Business Management Assignment: Accounting and Financial Analysis

VerifiedAdded on 2023/04/21

|11

|1515

|392

Homework Assignment

AI Summary

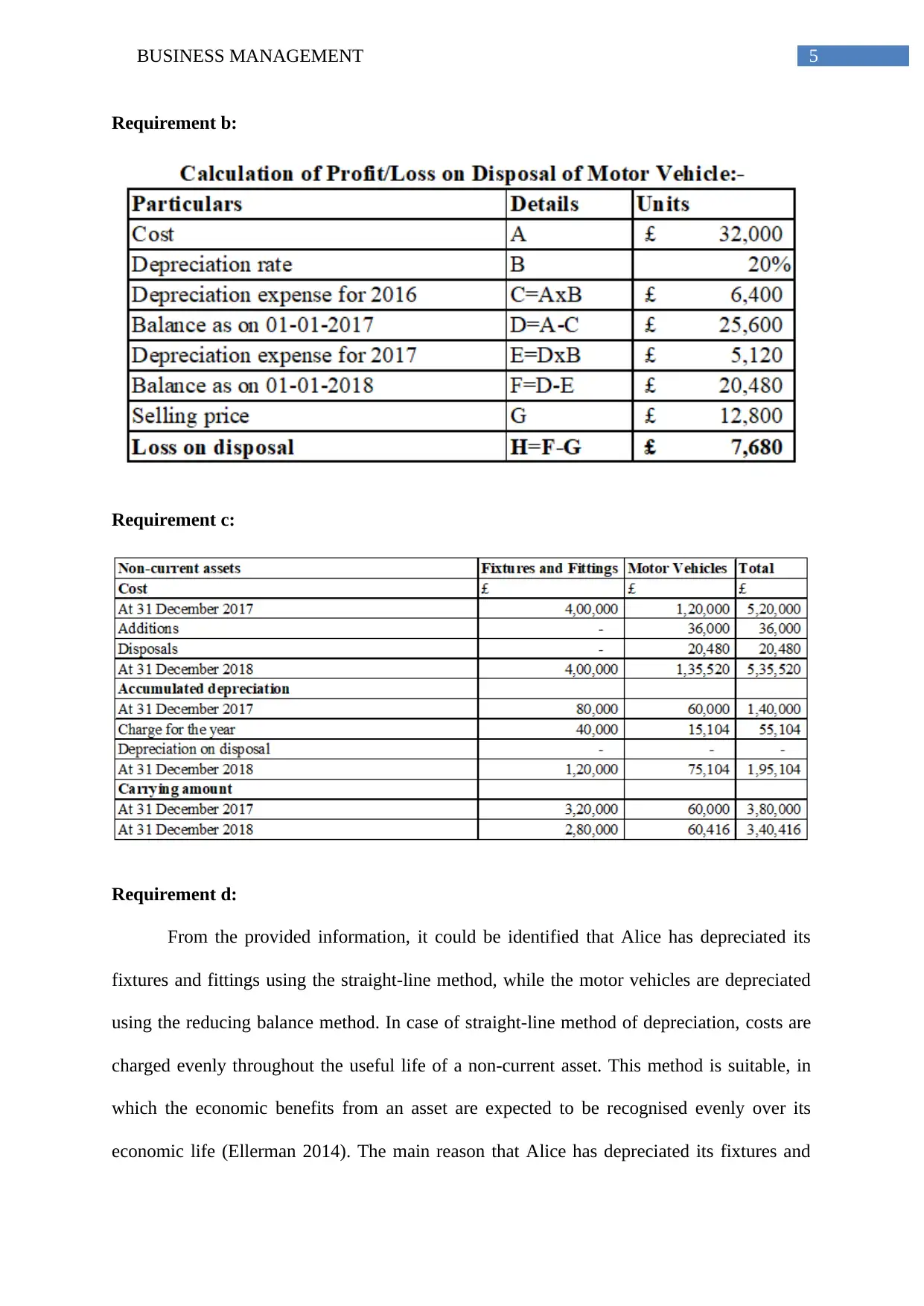

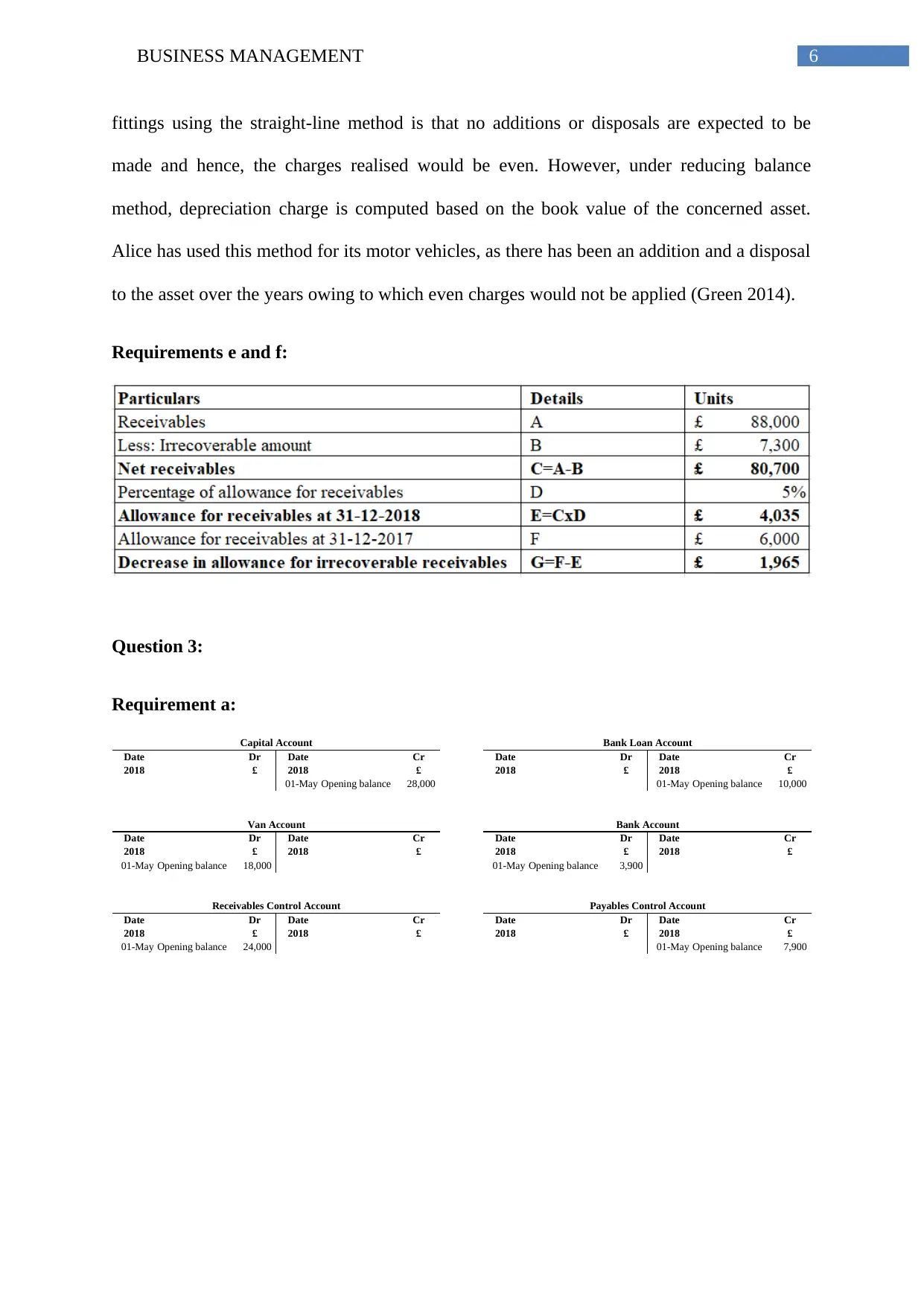

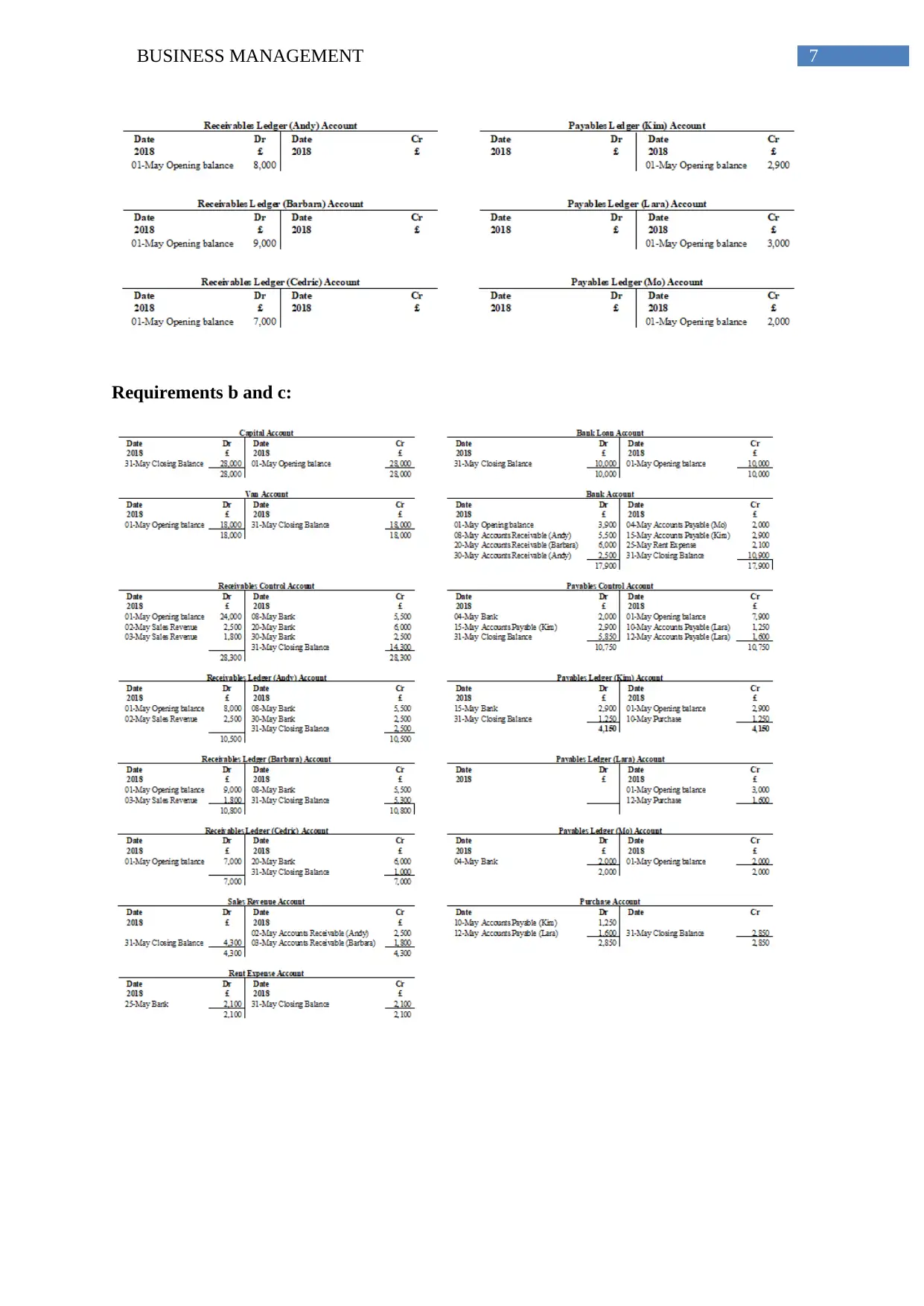

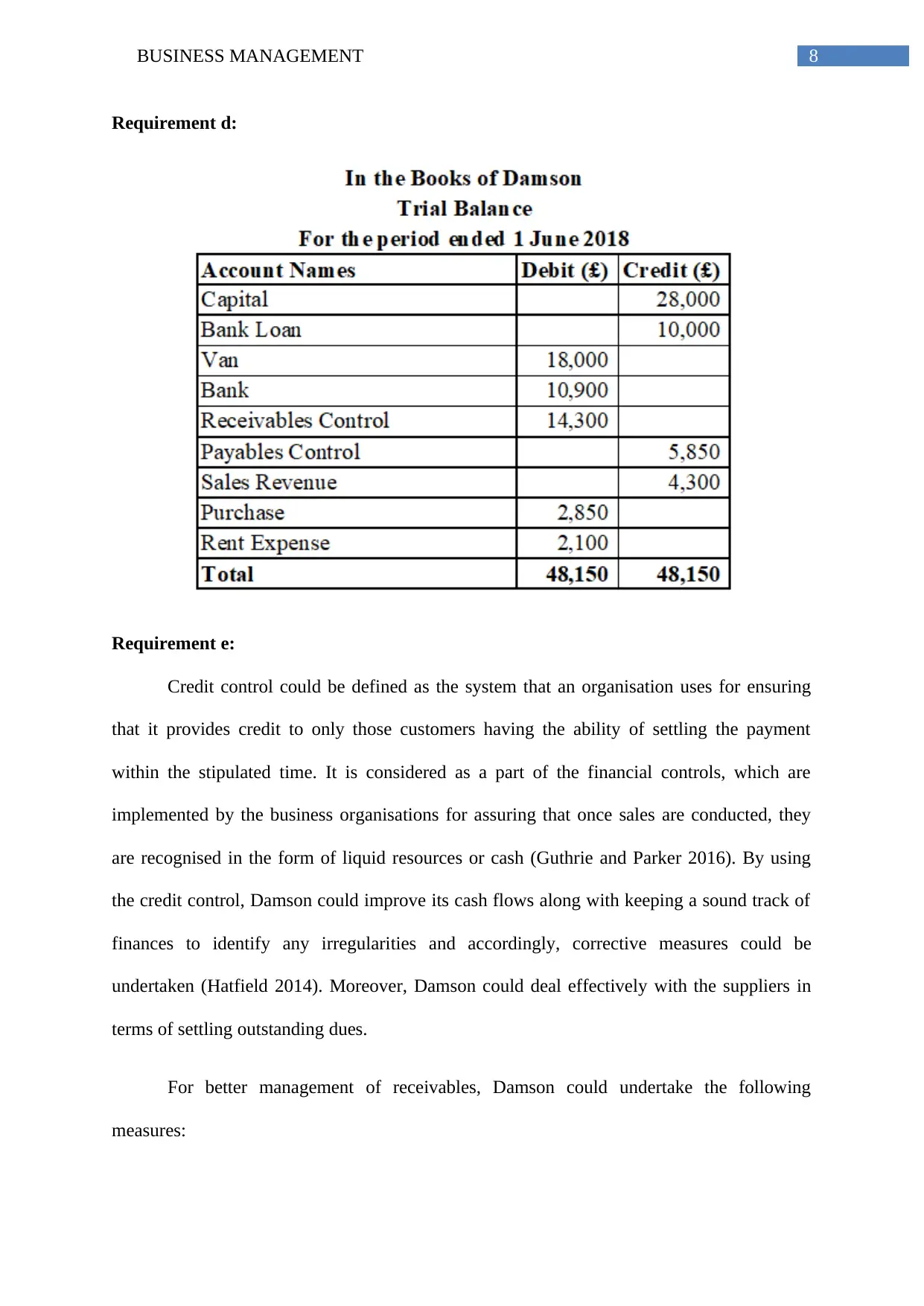

This document presents a detailed solution to a business management assignment, addressing key accounting and financial concepts. The assignment covers topics such as accrual accounting, depreciation methods (straight-line and reducing balance), and the impact of cash-based accounting. It includes calculations for depreciation charges, analysis of financial statements, and an examination of credit control systems. Furthermore, the solution provides insights into managing receivables and payables, along with a reflection on the learning process from a previous assignment. The student demonstrates an understanding of accounting principles, financial analysis, and the importance of effective financial controls, making this a valuable resource for students studying business management.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.