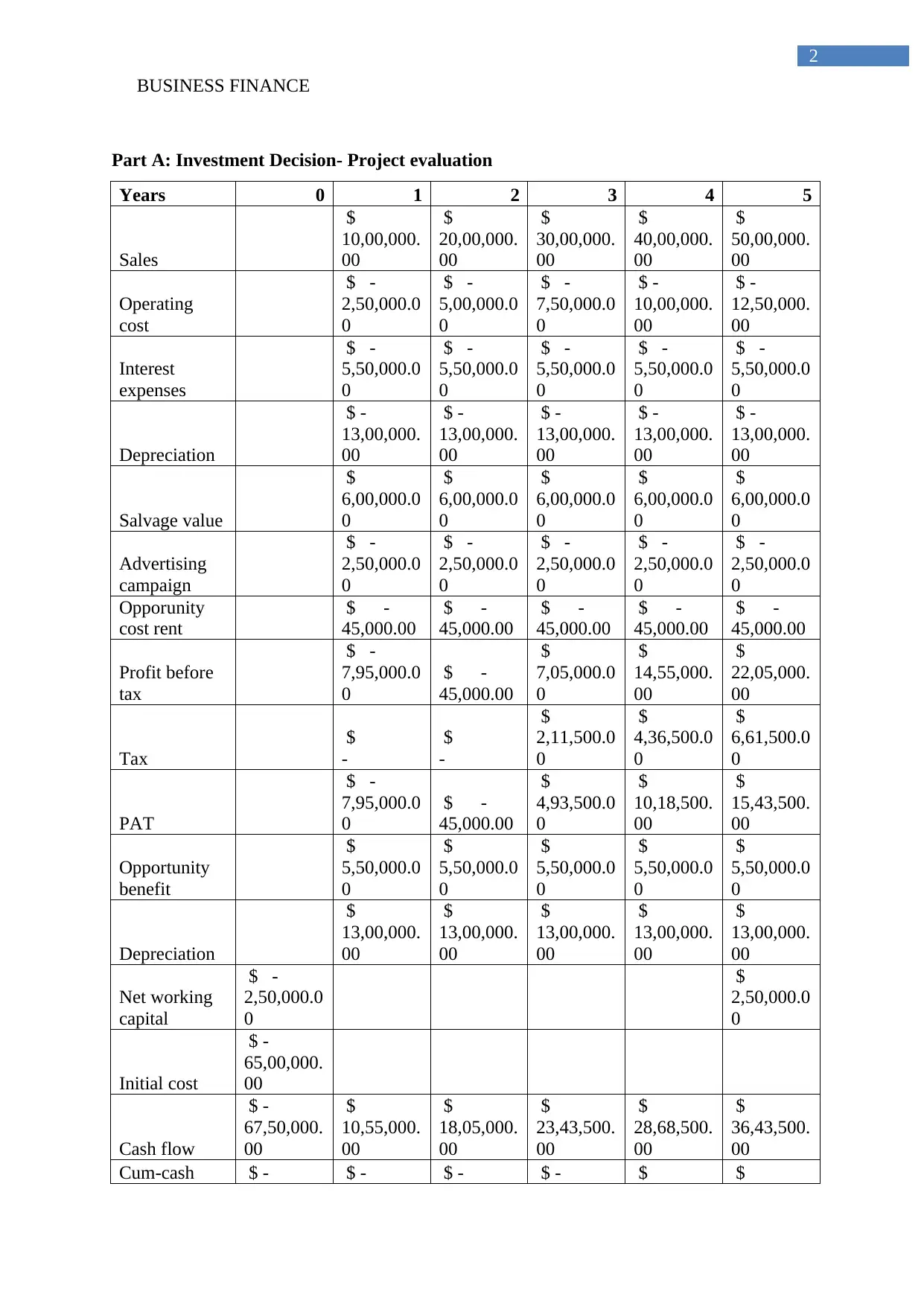

Part A: Investment Decision- Project evaluation

Years 0 1 2 3 4 5

Sales

$

10,00,000.

00

$

20,00,000.

00

$

30,00,000.

00

$

40,00,000.

00

$

50,00,000.

00

Operating

cost

$ -

2,50,000.0

0

$ -

5,00,000.0

0

$ -

7,50,000.0

0

$ -

10,00,000.

00

$ -

12,50,000.

00

Interest

expenses

$ -

5,50,000.0

0

$ -

5,50,000.0

0

$ -

5,50,000.0

0

$ -

5,50,000.0

0

$ -

5,50,000.0

0

Depreciation

$ -

13,00,000.

00

$ -

13,00,000.

00

$ -

13,00,000.

00

$ -

13,00,000.

00

$ -

13,00,000.

00

Salvage value

$

6,00,000.0

0

$

6,00,000.0

0

$

6,00,000.0

0

$

6,00,000.0

0

$

6,00,000.0

0

Advertising

campaign

$ -

2,50,000.0

0

$ -

2,50,000.0

0

$ -

2,50,000.0

0

$ -

2,50,000.0

0

$ -

2,50,000.0

0

Opporunity

cost rent

$ -

45,000.00

$ -

45,000.00

$ -

45,000.00

$ -

45,000.00

$ -

45,000.00

Profit before

tax

$ -

7,95,000.0

0

$ -

45,000.00

$

7,05,000.0

0

$

14,55,000.

00

$

22,05,000.

00

Tax

$

-

$

-

$

2,11,500.0

0

$

4,36,500.0

0

$

6,61,500.0

0

PAT

$ -

7,95,000.0

0

$ -

45,000.00

$

4,93,500.0

0

$

10,18,500.

00

$

15,43,500.

00

Opportunity

benefit

$

5,50,000.0

0

$

5,50,000.0

0

$

5,50,000.0

0

$

5,50,000.0

0

$

5,50,000.0

0

Depreciation

$

13,00,000.

00

$

13,00,000.

00

$

13,00,000.

00

$

13,00,000.

00

$

13,00,000.

00

Net working

capital

$ -

2,50,000.0

0

$

2,50,000.0

0

Initial cost

$ -

65,00,000.

00

Cash flow

$ -

67,50,000.

00

$

10,55,000.

00

$

18,05,000.

00

$

23,43,500.

00

$

28,68,500.

00

$

36,43,500.

00

Cum-cash $ - $ - $ - $ - $ $

2

Part A: Investment Decision- Project evaluation

Years 0 1 2 3 4 5

Sales

$

10,00,000.

00

$

20,00,000.

00

$

30,00,000.

00

$

40,00,000.

00

$

50,00,000.

00

Operating

cost

$ -

2,50,000.0

0

$ -

5,00,000.0

0

$ -

7,50,000.0

0

$ -

10,00,000.

00

$ -

12,50,000.

00

Interest

expenses

$ -

5,50,000.0

0

$ -

5,50,000.0

0

$ -

5,50,000.0

0

$ -

5,50,000.0

0

$ -

5,50,000.0

0

Depreciation

$ -

13,00,000.

00

$ -

13,00,000.

00

$ -

13,00,000.

00

$ -

13,00,000.

00

$ -

13,00,000.

00

Salvage value

$

6,00,000.0

0

$

6,00,000.0

0

$

6,00,000.0

0

$

6,00,000.0

0

$

6,00,000.0

0

Advertising

campaign

$ -

2,50,000.0

0

$ -

2,50,000.0

0

$ -

2,50,000.0

0

$ -

2,50,000.0

0

$ -

2,50,000.0

0

Opporunity

cost rent

$ -

45,000.00

$ -

45,000.00

$ -

45,000.00

$ -

45,000.00

$ -

45,000.00

Profit before

tax

$ -

7,95,000.0

0

$ -

45,000.00

$

7,05,000.0

0

$

14,55,000.

00

$

22,05,000.

00

Tax

$

-

$

-

$

2,11,500.0

0

$

4,36,500.0

0

$

6,61,500.0

0

PAT

$ -

7,95,000.0

0

$ -

45,000.00

$

4,93,500.0

0

$

10,18,500.

00

$

15,43,500.

00

Opportunity

benefit

$

5,50,000.0

0

$

5,50,000.0

0

$

5,50,000.0

0

$

5,50,000.0

0

$

5,50,000.0

0

Depreciation

$

13,00,000.

00

$

13,00,000.

00

$

13,00,000.

00

$

13,00,000.

00

$

13,00,000.

00

Net working

capital

$ -

2,50,000.0

0

$

2,50,000.0

0

Initial cost

$ -

65,00,000.

00

Cash flow

$ -

67,50,000.

00

$

10,55,000.

00

$

18,05,000.

00

$

23,43,500.

00

$

28,68,500.

00

$

36,43,500.

00

Cum-cash $ - $ - $ - $ - $ $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

3

flow

67,50,000.

00

56,95,000.

00

38,90,000.

00

15,46,500.

00

13,22,000.

00

49,65,500.

00

NPV $ 19,46,877.01

IRR 17.67%

Payback period 3.5 Years

Profitability index 1.29

The above table provides information about the overall investment appraisal

techniques, which has been used for detecting the financial viability of the investment. From

the relevant evaluation, it can be identified that investment option in the project is viable, as

the NPV value is considered to be positive. In addition, relevant confirmation is provided by

the internal rate of return of the project, which is at the levels of 17.67%, and is higher than

the cost of capital assumed for the analysis. Moreover, the payback period is less than 5

years, which indicates the financial viability of the investment option. Lastly, the profitability

index is higher than one, which directly depicts that Investment in the project would directly

allow the organisation to increase profitability in the long run (Baum and Crosby 2014).

The positive net present value directly indicates that the time value of money will not

erode the benefits that would be generated by the project of the period of time. Hence, the

initial investment conducted for the project can be e obtained without hindering the benefits

provided by the investment. Thus, it could be understood that investments in the project

would be beneficial for the organisation, as it would generate higher revenues and cash

inflow in the long run (Harris 2017).

Part B: Financing Decisions – Dividend policy and capital structure

Modigliani and Miller suggested an adequate dividend irrelevance and capital

structure theory, which states that in a Perfect World with no taxes of bankruptcy condition

there is no impact of dividend policy of capital structure on the share price of an organization.

The assumptions made by Modigliani and Miller was relatively considered to be inaccurate

3

flow

67,50,000.

00

56,95,000.

00

38,90,000.

00

15,46,500.

00

13,22,000.

00

49,65,500.

00

NPV $ 19,46,877.01

IRR 17.67%

Payback period 3.5 Years

Profitability index 1.29

The above table provides information about the overall investment appraisal

techniques, which has been used for detecting the financial viability of the investment. From

the relevant evaluation, it can be identified that investment option in the project is viable, as

the NPV value is considered to be positive. In addition, relevant confirmation is provided by

the internal rate of return of the project, which is at the levels of 17.67%, and is higher than

the cost of capital assumed for the analysis. Moreover, the payback period is less than 5

years, which indicates the financial viability of the investment option. Lastly, the profitability

index is higher than one, which directly depicts that Investment in the project would directly

allow the organisation to increase profitability in the long run (Baum and Crosby 2014).

The positive net present value directly indicates that the time value of money will not

erode the benefits that would be generated by the project of the period of time. Hence, the

initial investment conducted for the project can be e obtained without hindering the benefits

provided by the investment. Thus, it could be understood that investments in the project

would be beneficial for the organisation, as it would generate higher revenues and cash

inflow in the long run (Harris 2017).

Part B: Financing Decisions – Dividend policy and capital structure

Modigliani and Miller suggested an adequate dividend irrelevance and capital

structure theory, which states that in a Perfect World with no taxes of bankruptcy condition

there is no impact of dividend policy of capital structure on the share price of an organization.

The assumptions made by Modigliani and Miller was relatively considered to be inaccurate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

4

adjust it did not compensate the conditions of taxes and bankruptcy which might incur due to

the alterations in capital structure. moreover the Dividend policy and capital structure assume

by mm theory directly States about the relevant Perfect World which does not comply current

market situation as it ignores the assumptions that has been made by the analyst (Cline 2015).

The Modigliani and Miller Theorem directly utilize three different propositions, which

describe the overall impact of Capital structure on the share price performance of the

organization. The first proposition directly indicates that firm total market value is

independent of its capital structure, where the second proposition directly indicates about the

cost of equity increases with the debt equity ratio. Lastly, the third proposition directly

indicates that the firm’s total market value is independent of its Dividend policy. The three

propositions are depicted as follows.

First proposition- Irrelevance of the capital structure

The first proposition provided by the Modigliani and Miller theory of capital

structure, where it is detected that the capital structure of form does not influence its market

value. However, the theorem directly encourages some relevant assumptions that should be

conducted, which are that under certain conditions where debt to equity ratio performance

does not affect the overall firms market value. Functions made by Modigliani in the theorem

is regarding the perfect capital market conditions investors buy and sell securities freely

without any kind of such as brokers commission and transfer fees (Ahmeti and Prenaj 2015).

Additionally, the theorem also indicates that all the relevant information a directory presented

to the investors regarding the decisions made by the organization. However, the theory

directly violates the current real market conditions where adequate brokerage and transfer

fees need to be conducted by the investors for each and every trade. Moreover, the

information provided by the organization related takes time the investors, which is relatively

alters the share price of the organization and does not benefit some of the investors.

4

adjust it did not compensate the conditions of taxes and bankruptcy which might incur due to

the alterations in capital structure. moreover the Dividend policy and capital structure assume

by mm theory directly States about the relevant Perfect World which does not comply current

market situation as it ignores the assumptions that has been made by the analyst (Cline 2015).

The Modigliani and Miller Theorem directly utilize three different propositions, which

describe the overall impact of Capital structure on the share price performance of the

organization. The first proposition directly indicates that firm total market value is

independent of its capital structure, where the second proposition directly indicates about the

cost of equity increases with the debt equity ratio. Lastly, the third proposition directly

indicates that the firm’s total market value is independent of its Dividend policy. The three

propositions are depicted as follows.

First proposition- Irrelevance of the capital structure

The first proposition provided by the Modigliani and Miller theory of capital

structure, where it is detected that the capital structure of form does not influence its market

value. However, the theorem directly encourages some relevant assumptions that should be

conducted, which are that under certain conditions where debt to equity ratio performance

does not affect the overall firms market value. Functions made by Modigliani in the theorem

is regarding the perfect capital market conditions investors buy and sell securities freely

without any kind of such as brokers commission and transfer fees (Ahmeti and Prenaj 2015).

Additionally, the theorem also indicates that all the relevant information a directory presented

to the investors regarding the decisions made by the organization. However, the theory

directly violates the current real market conditions where adequate brokerage and transfer

fees need to be conducted by the investors for each and every trade. Moreover, the

information provided by the organization related takes time the investors, which is relatively

alters the share price of the organization and does not benefit some of the investors.

BUSINESS FINANCE

5

The theorem directly excludes the payment of taxes and interest conducted by the

firm. This condition is relatively not suitable in the real-world practices where adequate taxes

and interest needs to be paid by the organization. Moreover, the theorem also indicates that

additional that in the capital structure is more valuable as companies are able to acquire

adequate tax Shield effect from the rising debt in their capital structure (Gersbach, Haller and

Müller 2015). Assumptions made by the theorem is relatively adequate where with higher

debt conditions the company is able to increase tax shield, whereas it also raises the level of

debt to equity ratio and insolvency condition. The financial position of the organization will

not remain same, as alteration in the revenue generation capability, would negatively affect

the company's overall profits, as fixed interest rate needs to be paid due to the accumulation

of high debt. Therefore, companies having high debt in the capital structure are not

considered valuable in Real world scenarios.

Second proposition- Rate of Return on Equity

The second position is relatively related to the rate of return on equity, where the

model directly indicates that alterations in return on equity of the organization do not affect

the actual value of the firm. Moreover, Modigliani indicated that the weighted average cost of

capital is not affected by its leverage conditions, as the increment in debt to equity ratio

directly raises the level of cost of equity. Furthermore theorem also indicates that investors

are rational increment in the cost of capital of the organization does not increase any kind of

company value. However, the proposition is a relatively based on the tax conditions and laws

of a country where any changes in the country's regulations directly invalidate the overall

theorem of Modigliani (Charness and Neugebauer 2019).

Third proposition- Irreverence of Dividend policy

The third proposition directly indicates that the firm's total market value is not

affected by dividend policy, where growth and valuation of shares is not interrelated, which

5

The theorem directly excludes the payment of taxes and interest conducted by the

firm. This condition is relatively not suitable in the real-world practices where adequate taxes

and interest needs to be paid by the organization. Moreover, the theorem also indicates that

additional that in the capital structure is more valuable as companies are able to acquire

adequate tax Shield effect from the rising debt in their capital structure (Gersbach, Haller and

Müller 2015). Assumptions made by the theorem is relatively adequate where with higher

debt conditions the company is able to increase tax shield, whereas it also raises the level of

debt to equity ratio and insolvency condition. The financial position of the organization will

not remain same, as alteration in the revenue generation capability, would negatively affect

the company's overall profits, as fixed interest rate needs to be paid due to the accumulation

of high debt. Therefore, companies having high debt in the capital structure are not

considered valuable in Real world scenarios.

Second proposition- Rate of Return on Equity

The second position is relatively related to the rate of return on equity, where the

model directly indicates that alterations in return on equity of the organization do not affect

the actual value of the firm. Moreover, Modigliani indicated that the weighted average cost of

capital is not affected by its leverage conditions, as the increment in debt to equity ratio

directly raises the level of cost of equity. Furthermore theorem also indicates that investors

are rational increment in the cost of capital of the organization does not increase any kind of

company value. However, the proposition is a relatively based on the tax conditions and laws

of a country where any changes in the country's regulations directly invalidate the overall

theorem of Modigliani (Charness and Neugebauer 2019).

Third proposition- Irreverence of Dividend policy

The third proposition directly indicates that the firm's total market value is not

affected by dividend policy, where growth and valuation of shares is not interrelated, which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

6

does not have any kind of impact on the significance for the valuation of a firm. Modigliani

directly argued that the market value of a firm is determined by its earnings power and the

risk that is affecting the underlying Assets of the organization. However, the theorem of

Modigliani is not supported in real world practices, as dividend policy have a direct impact

on the overall evaluation of an organization. There are different types of models and

calculation such as dividend discount model, which directly utilizes the evidence provided by

the company to determine the level of share price for the company in future (Hugonnier,

Malamud and Morellec 2014). The current Dividend policy and dividend payments that are

conducted by the organization directly state about the relevant demand for the share price of

an organization. The demand for high dividend value stocks relatively increase due to the

possibility of higher returns that will be generated by the investors from their exposure.

Hence, it could be criticize that the overall theorem of Modigliani is relatively not adequate in

current real word practices where Dividend policy has a direct impact on the share price and

valuation of a company.

Therefore, after evaluating the Dividend policy and capital structure of Modigliani

and Miller, it could be identified that there are relevant corporate tax consideration and form

value in contemporary world that needs to be taken into consideration (Maina and Ishmail

2014). The company has a relevant corporate tax rate that alters the overall value of the firm,

as they are not able to provide adequate dividends to the investors. Theorem used by

Modigliani and Miller does not support the current market conditions where the capital

structure and dividend policy maintained by the organization directly affects valuation. The

high level of corporate taxes would directly reduce the level of retained incomes by the

organization, which in turn would affect the level of dividends that is paid to investors.

Alteration in the Dividend policy conditions of the organization has direct impact on the

demand for shares, which in turn alters the firm valuation. Thus, the theorem of Modigliani

6

does not have any kind of impact on the significance for the valuation of a firm. Modigliani

directly argued that the market value of a firm is determined by its earnings power and the

risk that is affecting the underlying Assets of the organization. However, the theorem of

Modigliani is not supported in real world practices, as dividend policy have a direct impact

on the overall evaluation of an organization. There are different types of models and

calculation such as dividend discount model, which directly utilizes the evidence provided by

the company to determine the level of share price for the company in future (Hugonnier,

Malamud and Morellec 2014). The current Dividend policy and dividend payments that are

conducted by the organization directly state about the relevant demand for the share price of

an organization. The demand for high dividend value stocks relatively increase due to the

possibility of higher returns that will be generated by the investors from their exposure.

Hence, it could be criticize that the overall theorem of Modigliani is relatively not adequate in

current real word practices where Dividend policy has a direct impact on the share price and

valuation of a company.

Therefore, after evaluating the Dividend policy and capital structure of Modigliani

and Miller, it could be identified that there are relevant corporate tax consideration and form

value in contemporary world that needs to be taken into consideration (Maina and Ishmail

2014). The company has a relevant corporate tax rate that alters the overall value of the firm,

as they are not able to provide adequate dividends to the investors. Theorem used by

Modigliani and Miller does not support the current market conditions where the capital

structure and dividend policy maintained by the organization directly affects valuation. The

high level of corporate taxes would directly reduce the level of retained incomes by the

organization, which in turn would affect the level of dividends that is paid to investors.

Alteration in the Dividend policy conditions of the organization has direct impact on the

demand for shares, which in turn alters the firm valuation. Thus, the theorem of Modigliani

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

7

and Miller can only be successful under specific terms and condition, where the in real world

practices the assumptions made by the theories become invalid and does not support both the

dividend policy and capital structure conditions.

7

and Miller can only be successful under specific terms and condition, where the in real world

practices the assumptions made by the theories become invalid and does not support both the

dividend policy and capital structure conditions.

BUSINESS FINANCE

8

Reference and Bibliography:

Ahmeti, F. and Prenaj, B., 2015. A critical review of Modigliani and Miller’s theorem of

capital structure. International Journal of Economics, Commerce and Management

(IJECM), 3(6).

Aktas, R., Acikalin, S., Bakin, B. and Celik, G., 2015. The Determinants of Banks' Capital

Adequacy Ratio: Some Evidence from South Eastern European Countries. Journal of

Economics and Behavioral Studies, 7(1), p.79.

Baltacı, N. and Ayaydın, H., 2014. Firm, country and macroeconomic determinants of capital

structure: Evidence from Turkish banking sector. EMAJ: Emerging Markets Journal, 3(3),

pp.47-58.

Baum, A.E. and Crosby, N., 2014. Property investment appraisal. John Wiley & Sons.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. Inflation in Brusov–

Filatova–Orekhova Theory and in Its Perpetuity Limit Modigliani–Miller Theory. In Modern

Corporate Finance, Investments, Taxation and Ratings (pp. 161-179). Springer, Cham.

Charness, G. and Neugebauer, T., 2019. A Test of the Modigliani‐Miller Invariance Theorem

and Arbitrage in Experimental Asset Markets. The Journal of Finance, 74(1), pp.493-529.

Cline, W.R., 2015. Testing the Modigliani-Miller theorem of capital structure irrelevance for

banks. Peterson Institute for International Economics Working Paper, (15-8).

Gersbach, H., Haller, H. and Müller, J., 2015. The macroeconomics of Modigliani–

Miller. Journal of Economic Theory, 157, pp.1081-1113.

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

8

Reference and Bibliography:

Ahmeti, F. and Prenaj, B., 2015. A critical review of Modigliani and Miller’s theorem of

capital structure. International Journal of Economics, Commerce and Management

(IJECM), 3(6).

Aktas, R., Acikalin, S., Bakin, B. and Celik, G., 2015. The Determinants of Banks' Capital

Adequacy Ratio: Some Evidence from South Eastern European Countries. Journal of

Economics and Behavioral Studies, 7(1), p.79.

Baltacı, N. and Ayaydın, H., 2014. Firm, country and macroeconomic determinants of capital

structure: Evidence from Turkish banking sector. EMAJ: Emerging Markets Journal, 3(3),

pp.47-58.

Baum, A.E. and Crosby, N., 2014. Property investment appraisal. John Wiley & Sons.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. Inflation in Brusov–

Filatova–Orekhova Theory and in Its Perpetuity Limit Modigliani–Miller Theory. In Modern

Corporate Finance, Investments, Taxation and Ratings (pp. 161-179). Springer, Cham.

Charness, G. and Neugebauer, T., 2019. A Test of the Modigliani‐Miller Invariance Theorem

and Arbitrage in Experimental Asset Markets. The Journal of Finance, 74(1), pp.493-529.

Cline, W.R., 2015. Testing the Modigliani-Miller theorem of capital structure irrelevance for

banks. Peterson Institute for International Economics Working Paper, (15-8).

Gersbach, H., Haller, H. and Müller, J., 2015. The macroeconomics of Modigliani–

Miller. Journal of Economic Theory, 157, pp.1081-1113.

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

9

Hugonnier, J., Malamud, S. and Morellec, E., 2014. Capital supply uncertainty, cash

holdings, and investment. The Review of Financial Studies, 28(2), pp.391-445.

Maina, L. and Ishmail, M., 2014. Capital structure and financial performance in Kenya:

Evidence from firms listed at the Nairobi Securities Exchange. International Journal of

Social Sciences and Entrepreneurship, 1(11), pp.209-223.

Santibáñez, J., Alcañiz, L. and Gómez-Bezares, F., 2014. Cost of funds on the basis of

Modigliani and Miller and CAPM propositions: a revision. Análisis financiero, 124, pp.6-16.

Serghiescu, L. and Văidean, V.L., 2014. Determinant factors of the capital structure of a

firm-an empirical analysis. Procedia Economics and Finance, 15, pp.1447-1457.

Wamser, G., 2014. The Impact of Thin‐Capitalization Rules on External Debt Usage–A

Propensity Score Matching Approach. Oxford Bulletin of Economics and Statistics, 76(5),

pp.764-781.

9

Hugonnier, J., Malamud, S. and Morellec, E., 2014. Capital supply uncertainty, cash

holdings, and investment. The Review of Financial Studies, 28(2), pp.391-445.

Maina, L. and Ishmail, M., 2014. Capital structure and financial performance in Kenya:

Evidence from firms listed at the Nairobi Securities Exchange. International Journal of

Social Sciences and Entrepreneurship, 1(11), pp.209-223.

Santibáñez, J., Alcañiz, L. and Gómez-Bezares, F., 2014. Cost of funds on the basis of

Modigliani and Miller and CAPM propositions: a revision. Análisis financiero, 124, pp.6-16.

Serghiescu, L. and Văidean, V.L., 2014. Determinant factors of the capital structure of a

firm-an empirical analysis. Procedia Economics and Finance, 15, pp.1447-1457.

Wamser, G., 2014. The Impact of Thin‐Capitalization Rules on External Debt Usage–A

Propensity Score Matching Approach. Oxford Bulletin of Economics and Statistics, 76(5),

pp.764-781.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.