Analyzing Business Performance: Economic Factors & Accounting Role

VerifiedAdded on 2023/06/17

|13

|3568

|189

Report

AI Summary

This report explores the intricate relationship between business finance, economics, and accounting practices. It begins by examining the main determinants of macroeconomic and microeconomic factors that influence business performance within a competitive environment, highlighting the impact of customers, suppliers, demographics, and political factors, as well as economic factors like interest rates, exchange values, and recession. The report then defines the importance of accounting within an organization, emphasizing its role in both reporting and decision-making through transparency, statutory compliance, debt management, taxation policies, and future assessments. It differentiates between the main financial statements—balance sheet and profit & loss statement—explaining their layouts and key terms. Furthermore, the report evaluates and interprets financial ratios such as return on shareholder's equity, return on capital employed, operating profit margin, and current ratio using provided balance sheet and income statement data for the years 2019 and 2020. Finally, it explains management accounting and discusses its importance for planning, controlling, and decision-making within an organization, underscoring its role in strategic planning, operational control, and effective decision support. The analysis concludes by reinforcing the significance of integrating financial and economic considerations for optimal business outcomes. This document is available on Desklib, a platform offering a wide range of study tools and resources for students.

Business Finance

&

Economics

&

Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK ..............................................................................................................................................3

1. Explanation about the main determinants of macro or micro economic factors to showcase

the business performance in impact with the competitive environment.....................................3

2. Defining the importance of accounting within an organisation with respect to both reporting

and decision-making...................................................................................................................4

3. Difference between the main financial statements and explain the layout & terms used

within the Statement....................................................................................................................6

4. Evaluate & Interpret the following ratios by using balance sheet and income statement:......8

5. Explain management accounting and discuss its importance for planning, controlling and

decision-making within an organisation.....................................................................................9

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION ..........................................................................................................................3

TASK ..............................................................................................................................................3

1. Explanation about the main determinants of macro or micro economic factors to showcase

the business performance in impact with the competitive environment.....................................3

2. Defining the importance of accounting within an organisation with respect to both reporting

and decision-making...................................................................................................................4

3. Difference between the main financial statements and explain the layout & terms used

within the Statement....................................................................................................................6

4. Evaluate & Interpret the following ratios by using balance sheet and income statement:......8

5. Explain management accounting and discuss its importance for planning, controlling and

decision-making within an organisation.....................................................................................9

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Organization finance and economies are the interlinkage between the financial and

economical criteria. Financing is focused upon the accounting system and economies is centred

on the assumptions which basis on the outcome of companies relative formulation(Aisy,

Mulyono and Susilowati, 2017). The company is also showing the different factors of economy

which will put down impact upon its competitive advantages. The company is also showing it

roles & importance over the accounting per-forma and management accounting with the proper

layout and calculation of resources of the major financial statements.

TASK

1. Explanation about the main determinants of macro or micro economic factors to showcase the

business performance in impact with the competitive environment.

Organisation is performing based upon various inclusion of the components in the

marketplace either with positive or negative impact. This supposed to be in the

controllable or uncontrollable environment for influential decision-making power. The

major determining factors in regards with firm performance are as follows:

1. Customers: Business has inclination of the large scaling individuals which can be B2B,

B2C, domestic or global recognized. They are majorly impacted upon the running

concern by taking their decisions of purchasing from the outside world. These are the

micro-economic factor because it can be controllable in nature by fulfilling their taste &

preferences without delay.

2. Suppliers: This determinant is consisting the control nature in the market-area to

establish their identification with various business. If supplier-person is setting up the

monopoly in the field by covering largest area, they can brought up impact upon the

performance of enterprise(Arnold, 2018). Because their products & services become core

and necessary for the business entity.

3. Demographics: This is the concept of considering various segmenting & targeting

market strategies which includes the age, region, culture, lifestyle and other factorization.

If the company is choosing right target market with different allocation strategy, this

means they are in the block of stable performance.

Organization finance and economies are the interlinkage between the financial and

economical criteria. Financing is focused upon the accounting system and economies is centred

on the assumptions which basis on the outcome of companies relative formulation(Aisy,

Mulyono and Susilowati, 2017). The company is also showing the different factors of economy

which will put down impact upon its competitive advantages. The company is also showing it

roles & importance over the accounting per-forma and management accounting with the proper

layout and calculation of resources of the major financial statements.

TASK

1. Explanation about the main determinants of macro or micro economic factors to showcase the

business performance in impact with the competitive environment.

Organisation is performing based upon various inclusion of the components in the

marketplace either with positive or negative impact. This supposed to be in the

controllable or uncontrollable environment for influential decision-making power. The

major determining factors in regards with firm performance are as follows:

1. Customers: Business has inclination of the large scaling individuals which can be B2B,

B2C, domestic or global recognized. They are majorly impacted upon the running

concern by taking their decisions of purchasing from the outside world. These are the

micro-economic factor because it can be controllable in nature by fulfilling their taste &

preferences without delay.

2. Suppliers: This determinant is consisting the control nature in the market-area to

establish their identification with various business. If supplier-person is setting up the

monopoly in the field by covering largest area, they can brought up impact upon the

performance of enterprise(Arnold, 2018). Because their products & services become core

and necessary for the business entity.

3. Demographics: This is the concept of considering various segmenting & targeting

market strategies which includes the age, region, culture, lifestyle and other factorization.

If the company is choosing right target market with different allocation strategy, this

means they are in the block of stable performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Political: Every business are under the eye-lock of the governmental & political power,

rules & regulation to legally optimize and running the enterprises in the smooth manner.

If entity is also not properly follows these cautions and obligations, this means they are

infringing the laws. This is showing the negative impact on the business performing

activity.

Economic Factors that affects competitive environment:

These facets having connection with the goods, services and cash-movement. This

determinants are showing the financial status of the company (Bikfalvi, 2017). These includes

some of the major objectives of the scenario which are:

1. Interest rate: It is vary from place-to-place along with individuals. These ratings amount

specially shown in the banking institutions for different transactions on money movement

for large loans for domestic as well as global companies. These type of rates for various

nations are impactful for its competitive benefit.

2. Exchange values: This scaling is based upon the export & import dealings fluctuation in

the market. It is focused on the present timing rates of transactions. Any kind of changing

values at the time of exporting & importing will directly affect the company's competitive

advantages because of high & low amounting in the marketplace.

3. Recession: It has the potentiality to change the buying behaviour of the customers based

on their demanding & supplying. If recession increases, companies have to drop out their

pricing level. It become highly impacted positive or negatively upon the beneficiary area

of the organization (Birch, 2017).

2. Defining the importance of accounting within an organisation with respect to both reporting

and decision-making.

Accounting system is using for the measurement and summarization of the monetary

funding. It is helpful for taking beneficiary judgements and to make improvement in the financial

positioning in the system by doing better placements of given information. Business also

recorded their data in the Statement of financial position and income portfolio. This reporting of

rules & regulation to legally optimize and running the enterprises in the smooth manner.

If entity is also not properly follows these cautions and obligations, this means they are

infringing the laws. This is showing the negative impact on the business performing

activity.

Economic Factors that affects competitive environment:

These facets having connection with the goods, services and cash-movement. This

determinants are showing the financial status of the company (Bikfalvi, 2017). These includes

some of the major objectives of the scenario which are:

1. Interest rate: It is vary from place-to-place along with individuals. These ratings amount

specially shown in the banking institutions for different transactions on money movement

for large loans for domestic as well as global companies. These type of rates for various

nations are impactful for its competitive benefit.

2. Exchange values: This scaling is based upon the export & import dealings fluctuation in

the market. It is focused on the present timing rates of transactions. Any kind of changing

values at the time of exporting & importing will directly affect the company's competitive

advantages because of high & low amounting in the marketplace.

3. Recession: It has the potentiality to change the buying behaviour of the customers based

on their demanding & supplying. If recession increases, companies have to drop out their

pricing level. It become highly impacted positive or negatively upon the beneficiary area

of the organization (Birch, 2017).

2. Defining the importance of accounting within an organisation with respect to both reporting

and decision-making.

Accounting system is using for the measurement and summarization of the monetary

funding. It is helpful for taking beneficiary judgements and to make improvement in the financial

positioning in the system by doing better placements of given information. Business also

recorded their data in the Statement of financial position and income portfolio. This reporting of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

data procedure has been disclosed the overall position and annual performance of the

organization.

Importance of accounting reporting & decision-making:

1. Amendment of beneficiary decisions: It is helpful for making concise, expert and

trending scenarios while compiling the informative judgement. It only gives knowledge

when the tracking of proper records has been done.

2. Transparency in nature: Company has been showing its financial position and profit-

loss scenario at the time to influence the shareholders and stakeholders (Borg, 2019).

This can be only possible when they are presenting transparent nature.

3. Statutory compliances: Accuracy and standardization in the financial reports of industry

has been considering the full support with the government norms. Because they have all

the legal compilation of financial structure.

4. Managing Debt-obligation: These accounting system and alignment of the company

structure has been providing the direct impact on its assets & liabilities transactions. It

become valuable for the effective & efficient management of the outstanding obligations

in the current and future time period.

5. Taxation policies: Corporation is also defining the tax portion deduction within the

revenue generation. It is conceptualize the rational risk-breaking decisions of the system

in against with the governing norms. It cannot take any burden from filing the tax-returns

because they are comes under the legislative theory (Cruz and Miranda, 2021).

6. Future assessment: The enterprise is also taking advancement & grabbing opportunities

about the future assignments in the firm. If their concept of futuristic goals and objective

are clear in mind, then it will be beneficial for them.

organization.

Importance of accounting reporting & decision-making:

1. Amendment of beneficiary decisions: It is helpful for making concise, expert and

trending scenarios while compiling the informative judgement. It only gives knowledge

when the tracking of proper records has been done.

2. Transparency in nature: Company has been showing its financial position and profit-

loss scenario at the time to influence the shareholders and stakeholders (Borg, 2019).

This can be only possible when they are presenting transparent nature.

3. Statutory compliances: Accuracy and standardization in the financial reports of industry

has been considering the full support with the government norms. Because they have all

the legal compilation of financial structure.

4. Managing Debt-obligation: These accounting system and alignment of the company

structure has been providing the direct impact on its assets & liabilities transactions. It

become valuable for the effective & efficient management of the outstanding obligations

in the current and future time period.

5. Taxation policies: Corporation is also defining the tax portion deduction within the

revenue generation. It is conceptualize the rational risk-breaking decisions of the system

in against with the governing norms. It cannot take any burden from filing the tax-returns

because they are comes under the legislative theory (Cruz and Miranda, 2021).

6. Future assessment: The enterprise is also taking advancement & grabbing opportunities

about the future assignments in the firm. If their concept of futuristic goals and objective

are clear in mind, then it will be beneficial for them.

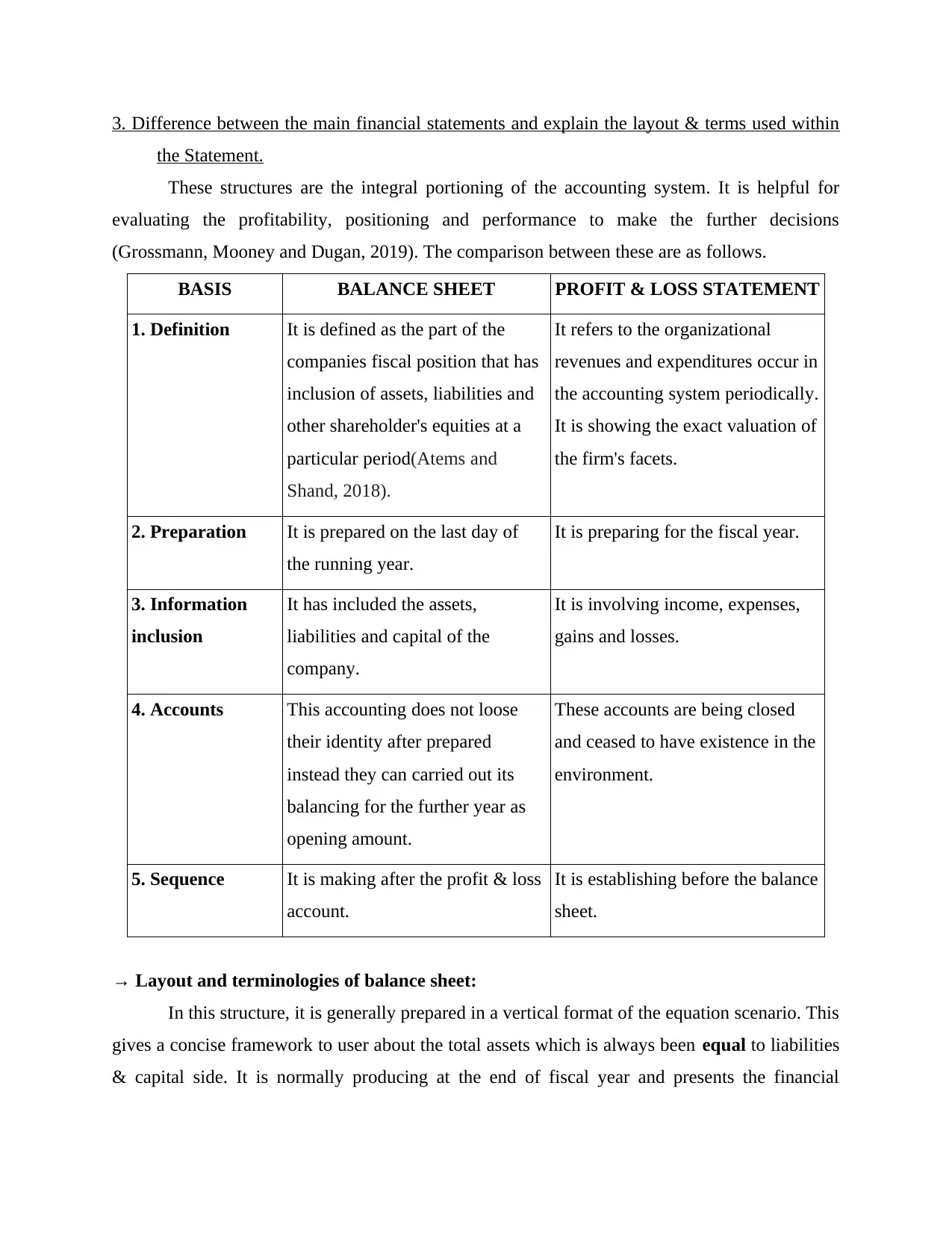

3. Difference between the main financial statements and explain the layout & terms used within

the Statement.

These structures are the integral portioning of the accounting system. It is helpful for

evaluating the profitability, positioning and performance to make the further decisions

(Grossmann, Mooney and Dugan, 2019). The comparison between these are as follows.

BASIS BALANCE SHEET PROFIT & LOSS STATEMENT

1. Definition It is defined as the part of the

companies fiscal position that has

inclusion of assets, liabilities and

other shareholder's equities at a

particular period(Atems and

Shand, 2018).

It refers to the organizational

revenues and expenditures occur in

the accounting system periodically.

It is showing the exact valuation of

the firm's facets.

2. Preparation It is prepared on the last day of

the running year.

It is preparing for the fiscal year.

3. Information

inclusion

It has included the assets,

liabilities and capital of the

company.

It is involving income, expenses,

gains and losses.

4. Accounts This accounting does not loose

their identity after prepared

instead they can carried out its

balancing for the further year as

opening amount.

These accounts are being closed

and ceased to have existence in the

environment.

5. Sequence It is making after the profit & loss

account.

It is establishing before the balance

sheet.

→ Layout and terminologies of balance sheet:

In this structure, it is generally prepared in a vertical format of the equation scenario. This

gives a concise framework to user about the total assets which is always been equal to liabilities

& capital side. It is normally producing at the end of fiscal year and presents the financial

the Statement.

These structures are the integral portioning of the accounting system. It is helpful for

evaluating the profitability, positioning and performance to make the further decisions

(Grossmann, Mooney and Dugan, 2019). The comparison between these are as follows.

BASIS BALANCE SHEET PROFIT & LOSS STATEMENT

1. Definition It is defined as the part of the

companies fiscal position that has

inclusion of assets, liabilities and

other shareholder's equities at a

particular period(Atems and

Shand, 2018).

It refers to the organizational

revenues and expenditures occur in

the accounting system periodically.

It is showing the exact valuation of

the firm's facets.

2. Preparation It is prepared on the last day of

the running year.

It is preparing for the fiscal year.

3. Information

inclusion

It has included the assets,

liabilities and capital of the

company.

It is involving income, expenses,

gains and losses.

4. Accounts This accounting does not loose

their identity after prepared

instead they can carried out its

balancing for the further year as

opening amount.

These accounts are being closed

and ceased to have existence in the

environment.

5. Sequence It is making after the profit & loss

account.

It is establishing before the balance

sheet.

→ Layout and terminologies of balance sheet:

In this structure, it is generally prepared in a vertical format of the equation scenario. This

gives a concise framework to user about the total assets which is always been equal to liabilities

& capital side. It is normally producing at the end of fiscal year and presents the financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

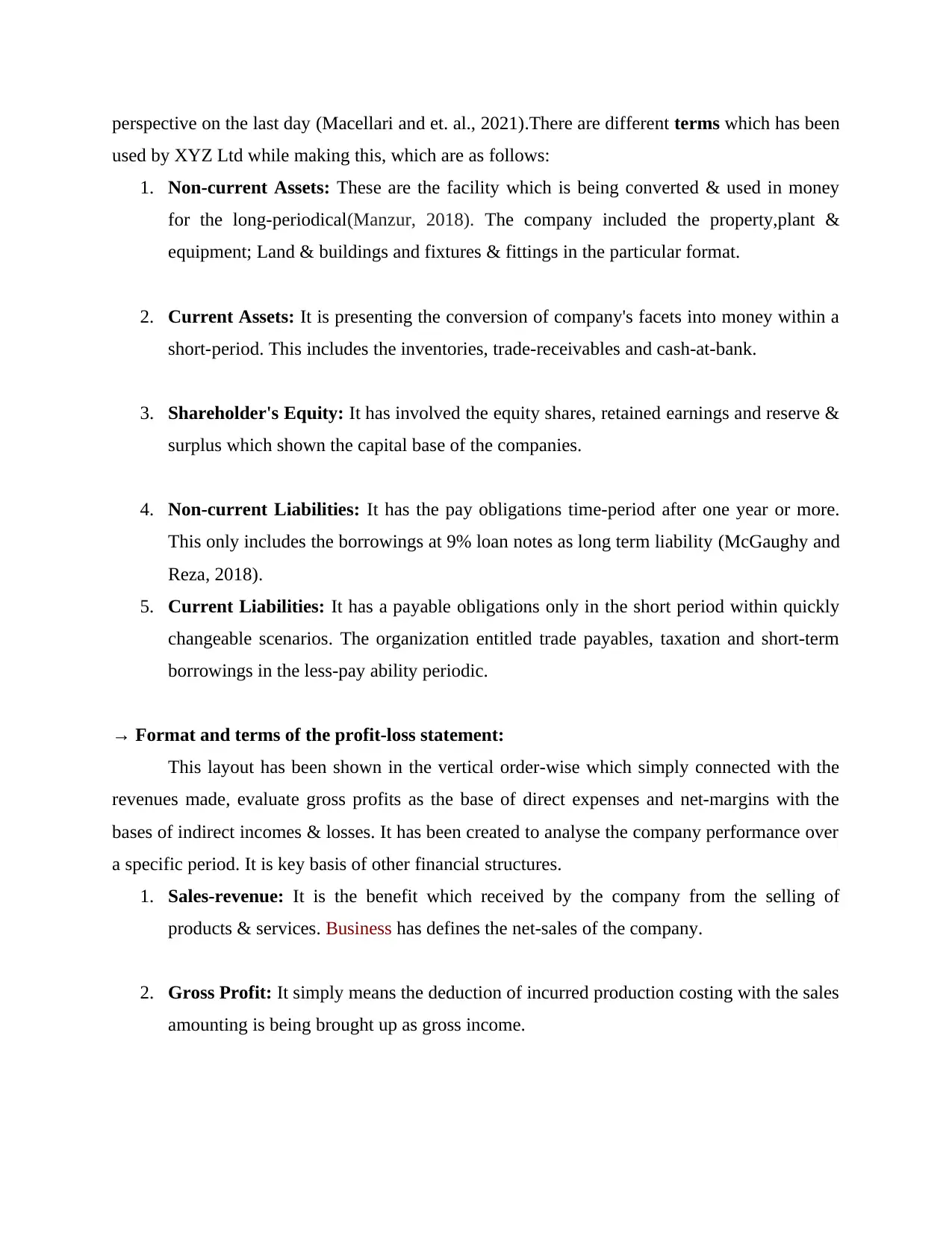

perspective on the last day (Macellari and et. al., 2021).There are different terms which has been

used by XYZ Ltd while making this, which are as follows:

1. Non-current Assets: These are the facility which is being converted & used in money

for the long-periodical(Manzur, 2018). The company included the property,plant &

equipment; Land & buildings and fixtures & fittings in the particular format.

2. Current Assets: It is presenting the conversion of company's facets into money within a

short-period. This includes the inventories, trade-receivables and cash-at-bank.

3. Shareholder's Equity: It has involved the equity shares, retained earnings and reserve &

surplus which shown the capital base of the companies.

4. Non-current Liabilities: It has the pay obligations time-period after one year or more.

This only includes the borrowings at 9% loan notes as long term liability (McGaughy and

Reza, 2018).

5. Current Liabilities: It has a payable obligations only in the short period within quickly

changeable scenarios. The organization entitled trade payables, taxation and short-term

borrowings in the less-pay ability periodic.

→ Format and terms of the profit-loss statement:

This layout has been shown in the vertical order-wise which simply connected with the

revenues made, evaluate gross profits as the base of direct expenses and net-margins with the

bases of indirect incomes & losses. It has been created to analyse the company performance over

a specific period. It is key basis of other financial structures.

1. Sales-revenue: It is the benefit which received by the company from the selling of

products & services. Business has defines the net-sales of the company.

2. Gross Profit: It simply means the deduction of incurred production costing with the sales

amounting is being brought up as gross income.

used by XYZ Ltd while making this, which are as follows:

1. Non-current Assets: These are the facility which is being converted & used in money

for the long-periodical(Manzur, 2018). The company included the property,plant &

equipment; Land & buildings and fixtures & fittings in the particular format.

2. Current Assets: It is presenting the conversion of company's facets into money within a

short-period. This includes the inventories, trade-receivables and cash-at-bank.

3. Shareholder's Equity: It has involved the equity shares, retained earnings and reserve &

surplus which shown the capital base of the companies.

4. Non-current Liabilities: It has the pay obligations time-period after one year or more.

This only includes the borrowings at 9% loan notes as long term liability (McGaughy and

Reza, 2018).

5. Current Liabilities: It has a payable obligations only in the short period within quickly

changeable scenarios. The organization entitled trade payables, taxation and short-term

borrowings in the less-pay ability periodic.

→ Format and terms of the profit-loss statement:

This layout has been shown in the vertical order-wise which simply connected with the

revenues made, evaluate gross profits as the base of direct expenses and net-margins with the

bases of indirect incomes & losses. It has been created to analyse the company performance over

a specific period. It is key basis of other financial structures.

1. Sales-revenue: It is the benefit which received by the company from the selling of

products & services. Business has defines the net-sales of the company.

2. Gross Profit: It simply means the deduction of incurred production costing with the sales

amounting is being brought up as gross income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Operating Expenses: These workings are the establishment of the key functional

expenditures within the company (Modell, 2020). It is also known as direct expenses.

These are impactful for the gross-marginality activity.

4. Non-operating expenditure: In this criteria, the coverage of administrative, selling &

distribution has been included. It is also known as the indirect costing. These shows the

impression on the net-benefits of the organization(Wang and et. al., 2020).

5. Net Margin: It is the overall performance after deduction of all the cash-outlays,

taxations, depreciation and other values which has the greatest impact upon the net-

valuation of the system.

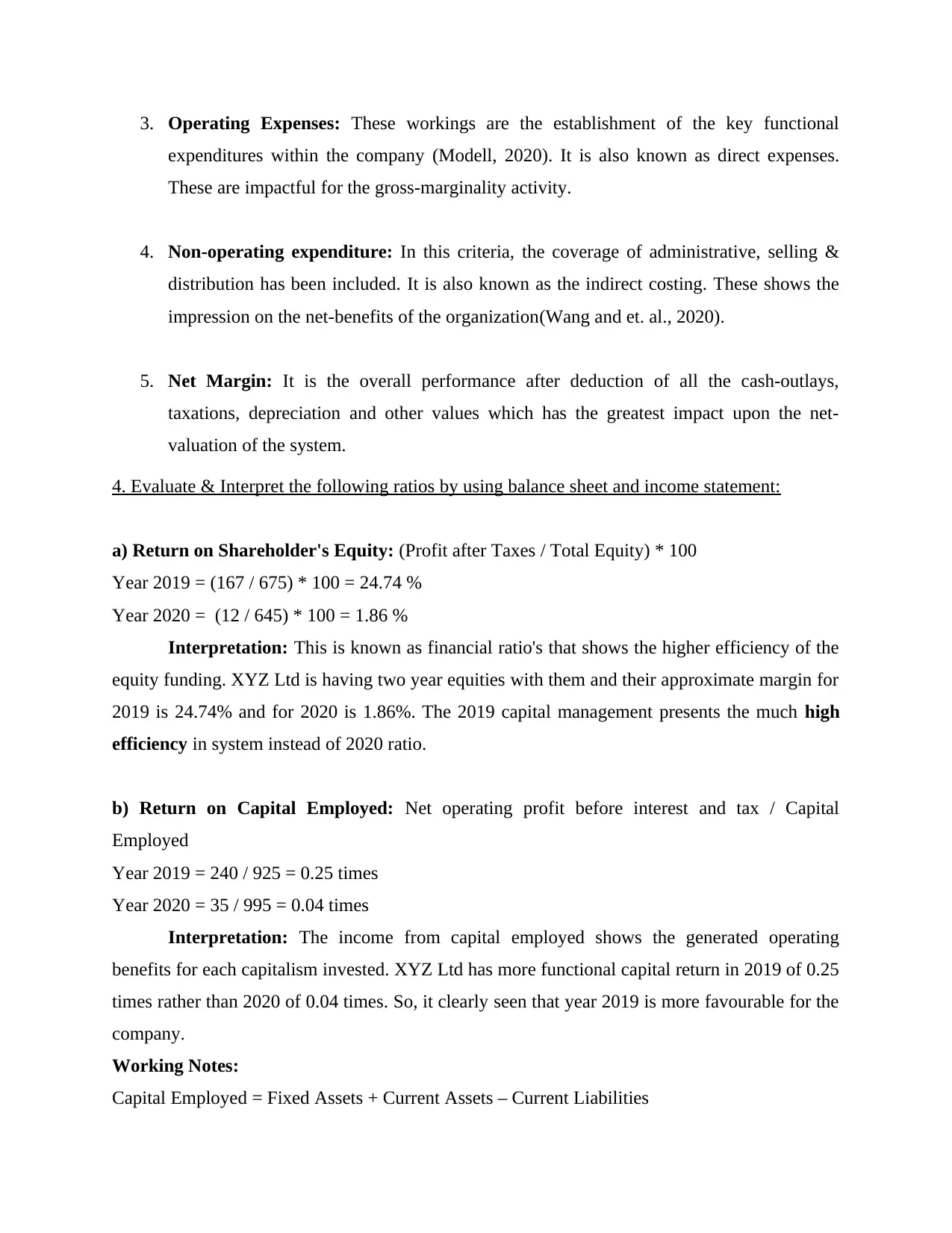

4. Evaluate & Interpret the following ratios by using balance sheet and income statement:

a) Return on Shareholder's Equity: (Profit after Taxes / Total Equity) * 100

Year 2019 = (167 / 675) * 100 = 24.74 %

Year 2020 = (12 / 645) * 100 = 1.86 %

Interpretation: This is known as financial ratio's that shows the higher efficiency of the

equity funding. XYZ Ltd is having two year equities with them and their approximate margin for

2019 is 24.74% and for 2020 is 1.86%. The 2019 capital management presents the much high

efficiency in system instead of 2020 ratio.

b) Return on Capital Employed: Net operating profit before interest and tax / Capital

Employed

Year 2019 = 240 / 925 = 0.25 times

Year 2020 = 35 / 995 = 0.04 times

Interpretation: The income from capital employed shows the generated operating

benefits for each capitalism invested. XYZ Ltd has more functional capital return in 2019 of 0.25

times rather than 2020 of 0.04 times. So, it clearly seen that year 2019 is more favourable for the

company.

Working Notes:

Capital Employed = Fixed Assets + Current Assets – Current Liabilities

expenditures within the company (Modell, 2020). It is also known as direct expenses.

These are impactful for the gross-marginality activity.

4. Non-operating expenditure: In this criteria, the coverage of administrative, selling &

distribution has been included. It is also known as the indirect costing. These shows the

impression on the net-benefits of the organization(Wang and et. al., 2020).

5. Net Margin: It is the overall performance after deduction of all the cash-outlays,

taxations, depreciation and other values which has the greatest impact upon the net-

valuation of the system.

4. Evaluate & Interpret the following ratios by using balance sheet and income statement:

a) Return on Shareholder's Equity: (Profit after Taxes / Total Equity) * 100

Year 2019 = (167 / 675) * 100 = 24.74 %

Year 2020 = (12 / 645) * 100 = 1.86 %

Interpretation: This is known as financial ratio's that shows the higher efficiency of the

equity funding. XYZ Ltd is having two year equities with them and their approximate margin for

2019 is 24.74% and for 2020 is 1.86%. The 2019 capital management presents the much high

efficiency in system instead of 2020 ratio.

b) Return on Capital Employed: Net operating profit before interest and tax / Capital

Employed

Year 2019 = 240 / 925 = 0.25 times

Year 2020 = 35 / 995 = 0.04 times

Interpretation: The income from capital employed shows the generated operating

benefits for each capitalism invested. XYZ Ltd has more functional capital return in 2019 of 0.25

times rather than 2020 of 0.04 times. So, it clearly seen that year 2019 is more favourable for the

company.

Working Notes:

Capital Employed = Fixed Assets + Current Assets – Current Liabilities

2019 = 520 + 595 -190 = 925

2020 = 600 + 690 – 295 = 995

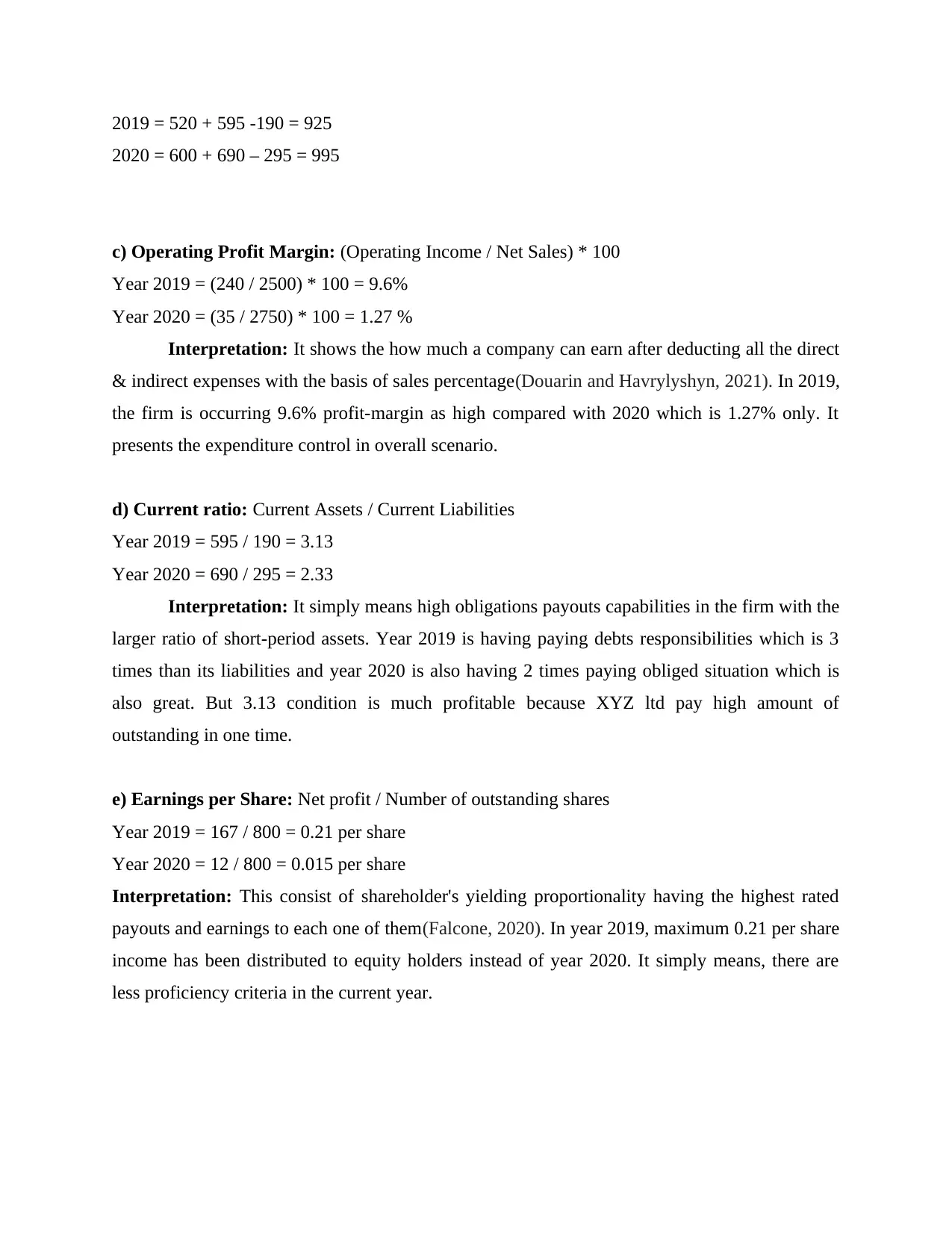

c) Operating Profit Margin: (Operating Income / Net Sales) * 100

Year 2019 = (240 / 2500) * 100 = 9.6%

Year 2020 = (35 / 2750) * 100 = 1.27 %

Interpretation: It shows the how much a company can earn after deducting all the direct

& indirect expenses with the basis of sales percentage(Douarin and Havrylyshyn, 2021). In 2019,

the firm is occurring 9.6% profit-margin as high compared with 2020 which is 1.27% only. It

presents the expenditure control in overall scenario.

d) Current ratio: Current Assets / Current Liabilities

Year 2019 = 595 / 190 = 3.13

Year 2020 = 690 / 295 = 2.33

Interpretation: It simply means high obligations payouts capabilities in the firm with the

larger ratio of short-period assets. Year 2019 is having paying debts responsibilities which is 3

times than its liabilities and year 2020 is also having 2 times paying obliged situation which is

also great. But 3.13 condition is much profitable because XYZ ltd pay high amount of

outstanding in one time.

e) Earnings per Share: Net profit / Number of outstanding shares

Year 2019 = 167 / 800 = 0.21 per share

Year 2020 = 12 / 800 = 0.015 per share

Interpretation: This consist of shareholder's yielding proportionality having the highest rated

payouts and earnings to each one of them(Falcone, 2020). In year 2019, maximum 0.21 per share

income has been distributed to equity holders instead of year 2020. It simply means, there are

less proficiency criteria in the current year.

2020 = 600 + 690 – 295 = 995

c) Operating Profit Margin: (Operating Income / Net Sales) * 100

Year 2019 = (240 / 2500) * 100 = 9.6%

Year 2020 = (35 / 2750) * 100 = 1.27 %

Interpretation: It shows the how much a company can earn after deducting all the direct

& indirect expenses with the basis of sales percentage(Douarin and Havrylyshyn, 2021). In 2019,

the firm is occurring 9.6% profit-margin as high compared with 2020 which is 1.27% only. It

presents the expenditure control in overall scenario.

d) Current ratio: Current Assets / Current Liabilities

Year 2019 = 595 / 190 = 3.13

Year 2020 = 690 / 295 = 2.33

Interpretation: It simply means high obligations payouts capabilities in the firm with the

larger ratio of short-period assets. Year 2019 is having paying debts responsibilities which is 3

times than its liabilities and year 2020 is also having 2 times paying obliged situation which is

also great. But 3.13 condition is much profitable because XYZ ltd pay high amount of

outstanding in one time.

e) Earnings per Share: Net profit / Number of outstanding shares

Year 2019 = 167 / 800 = 0.21 per share

Year 2020 = 12 / 800 = 0.015 per share

Interpretation: This consist of shareholder's yielding proportionality having the highest rated

payouts and earnings to each one of them(Falcone, 2020). In year 2019, maximum 0.21 per share

income has been distributed to equity holders instead of year 2020. It simply means, there are

less proficiency criteria in the current year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5. Explain management accounting and discuss its importance for planning, controlling and

decision-making within an organisation.

Managerial accountancy is the process of collection, formative, measurement, modify

and transmission the financial activity of the firm to explicate the organisational placement and

objectives. Company is also represents the important facets to the top executives, stakeholders

and shareholders for the purpose of transparency in the organization. They are aiming for the

informatory estimation in return of fruitful outcome. This has engagement of only the internal

individuals not the externals. Enterprise is doing customization of structure for the useful usage

of the statements.

Importance of management accounting:

Planning: In the system, company uses the collected data for the development of the

particular objectives and preparing strategical plan for the future orientation. It is also

important that all the information should be knowledgeable, properly maintained and

having maximize utilization of resources like budgets (Opute and Madichie, 2017). This

budgeting processing is also helpful for executives by providing the estimate effects of

the ability to achieve desired goals.

Controlling: It is the monitoring, measuring and evaluating the actual outcomes of the

enterprises to manage the fulfilment of the desired returns. It has the accomplishment

with the usage of the proper reviewing and feedback(Martina, 2020).

This review is again measured in some circumstances to check that the working

procedure is in the correct form or not. It is also helpful for the company to stay with

these kind of operations or wind up all the unnecessary activities. If somewhere, remedial

action happens the task can be continue in nature and control over them.

Decision-Making: It is the procedure of choosing one option from various alternatives

with the highly beneficial, competitive advantage and also social responsible.

Organisations are also doing the same while chosen of some important judgement in the

system for maintaining the specific day-to-day activity along with future perspective.

This process of working is the most important assets for the overall organization

(Rugman, 2019).

decision-making within an organisation.

Managerial accountancy is the process of collection, formative, measurement, modify

and transmission the financial activity of the firm to explicate the organisational placement and

objectives. Company is also represents the important facets to the top executives, stakeholders

and shareholders for the purpose of transparency in the organization. They are aiming for the

informatory estimation in return of fruitful outcome. This has engagement of only the internal

individuals not the externals. Enterprise is doing customization of structure for the useful usage

of the statements.

Importance of management accounting:

Planning: In the system, company uses the collected data for the development of the

particular objectives and preparing strategical plan for the future orientation. It is also

important that all the information should be knowledgeable, properly maintained and

having maximize utilization of resources like budgets (Opute and Madichie, 2017). This

budgeting processing is also helpful for executives by providing the estimate effects of

the ability to achieve desired goals.

Controlling: It is the monitoring, measuring and evaluating the actual outcomes of the

enterprises to manage the fulfilment of the desired returns. It has the accomplishment

with the usage of the proper reviewing and feedback(Martina, 2020).

This review is again measured in some circumstances to check that the working

procedure is in the correct form or not. It is also helpful for the company to stay with

these kind of operations or wind up all the unnecessary activities. If somewhere, remedial

action happens the task can be continue in nature and control over them.

Decision-Making: It is the procedure of choosing one option from various alternatives

with the highly beneficial, competitive advantage and also social responsible.

Organisations are also doing the same while chosen of some important judgement in the

system for maintaining the specific day-to-day activity along with future perspective.

This process of working is the most important assets for the overall organization

(Rugman, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

→ Thus, it is the technique through which company can plan, decide and controllability

over them to analyse and satisfy with the functionality.

CONCLUSION

It is concluded that firm is functioning in the linkage of finance as well as economies. By

doing this, they have coverage and excellent power to acknowledge about the overall financial

and economic scenario. This comes with lots of theories and concepts to observe the exact

situation within the organization.

over them to analyse and satisfy with the functionality.

CONCLUSION

It is concluded that firm is functioning in the linkage of finance as well as economies. By

doing this, they have coverage and excellent power to acknowledge about the overall financial

and economic scenario. This comes with lots of theories and concepts to observe the exact

situation within the organization.

REFERENCES

Books and Journals

Aisy, H.R., Mulyono, I. and Susilowati, K.D.S., 2017. Compilation of Financial Statements and

Financial Analysis for Non Profit Organizations. Jurnal Mahasiswa Akuntansi

Manajemen. 3(1).

Arnold, V., 2018. The changing technological environment and the future of behavioural

research in accounting. Accounting & Finance. 58(2). pp.315-339.

Atems, B. and Shand, G., 2018. An empirical analysis of the relationship between

entrepreneurship and income inequality. Small Business Economics. 51(4). pp.905-922.

Bikfalvi, A., 2017. History and conceptual developments in vascular biology and angiogenesis

research: a personal view. Angiogenesis. 20(4). pp.463-478.

Birch, K., 2017. Financing technoscience: Finance, assetization and rentiership. In The

Routledge handbook of the political economy of science. (pp. 169-181). Routledge.

Borg, A., 2019. Financial statements .(2017 and 2018).

Cruz, C. and Miranda, E., 2021. Damping ratios of the first mode for the seismic analysis of

buildings. Journal of Structural Engineering. 147(1). p.04020300.

Douarin, E. and Havrylyshyn, O. eds., 2021. The Palgrave Handbook of Comparative

Economics. Springer Nature.

Falcone, P.M., 2020. Environmental regulation and green investments: The role of green

finance. International Journal of Green Economics. 14(2). pp.159-173.

Grossmann, A., Mooney, L. and Dugan, M., 2019. Inclusion fairness in accounting, finance, and

management: An investigation of A-star publications on the ABDC journal list. Journal

of Business Research. 95. pp.232-241.

Macellari, M. and et. al., 2021. Exploring bluewashing practices of alleged sustainability leaders

through a counter-accounting analysis. Environmental Impact Assessment Review. 86.

p.106489.

Manzur, M., 2018. Exchange rate economics is always and everywhere controversial. Applied

Economics. 50(3). pp.216-232.

Martina, R.A., 2020. Toward a theory of affordable loss. Small Business Economics. 54(3).

McGaughy, K. and Reza, M.T., 2018. Recovery of macro and micro-nutrients by hydrothermal

carbonization of septage. Journal of agricultural and food chemistry. 66(8). pp.1854-

1862.

Modell, S., 2020. Accounting for institutional work: a critical review. European Accounting

Review. pp.1-26.

Opute, A.P. and Madichie, N.O., 2017. Accounting-marketing integration dimensions and

antecedents: insights from a frontier market. Journal of Business & Industrial

Marketing.

Rugman, A.M., 2019. From globalisation to regionalism: The foreign direct investment

dimension of international finance. In Shaping a new international financial system.

(pp. 203-219). Routledge.

Wang, Z. and et. al., 2020. Evaluation of the effects of Hg/DOC ratios on the reduction of Hg

(II) in lake water. Chemosphere. 253. p.126634.

Books and Journals

Aisy, H.R., Mulyono, I. and Susilowati, K.D.S., 2017. Compilation of Financial Statements and

Financial Analysis for Non Profit Organizations. Jurnal Mahasiswa Akuntansi

Manajemen. 3(1).

Arnold, V., 2018. The changing technological environment and the future of behavioural

research in accounting. Accounting & Finance. 58(2). pp.315-339.

Atems, B. and Shand, G., 2018. An empirical analysis of the relationship between

entrepreneurship and income inequality. Small Business Economics. 51(4). pp.905-922.

Bikfalvi, A., 2017. History and conceptual developments in vascular biology and angiogenesis

research: a personal view. Angiogenesis. 20(4). pp.463-478.

Birch, K., 2017. Financing technoscience: Finance, assetization and rentiership. In The

Routledge handbook of the political economy of science. (pp. 169-181). Routledge.

Borg, A., 2019. Financial statements .(2017 and 2018).

Cruz, C. and Miranda, E., 2021. Damping ratios of the first mode for the seismic analysis of

buildings. Journal of Structural Engineering. 147(1). p.04020300.

Douarin, E. and Havrylyshyn, O. eds., 2021. The Palgrave Handbook of Comparative

Economics. Springer Nature.

Falcone, P.M., 2020. Environmental regulation and green investments: The role of green

finance. International Journal of Green Economics. 14(2). pp.159-173.

Grossmann, A., Mooney, L. and Dugan, M., 2019. Inclusion fairness in accounting, finance, and

management: An investigation of A-star publications on the ABDC journal list. Journal

of Business Research. 95. pp.232-241.

Macellari, M. and et. al., 2021. Exploring bluewashing practices of alleged sustainability leaders

through a counter-accounting analysis. Environmental Impact Assessment Review. 86.

p.106489.

Manzur, M., 2018. Exchange rate economics is always and everywhere controversial. Applied

Economics. 50(3). pp.216-232.

Martina, R.A., 2020. Toward a theory of affordable loss. Small Business Economics. 54(3).

McGaughy, K. and Reza, M.T., 2018. Recovery of macro and micro-nutrients by hydrothermal

carbonization of septage. Journal of agricultural and food chemistry. 66(8). pp.1854-

1862.

Modell, S., 2020. Accounting for institutional work: a critical review. European Accounting

Review. pp.1-26.

Opute, A.P. and Madichie, N.O., 2017. Accounting-marketing integration dimensions and

antecedents: insights from a frontier market. Journal of Business & Industrial

Marketing.

Rugman, A.M., 2019. From globalisation to regionalism: The foreign direct investment

dimension of international finance. In Shaping a new international financial system.

(pp. 203-219). Routledge.

Wang, Z. and et. al., 2020. Evaluation of the effects of Hg/DOC ratios on the reduction of Hg

(II) in lake water. Chemosphere. 253. p.126634.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.