Finance Report: Business Organizations, Accounting, and Statements

VerifiedAdded on 2023/01/18

|16

|3785

|66

Report

AI Summary

This finance report provides a comprehensive overview of business organizations, accounting, and financial statements. It begins with an introduction to various business structures, including sole proprietorships, partnerships, and corporations, detailing their advantages and disadvantages. The report then delves into the importance of accounting information for different users, both internal and external, and the role of financial statements in assessing business performance. Subsequent sections cover journal entries, ledgers, trial balances, and the preparation of financial statements, including income statements and statements of financial position. The report emphasizes the significance of accounting frameworks in ensuring uniformity and comparability across different organizations. The report is designed to provide a solid foundation in financial reporting and analysis.

FINANCE PORTFOLIO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

A) Different types of business organisations with their advantages and disadvantages..............1

B) Main users of accounting information and its importance to different users.........................5

PART 2............................................................................................................................................7

Journal Entries.............................................................................................................................7

PART 3............................................................................................................................................9

A) Journals ..................................................................................................................................9

B) ledgers and Trial Balance......................................................................................................10

PART 4..........................................................................................................................................12

a) Income Statement of S Keyes for year ending 30th September 2019...................................12

b) Statement of Financial Position as at 30th September 2019. ...............................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

A) Different types of business organisations with their advantages and disadvantages..............1

B) Main users of accounting information and its importance to different users.........................5

PART 2............................................................................................................................................7

Journal Entries.............................................................................................................................7

PART 3............................................................................................................................................9

A) Journals ..................................................................................................................................9

B) ledgers and Trial Balance......................................................................................................10

PART 4..........................................................................................................................................12

a) Income Statement of S Keyes for year ending 30th September 2019...................................12

b) Statement of Financial Position as at 30th September 2019. ...............................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

The business operates at multiples levels. In the diversified market there are different

forms of business organisation that could be established depending on the needs and

requirements. There are different advantages and disadvantages associated with every types of

organisation. The forms of business organisation are sole trader, partnership and corporations.

These organisations are established complying with separated legal requirements. These

organisations have to prepare accounting records as per the applicable framework. Financial

statements are necessary for organisations to be prepared as they help the executives of the

business to review their performance. It helps them to make changes in their policies and

procedures for increasing the efficiency of business (Aljuwaiber, 2016). The type of business

organisation that is adopted will be influencing multiple factors that will decide about future of

company. There are several factors like tax liability, legal liability, establishment cost and the

operational costs that vary with the type of organisation. The report will cover give

understanding about different types of business organisations that can be established. It will also

reveal about the importance of financial information to users.

PART 1

A) Different types of business organisations with their advantages and disadvantages.

As an business owner first decision is about the structure of business organisation. Before

making any decision one should know about the advantages and disadvantages of every kind of

business. Legal configurations should be adopted by the business defining the right and

obligation related to the participants in control, ownership, legal liability, personal liability and

lifespan. Business types determines the income tax return to be filed and liabilities of owner and

company. When forming business following factors should be accounted for like nature and size

of business organisations , control level in organisation, structure, vulnerability of legal lawsuits,

tax implications and profit or loss (Dash, Satpathy and Dash, 2018). Types of business

organisation that are mostly incorporated are :

Sole Proprietorship

This is the mostly accepted business type. Business of sole proprietor is owned by single

owner. Business of sole proprietor is usually established for the benefit of the owner. It is

established by single person for becoming the sole owner of firm. Existence of business is

entirely dependent upon decisions taken by the owner. The sole right of taking decisions rests

1

The business operates at multiples levels. In the diversified market there are different

forms of business organisation that could be established depending on the needs and

requirements. There are different advantages and disadvantages associated with every types of

organisation. The forms of business organisation are sole trader, partnership and corporations.

These organisations are established complying with separated legal requirements. These

organisations have to prepare accounting records as per the applicable framework. Financial

statements are necessary for organisations to be prepared as they help the executives of the

business to review their performance. It helps them to make changes in their policies and

procedures for increasing the efficiency of business (Aljuwaiber, 2016). The type of business

organisation that is adopted will be influencing multiple factors that will decide about future of

company. There are several factors like tax liability, legal liability, establishment cost and the

operational costs that vary with the type of organisation. The report will cover give

understanding about different types of business organisations that can be established. It will also

reveal about the importance of financial information to users.

PART 1

A) Different types of business organisations with their advantages and disadvantages.

As an business owner first decision is about the structure of business organisation. Before

making any decision one should know about the advantages and disadvantages of every kind of

business. Legal configurations should be adopted by the business defining the right and

obligation related to the participants in control, ownership, legal liability, personal liability and

lifespan. Business types determines the income tax return to be filed and liabilities of owner and

company. When forming business following factors should be accounted for like nature and size

of business organisations , control level in organisation, structure, vulnerability of legal lawsuits,

tax implications and profit or loss (Dash, Satpathy and Dash, 2018). Types of business

organisation that are mostly incorporated are :

Sole Proprietorship

This is the mostly accepted business type. Business of sole proprietor is owned by single

owner. Business of sole proprietor is usually established for the benefit of the owner. It is

established by single person for becoming the sole owner of firm. Existence of business is

entirely dependent upon decisions taken by the owner. The sole right of taking decisions rests

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with the owner of business. Sole proprietor have the responsibility of running business on day to

day basis. There are large number of sole proprietary firms but in aggregate are accounting for

very small business receipts (Johanson and Vakkuri, 2017). Example of sole proprietors are

freelancers, independent contractors or photographers.

Advantages

Sole proprietor business is easy to form. Establishment of business is very simple like

printing business cards. Also the dissolution of business is an easy process it does not

involve lengthy legal requirements. It is least expensive business form that can be

established.

In this type of business start up costs are very low and also the operational cost are low as

they generally operate on small scale.

This type of business organisation do not have to follow and comply with major legal

requirements and regulations.

Owner of the business receives all the profits. They are not required to share the profits

with others.

Owners have the complete control over the company and have the sole authority of taking

decisions. They are not required to corporate income tax return. Income realized by the business of

sole proprietor are declared on the income tax return of the individual.

Disadvantages

Owner of the business has an unlimited liability. They are all liable personally for all the

business obligations inclusive of employee's action related to business functions.

Sole proprietary firms have limited life, business generally dies with the death of owner.

Raising funds for the business is difficult task, only limited loans can be raised.

A sole proprietary firm has no separate legal status.

Partnership

In a partnership business ownership is shared between more than two individuals.

Partnerships can be small as well big like accounting firms having dozens of business partners.

The partnership firm like sole proprietor is not differentiated from it owners. Partnership are

established on agreements between the partners. These agreements could be oral or written.

2

day basis. There are large number of sole proprietary firms but in aggregate are accounting for

very small business receipts (Johanson and Vakkuri, 2017). Example of sole proprietors are

freelancers, independent contractors or photographers.

Advantages

Sole proprietor business is easy to form. Establishment of business is very simple like

printing business cards. Also the dissolution of business is an easy process it does not

involve lengthy legal requirements. It is least expensive business form that can be

established.

In this type of business start up costs are very low and also the operational cost are low as

they generally operate on small scale.

This type of business organisation do not have to follow and comply with major legal

requirements and regulations.

Owner of the business receives all the profits. They are not required to share the profits

with others.

Owners have the complete control over the company and have the sole authority of taking

decisions. They are not required to corporate income tax return. Income realized by the business of

sole proprietor are declared on the income tax return of the individual.

Disadvantages

Owner of the business has an unlimited liability. They are all liable personally for all the

business obligations inclusive of employee's action related to business functions.

Sole proprietary firms have limited life, business generally dies with the death of owner.

Raising funds for the business is difficult task, only limited loans can be raised.

A sole proprietary firm has no separate legal status.

Partnership

In a partnership business ownership is shared between more than two individuals.

Partnerships can be small as well big like accounting firms having dozens of business partners.

The partnership firm like sole proprietor is not differentiated from it owners. Partnership are

established on agreements between the partners. These agreements could be oral or written.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Partnership firms are required to be registered under Partnership Act. Legal agreements about the

partnership are generally based on decision-making structures, sharing of profits, resolution of

disputes, admission of partners and action procedures on dissolution. It is essential for

partnerships to have the agreements before the establishment so that they do not face conflicts at

later stage.

There are two types of partnership firms that are general & limited. In general form of

partnership investment in business is made by all the partners and these partners are responsible

for all the debts of business (Mbuga, 2015). Formal agreements are not required in this kind of

partnership, agreements could be verbal or implied among the business partners. On the other

hand limited partnership are required to have formal agreements among the partners. Certificate

of partnership is to be obtained by firm. In this form business partners are allowed to limit their

liability in agreed proportion of ownership.

Advantages

Business potential is raised by combining the strengths of individual partners. All the

partners share the resources for business that increases the capital of firm.

Partnership firms are easy to establish, are flexible and do not have much regulatory

compliances. Attention is only paid while making agreements.

Profits are shared among the partners based on the agreements entered into by partners.

There is an increased access over the resources that could be used for business.

Partnership firms have separate legal status that gives protection in the event of liability.

They are not liable for any corporate income taxes. Income is declared by filing tax return

of partnership firms but the partners have to declare their proportion of income in

individual tax returns. Partnership firms are not expensive to establish whether limited or general.

Disadvantages

Partners are personally liable for all the business obligations to an unlimited level. It

creates personal risk over the partners for the business debts.

Decision-making process may not be effective as views of partners may differ depending

on the individual perspectives to the point.

In absence of partnership agreements conflicts may arise among the partners.

A wrong action of single partner can make liable all the partners of the firm.

3

partnership are generally based on decision-making structures, sharing of profits, resolution of

disputes, admission of partners and action procedures on dissolution. It is essential for

partnerships to have the agreements before the establishment so that they do not face conflicts at

later stage.

There are two types of partnership firms that are general & limited. In general form of

partnership investment in business is made by all the partners and these partners are responsible

for all the debts of business (Mbuga, 2015). Formal agreements are not required in this kind of

partnership, agreements could be verbal or implied among the business partners. On the other

hand limited partnership are required to have formal agreements among the partners. Certificate

of partnership is to be obtained by firm. In this form business partners are allowed to limit their

liability in agreed proportion of ownership.

Advantages

Business potential is raised by combining the strengths of individual partners. All the

partners share the resources for business that increases the capital of firm.

Partnership firms are easy to establish, are flexible and do not have much regulatory

compliances. Attention is only paid while making agreements.

Profits are shared among the partners based on the agreements entered into by partners.

There is an increased access over the resources that could be used for business.

Partnership firms have separate legal status that gives protection in the event of liability.

They are not liable for any corporate income taxes. Income is declared by filing tax return

of partnership firms but the partners have to declare their proportion of income in

individual tax returns. Partnership firms are not expensive to establish whether limited or general.

Disadvantages

Partners are personally liable for all the business obligations to an unlimited level. It

creates personal risk over the partners for the business debts.

Decision-making process may not be effective as views of partners may differ depending

on the individual perspectives to the point.

In absence of partnership agreements conflicts may arise among the partners.

A wrong action of single partner can make liable all the partners of the firm.

3

Dissolution of partnership and distribution of the assets and liabilities is complex process.

Corporation

Corporations are established as separate legal enterprise from that of its owners. A

corporation is considered as separate legal person for the tax purposes. Corporation has all the

power that rests with an individual. A corporation can be sued, taxes and also it can enter

contractual agreements in it own name. Corporation can have its own bank account, can raise

loan on its own and can sue or be sued in its own name (Borkowski, 2016.). A corporation is

born by law and dies by law. Corporation do not dies with the death of owners. Income

generated by the business belongs to company as its personal income.

Income is taxed as personal income of the company. Corporation can be private as well

as public. Legal requirement related to both the organisations differ from each other. Private

organisations are not large as public organisations. Shareholders are the owners of the

corporations. All the activities and procedures of corporations have to comply with the rules and

regulations under the law. Legislations are established for guiding and monitoring the

corporations over all the business affairs. Single person or director cannot take the decisions of

business. Decisions of the businesses are taken by conducting board meeting and general

meetings. Profits after transferring certain amount in reserves are distributed among the

shareholders of company. Establishment of corporation is an expensive process and require lot of

legal requirements to be followed (Business Organisations. 2019).

Advantages

A corporation has an unlimited commercial life. Corporation do not dissolves with the

death of owner but remains in existence it is dissolved by law.

Corporations can raise funds for the business from public by issuing different securities.

Companies can be listed on the stock exchange.

Ownership of corporations is transferable and can be transferred number of times by

selling the shares.

Biggest advantage of establishing corporation is limited liability of feature. The liability

of the shareholders is limited to their part of shareholdings. Owners are not personally

liable for the debs and losses of company.

Personal assets of owners cannot be charged for payment of business debts. Profits are distributed fairly among the shareholders on the basis of their shareholdings.

4

Corporation

Corporations are established as separate legal enterprise from that of its owners. A

corporation is considered as separate legal person for the tax purposes. Corporation has all the

power that rests with an individual. A corporation can be sued, taxes and also it can enter

contractual agreements in it own name. Corporation can have its own bank account, can raise

loan on its own and can sue or be sued in its own name (Borkowski, 2016.). A corporation is

born by law and dies by law. Corporation do not dies with the death of owners. Income

generated by the business belongs to company as its personal income.

Income is taxed as personal income of the company. Corporation can be private as well

as public. Legal requirement related to both the organisations differ from each other. Private

organisations are not large as public organisations. Shareholders are the owners of the

corporations. All the activities and procedures of corporations have to comply with the rules and

regulations under the law. Legislations are established for guiding and monitoring the

corporations over all the business affairs. Single person or director cannot take the decisions of

business. Decisions of the businesses are taken by conducting board meeting and general

meetings. Profits after transferring certain amount in reserves are distributed among the

shareholders of company. Establishment of corporation is an expensive process and require lot of

legal requirements to be followed (Business Organisations. 2019).

Advantages

A corporation has an unlimited commercial life. Corporation do not dissolves with the

death of owner but remains in existence it is dissolved by law.

Corporations can raise funds for the business from public by issuing different securities.

Companies can be listed on the stock exchange.

Ownership of corporations is transferable and can be transferred number of times by

selling the shares.

Biggest advantage of establishing corporation is limited liability of feature. The liability

of the shareholders is limited to their part of shareholdings. Owners are not personally

liable for the debs and losses of company.

Personal assets of owners cannot be charged for payment of business debts. Profits are distributed fairly among the shareholders on the basis of their shareholdings.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantages

Corporations are regulated by laws and legislations and company cannot contravene the

provisions of the act. Compliance with regulations is costly process.

Corporations have high operation and organisational costs. Clerical and legal expenses of

company can increase the budgetary limits.

Decision-making is a lengthy process in corporations it has to undergo different

procedures before making the decisions (Dipboye, 2016).

There is a disadvantage of double taxation in corporations. Taxes are paid on profits of

company and also shareholders have to pay taxes on the dividend income.

B) Main users of accounting information and its importance to different users.

Motive of accounting is accumulating and reporting on the financial informations related

to financial positions, performance and business cash flows. The accounting information enable

to make decisions on management of business, investments and borrowing money for carrying

business transactions. The accounting information are recorded in the accounting records of

business where all the transactions are recorded through standardized business transactions.

Based on these accounting information financial statements are prepared which include, incomes

statement, statement of financial position, cash flow statements, statement for retained earning

and the disclosures for accompanying financial statements.

Financial statements are prepared using basic accounting frameworks. This frameworks

and standards are established for maintaining uniformity in all companies (Judge and Robbins,

2017). This enables users of financial information to make comparisons between the different

organisations. Information related to the business operation are provided to companies by

accounting department. They keep record of all the accounting transactions and these

informations are reviewed by accounting and auditing firms. These informations are used by

business executives for deciding about their future growth plans or enhancement of the existing

business structure. Accounting information is used by both internal as well as external users.

Users and their needs to users.

Internal Users

Owners

First and foremost user of accounting information are owners of the business. Owners use

accounting information for assessing the performance of company. They provide owners

5

Corporations are regulated by laws and legislations and company cannot contravene the

provisions of the act. Compliance with regulations is costly process.

Corporations have high operation and organisational costs. Clerical and legal expenses of

company can increase the budgetary limits.

Decision-making is a lengthy process in corporations it has to undergo different

procedures before making the decisions (Dipboye, 2016).

There is a disadvantage of double taxation in corporations. Taxes are paid on profits of

company and also shareholders have to pay taxes on the dividend income.

B) Main users of accounting information and its importance to different users.

Motive of accounting is accumulating and reporting on the financial informations related

to financial positions, performance and business cash flows. The accounting information enable

to make decisions on management of business, investments and borrowing money for carrying

business transactions. The accounting information are recorded in the accounting records of

business where all the transactions are recorded through standardized business transactions.

Based on these accounting information financial statements are prepared which include, incomes

statement, statement of financial position, cash flow statements, statement for retained earning

and the disclosures for accompanying financial statements.

Financial statements are prepared using basic accounting frameworks. This frameworks

and standards are established for maintaining uniformity in all companies (Judge and Robbins,

2017). This enables users of financial information to make comparisons between the different

organisations. Information related to the business operation are provided to companies by

accounting department. They keep record of all the accounting transactions and these

informations are reviewed by accounting and auditing firms. These informations are used by

business executives for deciding about their future growth plans or enhancement of the existing

business structure. Accounting information is used by both internal as well as external users.

Users and their needs to users.

Internal Users

Owners

First and foremost user of accounting information are owners of the business. Owners use

accounting information for assessing the performance of company. They provide owners

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information about whether business is generating required level of profits or not. It also allows

companies to find out the profitability of individual products, departments, branches and of the

overall business. This enables owners to identify the risk factor that are to be dealt so that do no

affect the growth of organisations (Kinicki and Fugate, 2017).

It allow owners to assess the stability level of business for given period of time and

identifying the extent to which economic factors have affected bottom line of business. Owners

can make decisions about whether they should make further investments in business or the

financial resources of the company should be used in promising ventures of business. Primary

motive of starting a business by owners is of earning profit and the information helps to know

the position of company.

Managers

Another users of accounting information are the mangers. Accounting information is

required by management for planning, monitoring and making the business decisions.

Accounting information is used by managers for allocation of human, financial & capital

resources for competing with the business needs by budgetary processes. Relevant accounting

information is required by managers of company so that they can make prepare and monitor the

budgets for various processes, activities, services, department and segments of business.

Accounting information is required by managers for monitoring the business

performances by comparing competitor analysis, past performances industry benchmarks and

key performance indicators. Accounting information is required by managers for making

business decisions like pricing decisions, investments and financing (Lăzăroiu, 2015). Using the

accounting information management of the company frame policies and procedures for

achieving the organisational goals. For these purposes financial information is used by the

management.

External Users

Investors

Financial information is used by investors for knowing the performance of investments.

Financial information is required for assessing the profitability, risks and valuation of

investments. This information is required by investors for determining about the investment

6

companies to find out the profitability of individual products, departments, branches and of the

overall business. This enables owners to identify the risk factor that are to be dealt so that do no

affect the growth of organisations (Kinicki and Fugate, 2017).

It allow owners to assess the stability level of business for given period of time and

identifying the extent to which economic factors have affected bottom line of business. Owners

can make decisions about whether they should make further investments in business or the

financial resources of the company should be used in promising ventures of business. Primary

motive of starting a business by owners is of earning profit and the information helps to know

the position of company.

Managers

Another users of accounting information are the mangers. Accounting information is

required by management for planning, monitoring and making the business decisions.

Accounting information is used by managers for allocation of human, financial & capital

resources for competing with the business needs by budgetary processes. Relevant accounting

information is required by managers of company so that they can make prepare and monitor the

budgets for various processes, activities, services, department and segments of business.

Accounting information is required by managers for monitoring the business

performances by comparing competitor analysis, past performances industry benchmarks and

key performance indicators. Accounting information is required by managers for making

business decisions like pricing decisions, investments and financing (Lăzăroiu, 2015). Using the

accounting information management of the company frame policies and procedures for

achieving the organisational goals. For these purposes financial information is used by the

management.

External Users

Investors

Financial information is used by investors for knowing the performance of investments.

Financial information is required for assessing the profitability, risks and valuation of

investments. This information is required by investors for determining about the investment

6

whether the investment should be retained, bought or sold. It also used by investors for

determining how effectively their funds have been utilised by company (Miner, 2015).

Lenders

Lenders are the financial institutions or individuals who lend funds to company for

earning interest income. Accounting information is used by lenders before availing funds for

identifying whether business will be able to repay the loans along with interest. They can identify

the assets and liability position of company before granting loans to company.

Suppliers

Sellers are the business organisations or individuals who provide raw materials to

business on credit. Accounting information give idea about credit worthiness of business so that

they can make decisions before giving raw materials. It is also used by suppliers for assessing the

wealth of its customers.

Customers

Accounting information is used by consumers for knowing the current market position of

business and making judgement for business future. Customers of business can be wholesalers,m

retailers and final consumers (Musringudin, Akbar and Karnati, 2017). Customers use

accounting information for knowing the business performance whether company will be able to

continue the supply of parts, raw materials or components that are used for various uses.

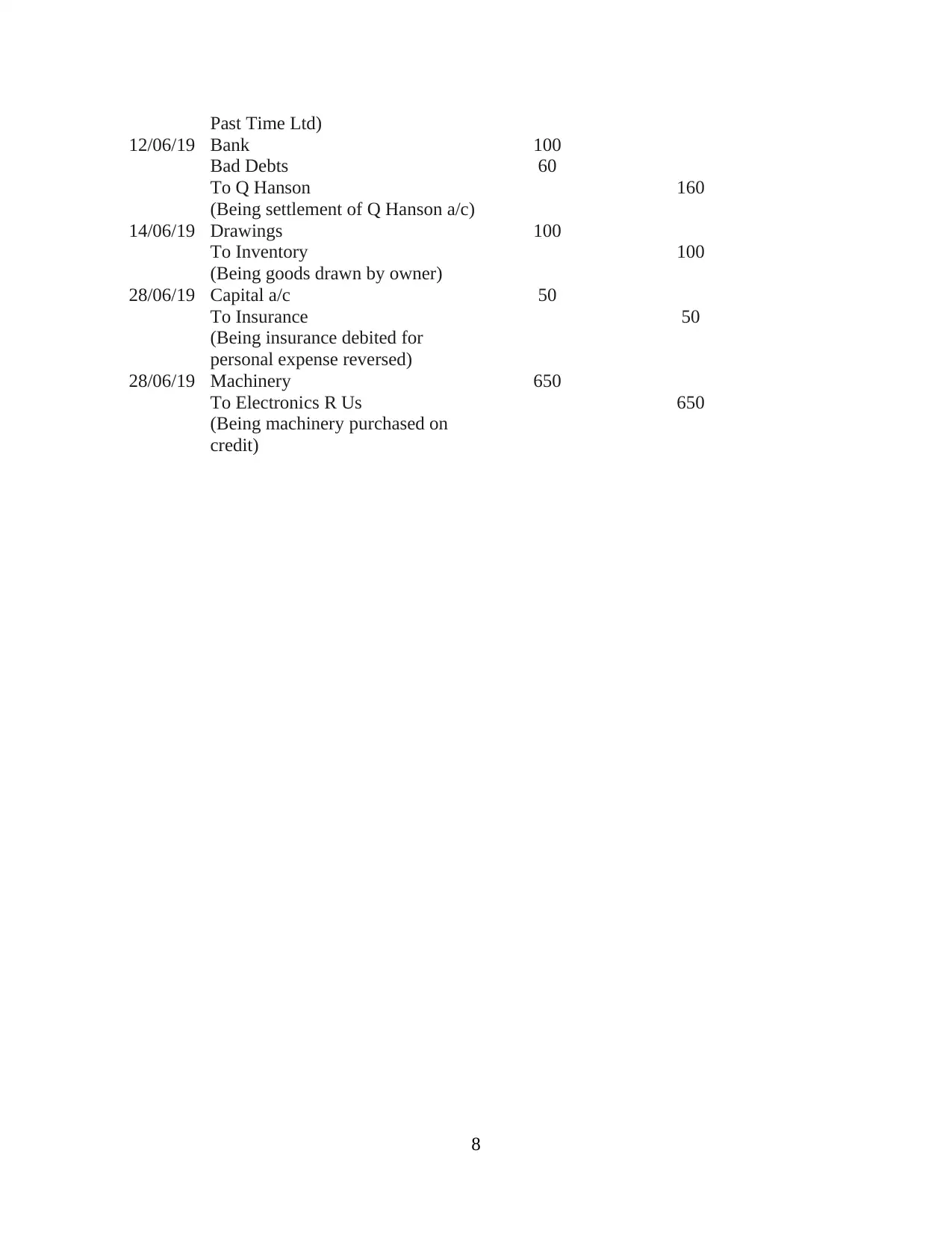

PART 2

Journal Entries

Journal Entries

Date Particulars Debit Credit

01/06/19 Van 2696

To Pressed Garages 2696

( Being van purchased on credit

from Pressed Garages)

03/06/19 Bad Debts 50

To K. Patel 50

(Being bed debt written off for due

from K.Patel)

08/06/19 Past Time ltd 400

To Office Fixtures 400

(Being office fixtures returned to

7

determining how effectively their funds have been utilised by company (Miner, 2015).

Lenders

Lenders are the financial institutions or individuals who lend funds to company for

earning interest income. Accounting information is used by lenders before availing funds for

identifying whether business will be able to repay the loans along with interest. They can identify

the assets and liability position of company before granting loans to company.

Suppliers

Sellers are the business organisations or individuals who provide raw materials to

business on credit. Accounting information give idea about credit worthiness of business so that

they can make decisions before giving raw materials. It is also used by suppliers for assessing the

wealth of its customers.

Customers

Accounting information is used by consumers for knowing the current market position of

business and making judgement for business future. Customers of business can be wholesalers,m

retailers and final consumers (Musringudin, Akbar and Karnati, 2017). Customers use

accounting information for knowing the business performance whether company will be able to

continue the supply of parts, raw materials or components that are used for various uses.

PART 2

Journal Entries

Journal Entries

Date Particulars Debit Credit

01/06/19 Van 2696

To Pressed Garages 2696

( Being van purchased on credit

from Pressed Garages)

03/06/19 Bad Debts 50

To K. Patel 50

(Being bed debt written off for due

from K.Patel)

08/06/19 Past Time ltd 400

To Office Fixtures 400

(Being office fixtures returned to

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Past Time Ltd)

12/06/19 Bank 100

Bad Debts 60

To Q Hanson 160

(Being settlement of Q Hanson a/c)

14/06/19 Drawings 100

To Inventory 100

(Being goods drawn by owner)

28/06/19 Capital a/c 50

To Insurance 50

(Being insurance debited for

personal expense reversed)

28/06/19 Machinery 650

To Electronics R Us 650

(Being machinery purchased on

credit)

8

12/06/19 Bank 100

Bad Debts 60

To Q Hanson 160

(Being settlement of Q Hanson a/c)

14/06/19 Drawings 100

To Inventory 100

(Being goods drawn by owner)

28/06/19 Capital a/c 50

To Insurance 50

(Being insurance debited for

personal expense reversed)

28/06/19 Machinery 650

To Electronics R Us 650

(Being machinery purchased on

credit)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

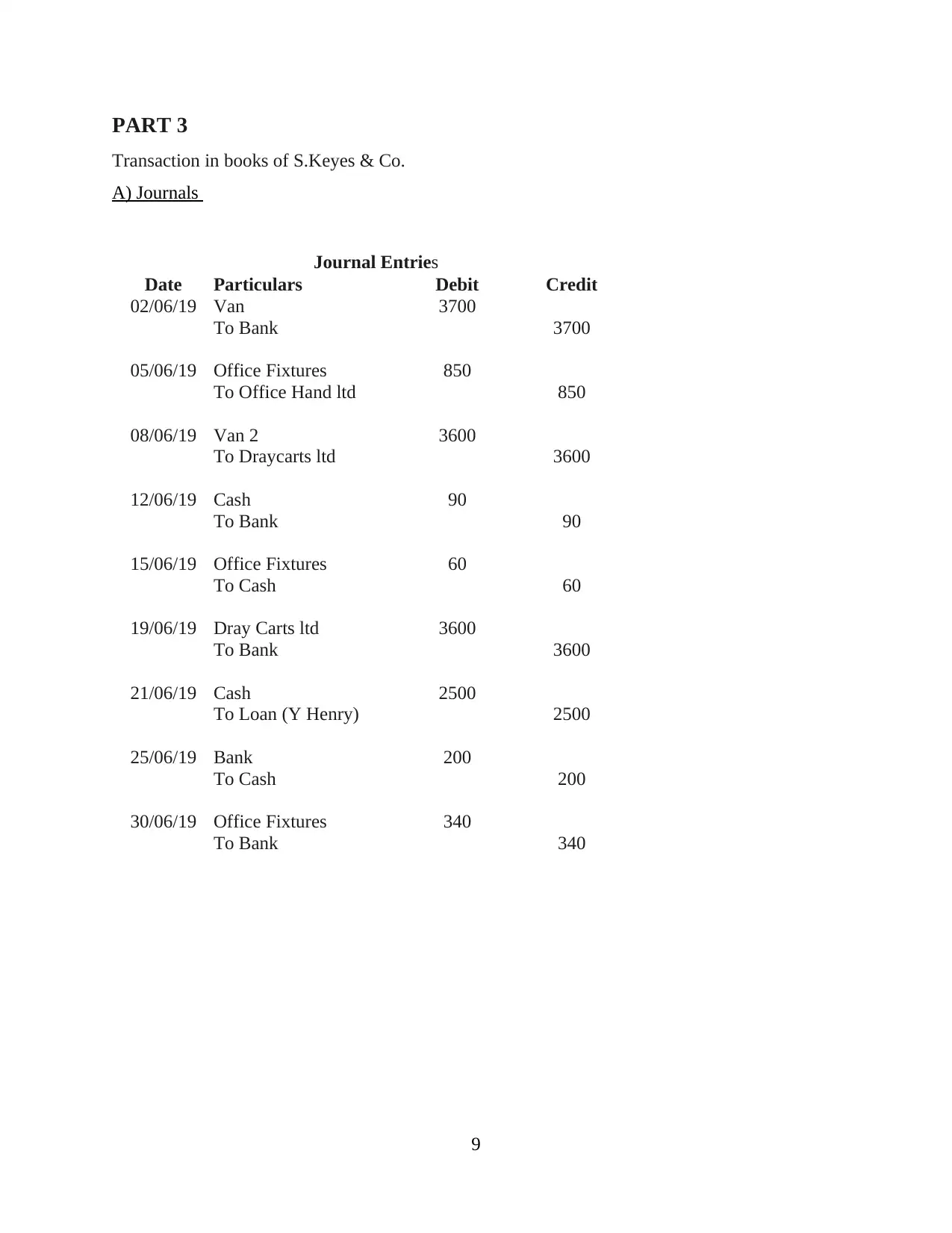

PART 3

Transaction in books of S.Keyes & Co.

A) Journals

Journal Entries

Date Particulars Debit Credit

02/06/19 Van 3700

To Bank 3700

05/06/19 Office Fixtures 850

To Office Hand ltd 850

08/06/19 Van 2 3600

To Draycarts ltd 3600

12/06/19 Cash 90

To Bank 90

15/06/19 Office Fixtures 60

To Cash 60

19/06/19 Dray Carts ltd 3600

To Bank 3600

21/06/19 Cash 2500

To Loan (Y Henry) 2500

25/06/19 Bank 200

To Cash 200

30/06/19 Office Fixtures 340

To Bank 340

9

Transaction in books of S.Keyes & Co.

A) Journals

Journal Entries

Date Particulars Debit Credit

02/06/19 Van 3700

To Bank 3700

05/06/19 Office Fixtures 850

To Office Hand ltd 850

08/06/19 Van 2 3600

To Draycarts ltd 3600

12/06/19 Cash 90

To Bank 90

15/06/19 Office Fixtures 60

To Cash 60

19/06/19 Dray Carts ltd 3600

To Bank 3600

21/06/19 Cash 2500

To Loan (Y Henry) 2500

25/06/19 Bank 200

To Cash 200

30/06/19 Office Fixtures 340

To Bank 340

9

B) ledgers and Trial Balance

a) Ledgers

LEDGER OF S. KEYES

CASH A/C

Date Particulars DR. £ Date Particulars CR. £

01/06/19 To capital 7500 15/06/19 By fixtures 60

25/06/19 By bank 200

30/06/19 By bal b/f 7240

7500 7500

CAPITAL A/C

Date Particulars DR. £ Date Particulars CR. £

30/06/19 To bal b/f 7500 01/06/19 By cash 7500

7500 7500

VAN A/C

Date Particulars DR. £ Date Particulars CR. £

02/06/19 To bank 3700

08/06/19

To

Draycarts 3600 30/06/19 By bal b/f 7300

7300 7300

BANK A/C

Date Particulars DR. £ Date Particulars CR. £

25/06/19 To cash 200 02/06/19 By van 3700

30/06/19 To bal b/f 7530 12/06/19

By petty

cash 90

19/06/19

By

Draycarts 3600

30/06/19 By fixtures 340

7730 7730

FIXTURES A/C

Date Particulars DR. £ Date Particulars CR. £

05/06/19

To office

hand ltd 850 30/06/19 By bal b/f 1250

15/06/19 To cash 60

30/06/19 To bank 340

10

a) Ledgers

LEDGER OF S. KEYES

CASH A/C

Date Particulars DR. £ Date Particulars CR. £

01/06/19 To capital 7500 15/06/19 By fixtures 60

25/06/19 By bank 200

30/06/19 By bal b/f 7240

7500 7500

CAPITAL A/C

Date Particulars DR. £ Date Particulars CR. £

30/06/19 To bal b/f 7500 01/06/19 By cash 7500

7500 7500

VAN A/C

Date Particulars DR. £ Date Particulars CR. £

02/06/19 To bank 3700

08/06/19

To

Draycarts 3600 30/06/19 By bal b/f 7300

7300 7300

BANK A/C

Date Particulars DR. £ Date Particulars CR. £

25/06/19 To cash 200 02/06/19 By van 3700

30/06/19 To bal b/f 7530 12/06/19

By petty

cash 90

19/06/19

By

Draycarts 3600

30/06/19 By fixtures 340

7730 7730

FIXTURES A/C

Date Particulars DR. £ Date Particulars CR. £

05/06/19

To office

hand ltd 850 30/06/19 By bal b/f 1250

15/06/19 To cash 60

30/06/19 To bank 340

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.