Business Model Finance: Capital Structure and Working Capital Analysis

VerifiedAdded on 2023/06/17

|11

|2672

|476

Report

AI Summary

This report provides a comprehensive analysis of a business model, focusing on capital structure, working capital management, and related financial decisions. It includes calculations for right issues, earnings per share (EPS) under different financing scenarios, cost of equity, and company valuation. The report also examines the impact of takeovers on share prices, determines optimal cash offers, and evaluates inventory management policies using economic order quantity (EOQ). Furthermore, it discusses the theoretical aspects of capital structure, including bankruptcy costs and their changes during financial crises, and explores various strategies for effective working capital management, such as inventory, cash, and accounts receivable management. Desklib offers this and many other solved assignments to aid students.

Business Model

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

SECTION A.....................................................................................................................................3

Q1................................................................................................................................................3

Q2................................................................................................................................................4

Q3................................................................................................................................................5

Q4................................................................................................................................................5

Q5................................................................................................................................................6

Q6................................................................................................................................................7

SECTION B.....................................................................................................................................8

Q3................................................................................................................................................8

SECTION C.....................................................................................................................................9

Q4................................................................................................................................................9

REFERENCES..............................................................................................................................11

SECTION A.....................................................................................................................................3

Q1................................................................................................................................................3

Q2................................................................................................................................................4

Q3................................................................................................................................................5

Q4................................................................................................................................................5

Q5................................................................................................................................................6

Q6................................................................................................................................................7

SECTION B.....................................................................................................................................8

Q3................................................................................................................................................8

SECTION C.....................................................................................................................................9

Q4................................................................................................................................................9

REFERENCES..............................................................................................................................11

SECTION A

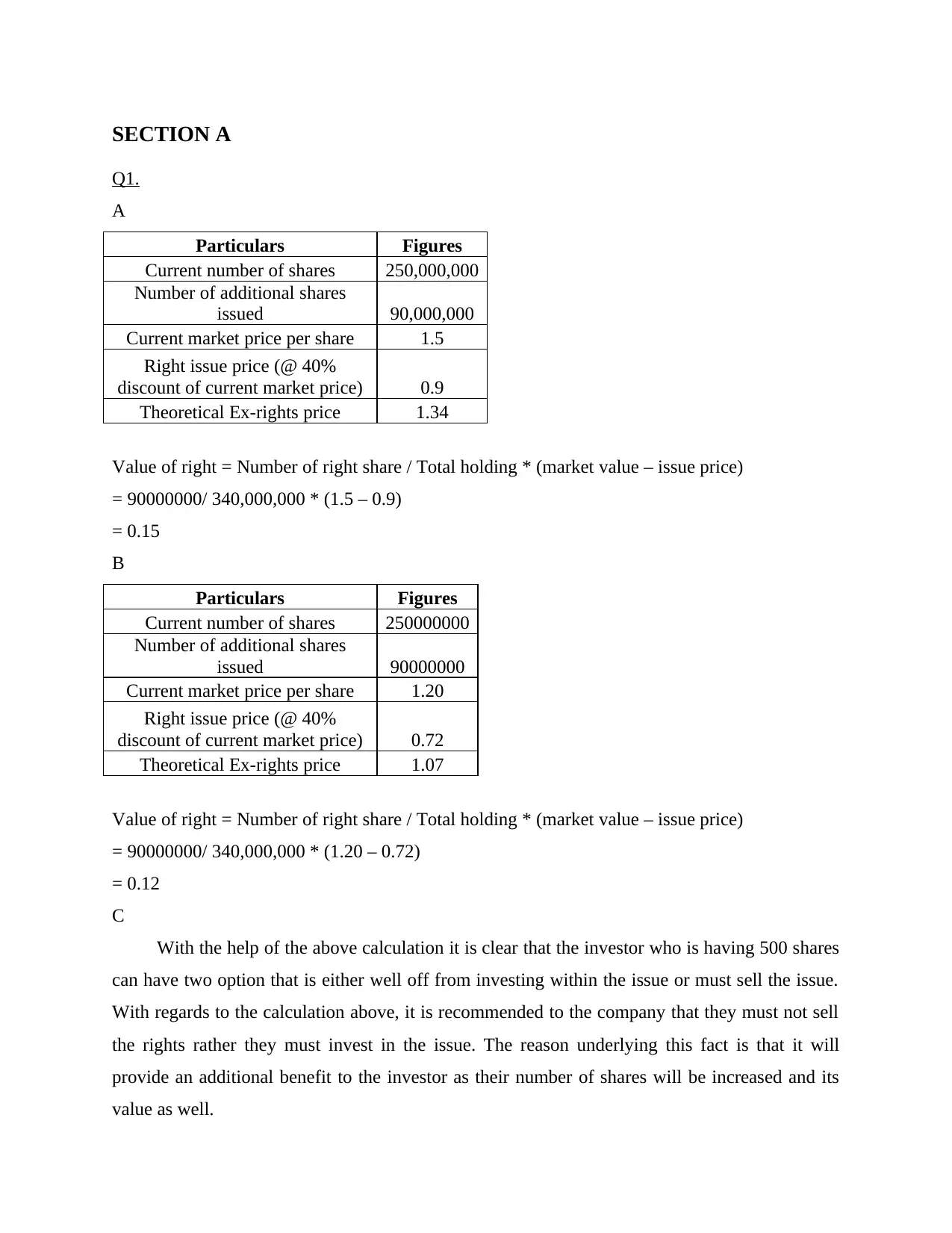

Q1.

A

Particulars Figures

Current number of shares 250,000,000

Number of additional shares

issued 90,000,000

Current market price per share 1.5

Right issue price (@ 40%

discount of current market price) 0.9

Theoretical Ex-rights price 1.34

Value of right = Number of right share / Total holding * (market value – issue price)

= 90000000/ 340,000,000 * (1.5 – 0.9)

= 0.15

B

Particulars Figures

Current number of shares 250000000

Number of additional shares

issued 90000000

Current market price per share 1.20

Right issue price (@ 40%

discount of current market price) 0.72

Theoretical Ex-rights price 1.07

Value of right = Number of right share / Total holding * (market value – issue price)

= 90000000/ 340,000,000 * (1.20 – 0.72)

= 0.12

C

With the help of the above calculation it is clear that the investor who is having 500 shares

can have two option that is either well off from investing within the issue or must sell the issue.

With regards to the calculation above, it is recommended to the company that they must not sell

the rights rather they must invest in the issue. The reason underlying this fact is that it will

provide an additional benefit to the investor as their number of shares will be increased and its

value as well.

Q1.

A

Particulars Figures

Current number of shares 250,000,000

Number of additional shares

issued 90,000,000

Current market price per share 1.5

Right issue price (@ 40%

discount of current market price) 0.9

Theoretical Ex-rights price 1.34

Value of right = Number of right share / Total holding * (market value – issue price)

= 90000000/ 340,000,000 * (1.5 – 0.9)

= 0.15

B

Particulars Figures

Current number of shares 250000000

Number of additional shares

issued 90000000

Current market price per share 1.20

Right issue price (@ 40%

discount of current market price) 0.72

Theoretical Ex-rights price 1.07

Value of right = Number of right share / Total holding * (market value – issue price)

= 90000000/ 340,000,000 * (1.20 – 0.72)

= 0.12

C

With the help of the above calculation it is clear that the investor who is having 500 shares

can have two option that is either well off from investing within the issue or must sell the issue.

With regards to the calculation above, it is recommended to the company that they must not sell

the rights rather they must invest in the issue. The reason underlying this fact is that it will

provide an additional benefit to the investor as their number of shares will be increased and its

value as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

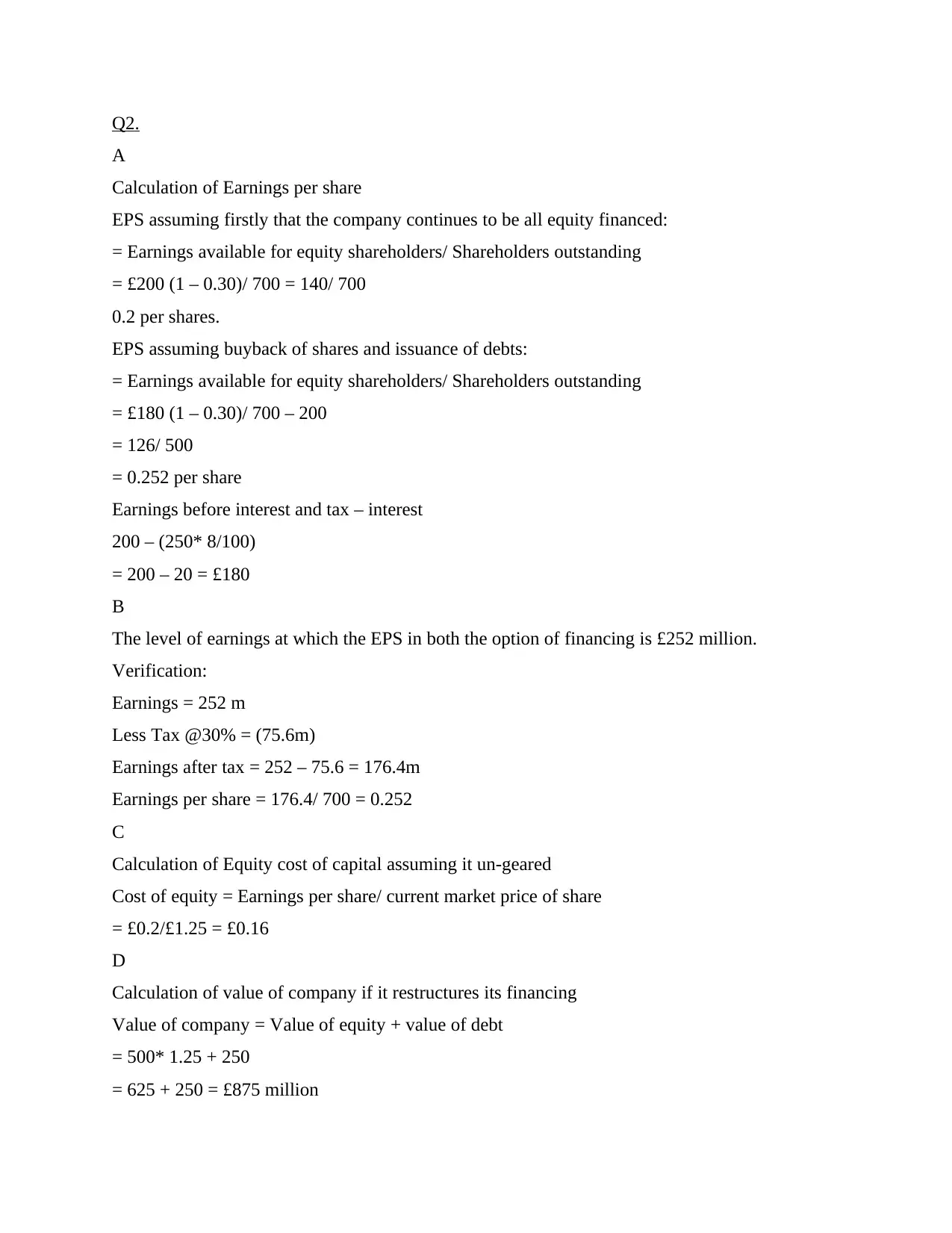

Q2.

A

Calculation of Earnings per share

EPS assuming firstly that the company continues to be all equity financed:

= Earnings available for equity shareholders/ Shareholders outstanding

= £200 (1 – 0.30)/ 700 = 140/ 700

0.2 per shares.

EPS assuming buyback of shares and issuance of debts:

= Earnings available for equity shareholders/ Shareholders outstanding

= £180 (1 – 0.30)/ 700 – 200

= 126/ 500

= 0.252 per share

Earnings before interest and tax – interest

200 – (250* 8/100)

= 200 – 20 = £180

B

The level of earnings at which the EPS in both the option of financing is £252 million.

Verification:

Earnings = 252 m

Less Tax @30% = (75.6m)

Earnings after tax = 252 – 75.6 = 176.4m

Earnings per share = 176.4/ 700 = 0.252

C

Calculation of Equity cost of capital assuming it un-geared

Cost of equity = Earnings per share/ current market price of share

= £0.2/£1.25 = £0.16

D

Calculation of value of company if it restructures its financing

Value of company = Value of equity + value of debt

= 500* 1.25 + 250

= 625 + 250 = £875 million

A

Calculation of Earnings per share

EPS assuming firstly that the company continues to be all equity financed:

= Earnings available for equity shareholders/ Shareholders outstanding

= £200 (1 – 0.30)/ 700 = 140/ 700

0.2 per shares.

EPS assuming buyback of shares and issuance of debts:

= Earnings available for equity shareholders/ Shareholders outstanding

= £180 (1 – 0.30)/ 700 – 200

= 126/ 500

= 0.252 per share

Earnings before interest and tax – interest

200 – (250* 8/100)

= 200 – 20 = £180

B

The level of earnings at which the EPS in both the option of financing is £252 million.

Verification:

Earnings = 252 m

Less Tax @30% = (75.6m)

Earnings after tax = 252 – 75.6 = 176.4m

Earnings per share = 176.4/ 700 = 0.252

C

Calculation of Equity cost of capital assuming it un-geared

Cost of equity = Earnings per share/ current market price of share

= £0.2/£1.25 = £0.16

D

Calculation of value of company if it restructures its financing

Value of company = Value of equity + value of debt

= 500* 1.25 + 250

= 625 + 250 = £875 million

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

E

Expected earnings for the next year = 200m

Less: Interest @8% on 250m = (20m)

Profit before tax = 180m

less: Tax @30% of 180m = (54m)

Profit after interest and tax = 126m

Expected Earnings per share = 126000000 / 500000000 = 0.252

Cost of equity = Expected earnings per share / Current market share price

= 0.252 / 1.25 * 100 = 20.16%

Weighted Average Cost of Capital

= equity capital / total capital * cost of equity + debt capital / total capital * Cost of debt

= (500m / 500m+250m) * 20.16% + (250m / 750m) * 8%

Q3.

A

Cost of proposed takeover:

500 * 7 – 300 * 10.2

= 440 million

B

The takeover will have a positive impact over the share price of Robertson plc as the

company is offering a share of less value of 3060 million and in against to this company is taking

a share value of 3500 million. As the entire deal is favourable for the Robortson plc which will

create a positive impact over the value of shares of company. The entire deal is profitable for the

company. The value of the shares of Kane plc is more than the value of the shares allotted to the

company that will further have a positive impact over value of company. This entire deal will

allow the Robertson plc to achieve the cost saving objective of the deal.

Q4.

A

Determine the highest cash offer that Tierney could afford to make for Shaw’s shares and still

meet the management’s objective of increasing share price by 5 per cent, and the premium to the

current market value of Shaw Plc.

Value of Tierney= 50 * 5 = 250

Expected earnings for the next year = 200m

Less: Interest @8% on 250m = (20m)

Profit before tax = 180m

less: Tax @30% of 180m = (54m)

Profit after interest and tax = 126m

Expected Earnings per share = 126000000 / 500000000 = 0.252

Cost of equity = Expected earnings per share / Current market share price

= 0.252 / 1.25 * 100 = 20.16%

Weighted Average Cost of Capital

= equity capital / total capital * cost of equity + debt capital / total capital * Cost of debt

= (500m / 500m+250m) * 20.16% + (250m / 750m) * 8%

Q3.

A

Cost of proposed takeover:

500 * 7 – 300 * 10.2

= 440 million

B

The takeover will have a positive impact over the share price of Robertson plc as the

company is offering a share of less value of 3060 million and in against to this company is taking

a share value of 3500 million. As the entire deal is favourable for the Robortson plc which will

create a positive impact over the value of shares of company. The entire deal is profitable for the

company. The value of the shares of Kane plc is more than the value of the shares allotted to the

company that will further have a positive impact over value of company. This entire deal will

allow the Robertson plc to achieve the cost saving objective of the deal.

Q4.

A

Determine the highest cash offer that Tierney could afford to make for Shaw’s shares and still

meet the management’s objective of increasing share price by 5 per cent, and the premium to the

current market value of Shaw Plc.

Value of Tierney= 50 * 5 = 250

Value of Shaw’s equity = 60 * 0.5 = 30

Afford to pay premium = 20 – 12.5 = 7.5

Maximum offer = market value + premium

= 30 + 7.5 = 37.5

Maximum premium = 7.5 / 30 = 0.25

Value after takeover on basis of market value

V(TS) = V (T) + V(S) + GAIN – cost

= 250 + 30 + 20 – (37.5)

= 262.5

B

Value after takeover

V(TS) = V(T) + V (S) + gain

=250 + 30 + 20

300

The company Tierney in requiring 262.5 for acquiring the company so it reflects the share price

of will be 262.5 / 50 = 5.25

Maximum number of shares which can issues is (300 – 262.5) / 5.25 = 7142857.14 shares.

Q5.

A

The order cost for each time machine is 10000

So for 6 runs it will be 10000*6 = 60000

For holding one unit of stock is 20

So for 4800 units holding cost = 4800 * 20 = 96000

B

The company must amend the inventory management policy with respect to the above

calculation. The reason underlying the fact is that the holding cost is high for the company and

because of this they must work on their inventory management. The reason pertaining to the fact

is that when the company will be having good inventory management techniques then stock will

be sold fast and company will not have to hold the inventory. Hence, as a result of this, the

holding cost will be reduced.

C

Afford to pay premium = 20 – 12.5 = 7.5

Maximum offer = market value + premium

= 30 + 7.5 = 37.5

Maximum premium = 7.5 / 30 = 0.25

Value after takeover on basis of market value

V(TS) = V (T) + V(S) + GAIN – cost

= 250 + 30 + 20 – (37.5)

= 262.5

B

Value after takeover

V(TS) = V(T) + V (S) + gain

=250 + 30 + 20

300

The company Tierney in requiring 262.5 for acquiring the company so it reflects the share price

of will be 262.5 / 50 = 5.25

Maximum number of shares which can issues is (300 – 262.5) / 5.25 = 7142857.14 shares.

Q5.

A

The order cost for each time machine is 10000

So for 6 runs it will be 10000*6 = 60000

For holding one unit of stock is 20

So for 4800 units holding cost = 4800 * 20 = 96000

B

The company must amend the inventory management policy with respect to the above

calculation. The reason underlying the fact is that the holding cost is high for the company and

because of this they must work on their inventory management. The reason pertaining to the fact

is that when the company will be having good inventory management techniques then stock will

be sold fast and company will not have to hold the inventory. Hence, as a result of this, the

holding cost will be reduced.

C

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Economic order quantity = √ (2 * D * S) / H

√ (2 * 4800 * 60000) / 96000

= √576000000 / 96000

=√6000

= 77.460

D

It is assumed that there is not any delay or wastage in any of the 6 product runs of the

machine and there is total of 800 windows produced per run.

For the present calculation of economic order quantity, it is assumed that ordering cost

remains constant for every run. This simply means that in every run of production the ordering

cost is 10000 and for total runs of production the total cost is 60000.

Q6.

A

The daily opportunity cost of holding cash.

The real interest rate is 4 % and it is assumed that expected inflation rate will be 10 %=

0.04 + 0.10 = 0.14

Opportunity cost = 2800

B

The target / return cash balance for the company under the Miller-Orr model.

Lower limit = 20000

Spread= 3 (3/4 * 150*114.0175 / 0.04) = 40205.34

Return point= lower limit + 1/3 * spread

20000 + 1/3 * 40205.34

33401.78

C

The upper limit of the company’s cash balance.

20205.34

D

The average daily cash balance.

40205.34 / 30 = 1340.178

√ (2 * 4800 * 60000) / 96000

= √576000000 / 96000

=√6000

= 77.460

D

It is assumed that there is not any delay or wastage in any of the 6 product runs of the

machine and there is total of 800 windows produced per run.

For the present calculation of economic order quantity, it is assumed that ordering cost

remains constant for every run. This simply means that in every run of production the ordering

cost is 10000 and for total runs of production the total cost is 60000.

Q6.

A

The daily opportunity cost of holding cash.

The real interest rate is 4 % and it is assumed that expected inflation rate will be 10 %=

0.04 + 0.10 = 0.14

Opportunity cost = 2800

B

The target / return cash balance for the company under the Miller-Orr model.

Lower limit = 20000

Spread= 3 (3/4 * 150*114.0175 / 0.04) = 40205.34

Return point= lower limit + 1/3 * spread

20000 + 1/3 * 40205.34

33401.78

C

The upper limit of the company’s cash balance.

20205.34

D

The average daily cash balance.

40205.34 / 30 = 1340.178

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION B

Q3.

Capital structure theory is concerned with proportion of equity & debt so that systematic

approach of financing can be done effectively. This is one of the systematic approach of that

allows particular organization to finance its business activities through combing suitable ratio of

equity & liabilities. There are two types of cost such as direct and indirect that play important in

identifying total cost of capital.

Bankruptcy usually occurs when there is higher proportion of debt in capital structure of

company as compared to equity. For utilizing debt, it becomes essential for the organization to

give higher emphasis on keeping certain amount of money apart from utilizing in order to pay as

interest for using fund (Dou, and et.al., 2021). It need to pay on timely basis and inability to

overcome this can result in bankrupt situation of business. On the other side, for gaining optimal

structure of capital for the organization, company concentrate on inclining debt so that less tax

liability is can be paid.

Bankruptcy cost are distinct between two categories such as direct and indirect. The

direct cost includes bankruptcy filing, lawyers’ accounting fees and professional service cost. In

addition to this, indirect cost includes agency related expenses, decreased sales, lost managerial

time in anticipation of bankruptcy cost (Rosslyn-Smith, De Abreu and Pretorius, 2020). These

both the cost need to be paid by organization in respect of get optimal capital structure. These

cost are required to be overcome for meeting its objective of overcoming prevailing obligations.

In the financial crises, indirect costs of bankruptcy are expected to change as there are

various affecting factors (Shah, 2021). It is found to be inclined due to breakdown of explicit and

implicit contracts of capital structure. There is found in inclined due to decrease in risk taking

power of stakeholders which result in low availability of liquidity and impact processing of firm.

In the times of financial crises, mobility of funds decreases that highly affect operational

practices of business. It affects purchasing power of customers that result in decrease

profitability and sales revenue of company. There is need to increase such productivity and

trustworthiness among stakeholders in turn risk taking power can be developed. Financial crises

majorly affect functioning and operational practices due to low availability of liquidity. It does

not allow firm to overcome its obligations which indirectly affect reputation for company.

Q3.

Capital structure theory is concerned with proportion of equity & debt so that systematic

approach of financing can be done effectively. This is one of the systematic approach of that

allows particular organization to finance its business activities through combing suitable ratio of

equity & liabilities. There are two types of cost such as direct and indirect that play important in

identifying total cost of capital.

Bankruptcy usually occurs when there is higher proportion of debt in capital structure of

company as compared to equity. For utilizing debt, it becomes essential for the organization to

give higher emphasis on keeping certain amount of money apart from utilizing in order to pay as

interest for using fund (Dou, and et.al., 2021). It need to pay on timely basis and inability to

overcome this can result in bankrupt situation of business. On the other side, for gaining optimal

structure of capital for the organization, company concentrate on inclining debt so that less tax

liability is can be paid.

Bankruptcy cost are distinct between two categories such as direct and indirect. The

direct cost includes bankruptcy filing, lawyers’ accounting fees and professional service cost. In

addition to this, indirect cost includes agency related expenses, decreased sales, lost managerial

time in anticipation of bankruptcy cost (Rosslyn-Smith, De Abreu and Pretorius, 2020). These

both the cost need to be paid by organization in respect of get optimal capital structure. These

cost are required to be overcome for meeting its objective of overcoming prevailing obligations.

In the financial crises, indirect costs of bankruptcy are expected to change as there are

various affecting factors (Shah, 2021). It is found to be inclined due to breakdown of explicit and

implicit contracts of capital structure. There is found in inclined due to decrease in risk taking

power of stakeholders which result in low availability of liquidity and impact processing of firm.

In the times of financial crises, mobility of funds decreases that highly affect operational

practices of business. It affects purchasing power of customers that result in decrease

profitability and sales revenue of company. There is need to increase such productivity and

trustworthiness among stakeholders in turn risk taking power can be developed. Financial crises

majorly affect functioning and operational practices due to low availability of liquidity. It does

not allow firm to overcome its obligations which indirectly affect reputation for company.

From the evaluation, it can be interpreted that direct costing in financial crises includes

legal and administrative cost regarding proceeding of bankruptcy. On the other side, indirect

cost involves issues arising due to distress coming from incentives problems which makes firms

financial health weak (Kruk, 2021.). In this time of financial crises, it can be articulated that

such indirect cost arising in bankruptcy processing in the context of capital structure theory

changes due to higher distress coming from additional problems which are difficult to control.

These cost highly affect functioning of company which leads to bankruptcy situation in turn

occurring of negative impact in organizational process is found.

SECTION C

Q4.

Different types of strategies for management of working capital

Working capital management means the management of the liabilities, assets and relation

between them. The company should focus on the two things while managing the working capital

i.e. to consider the net working capital and to choose the best method of financing the working

capital. There are some strategies to manage the working capital are:

Inventory management: this management is the most important for any business to focus.

It includes the finished good of the business which is ready to sell in the market (Chalmers,

Sensini and Shan, 2020). This management focus on the raw material required to completion of

the production. The investment in the inventory should not be more as machines are depreciable.

The amount invested in the inventory depends upon the size of the organization. It is an

important part of the company because by selling the finished goods the company will be earning

the profits. So, the management of the company must manage the inventories effectively.

Cash management: The most liquid assets of the company is cash. The cash includes the

cheques, drafts, money and deposits in bank. It also includes the shares and other securities of

the market which are easily converted in cash. It is the most important part of the current assets.

The company should manage it cash for the better working capital. Cash management helps to

make the due payment of the company or to take cash from anyone. This makes to utilize the

proper cash flow in the company. The company should prepare budget for the proper flow of the

cash. It helps the company to reduce the wastage of the company.

Account Receivable Management: This is the important management that every company

must have. This helps the company to know about their debtors. As every company sells goods

legal and administrative cost regarding proceeding of bankruptcy. On the other side, indirect

cost involves issues arising due to distress coming from incentives problems which makes firms

financial health weak (Kruk, 2021.). In this time of financial crises, it can be articulated that

such indirect cost arising in bankruptcy processing in the context of capital structure theory

changes due to higher distress coming from additional problems which are difficult to control.

These cost highly affect functioning of company which leads to bankruptcy situation in turn

occurring of negative impact in organizational process is found.

SECTION C

Q4.

Different types of strategies for management of working capital

Working capital management means the management of the liabilities, assets and relation

between them. The company should focus on the two things while managing the working capital

i.e. to consider the net working capital and to choose the best method of financing the working

capital. There are some strategies to manage the working capital are:

Inventory management: this management is the most important for any business to focus.

It includes the finished good of the business which is ready to sell in the market (Chalmers,

Sensini and Shan, 2020). This management focus on the raw material required to completion of

the production. The investment in the inventory should not be more as machines are depreciable.

The amount invested in the inventory depends upon the size of the organization. It is an

important part of the company because by selling the finished goods the company will be earning

the profits. So, the management of the company must manage the inventories effectively.

Cash management: The most liquid assets of the company is cash. The cash includes the

cheques, drafts, money and deposits in bank. It also includes the shares and other securities of

the market which are easily converted in cash. It is the most important part of the current assets.

The company should manage it cash for the better working capital. Cash management helps to

make the due payment of the company or to take cash from anyone. This makes to utilize the

proper cash flow in the company. The company should prepare budget for the proper flow of the

cash. It helps the company to reduce the wastage of the company.

Account Receivable Management: This is the important management that every company

must have. This helps the company to know about their debtors. As every company sells goods

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

on credit because it attracts the customers to purchase the goods (NGUYEN, PHAM and

NGUYEN, 2020). The company must clearly state their credit policies to their customers as it

will not lead to any confusion in the future. This includes the terms of credit, standard of credit

and discounts offered by the company. This management helps in the collection of the payment

in the future time. The company should also check that the creditors are paying on the terms of

the credit.

Main cost: There are two types of main costs i.e. direct cost and indirect cost. Direct cost

is the cost which includes the direct expenses of the company like cost of raw materials, labour,

distribution costs etc. On the other hand, indirect cost includes the expenses which bare not

related with the production of goods and services.

Benefits of the Aggressive and conservative working capital:

Aggressive working capital benefits are that in this working capital management the short

term financing is economical as compared to long term financing. It reduces the risk of the

company as it is cheaper.

Conservative working capital benefits are- it helps the company to increase the liquidity

of the company. It also lower down the interest rate risk of the company.

NGUYEN, 2020). The company must clearly state their credit policies to their customers as it

will not lead to any confusion in the future. This includes the terms of credit, standard of credit

and discounts offered by the company. This management helps in the collection of the payment

in the future time. The company should also check that the creditors are paying on the terms of

the credit.

Main cost: There are two types of main costs i.e. direct cost and indirect cost. Direct cost

is the cost which includes the direct expenses of the company like cost of raw materials, labour,

distribution costs etc. On the other hand, indirect cost includes the expenses which bare not

related with the production of goods and services.

Benefits of the Aggressive and conservative working capital:

Aggressive working capital benefits are that in this working capital management the short

term financing is economical as compared to long term financing. It reduces the risk of the

company as it is cheaper.

Conservative working capital benefits are- it helps the company to increase the liquidity

of the company. It also lower down the interest rate risk of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Chalmers, D. K., Sensini, L. and Shan, A., 2020. Working Capital Management (WCM) and

Performance of SMEs: Evidence from India. International Journal of Business and

Social Science. 11(7). pp.57-63.

Dou, W. W. and et.al., 2021. Dissecting bankruptcy frictions. Journal of Financial Economics.

Kruk, S., 2021. Impact of Capital Structure on Corporate Value—Review of Literature. Journal

of Risk and Financial Management. 14(4). p.155.

NGUYEN, A. H., PHAM, H. T. and NGUYEN, H. T., 2020. Impact of working capital

management on firm's profitability: Empirical evidence from Vietnam. The Journal of

Asian Finance, Economics, and Business. 7(3). pp.115-125.

Rosslyn-Smith, W., De Abreu, N. V. A. and Pretorius, M., 2020. Exploring the indirect costs of a

firm in business rescue. South African Journal of Accounting Research. 34(1). pp.24-

44.

Shah, D. G., 2021. Durability, Indirect Bankruptcy Costs, and Capital Structure (Doctoral

dissertation, The University of North Carolina at Charlotte).

Books and Journals

Chalmers, D. K., Sensini, L. and Shan, A., 2020. Working Capital Management (WCM) and

Performance of SMEs: Evidence from India. International Journal of Business and

Social Science. 11(7). pp.57-63.

Dou, W. W. and et.al., 2021. Dissecting bankruptcy frictions. Journal of Financial Economics.

Kruk, S., 2021. Impact of Capital Structure on Corporate Value—Review of Literature. Journal

of Risk and Financial Management. 14(4). p.155.

NGUYEN, A. H., PHAM, H. T. and NGUYEN, H. T., 2020. Impact of working capital

management on firm's profitability: Empirical evidence from Vietnam. The Journal of

Asian Finance, Economics, and Business. 7(3). pp.115-125.

Rosslyn-Smith, W., De Abreu, N. V. A. and Pretorius, M., 2020. Exploring the indirect costs of a

firm in business rescue. South African Journal of Accounting Research. 34(1). pp.24-

44.

Shah, D. G., 2021. Durability, Indirect Bankruptcy Costs, and Capital Structure (Doctoral

dissertation, The University of North Carolina at Charlotte).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.