Business Finance Module: Analyzing Financial Statements and Ratios

VerifiedAdded on 2021/02/22

|12

|2839

|46

Homework Assignment

AI Summary

This business finance assignment provides a comprehensive overview of accounting principles and financial statement analysis. It begins with the presentation of transactions through T-accounts and balance sheets, detailing journal entries for various financial activities. The assignment the...

Read More

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION................................................................................................................................3

Task 1 ...................................................................................................................................................3

1.1 & 1.2 Presenting the set of transactions by preparing relevant T- accounts and Balance Sheet

T- accounts.......................................................................................................................................3

2.1 Preparation of Trading A/C and Balance sheet for a business organisation..............................6

2.2 Evaluation of a set of Final Business Accounts ........................................................................6

3.1 Analysing and Interpretation of business accounts using ratio analysis between two

companies........................................................................................................................................8

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

INTRODUCTION................................................................................................................................3

Task 1 ...................................................................................................................................................3

1.1 & 1.2 Presenting the set of transactions by preparing relevant T- accounts and Balance Sheet

T- accounts.......................................................................................................................................3

2.1 Preparation of Trading A/C and Balance sheet for a business organisation..............................6

2.2 Evaluation of a set of Final Business Accounts ........................................................................6

3.1 Analysing and Interpretation of business accounts using ratio analysis between two

companies........................................................................................................................................8

CONCLUSION...................................................................................................................................11

REFERENCES...................................................................................................................................12

INTRODUCTION

Business Finance is about the various case studies related to the preparation of final

accounts of various companies. It also includes the summary of income statements and balance

sheet by calculating the % change in the statements based on the past year's performance of the

company. Also, it includes the evaluation of a set of final business accounts. It also includes the

analysis and interpretation of the business accounts using the ratio analysis. It shows the

performance of the various companies on the basis of their past performances of the company.

Task 1

1.1 & 1.2 Presenting the set of transactions by preparing relevant T- accounts and Balance Sheet T-

accounts

Journal Entries of Adek Lisowski as on 01 January 20xx

Date Particulars Debit Credit

2 Jan. 20xx Bank a/c Dr. 740

To J Jennings a/c (debtor) 740

3 Jan. 20xx Purchases a/c Dr. 1070

To G Frazer a/c(Creditors) 1070

4 Jan. 20xx Office Equipments a/c Dr. 560

To Bank a/c 560

5 Jan. 20xx A Hussain (Debtors) a/c Dr. 930

To Sales a/c 930

8 Jan. 20xx G Frazer (Creditors) a/c Dr. 880

To Bank a/c 880

11 Jan. 20xx Sales Return a/c Dr. 37

To A Hussain (debtor) a/c 37

14 Jan. 20xx J Jennings (Debtors) a/c Dr. 590

To Sales a/c 590

17 Jan. 20xx Drawings a/c Dr. 500

To Bank a/c 500

20 Jan. 20xx Purchases a/c Dr. 760

To G Frazer (Creditors) a/c 760

22 Jan. 20xx Bank a/c Dr. 1100

To A Hussain (debtors) a/c 1100

26 Jan. 20xx A Hussain (debtors) a/c 710

To Sales a/c 710

28 Jan. 20xx G Frazer (Creditors) a/c 98

Business Finance is about the various case studies related to the preparation of final

accounts of various companies. It also includes the summary of income statements and balance

sheet by calculating the % change in the statements based on the past year's performance of the

company. Also, it includes the evaluation of a set of final business accounts. It also includes the

analysis and interpretation of the business accounts using the ratio analysis. It shows the

performance of the various companies on the basis of their past performances of the company.

Task 1

1.1 & 1.2 Presenting the set of transactions by preparing relevant T- accounts and Balance Sheet T-

accounts

Journal Entries of Adek Lisowski as on 01 January 20xx

Date Particulars Debit Credit

2 Jan. 20xx Bank a/c Dr. 740

To J Jennings a/c (debtor) 740

3 Jan. 20xx Purchases a/c Dr. 1070

To G Frazer a/c(Creditors) 1070

4 Jan. 20xx Office Equipments a/c Dr. 560

To Bank a/c 560

5 Jan. 20xx A Hussain (Debtors) a/c Dr. 930

To Sales a/c 930

8 Jan. 20xx G Frazer (Creditors) a/c Dr. 880

To Bank a/c 880

11 Jan. 20xx Sales Return a/c Dr. 37

To A Hussain (debtor) a/c 37

14 Jan. 20xx J Jennings (Debtors) a/c Dr. 590

To Sales a/c 590

17 Jan. 20xx Drawings a/c Dr. 500

To Bank a/c 500

20 Jan. 20xx Purchases a/c Dr. 760

To G Frazer (Creditors) a/c 760

22 Jan. 20xx Bank a/c Dr. 1100

To A Hussain (debtors) a/c 1100

26 Jan. 20xx A Hussain (debtors) a/c 710

To Sales a/c 710

28 Jan. 20xx G Frazer (Creditors) a/c 98

To purchases return a/c 98

31 Jan. 20xx Wages a/c 480

To Bank a/c 480

Ledger Postings of Adek Lisowski as on 01 January 20xx

Bank A/C

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

1 Jan 20xx To Bal. B/d 2040 4 Jan. 20xx

By Office

Equipments

a/c 560

2 Jan. 20xx To J Jennings a/c (debtor) 740 8 Jan. 20xx

By G Frazer

(Creditors)

a/c 880

22 Jan. 20xx To A Hussain (debtors) a/c 1100 17 Jan. 20xx

By Drawings

a/c 500

31 Jan. 20xx

By Wages

a/c 480

31 Jan. 20xx By Bal. C/d 1460

3880 3880

Purchases a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

3 Jan. 20xx To G Frazer a/c(Creditors) 1070 31 Jan. 20xx By Bal. C/d 1830

20 Jan. 20xx To G Frazer (Creditors) a/c 760

1830 1830

Sales A/C

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

31 Jan. 20xx To Bal. C/d 2230 5 Jan. 20xx

BY A

Hussain

(Debtors) a/c 930

14 Jan. 20xx

BYJ

Jennings

(Debtors) a/c 590

26 Jan. 20xx

A Hussain

(debtors) a/c 710

2230 2230

Purchases return a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

31 Jan. 20xx To Bal. C/d 98 28 Jan. 20xx

By G Frazer

(Creditors)

a/c 98

31 Jan. 20xx Wages a/c 480

To Bank a/c 480

Ledger Postings of Adek Lisowski as on 01 January 20xx

Bank A/C

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

1 Jan 20xx To Bal. B/d 2040 4 Jan. 20xx

By Office

Equipments

a/c 560

2 Jan. 20xx To J Jennings a/c (debtor) 740 8 Jan. 20xx

By G Frazer

(Creditors)

a/c 880

22 Jan. 20xx To A Hussain (debtors) a/c 1100 17 Jan. 20xx

By Drawings

a/c 500

31 Jan. 20xx

By Wages

a/c 480

31 Jan. 20xx By Bal. C/d 1460

3880 3880

Purchases a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

3 Jan. 20xx To G Frazer a/c(Creditors) 1070 31 Jan. 20xx By Bal. C/d 1830

20 Jan. 20xx To G Frazer (Creditors) a/c 760

1830 1830

Sales A/C

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

31 Jan. 20xx To Bal. C/d 2230 5 Jan. 20xx

BY A

Hussain

(Debtors) a/c 930

14 Jan. 20xx

BYJ

Jennings

(Debtors) a/c 590

26 Jan. 20xx

A Hussain

(debtors) a/c 710

2230 2230

Purchases return a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

31 Jan. 20xx To Bal. C/d 98 28 Jan. 20xx

By G Frazer

(Creditors)

a/c 98

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

98 98

Sales return a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

11 Jan. 20xx To A Hussain (debtor) a/c 37 31 Jan. 20xx By Bal. C/d 37

37 37

J Jennings a/c (debtor)

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

1 Jan 20xx To Bal. B/d 740 2 Jan. 20xx By Bank a/c 740

14 Jan. 20xx To Sales a/c 590 31 Jan. 20xx By Bal. C/d 590

1330 1330

A Hussain (Debtors) a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

1 Jan 20xx To Bal. B/d 1100 11 Jan. 20xx

By Sales

Return a/c 37

5 Jan. 20xx To Sales a/c 930 22 Jan. 20xx By Bank a/c 1100

26 Jan. 20xx By A Hussain (debtors) a/c 710

31 Jan. 20xx By Bal. C/d 1603

2740 2740

G Frazer a/c(Creditors)

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

8 Jan. 20xx To Bank a/c 880 1 Jan. 20xx By Bal. B/d 880

28 Jan. 20xx To purchases return a/c 98 3 Jan. 20xx

By

Purchases

a/c 1070

31 Jan. 20xx To Bal. C/d 1732 20 Jan. 20xx

By

Purchases

a/c Dr. 760

2710 2710

Office Equipments a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

4 Jan. 20xx To Bank a/c 560 31 Jan. 20xx By Bal. C/d 560

560 560

Drawings a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

17 Jan. 20xx To Bank a/c 500 31 Jan. 20xx By Bal. C/d 500

Sales return a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

11 Jan. 20xx To A Hussain (debtor) a/c 37 31 Jan. 20xx By Bal. C/d 37

37 37

J Jennings a/c (debtor)

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

1 Jan 20xx To Bal. B/d 740 2 Jan. 20xx By Bank a/c 740

14 Jan. 20xx To Sales a/c 590 31 Jan. 20xx By Bal. C/d 590

1330 1330

A Hussain (Debtors) a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

1 Jan 20xx To Bal. B/d 1100 11 Jan. 20xx

By Sales

Return a/c 37

5 Jan. 20xx To Sales a/c 930 22 Jan. 20xx By Bank a/c 1100

26 Jan. 20xx By A Hussain (debtors) a/c 710

31 Jan. 20xx By Bal. C/d 1603

2740 2740

G Frazer a/c(Creditors)

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

8 Jan. 20xx To Bank a/c 880 1 Jan. 20xx By Bal. B/d 880

28 Jan. 20xx To purchases return a/c 98 3 Jan. 20xx

By

Purchases

a/c 1070

31 Jan. 20xx To Bal. C/d 1732 20 Jan. 20xx

By

Purchases

a/c Dr. 760

2710 2710

Office Equipments a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

4 Jan. 20xx To Bank a/c 560 31 Jan. 20xx By Bal. C/d 560

560 560

Drawings a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

17 Jan. 20xx To Bank a/c 500 31 Jan. 20xx By Bal. C/d 500

500 500

Wages a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

31 Jan. 20xx To Bank a/c 480 31 Jan. 20xx By Bal. C/d 480

480 480

Trial Balance of Adek Lisowski as on 01 January 20xx

S. No. Particulars Amount (Dr.) Amount (Cr.)

1 Capital a/c 6800

2 Motor Vehicle a/c 3800

3 Bank A/C 1460

4 Purchases a/c 1830

5 Sales a/c 2230

6 Purchases return a/c 98

7 Sales return a/c 37

8 J Jennings a/c (debtor) 590

9 A Hussain (Debtors) a/c 1603

10 G Frazer a/c(Creditors) 1732

11 Office Equipments a/c 560

12 Drawings a/c 500

13 Wages a/c 480

10860 10860

2.1 Preparation of Trading A/C and Balance sheet for a business organisation

Trading and Profit/ Loss account for Adya Kumar as at 31 December 20xx

Trading A/C

Particulars Amount (Dr.) Particulars Amount (Cr.)

To opening stock a/c 13250 By sales a/c 85500

To purchases a/c 55000 By closing stock a/c 18100

To Gross Profit c/f 35350

103600 103600

Profit and Loss a/c

To wages and salaries 9220 by Gross Profit b/d 35350

To office expenses 850

To rates 1200

To delivery van 5250

To Telephone charges 800

To travel expenses 330

To Net Profit c/f 17700

35350 35350

2.2 Evaluation of a set of Final Business Accounts

Wages a/c

Date Particulars

Amount

(Dr.) Date Particulars

Amount

(Cr.)

31 Jan. 20xx To Bank a/c 480 31 Jan. 20xx By Bal. C/d 480

480 480

Trial Balance of Adek Lisowski as on 01 January 20xx

S. No. Particulars Amount (Dr.) Amount (Cr.)

1 Capital a/c 6800

2 Motor Vehicle a/c 3800

3 Bank A/C 1460

4 Purchases a/c 1830

5 Sales a/c 2230

6 Purchases return a/c 98

7 Sales return a/c 37

8 J Jennings a/c (debtor) 590

9 A Hussain (Debtors) a/c 1603

10 G Frazer a/c(Creditors) 1732

11 Office Equipments a/c 560

12 Drawings a/c 500

13 Wages a/c 480

10860 10860

2.1 Preparation of Trading A/C and Balance sheet for a business organisation

Trading and Profit/ Loss account for Adya Kumar as at 31 December 20xx

Trading A/C

Particulars Amount (Dr.) Particulars Amount (Cr.)

To opening stock a/c 13250 By sales a/c 85500

To purchases a/c 55000 By closing stock a/c 18100

To Gross Profit c/f 35350

103600 103600

Profit and Loss a/c

To wages and salaries 9220 by Gross Profit b/d 35350

To office expenses 850

To rates 1200

To delivery van 5250

To Telephone charges 800

To travel expenses 330

To Net Profit c/f 17700

35350 35350

2.2 Evaluation of a set of Final Business Accounts

Analysis and Interpretation of Income Statement of LMN Plc.

Income Statement

Particulars 2016 $(m) 2017 $(m) % change

Revenue 150 250 66.67%

Less:Cost of Sales -100 -175 75.00%

Gross Profit 50 75 50.00%

Less:Operating Expenses -38 -49 28.95%

Operating Profit 12 26 116.67%

Less:Interest Payable 0 -1

Net Profit after tax 12 25 108.33%

Less:taxation -5 -11 120.00%

Net Profit after tax 7 14 100.00%

LMN Plc. Revenue increases by 66.67% over the past year of the company. Company's

overall performance is good because net profit after tax has been increased by 100% which shows

the good sign for the company. Company's operating profit have also been increased by 116.67%

which is very good for any company (Abernathy and et.al, 2017). Company should try to maintain

the same performance every year so that the company's growth will be increasing fast.

Analysis and Interpretation of Balance Sheet of LMN Plc.

Balance Sheet

Particulars 2016 $(m) 2017 $ (m) % change

$ (m) $ (m) $ (m) $ (m) %

Assets

Non current assets (fixed

assets)

Plant & Equipment 52 85 63.46%

Current Assets

Inventory 12 16 33.33%

Trade Receivables 18 40 122.22%

Cash 10 4 -60.00%

40 60 50.00%

Total Assets 92 145 57.61%

Liabilities & Capital

Shareholders Fund

Share Capital 60 60 0.00%

Reserves 12 20 66.67%

72 80 11.11%

Current Liabilities

Trade Payables 11 28 154.55%

Overdraft 9 17 88.89%

20 45 125.00%

Non current Liabilities

Loans 0 0 20 20

Total Liabilities &

Capital 92 145 57.61%

Income Statement

Particulars 2016 $(m) 2017 $(m) % change

Revenue 150 250 66.67%

Less:Cost of Sales -100 -175 75.00%

Gross Profit 50 75 50.00%

Less:Operating Expenses -38 -49 28.95%

Operating Profit 12 26 116.67%

Less:Interest Payable 0 -1

Net Profit after tax 12 25 108.33%

Less:taxation -5 -11 120.00%

Net Profit after tax 7 14 100.00%

LMN Plc. Revenue increases by 66.67% over the past year of the company. Company's

overall performance is good because net profit after tax has been increased by 100% which shows

the good sign for the company. Company's operating profit have also been increased by 116.67%

which is very good for any company (Abernathy and et.al, 2017). Company should try to maintain

the same performance every year so that the company's growth will be increasing fast.

Analysis and Interpretation of Balance Sheet of LMN Plc.

Balance Sheet

Particulars 2016 $(m) 2017 $ (m) % change

$ (m) $ (m) $ (m) $ (m) %

Assets

Non current assets (fixed

assets)

Plant & Equipment 52 85 63.46%

Current Assets

Inventory 12 16 33.33%

Trade Receivables 18 40 122.22%

Cash 10 4 -60.00%

40 60 50.00%

Total Assets 92 145 57.61%

Liabilities & Capital

Shareholders Fund

Share Capital 60 60 0.00%

Reserves 12 20 66.67%

72 80 11.11%

Current Liabilities

Trade Payables 11 28 154.55%

Overdraft 9 17 88.89%

20 45 125.00%

Non current Liabilities

Loans 0 0 20 20

Total Liabilities &

Capital 92 145 57.61%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LMN plc. Balance sheet shows that even though the assets of the company has been by

63.46% but than also its profit has been by 100% which shows that assets are productively used in

the company. The company should invest more in the assets in order to increase the sales of the

company (Easton and et.al., 2018). The company is retaining its profits and that's why reserves have

been increased by 66.67%. It means that the company is using its own profits for investment.

3.1 Analysing and Interpretation of business accounts using ratio analysis between two companies

Liquidity Ratio

Current Ratio

Particulars C Plc D Plc

Current Assets 7.9 11.1

Current Liabilities 5.1 10.7

Current Ratio 1.55 1.04

Current Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8 1.55

1.04

C Plc

D Plc

Acid/ Quick Ratio

Particulars C Plc D Plc

Quick Assets 4.10 7.00

Current Liabilities 5.1 10.7

Acid ratio 0.80 0.65

63.46% but than also its profit has been by 100% which shows that assets are productively used in

the company. The company should invest more in the assets in order to increase the sales of the

company (Easton and et.al., 2018). The company is retaining its profits and that's why reserves have

been increased by 66.67%. It means that the company is using its own profits for investment.

3.1 Analysing and Interpretation of business accounts using ratio analysis between two companies

Liquidity Ratio

Current Ratio

Particulars C Plc D Plc

Current Assets 7.9 11.1

Current Liabilities 5.1 10.7

Current Ratio 1.55 1.04

Current Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8 1.55

1.04

C Plc

D Plc

Acid/ Quick Ratio

Particulars C Plc D Plc

Quick Assets 4.10 7.00

Current Liabilities 5.1 10.7

Acid ratio 0.80 0.65

Acid ratio

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9 0.80

0.65

C Plc

D Plc

Turnover Ratio

Debtors Turnover Ratio

Particulars C Plc D Plc

Net Sales/ revenue 43.9 96.3

Average Debtors 4.5 0.7

Debtors Turnover Ratio 9.756 137.571

Debtors collection Period (in

days) 37 3

Debtors Turnover Ratio

0

20

40

60

80

100

120

140

160

9.756

137.571

C Plc

D Plc

Creditors Turnover Ratio

Particulars C Plc D Plc

COGS 33.6 84.7

Average Creditors 5.1 10.7

Creditors Turnover Ratio 6.588 7.916

Creditors Payment Period (in

days) 55 46

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9 0.80

0.65

C Plc

D Plc

Turnover Ratio

Debtors Turnover Ratio

Particulars C Plc D Plc

Net Sales/ revenue 43.9 96.3

Average Debtors 4.5 0.7

Debtors Turnover Ratio 9.756 137.571

Debtors collection Period (in

days) 37 3

Debtors Turnover Ratio

0

20

40

60

80

100

120

140

160

9.756

137.571

C Plc

D Plc

Creditors Turnover Ratio

Particulars C Plc D Plc

COGS 33.6 84.7

Average Creditors 5.1 10.7

Creditors Turnover Ratio 6.588 7.916

Creditors Payment Period (in

days) 55 46

Creditors Turnover Ratio

0

1

2

3

4

5

6

7

8

9

6.588

7.916

C Plc

D Plc

Inventory Turnover Ratio

Particulars C Plc D Plc

COGS 33.6 84.7

Average Inventory 3.8 4.1

Inventory Turnover ratio 8.842 20.659

Inventory Turnover ratio

0

5

10

15

20

25

8.842

20.659

C Plc

D Plc

Gearing Ratio

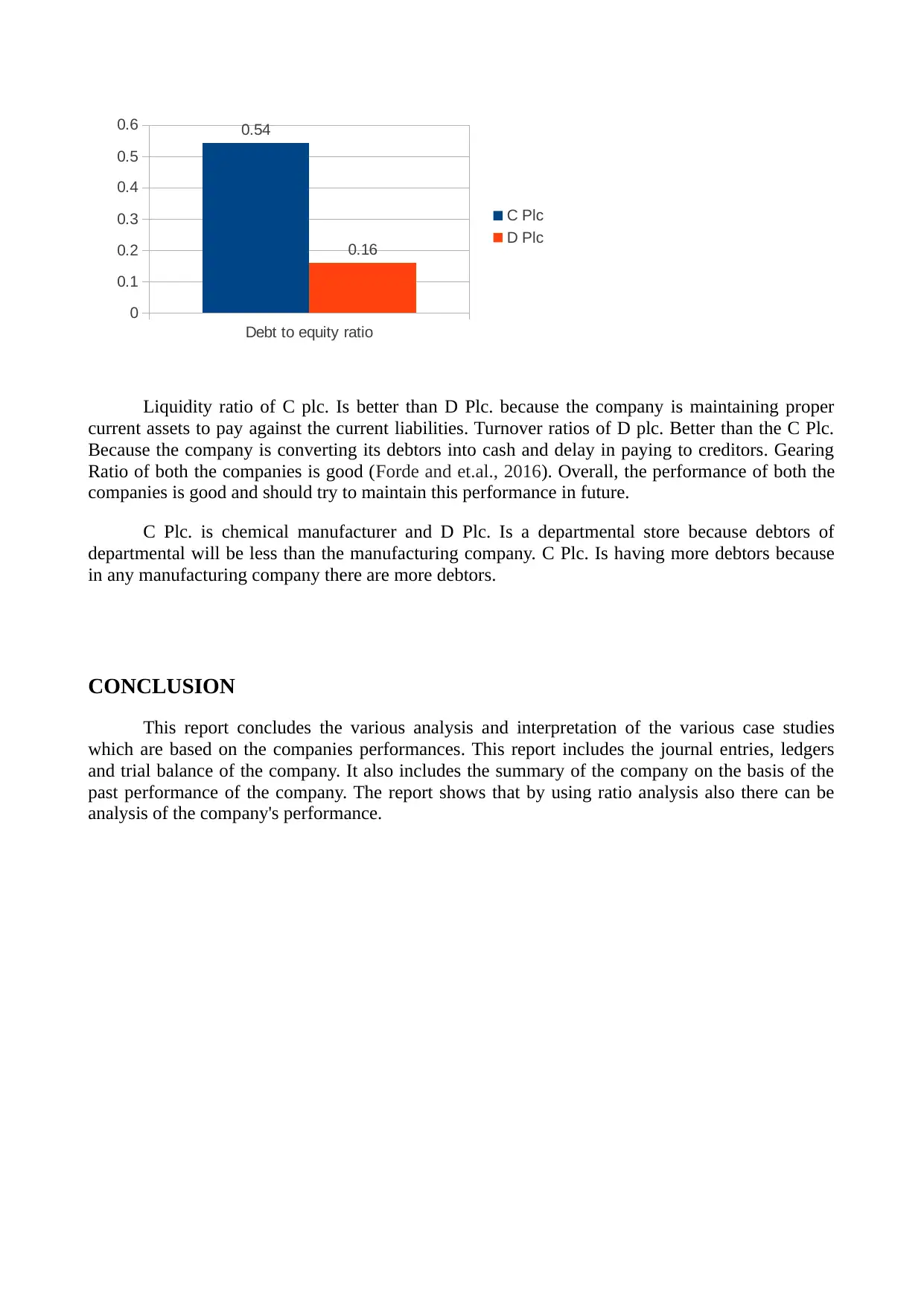

Debt to Equity Ratio

Particulars C Plc D Plc

Total Debt 3.2 2.1

Total shareholders fund 5.9 13.1

Debt to equity ratio 0.54 0.16

0

1

2

3

4

5

6

7

8

9

6.588

7.916

C Plc

D Plc

Inventory Turnover Ratio

Particulars C Plc D Plc

COGS 33.6 84.7

Average Inventory 3.8 4.1

Inventory Turnover ratio 8.842 20.659

Inventory Turnover ratio

0

5

10

15

20

25

8.842

20.659

C Plc

D Plc

Gearing Ratio

Debt to Equity Ratio

Particulars C Plc D Plc

Total Debt 3.2 2.1

Total shareholders fund 5.9 13.1

Debt to equity ratio 0.54 0.16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Debt to equity ratio

0

0.1

0.2

0.3

0.4

0.5

0.6 0.54

0.16

C Plc

D Plc

Liquidity ratio of C plc. Is better than D Plc. because the company is maintaining proper

current assets to pay against the current liabilities. Turnover ratios of D plc. Better than the C Plc.

Because the company is converting its debtors into cash and delay in paying to creditors. Gearing

Ratio of both the companies is good (Forde and et.al., 2016). Overall, the performance of both the

companies is good and should try to maintain this performance in future.

C Plc. is chemical manufacturer and D Plc. Is a departmental store because debtors of

departmental will be less than the manufacturing company. C Plc. Is having more debtors because

in any manufacturing company there are more debtors.

CONCLUSION

This report concludes the various analysis and interpretation of the various case studies

which are based on the companies performances. This report includes the journal entries, ledgers

and trial balance of the company. It also includes the summary of the company on the basis of the

past performance of the company. The report shows that by using ratio analysis also there can be

analysis of the company's performance.

0

0.1

0.2

0.3

0.4

0.5

0.6 0.54

0.16

C Plc

D Plc

Liquidity ratio of C plc. Is better than D Plc. because the company is maintaining proper

current assets to pay against the current liabilities. Turnover ratios of D plc. Better than the C Plc.

Because the company is converting its debtors into cash and delay in paying to creditors. Gearing

Ratio of both the companies is good (Forde and et.al., 2016). Overall, the performance of both the

companies is good and should try to maintain this performance in future.

C Plc. is chemical manufacturer and D Plc. Is a departmental store because debtors of

departmental will be less than the manufacturing company. C Plc. Is having more debtors because

in any manufacturing company there are more debtors.

CONCLUSION

This report concludes the various analysis and interpretation of the various case studies

which are based on the companies performances. This report includes the journal entries, ledgers

and trial balance of the company. It also includes the summary of the company on the basis of the

past performance of the company. The report shows that by using ratio analysis also there can be

analysis of the company's performance.

REFERENCES

Books and Journals

Abernathy, J. L. And et.al, 2017. Income statement reporting discretion allowed by FIN 48: Interest

and penalty expense classification. The Journal of the American Taxation

Association. 39(1). pp.45-66.

Easton, M. and et.al., 2018. Financial Statement Analysis & Valuation. 5e.

Forde, M. C. And et.al., 2016. Predicting the Ultimate Load Capacity of Concrete Bridge Beams

from the" Relaxation Ratio" Analysis of AE Signals. Progress in Acoustic Emission. 18.

pp.359-364.

Online

Ratio Analysis. [Online]. Available through: <https://www.accountingtools.com/articles/ratio-

analysis.html >.

Books and Journals

Abernathy, J. L. And et.al, 2017. Income statement reporting discretion allowed by FIN 48: Interest

and penalty expense classification. The Journal of the American Taxation

Association. 39(1). pp.45-66.

Easton, M. and et.al., 2018. Financial Statement Analysis & Valuation. 5e.

Forde, M. C. And et.al., 2016. Predicting the Ultimate Load Capacity of Concrete Bridge Beams

from the" Relaxation Ratio" Analysis of AE Signals. Progress in Acoustic Emission. 18.

pp.359-364.

Online

Ratio Analysis. [Online]. Available through: <https://www.accountingtools.com/articles/ratio-

analysis.html >.

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.