Business Organization Report

VerifiedAdded on 2019/12/03

|16

|3852

|155

Report

AI Summary

This report analyzes the financial performance of Greggs Plc, a UK bakery chain, and compares it with its competitor, Whitbread Plc. It begins by explaining the purpose of financial statements and the different types prepared by various organizations (sole trader, partnership, public company). A detailed ratio analysis of Greggs Plc's financial statements (2012-2014) is presented, covering profitability, liquidity, efficiency, gearing, and investor ratios. The report interprets these ratios, assessing Greggs's financial health and operational efficiency. A competitor analysis compares Greggs Plc with Whitbread Plc, highlighting key differences in profitability, liquidity, and efficiency. The report concludes with an investment recommendation based on the comparative analysis, suggesting Whitbread Plc as a potentially better investment due to its higher profitability and return on equity. The report includes a table summarizing the key financial ratios for both companies and references the sources used.

Business organization

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................1

TASK 3......................................................................................................................................1

Q. 1. Purpose of financial statements................................................................................1

Q. 2. Different type of organization and their financial statements..................................2

Q.3. Financial statements analysis of Greggs Plc.............................................................3

Q.4. Report........................................................................................................................6

Q. 5. Competitor analysis..................................................................................................7

Q. 6. Conclusion...............................................................................................................8

Q. 7. Presentation..............................................................................................................9

References................................................................................................................................10

INTRODUCTION......................................................................................................................1

TASK 3......................................................................................................................................1

Q. 1. Purpose of financial statements................................................................................1

Q. 2. Different type of organization and their financial statements..................................2

Q.3. Financial statements analysis of Greggs Plc.............................................................3

Q.4. Report........................................................................................................................6

Q. 5. Competitor analysis..................................................................................................7

Q. 6. Conclusion...............................................................................................................8

Q. 7. Presentation..............................................................................................................9

References................................................................................................................................10

INTRODUCTION

Every business prepares its financial accounts in order to identify their financial as

well as operational performance. Different organization prepares distinct type of financial

accounts. In this report we identify the type of financial accounts prepared by the

organizations with their purpose. Moreover, comparative financial statements are also

analysed in context to Greegs Plc. It is the largest bakery chain in the UK established in 1939.

Headquarter of the company is established in Jesmond, Newcastle upon Tyne, United

Kingdom. It produces sandwiches, Pies, pastries and another kind of baked foods for the

consumers. Furthermore, the report discusses the competitor analysis of Greggs Plc with

Whitbread Plc.

TASK 3

Q. 1. Purpose of financial statements

Financial statements: It is prepared to determine the operational and financial results

of every business organizations. It helps to identify the business changes over the years.

Moreover, comparative analysis helps to take effective business decision through mitigate the

negative business impacts.

Accounting terminology: Every transaction has two aspects debit and credit. Debit

transaction indicates the increase in assets and expenses or decrease in liability. However,

credit transaction indicates either increase in liability and income or decrease in assets.

Moreover, balance sheet includes two terminologies that are assets and liability (Taylor,

2010). Assets are such things that are used for future economic benefits to the organization.

However, liabilities are the company's obligation for which payment is required by the

company.

Prime Entry Books: Initially, every business transaction is recorded in books of prime

entry. It is also termed as books of original entry includes sales and purchase book, Return

books, Cash receipts and payment book, petty cash book, bank book and journal.

Accounts and ledgers: Accounts are prepared with debiting and crediting all the

income and expenditures that have taken place in the accounting period. However, ledger is

prepared for all the individual business transaction (Penman and Penman, 2007).

Trial balance: It is prepared to determine the mathematical or arithmetical accuracy

through combining all the ledger account balances. Moreover, it helps in preparing the

business final accounts.

1 | P a g e

Every business prepares its financial accounts in order to identify their financial as

well as operational performance. Different organization prepares distinct type of financial

accounts. In this report we identify the type of financial accounts prepared by the

organizations with their purpose. Moreover, comparative financial statements are also

analysed in context to Greegs Plc. It is the largest bakery chain in the UK established in 1939.

Headquarter of the company is established in Jesmond, Newcastle upon Tyne, United

Kingdom. It produces sandwiches, Pies, pastries and another kind of baked foods for the

consumers. Furthermore, the report discusses the competitor analysis of Greggs Plc with

Whitbread Plc.

TASK 3

Q. 1. Purpose of financial statements

Financial statements: It is prepared to determine the operational and financial results

of every business organizations. It helps to identify the business changes over the years.

Moreover, comparative analysis helps to take effective business decision through mitigate the

negative business impacts.

Accounting terminology: Every transaction has two aspects debit and credit. Debit

transaction indicates the increase in assets and expenses or decrease in liability. However,

credit transaction indicates either increase in liability and income or decrease in assets.

Moreover, balance sheet includes two terminologies that are assets and liability (Taylor,

2010). Assets are such things that are used for future economic benefits to the organization.

However, liabilities are the company's obligation for which payment is required by the

company.

Prime Entry Books: Initially, every business transaction is recorded in books of prime

entry. It is also termed as books of original entry includes sales and purchase book, Return

books, Cash receipts and payment book, petty cash book, bank book and journal.

Accounts and ledgers: Accounts are prepared with debiting and crediting all the

income and expenditures that have taken place in the accounting period. However, ledger is

prepared for all the individual business transaction (Penman and Penman, 2007).

Trial balance: It is prepared to determine the mathematical or arithmetical accuracy

through combining all the ledger account balances. Moreover, it helps in preparing the

business final accounts.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Final accounts: Two statements are prepared as the final accounts of the every

organization that are income statement and balance sheet.

Particulars Purpose

Income statements Trading Account - It is prepared to

determine the amount of gross profit or gross

loss from its trading operations. It is

calculated by subtracting cost of goods sold

from net sales.

Profit and loss Account – It is prepared to

determine the net results through deducting

the gross profit plus indirect incomes to total

indirect expenses.

Balance sheet It is prepared to determine the financial

position of the organization (Benninga,

2008). Business can identify their financial

strengths and weakness through this

statement.

Q. 2. Different type of organization and their financial statements

Greggs Plc: It is a public company hence prepares income statements and balance

sheet as final accounts so as to know their profits and financial status. Moreover, retained

earnings statements, cash flow statement and fund flow statements are also prepared by the

company in order to determine respective changes. It prepares its statements according to the

act requirement. Further, consolidated financial statements are also prepared by the company

through combining all the Subsidiary operations.

Sole trader: In this type of business only a single person establishes the business

organization. Therefore, all the money is invested by themselves and bear all the profits as

well as losses. It prepares its financial statements according to their own requirements. All

trading, profit and loss account and balance sheet is prepared by the entrepreneur (Schroeder,

Clark and Cathey, 2011). The statements help to determine their profits or loss situation.

Income statement: It includes trading and profit and loss account. Trading account is

prepared to ascertain the gross profit or loss. The amount of net profit or net loss is

ascertained through profit and loss account.

2 | P a g e

organization that are income statement and balance sheet.

Particulars Purpose

Income statements Trading Account - It is prepared to

determine the amount of gross profit or gross

loss from its trading operations. It is

calculated by subtracting cost of goods sold

from net sales.

Profit and loss Account – It is prepared to

determine the net results through deducting

the gross profit plus indirect incomes to total

indirect expenses.

Balance sheet It is prepared to determine the financial

position of the organization (Benninga,

2008). Business can identify their financial

strengths and weakness through this

statement.

Q. 2. Different type of organization and their financial statements

Greggs Plc: It is a public company hence prepares income statements and balance

sheet as final accounts so as to know their profits and financial status. Moreover, retained

earnings statements, cash flow statement and fund flow statements are also prepared by the

company in order to determine respective changes. It prepares its statements according to the

act requirement. Further, consolidated financial statements are also prepared by the company

through combining all the Subsidiary operations.

Sole trader: In this type of business only a single person establishes the business

organization. Therefore, all the money is invested by themselves and bear all the profits as

well as losses. It prepares its financial statements according to their own requirements. All

trading, profit and loss account and balance sheet is prepared by the entrepreneur (Schroeder,

Clark and Cathey, 2011). The statements help to determine their profits or loss situation.

Income statement: It includes trading and profit and loss account. Trading account is

prepared to ascertain the gross profit or loss. The amount of net profit or net loss is

ascertained through profit and loss account.

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Balance sheet: It shows the financial growth of the business. Financial status of the

business can be determined through this statement.

The sample statement of all the financial statements is given as under:

Figure 1: Pro-forma of Balance sheet

3 | P a g e

business can be determined through this statement.

The sample statement of all the financial statements is given as under:

Figure 1: Pro-forma of Balance sheet

3 | P a g e

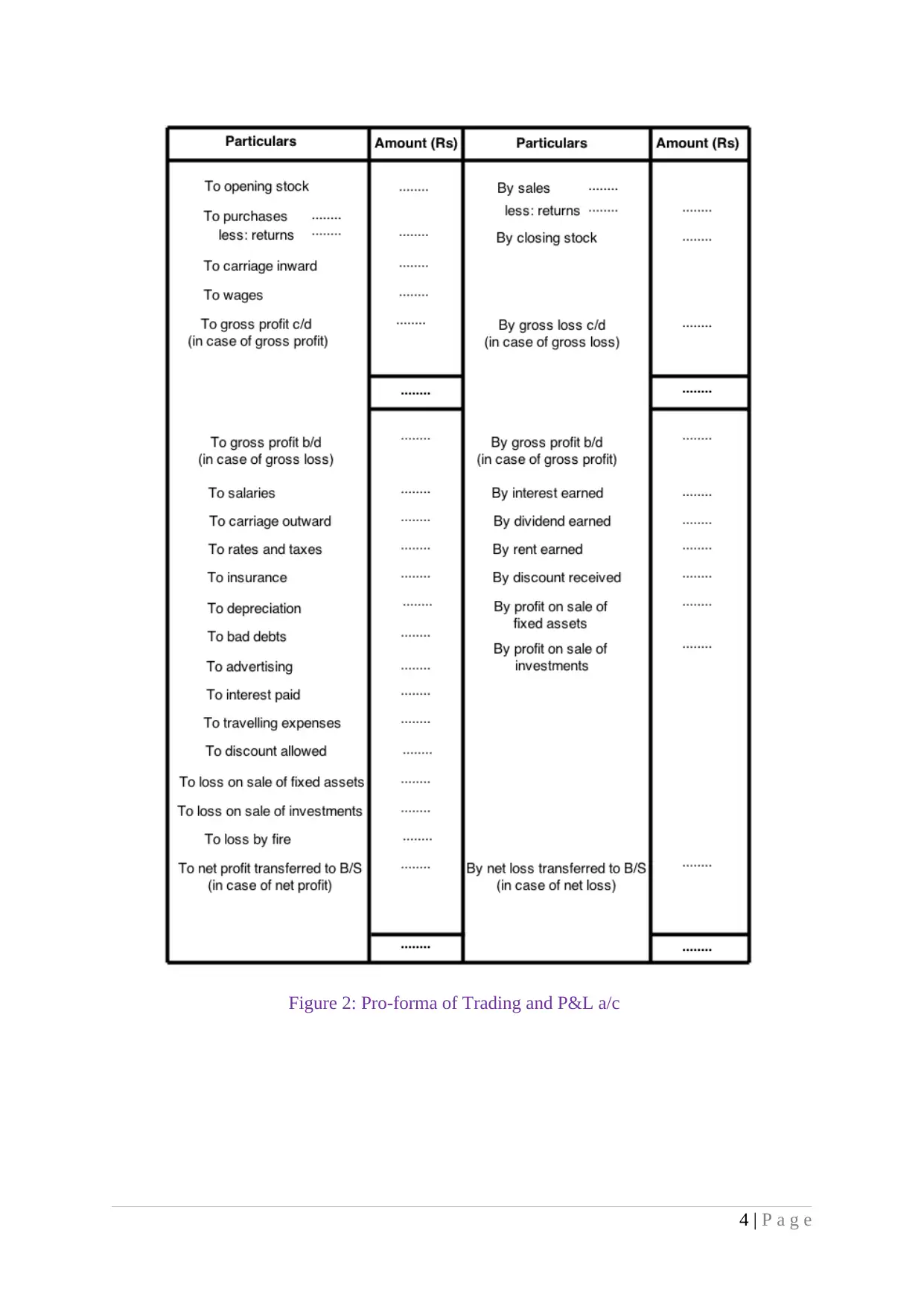

Figure 2: Pro-forma of Trading and P&L a/c

4 | P a g e

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Partnership: Another type of business form is partnership. In this, the business is

established by two or more partners. Therefore, all the partnership business profits and losses

are distributed among the partners. It prepares its financial statements through adopting two

methods include fixed capital method and fluctuating capital method. Under the fixed

method, profit and loss appropriation, partner's capital account and partner's current account

are prepared (Fridson and Alvarez, 2011). However, under the fluctuating capital method

Profit and loss appropriation and partner’s capital account are prepared. Moreover, it prepares

its financial statements according to the partnership act requirements.

Q.3. Financial statements analysis of Greggs Plc

Financial statements of Greegs Plc can be analysed by computing distinct kind of

ratios. Ratio indicates the degree of relations between two variables. As per the scenario,

profitability, liquidity, efficiency, gearing and investor ratio are calculated here for three

years 2012, 2013 and 2014.

Profitability ratio: It measures the business profitability in terms of both gross profit

and net operating profit. Higher the profitability ratio indicates increased business

performance. However, lower the profitability ratio shows worst business performance. It

includes gross profit ratio, operating profit ratio and return on capital employed (Gujarathi,

2008). Gross profit ratio is calculated by dividing the gross margin to the total sales revenue

of the company. However, operating profit margin is computed by dividing business

operational profits to the total sales. On contrary, return on capital employed is calculated by

dividing the business operational profits to the total capital employed.

Liquidity ratio: It is financial ratio that indicates the company's ability to meet its

short term obligations. Further, it measures the business liquid position available for meet

working capital requirements. Higher the ratios indicate higher liquid position and vice versa.

Current ratio and Acid test ratio is computed here for this purpose.

Efficiency ratio: The kind of ratio is efficiency ratio. It indicates the business ability

to use its assets. Efficient and maximum use of assets leads to higher the efficiency ratio and

vice versa (Garrison and et. al., 2010). Receivable days, payable days and inventory days

helps to measure the business efficiency.

Gearing ratio: It determine the capital structure of the company calculated by

dividing noncurrent liability to the total of equity and noncurrent liability of Greggs Plc. It is

a measure of business financial leverage indicates the degree to which firm is using debts and

owner's equity.

5 | P a g e

established by two or more partners. Therefore, all the partnership business profits and losses

are distributed among the partners. It prepares its financial statements through adopting two

methods include fixed capital method and fluctuating capital method. Under the fixed

method, profit and loss appropriation, partner's capital account and partner's current account

are prepared (Fridson and Alvarez, 2011). However, under the fluctuating capital method

Profit and loss appropriation and partner’s capital account are prepared. Moreover, it prepares

its financial statements according to the partnership act requirements.

Q.3. Financial statements analysis of Greggs Plc

Financial statements of Greegs Plc can be analysed by computing distinct kind of

ratios. Ratio indicates the degree of relations between two variables. As per the scenario,

profitability, liquidity, efficiency, gearing and investor ratio are calculated here for three

years 2012, 2013 and 2014.

Profitability ratio: It measures the business profitability in terms of both gross profit

and net operating profit. Higher the profitability ratio indicates increased business

performance. However, lower the profitability ratio shows worst business performance. It

includes gross profit ratio, operating profit ratio and return on capital employed (Gujarathi,

2008). Gross profit ratio is calculated by dividing the gross margin to the total sales revenue

of the company. However, operating profit margin is computed by dividing business

operational profits to the total sales. On contrary, return on capital employed is calculated by

dividing the business operational profits to the total capital employed.

Liquidity ratio: It is financial ratio that indicates the company's ability to meet its

short term obligations. Further, it measures the business liquid position available for meet

working capital requirements. Higher the ratios indicate higher liquid position and vice versa.

Current ratio and Acid test ratio is computed here for this purpose.

Efficiency ratio: The kind of ratio is efficiency ratio. It indicates the business ability

to use its assets. Efficient and maximum use of assets leads to higher the efficiency ratio and

vice versa (Garrison and et. al., 2010). Receivable days, payable days and inventory days

helps to measure the business efficiency.

Gearing ratio: It determine the capital structure of the company calculated by

dividing noncurrent liability to the total of equity and noncurrent liability of Greggs Plc. It is

a measure of business financial leverage indicates the degree to which firm is using debts and

owner's equity.

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Investor ratio: Investor desire maximum return on their invested funds. Therefore, it

is the responsibility of the organization to enhance investor return on a regular basis (Scott,

2014). It includes dividend cover, dividend yield, earning per share and price earnings ratios.

Higher the ratio indicate higher amount of returns for the investors and vice versa.

Table 1: Financial statement of Greggs Plc

Ratio

Formula Year

(2014) Year (2013)

Year

(2012)

Current Assets 101496 64989 63956

Current liability 102119 80716 79415

Stock 15290 15405 17658

Current Ratio

(Current Assets/Current

Liabilities) 0.99:1 0.81:1 0.81:1

Acid Test

(Current assets –

Inventory)/Current Liabilities 0.84:1 0.61:1 0.58:1

Gross profit 488164 454781 448754

Operating profit 49568 33358 52740

Sales 803961 762379 734502

Gross Profit Margin (Gross profit/Revenue)*100 60.72 59.65 61.1

Operating Profit

Margin (Operating profit/Revenue)*100 6.16 4.38 7.18

Equity 246703 236177 226790

Non Current Liability 20114 16960 22152

6 | P a g e

is the responsibility of the organization to enhance investor return on a regular basis (Scott,

2014). It includes dividend cover, dividend yield, earning per share and price earnings ratios.

Higher the ratio indicate higher amount of returns for the investors and vice versa.

Table 1: Financial statement of Greggs Plc

Ratio

Formula Year

(2014) Year (2013)

Year

(2012)

Current Assets 101496 64989 63956

Current liability 102119 80716 79415

Stock 15290 15405 17658

Current Ratio

(Current Assets/Current

Liabilities) 0.99:1 0.81:1 0.81:1

Acid Test

(Current assets –

Inventory)/Current Liabilities 0.84:1 0.61:1 0.58:1

Gross profit 488164 454781 448754

Operating profit 49568 33358 52740

Sales 803961 762379 734502

Gross Profit Margin (Gross profit/Revenue)*100 60.72 59.65 61.1

Operating Profit

Margin (Operating profit/Revenue)*100 6.16 4.38 7.18

Equity 246703 236177 226790

Non Current Liability 20114 16960 22152

6 | P a g e

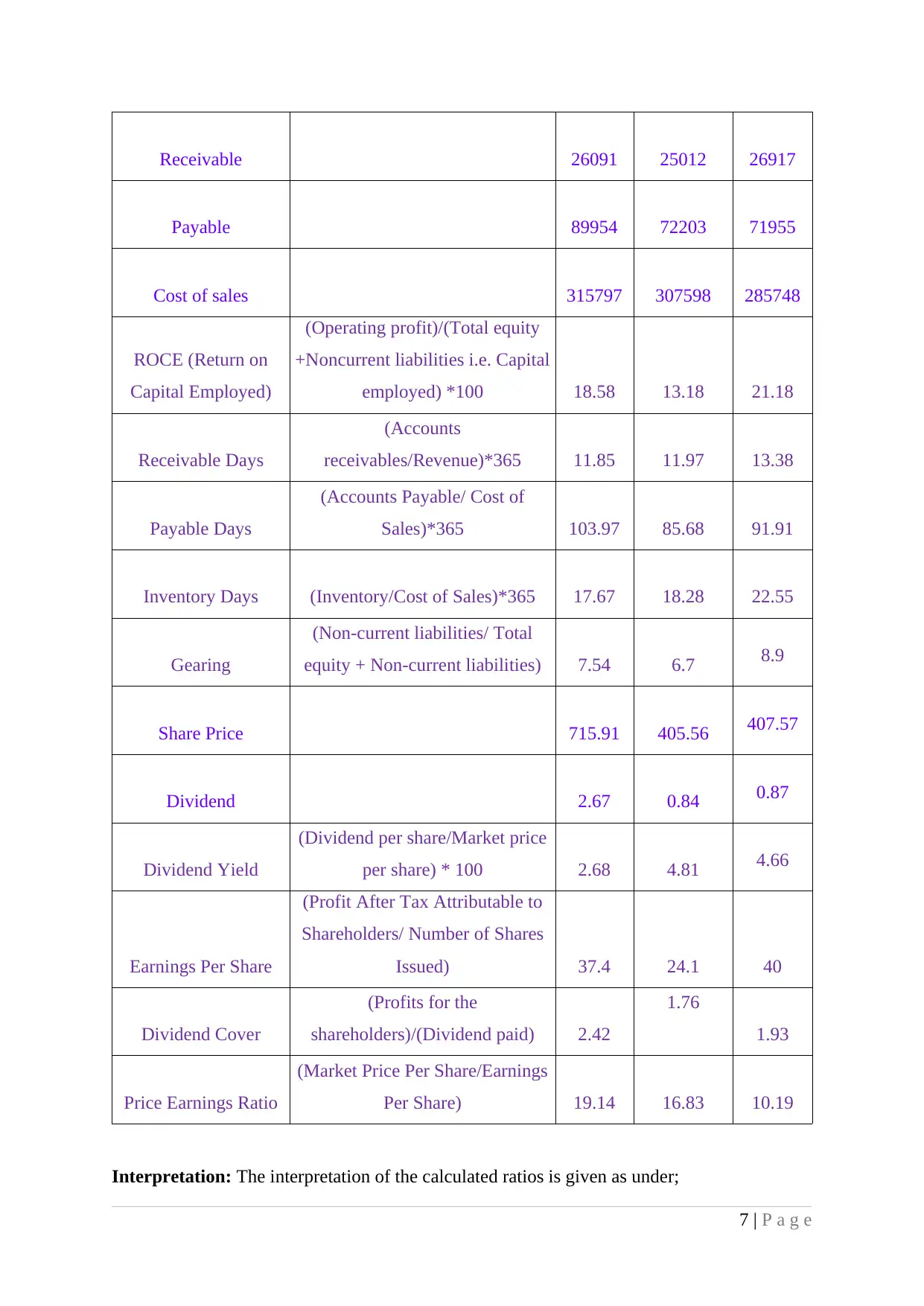

Receivable 26091 25012 26917

Payable 89954 72203 71955

Cost of sales 315797 307598 285748

ROCE (Return on

Capital Employed)

(Operating profit)/(Total equity

+Noncurrent liabilities i.e. Capital

employed) *100 18.58 13.18 21.18

Receivable Days

(Accounts

receivables/Revenue)*365 11.85 11.97 13.38

Payable Days

(Accounts Payable/ Cost of

Sales)*365 103.97 85.68 91.91

Inventory Days (Inventory/Cost of Sales)*365 17.67 18.28 22.55

Gearing

(Non-current liabilities/ Total

equity + Non-current liabilities) 7.54 6.7 8.9

Share Price 715.91 405.56 407.57

Dividend 2.67 0.84 0.87

Dividend Yield

(Dividend per share/Market price

per share) * 100 2.68 4.81 4.66

Earnings Per Share

(Profit After Tax Attributable to

Shareholders/ Number of Shares

Issued) 37.4 24.1 40

Dividend Cover

(Profits for the

shareholders)/(Dividend paid) 2.42

1.76

1.93

Price Earnings Ratio

(Market Price Per Share/Earnings

Per Share) 19.14 16.83 10.19

Interpretation: The interpretation of the calculated ratios is given as under;

7 | P a g e

Payable 89954 72203 71955

Cost of sales 315797 307598 285748

ROCE (Return on

Capital Employed)

(Operating profit)/(Total equity

+Noncurrent liabilities i.e. Capital

employed) *100 18.58 13.18 21.18

Receivable Days

(Accounts

receivables/Revenue)*365 11.85 11.97 13.38

Payable Days

(Accounts Payable/ Cost of

Sales)*365 103.97 85.68 91.91

Inventory Days (Inventory/Cost of Sales)*365 17.67 18.28 22.55

Gearing

(Non-current liabilities/ Total

equity + Non-current liabilities) 7.54 6.7 8.9

Share Price 715.91 405.56 407.57

Dividend 2.67 0.84 0.87

Dividend Yield

(Dividend per share/Market price

per share) * 100 2.68 4.81 4.66

Earnings Per Share

(Profit After Tax Attributable to

Shareholders/ Number of Shares

Issued) 37.4 24.1 40

Dividend Cover

(Profits for the

shareholders)/(Dividend paid) 2.42

1.76

1.93

Price Earnings Ratio

(Market Price Per Share/Earnings

Per Share) 19.14 16.83 10.19

Interpretation: The interpretation of the calculated ratios is given as under;

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

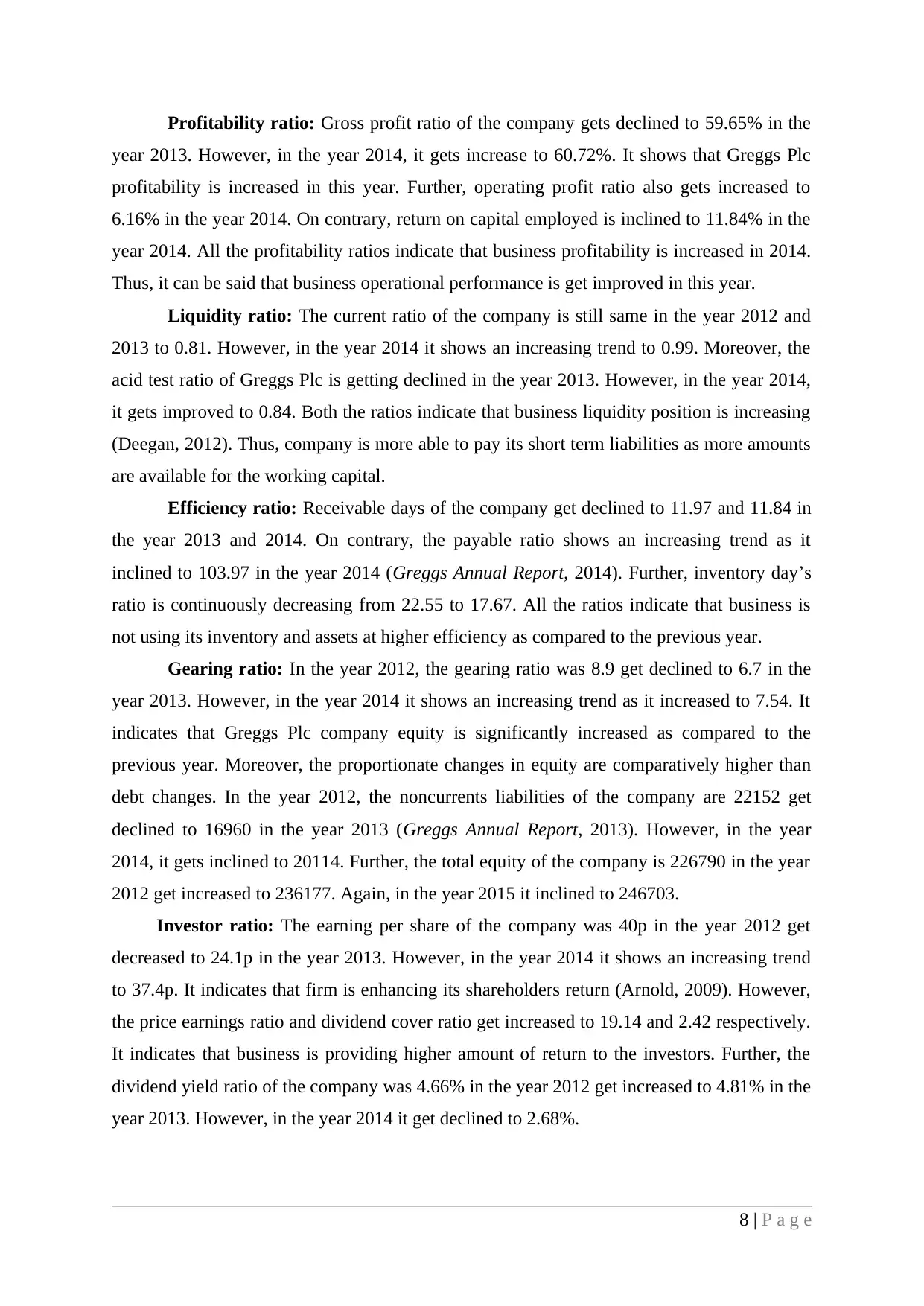

Profitability ratio: Gross profit ratio of the company gets declined to 59.65% in the

year 2013. However, in the year 2014, it gets increase to 60.72%. It shows that Greggs Plc

profitability is increased in this year. Further, operating profit ratio also gets increased to

6.16% in the year 2014. On contrary, return on capital employed is inclined to 11.84% in the

year 2014. All the profitability ratios indicate that business profitability is increased in 2014.

Thus, it can be said that business operational performance is get improved in this year.

Liquidity ratio: The current ratio of the company is still same in the year 2012 and

2013 to 0.81. However, in the year 2014 it shows an increasing trend to 0.99. Moreover, the

acid test ratio of Greggs Plc is getting declined in the year 2013. However, in the year 2014,

it gets improved to 0.84. Both the ratios indicate that business liquidity position is increasing

(Deegan, 2012). Thus, company is more able to pay its short term liabilities as more amounts

are available for the working capital.

Efficiency ratio: Receivable days of the company get declined to 11.97 and 11.84 in

the year 2013 and 2014. On contrary, the payable ratio shows an increasing trend as it

inclined to 103.97 in the year 2014 (Greggs Annual Report, 2014). Further, inventory day’s

ratio is continuously decreasing from 22.55 to 17.67. All the ratios indicate that business is

not using its inventory and assets at higher efficiency as compared to the previous year.

Gearing ratio: In the year 2012, the gearing ratio was 8.9 get declined to 6.7 in the

year 2013. However, in the year 2014 it shows an increasing trend as it increased to 7.54. It

indicates that Greggs Plc company equity is significantly increased as compared to the

previous year. Moreover, the proportionate changes in equity are comparatively higher than

debt changes. In the year 2012, the noncurrents liabilities of the company are 22152 get

declined to 16960 in the year 2013 (Greggs Annual Report, 2013). However, in the year

2014, it gets inclined to 20114. Further, the total equity of the company is 226790 in the year

2012 get increased to 236177. Again, in the year 2015 it inclined to 246703.

Investor ratio: The earning per share of the company was 40p in the year 2012 get

decreased to 24.1p in the year 2013. However, in the year 2014 it shows an increasing trend

to 37.4p. It indicates that firm is enhancing its shareholders return (Arnold, 2009). However,

the price earnings ratio and dividend cover ratio get increased to 19.14 and 2.42 respectively.

It indicates that business is providing higher amount of return to the investors. Further, the

dividend yield ratio of the company was 4.66% in the year 2012 get increased to 4.81% in the

year 2013. However, in the year 2014 it get declined to 2.68%.

8 | P a g e

year 2013. However, in the year 2014, it gets increase to 60.72%. It shows that Greggs Plc

profitability is increased in this year. Further, operating profit ratio also gets increased to

6.16% in the year 2014. On contrary, return on capital employed is inclined to 11.84% in the

year 2014. All the profitability ratios indicate that business profitability is increased in 2014.

Thus, it can be said that business operational performance is get improved in this year.

Liquidity ratio: The current ratio of the company is still same in the year 2012 and

2013 to 0.81. However, in the year 2014 it shows an increasing trend to 0.99. Moreover, the

acid test ratio of Greggs Plc is getting declined in the year 2013. However, in the year 2014,

it gets improved to 0.84. Both the ratios indicate that business liquidity position is increasing

(Deegan, 2012). Thus, company is more able to pay its short term liabilities as more amounts

are available for the working capital.

Efficiency ratio: Receivable days of the company get declined to 11.97 and 11.84 in

the year 2013 and 2014. On contrary, the payable ratio shows an increasing trend as it

inclined to 103.97 in the year 2014 (Greggs Annual Report, 2014). Further, inventory day’s

ratio is continuously decreasing from 22.55 to 17.67. All the ratios indicate that business is

not using its inventory and assets at higher efficiency as compared to the previous year.

Gearing ratio: In the year 2012, the gearing ratio was 8.9 get declined to 6.7 in the

year 2013. However, in the year 2014 it shows an increasing trend as it increased to 7.54. It

indicates that Greggs Plc company equity is significantly increased as compared to the

previous year. Moreover, the proportionate changes in equity are comparatively higher than

debt changes. In the year 2012, the noncurrents liabilities of the company are 22152 get

declined to 16960 in the year 2013 (Greggs Annual Report, 2013). However, in the year

2014, it gets inclined to 20114. Further, the total equity of the company is 226790 in the year

2012 get increased to 236177. Again, in the year 2015 it inclined to 246703.

Investor ratio: The earning per share of the company was 40p in the year 2012 get

decreased to 24.1p in the year 2013. However, in the year 2014 it shows an increasing trend

to 37.4p. It indicates that firm is enhancing its shareholders return (Arnold, 2009). However,

the price earnings ratio and dividend cover ratio get increased to 19.14 and 2.42 respectively.

It indicates that business is providing higher amount of return to the investors. Further, the

dividend yield ratio of the company was 4.66% in the year 2012 get increased to 4.81% in the

year 2013. However, in the year 2014 it get declined to 2.68%.

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

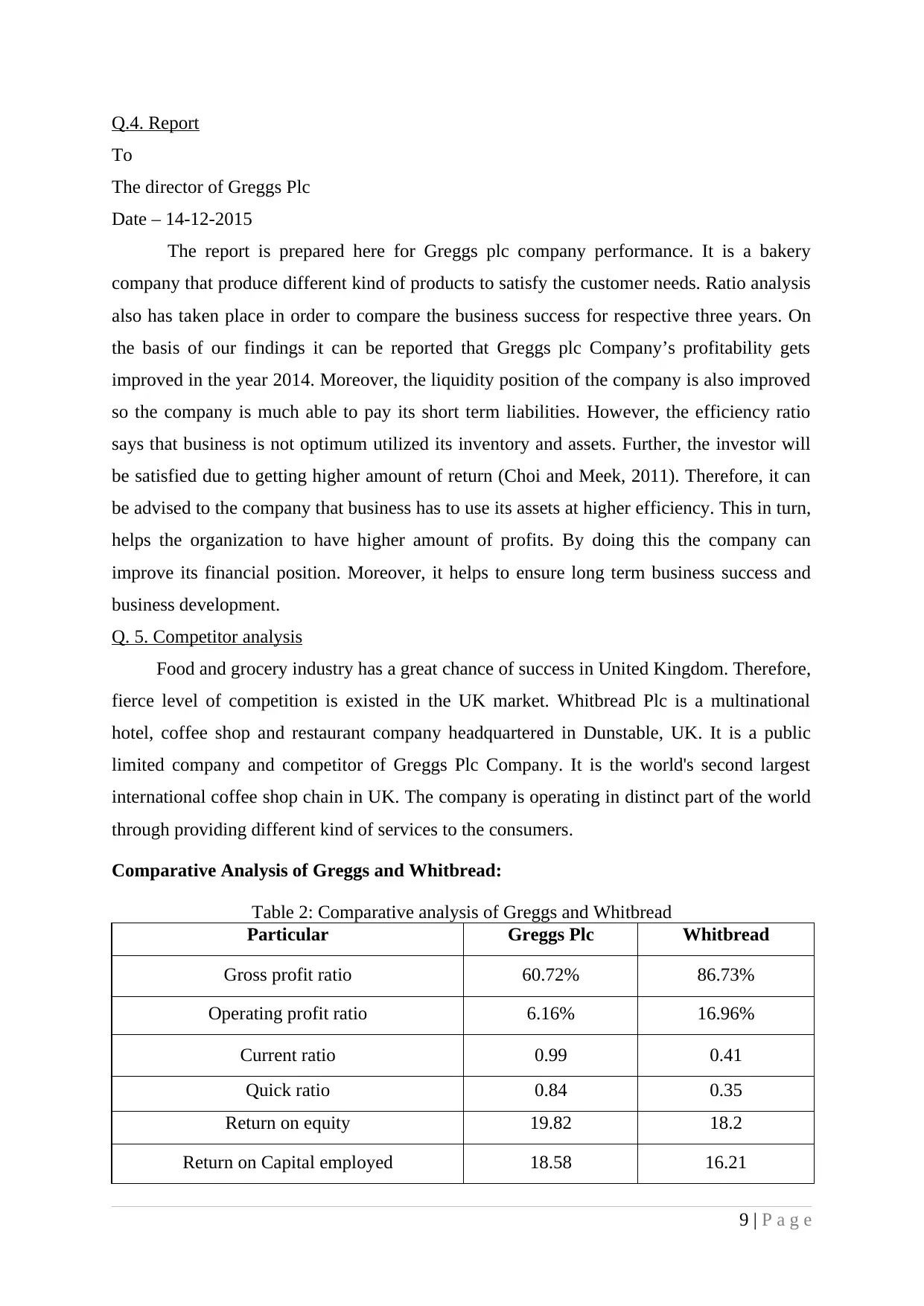

Q.4. Report

To

The director of Greggs Plc

Date – 14-12-2015

The report is prepared here for Greggs plc company performance. It is a bakery

company that produce different kind of products to satisfy the customer needs. Ratio analysis

also has taken place in order to compare the business success for respective three years. On

the basis of our findings it can be reported that Greggs plc Company’s profitability gets

improved in the year 2014. Moreover, the liquidity position of the company is also improved

so the company is much able to pay its short term liabilities. However, the efficiency ratio

says that business is not optimum utilized its inventory and assets. Further, the investor will

be satisfied due to getting higher amount of return (Choi and Meek, 2011). Therefore, it can

be advised to the company that business has to use its assets at higher efficiency. This in turn,

helps the organization to have higher amount of profits. By doing this the company can

improve its financial position. Moreover, it helps to ensure long term business success and

business development.

Q. 5. Competitor analysis

Food and grocery industry has a great chance of success in United Kingdom. Therefore,

fierce level of competition is existed in the UK market. Whitbread Plc is a multinational

hotel, coffee shop and restaurant company headquartered in Dunstable, UK. It is a public

limited company and competitor of Greggs Plc Company. It is the world's second largest

international coffee shop chain in UK. The company is operating in distinct part of the world

through providing different kind of services to the consumers.

Comparative Analysis of Greggs and Whitbread:

Table 2: Comparative analysis of Greggs and Whitbread

Particular Greggs Plc Whitbread

Gross profit ratio 60.72% 86.73%

Operating profit ratio 6.16% 16.96%

Current ratio 0.99 0.41

Quick ratio 0.84 0.35

Return on equity 19.82 18.2

Return on Capital employed 18.58 16.21

9 | P a g e

To

The director of Greggs Plc

Date – 14-12-2015

The report is prepared here for Greggs plc company performance. It is a bakery

company that produce different kind of products to satisfy the customer needs. Ratio analysis

also has taken place in order to compare the business success for respective three years. On

the basis of our findings it can be reported that Greggs plc Company’s profitability gets

improved in the year 2014. Moreover, the liquidity position of the company is also improved

so the company is much able to pay its short term liabilities. However, the efficiency ratio

says that business is not optimum utilized its inventory and assets. Further, the investor will

be satisfied due to getting higher amount of return (Choi and Meek, 2011). Therefore, it can

be advised to the company that business has to use its assets at higher efficiency. This in turn,

helps the organization to have higher amount of profits. By doing this the company can

improve its financial position. Moreover, it helps to ensure long term business success and

business development.

Q. 5. Competitor analysis

Food and grocery industry has a great chance of success in United Kingdom. Therefore,

fierce level of competition is existed in the UK market. Whitbread Plc is a multinational

hotel, coffee shop and restaurant company headquartered in Dunstable, UK. It is a public

limited company and competitor of Greggs Plc Company. It is the world's second largest

international coffee shop chain in UK. The company is operating in distinct part of the world

through providing different kind of services to the consumers.

Comparative Analysis of Greggs and Whitbread:

Table 2: Comparative analysis of Greggs and Whitbread

Particular Greggs Plc Whitbread

Gross profit ratio 60.72% 86.73%

Operating profit ratio 6.16% 16.96%

Current ratio 0.99 0.41

Quick ratio 0.84 0.35

Return on equity 19.82 18.2

Return on Capital employed 18.58 16.21

9 | P a g e

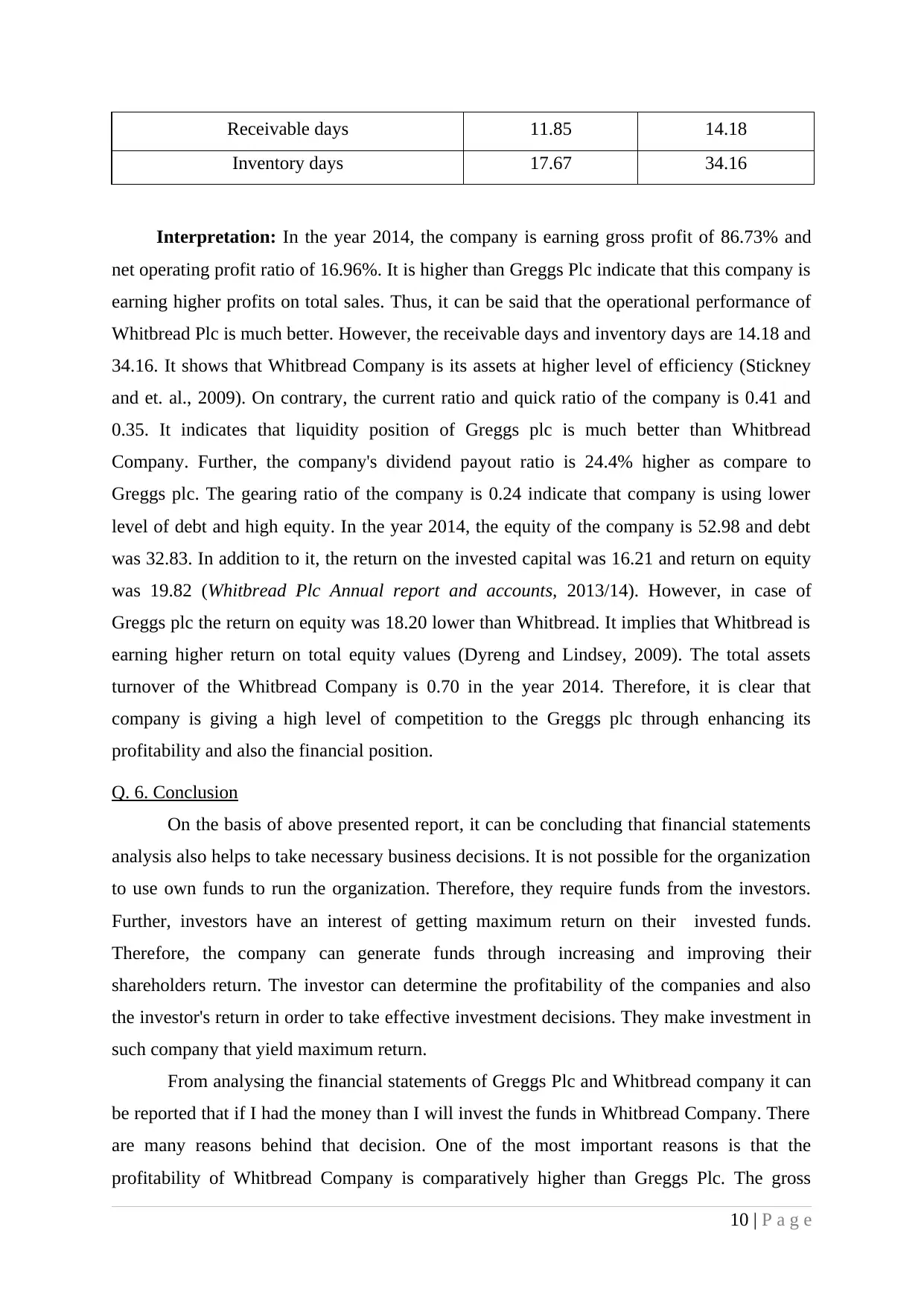

Receivable days 11.85 14.18

Inventory days 17.67 34.16

Interpretation: In the year 2014, the company is earning gross profit of 86.73% and

net operating profit ratio of 16.96%. It is higher than Greggs Plc indicate that this company is

earning higher profits on total sales. Thus, it can be said that the operational performance of

Whitbread Plc is much better. However, the receivable days and inventory days are 14.18 and

34.16. It shows that Whitbread Company is its assets at higher level of efficiency (Stickney

and et. al., 2009). On contrary, the current ratio and quick ratio of the company is 0.41 and

0.35. It indicates that liquidity position of Greggs plc is much better than Whitbread

Company. Further, the company's dividend payout ratio is 24.4% higher as compare to

Greggs plc. The gearing ratio of the company is 0.24 indicate that company is using lower

level of debt and high equity. In the year 2014, the equity of the company is 52.98 and debt

was 32.83. In addition to it, the return on the invested capital was 16.21 and return on equity

was 19.82 (Whitbread Plc Annual report and accounts, 2013/14). However, in case of

Greggs plc the return on equity was 18.20 lower than Whitbread. It implies that Whitbread is

earning higher return on total equity values (Dyreng and Lindsey, 2009). The total assets

turnover of the Whitbread Company is 0.70 in the year 2014. Therefore, it is clear that

company is giving a high level of competition to the Greggs plc through enhancing its

profitability and also the financial position.

Q. 6. Conclusion

On the basis of above presented report, it can be concluding that financial statements

analysis also helps to take necessary business decisions. It is not possible for the organization

to use own funds to run the organization. Therefore, they require funds from the investors.

Further, investors have an interest of getting maximum return on their invested funds.

Therefore, the company can generate funds through increasing and improving their

shareholders return. The investor can determine the profitability of the companies and also

the investor's return in order to take effective investment decisions. They make investment in

such company that yield maximum return.

From analysing the financial statements of Greggs Plc and Whitbread company it can

be reported that if I had the money than I will invest the funds in Whitbread Company. There

are many reasons behind that decision. One of the most important reasons is that the

profitability of Whitbread Company is comparatively higher than Greggs Plc. The gross

10 | P a g e

Inventory days 17.67 34.16

Interpretation: In the year 2014, the company is earning gross profit of 86.73% and

net operating profit ratio of 16.96%. It is higher than Greggs Plc indicate that this company is

earning higher profits on total sales. Thus, it can be said that the operational performance of

Whitbread Plc is much better. However, the receivable days and inventory days are 14.18 and

34.16. It shows that Whitbread Company is its assets at higher level of efficiency (Stickney

and et. al., 2009). On contrary, the current ratio and quick ratio of the company is 0.41 and

0.35. It indicates that liquidity position of Greggs plc is much better than Whitbread

Company. Further, the company's dividend payout ratio is 24.4% higher as compare to

Greggs plc. The gearing ratio of the company is 0.24 indicate that company is using lower

level of debt and high equity. In the year 2014, the equity of the company is 52.98 and debt

was 32.83. In addition to it, the return on the invested capital was 16.21 and return on equity

was 19.82 (Whitbread Plc Annual report and accounts, 2013/14). However, in case of

Greggs plc the return on equity was 18.20 lower than Whitbread. It implies that Whitbread is

earning higher return on total equity values (Dyreng and Lindsey, 2009). The total assets

turnover of the Whitbread Company is 0.70 in the year 2014. Therefore, it is clear that

company is giving a high level of competition to the Greggs plc through enhancing its

profitability and also the financial position.

Q. 6. Conclusion

On the basis of above presented report, it can be concluding that financial statements

analysis also helps to take necessary business decisions. It is not possible for the organization

to use own funds to run the organization. Therefore, they require funds from the investors.

Further, investors have an interest of getting maximum return on their invested funds.

Therefore, the company can generate funds through increasing and improving their

shareholders return. The investor can determine the profitability of the companies and also

the investor's return in order to take effective investment decisions. They make investment in

such company that yield maximum return.

From analysing the financial statements of Greggs Plc and Whitbread company it can

be reported that if I had the money than I will invest the funds in Whitbread Company. There

are many reasons behind that decision. One of the most important reasons is that the

profitability of Whitbread Company is comparatively higher than Greggs Plc. The gross

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.