Business Finance Report: Capital Budgeting and Investment Analysis

VerifiedAdded on 2020/12/18

|11

|2888

|130

Report

AI Summary

This report delves into core concepts in business finance, addressing critical questions related to capital asset pricing model (CAPM), efficient capital markets, dividend valuation, and net present value (NPV). It explains how CAPM is used to assess investment risk and return, the significance of efficient capital markets for financial managers, and the assumptions underlying the dividend valuation model. Furthermore, the report elucidates NPV as a capital budgeting tool, demonstrating its application in project evaluation. The report also includes practical applications, such as evaluating investment in securities and calculating the weighted average cost of capital (WACC). The analysis includes calculations for WACC and NPV, providing a comprehensive understanding of financial decision-making processes. This report is a valuable resource for finance students seeking to understand key financial concepts and their practical implications.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

CLIENTS FINANCIAL QUESTIONS...........................................................................................1

1.Capital asset pricing method and how it is used for evaluating whether the expected return

on asset is sufficient to compensate the investor for the risk it takes..........................................1

2. What is efficient capital market and why it is necessary for financial managers?..................2

3. Identifying the assumptions for dividend valuation model......................................................3

4.Explaining Net Present Value as a capital budgetary tool and how it is used for the

evaluation of the investment........................................................................................................3

CLIENTS INVESTMENTS............................................................................................................4

1. Evaluating the information whether to invest in securities or not...........................................4

2. Weighted average cost of capital for the company (WACC)..................................................4

3. Calculation of Net present value of two projects.....................................................................6

CONCLUSION ...............................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

CLIENTS FINANCIAL QUESTIONS...........................................................................................1

1.Capital asset pricing method and how it is used for evaluating whether the expected return

on asset is sufficient to compensate the investor for the risk it takes..........................................1

2. What is efficient capital market and why it is necessary for financial managers?..................2

3. Identifying the assumptions for dividend valuation model......................................................3

4.Explaining Net Present Value as a capital budgetary tool and how it is used for the

evaluation of the investment........................................................................................................3

CLIENTS INVESTMENTS............................................................................................................4

1. Evaluating the information whether to invest in securities or not...........................................4

2. Weighted average cost of capital for the company (WACC)..................................................4

3. Calculation of Net present value of two projects.....................................................................6

CONCLUSION ...............................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION

Business finance can be described as such business activities which are concerned with

the procurement and conservation of capital funds for the purpose of meeting financial

requirements and overall goals and objectives of a business enterprise (Al-Mutairi, Naser and

Saeid, 2018). The present project report will cover the capital asset pricing model (CAPM) that

how it is used for evaluating whether the expected return on an asset is adequate to mitigate the

inherent risk. It will higher what is an efficient capital market and why it is necessary for

financial mangers. Further, it will show what is NPV along with calculations and dividend

valuation model.

CLIENTS FINANCIAL QUESTIONS

1.Capital asset pricing method and how it is used for evaluating whether the expected return on

asset is sufficient to compensate the investor for the risk it takes

In simple words, capital asset pricing method (CAPM) demonstrates the relationship

between the systematic risk and the expected return for assets, especially stocks and shares. The

CAPM model is used very commonly for pricing the securities that are characterised by high

risk. It was found by Harry Markowitz in 1952. As per the theory of CAPM, the expected return

of specific security or stocks/portfolio is equal to the rate of risk free security plus a risk

premium. If the security does not match with the expected return, then the investor is advised to

not to make the investment in those securities (Capital Asset Pricing Model (CAPM), 2019).

Formula of CAPM :

Expected return = Risk free rate + (Market return – Risk free rate)* Beta

The model takes into consideration the responsiveness or sensitivity of assets to the non

diversified risk or systematic risk or market risk which is commonly represented by the symbol

beta (β).

The theory of the model could be understood by taking an example. Lets assume the

current risk free rate is 6 % and the Australia stock exchange 200 is expected to yield 15% over

the next year. Now there is a company called ABC Ltd whose evaluation is required in terms of

its securities for the purpose of investment. It has ascertained that company's beta (systematic

risk) is 1.5 and the overall market has a beta which is 1. This shows that company has higher risk

as compared to market which in turn shows that securities of this company will provide more

return as compared to the overall market return which is 15%.

1

Business finance can be described as such business activities which are concerned with

the procurement and conservation of capital funds for the purpose of meeting financial

requirements and overall goals and objectives of a business enterprise (Al-Mutairi, Naser and

Saeid, 2018). The present project report will cover the capital asset pricing model (CAPM) that

how it is used for evaluating whether the expected return on an asset is adequate to mitigate the

inherent risk. It will higher what is an efficient capital market and why it is necessary for

financial mangers. Further, it will show what is NPV along with calculations and dividend

valuation model.

CLIENTS FINANCIAL QUESTIONS

1.Capital asset pricing method and how it is used for evaluating whether the expected return on

asset is sufficient to compensate the investor for the risk it takes

In simple words, capital asset pricing method (CAPM) demonstrates the relationship

between the systematic risk and the expected return for assets, especially stocks and shares. The

CAPM model is used very commonly for pricing the securities that are characterised by high

risk. It was found by Harry Markowitz in 1952. As per the theory of CAPM, the expected return

of specific security or stocks/portfolio is equal to the rate of risk free security plus a risk

premium. If the security does not match with the expected return, then the investor is advised to

not to make the investment in those securities (Capital Asset Pricing Model (CAPM), 2019).

Formula of CAPM :

Expected return = Risk free rate + (Market return – Risk free rate)* Beta

The model takes into consideration the responsiveness or sensitivity of assets to the non

diversified risk or systematic risk or market risk which is commonly represented by the symbol

beta (β).

The theory of the model could be understood by taking an example. Lets assume the

current risk free rate is 6 % and the Australia stock exchange 200 is expected to yield 15% over

the next year. Now there is a company called ABC Ltd whose evaluation is required in terms of

its securities for the purpose of investment. It has ascertained that company's beta (systematic

risk) is 1.5 and the overall market has a beta which is 1. This shows that company has higher risk

as compared to market which in turn shows that securities of this company will provide more

return as compared to the overall market return which is 15%.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expected return = 6% + (15%-6%)*1.5

= 27.15%

The above evaluation depicts that the investor by investing in the securities of ABS Ltd

will at least get 27.15% returns on its investment.

2. What is efficient capital market and why it is necessary for financial managers?

Capital market is a financial market in which the long term security usually for more than

a year or equity shares and securities are bought and sold by the investors. Capital markets

provides a platform where the wealth of investors/ savers are provided to those who utilises such

wealth for long term productive purpose. The players in the markets individuals, public financial

institutions, government etc (Andor, Mohanty and Toth, 2015).

A capital market is said to be efficient when the securities are priced in accordance with

their value given all publicly available information. Capital market efficiency analyse how much,

how quick and how accurately the information which is available publicly is incorporated into

the prices of securities. There are three categories in which this available information is

categorised. These are :

weak : In weak form efficiency, the prices of securities reflects the information contained

in the past returns and prices.

Semi-strong : In this type of efficiency, the prices of securities totally reflect all the

public information. This means that only those investors such as corporate insiders who

have insights of companies and secret information are able to earn profits on the stock

exchange

strong : In strong form of efficiency, the prices of securities reflects all the information

possible even the most confidential one. This means that no investors can make excess

profits in the capital market.

Efficiency of the capital market is important to financial mangers because the effect of

management of the companies is shown their respective share prices which decides the valuation

of the company in the market. Also, when the share price of a company is low, the financial

manger is restricted in raising and allocating its funds more optimally because investors do not

show much trust in the company whose securities prices are lower. This is because the investor

feels that company will not provide good returns if they invest in such company (Efficient

Capital Market, 2002).

2

= 27.15%

The above evaluation depicts that the investor by investing in the securities of ABS Ltd

will at least get 27.15% returns on its investment.

2. What is efficient capital market and why it is necessary for financial managers?

Capital market is a financial market in which the long term security usually for more than

a year or equity shares and securities are bought and sold by the investors. Capital markets

provides a platform where the wealth of investors/ savers are provided to those who utilises such

wealth for long term productive purpose. The players in the markets individuals, public financial

institutions, government etc (Andor, Mohanty and Toth, 2015).

A capital market is said to be efficient when the securities are priced in accordance with

their value given all publicly available information. Capital market efficiency analyse how much,

how quick and how accurately the information which is available publicly is incorporated into

the prices of securities. There are three categories in which this available information is

categorised. These are :

weak : In weak form efficiency, the prices of securities reflects the information contained

in the past returns and prices.

Semi-strong : In this type of efficiency, the prices of securities totally reflect all the

public information. This means that only those investors such as corporate insiders who

have insights of companies and secret information are able to earn profits on the stock

exchange

strong : In strong form of efficiency, the prices of securities reflects all the information

possible even the most confidential one. This means that no investors can make excess

profits in the capital market.

Efficiency of the capital market is important to financial mangers because the effect of

management of the companies is shown their respective share prices which decides the valuation

of the company in the market. Also, when the share price of a company is low, the financial

manger is restricted in raising and allocating its funds more optimally because investors do not

show much trust in the company whose securities prices are lower. This is because the investor

feels that company will not provide good returns if they invest in such company (Efficient

Capital Market, 2002).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Identifying the assumptions for dividend valuation model

Dividend valuation policy is a quantifiable method of forecasting the price of company's

stock which is based on the theory that stock's current price is worth the sum of all of its

upcoming dividend payments when these payments are discounted back to their present value.

The objective of dividend valuation model is to calculate the fair value of stock of the company

which is irrespective of the conditions prevailing in the market. It takes into account dividend

payout factors and expected returns of overall market (Abor, 2017).

Value of stock = Expected dividend per share/(cost of equity – dividend growth rate)

If the value of the stock ascertained by using DDM model is greater than the current price

trading on the stock exchange, then the stock of a particular company said to be undervalued and

is advisable to the investor to buy the shares of undervalued company and vice versa.

Assumptions of the Dividend valuation model:

Consistent dividend payout

model is based on assumption that it applies only to those companies that pay regular

dividends

it does not consider the current market conditions

rate of equity is calculated by using CAPM

Assumption regarding estimating future dividends of company (Ang, 2018)

4.Explaining Net Present Value as a capital budgetary tool and how it is used for the evaluation

of the investment

Net present value can be referred to as the difference between the present value of cash

flows from an investment and the cost of acquiring investment. In capital budgeting, NPV

method is used for evaluating and analysing the profitability of a project or capital investment.

NPV = Discounted value of cash flows – cost of investment

It is used for evaluating whether a project should be taken up or not. It helps company in

by telling it whether taking up of a particular project or investment will add an value to company

or not (Smit and Trigeorgis,2017). If the NPV of a project or investment is positive, it indicates

that project should be accepted by the person as it will add value to its wealth whereas if the

NPV is negative, it indicates that investment should not be accepted by the person as it will not

add value to the wealth of the person instead it will bring losses for the person in the future.

3

Dividend valuation policy is a quantifiable method of forecasting the price of company's

stock which is based on the theory that stock's current price is worth the sum of all of its

upcoming dividend payments when these payments are discounted back to their present value.

The objective of dividend valuation model is to calculate the fair value of stock of the company

which is irrespective of the conditions prevailing in the market. It takes into account dividend

payout factors and expected returns of overall market (Abor, 2017).

Value of stock = Expected dividend per share/(cost of equity – dividend growth rate)

If the value of the stock ascertained by using DDM model is greater than the current price

trading on the stock exchange, then the stock of a particular company said to be undervalued and

is advisable to the investor to buy the shares of undervalued company and vice versa.

Assumptions of the Dividend valuation model:

Consistent dividend payout

model is based on assumption that it applies only to those companies that pay regular

dividends

it does not consider the current market conditions

rate of equity is calculated by using CAPM

Assumption regarding estimating future dividends of company (Ang, 2018)

4.Explaining Net Present Value as a capital budgetary tool and how it is used for the evaluation

of the investment

Net present value can be referred to as the difference between the present value of cash

flows from an investment and the cost of acquiring investment. In capital budgeting, NPV

method is used for evaluating and analysing the profitability of a project or capital investment.

NPV = Discounted value of cash flows – cost of investment

It is used for evaluating whether a project should be taken up or not. It helps company in

by telling it whether taking up of a particular project or investment will add an value to company

or not (Smit and Trigeorgis,2017). If the NPV of a project or investment is positive, it indicates

that project should be accepted by the person as it will add value to its wealth whereas if the

NPV is negative, it indicates that investment should not be accepted by the person as it will not

add value to the wealth of the person instead it will bring losses for the person in the future.

3

This method ODF evaluating the viability and profitability of project or investment is one

of the most sought after method as it considers the time value of money. It considers that future

worth of currency will less than the current worth of the currency/ Thus, it discounts the future

cash flows to find out their current worth (Turner, 2017).

CLIENTS INVESTMENTS

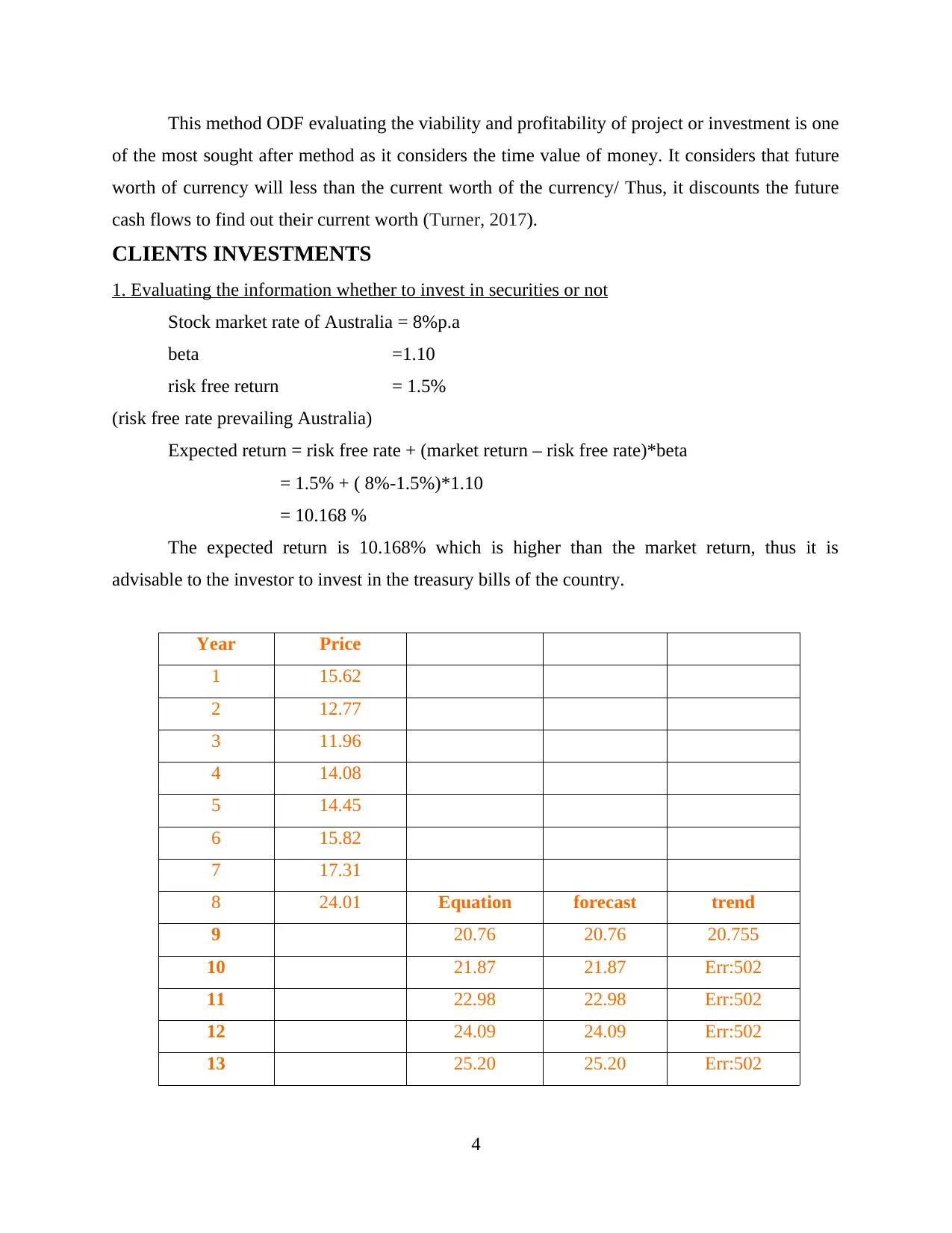

1. Evaluating the information whether to invest in securities or not

Stock market rate of Australia = 8%p.a

beta =1.10

risk free return = 1.5%

(risk free rate prevailing Australia)

Expected return = risk free rate + (market return – risk free rate)*beta

= 1.5% + ( 8%-1.5%)*1.10

= 10.168 %

The expected return is 10.168% which is higher than the market return, thus it is

advisable to the investor to invest in the treasury bills of the country.

Year Price

1 15.62

2 12.77

3 11.96

4 14.08

5 14.45

6 15.82

7 17.31

8 24.01 Equation forecast trend

9 20.76 20.76 20.755

10 21.87 21.87 Err:502

11 22.98 22.98 Err:502

12 24.09 24.09 Err:502

13 25.20 25.20 Err:502

4

of the most sought after method as it considers the time value of money. It considers that future

worth of currency will less than the current worth of the currency/ Thus, it discounts the future

cash flows to find out their current worth (Turner, 2017).

CLIENTS INVESTMENTS

1. Evaluating the information whether to invest in securities or not

Stock market rate of Australia = 8%p.a

beta =1.10

risk free return = 1.5%

(risk free rate prevailing Australia)

Expected return = risk free rate + (market return – risk free rate)*beta

= 1.5% + ( 8%-1.5%)*1.10

= 10.168 %

The expected return is 10.168% which is higher than the market return, thus it is

advisable to the investor to invest in the treasury bills of the country.

Year Price

1 15.62

2 12.77

3 11.96

4 14.08

5 14.45

6 15.82

7 17.31

8 24.01 Equation forecast trend

9 20.76 20.76 20.755

10 21.87 21.87 Err:502

11 22.98 22.98 Err:502

12 24.09 24.09 Err:502

13 25.20 25.20 Err:502

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

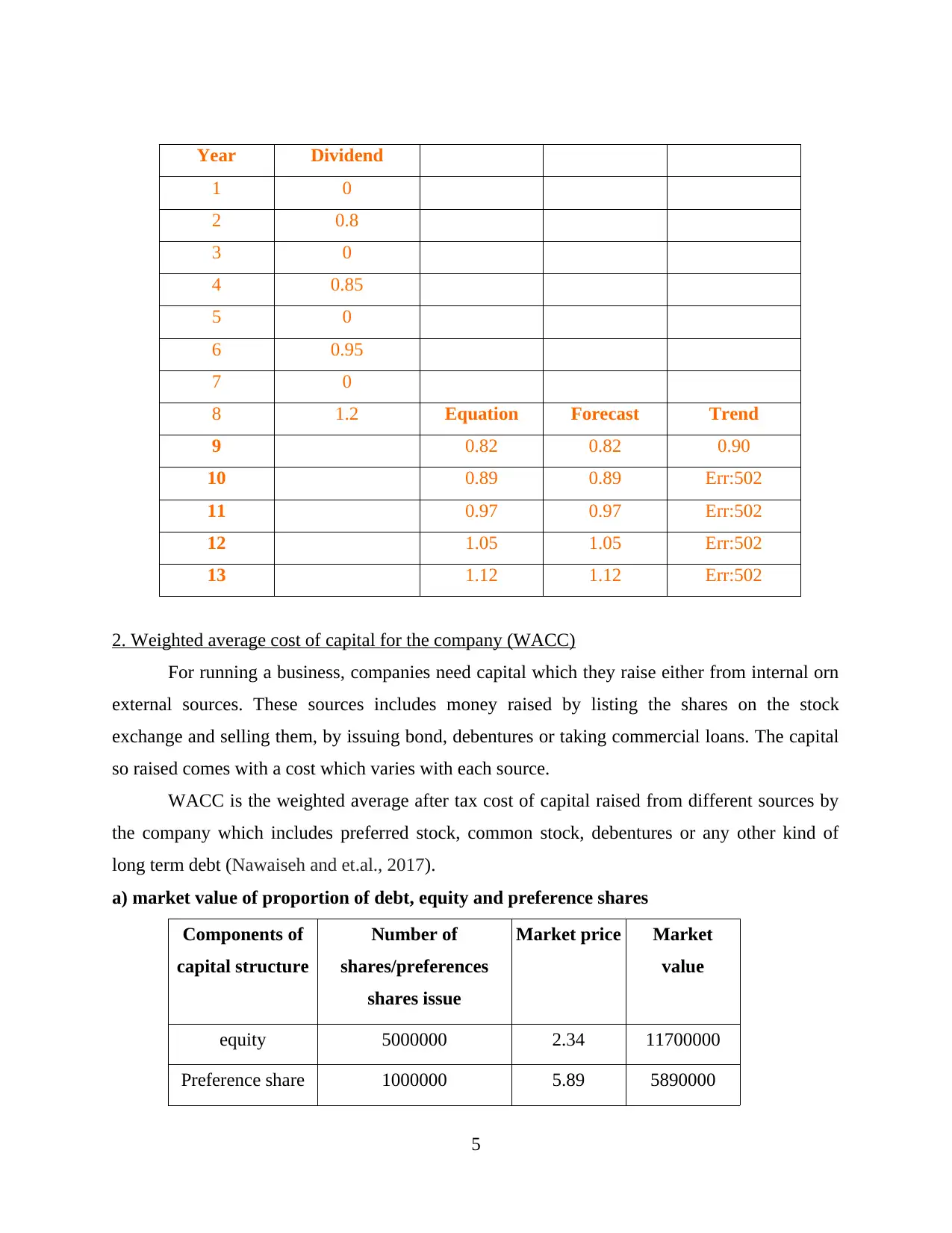

Year Dividend

1 0

2 0.8

3 0

4 0.85

5 0

6 0.95

7 0

8 1.2 Equation Forecast Trend

9 0.82 0.82 0.90

10 0.89 0.89 Err:502

11 0.97 0.97 Err:502

12 1.05 1.05 Err:502

13 1.12 1.12 Err:502

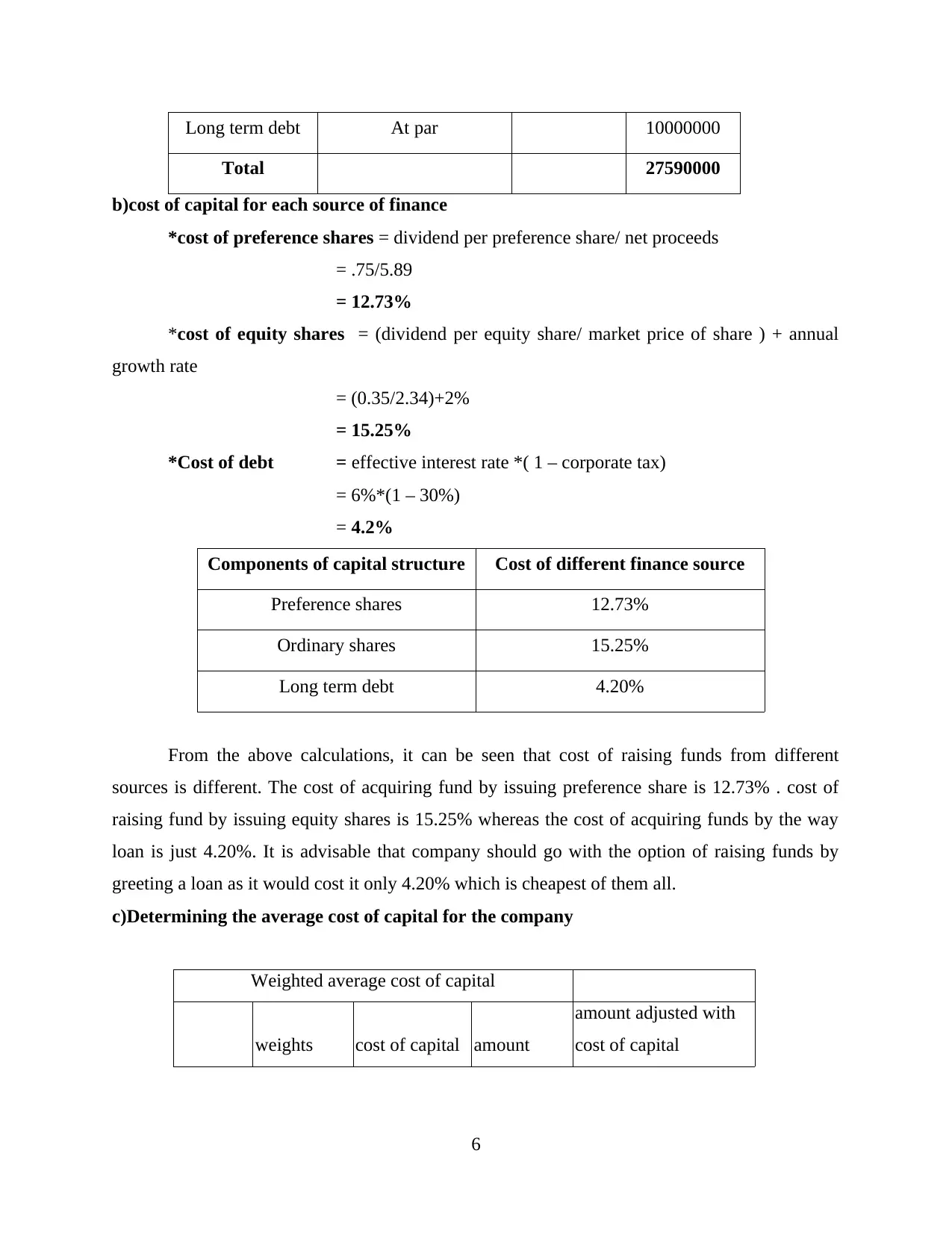

2. Weighted average cost of capital for the company (WACC)

For running a business, companies need capital which they raise either from internal orn

external sources. These sources includes money raised by listing the shares on the stock

exchange and selling them, by issuing bond, debentures or taking commercial loans. The capital

so raised comes with a cost which varies with each source.

WACC is the weighted average after tax cost of capital raised from different sources by

the company which includes preferred stock, common stock, debentures or any other kind of

long term debt (Nawaiseh and et.al., 2017).

a) market value of proportion of debt, equity and preference shares

Components of

capital structure

Number of

shares/preferences

shares issue

Market price Market

value

equity 5000000 2.34 11700000

Preference share 1000000 5.89 5890000

5

1 0

2 0.8

3 0

4 0.85

5 0

6 0.95

7 0

8 1.2 Equation Forecast Trend

9 0.82 0.82 0.90

10 0.89 0.89 Err:502

11 0.97 0.97 Err:502

12 1.05 1.05 Err:502

13 1.12 1.12 Err:502

2. Weighted average cost of capital for the company (WACC)

For running a business, companies need capital which they raise either from internal orn

external sources. These sources includes money raised by listing the shares on the stock

exchange and selling them, by issuing bond, debentures or taking commercial loans. The capital

so raised comes with a cost which varies with each source.

WACC is the weighted average after tax cost of capital raised from different sources by

the company which includes preferred stock, common stock, debentures or any other kind of

long term debt (Nawaiseh and et.al., 2017).

a) market value of proportion of debt, equity and preference shares

Components of

capital structure

Number of

shares/preferences

shares issue

Market price Market

value

equity 5000000 2.34 11700000

Preference share 1000000 5.89 5890000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

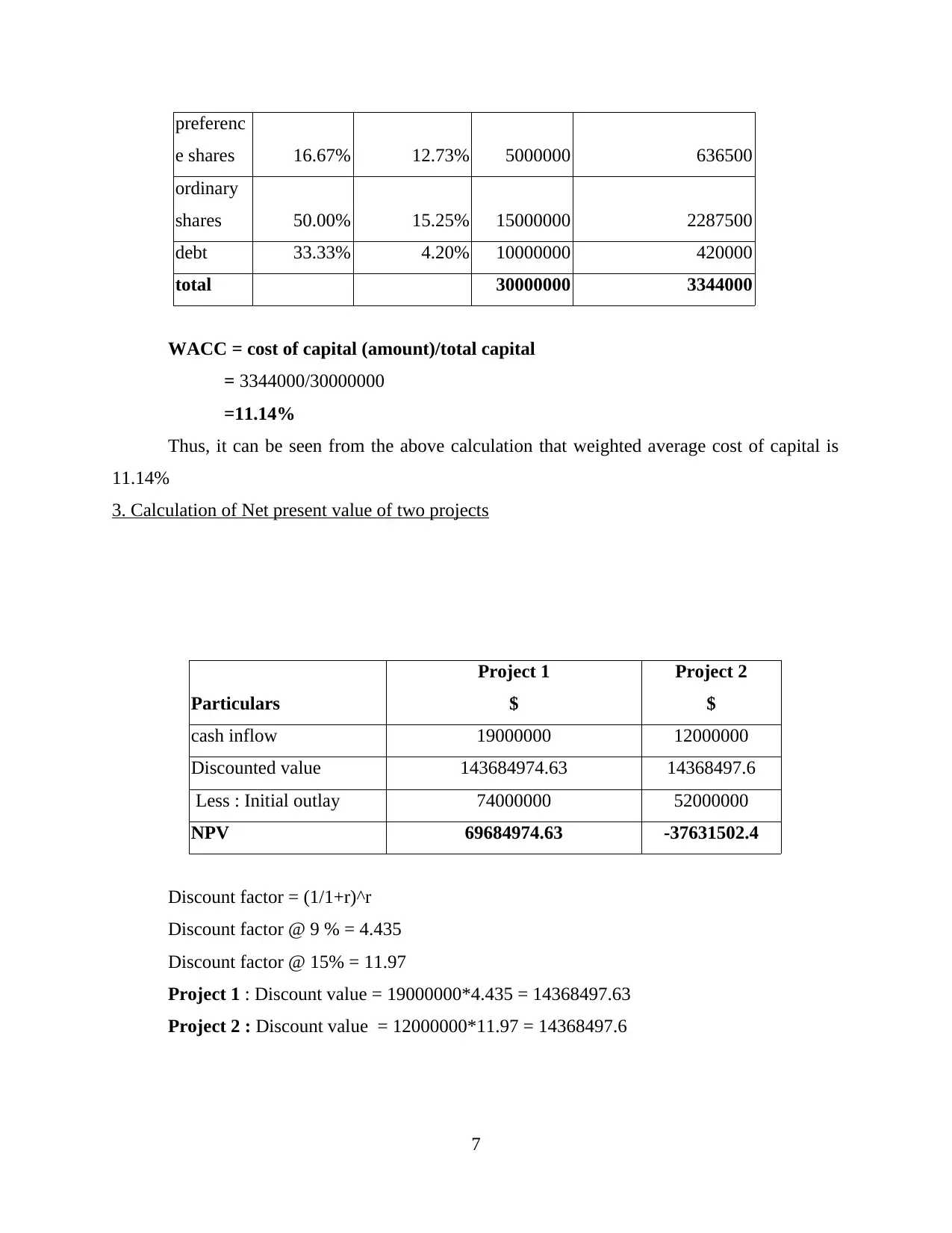

Long term debt At par 10000000

Total 27590000

b)cost of capital for each source of finance

*cost of preference shares = dividend per preference share/ net proceeds

= .75/5.89

= 12.73%

*cost of equity shares = (dividend per equity share/ market price of share ) + annual

growth rate

= (0.35/2.34)+2%

= 15.25%

*Cost of debt = effective interest rate *( 1 – corporate tax)

= 6%*(1 – 30%)

= 4.2%

Components of capital structure Cost of different finance source

Preference shares 12.73%

Ordinary shares 15.25%

Long term debt 4.20%

From the above calculations, it can be seen that cost of raising funds from different

sources is different. The cost of acquiring fund by issuing preference share is 12.73% . cost of

raising fund by issuing equity shares is 15.25% whereas the cost of acquiring funds by the way

loan is just 4.20%. It is advisable that company should go with the option of raising funds by

greeting a loan as it would cost it only 4.20% which is cheapest of them all.

c)Determining the average cost of capital for the company

Weighted average cost of capital

weights cost of capital amount

amount adjusted with

cost of capital

6

Total 27590000

b)cost of capital for each source of finance

*cost of preference shares = dividend per preference share/ net proceeds

= .75/5.89

= 12.73%

*cost of equity shares = (dividend per equity share/ market price of share ) + annual

growth rate

= (0.35/2.34)+2%

= 15.25%

*Cost of debt = effective interest rate *( 1 – corporate tax)

= 6%*(1 – 30%)

= 4.2%

Components of capital structure Cost of different finance source

Preference shares 12.73%

Ordinary shares 15.25%

Long term debt 4.20%

From the above calculations, it can be seen that cost of raising funds from different

sources is different. The cost of acquiring fund by issuing preference share is 12.73% . cost of

raising fund by issuing equity shares is 15.25% whereas the cost of acquiring funds by the way

loan is just 4.20%. It is advisable that company should go with the option of raising funds by

greeting a loan as it would cost it only 4.20% which is cheapest of them all.

c)Determining the average cost of capital for the company

Weighted average cost of capital

weights cost of capital amount

amount adjusted with

cost of capital

6

preferenc

e shares 16.67% 12.73% 5000000 636500

ordinary

shares 50.00% 15.25% 15000000 2287500

debt 33.33% 4.20% 10000000 420000

total 30000000 3344000

WACC = cost of capital (amount)/total capital

= 3344000/30000000

=11.14%

Thus, it can be seen from the above calculation that weighted average cost of capital is

11.14%

3. Calculation of Net present value of two projects

Particulars

Project 1

$

Project 2

$

cash inflow 19000000 12000000

Discounted value 143684974.63 14368497.6

Less : Initial outlay 74000000 52000000

NPV 69684974.63 -37631502.4

Discount factor = (1/1+r)^r

Discount factor @ 9 % = 4.435

Discount factor @ 15% = 11.97

Project 1 : Discount value = 19000000*4.435 = 14368497.63

Project 2 : Discount value = 12000000*11.97 = 14368497.6

7

e shares 16.67% 12.73% 5000000 636500

ordinary

shares 50.00% 15.25% 15000000 2287500

debt 33.33% 4.20% 10000000 420000

total 30000000 3344000

WACC = cost of capital (amount)/total capital

= 3344000/30000000

=11.14%

Thus, it can be seen from the above calculation that weighted average cost of capital is

11.14%

3. Calculation of Net present value of two projects

Particulars

Project 1

$

Project 2

$

cash inflow 19000000 12000000

Discounted value 143684974.63 14368497.6

Less : Initial outlay 74000000 52000000

NPV 69684974.63 -37631502.4

Discount factor = (1/1+r)^r

Discount factor @ 9 % = 4.435

Discount factor @ 15% = 11.97

Project 1 : Discount value = 19000000*4.435 = 14368497.63

Project 2 : Discount value = 12000000*11.97 = 14368497.6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation : From the above calculation, it can be interpreted that the NPV of project

1 is positive at the $ 69684974.63 as compared to the project 2 whose NPV is negative which is

$-37631502.4. The scientist is advisable to accept the project 1 because the net present value of

the cash flow of it is positive which means that this project will add value to the wealth of the

client while project 2 which have the negative NPV will bring losses to the client if the

investment is done in it. Thus, project 1 should be accepted by the client.

CONCLUSION

From the above project report, it can be summarised that business finance is the most

essential thing without which a company cannot be run. Finance is required for undertaking all

the commercial activities for which an organisation has been set up. Procuring finance and

optimally allocating to the most productive use is the main purpose of financial management. In

the project report, it was seen that before making huge investment in a project or asset, it is

advisable to look into the viability and profitability of the asset intending to be purchased. This is

necessary because the amount involved in investment is so huge that it decision went wrong, it

can bring huge losses for the company. Evaluation of the project could be done by using NPV

method which analyses the profitability of the different project that tells which project should be

taken up and which not.

8

1 is positive at the $ 69684974.63 as compared to the project 2 whose NPV is negative which is

$-37631502.4. The scientist is advisable to accept the project 1 because the net present value of

the cash flow of it is positive which means that this project will add value to the wealth of the

client while project 2 which have the negative NPV will bring losses to the client if the

investment is done in it. Thus, project 1 should be accepted by the client.

CONCLUSION

From the above project report, it can be summarised that business finance is the most

essential thing without which a company cannot be run. Finance is required for undertaking all

the commercial activities for which an organisation has been set up. Procuring finance and

optimally allocating to the most productive use is the main purpose of financial management. In

the project report, it was seen that before making huge investment in a project or asset, it is

advisable to look into the viability and profitability of the asset intending to be purchased. This is

necessary because the amount involved in investment is so huge that it decision went wrong, it

can bring huge losses for the company. Evaluation of the project could be done by using NPV

method which analyses the profitability of the different project that tells which project should be

taken up and which not.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abor, J.Y., 2017. Evaluating Capital Investment Decisions: Capital Budgeting.

In Entrepreneurial Finance for MSMEs (pp. 293-320). Palgrave Macmillan, Cham.

Al-Mutairi, A., Naser, K. and Saeid, M., 2018. Capital budgeting practices by non-financial

companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance. 6(1).

p.1468232.

Andor, G., Mohanty, S. K. and Toth, T., 2015. Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review. 23. pp.148-172.

Ang, J. S., 2018. Toward a Corporate Finance Theory for the Entrepreneurial Firm. FSU College

of Law, Public Law Research Paper, (872).

Nawaiseh, M.E and et.al., 2017, September. The Use of Capital Budgeting Techniques as a Tool

for Management Decisions: Evidence from Jordan. In International Conference on

Engineering, Project, and Product Management (pp. 301-309). Springer, Cham.

Smit, H. T. and Trigeorgis, L., 2017. Strategic NPV: Real options and strategic games under

different information structures. Strategic Management Journal. 38(13). pp.2555-2578.

Turner, M.J., 2017. Precursors to the financial and strategic orientation of hotel property capital

budgeting. Journal of Hospitality and Tourism Management. 33. pp.31-42.

Online

Capital Asset Pricing Model (CAPM). 2019. [Online] Available through :

<https://investinganswers.com/dictionary/c/capital-asset-pricing-model-capm>

Efficient Capital Market.2002. [Online] Available through

<http://www.econlib.org/library/Enc1/EfficientCapitalMarkets.html>

9

Books and Journals

Abor, J.Y., 2017. Evaluating Capital Investment Decisions: Capital Budgeting.

In Entrepreneurial Finance for MSMEs (pp. 293-320). Palgrave Macmillan, Cham.

Al-Mutairi, A., Naser, K. and Saeid, M., 2018. Capital budgeting practices by non-financial

companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance. 6(1).

p.1468232.

Andor, G., Mohanty, S. K. and Toth, T., 2015. Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review. 23. pp.148-172.

Ang, J. S., 2018. Toward a Corporate Finance Theory for the Entrepreneurial Firm. FSU College

of Law, Public Law Research Paper, (872).

Nawaiseh, M.E and et.al., 2017, September. The Use of Capital Budgeting Techniques as a Tool

for Management Decisions: Evidence from Jordan. In International Conference on

Engineering, Project, and Product Management (pp. 301-309). Springer, Cham.

Smit, H. T. and Trigeorgis, L., 2017. Strategic NPV: Real options and strategic games under

different information structures. Strategic Management Journal. 38(13). pp.2555-2578.

Turner, M.J., 2017. Precursors to the financial and strategic orientation of hotel property capital

budgeting. Journal of Hospitality and Tourism Management. 33. pp.31-42.

Online

Capital Asset Pricing Model (CAPM). 2019. [Online] Available through :

<https://investinganswers.com/dictionary/c/capital-asset-pricing-model-capm>

Efficient Capital Market.2002. [Online] Available through

<http://www.econlib.org/library/Enc1/EfficientCapitalMarkets.html>

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.