Business Modelling for Decision Making: Inventory, Profit, and Tree

VerifiedAdded on 2022/12/28

|14

|3187

|1

Report

AI Summary

This report delves into business modelling as a crucial aspect of business, enabling effective exploration of complex choices through various assumptions. It covers inventory management, non-linear/extremum problems, and decision tree analysis. Part A focuses on inventory, calculating EOQ for A545 Plasma TVs, determining optimal deliveries, and computing total annual variable costs. Part B explores non-linear/extremum analysis, creating a profit equation for a London furniture maker, setting up demand, costs, and profit tables, and differentiating the profit equation to maximize profit. Part C involves constructing and analyzing a decision tree based on a case study. The report concludes by highlighting the importance of business modelling in achieving organizational objectives and ensuring sustainability.

Business Modelling for

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION................................................................................................................................3

MAIN BODY......................................................................................................................................3

Part A – INVENTORY.........................................................................................................................3

(a). Computation of EOQ (economic-order quantity) with respect to A545 Plasma TV, applying

specific formula:...........................................................................................................................3

(b). On the basis of above computed EOQ level assessing how much quantities/deliveries

should be made of A545 Plasma TVs per year:............................................................................3

(c). Find the total annual variable cost for TV King Ltd:...............................................................4

(d).................................................................................................................................................4

(e).................................................................................................................................................4

Part B – NON-LINEAR/EXTREMUM..................................................................................................7

a) Finding out an equation with respect to profit level of London furniture makers:................7

b) Setting up demand, costs and profit table...............................................................................8

c) Using values from above stated table and drawing a demand, costs and profitability graph 8

(d). Based on above displayed graph, differentiating profit level equation to assess actual

value of ‘q’ where profit level maximises:...................................................................................9

e) Assessing value of ‘X’ coefficients dependent on q (Liverpool):..............................................9

f. Strong and weak points in the London and Liverpool models:................................................9

Part C – DECISION TREE.................................................................................................................10

SECTION 1...................................................................................................................................10

i...................................................................................................................................................10

ii. Decision Tree:.........................................................................................................................12

SECTION 2...................................................................................................................................12

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................14

INTRODUCTION................................................................................................................................3

MAIN BODY......................................................................................................................................3

Part A – INVENTORY.........................................................................................................................3

(a). Computation of EOQ (economic-order quantity) with respect to A545 Plasma TV, applying

specific formula:...........................................................................................................................3

(b). On the basis of above computed EOQ level assessing how much quantities/deliveries

should be made of A545 Plasma TVs per year:............................................................................3

(c). Find the total annual variable cost for TV King Ltd:...............................................................4

(d).................................................................................................................................................4

(e).................................................................................................................................................4

Part B – NON-LINEAR/EXTREMUM..................................................................................................7

a) Finding out an equation with respect to profit level of London furniture makers:................7

b) Setting up demand, costs and profit table...............................................................................8

c) Using values from above stated table and drawing a demand, costs and profitability graph 8

(d). Based on above displayed graph, differentiating profit level equation to assess actual

value of ‘q’ where profit level maximises:...................................................................................9

e) Assessing value of ‘X’ coefficients dependent on q (Liverpool):..............................................9

f. Strong and weak points in the London and Liverpool models:................................................9

Part C – DECISION TREE.................................................................................................................10

SECTION 1...................................................................................................................................10

i...................................................................................................................................................10

ii. Decision Tree:.........................................................................................................................12

SECTION 2...................................................................................................................................12

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................14

INTRODUCTION

Business modelling is vital aspect in business which allow managing personnel to effectively

explore complicated choices/alternatives, employing a comprehensive range of assumptions for

representing alternative potential operational business environments. Business modelling

is conceptual framework that promotes the company's sustainability and describes how it

works, makes cash including how it aims to accomplish its objectives. Business modelling

contains all of business processes and practices that business embraces and implements

(Cosenz and Noto, 2018). The study contains three different parts which are mainly focused on

different business modelling aspects. The first part covers inventory related aspects of business

modelling like EOQ, inventory system. Second part comprises non-linear/extremum tasks while

the third part covers creation of decision tree and analysis of decision tree based on a case

study.

MAIN BODY

Part A – INVENTORY

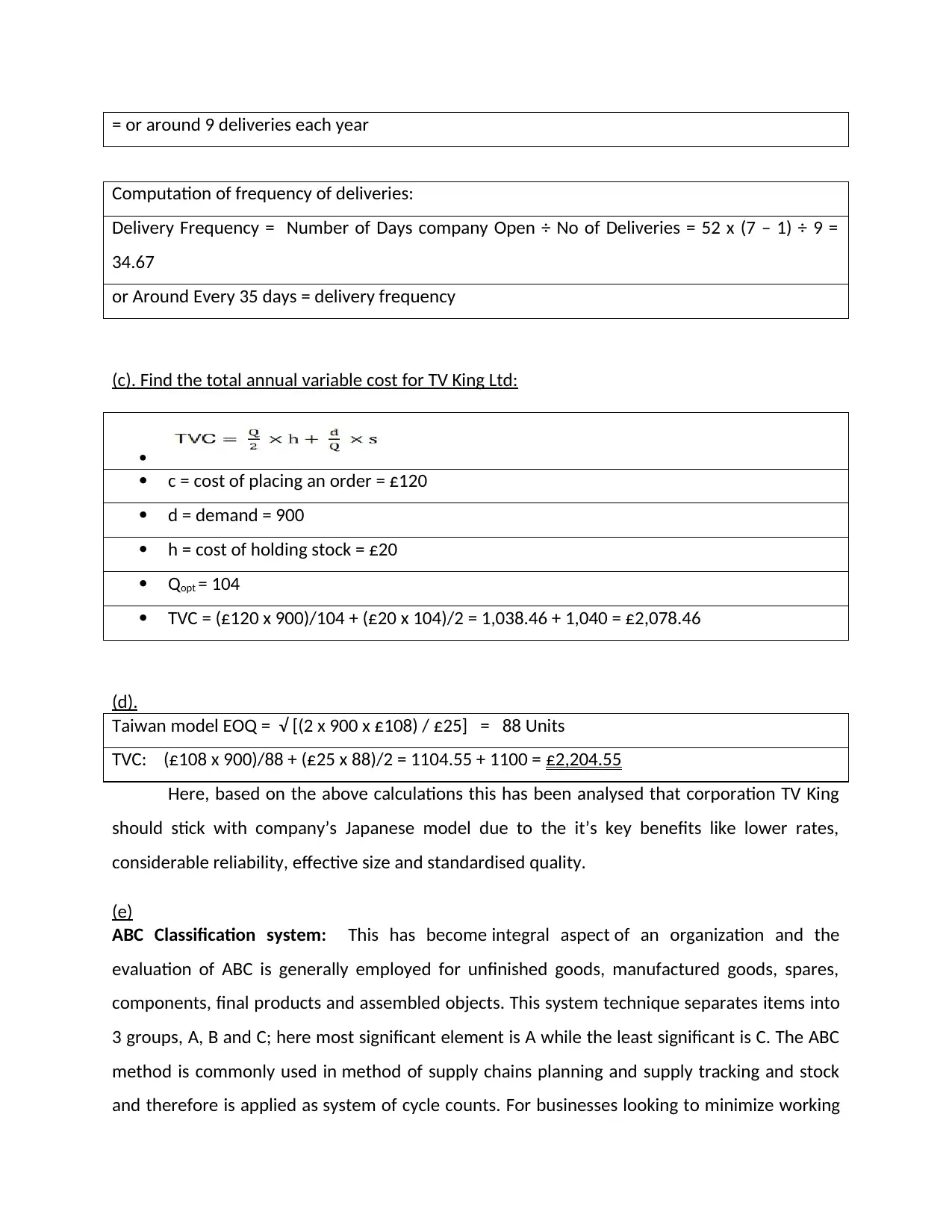

(a). Computation of EOQ (economic-order quantity) with respect to A545 Plasma TV, applying

specific formula:

EOQ = √ [(2*d*s)/h]

“d” denotes to 900 (A545 plasma TVs),

“c” implies to cost of placing an order i.e. £120

“h” refers to cost of holding stock i.e. £20

EOQ = √ [(2 x 900 x £120) / £20] = 104 Units

(b). On the basis of above computed EOQ level assessing how much quantities/deliveries should

be made of A545 Plasma TVs per year:

Number of deliveries of TVs= Annual/yearly Demands ÷ Ordered Quantity

= 900 ÷ 104= 8.65

Business modelling is vital aspect in business which allow managing personnel to effectively

explore complicated choices/alternatives, employing a comprehensive range of assumptions for

representing alternative potential operational business environments. Business modelling

is conceptual framework that promotes the company's sustainability and describes how it

works, makes cash including how it aims to accomplish its objectives. Business modelling

contains all of business processes and practices that business embraces and implements

(Cosenz and Noto, 2018). The study contains three different parts which are mainly focused on

different business modelling aspects. The first part covers inventory related aspects of business

modelling like EOQ, inventory system. Second part comprises non-linear/extremum tasks while

the third part covers creation of decision tree and analysis of decision tree based on a case

study.

MAIN BODY

Part A – INVENTORY

(a). Computation of EOQ (economic-order quantity) with respect to A545 Plasma TV, applying

specific formula:

EOQ = √ [(2*d*s)/h]

“d” denotes to 900 (A545 plasma TVs),

“c” implies to cost of placing an order i.e. £120

“h” refers to cost of holding stock i.e. £20

EOQ = √ [(2 x 900 x £120) / £20] = 104 Units

(b). On the basis of above computed EOQ level assessing how much quantities/deliveries should

be made of A545 Plasma TVs per year:

Number of deliveries of TVs= Annual/yearly Demands ÷ Ordered Quantity

= 900 ÷ 104= 8.65

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= or around 9 deliveries each year

Computation of frequency of deliveries:

Delivery Frequency = Number of Days company Open ÷ No of Deliveries = 52 x (7 – 1) ÷ 9 =

34.67

or Around Every 35 days = delivery frequency

(c). Find the total annual variable cost for TV King Ltd:

c = cost of placing an order = £120

d = demand = 900

h = cost of holding stock = £20

Qopt = 104

TVC = (£120 x 900)/104 + (£20 x 104)/2 = 1,038.46 + 1,040 = £2,078.46

(d).

Taiwan model EOQ = √ [(2 x 900 x £108) / £25] = 88 Units

TVC: (£108 x 900)/88 + (£25 x 88)/2 = 1104.55 + 1100 = £2,204.55

Here, based on the above calculations this has been analysed that corporation TV King

should stick with company’s Japanese model due to the it’s key benefits like lower rates,

considerable reliability, effective size and standardised quality.

(e)

ABC Classification system: This has become integral aspect of an organization and the

evaluation of ABC is generally employed for unfinished goods, manufactured goods, spares,

components, final products and assembled objects. This system technique separates items into

3 groups, A, B and C; here most significant element is A while the least significant is C. The ABC

method is commonly used in method of supply chains planning and supply tracking and stock

and therefore is applied as system of cycle counts. For businesses looking to minimize working

Computation of frequency of deliveries:

Delivery Frequency = Number of Days company Open ÷ No of Deliveries = 52 x (7 – 1) ÷ 9 =

34.67

or Around Every 35 days = delivery frequency

(c). Find the total annual variable cost for TV King Ltd:

c = cost of placing an order = £120

d = demand = 900

h = cost of holding stock = £20

Qopt = 104

TVC = (£120 x 900)/104 + (£20 x 104)/2 = 1,038.46 + 1,040 = £2,078.46

(d).

Taiwan model EOQ = √ [(2 x 900 x £108) / £25] = 88 Units

TVC: (£108 x 900)/88 + (£25 x 88)/2 = 1104.55 + 1100 = £2,204.55

Here, based on the above calculations this has been analysed that corporation TV King

should stick with company’s Japanese model due to the it’s key benefits like lower rates,

considerable reliability, effective size and standardised quality.

(e)

ABC Classification system: This has become integral aspect of an organization and the

evaluation of ABC is generally employed for unfinished goods, manufactured goods, spares,

components, final products and assembled objects. This system technique separates items into

3 groups, A, B and C; here most significant element is A while the least significant is C. The ABC

method is commonly used in method of supply chains planning and supply tracking and stock

and therefore is applied as system of cycle counts. For businesses looking to minimize working

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capital and carrying expenses, this is most essential. This is achieved by reviewing the inventory

which is in surplus inventory as well as those which are outdated by making room for readily

sales made. Instead of keeping it locked up in unsafe stock, this allows to prevent

keeping working capital accessible for use. This allows them to retain control over value

of assets kept at single time if a business is better equipped to monitor the inventory and retain

controlling over high-value products. It also adds order to process of reordering as well as

ensuring that such items are really in inventory to fulfil the requirements. Items falling within

class C are sluggish items which do not need to be re-ordered at same regularity as the items A

or items B (HR and Aithal, 2020). If one brings the products into such three categories,

recognizing the ones that require to be kept and those which could be replaced is useful

for wholesalers as well as distributors. This approach helps corporations retain leverage of

expensive goods that have vast sums of capital investing in them. This offers a means of

keeping control over all inventory for the madness. This not only eliminates excessive payroll

costs, but also ensures that optimal inventory levels are preserved at all stages. The ABC

approach ensures that the inventory turnover rate is sustained at relatively greater level by

systematic inventory management. With this method, storage costs are significantly reduced.

There is arrangement to have adequate stocks in C group to be managed without sacrificing

on more relevant products. Following is categories of items classified under this system:

Item A = Extremely important

Item B = Moderately important

Item C = Relatively unimportant

Item A:

Under ABC system of inventory management and controlling, items grouped under class A are

those items which report maximum values with regard to yearly consumptions. This is

considerable that overall top seventy to eighty percentage of overall annual consumption figure

of corporation generated through just around ten to twenty percentage of aggregate inventory

items. Therefore, this is significant to properly prioritize such items.

Item B:

This includes all items which have mid-range consumption values. These generally equivalent to

which is in surplus inventory as well as those which are outdated by making room for readily

sales made. Instead of keeping it locked up in unsafe stock, this allows to prevent

keeping working capital accessible for use. This allows them to retain control over value

of assets kept at single time if a business is better equipped to monitor the inventory and retain

controlling over high-value products. It also adds order to process of reordering as well as

ensuring that such items are really in inventory to fulfil the requirements. Items falling within

class C are sluggish items which do not need to be re-ordered at same regularity as the items A

or items B (HR and Aithal, 2020). If one brings the products into such three categories,

recognizing the ones that require to be kept and those which could be replaced is useful

for wholesalers as well as distributors. This approach helps corporations retain leverage of

expensive goods that have vast sums of capital investing in them. This offers a means of

keeping control over all inventory for the madness. This not only eliminates excessive payroll

costs, but also ensures that optimal inventory levels are preserved at all stages. The ABC

approach ensures that the inventory turnover rate is sustained at relatively greater level by

systematic inventory management. With this method, storage costs are significantly reduced.

There is arrangement to have adequate stocks in C group to be managed without sacrificing

on more relevant products. Following is categories of items classified under this system:

Item A = Extremely important

Item B = Moderately important

Item C = Relatively unimportant

Item A:

Under ABC system of inventory management and controlling, items grouped under class A are

those items which report maximum values with regard to yearly consumptions. This is

considerable that overall top seventy to eighty percentage of overall annual consumption figure

of corporation generated through just around ten to twenty percentage of aggregate inventory

items. Therefore, this is significant to properly prioritize such items.

Item B:

This includes all items which have mid-range consumption values. These generally equivalent to

around 30 percentage of aggregate stock within corporation that accounts around fifteen to

twenty percentage of overall aggregate yearly consumption values.

Item C:

All items classified under this class bear minimum consumption values as well as account for

around lower than five percentage of total annual consumptions value which implies around

fifty percentage of aggregate stock items.

Note: Here, Yearly consumption value = (Annual demand units) × (item cost per unit)

Buffer/Safety Stock: Safety inventory, commonly alluded to buffer stock,

is surplus/additional inventory which a corporation maintains to ensure that anything does not

running out of inventory One can thought of this as inventory just in scenario. Just in scenario

they running out of items on the shelf, this is additional products held. Many businesses have

been buying small quantities of stock on a daily basis after the introduction of just-in-time stock

systems The premise of just-in-time stock is that businesses should get out of all their storage

centres and only order adequate stock for day or fortnight. Often the inventory is distributed

only as much as few times each day. Just-in-time inventory mechanism will not be used by

many businesses because vendors are not near enough or inventory is hard to deliver. A

protection inventory system is used by these businesses. In this stock method firms purchase

more stocks than they intend to sell. The additional inventory is referred to as their stocks of

protection. This means that during busy seasons/peak time business won't running out of stock.

Buffer inventory is good idea for the satisfaction of clients, although it is risky for the cash flow

of business. Clients are still pleased because famous goods never running out of inventory

(Cosenz and Bivona, 2020).

Pipeline inventory: Pipeline inventory corresponds to stock items which have remained to hit

their ultimate destination in shipping chain of the business. Such items are regarded to be

component of inventory of shipping company through their transit before they have been paid

for by the recipient. When a recipient payment for the objects, furthermore, pipeline inventory

stays on inventory list of a recipient, even though such recipient has still not actually received

them. Before being a final commodity for purchasing by a customer, inventory passes through

twenty percentage of overall aggregate yearly consumption values.

Item C:

All items classified under this class bear minimum consumption values as well as account for

around lower than five percentage of total annual consumptions value which implies around

fifty percentage of aggregate stock items.

Note: Here, Yearly consumption value = (Annual demand units) × (item cost per unit)

Buffer/Safety Stock: Safety inventory, commonly alluded to buffer stock,

is surplus/additional inventory which a corporation maintains to ensure that anything does not

running out of inventory One can thought of this as inventory just in scenario. Just in scenario

they running out of items on the shelf, this is additional products held. Many businesses have

been buying small quantities of stock on a daily basis after the introduction of just-in-time stock

systems The premise of just-in-time stock is that businesses should get out of all their storage

centres and only order adequate stock for day or fortnight. Often the inventory is distributed

only as much as few times each day. Just-in-time inventory mechanism will not be used by

many businesses because vendors are not near enough or inventory is hard to deliver. A

protection inventory system is used by these businesses. In this stock method firms purchase

more stocks than they intend to sell. The additional inventory is referred to as their stocks of

protection. This means that during busy seasons/peak time business won't running out of stock.

Buffer inventory is good idea for the satisfaction of clients, although it is risky for the cash flow

of business. Clients are still pleased because famous goods never running out of inventory

(Cosenz and Bivona, 2020).

Pipeline inventory: Pipeline inventory corresponds to stock items which have remained to hit

their ultimate destination in shipping chain of the business. Such items are regarded to be

component of inventory of shipping company through their transit before they have been paid

for by the recipient. When a recipient payment for the objects, furthermore, pipeline inventory

stays on inventory list of a recipient, even though such recipient has still not actually received

them. Before being a final commodity for purchasing by a customer, inventory passes through

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

several distinct locations. Products could arrive from several different nations-for example, one

portion of product may come through China as well as another portion of same product may

come through US. Therefore, product which is on their way through one position to others as

this is referred to as pipeline inventory as it's heading back to next stop in pipeline. It might be

on way from large distributor to warehouse where the finished product would be converted, or

it might be on way from warehouse to local distributor.

Inventory system:

The inventory system is comprehensive approach to inventory acquisition, storage and

distribution of both raw resources (parts) and final products. In commercial sense inventory

system assures the appropriate stock, at right levels, in right place, at right moment, at right

price and at right costs. As aspect of entire supply chain, inventory system involves factors like

monitoring and managing orders, managing stock storage, tracking the quantity of merchandise

for delivery, and order processing from manufacturers as well as consumers. There is series of

guidelines and measures that decide and monitor volume of stocks when inventory needs to be

refilled, and also the amount of inventories that should actually be bought. The inventory

system applies to procedures involving the procurement, storage and profitability of products

from manufacturer to customer across the supply chain. Which appears straightforward but in

attempt to maintain an organized and efficient stock, there are several important daily

processes. A satisfactory equilibrium between all the shifting parts of the storage device cannot

be achieved. Combating statistics like this requires a well-considered strategy and framework

structure for the inventory system. Depending on the, company the items they produce, the

policies they want to uphold, and the scope of their operation, it will take many procedures and

mechanisms to keep operations running (Kalloniatis, McLennan-Smith and Roberts, 2020).

Part B – NON-LINEAR/EXTREMUM

a) Finding out an equation with respect to profit level of London furniture makers:

Demand = 200-15q

Revenue = 200q - 15q2(demand * q2)

portion of product may come through China as well as another portion of same product may

come through US. Therefore, product which is on their way through one position to others as

this is referred to as pipeline inventory as it's heading back to next stop in pipeline. It might be

on way from large distributor to warehouse where the finished product would be converted, or

it might be on way from warehouse to local distributor.

Inventory system:

The inventory system is comprehensive approach to inventory acquisition, storage and

distribution of both raw resources (parts) and final products. In commercial sense inventory

system assures the appropriate stock, at right levels, in right place, at right moment, at right

price and at right costs. As aspect of entire supply chain, inventory system involves factors like

monitoring and managing orders, managing stock storage, tracking the quantity of merchandise

for delivery, and order processing from manufacturers as well as consumers. There is series of

guidelines and measures that decide and monitor volume of stocks when inventory needs to be

refilled, and also the amount of inventories that should actually be bought. The inventory

system applies to procedures involving the procurement, storage and profitability of products

from manufacturer to customer across the supply chain. Which appears straightforward but in

attempt to maintain an organized and efficient stock, there are several important daily

processes. A satisfactory equilibrium between all the shifting parts of the storage device cannot

be achieved. Combating statistics like this requires a well-considered strategy and framework

structure for the inventory system. Depending on the, company the items they produce, the

policies they want to uphold, and the scope of their operation, it will take many procedures and

mechanisms to keep operations running (Kalloniatis, McLennan-Smith and Roberts, 2020).

Part B – NON-LINEAR/EXTREMUM

a) Finding out an equation with respect to profit level of London furniture makers:

Demand = 200-15q

Revenue = 200q - 15q2(demand * q2)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

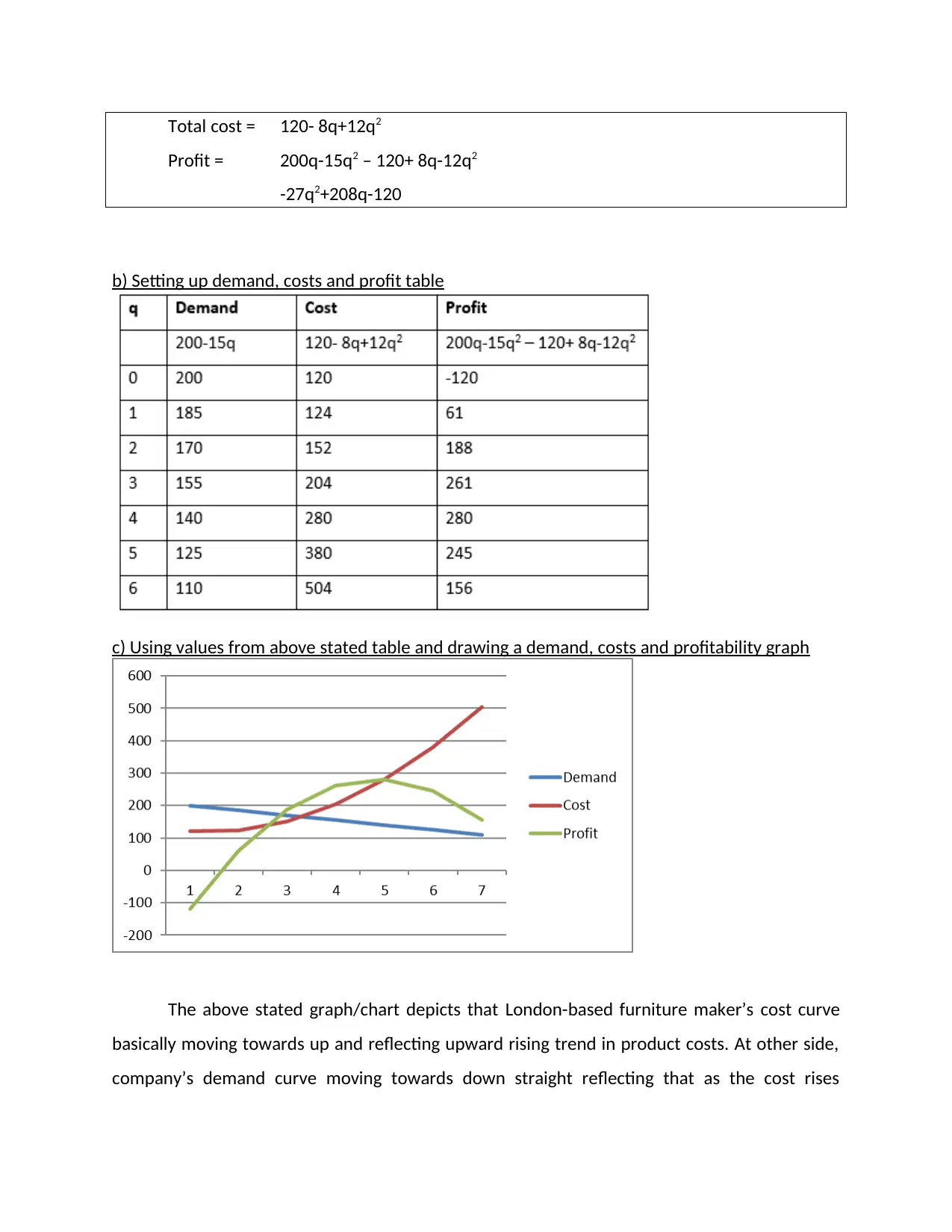

Total cost = 120- 8q+12q2

Profit = 200q-15q2 – 120+ 8q-12q2

-27q2+208q-120

b) Setting up demand, costs and profit table

c) Using values from above stated table and drawing a demand, costs and profitability graph

The above stated graph/chart depicts that London-based furniture maker’s cost curve

basically moving towards up and reflecting upward rising trend in product costs. At other side,

company’s demand curve moving towards down straight reflecting that as the cost rises

Profit = 200q-15q2 – 120+ 8q-12q2

-27q2+208q-120

b) Setting up demand, costs and profit table

c) Using values from above stated table and drawing a demand, costs and profitability graph

The above stated graph/chart depicts that London-based furniture maker’s cost curve

basically moving towards up and reflecting upward rising trend in product costs. At other side,

company’s demand curve moving towards down straight reflecting that as the cost rises

demand for product goes down. Whereas line denoting Profit level goes upward to an extent

then slightly goes downwards which indicates that as the cost rises to 280 profit will decline

along with product demand.

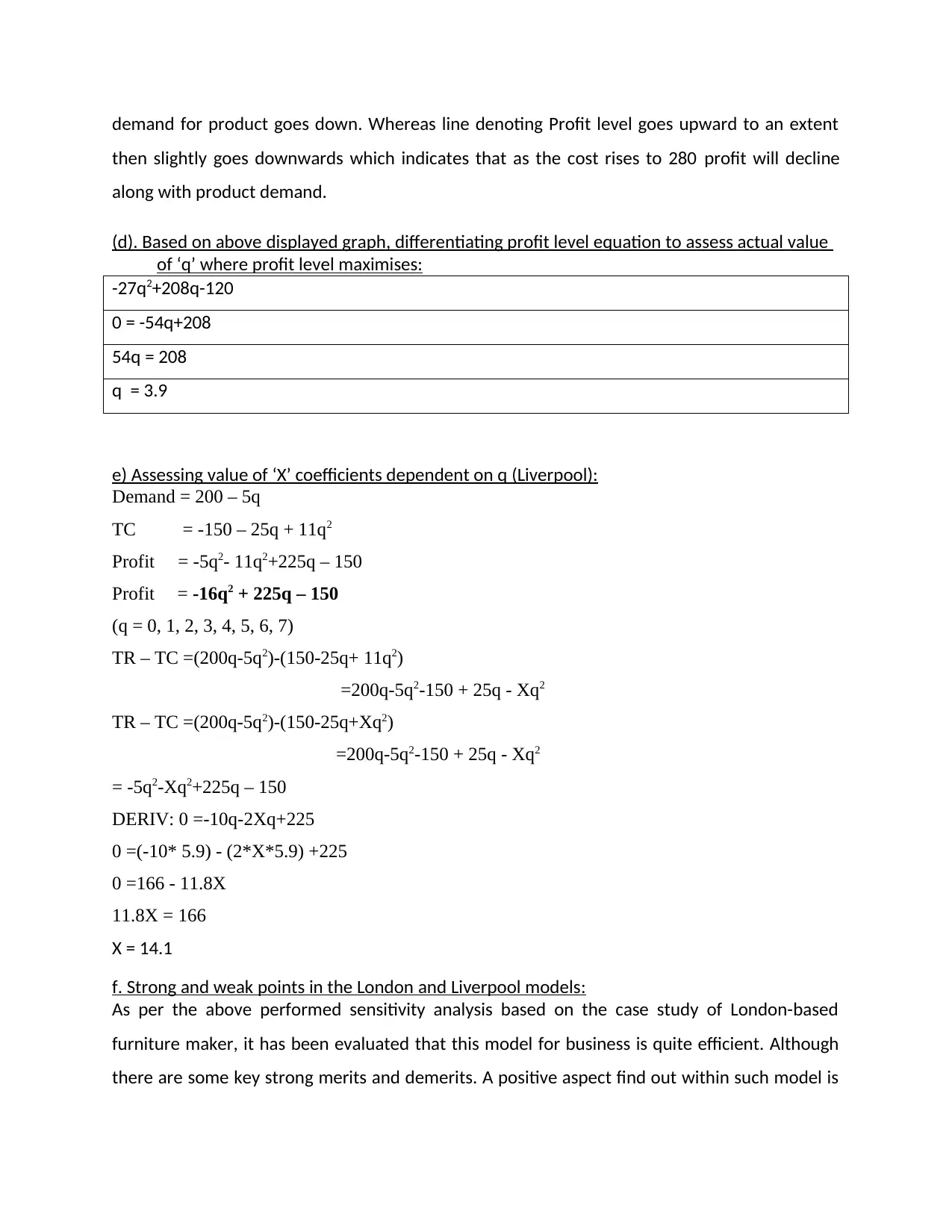

(d). Based on above displayed graph, differentiating profit level equation to assess actual value

of ‘q’ where profit level maximises:

-27q2+208q-120

0 = -54q+208

54q = 208

q = 3.9

e) Assessing value of ‘X’ coefficients dependent on q (Liverpool):

Demand = 200 – 5q

TC = -150 – 25q + 11q2

Profit = -5q2- 11q2+225q – 150

Profit = -16q2 + 225q – 150

(q = 0, 1, 2, 3, 4, 5, 6, 7)

TR – TC =(200q-5q2)-(150-25q+ 11q2)

=200q-5q2-150 + 25q - Xq2

TR – TC =(200q-5q2)-(150-25q+Xq2)

=200q-5q2-150 + 25q - Xq2

= -5q2-Xq2+225q – 150

DERIV: 0 =-10q-2Xq+225

0 =(-10* 5.9) - (2*X*5.9) +225

0 =166 - 11.8X

11.8X = 166

X = 14.1

f. Strong and weak points in the London and Liverpool models:

As per the above performed sensitivity analysis based on the case study of London-based

furniture maker, it has been evaluated that this model for business is quite efficient. Although

there are some key strong merits and demerits. A positive aspect find out within such model is

then slightly goes downwards which indicates that as the cost rises to 280 profit will decline

along with product demand.

(d). Based on above displayed graph, differentiating profit level equation to assess actual value

of ‘q’ where profit level maximises:

-27q2+208q-120

0 = -54q+208

54q = 208

q = 3.9

e) Assessing value of ‘X’ coefficients dependent on q (Liverpool):

Demand = 200 – 5q

TC = -150 – 25q + 11q2

Profit = -5q2- 11q2+225q – 150

Profit = -16q2 + 225q – 150

(q = 0, 1, 2, 3, 4, 5, 6, 7)

TR – TC =(200q-5q2)-(150-25q+ 11q2)

=200q-5q2-150 + 25q - Xq2

TR – TC =(200q-5q2)-(150-25q+Xq2)

=200q-5q2-150 + 25q - Xq2

= -5q2-Xq2+225q – 150

DERIV: 0 =-10q-2Xq+225

0 =(-10* 5.9) - (2*X*5.9) +225

0 =166 - 11.8X

11.8X = 166

X = 14.1

f. Strong and weak points in the London and Liverpool models:

As per the above performed sensitivity analysis based on the case study of London-based

furniture maker, it has been evaluated that this model for business is quite efficient. Although

there are some key strong merits and demerits. A positive aspect find out within such model is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that in business even product demand is overall less but this model enable business to generate

profits. As well as rising costs herein do not directly impact overall profit-level to an extent. On

other hand, demerits of that model is – as demand level increases this model offer decline in

profits and after a certain point even losses.

Moreover, one other demerit of such model asserted is that with decline in overall costs,

business will report decline in overall profit or loss.

Part C – DECISION TREE

SECTION 1

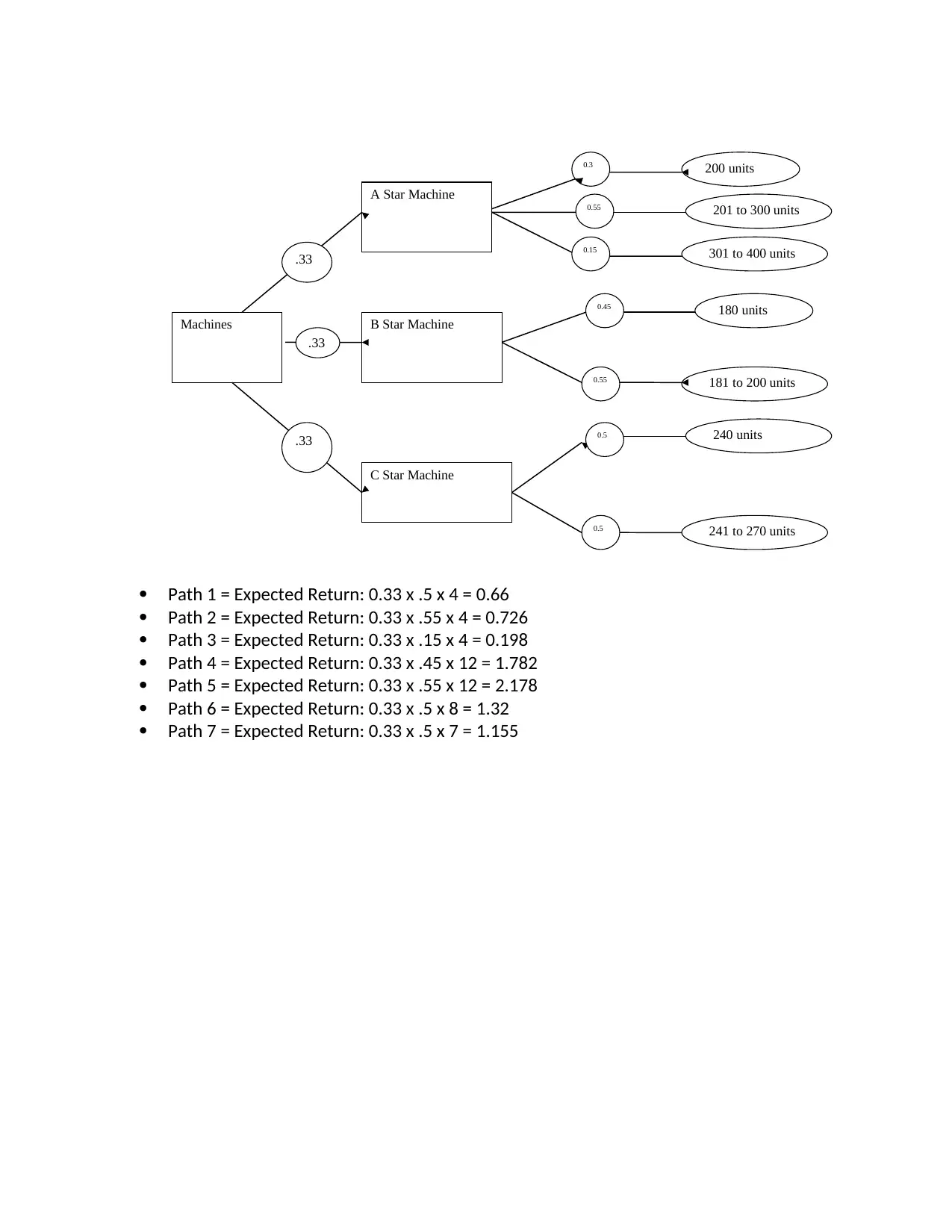

i.

A-Star Machine:

200 units 0.3

Between 201 and 300 0.55

Between 301 and 400 0.15

B-Star Machine:

180 units 0.45

Between 181 and 200 0.55

C-Star Machine:

180 units 0.45

Between 181 and 200 0.55

Decision Tree:

profits. As well as rising costs herein do not directly impact overall profit-level to an extent. On

other hand, demerits of that model is – as demand level increases this model offer decline in

profits and after a certain point even losses.

Moreover, one other demerit of such model asserted is that with decline in overall costs,

business will report decline in overall profit or loss.

Part C – DECISION TREE

SECTION 1

i.

A-Star Machine:

200 units 0.3

Between 201 and 300 0.55

Between 301 and 400 0.15

B-Star Machine:

180 units 0.45

Between 181 and 200 0.55

C-Star Machine:

180 units 0.45

Between 181 and 200 0.55

Decision Tree:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Machines

A Star Machine

B Star Machine

C Star Machine

0.3 200 units

.33

.33

.33

0.55 201 to 300 units

units

0.15 301 to 400 units

0.45

0.55

180 units

181 to 200 units

units

0.5

0.5

240 units

241 to 270 units

Path 1 = Expected Return: 0.33 x .5 x 4 = 0.66

Path 2 = Expected Return: 0.33 x .55 x 4 = 0.726

Path 3 = Expected Return: 0.33 x .15 x 4 = 0.198

Path 4 = Expected Return: 0.33 x .45 x 12 = 1.782

Path 5 = Expected Return: 0.33 x .55 x 12 = 2.178

Path 6 = Expected Return: 0.33 x .5 x 8 = 1.32

Path 7 = Expected Return: 0.33 x .5 x 7 = 1.155

A Star Machine

B Star Machine

C Star Machine

0.3 200 units

.33

.33

.33

0.55 201 to 300 units

units

0.15 301 to 400 units

0.45

0.55

180 units

181 to 200 units

units

0.5

0.5

240 units

241 to 270 units

Path 1 = Expected Return: 0.33 x .5 x 4 = 0.66

Path 2 = Expected Return: 0.33 x .55 x 4 = 0.726

Path 3 = Expected Return: 0.33 x .15 x 4 = 0.198

Path 4 = Expected Return: 0.33 x .45 x 12 = 1.782

Path 5 = Expected Return: 0.33 x .55 x 12 = 2.178

Path 6 = Expected Return: 0.33 x .5 x 8 = 1.32

Path 7 = Expected Return: 0.33 x .5 x 7 = 1.155

ii. Decision Tree:

Machines

A Star

Machine

B Star

Machine

C Star

Machine

0.3 200 units

.33

.33

.33

0.55 201 to 300 units

units

0.15 301 to 400 units

0.45

0.55

180 units

181 to 200 units

units

0.5

0.5

240 units

241 to 270 units

£4

£4

£6.4

£12

£12

£8

£7

£2.4

.7

.3

Path 1 = Expected Return: 0.33 * .5 * 4 = 0.66

Path 2 = Expected Return: 0.33 * .55 * 4 = 0.726

Path 3 = Expected Return: 0.33 * .15 * 6.4 = 0.3168

Path 4 = Expected Return: 0.33 * .15 * 2.4 = 0.1188

Path 5 = Expected Return: 0.33 * .45 * 12 = 1.782

Path 6 = Expected Return: 0.33 * .55 * 12 = 2.178

Path 7 = Expected Return: 0.33 * .5 * 8 = 1.32

Path 8 = Expected Return: 0.33 * .5 * 7 = 1.155

SECTION 2

As per above formulated decision tree as well as the sensitivity analysis based on give case

study, it has been evaluated that in scenario specified in point (i) and its decision tree depicts

most higher expected profit through path 5 which is 2.178 each unit and minimum lowest profit

through path 3 which is 0.198. In different scenario as stated in point (ii), decision tree is

formed by considering additional conditions depicts that there will be total eight paths instead

of 7 paths. All the outcomes would be same as of assessed in point (i) scenario except path 3

and 4 wherein profit would be 0.3168 and 0.1188 respectively.

Machines

A Star

Machine

B Star

Machine

C Star

Machine

0.3 200 units

.33

.33

.33

0.55 201 to 300 units

units

0.15 301 to 400 units

0.45

0.55

180 units

181 to 200 units

units

0.5

0.5

240 units

241 to 270 units

£4

£4

£6.4

£12

£12

£8

£7

£2.4

.7

.3

Path 1 = Expected Return: 0.33 * .5 * 4 = 0.66

Path 2 = Expected Return: 0.33 * .55 * 4 = 0.726

Path 3 = Expected Return: 0.33 * .15 * 6.4 = 0.3168

Path 4 = Expected Return: 0.33 * .15 * 2.4 = 0.1188

Path 5 = Expected Return: 0.33 * .45 * 12 = 1.782

Path 6 = Expected Return: 0.33 * .55 * 12 = 2.178

Path 7 = Expected Return: 0.33 * .5 * 8 = 1.32

Path 8 = Expected Return: 0.33 * .5 * 7 = 1.155

SECTION 2

As per above formulated decision tree as well as the sensitivity analysis based on give case

study, it has been evaluated that in scenario specified in point (i) and its decision tree depicts

most higher expected profit through path 5 which is 2.178 each unit and minimum lowest profit

through path 3 which is 0.198. In different scenario as stated in point (ii), decision tree is

formed by considering additional conditions depicts that there will be total eight paths instead

of 7 paths. All the outcomes would be same as of assessed in point (i) scenario except path 3

and 4 wherein profit would be 0.3168 and 0.1188 respectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.