Business Finance Report: Financial Analysis of Fashion Locker

VerifiedAdded on 2020/07/22

|11

|3735

|420

Report

AI Summary

This report provides a comprehensive financial analysis of a business, Fashion Locker, owned by Lisa and John. It begins with the preparation of an income statement and balance sheet, offering insights into the company's financial performance. The report calculates and interprets key financial ratios, including current ratio, acid-test ratio, operating profit ratio, return on assets, debt-equity ratio, inventory turnover ratio, and interest coverage ratio. These ratios are used to assess the company's liquidity, profitability, and solvency. The report then offers advice to Lisa and John based on the financial analysis, comparing profit and cash flow, highlighting the timing differences and accounting conventions that impact financial statements. Overall, the report offers a detailed overview of the business's financial standing and provides recommendations for improvement.

Business finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Income statement and balance sheet.......................................................................................1

2. Calculation of appropriate ratios.............................................................................................2

3. Report to Lisa and John...........................................................................................................3

4. Explanation of the difference between Profit and cash...........................................................5

5. Accounting conventions and their impact on statements........................................................6

CONCLUSION................................................................................................................................8

REFERENCES ...............................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Income statement and balance sheet.......................................................................................1

2. Calculation of appropriate ratios.............................................................................................2

3. Report to Lisa and John...........................................................................................................3

4. Explanation of the difference between Profit and cash...........................................................5

5. Accounting conventions and their impact on statements........................................................6

CONCLUSION................................................................................................................................8

REFERENCES ...............................................................................................................................9

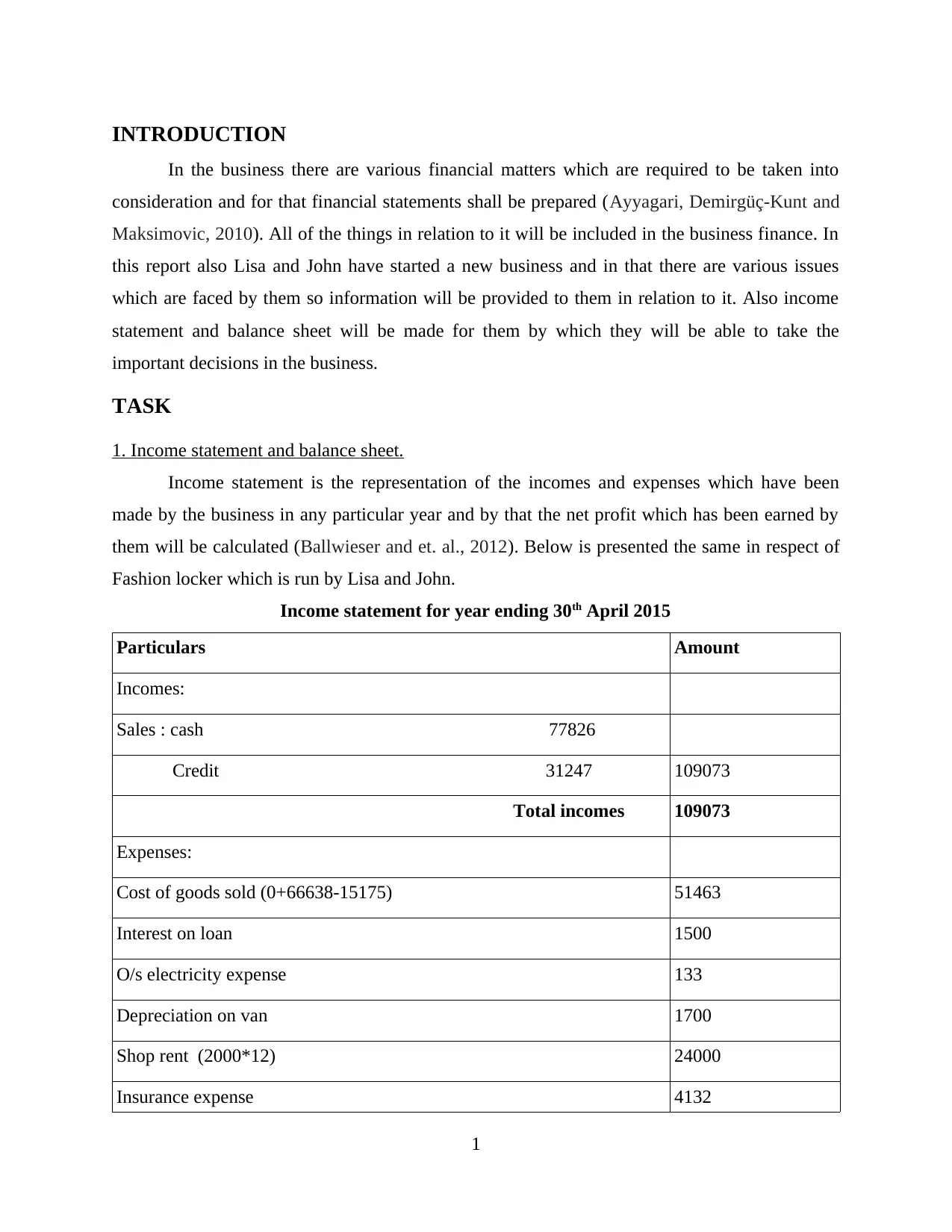

INTRODUCTION

In the business there are various financial matters which are required to be taken into

consideration and for that financial statements shall be prepared (Ayyagari, Demirgüç-Kunt and

Maksimovic, 2010). All of the things in relation to it will be included in the business finance. In

this report also Lisa and John have started a new business and in that there are various issues

which are faced by them so information will be provided to them in relation to it. Also income

statement and balance sheet will be made for them by which they will be able to take the

important decisions in the business.

TASK

1. Income statement and balance sheet.

Income statement is the representation of the incomes and expenses which have been

made by the business in any particular year and by that the net profit which has been earned by

them will be calculated (Ballwieser and et. al., 2012). Below is presented the same in respect of

Fashion locker which is run by Lisa and John.

Income statement for year ending 30th April 2015

Particulars Amount

Incomes:

Sales : cash 77826

Credit 31247 109073

Total incomes 109073

Expenses:

Cost of goods sold (0+66638-15175) 51463

Interest on loan 1500

O/s electricity expense 133

Depreciation on van 1700

Shop rent (2000*12) 24000

Insurance expense 4132

1

In the business there are various financial matters which are required to be taken into

consideration and for that financial statements shall be prepared (Ayyagari, Demirgüç-Kunt and

Maksimovic, 2010). All of the things in relation to it will be included in the business finance. In

this report also Lisa and John have started a new business and in that there are various issues

which are faced by them so information will be provided to them in relation to it. Also income

statement and balance sheet will be made for them by which they will be able to take the

important decisions in the business.

TASK

1. Income statement and balance sheet.

Income statement is the representation of the incomes and expenses which have been

made by the business in any particular year and by that the net profit which has been earned by

them will be calculated (Ballwieser and et. al., 2012). Below is presented the same in respect of

Fashion locker which is run by Lisa and John.

Income statement for year ending 30th April 2015

Particulars Amount

Incomes:

Sales : cash 77826

Credit 31247 109073

Total incomes 109073

Expenses:

Cost of goods sold (0+66638-15175) 51463

Interest on loan 1500

O/s electricity expense 133

Depreciation on van 1700

Shop rent (2000*12) 24000

Insurance expense 4132

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Other expenses 2463

Rates bill 3000

Electricity expense (255+390+410+385) 1440

Bad debts 850

Total expenses 90681

Net profit 18392

Balance sheet is the statement in which the assets and the liabilities of the business are

represented in the tabular manner. In this the assets will be equal to the liabilities and by this the

position of the business will be determined. The same is provided below:

Balance sheet as on 30th April 2015

Particulars Amount

Assets

Van (17000-1700) 15300

Debtors (7459-850) 6609

Inventory 15175

Petty cash 854

Total assets 37938

Liabilities and equity

Bank loan 7500

Bank overdraft 4668

Creditors 8245

O/s expenses 133

Owner's capital:

2

Rates bill 3000

Electricity expense (255+390+410+385) 1440

Bad debts 850

Total expenses 90681

Net profit 18392

Balance sheet is the statement in which the assets and the liabilities of the business are

represented in the tabular manner. In this the assets will be equal to the liabilities and by this the

position of the business will be determined. The same is provided below:

Balance sheet as on 30th April 2015

Particulars Amount

Assets

Van (17000-1700) 15300

Debtors (7459-850) 6609

Inventory 15175

Petty cash 854

Total assets 37938

Liabilities and equity

Bank loan 7500

Bank overdraft 4668

Creditors 8245

O/s expenses 133

Owner's capital:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital 25000

Add: Net profit 18392

Less: Drawings 26000 17392

Total equities and liabilities 37938

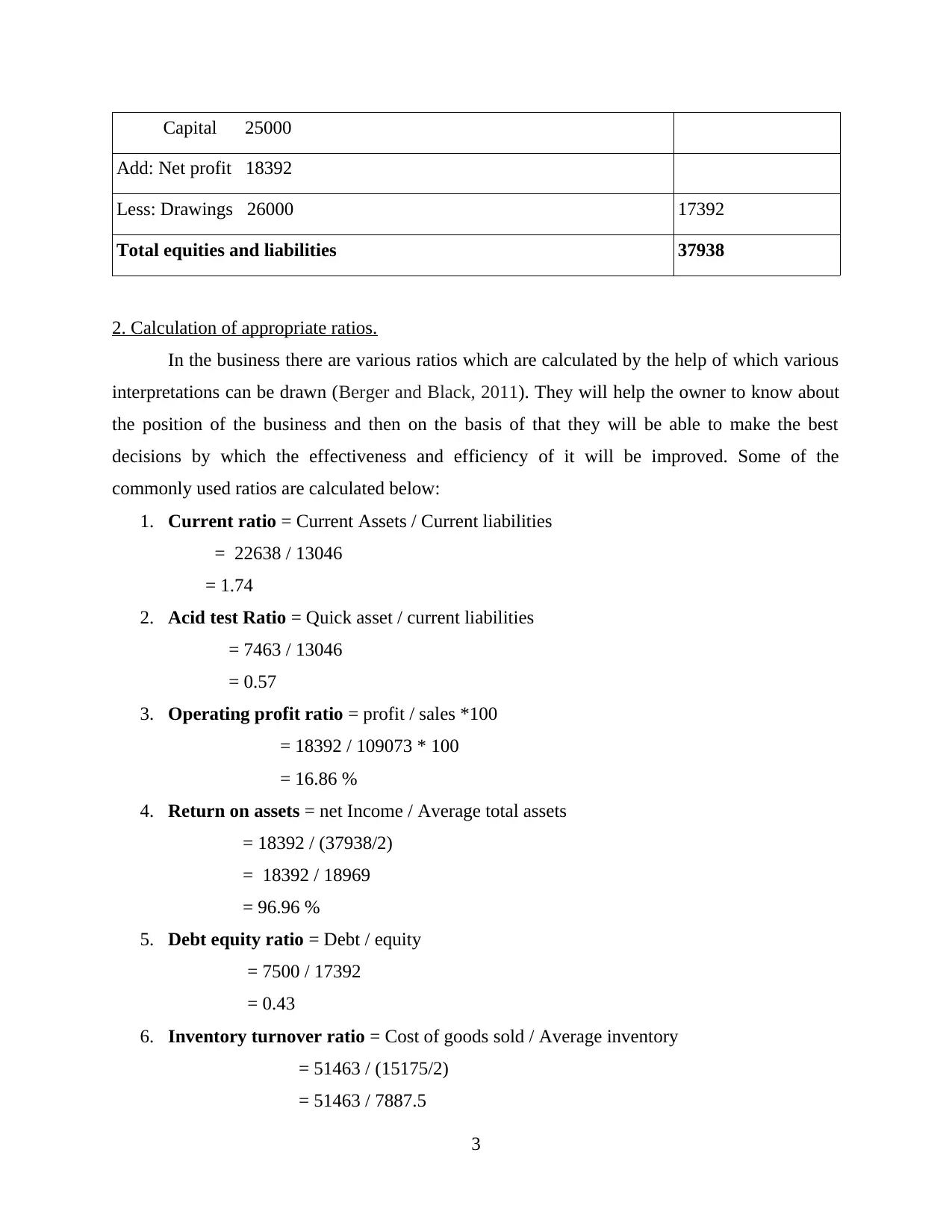

2. Calculation of appropriate ratios.

In the business there are various ratios which are calculated by the help of which various

interpretations can be drawn (Berger and Black, 2011). They will help the owner to know about

the position of the business and then on the basis of that they will be able to make the best

decisions by which the effectiveness and efficiency of it will be improved. Some of the

commonly used ratios are calculated below:

1. Current ratio = Current Assets / Current liabilities

= 22638 / 13046

= 1.74

2. Acid test Ratio = Quick asset / current liabilities

= 7463 / 13046

= 0.57

3. Operating profit ratio = profit / sales *100

= 18392 / 109073 * 100

= 16.86 %

4. Return on assets = net Income / Average total assets

= 18392 / (37938/2)

= 18392 / 18969

= 96.96 %

5. Debt equity ratio = Debt / equity

= 7500 / 17392

= 0.43

6. Inventory turnover ratio = Cost of goods sold / Average inventory

= 51463 / (15175/2)

= 51463 / 7887.5

3

Add: Net profit 18392

Less: Drawings 26000 17392

Total equities and liabilities 37938

2. Calculation of appropriate ratios.

In the business there are various ratios which are calculated by the help of which various

interpretations can be drawn (Berger and Black, 2011). They will help the owner to know about

the position of the business and then on the basis of that they will be able to make the best

decisions by which the effectiveness and efficiency of it will be improved. Some of the

commonly used ratios are calculated below:

1. Current ratio = Current Assets / Current liabilities

= 22638 / 13046

= 1.74

2. Acid test Ratio = Quick asset / current liabilities

= 7463 / 13046

= 0.57

3. Operating profit ratio = profit / sales *100

= 18392 / 109073 * 100

= 16.86 %

4. Return on assets = net Income / Average total assets

= 18392 / (37938/2)

= 18392 / 18969

= 96.96 %

5. Debt equity ratio = Debt / equity

= 7500 / 17392

= 0.43

6. Inventory turnover ratio = Cost of goods sold / Average inventory

= 51463 / (15175/2)

= 51463 / 7887.5

3

= 6.52

7. Asset turnover ratio = Sales / Average total assets

= 109073 / 18969

= 5.75

8. Interest coverage ratio = EBIT / Interest expense

= (18392 + 1500) / 1500

= 19892 / 1500

= 13.26

3. Report to Lisa and John.

From the above made calculations, there are many findings which can be reported and on

the basis of them Lisa and John can evaluate the performance of the business (Britten‐Jones,

Neuberger and Nolte, 2011). All of the ratios are telling about some or the other aspect of the

business.

The first ratio which has been calculated is current ratio which tells about the position of

the current assets and liabilities of the business (Cole, 2013). By this it will be determined that

whether the organisation will be able to meet its current liabilities on time or not. The standard in

respect of it has been set at 2:1. it is said that the ratio will be good if it is at higher level. In the

given case it has been calculated at 1.74 which means that it is not upto the margin and can be

improved further. The company is having good amount to payoff its liabilities as a new venture

and will be able to make its position even better.

The next ratio is the quick ratio by which the liquid asset available with the business will

be identified. In this inventory is not included as it takes time to be converted into cash. It is

calculated to be 0.57 which shows that company is not in the position to pay its all the liabilities

with the available resources and needs to take some action in this aspect.

Then comes the operating profit ratio by which the amount of profit made on the sales id

determined and is at 16.86 %. as a beginner it is a good amount and the business is earning well.

Return on asset is the ratio by which the earnings made with the available assets is

identified and this will tell that whether the business is making proper use of the assets present

(Columba, Gambacorta and Mistrulli, 2010). It is 96.96 % which is a very good margin and

shows that most of the assets are utilised in effective manner.

4

7. Asset turnover ratio = Sales / Average total assets

= 109073 / 18969

= 5.75

8. Interest coverage ratio = EBIT / Interest expense

= (18392 + 1500) / 1500

= 19892 / 1500

= 13.26

3. Report to Lisa and John.

From the above made calculations, there are many findings which can be reported and on

the basis of them Lisa and John can evaluate the performance of the business (Britten‐Jones,

Neuberger and Nolte, 2011). All of the ratios are telling about some or the other aspect of the

business.

The first ratio which has been calculated is current ratio which tells about the position of

the current assets and liabilities of the business (Cole, 2013). By this it will be determined that

whether the organisation will be able to meet its current liabilities on time or not. The standard in

respect of it has been set at 2:1. it is said that the ratio will be good if it is at higher level. In the

given case it has been calculated at 1.74 which means that it is not upto the margin and can be

improved further. The company is having good amount to payoff its liabilities as a new venture

and will be able to make its position even better.

The next ratio is the quick ratio by which the liquid asset available with the business will

be identified. In this inventory is not included as it takes time to be converted into cash. It is

calculated to be 0.57 which shows that company is not in the position to pay its all the liabilities

with the available resources and needs to take some action in this aspect.

Then comes the operating profit ratio by which the amount of profit made on the sales id

determined and is at 16.86 %. as a beginner it is a good amount and the business is earning well.

Return on asset is the ratio by which the earnings made with the available assets is

identified and this will tell that whether the business is making proper use of the assets present

(Columba, Gambacorta and Mistrulli, 2010). It is 96.96 % which is a very good margin and

shows that most of the assets are utilised in effective manner.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further debt equity is found which will be representing the amount of the debts business

is having in comparison to the equity funds. By this it will be known that the debts shall be at

optimum level. The business is having it as 0.43 which is good as the debts are lower which

means that there is less risk involved that will have to be faced.

The level of the inventory maintained in respect the cost of goods sold will be shown by

the inventory turnover ratio. This is 6.52 which shows that the business is having this times of

inventory and it is a good as by this it is known that company is having proper control.

By interest coverage ratio it will be determined that how efficient will be the business in

the payment of the interest and it can be seen that it is 13.26 which says that Lisa and John will

be able to meet the interest expense even if it will be increased (Cuthbertson, Nitzsche and

O'Sullivan, 2010).

The acid test ratio and operating profit of the business can be improved by Lisa and John

by increasing the balance of the liquid assets and for that cash balance will have to be increased.

In order to improve the operating profit ratio they can raise the level of the sales and also the

control will have to be established on the expenses which are made by them in the maintenance

of the operations at the lowest cost possible.

4. Explanation of the difference between Profit and cash.

In any business cash will be the main need as all the operations which will be conducted

would be requiring the funds (Ghosh and Moon, 2010). All of the aspects will be needing it and

it will not be possible to carry on the business without it. Whereas profit is the amount which is

earned and is the major objective or can say motive for which the business is established but in

this it cannot be said that operation cannot be carried out without it. In order to achieve the

growth profit will be required and in case that the business is not making any profits for long

then the business will have to suffer the consequences of it as all the investments which have

been made will dwindle. The profits will be calculated after deducting the expenses which have

been incurred from the amount of sales made in any particular period of time. The cash balance

at the end of the year will be determined by the deduction of all the outflows which have been

made from the amount of the inflows.

In the given case it can be seen that there is the income which is made by Lisa and John

but their cash balance is in overdraft and there can be various reasons of it (Gitman and Zutter,

2012). There are mainly two reasons due to which difference exist among both of them and the

5

is having in comparison to the equity funds. By this it will be known that the debts shall be at

optimum level. The business is having it as 0.43 which is good as the debts are lower which

means that there is less risk involved that will have to be faced.

The level of the inventory maintained in respect the cost of goods sold will be shown by

the inventory turnover ratio. This is 6.52 which shows that the business is having this times of

inventory and it is a good as by this it is known that company is having proper control.

By interest coverage ratio it will be determined that how efficient will be the business in

the payment of the interest and it can be seen that it is 13.26 which says that Lisa and John will

be able to meet the interest expense even if it will be increased (Cuthbertson, Nitzsche and

O'Sullivan, 2010).

The acid test ratio and operating profit of the business can be improved by Lisa and John

by increasing the balance of the liquid assets and for that cash balance will have to be increased.

In order to improve the operating profit ratio they can raise the level of the sales and also the

control will have to be established on the expenses which are made by them in the maintenance

of the operations at the lowest cost possible.

4. Explanation of the difference between Profit and cash.

In any business cash will be the main need as all the operations which will be conducted

would be requiring the funds (Ghosh and Moon, 2010). All of the aspects will be needing it and

it will not be possible to carry on the business without it. Whereas profit is the amount which is

earned and is the major objective or can say motive for which the business is established but in

this it cannot be said that operation cannot be carried out without it. In order to achieve the

growth profit will be required and in case that the business is not making any profits for long

then the business will have to suffer the consequences of it as all the investments which have

been made will dwindle. The profits will be calculated after deducting the expenses which have

been incurred from the amount of sales made in any particular period of time. The cash balance

at the end of the year will be determined by the deduction of all the outflows which have been

made from the amount of the inflows.

In the given case it can be seen that there is the income which is made by Lisa and John

but their cash balance is in overdraft and there can be various reasons of it (Gitman and Zutter,

2012). There are mainly two reasons due to which difference exist among both of them and the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

main among them is timing difference which exist when the operation is carried out but the

payment or the receipt in relation to it has not occurred in the given period. Also sometimes there

is different manner which is used to record the fixed assets and then it will be affecting the

amount of the cash and also the profits.

In the given case there are various expenses which are made and have been paid from the

cash so due to them the balance of the cash is affected but as they are not included in income

statements so there will be no impact of it on the amount of the profits made. Such as the

business is new and is not having much of the cash balance and had taken loan for it. It can be

seen that the amount of the loan which has been taken from the bank is 15000 out of which 7500

had been repaid in the current year so the cash balance has been reduced (Hillier, Grinblatt and

Titman, 2011). Also the van has been purchased costing to 17000 which is high amount and is

leading to the shortage of the funds.

Company has made insurance and the premium is paid in relation to it in the current

period by which the cash balance is affected and this is not the expense of the current year or it

can be said that although the amount is paid but there is no advantage which has been received in

relation to it. The purchase of the asset although has led to the decrease in the mount of the cash

but there has been no effect of it on the profit as it is not included in the calculation of it (Karlan

and Valdivia, 2011). The repayment made of the bank loan is also not considered in the profit

and loss account whereas they will be treated in the calculation of the closing balance of the cash

so that will be declined. These are the major aspects because of which the situation has arisen.

The another matter which will be considered in this is that the business is allowing the

credit facility to the customers so the sales will be made but the cash will not be received in this

case. By this the net profit will be increased as the credit sales is also included in the total

revenues but this will not be added in the cash account.

The balance is overdrawn and the another example of it in the present scenario is the

drawings which are made by Lisa and John. By this the profit will not be declining as they are

not deducted as an expense and they are treated in the capital account but since the amount will

be withdrawn so the balance of the funds will be declining and which will be having an adverse

impact as the business is new and in the initial stage only if the drawings will be made then it

will not be left with much funds and will not be able to carry on the activities in the appropriate

manner. So it will have to be ensured that the amount of the cash shall be maintained at correct

6

payment or the receipt in relation to it has not occurred in the given period. Also sometimes there

is different manner which is used to record the fixed assets and then it will be affecting the

amount of the cash and also the profits.

In the given case there are various expenses which are made and have been paid from the

cash so due to them the balance of the cash is affected but as they are not included in income

statements so there will be no impact of it on the amount of the profits made. Such as the

business is new and is not having much of the cash balance and had taken loan for it. It can be

seen that the amount of the loan which has been taken from the bank is 15000 out of which 7500

had been repaid in the current year so the cash balance has been reduced (Hillier, Grinblatt and

Titman, 2011). Also the van has been purchased costing to 17000 which is high amount and is

leading to the shortage of the funds.

Company has made insurance and the premium is paid in relation to it in the current

period by which the cash balance is affected and this is not the expense of the current year or it

can be said that although the amount is paid but there is no advantage which has been received in

relation to it. The purchase of the asset although has led to the decrease in the mount of the cash

but there has been no effect of it on the profit as it is not included in the calculation of it (Karlan

and Valdivia, 2011). The repayment made of the bank loan is also not considered in the profit

and loss account whereas they will be treated in the calculation of the closing balance of the cash

so that will be declined. These are the major aspects because of which the situation has arisen.

The another matter which will be considered in this is that the business is allowing the

credit facility to the customers so the sales will be made but the cash will not be received in this

case. By this the net profit will be increased as the credit sales is also included in the total

revenues but this will not be added in the cash account.

The balance is overdrawn and the another example of it in the present scenario is the

drawings which are made by Lisa and John. By this the profit will not be declining as they are

not deducted as an expense and they are treated in the capital account but since the amount will

be withdrawn so the balance of the funds will be declining and which will be having an adverse

impact as the business is new and in the initial stage only if the drawings will be made then it

will not be left with much funds and will not be able to carry on the activities in the appropriate

manner. So it will have to be ensured that the amount of the cash shall be maintained at correct

6

level and for this proper control system will have to be established by which the expenses which

are incurred will be monitored on the regular basis and thereby the expenses which can be

avoided will be identified and measures will be taken to overcome the excessive expenditures.

All of these were some of the reasons due to which the difference has arisen and also the

variation among the cash and profit is made which are two separate aspects and will have to be

managed in the best manner possible.

5. Accounting conventions and their impact on statements.

In the business there are various accounting processes which are undertaken and among

them several statements are made and in relation to them there are many rules and regulation

which have been made (Ryan, Buchholtz and Kolb, 2010). They are known as the accounting

conventions and are required to be followed in the business so that the recording of all the

transactions can be made on the appropriate basis. There are various conventions which are

specified by the authorities and the two among them which have been used by the Lisa and John

are described below:

Convention of conservatism: In this the main focus is provided on keeping the business

in the safe position. In this the transactions are recorded by keeping in view the concept

that all the expenses and losses which are involved in the business shall be taken into

consideration and the incomes which will be earned in the future and are not made in the

current period will have to be ignored (Abor and Quartey, 2010). By this it will be

provided that al the risk and the uncertainties which are present will be given proper

importance so that the adverse impact of them can be dealt with in the most appropriate

manner. In this the main example which can be considered is the valuation of the stock in

which the rule which is followed specifies that the inventory shall be valued at the

amount which will be lower of the cost value or the price in the market.

The another major part which is dealt in this convention is the bad debts which are the amount of

the debtors about whom the uncertainty is there that whether they will be paying back the

amount or not. The same case is present in the given situation as there is one mail order customer

who purchase the products on credit and she owes 850 and now she is not able to pay the amount

and is requesting that she should be given some extra time to repay the amount. But John has

identified that there are very less chances that the amount will be recovered as it is the image of

that customer in the market. So while making the statements the amount has been involved in the

7

are incurred will be monitored on the regular basis and thereby the expenses which can be

avoided will be identified and measures will be taken to overcome the excessive expenditures.

All of these were some of the reasons due to which the difference has arisen and also the

variation among the cash and profit is made which are two separate aspects and will have to be

managed in the best manner possible.

5. Accounting conventions and their impact on statements.

In the business there are various accounting processes which are undertaken and among

them several statements are made and in relation to them there are many rules and regulation

which have been made (Ryan, Buchholtz and Kolb, 2010). They are known as the accounting

conventions and are required to be followed in the business so that the recording of all the

transactions can be made on the appropriate basis. There are various conventions which are

specified by the authorities and the two among them which have been used by the Lisa and John

are described below:

Convention of conservatism: In this the main focus is provided on keeping the business

in the safe position. In this the transactions are recorded by keeping in view the concept

that all the expenses and losses which are involved in the business shall be taken into

consideration and the incomes which will be earned in the future and are not made in the

current period will have to be ignored (Abor and Quartey, 2010). By this it will be

provided that al the risk and the uncertainties which are present will be given proper

importance so that the adverse impact of them can be dealt with in the most appropriate

manner. In this the main example which can be considered is the valuation of the stock in

which the rule which is followed specifies that the inventory shall be valued at the

amount which will be lower of the cost value or the price in the market.

The another major part which is dealt in this convention is the bad debts which are the amount of

the debtors about whom the uncertainty is there that whether they will be paying back the

amount or not. The same case is present in the given situation as there is one mail order customer

who purchase the products on credit and she owes 850 and now she is not able to pay the amount

and is requesting that she should be given some extra time to repay the amount. But John has

identified that there are very less chances that the amount will be recovered as it is the image of

that customer in the market. So while making the statements the amount has been involved in the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

income statement as the bad debt and also it has been reduced from the amount of the total

debtors outstanding at the end of the period. So by this it can be said that the convention of the

conservatism has been applied in the business.

Convention of materiality: Under this it has been specified that all the material aspects

which are there and the transactions shall be included in the preparation of the financial

statements. It shall be noted that the transactions which are of small amount and are not

of much significance shall be not given the emphasis (Anandarajan, Anandarajan and

Srinivasan, 2012). This is done as they will not be of much importance to the

management as there will be no effect which will have to be borne due to them and also

no information will be provided by them which can be used in the decision making

process of the business.

The item will be considered to be material when there will be the significant impact which will

have to be dealt with if it will be omitted to be included in the accounting. Also the decisions will

be affected because of them which will be made by the persons who will be using them. In this

sometimes it happens that the many small matters are accumulated and then on the combined

basis they become relevant so they will be included. Such as in the given case the head is

provided with the name of other expenses in which nothing is specified separately but all of them

are included and the profit is affected by them. The other material aspects which will be involved

in the business will also be incorporated so that the the true picture can be made and all the

decisions which will be taken on the basis of them will be the best and the business will be able

to achieve the advantage of it.

So these are the two conventions which are considered and are to be followed

compulsorily in the business so that the accounting records which are kept by Lisa and John will

be in appropriate format and they will be able to have all the information which will be utilised

in the future period so that the further growth can be achieved by the company. Also as the

venture is new so it will be ensured that its going concern can be maintained and there will be no

r8isk in relation to it which will have to be dealt with by the business.

CONCLUSION

From the above mentioned report it can be concluded that there are various matters which

will have to be given due importance in the business by which the management of business can

be carried out in the most appropriate manner. For this there has been analysation made for

8

debtors outstanding at the end of the period. So by this it can be said that the convention of the

conservatism has been applied in the business.

Convention of materiality: Under this it has been specified that all the material aspects

which are there and the transactions shall be included in the preparation of the financial

statements. It shall be noted that the transactions which are of small amount and are not

of much significance shall be not given the emphasis (Anandarajan, Anandarajan and

Srinivasan, 2012). This is done as they will not be of much importance to the

management as there will be no effect which will have to be borne due to them and also

no information will be provided by them which can be used in the decision making

process of the business.

The item will be considered to be material when there will be the significant impact which will

have to be dealt with if it will be omitted to be included in the accounting. Also the decisions will

be affected because of them which will be made by the persons who will be using them. In this

sometimes it happens that the many small matters are accumulated and then on the combined

basis they become relevant so they will be included. Such as in the given case the head is

provided with the name of other expenses in which nothing is specified separately but all of them

are included and the profit is affected by them. The other material aspects which will be involved

in the business will also be incorporated so that the the true picture can be made and all the

decisions which will be taken on the basis of them will be the best and the business will be able

to achieve the advantage of it.

So these are the two conventions which are considered and are to be followed

compulsorily in the business so that the accounting records which are kept by Lisa and John will

be in appropriate format and they will be able to have all the information which will be utilised

in the future period so that the further growth can be achieved by the company. Also as the

venture is new so it will be ensured that its going concern can be maintained and there will be no

r8isk in relation to it which will have to be dealt with by the business.

CONCLUSION

From the above mentioned report it can be concluded that there are various matters which

will have to be given due importance in the business by which the management of business can

be carried out in the most appropriate manner. For this there has been analysation made for

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which the ratios have been calculated that are telling about the position and performance of the

business. Then the interpretation is done and the reasons which are there by which the profits and

cash are different and there is an overdraft in the balance of cash. The conventions which are

complied with are also described with the help of which proper accounting has been undertaken.

9

business. Then the interpretation is done and the reasons which are there by which the profits and

cash are different and there is an overdraft in the balance of cash. The conventions which are

complied with are also described with the help of which proper accounting has been undertaken.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.