Business Maths: Financial Analysis, Forecasting, and Investment

VerifiedAdded on 2023/06/15

|18

|3574

|489

Homework Assignment

AI Summary

This Business Maths assignment solution covers a range of topics including simplification of algebraic expressions, calculation of mark up and margin, forecasting using moving averages, investment appraisal techniques such as payback period and net present value (NPV), and correlation analysis. The assignment demonstrates the application of these mathematical concepts to business scenarios, providing detailed calculations and explanations for each question. It includes definitions of key terms like mark up, margin, trade discount, bulk discount, and early settlement discount. Furthermore, it assesses the profitability of investments using expected return calculations and evaluates the impact of cost reductions on operating profit margin. The solutions provided offer a comprehensive understanding of business mathematics and its practical relevance in financial decision-making. Desklib provides access to this solution along with many others, offering students a valuable resource for their studies.

Business Maths

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1........................................................................................................................................4

a. Simplification..........................................................................................................................4

b. Working out two possible values of C....................................................................................4

c. Simplification of expression....................................................................................................4

d. Finding the value of x.............................................................................................................4

e. Finding the value of v..............................................................................................................5

Question 2........................................................................................................................................5

a. Definitions and business uses of mark up and margin............................................................5

b. Calculation of mark up............................................................................................................6

c. calculation of margin...............................................................................................................6

d. Operating profit margin after reducing admin cost by 60%...................................................6

e. Definitions and their examples................................................................................................6

f. .................................................................................................................................................7

g...................................................................................................................................................7

Question 3........................................................................................................................................8

a. Calculation of three point moving average.............................................................................8

b. Definition of moving averages and usefulness in forecasting................................................9

c...................................................................................................................................................9

d...................................................................................................................................................9

e...................................................................................................................................................9

Question 4......................................................................................................................................10

(a) Calculation of Pay Back Period...........................................................................................10

(b) Calculation of Net Present Value........................................................................................10

(c)..............................................................................................................................................11

(d) Calculation of Internal Rate of Return................................................................................12

(e)..............................................................................................................................................12

Question 5......................................................................................................................................14

(a) Calculation of correlation....................................................................................................14

(b)..............................................................................................................................................14

(c)..............................................................................................................................................15

Question 1........................................................................................................................................4

a. Simplification..........................................................................................................................4

b. Working out two possible values of C....................................................................................4

c. Simplification of expression....................................................................................................4

d. Finding the value of x.............................................................................................................4

e. Finding the value of v..............................................................................................................5

Question 2........................................................................................................................................5

a. Definitions and business uses of mark up and margin............................................................5

b. Calculation of mark up............................................................................................................6

c. calculation of margin...............................................................................................................6

d. Operating profit margin after reducing admin cost by 60%...................................................6

e. Definitions and their examples................................................................................................6

f. .................................................................................................................................................7

g...................................................................................................................................................7

Question 3........................................................................................................................................8

a. Calculation of three point moving average.............................................................................8

b. Definition of moving averages and usefulness in forecasting................................................9

c...................................................................................................................................................9

d...................................................................................................................................................9

e...................................................................................................................................................9

Question 4......................................................................................................................................10

(a) Calculation of Pay Back Period...........................................................................................10

(b) Calculation of Net Present Value........................................................................................10

(c)..............................................................................................................................................11

(d) Calculation of Internal Rate of Return................................................................................12

(e)..............................................................................................................................................12

Question 5......................................................................................................................................14

(a) Calculation of correlation....................................................................................................14

(b)..............................................................................................................................................14

(c)..............................................................................................................................................15

(d)..............................................................................................................................................15

REFRENCES.................................................................................................................................16

REFRENCES.................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

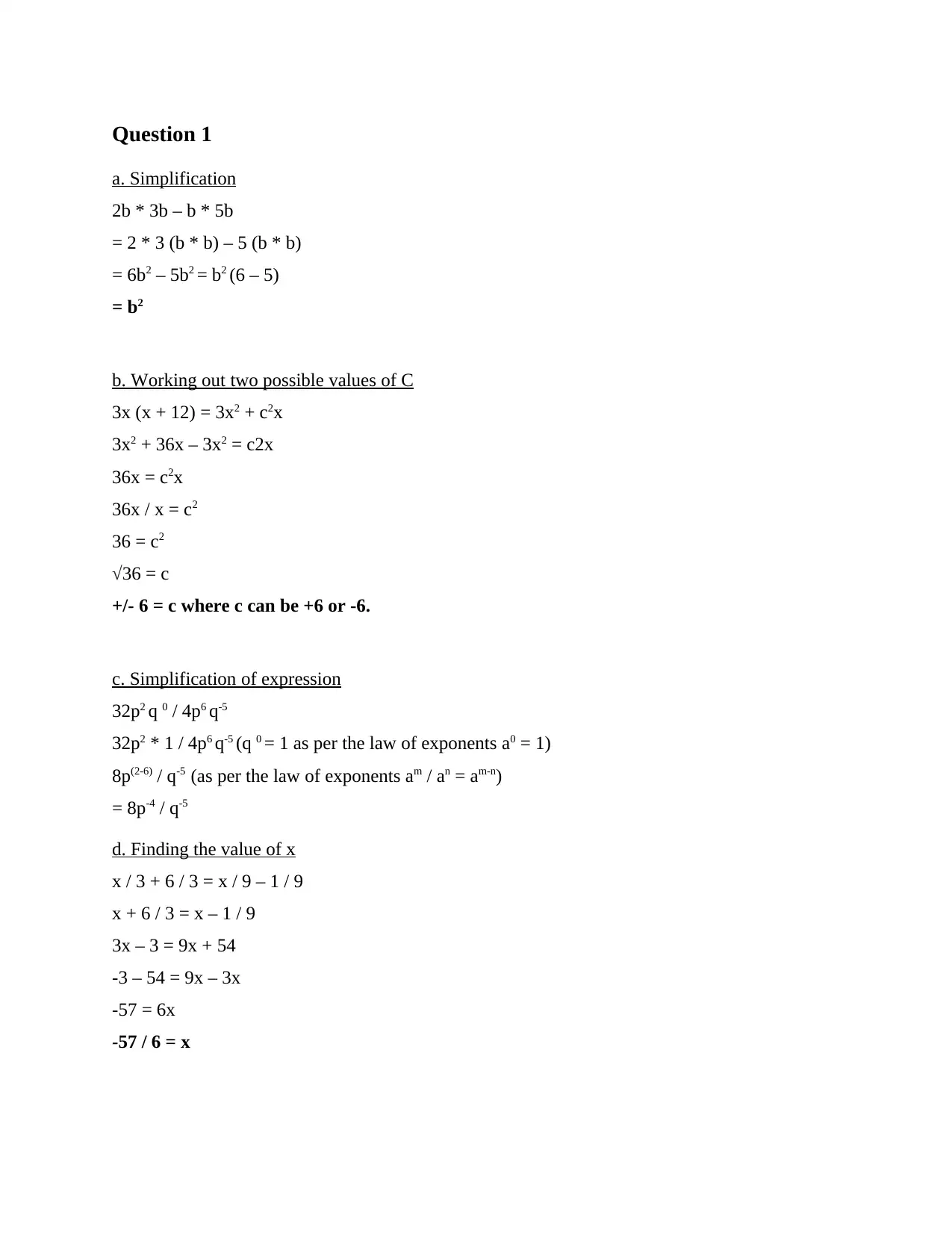

Question 1

a. Simplification

2b * 3b – b * 5b

= 2 * 3 (b * b) – 5 (b * b)

= 6b2 – 5b2 = b2 (6 – 5)

= b2

b. Working out two possible values of C

3x (x + 12) = 3x2 + c2x

3x2 + 36x – 3x2 = c2x

36x = c2x

36x / x = c2

36 = c2

√36 = c

+/- 6 = c where c can be +6 or -6.

c. Simplification of expression

32p2 q 0 / 4p6 q-5

32p2 * 1 / 4p6 q-5 (q 0 = 1 as per the law of exponents a0 = 1)

8p(2-6) / q-5 (as per the law of exponents am / an = am-n)

= 8p-4 / q-5

d. Finding the value of x

x / 3 + 6 / 3 = x / 9 – 1 / 9

x + 6 / 3 = x – 1 / 9

3x – 3 = 9x + 54

-3 – 54 = 9x – 3x

-57 = 6x

-57 / 6 = x

a. Simplification

2b * 3b – b * 5b

= 2 * 3 (b * b) – 5 (b * b)

= 6b2 – 5b2 = b2 (6 – 5)

= b2

b. Working out two possible values of C

3x (x + 12) = 3x2 + c2x

3x2 + 36x – 3x2 = c2x

36x = c2x

36x / x = c2

36 = c2

√36 = c

+/- 6 = c where c can be +6 or -6.

c. Simplification of expression

32p2 q 0 / 4p6 q-5

32p2 * 1 / 4p6 q-5 (q 0 = 1 as per the law of exponents a0 = 1)

8p(2-6) / q-5 (as per the law of exponents am / an = am-n)

= 8p-4 / q-5

d. Finding the value of x

x / 3 + 6 / 3 = x / 9 – 1 / 9

x + 6 / 3 = x – 1 / 9

3x – 3 = 9x + 54

-3 – 54 = 9x – 3x

-57 = 6x

-57 / 6 = x

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

e. Finding the value of v

2v + 8 / 4 = v – 6 / 6

12v + 48 = 4v – 24

12v – 4v = -24 – 48

8v = -72

v = -72 / 8

v = -9

Question 2

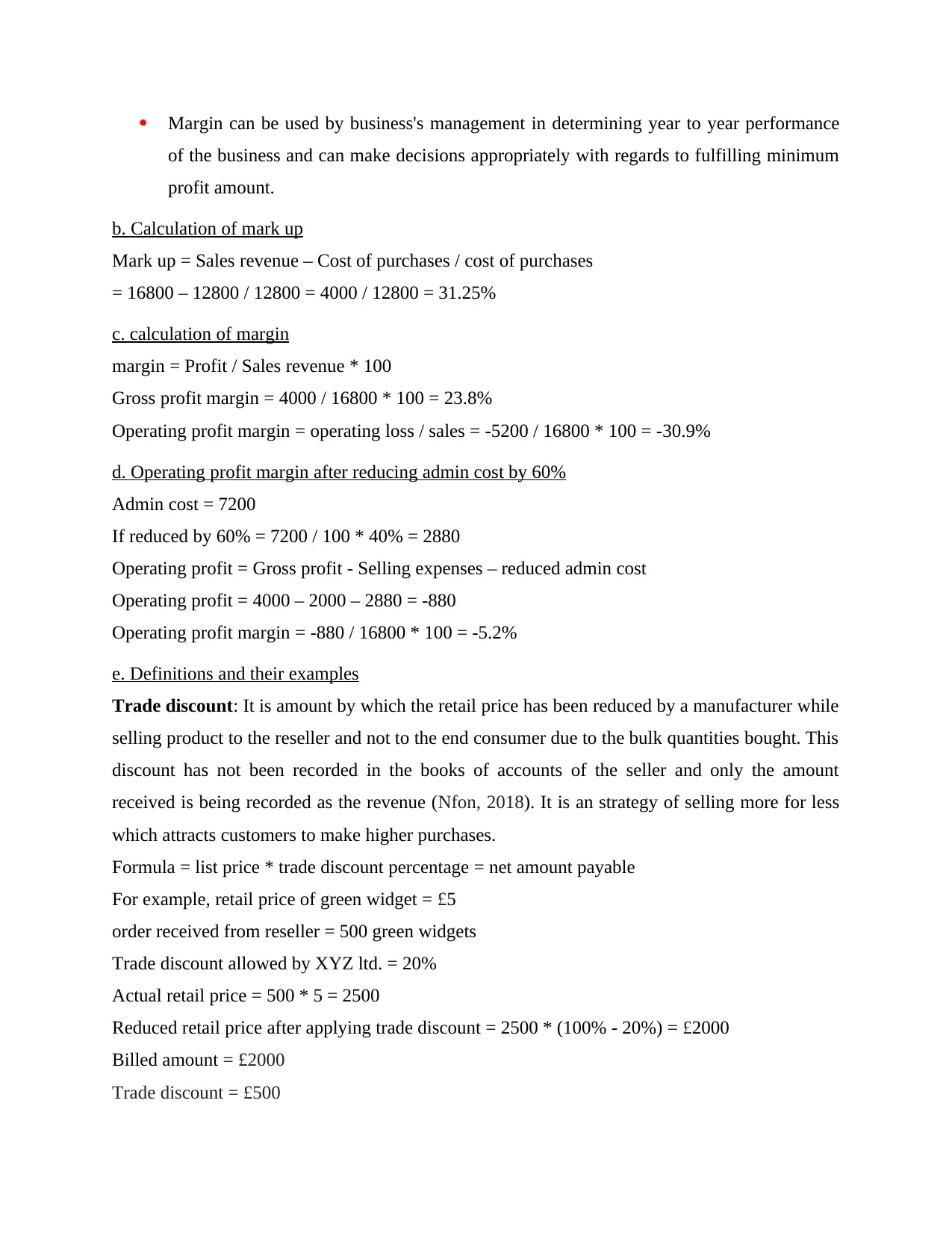

a. Definitions and business uses of mark up and margin

Mark up can be defined as the difference between the selling price of a product and cost of the

product which is expresses as a proportion of the cost of the product. It is also known as the

premium over and above the total cost of sales which is meant as a profit for seller.

The formula for mark up = Selling price - cost of the product / cost of the product * 100.

Margin can be defined as the difference between selling price of the product or services and the

cost of product. It can be expressed as the ratio of profit to sales. It is a percentage which reflects

the profitability of the business after deducting the all the expenses of the business from their

revenues. It is also known as profit margin.

Business uses of mark up

Once mark up has been determined it when gets added to the cost price of the products

gives the management with the final retail price at which the product would be sold in the

market.

By determining the mark up, management can determine how much amount of money

they can make after selling each and every of their products in the market.

Mark up if determined appropriately aids in covering all the costs of the business along

with ensuring that the business could be able to make profit.

Business uses of margin

Margin allows for measuring business profitability, product profitability and management

performance as a whole.

Margin indicates that business has prices its product appropriately and also their sales

performance in the market is well and good.

2v + 8 / 4 = v – 6 / 6

12v + 48 = 4v – 24

12v – 4v = -24 – 48

8v = -72

v = -72 / 8

v = -9

Question 2

a. Definitions and business uses of mark up and margin

Mark up can be defined as the difference between the selling price of a product and cost of the

product which is expresses as a proportion of the cost of the product. It is also known as the

premium over and above the total cost of sales which is meant as a profit for seller.

The formula for mark up = Selling price - cost of the product / cost of the product * 100.

Margin can be defined as the difference between selling price of the product or services and the

cost of product. It can be expressed as the ratio of profit to sales. It is a percentage which reflects

the profitability of the business after deducting the all the expenses of the business from their

revenues. It is also known as profit margin.

Business uses of mark up

Once mark up has been determined it when gets added to the cost price of the products

gives the management with the final retail price at which the product would be sold in the

market.

By determining the mark up, management can determine how much amount of money

they can make after selling each and every of their products in the market.

Mark up if determined appropriately aids in covering all the costs of the business along

with ensuring that the business could be able to make profit.

Business uses of margin

Margin allows for measuring business profitability, product profitability and management

performance as a whole.

Margin indicates that business has prices its product appropriately and also their sales

performance in the market is well and good.

Margin can be used by business's management in determining year to year performance

of the business and can make decisions appropriately with regards to fulfilling minimum

profit amount.

b. Calculation of mark up

Mark up = Sales revenue – Cost of purchases / cost of purchases

= 16800 – 12800 / 12800 = 4000 / 12800 = 31.25%

c. calculation of margin

margin = Profit / Sales revenue * 100

Gross profit margin = 4000 / 16800 * 100 = 23.8%

Operating profit margin = operating loss / sales = -5200 / 16800 * 100 = -30.9%

d. Operating profit margin after reducing admin cost by 60%

Admin cost = 7200

If reduced by 60% = 7200 / 100 * 40% = 2880

Operating profit = Gross profit - Selling expenses – reduced admin cost

Operating profit = 4000 – 2000 – 2880 = -880

Operating profit margin = -880 / 16800 * 100 = -5.2%

e. Definitions and their examples

Trade discount: It is amount by which the retail price has been reduced by a manufacturer while

selling product to the reseller and not to the end consumer due to the bulk quantities bought. This

discount has not been recorded in the books of accounts of the seller and only the amount

received is being recorded as the revenue (Nfon, 2018). It is an strategy of selling more for less

which attracts customers to make higher purchases.

Formula = list price * trade discount percentage = net amount payable

For example, retail price of green widget = £5

order received from reseller = 500 green widgets

Trade discount allowed by XYZ ltd. = 20%

Actual retail price = 500 * 5 = 2500

Reduced retail price after applying trade discount = 2500 * (100% - 20%) = £2000

Billed amount = £2000

Trade discount = £500

of the business and can make decisions appropriately with regards to fulfilling minimum

profit amount.

b. Calculation of mark up

Mark up = Sales revenue – Cost of purchases / cost of purchases

= 16800 – 12800 / 12800 = 4000 / 12800 = 31.25%

c. calculation of margin

margin = Profit / Sales revenue * 100

Gross profit margin = 4000 / 16800 * 100 = 23.8%

Operating profit margin = operating loss / sales = -5200 / 16800 * 100 = -30.9%

d. Operating profit margin after reducing admin cost by 60%

Admin cost = 7200

If reduced by 60% = 7200 / 100 * 40% = 2880

Operating profit = Gross profit - Selling expenses – reduced admin cost

Operating profit = 4000 – 2000 – 2880 = -880

Operating profit margin = -880 / 16800 * 100 = -5.2%

e. Definitions and their examples

Trade discount: It is amount by which the retail price has been reduced by a manufacturer while

selling product to the reseller and not to the end consumer due to the bulk quantities bought. This

discount has not been recorded in the books of accounts of the seller and only the amount

received is being recorded as the revenue (Nfon, 2018). It is an strategy of selling more for less

which attracts customers to make higher purchases.

Formula = list price * trade discount percentage = net amount payable

For example, retail price of green widget = £5

order received from reseller = 500 green widgets

Trade discount allowed by XYZ ltd. = 20%

Actual retail price = 500 * 5 = 2500

Reduced retail price after applying trade discount = 2500 * (100% - 20%) = £2000

Billed amount = £2000

Trade discount = £500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

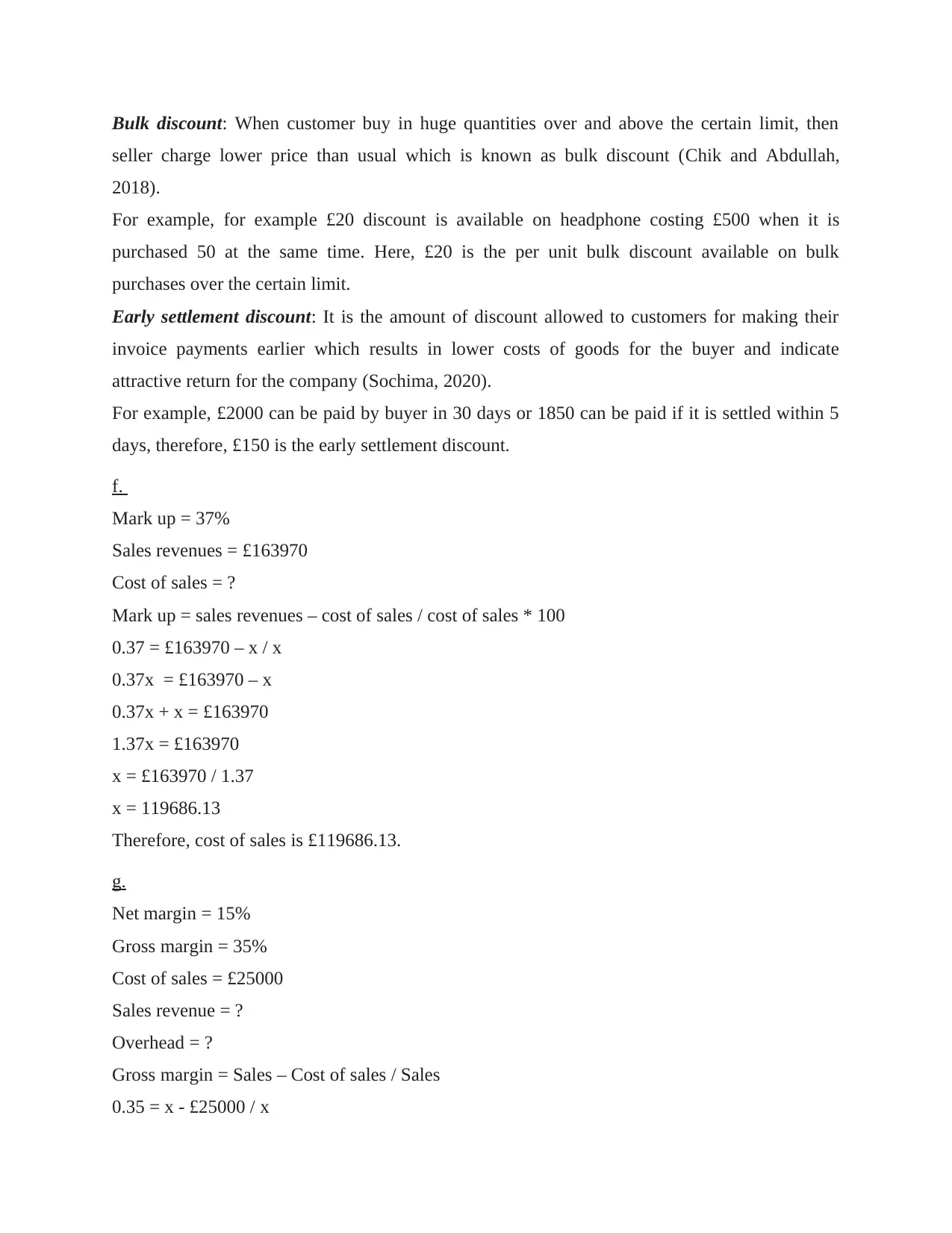

Bulk discount: When customer buy in huge quantities over and above the certain limit, then

seller charge lower price than usual which is known as bulk discount (Chik and Abdullah,

2018).

For example, for example £20 discount is available on headphone costing £500 when it is

purchased 50 at the same time. Here, £20 is the per unit bulk discount available on bulk

purchases over the certain limit.

Early settlement discount: It is the amount of discount allowed to customers for making their

invoice payments earlier which results in lower costs of goods for the buyer and indicate

attractive return for the company (Sochima, 2020).

For example, £2000 can be paid by buyer in 30 days or 1850 can be paid if it is settled within 5

days, therefore, £150 is the early settlement discount.

f.

Mark up = 37%

Sales revenues = £163970

Cost of sales = ?

Mark up = sales revenues – cost of sales / cost of sales * 100

0.37 = £163970 – x / x

0.37x = £163970 – x

0.37x + x = £163970

1.37x = £163970

x = £163970 / 1.37

x = 119686.13

Therefore, cost of sales is £119686.13.

g.

Net margin = 15%

Gross margin = 35%

Cost of sales = £25000

Sales revenue = ?

Overhead = ?

Gross margin = Sales – Cost of sales / Sales

0.35 = x - £25000 / x

seller charge lower price than usual which is known as bulk discount (Chik and Abdullah,

2018).

For example, for example £20 discount is available on headphone costing £500 when it is

purchased 50 at the same time. Here, £20 is the per unit bulk discount available on bulk

purchases over the certain limit.

Early settlement discount: It is the amount of discount allowed to customers for making their

invoice payments earlier which results in lower costs of goods for the buyer and indicate

attractive return for the company (Sochima, 2020).

For example, £2000 can be paid by buyer in 30 days or 1850 can be paid if it is settled within 5

days, therefore, £150 is the early settlement discount.

f.

Mark up = 37%

Sales revenues = £163970

Cost of sales = ?

Mark up = sales revenues – cost of sales / cost of sales * 100

0.37 = £163970 – x / x

0.37x = £163970 – x

0.37x + x = £163970

1.37x = £163970

x = £163970 / 1.37

x = 119686.13

Therefore, cost of sales is £119686.13.

g.

Net margin = 15%

Gross margin = 35%

Cost of sales = £25000

Sales revenue = ?

Overhead = ?

Gross margin = Sales – Cost of sales / Sales

0.35 = x - £25000 / x

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

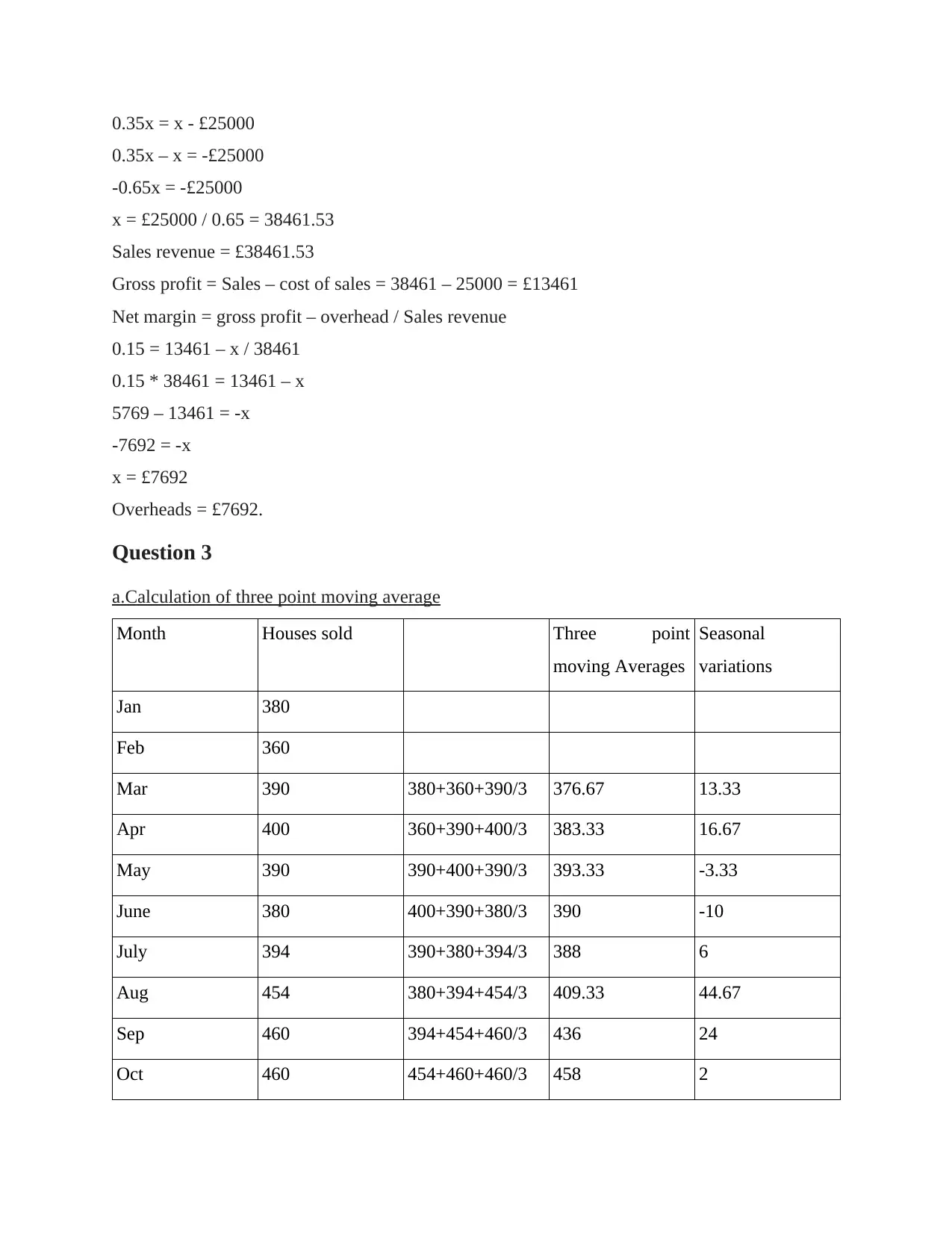

0.35x = x - £25000

0.35x – x = -£25000

-0.65x = -£25000

x = £25000 / 0.65 = 38461.53

Sales revenue = £38461.53

Gross profit = Sales – cost of sales = 38461 – 25000 = £13461

Net margin = gross profit – overhead / Sales revenue

0.15 = 13461 – x / 38461

0.15 * 38461 = 13461 – x

5769 – 13461 = -x

-7692 = -x

x = £7692

Overheads = £7692.

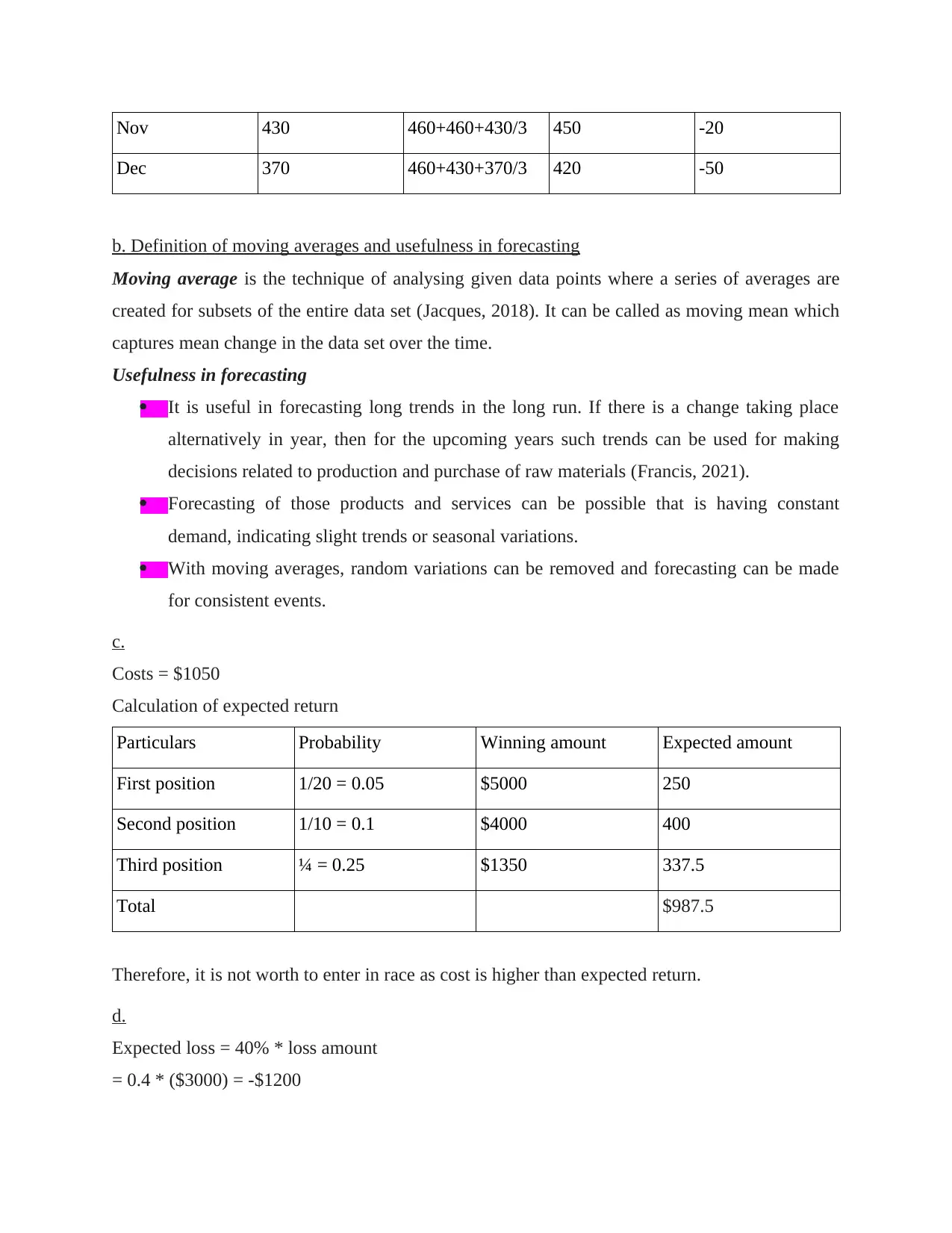

Question 3

a.Calculation of three point moving average

Month Houses sold Three point

moving Averages

Seasonal

variations

Jan 380

Feb 360

Mar 390 380+360+390/3 376.67 13.33

Apr 400 360+390+400/3 383.33 16.67

May 390 390+400+390/3 393.33 -3.33

June 380 400+390+380/3 390 -10

July 394 390+380+394/3 388 6

Aug 454 380+394+454/3 409.33 44.67

Sep 460 394+454+460/3 436 24

Oct 460 454+460+460/3 458 2

0.35x – x = -£25000

-0.65x = -£25000

x = £25000 / 0.65 = 38461.53

Sales revenue = £38461.53

Gross profit = Sales – cost of sales = 38461 – 25000 = £13461

Net margin = gross profit – overhead / Sales revenue

0.15 = 13461 – x / 38461

0.15 * 38461 = 13461 – x

5769 – 13461 = -x

-7692 = -x

x = £7692

Overheads = £7692.

Question 3

a.Calculation of three point moving average

Month Houses sold Three point

moving Averages

Seasonal

variations

Jan 380

Feb 360

Mar 390 380+360+390/3 376.67 13.33

Apr 400 360+390+400/3 383.33 16.67

May 390 390+400+390/3 393.33 -3.33

June 380 400+390+380/3 390 -10

July 394 390+380+394/3 388 6

Aug 454 380+394+454/3 409.33 44.67

Sep 460 394+454+460/3 436 24

Oct 460 454+460+460/3 458 2

Nov 430 460+460+430/3 450 -20

Dec 370 460+430+370/3 420 -50

b. Definition of moving averages and usefulness in forecasting

Moving average is the technique of analysing given data points where a series of averages are

created for subsets of the entire data set (Jacques, 2018). It can be called as moving mean which

captures mean change in the data set over the time.

Usefulness in forecasting

It is useful in forecasting long trends in the long run. If there is a change taking place

alternatively in year, then for the upcoming years such trends can be used for making

decisions related to production and purchase of raw materials (Francis, 2021).

Forecasting of those products and services can be possible that is having constant

demand, indicating slight trends or seasonal variations.

With moving averages, random variations can be removed and forecasting can be made

for consistent events.

c.

Costs = $1050

Calculation of expected return

Particulars Probability Winning amount Expected amount

First position 1/20 = 0.05 $5000 250

Second position 1/10 = 0.1 $4000 400

Third position ¼ = 0.25 $1350 337.5

Total $987.5

Therefore, it is not worth to enter in race as cost is higher than expected return.

d.

Expected loss = 40% * loss amount

= 0.4 * ($3000) = -$1200

Dec 370 460+430+370/3 420 -50

b. Definition of moving averages and usefulness in forecasting

Moving average is the technique of analysing given data points where a series of averages are

created for subsets of the entire data set (Jacques, 2018). It can be called as moving mean which

captures mean change in the data set over the time.

Usefulness in forecasting

It is useful in forecasting long trends in the long run. If there is a change taking place

alternatively in year, then for the upcoming years such trends can be used for making

decisions related to production and purchase of raw materials (Francis, 2021).

Forecasting of those products and services can be possible that is having constant

demand, indicating slight trends or seasonal variations.

With moving averages, random variations can be removed and forecasting can be made

for consistent events.

c.

Costs = $1050

Calculation of expected return

Particulars Probability Winning amount Expected amount

First position 1/20 = 0.05 $5000 250

Second position 1/10 = 0.1 $4000 400

Third position ¼ = 0.25 $1350 337.5

Total $987.5

Therefore, it is not worth to enter in race as cost is higher than expected return.

d.

Expected loss = 40% * loss amount

= 0.4 * ($3000) = -$1200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expected profit = 15% * $5500 = $825

Therefore, investment is not profitable as expected loss is higher than expected profit.

e.

Cost of inventory destroyed by fire = Opening inventory on 1st January 2006 + Purchases made

during the month – cost of goods sold – closing inventory on 31st January 2006

Cost of goods sold = Sales amount / gross profit margin

= $32500 / 130 * 100 = $25000

Cost of inventory destroyed = $19000 + $24000 - $25000 - $11000 = $7000.

Question 4

(a) Calculation of Pay Back Period

Product A

Years Cash flows £ Cumulative cash flows £

0 -45000 -45000

1 7200 -37800

2 7200 -30600

3 13200 -17400

4 25200 7800

Pay Back Period = 3 years + 17400/25200

= 3 years + 0.69 months

= 3.7 years (approx)

Product B

Years Cash flows £ Cumulative cash flows £

0 -45000 -45000

1 3600 -41400

2 7600 -33800

Therefore, investment is not profitable as expected loss is higher than expected profit.

e.

Cost of inventory destroyed by fire = Opening inventory on 1st January 2006 + Purchases made

during the month – cost of goods sold – closing inventory on 31st January 2006

Cost of goods sold = Sales amount / gross profit margin

= $32500 / 130 * 100 = $25000

Cost of inventory destroyed = $19000 + $24000 - $25000 - $11000 = $7000.

Question 4

(a) Calculation of Pay Back Period

Product A

Years Cash flows £ Cumulative cash flows £

0 -45000 -45000

1 7200 -37800

2 7200 -30600

3 13200 -17400

4 25200 7800

Pay Back Period = 3 years + 17400/25200

= 3 years + 0.69 months

= 3.7 years (approx)

Product B

Years Cash flows £ Cumulative cash flows £

0 -45000 -45000

1 3600 -41400

2 7600 -33800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3 15600 -18200

4 19000 800

Pay Back Period = 3 years + 18200/ 19000

= 3 years + 0.96 months

= 4 years (approx)

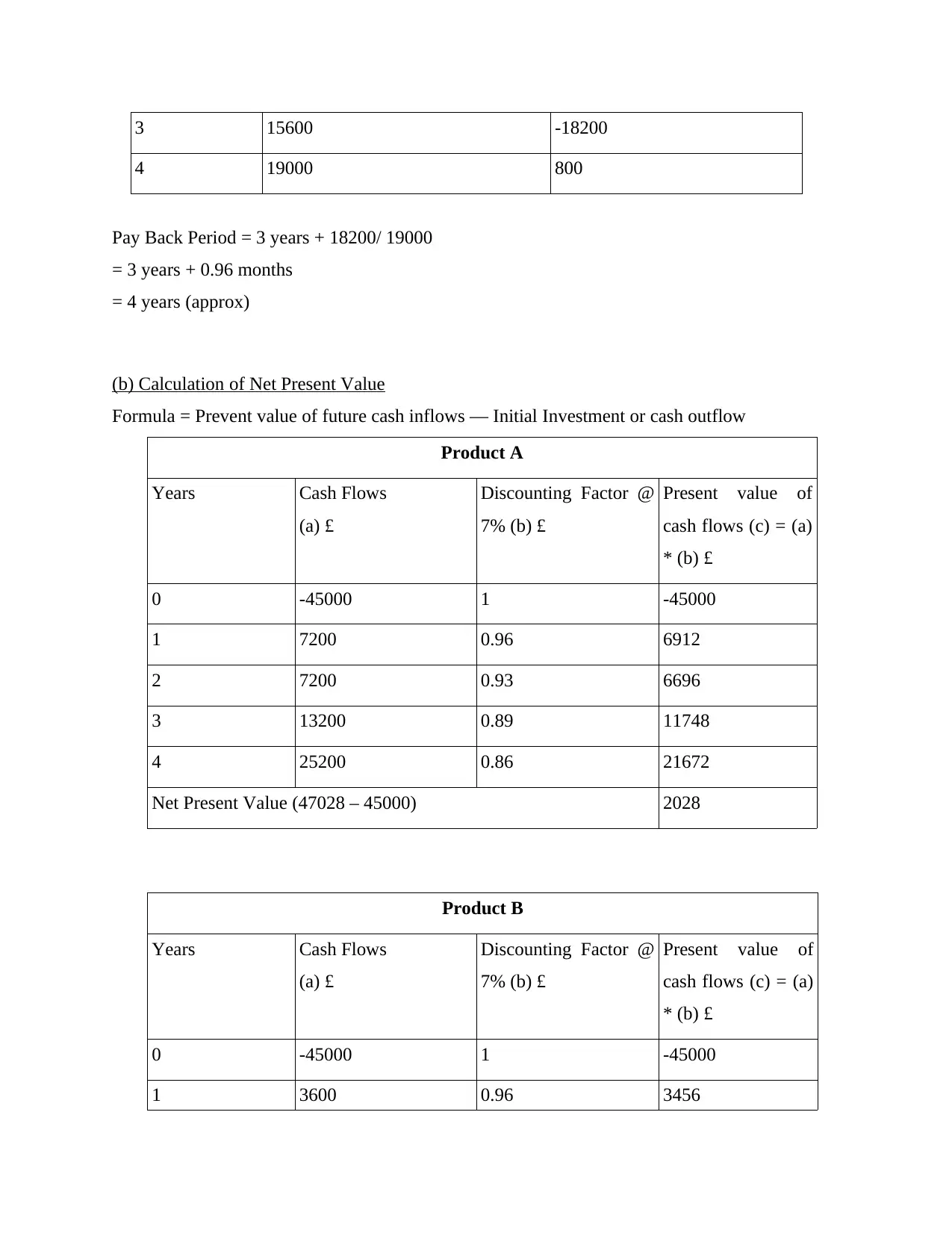

(b) Calculation of Net Present Value

Formula = Prevent value of future cash inflows — Initial Investment or cash outflow

Product A

Years Cash Flows

(a) £

Discounting Factor @

7% (b) £

Present value of

cash flows (c) = (a)

* (b) £

0 -45000 1 -45000

1 7200 0.96 6912

2 7200 0.93 6696

3 13200 0.89 11748

4 25200 0.86 21672

Net Present Value (47028 – 45000) 2028

Product B

Years Cash Flows

(a) £

Discounting Factor @

7% (b) £

Present value of

cash flows (c) = (a)

* (b) £

0 -45000 1 -45000

1 3600 0.96 3456

4 19000 800

Pay Back Period = 3 years + 18200/ 19000

= 3 years + 0.96 months

= 4 years (approx)

(b) Calculation of Net Present Value

Formula = Prevent value of future cash inflows — Initial Investment or cash outflow

Product A

Years Cash Flows

(a) £

Discounting Factor @

7% (b) £

Present value of

cash flows (c) = (a)

* (b) £

0 -45000 1 -45000

1 7200 0.96 6912

2 7200 0.93 6696

3 13200 0.89 11748

4 25200 0.86 21672

Net Present Value (47028 – 45000) 2028

Product B

Years Cash Flows

(a) £

Discounting Factor @

7% (b) £

Present value of

cash flows (c) = (a)

* (b) £

0 -45000 1 -45000

1 3600 0.96 3456

2 7600 0.93 7068

3 15600 0.89 13884

4 19000 0.86 16340

Net Present Value (40748 – 45000) -4252

(c)

On the basis of analysis of both products using pay back and NPV technique, it is

recommendable to the company that they have to opt for Product A. It is because the overall the

net present value of product A is positives along with small pay back period. This means that

Product A is most suitable and profitable option for the company as NPV consider time value

concept in their calculations (Harris, Hoang and Ngan, 2017). This technique is best for selecting

options of same size and identifying which option will provide more benefits to the company.

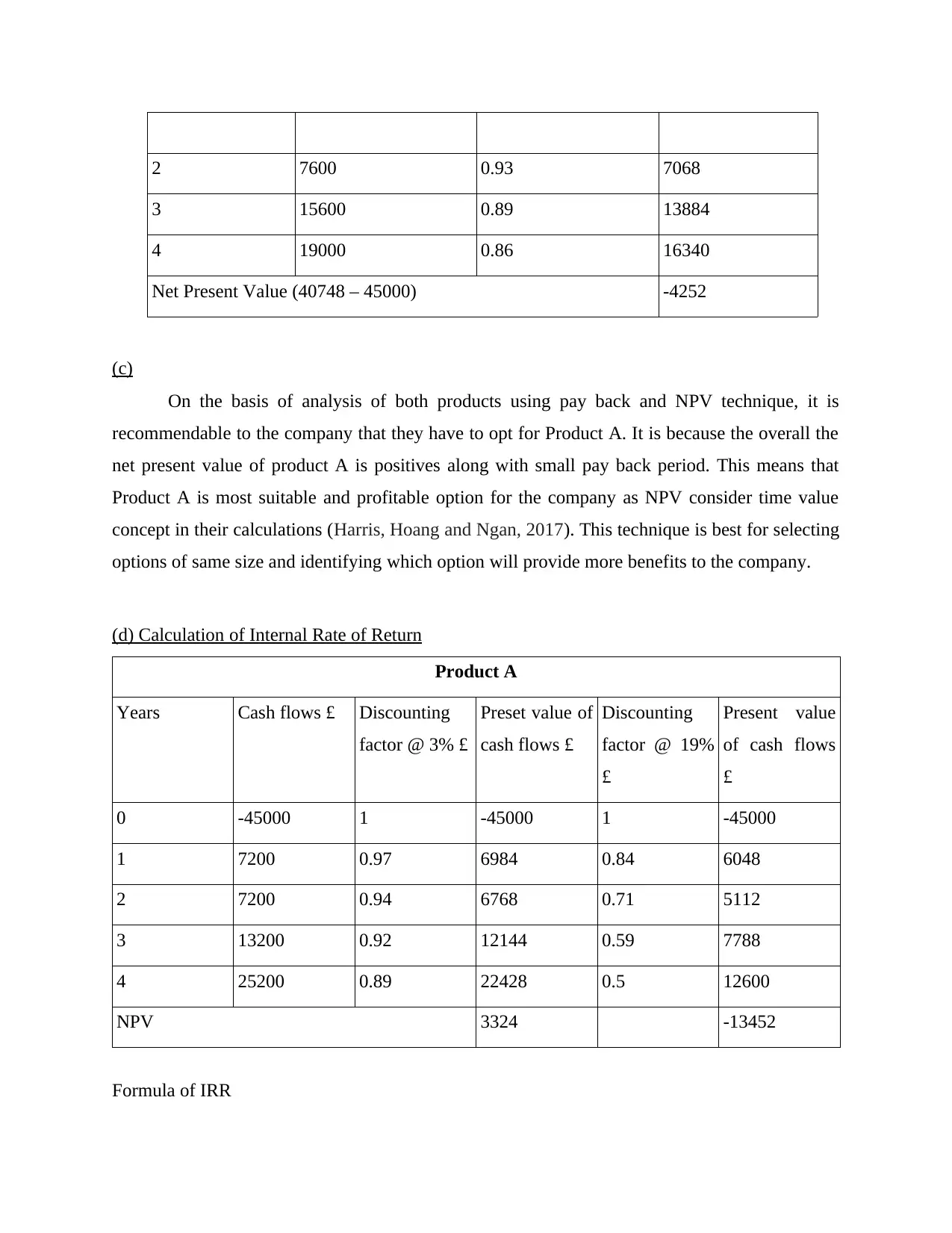

(d) Calculation of Internal Rate of Return

Product A

Years Cash flows £ Discounting

factor @ 3% £

Preset value of

cash flows £

Discounting

factor @ 19%

£

Present value

of cash flows

£

0 -45000 1 -45000 1 -45000

1 7200 0.97 6984 0.84 6048

2 7200 0.94 6768 0.71 5112

3 13200 0.92 12144 0.59 7788

4 25200 0.89 22428 0.5 12600

NPV 3324 -13452

Formula of IRR

3 15600 0.89 13884

4 19000 0.86 16340

Net Present Value (40748 – 45000) -4252

(c)

On the basis of analysis of both products using pay back and NPV technique, it is

recommendable to the company that they have to opt for Product A. It is because the overall the

net present value of product A is positives along with small pay back period. This means that

Product A is most suitable and profitable option for the company as NPV consider time value

concept in their calculations (Harris, Hoang and Ngan, 2017). This technique is best for selecting

options of same size and identifying which option will provide more benefits to the company.

(d) Calculation of Internal Rate of Return

Product A

Years Cash flows £ Discounting

factor @ 3% £

Preset value of

cash flows £

Discounting

factor @ 19%

£

Present value

of cash flows

£

0 -45000 1 -45000 1 -45000

1 7200 0.97 6984 0.84 6048

2 7200 0.94 6768 0.71 5112

3 13200 0.92 12144 0.59 7788

4 25200 0.89 22428 0.5 12600

NPV 3324 -13452

Formula of IRR

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.