Business Development: Management Accounting Report and Analysis

VerifiedAdded on 2020/07/22

|14

|4107

|67

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within the context of IMDA Tech, an electronic gadget company. It begins by differentiating management accounting from financial accounting, emphasizing its role in internal decision-making and strategic planning. The report then explores various types of management accounting, including cost accounting, inventory management, and pricing optimization, highlighting their benefits for business operations. It further analyzes the integration of management accounting systems within a firm's processes, using absorption and marginal costing methods for profit computation. The report also delves into budgeting, discussing its advantages, disadvantages, and the process of budget preparation, alongside an examination of pricing strategies. The analysis includes application of techniques, interpretation of data, and the role of planning tools in achieving sustainable advantages for the firm. The report concludes by summarizing the key findings and implications of management accounting practices for business development and success, with references to relevant literature.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

1. Management accounting and its differences between financial accounting:..........................1

2. Importance of management accounting information:............................................................2

Different types of management accounting:...............................................................................3

M1 Benefits of management systems under the cited company context:...................................4

D1 How MA system and MA reporting integrates within the firm process:..............................4

TASK 2............................................................................................................................................4

M2 Application of techniques:....................................................................................................6

D2 Interpretation of data:............................................................................................................6

TASK 3............................................................................................................................................6

a). Budgets and its advantages and disadvantages:....................................................................6

b). Process of preparing budgets:................................................................................................8

C). Pricing strategies:..................................................................................................................9

M3. Analyse the use of various planning and their application:.................................................9

D4. Planning tools helps the firm to attain sustainable advantages:...........................................9

TASK 4............................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Books and Journals:..................................................................................................................11

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

1. Management accounting and its differences between financial accounting:..........................1

2. Importance of management accounting information:............................................................2

Different types of management accounting:...............................................................................3

M1 Benefits of management systems under the cited company context:...................................4

D1 How MA system and MA reporting integrates within the firm process:..............................4

TASK 2............................................................................................................................................4

M2 Application of techniques:....................................................................................................6

D2 Interpretation of data:............................................................................................................6

TASK 3............................................................................................................................................6

a). Budgets and its advantages and disadvantages:....................................................................6

b). Process of preparing budgets:................................................................................................8

C). Pricing strategies:..................................................................................................................9

M3. Analyse the use of various planning and their application:.................................................9

D4. Planning tools helps the firm to attain sustainable advantages:...........................................9

TASK 4............................................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Books and Journals:..................................................................................................................11

INTRODUCTION

Management accounting system is the main tool which is used by the company to attain

the business long term objectives. Now, this has been observed that the IMDA tech wants to

attain its objectives which can mostly achieved by using management accounting system. With

the help of management accounting, IMDA tech can produce electronic gadgets in a most

effective manner (Quagli, 2011). Now, management of IMDA tech due to lack of financial

information, it faces various decisions that is why it is not to make decisions effective. But, after

implementing management accounting tools, company is able to frame better strategies so that

the fime decisions could be attained.

Task 1

A).

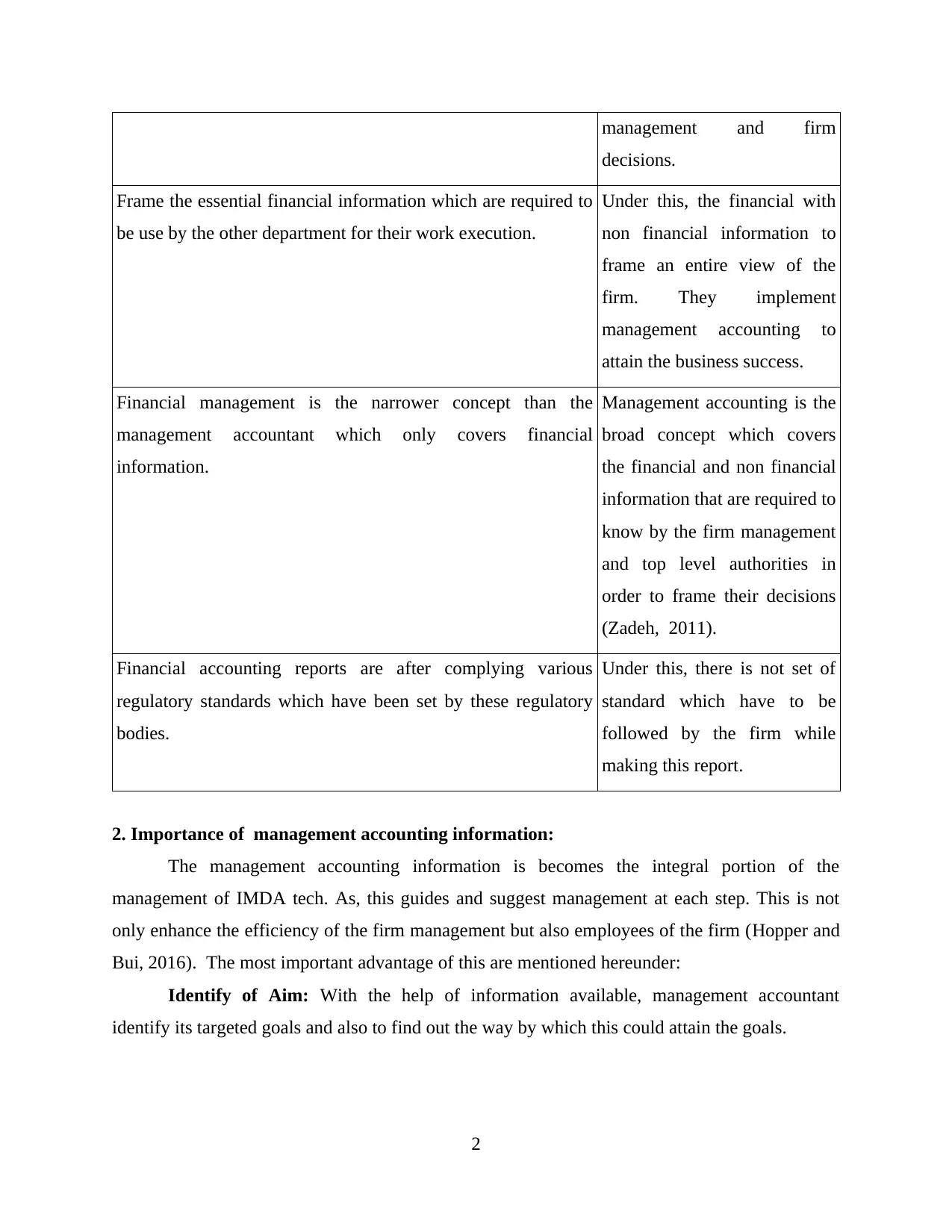

1. Management accounting and its differences between financial accounting:

Management accounting helps the firm to generate information internally and it also

covers sourcing, analysis, communication and implement of financial and non-financial

information decisions in order to build and procure value for firms (Management Accounting,

2017). As, this covers accounting, finance and management by taking help of business skills and

other essential techniques that the management accountant is required to add genuine value to

any firm (Hutaibat, K.A., 2012). They are the well qualified person which do works across the

firm, not only in finance, but also on the overall field which are needed to make business

operations effective. They implement information of various types which could lead to form

business strategy and able to gain the sustainability.

Difference between management accounting and financial accounting:

Financial accounting Management accounting

Frame reports which is totally based on the previous

performance; in line with reporting needs.

Gather information like as

profits, cash flow and due

debts to manufacture trend

reports within a time frame

and statistics in order to inform

imperative, regular

1

Management accounting system is the main tool which is used by the company to attain

the business long term objectives. Now, this has been observed that the IMDA tech wants to

attain its objectives which can mostly achieved by using management accounting system. With

the help of management accounting, IMDA tech can produce electronic gadgets in a most

effective manner (Quagli, 2011). Now, management of IMDA tech due to lack of financial

information, it faces various decisions that is why it is not to make decisions effective. But, after

implementing management accounting tools, company is able to frame better strategies so that

the fime decisions could be attained.

Task 1

A).

1. Management accounting and its differences between financial accounting:

Management accounting helps the firm to generate information internally and it also

covers sourcing, analysis, communication and implement of financial and non-financial

information decisions in order to build and procure value for firms (Management Accounting,

2017). As, this covers accounting, finance and management by taking help of business skills and

other essential techniques that the management accountant is required to add genuine value to

any firm (Hutaibat, K.A., 2012). They are the well qualified person which do works across the

firm, not only in finance, but also on the overall field which are needed to make business

operations effective. They implement information of various types which could lead to form

business strategy and able to gain the sustainability.

Difference between management accounting and financial accounting:

Financial accounting Management accounting

Frame reports which is totally based on the previous

performance; in line with reporting needs.

Gather information like as

profits, cash flow and due

debts to manufacture trend

reports within a time frame

and statistics in order to inform

imperative, regular

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management and firm

decisions.

Frame the essential financial information which are required to

be use by the other department for their work execution.

Under this, the financial with

non financial information to

frame an entire view of the

firm. They implement

management accounting to

attain the business success.

Financial management is the narrower concept than the

management accountant which only covers financial

information.

Management accounting is the

broad concept which covers

the financial and non financial

information that are required to

know by the firm management

and top level authorities in

order to frame their decisions

(Zadeh, 2011).

Financial accounting reports are after complying various

regulatory standards which have been set by these regulatory

bodies.

Under this, there is not set of

standard which have to be

followed by the firm while

making this report.

2. Importance of management accounting information:

The management accounting information is becomes the integral portion of the

management of IMDA tech. As, this guides and suggest management at each step. This is not

only enhance the efficiency of the firm management but also employees of the firm (Hopper and

Bui, 2016). The most important advantage of this are mentioned hereunder:

Identify of Aim: With the help of information available, management accountant

identify its targeted goals and also to find out the way by which this could attain the goals.

2

decisions.

Frame the essential financial information which are required to

be use by the other department for their work execution.

Under this, the financial with

non financial information to

frame an entire view of the

firm. They implement

management accounting to

attain the business success.

Financial management is the narrower concept than the

management accountant which only covers financial

information.

Management accounting is the

broad concept which covers

the financial and non financial

information that are required to

know by the firm management

and top level authorities in

order to frame their decisions

(Zadeh, 2011).

Financial accounting reports are after complying various

regulatory standards which have been set by these regulatory

bodies.

Under this, there is not set of

standard which have to be

followed by the firm while

making this report.

2. Importance of management accounting information:

The management accounting information is becomes the integral portion of the

management of IMDA tech. As, this guides and suggest management at each step. This is not

only enhance the efficiency of the firm management but also employees of the firm (Hopper and

Bui, 2016). The most important advantage of this are mentioned hereunder:

Identify of Aim: With the help of information available, management accountant

identify its targeted goals and also to find out the way by which this could attain the goals.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assist under the form of plan: MA assist top level authorities to frame the plan in order

to make their business objectives. But before going to make any plan, the manager is required to

have the proper analysis of the present and future market scenario.

Great services to customers: With the help of MA, company is able to limit the cost of

the product so that the final outcome can render to the customer at a cheaper rate.

Easy to take judgement: The top level management of the company is able to take the

decisions. This is only possible after implementing management accounting practice effectively.

Assessment of work execution: The standard costing and other management accounting

tools enables the firm to assess the performance of it.

These are the benefits that can only be achieved after implementing management

accounting system under firm. With the help of this, the company needs to make business

decisions so that the pre-set objectives could achieve.

B). Different types of management accounting:

There are various kinds in the management accounting which are used under firm in

order to get the sustainable development. The company needs to make their business operations

effective in order to gain the business pre-set objectives. These are mentioned hereunder:

Cost accounting system: This helps the firm to lower the cost of the product and assess

the costs which are used for making the product. Now, this is the major part under which the

company is able to attain the firm objectives. This does not only consider the cost but also assist

the management for making strategies for attaining firm objectives. Basically, it is divided into

five parts which are:

An input measurement

An stock valuation tool

A cost collection method

A cost flow hypothesis

A capability of opting inventory cost flows at definite intervals.

Inventory management system: The company needs to opt inventory management

system in order to optimum use of resources. As, this is the continuous procedure of shifting

products into out of locations. Firms control their stock on a regular basis because they place

new orders for goods and dispatch orders out to consumers. This is the most imperative thing

that the firm top management gain a appreciation of each activity which is covered under

3

to make their business objectives. But before going to make any plan, the manager is required to

have the proper analysis of the present and future market scenario.

Great services to customers: With the help of MA, company is able to limit the cost of

the product so that the final outcome can render to the customer at a cheaper rate.

Easy to take judgement: The top level management of the company is able to take the

decisions. This is only possible after implementing management accounting practice effectively.

Assessment of work execution: The standard costing and other management accounting

tools enables the firm to assess the performance of it.

These are the benefits that can only be achieved after implementing management

accounting system under firm. With the help of this, the company needs to make business

decisions so that the pre-set objectives could achieve.

B). Different types of management accounting:

There are various kinds in the management accounting which are used under firm in

order to get the sustainable development. The company needs to make their business operations

effective in order to gain the business pre-set objectives. These are mentioned hereunder:

Cost accounting system: This helps the firm to lower the cost of the product and assess

the costs which are used for making the product. Now, this is the major part under which the

company is able to attain the firm objectives. This does not only consider the cost but also assist

the management for making strategies for attaining firm objectives. Basically, it is divided into

five parts which are:

An input measurement

An stock valuation tool

A cost collection method

A cost flow hypothesis

A capability of opting inventory cost flows at definite intervals.

Inventory management system: The company needs to opt inventory management

system in order to optimum use of resources. As, this is the continuous procedure of shifting

products into out of locations. Firms control their stock on a regular basis because they place

new orders for goods and dispatch orders out to consumers. This is the most imperative thing

that the firm top management gain a appreciation of each activity which is covered under

3

inventory management process (Giovannoni, Maraghini,and Riccaboni, 2011). With the help of

this system, IMDA tech is able to manage their inventory management system in order to

optimize the resources in an effective manner.

Price optimising system: It is the procedure of identifying that price level where the

consumer is ready to ply to them. Firms fluctuating the supply chain is devoted vast amount of

time towards price optimisation to assure that their goods would need to offer fast at an

appropriate price while making a healthy profits. If any product price is so high, then this could

not sell at large scale, and just because the price of the products and services constantly vary, it is

the continuous task for most of the firm.

M1 Benefits of management systems under the cited company context:

MA helps in making the systems more strong and affirm, which helps in attaining IMDA

tech objectives. By using MA practices, cited company can produce electronic gadgets at a

cheaper rate which will help the firm to attract more customers.

D1 How MA system and MA reporting integrates within the firm process:

Management accounting system integrates with the MA reporting because, company can

not run their operations effectively without integrating each other. Under a given circumstances,

IMDA tech is producing electronic gadgets which can possible by using operational report.

TASK 2

Absorption costing: Under absorption costing method, all the costs which are related to

production of goods whether these are related to fixed or variable (Figge and Hahn, 2013).

Under this method, management analyse the method for measuring cost of a product by

considering indirect or indirect overheads along with the direct costs.

Marginal costing: Fluctuation under total costs of production operates for framing one extra

unit of an item. This is calculated in a point where break even point is reached. This consists

the variable costs covering of labour and material costs plus an forecasted point of fixed

costs.

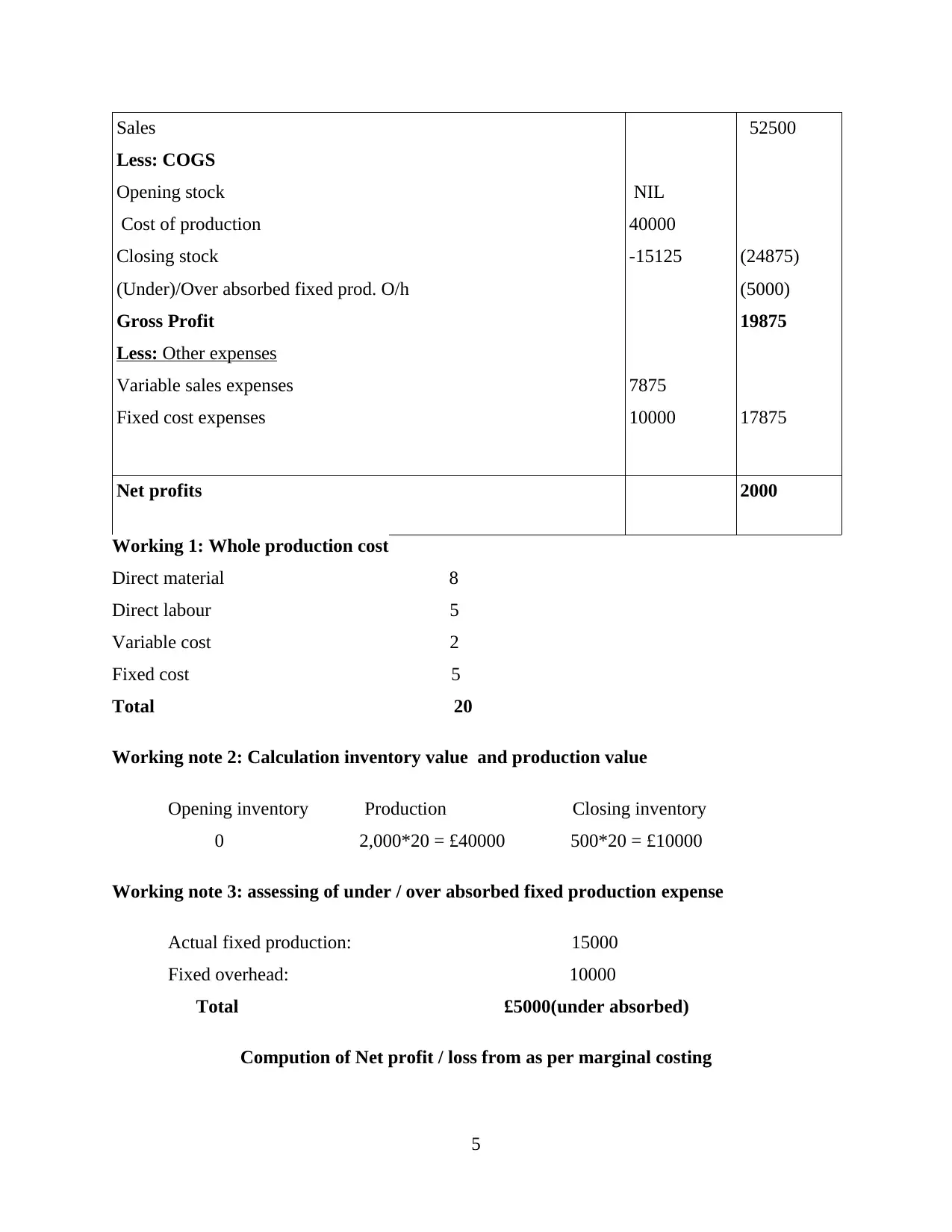

Computation of Net profit through using absorption costing

PARTICULAR £Amount £Amount

4

this system, IMDA tech is able to manage their inventory management system in order to

optimize the resources in an effective manner.

Price optimising system: It is the procedure of identifying that price level where the

consumer is ready to ply to them. Firms fluctuating the supply chain is devoted vast amount of

time towards price optimisation to assure that their goods would need to offer fast at an

appropriate price while making a healthy profits. If any product price is so high, then this could

not sell at large scale, and just because the price of the products and services constantly vary, it is

the continuous task for most of the firm.

M1 Benefits of management systems under the cited company context:

MA helps in making the systems more strong and affirm, which helps in attaining IMDA

tech objectives. By using MA practices, cited company can produce electronic gadgets at a

cheaper rate which will help the firm to attract more customers.

D1 How MA system and MA reporting integrates within the firm process:

Management accounting system integrates with the MA reporting because, company can

not run their operations effectively without integrating each other. Under a given circumstances,

IMDA tech is producing electronic gadgets which can possible by using operational report.

TASK 2

Absorption costing: Under absorption costing method, all the costs which are related to

production of goods whether these are related to fixed or variable (Figge and Hahn, 2013).

Under this method, management analyse the method for measuring cost of a product by

considering indirect or indirect overheads along with the direct costs.

Marginal costing: Fluctuation under total costs of production operates for framing one extra

unit of an item. This is calculated in a point where break even point is reached. This consists

the variable costs covering of labour and material costs plus an forecasted point of fixed

costs.

Computation of Net profit through using absorption costing

PARTICULAR £Amount £Amount

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales

Less: COGS

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Other expenses

Variable sales expenses

Fixed cost expenses

NIL

40000

-15125

7875

10000

52500

(24875)

(5000)

19875

17875

Net profits 2000

Working 1: Whole production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working note 2: Calculation inventory value and production value

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working note 3: assessing of under / over absorbed fixed production expense

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Compution of Net profit / loss from as per marginal costing

5

Less: COGS

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Other expenses

Variable sales expenses

Fixed cost expenses

NIL

40000

-15125

7875

10000

52500

(24875)

(5000)

19875

17875

Net profits 2000

Working 1: Whole production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working note 2: Calculation inventory value and production value

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working note 3: assessing of under / over absorbed fixed production expense

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Compution of Net profit / loss from as per marginal costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit using marginal costing £Amount £Amount

SALES

Less: Variable costs

Opening stock

Business costs

Closing stock

Variable costs

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Marginal costing

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production O/h 2

Total variable cost 15

Working 2: Computation of value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

M2 Application of techniques:

Under the cited question, company is required to use management accounting techniques

so that the optimum results could be attained. This also makes the operations so smooth which

brings the operations effective.

D2 Interpretation of data:

The profits achieved as per marginal costing and absorption costing represent the

different value. Which ultimately helps in making the business sustainable. Under absorption

costing, the company earn 2000 profits but as per marginal costing, company uses -2875.

6

SALES

Less: Variable costs

Opening stock

Business costs

Closing stock

Variable costs

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Marginal costing

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production O/h 2

Total variable cost 15

Working 2: Computation of value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

M2 Application of techniques:

Under the cited question, company is required to use management accounting techniques

so that the optimum results could be attained. This also makes the operations so smooth which

brings the operations effective.

D2 Interpretation of data:

The profits achieved as per marginal costing and absorption costing represent the

different value. Which ultimately helps in making the business sustainable. Under absorption

costing, the company earn 2000 profits but as per marginal costing, company uses -2875.

6

TASK 3

a). Budgets and its advantages and disadvantages:

Budget is the forecasting of financial plan for a certain period of time. This may covers

forecasted sales volumes and revenues, assets, liabilities, resource quantities and much more.

This reflects strategic plans of firm units, and a units. A budget is the total of resource allocated

for a specific aim and the statement of planned expenditure along with the proposals for how to

cover them. To run a company effectively, company uses various budgets strategies, some of

them are as follows:

Production budget: This is the budget which can be used for estimating costs about all

producing goods that the company is producing. This helps the firm to know about the product

cost and then make strategy in order to attain the objectives (Bennett, Schaltegger and Zvezdov,

2011). This has been seen that the management of IMDA tech is required to consider their

production budget in it operations so that they would get to know about the costs related to the

production of the goods.

Benefits of production budget: Production budget is helpful for estimating the production

related requirement of the firm so that the company acts accordingly. These kinds of stuff assist

the firm to lower the costs related to the production by effectively utilising the available

resources. The advantages relating to the cost of production can be attained after making

production budgets.

Disadvantages of production budget: The production budget which is prepared by the

accounts department is not always represents the fair value. This is entirely based on the

predictions which might wrong sometimes. Hence, the data which have been collected by the

firm on the basis of such production budgets will make the wrong interpretation. Hence, the

exact value can't be created by the firm.

Cash budget: This is a prediction of cash inflows and outflows for a firm over a particular time,

and this budget is implemented to assess whether the firm has enough cash to run the operation.

With the help of this, company would get to know about the cash inflows and then make the plan

to spend inflows in a better manner (Bagautdinova, Kundakchyan and Malakhov, 2013).

Advantages of cash budget: There are various advantages of opting cash budget, but there are

mostly two advantages which are described here. First, with the help of cash budget, company

7

a). Budgets and its advantages and disadvantages:

Budget is the forecasting of financial plan for a certain period of time. This may covers

forecasted sales volumes and revenues, assets, liabilities, resource quantities and much more.

This reflects strategic plans of firm units, and a units. A budget is the total of resource allocated

for a specific aim and the statement of planned expenditure along with the proposals for how to

cover them. To run a company effectively, company uses various budgets strategies, some of

them are as follows:

Production budget: This is the budget which can be used for estimating costs about all

producing goods that the company is producing. This helps the firm to know about the product

cost and then make strategy in order to attain the objectives (Bennett, Schaltegger and Zvezdov,

2011). This has been seen that the management of IMDA tech is required to consider their

production budget in it operations so that they would get to know about the costs related to the

production of the goods.

Benefits of production budget: Production budget is helpful for estimating the production

related requirement of the firm so that the company acts accordingly. These kinds of stuff assist

the firm to lower the costs related to the production by effectively utilising the available

resources. The advantages relating to the cost of production can be attained after making

production budgets.

Disadvantages of production budget: The production budget which is prepared by the

accounts department is not always represents the fair value. This is entirely based on the

predictions which might wrong sometimes. Hence, the data which have been collected by the

firm on the basis of such production budgets will make the wrong interpretation. Hence, the

exact value can't be created by the firm.

Cash budget: This is a prediction of cash inflows and outflows for a firm over a particular time,

and this budget is implemented to assess whether the firm has enough cash to run the operation.

With the help of this, company would get to know about the cash inflows and then make the plan

to spend inflows in a better manner (Bagautdinova, Kundakchyan and Malakhov, 2013).

Advantages of cash budget: There are various advantages of opting cash budget, but there are

mostly two advantages which are described here. First, with the help of cash budget, company

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

can control its spendings. Second, by implementing cash budget, company cut approximately

80% of the time spent reconciling its budgeting at month end.

Disadvantages of Cash budget: Each company makes cash budgets in its entire budgeting

process. This review anticipated cash receipts and cash disbursement for the budgeted period.

Sometimes, this may lead to have wrong budgeted estimates for the future events. Cash budget

once made, then it can't be altered. This is the major disadvantage of cash budget.

b). Process of preparing budgets:

Here, are the steps which are need to adhere when preparing a budget:

1. Update budget assumption: The company needs to assume about the firm's business

environment which is made on the basis of past records.

2. Review bottlenecks: Identify the capacity level of basic bottleneck which limiting firm

from producing further sales, and elaborate how this affect any extra revenue growth.

3. Available funding: Company needs to determine the amount of funding which is

available at the time of budget period, that might reduce the growth plans.

4. Step costing points: Identify the step which happen during likely range of business

activity in the forthcoming business period, and elaborate the amount of costs and also

know about the activity level where they will happen.

5. Frame budget package and allow the management to issue the amount which is required

for budget package.

6. Getting revenue forecast: The company would attain the profits estimation from the sales

managers, authenticate it with the company's managing director, and after that disperse it

to various divisional managers (Alleyne and Weekes-Marshall, 2011). They implement

the revenue information for making their own budget.

7. Getting divisional budgets: Getting budgets from entire divisions in order to check the

errors, and compare to the bottleneck, funding and step costing restrictions. Arrange the

budget accordingly.

8. Update budget model accordingly.

9. Review the budget: Management team review the budget. Make restraint issues, and any

restrictions caused by funding limitations.

10. Issue the budget: Make a bound version of budget and disperse it to the authorised

person.

8

80% of the time spent reconciling its budgeting at month end.

Disadvantages of Cash budget: Each company makes cash budgets in its entire budgeting

process. This review anticipated cash receipts and cash disbursement for the budgeted period.

Sometimes, this may lead to have wrong budgeted estimates for the future events. Cash budget

once made, then it can't be altered. This is the major disadvantage of cash budget.

b). Process of preparing budgets:

Here, are the steps which are need to adhere when preparing a budget:

1. Update budget assumption: The company needs to assume about the firm's business

environment which is made on the basis of past records.

2. Review bottlenecks: Identify the capacity level of basic bottleneck which limiting firm

from producing further sales, and elaborate how this affect any extra revenue growth.

3. Available funding: Company needs to determine the amount of funding which is

available at the time of budget period, that might reduce the growth plans.

4. Step costing points: Identify the step which happen during likely range of business

activity in the forthcoming business period, and elaborate the amount of costs and also

know about the activity level where they will happen.

5. Frame budget package and allow the management to issue the amount which is required

for budget package.

6. Getting revenue forecast: The company would attain the profits estimation from the sales

managers, authenticate it with the company's managing director, and after that disperse it

to various divisional managers (Alleyne and Weekes-Marshall, 2011). They implement

the revenue information for making their own budget.

7. Getting divisional budgets: Getting budgets from entire divisions in order to check the

errors, and compare to the bottleneck, funding and step costing restrictions. Arrange the

budget accordingly.

8. Update budget model accordingly.

9. Review the budget: Management team review the budget. Make restraint issues, and any

restrictions caused by funding limitations.

10. Issue the budget: Make a bound version of budget and disperse it to the authorised

person.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C). Pricing strategies:

Pricing is the most imperative factors of the marketing mix, as this is only component of

marketing mix, that produces a turnover for the firm. Pricing strategies are adopting a number of

pricing strategies, this will usually be depends on the corporate objectives (Ahmad, 2013). There

are few kinds of pricing strategies. Which are penetration pricing, skimming, and competition

pricing, Product line pricing, bundle pricing, premium pricing, psychological pricing, optional

pricing, cost plus pricing, cost based pricing, value based pricing. Some of them are defined

hereunder:

Penetration Pricing: Under this, organisation fix a low price to enhance sales and market stake.

Once market stake has been captured the firm, in that case , enhance their market price.

Skimming pricing: Firm fix starting high price and after that gradually lower the price in order

to make the product available to a wider market. The main aim is to skim profits of the market

gradually.

Competition pricing: Fixing a price in comparison with the rivals. In fact, a firm has three

options and these are helpful for making the price lower, constant the price and more than the

contenders.

M3. Analyse the use of various planning and their application:

Planning tools are used by the firm in order to attain the firm pre-set objectives so that the

firm could attain their pre-set objectives. The company needs to consider various budgeted plan

in order to effectively utilise their business operations. These planning tools helps the firm to

attain their pre-set objectives.

D4. Planning tools helps the firm to attain sustainable advantages:

Different planning tools are used by the firm in order to attain business pre-set objectives

which also need to get the sustainable advantages over the other rivals.

TASK 4

A). Balance scorecard approach is the major approach which is used in order to identify the

financial problems and also takes certain actions which can be achieved so that the financial

problems can be attained (Abrahamsson, Englund and Gerdin, 2011). By considering these

technique, many firms tended to control their operations which are totally based on the financial

9

Pricing is the most imperative factors of the marketing mix, as this is only component of

marketing mix, that produces a turnover for the firm. Pricing strategies are adopting a number of

pricing strategies, this will usually be depends on the corporate objectives (Ahmad, 2013). There

are few kinds of pricing strategies. Which are penetration pricing, skimming, and competition

pricing, Product line pricing, bundle pricing, premium pricing, psychological pricing, optional

pricing, cost plus pricing, cost based pricing, value based pricing. Some of them are defined

hereunder:

Penetration Pricing: Under this, organisation fix a low price to enhance sales and market stake.

Once market stake has been captured the firm, in that case , enhance their market price.

Skimming pricing: Firm fix starting high price and after that gradually lower the price in order

to make the product available to a wider market. The main aim is to skim profits of the market

gradually.

Competition pricing: Fixing a price in comparison with the rivals. In fact, a firm has three

options and these are helpful for making the price lower, constant the price and more than the

contenders.

M3. Analyse the use of various planning and their application:

Planning tools are used by the firm in order to attain the firm pre-set objectives so that the

firm could attain their pre-set objectives. The company needs to consider various budgeted plan

in order to effectively utilise their business operations. These planning tools helps the firm to

attain their pre-set objectives.

D4. Planning tools helps the firm to attain sustainable advantages:

Different planning tools are used by the firm in order to attain business pre-set objectives

which also need to get the sustainable advantages over the other rivals.

TASK 4

A). Balance scorecard approach is the major approach which is used in order to identify the

financial problems and also takes certain actions which can be achieved so that the financial

problems can be attained (Abrahamsson, Englund and Gerdin, 2011). By considering these

technique, many firms tended to control their operations which are totally based on the financial

9

measures. As, financial measures are essential, these are helpful in reporting about past

happenings. Management system which authorises firm to fix, track and also attain its major

strategies and pre-set objectives. After making the business strategies, then these would be

implemented and tracked via four legs of BSC. Such four legs are used by the firm to attain four

different firm perspectives. These are: financial leg, internal leg, customer leg and knowledge

leg. These are essential for attaining pre-set targets and managers to be plan, implement, and

attain their firm strategies. These are described hereunder:

Customer leg: By using this leg, company would assess customers' satisfaction and their

performance requirements and also assess about it products or services.

Financial leg: Tracks firm financial needs and performance.

Internal business process leg: Assessing company's critical to customer process needs and

assessment.

Knowledge, Education, and growth leg: Concentrates on how company educate their

employees, how they enhance and capture their knowledge, and how they implement it to sustain

a competitive edge throughout the markets.

These are required to be measured, analysed, and enhanced together regularly for

responding the financial problems ( Hammad, Jusoh, and Ghozali, 2013). If company ignore

any one from the above, in that case, this would create a situation where someone is sitting on a

four -legged stool with the broken leg, and suddenly he lose his balance and fall flat on his face.

CONCLUSION

From the above mentioned report, this has been seen that the management accounting

tools have been used in order to make the business sustainable. Under this report, this net profits

as per marginal and absorption costing has been drawn, which reflects that by using these

techniques, company could maximise their business profits. Under this report, the company uses

various planning tools which are used in order to make their business operations effective. Under

this report, the IMDA tech also address various financial problems and then acts accordingly.

10

happenings. Management system which authorises firm to fix, track and also attain its major

strategies and pre-set objectives. After making the business strategies, then these would be

implemented and tracked via four legs of BSC. Such four legs are used by the firm to attain four

different firm perspectives. These are: financial leg, internal leg, customer leg and knowledge

leg. These are essential for attaining pre-set targets and managers to be plan, implement, and

attain their firm strategies. These are described hereunder:

Customer leg: By using this leg, company would assess customers' satisfaction and their

performance requirements and also assess about it products or services.

Financial leg: Tracks firm financial needs and performance.

Internal business process leg: Assessing company's critical to customer process needs and

assessment.

Knowledge, Education, and growth leg: Concentrates on how company educate their

employees, how they enhance and capture their knowledge, and how they implement it to sustain

a competitive edge throughout the markets.

These are required to be measured, analysed, and enhanced together regularly for

responding the financial problems ( Hammad, Jusoh, and Ghozali, 2013). If company ignore

any one from the above, in that case, this would create a situation where someone is sitting on a

four -legged stool with the broken leg, and suddenly he lose his balance and fall flat on his face.

CONCLUSION

From the above mentioned report, this has been seen that the management accounting

tools have been used in order to make the business sustainable. Under this report, this net profits

as per marginal and absorption costing has been drawn, which reflects that by using these

techniques, company could maximise their business profits. Under this report, the company uses

various planning tools which are used in order to make their business operations effective. Under

this report, the IMDA tech also address various financial problems and then acts accordingly.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.