The Impact of Input Costs and Competition on Supply Decisions

VerifiedAdded on 2023/06/18

|13

|3291

|156

Report

AI Summary

This report examines the influence of input costs and perfect competition on supply decisions within the UK economy between 2010 and 2020. It begins by explaining how input costs, including land, labor, capital, and raw materials, affect production decisions and profitability, referencing the law of supply and demand. The report also discusses fixed and variable costs, average fixed and variable costs, and their impact on supply. Furthermore, it analyzes how factors like personnel costs, capital management, raw material allocation, and entrepreneurship influence manufacturing choices. The second part of the report defines perfect competition, emphasizing the role of price-taking producers and consumers, the importance of a large number of producers with small market shares, and the presence of standardized products. Finally, the report explains the supply curve in perfect competition, differentiating between short-run and long-run decision-making, highlighting the significance of costs, revenue, and shutdown points in determining profitability.

Economics for

business

business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Why input and costs impact production decisions related to supply of goods and services. .1

Definition and explanation of perfect competition or highly competitive markets impact on

supply of goods and services..................................................................................................4

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Why input and costs impact production decisions related to supply of goods and services. .1

Definition and explanation of perfect competition or highly competitive markets impact on

supply of goods and services..................................................................................................4

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Economics is defined as a social science which investigates production, distribution and

consumption of goods and services (Maresova and et. al., 2018). This report identifies the reason

behind the impact of input and costs on the production decisions related to supply chains in

context of the UK economy between 2010 and 2020. In addition to this, the impact of perfect

competition on supply of goods and services is explained in this report.

MAIN BODY

Why input and costs impact production decisions related to supply of goods and services

As per the law of supply and demand, if an economic commodity has high prices that the

demand from buyers will be low while the supply from buyers will be high. Similarly, if the

price of an economic good is low demand from buyers will be high while the supply from the

buyers will be low (Soelton and et. al., 2020). This is related to the decision making done for

supply of goods and services. The cost producing a specific commodity affects the price of the

commodity as producers aim to maximise profitability from each sale. Therefore, costs play an

important role in decision making of supply of goods and services as this element helps the

producers enhance profits. The law of supply and demand is depicted graphically below:

1

Economics is defined as a social science which investigates production, distribution and

consumption of goods and services (Maresova and et. al., 2018). This report identifies the reason

behind the impact of input and costs on the production decisions related to supply chains in

context of the UK economy between 2010 and 2020. In addition to this, the impact of perfect

competition on supply of goods and services is explained in this report.

MAIN BODY

Why input and costs impact production decisions related to supply of goods and services

As per the law of supply and demand, if an economic commodity has high prices that the

demand from buyers will be low while the supply from buyers will be high. Similarly, if the

price of an economic good is low demand from buyers will be high while the supply from the

buyers will be low (Soelton and et. al., 2020). This is related to the decision making done for

supply of goods and services. The cost producing a specific commodity affects the price of the

commodity as producers aim to maximise profitability from each sale. Therefore, costs play an

important role in decision making of supply of goods and services as this element helps the

producers enhance profits. The law of supply and demand is depicted graphically below:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above graph it is determined that, the supply of specific commodity is directly

related to the product. This can be seen as the price reaches from P3 to P1, the increase is also

reflected in increase in supply of commodities. Low price of commodity leads to low supply of

products or services.

The production function refers to the relationship between quantity of input used and

quantity of output produced by the firm. The output produced by the firm dictates the level of

supply of goods and services (Arnott, Lizama and Song, 2017). The decisions made in context of

supply of goods and services are dependent on input. This includes both fixed input and variable

inputs. Fixed inputs as input whose quantity is fixed over period of time such as land while the

quantity of variable input changes with time such as labour. The quantity of output is dependent

on the quantity of variable input for specific quantity of fixed input. This showcases the relation

between input and the put-put produced. Thus decisions relation to the supply of products and

services are dependent on the quantity of variable input present at the company for specific

period of time.

There is also the concept of demising returns to an input. This refers to the decline in

marginal product of an input when the quantity of the input is increased keeping all other inputs

fixes. Marginal product of an input is defined as change in output gained from using additional

unite of the specific input assuming that the concepts of other inputs remain content. This

showcases that input affects the output produced and is considered a critical element in decision

making related to supply of goods and services.

The inputs which affect the quantity of output produced, and are considered during making

decisions related to controlling supply of gods and services are explained below:

Land: This is an example of fixed input. From an economic point of view, land refers to

renewable and non-renewable resources along with sea oceans and rivers (Lipton and

Treccani, 2021). In case of short-run production this is considered a fixed input because it

provides the company capacity of constraint for sort-run production at a firm.

Labour: This input is variable input in most industries. This input refers the intellectual

and corporeal actions conducted by the employees of the company for the production of

specific commodity. The amount of output produced by specific employee is the

measured labour of the employee. This is considered a variable cost in short-run

2

related to the product. This can be seen as the price reaches from P3 to P1, the increase is also

reflected in increase in supply of commodities. Low price of commodity leads to low supply of

products or services.

The production function refers to the relationship between quantity of input used and

quantity of output produced by the firm. The output produced by the firm dictates the level of

supply of goods and services (Arnott, Lizama and Song, 2017). The decisions made in context of

supply of goods and services are dependent on input. This includes both fixed input and variable

inputs. Fixed inputs as input whose quantity is fixed over period of time such as land while the

quantity of variable input changes with time such as labour. The quantity of output is dependent

on the quantity of variable input for specific quantity of fixed input. This showcases the relation

between input and the put-put produced. Thus decisions relation to the supply of products and

services are dependent on the quantity of variable input present at the company for specific

period of time.

There is also the concept of demising returns to an input. This refers to the decline in

marginal product of an input when the quantity of the input is increased keeping all other inputs

fixes. Marginal product of an input is defined as change in output gained from using additional

unite of the specific input assuming that the concepts of other inputs remain content. This

showcases that input affects the output produced and is considered a critical element in decision

making related to supply of goods and services.

The inputs which affect the quantity of output produced, and are considered during making

decisions related to controlling supply of gods and services are explained below:

Land: This is an example of fixed input. From an economic point of view, land refers to

renewable and non-renewable resources along with sea oceans and rivers (Lipton and

Treccani, 2021). In case of short-run production this is considered a fixed input because it

provides the company capacity of constraint for sort-run production at a firm.

Labour: This input is variable input in most industries. This input refers the intellectual

and corporeal actions conducted by the employees of the company for the production of

specific commodity. The amount of output produced by specific employee is the

measured labour of the employee. This is considered a variable cost in short-run

2

production because the quantity of this input can vary any time on the basis of the

productivity of the workforce of employees recently hired or terminated by the company.

Capital: This is a commonly used example of fixed input (Susskind and Vines, 2020).

The amount of money available at the company is termed as the capital of the firm. It

includes machinery, equipment, production plants etc. This input remains fixed in the

short-run and defines the maximum output of the company. In this way the capital of the

company affects the supply of goods and services in short-run.

Raw material: This is another example of variable costs. The material cost includes the

amount of raw material is purchased for producing specific quantity of goods or services.

This is variable input because it can be changed by the company at any point of time in

case of short run production.

Cost is defined as the amount of money paid by the company for various input used in

production. The total costs for specific quantity of output affects the decision making related to

supply of goods and services as it is used to increase profitability of the company. The total

costs for creating a specific quantity of output is the sum of fixed costs and variable cost of

producing the specific output. Fixed costs refer to the cost which is not dependent on the quantity

of output produced. It is also referred to as overhead costs and are the costs of fixed input.

Variable costs are defined as the costs that are dependent on the output produced. It is the costs

associated with variable input. Average fixed and Average variable costs are the cost per unit

output (Cox, Craig and Tourish, 2018).

As per the spreading effect large quantity of output increases the quantity of output over

which the fixed costs are spread which leads to lower average fixed costs. According to the

diminishing effect, larger quantity of output increases the amount of variable input needed to

produce additional units. This increases average variable costs. Business firms consider average

fixed and variable costs in decision making of supply of goods and services because controlling

these costs leads to higher profitability while also supplying adequate amount of goods and

services to the consumers. These costs are dependent on variable and fixed inputs, these factors

are also taken into consideration during production decision making.

Influence on manufacture choices

Costs of Personnel: This variable input influenced as it is related to the current GDP

of the country. In case of UK, the rise in price of the products affects the Gross

3

productivity of the workforce of employees recently hired or terminated by the company.

Capital: This is a commonly used example of fixed input (Susskind and Vines, 2020).

The amount of money available at the company is termed as the capital of the firm. It

includes machinery, equipment, production plants etc. This input remains fixed in the

short-run and defines the maximum output of the company. In this way the capital of the

company affects the supply of goods and services in short-run.

Raw material: This is another example of variable costs. The material cost includes the

amount of raw material is purchased for producing specific quantity of goods or services.

This is variable input because it can be changed by the company at any point of time in

case of short run production.

Cost is defined as the amount of money paid by the company for various input used in

production. The total costs for specific quantity of output affects the decision making related to

supply of goods and services as it is used to increase profitability of the company. The total

costs for creating a specific quantity of output is the sum of fixed costs and variable cost of

producing the specific output. Fixed costs refer to the cost which is not dependent on the quantity

of output produced. It is also referred to as overhead costs and are the costs of fixed input.

Variable costs are defined as the costs that are dependent on the output produced. It is the costs

associated with variable input. Average fixed and Average variable costs are the cost per unit

output (Cox, Craig and Tourish, 2018).

As per the spreading effect large quantity of output increases the quantity of output over

which the fixed costs are spread which leads to lower average fixed costs. According to the

diminishing effect, larger quantity of output increases the amount of variable input needed to

produce additional units. This increases average variable costs. Business firms consider average

fixed and variable costs in decision making of supply of goods and services because controlling

these costs leads to higher profitability while also supplying adequate amount of goods and

services to the consumers. These costs are dependent on variable and fixed inputs, these factors

are also taken into consideration during production decision making.

Influence on manufacture choices

Costs of Personnel: This variable input influenced as it is related to the current GDP

of the country. In case of UK, the rise in price of the products affects the Gross

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

domestic product of the country. During the recession in 2010, supply reduced

because of this.

Capital: This fixed input plays an important role in economic growth of a country.

Ineffective decision making by the UK government in relation to mamnaging capital

and budget of the country hinders supply of goods and services and economic

prosperity of the region (Van Witteloostuijn, 2017).

Raw material: This is variable input which also influenced decisions related to

supply of goods and services. Timely allocation of raw material is important for

smooth functioning of the economy. Supply chain disruptions caused by US china

trade war in the year 2018 delayed supply of raw materials. This negatively affected

economic growth of the country.

Entrepreneurship: The decision making in context of supply of goods and services

is also influenced by entrepreneurship. In case of the UK economy, the change in

government in the year 2018 lead to satisfaction of various trade unions which

affected the supply of goods and services in the market.

Definition and explanation of perfect competition or highly competitive markets impact on

supply of goods and services

It is important to understand the concept of price taking producer in order to understand

perfect competition. A price taking producer refers to a producer who does not have the

ability to impact the market price of goods or services with actions or measures. This type of

producer looks at market price as given as the market price is remains unaffected by the

producer. On the other and a price taking consumer is defined as a consumer is defined as

consumer who does not impact the price of commodity purchased though their actions

(NUGROHO, HALIK and ARIF, 2020).

A simplistic definition of market with perfect competition is a market in which every

consumer and producer is a price taker. There are two conditions which need to be fulfilled

by market to become perfectly competitive. The first condition is that in order for an

industry to be competitive, it must have large number of producers with small market share.

The marker share of a producer in a perfectly competitive market is fraction of the total

industry output accounted for by the production of the specific manufacturer (Essentials of

Economics, 2020).

4

because of this.

Capital: This fixed input plays an important role in economic growth of a country.

Ineffective decision making by the UK government in relation to mamnaging capital

and budget of the country hinders supply of goods and services and economic

prosperity of the region (Van Witteloostuijn, 2017).

Raw material: This is variable input which also influenced decisions related to

supply of goods and services. Timely allocation of raw material is important for

smooth functioning of the economy. Supply chain disruptions caused by US china

trade war in the year 2018 delayed supply of raw materials. This negatively affected

economic growth of the country.

Entrepreneurship: The decision making in context of supply of goods and services

is also influenced by entrepreneurship. In case of the UK economy, the change in

government in the year 2018 lead to satisfaction of various trade unions which

affected the supply of goods and services in the market.

Definition and explanation of perfect competition or highly competitive markets impact on

supply of goods and services

It is important to understand the concept of price taking producer in order to understand

perfect competition. A price taking producer refers to a producer who does not have the

ability to impact the market price of goods or services with actions or measures. This type of

producer looks at market price as given as the market price is remains unaffected by the

producer. On the other and a price taking consumer is defined as a consumer is defined as

consumer who does not impact the price of commodity purchased though their actions

(NUGROHO, HALIK and ARIF, 2020).

A simplistic definition of market with perfect competition is a market in which every

consumer and producer is a price taker. There are two conditions which need to be fulfilled

by market to become perfectly competitive. The first condition is that in order for an

industry to be competitive, it must have large number of producers with small market share.

The marker share of a producer in a perfectly competitive market is fraction of the total

industry output accounted for by the production of the specific manufacturer (Essentials of

Economics, 2020).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The scorned condition required for market to be perfectly competitive it is essential that

consumers consider each product to be of equal quality. In other words, a competitive

market deals in standardized products where consumers regard the product to be of same

quality even if it is from different brands. It is also referred to as commodity. In a perfectly

competitive market, standardized products are present in which consumers consider products

of different brands to be of the same quality (PRAMONO and et. al., 2021).

Apart from this, free entry and exit is another characteristic of perfectly competitive market

which is not an essential characteristic. This characteristic states that producers can easily

enter the industry and exiting producers can easily leave the industry. Therefore, it is

determining that a competitive market fulfils the two conditions. The first condition of

producer’s market share being fraction of market share of the company and the second

condition of presence of standardized goods. Most competitive market shares the

characteristic of free entry and exit, although it is not an essential characteristic.

Supply Curve in Perfect Competition

The supply curve depicts the relationship between price of a good and total production

output of the industry as a singular entity. The supply curve is created on the basis of key

terms of marginal revenues and cost indication. The two concepts provided in the supply

curve of perfect competition are explained below:

Short-run decision making

In short run production one factor remains fixed whole other factor varies with passage of

time. In case of short-run production the main elements which affect decision making are

costs, revenue generated and process of shutting down the system. The supply curve in

perfectly competitive market of short run production consists of marginal costing curve line

being placed at or above the shutdown point (Alston, 2018). The graph provided below

depicts the supply curve in case of short run production.

5

consumers consider each product to be of equal quality. In other words, a competitive

market deals in standardized products where consumers regard the product to be of same

quality even if it is from different brands. It is also referred to as commodity. In a perfectly

competitive market, standardized products are present in which consumers consider products

of different brands to be of the same quality (PRAMONO and et. al., 2021).

Apart from this, free entry and exit is another characteristic of perfectly competitive market

which is not an essential characteristic. This characteristic states that producers can easily

enter the industry and exiting producers can easily leave the industry. Therefore, it is

determining that a competitive market fulfils the two conditions. The first condition of

producer’s market share being fraction of market share of the company and the second

condition of presence of standardized goods. Most competitive market shares the

characteristic of free entry and exit, although it is not an essential characteristic.

Supply Curve in Perfect Competition

The supply curve depicts the relationship between price of a good and total production

output of the industry as a singular entity. The supply curve is created on the basis of key

terms of marginal revenues and cost indication. The two concepts provided in the supply

curve of perfect competition are explained below:

Short-run decision making

In short run production one factor remains fixed whole other factor varies with passage of

time. In case of short-run production the main elements which affect decision making are

costs, revenue generated and process of shutting down the system. The supply curve in

perfectly competitive market of short run production consists of marginal costing curve line

being placed at or above the shutdown point (Alston, 2018). The graph provided below

depicts the supply curve in case of short run production.

5

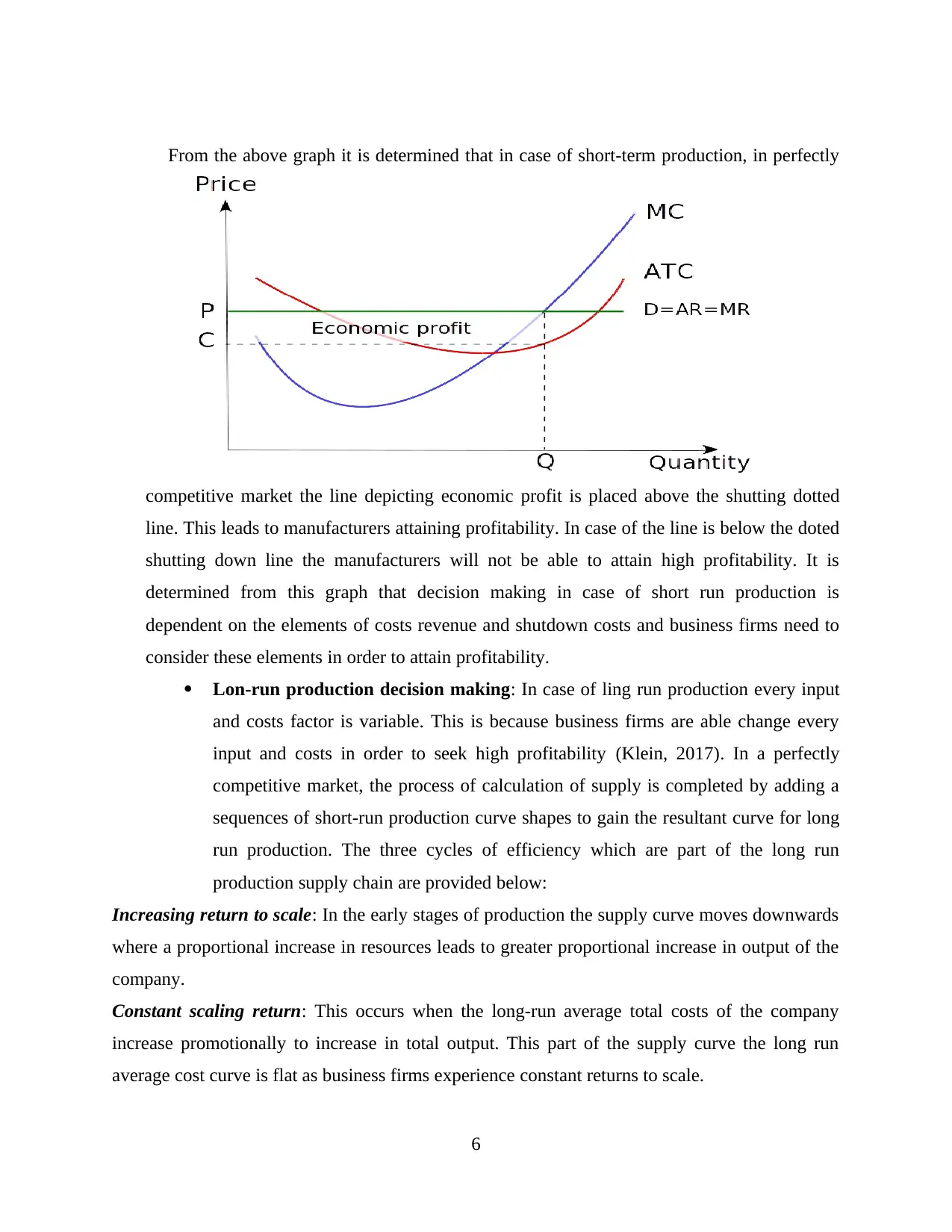

From the above graph it is determined that in case of short-term production, in perfectly

competitive market the line depicting economic profit is placed above the shutting dotted

line. This leads to manufacturers attaining profitability. In case of the line is below the doted

shutting down line the manufacturers will not be able to attain high profitability. It is

determined from this graph that decision making in case of short run production is

dependent on the elements of costs revenue and shutdown costs and business firms need to

consider these elements in order to attain profitability.

Lon-run production decision making: In case of ling run production every input

and costs factor is variable. This is because business firms are able change every

input and costs in order to seek high profitability (Klein, 2017). In a perfectly

competitive market, the process of calculation of supply is completed by adding a

sequences of short-run production curve shapes to gain the resultant curve for long

run production. The three cycles of efficiency which are part of the long run

production supply chain are provided below:

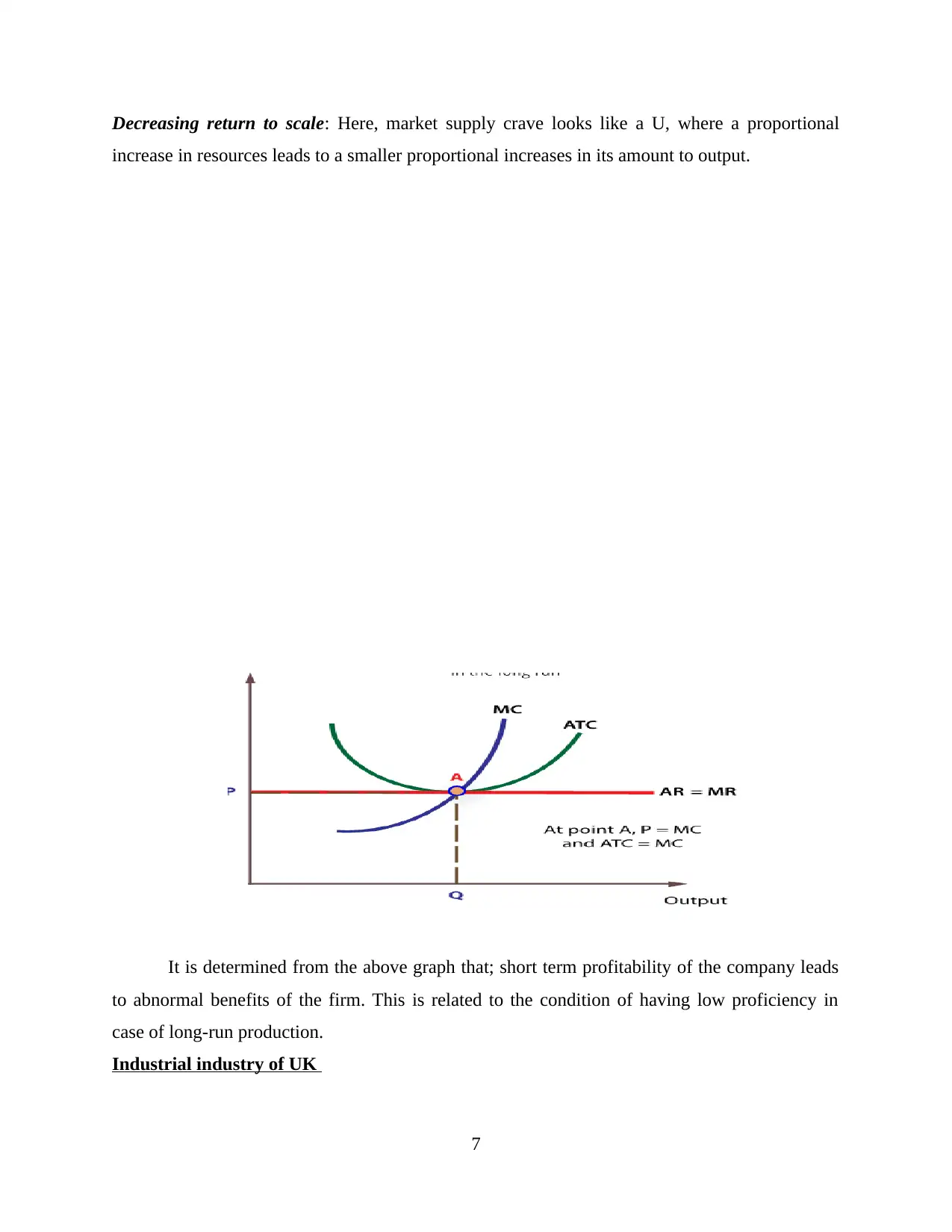

Increasing return to scale: In the early stages of production the supply curve moves downwards

where a proportional increase in resources leads to greater proportional increase in output of the

company.

Constant scaling return: This occurs when the long-run average total costs of the company

increase promotionally to increase in total output. This part of the supply curve the long run

average cost curve is flat as business firms experience constant returns to scale.

6

competitive market the line depicting economic profit is placed above the shutting dotted

line. This leads to manufacturers attaining profitability. In case of the line is below the doted

shutting down line the manufacturers will not be able to attain high profitability. It is

determined from this graph that decision making in case of short run production is

dependent on the elements of costs revenue and shutdown costs and business firms need to

consider these elements in order to attain profitability.

Lon-run production decision making: In case of ling run production every input

and costs factor is variable. This is because business firms are able change every

input and costs in order to seek high profitability (Klein, 2017). In a perfectly

competitive market, the process of calculation of supply is completed by adding a

sequences of short-run production curve shapes to gain the resultant curve for long

run production. The three cycles of efficiency which are part of the long run

production supply chain are provided below:

Increasing return to scale: In the early stages of production the supply curve moves downwards

where a proportional increase in resources leads to greater proportional increase in output of the

company.

Constant scaling return: This occurs when the long-run average total costs of the company

increase promotionally to increase in total output. This part of the supply curve the long run

average cost curve is flat as business firms experience constant returns to scale.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Decreasing return to scale: Here, market supply crave looks like a U, where a proportional

increase in resources leads to a smaller proportional increases in its amount to output.

It is determined from the above graph that; short term profitability of the company leads

to abnormal benefits of the firm. This is related to the condition of having low proficiency in

case of long-run production.

Industrial industry of UK

7

increase in resources leads to a smaller proportional increases in its amount to output.

It is determined from the above graph that; short term profitability of the company leads

to abnormal benefits of the firm. This is related to the condition of having low proficiency in

case of long-run production.

Industrial industry of UK

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The UK manufacturing industry consists of diverse sets of industries which includes

small business firms along with large international corporations. UK is economically developed

country which has created a manufacturing industry consisting of firms from different sectors

such as food and beverage, automobile, technology and home appliances. In a perfectly

competitive industry the supply of products is dependent by the specific environment of the

competitive industry (Gálová, Rajnoha and Ondra, 2018). The impact of perfect competition on

supply of products in UK is provided explained below;

Prices: The price of the product remain constant as both the buyers and producers

are price taking. This means that the actions of buyers and producers do not have

impact on the price of the products. An example of market price of product being

affected because of perfect competition in this way is IKEA. The company is retails

furniture in the UK the product offered by the company is ready to assemble

furniture in UK where the price of the product remains unchanged and the demand

for the products is equal to the total number of items produced.

Number of sellers: In case of perfect competition the number of producers in the

industry is infinite. This is because different brands sell standardized products

which considered to be of equal quality by the market (ALAM, ALAM and

CHAVALI, 2020). In addition to this in a perfectly competitive market there is not

barrier to entry which affects the ability of the producers to determine suitable

quantity of product which neds to be supplies in the market. In this way the supply

of an item is impacted because of perfect competition. This situation harms the UK

economy.

Competition: In a perfectly competitive market large number of competitors are

present. This means that every competitors has only small fraction of market share.

The large number of competitors present in the industry provide high quality goods

but sell them at low cost in order to earn profitability. This affects the supply of

products in the market.

8

small business firms along with large international corporations. UK is economically developed

country which has created a manufacturing industry consisting of firms from different sectors

such as food and beverage, automobile, technology and home appliances. In a perfectly

competitive industry the supply of products is dependent by the specific environment of the

competitive industry (Gálová, Rajnoha and Ondra, 2018). The impact of perfect competition on

supply of products in UK is provided explained below;

Prices: The price of the product remain constant as both the buyers and producers

are price taking. This means that the actions of buyers and producers do not have

impact on the price of the products. An example of market price of product being

affected because of perfect competition in this way is IKEA. The company is retails

furniture in the UK the product offered by the company is ready to assemble

furniture in UK where the price of the product remains unchanged and the demand

for the products is equal to the total number of items produced.

Number of sellers: In case of perfect competition the number of producers in the

industry is infinite. This is because different brands sell standardized products

which considered to be of equal quality by the market (ALAM, ALAM and

CHAVALI, 2020). In addition to this in a perfectly competitive market there is not

barrier to entry which affects the ability of the producers to determine suitable

quantity of product which neds to be supplies in the market. In this way the supply

of an item is impacted because of perfect competition. This situation harms the UK

economy.

Competition: In a perfectly competitive market large number of competitors are

present. This means that every competitors has only small fraction of market share.

The large number of competitors present in the industry provide high quality goods

but sell them at low cost in order to earn profitability. This affects the supply of

products in the market.

8

CONCLUSION

From the above report it is concluded that input and costs play an important role in making

decisions related to supply of goods and services. In case of perfect competition, the supply of

goods is affected by the large number of competitors, free entry and exit from the market and

low price of the product. In addition to this the perception of the consumer that every product is

of same quality also affects supply of product in perfect competition.

9

From the above report it is concluded that input and costs play an important role in making

decisions related to supply of goods and services. In case of perfect competition, the supply of

goods is affected by the large number of competitors, free entry and exit from the market and

low price of the product. In addition to this the perception of the consumer that every product is

of same quality also affects supply of product in perfect competition.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.