Applied Business Finance: Financial Performance Analysis and Review

VerifiedAdded on 2022/11/30

|9

|2616

|174

Homework Assignment

AI Summary

This finance assignment provides a comprehensive analysis of a business's financial performance. It begins with an introduction to financial management, emphasizing its importance in optimizing resource allocation and ensuring business sustainability. The assignment then delves into the core financial statements: the balance sheet, income statement, and cash flow statement, explaining their significance in assessing a company's financial health. Ratio analysis is highlighted as a crucial tool for interpreting financial data, enabling comparisons across periods and with competitors. The assignment includes a business review template, calculating key financial metrics such as profit, shareholder's equity, and various ratios, and then proceeds to analyze the company's profitability, liquidity, and efficiency based on provided financial data. The analysis reveals the company's strengths and weaknesses, particularly in liquidity and efficiency, and suggests strategies to improve its performance. These strategies include better management of expenses, negotiation with creditors and debtors, and optimizing asset utilization to enhance financial stability and achieve better financial outcomes.

APPLIED BUSINESS

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section: 1

INTRODUCTION

Financial management is one of the most important function that has been performed within

every businesses which involves an acquisition of finance for the business at a minimum possible

costs, utilizing the same in an optimized way in order to run the operations of the business in a

smooth way (Nso, 2018). Financial management is done in any business to ensure that the

returns derived from the acquired finance should be greater than the cost paid for the acquisition

of funds. Also, it aims to ensure that at any point of time there should be sufficient funds

available with the company, so that operations of the company should not be in any ways got

hindered.

“Financial management can be defined as the activity of business management aimed to ensure

judicious utilization of capital by selecting the correct and efficient sources of finance to raise

sufficient amount of funds to allow an entity to reach its goals and objectives.”

There are certain importance of financial management such as:

It helps in ensuring adequate and regular injection of funds in to the business.

It helps in wealth maximization of the shareholders of the company by facilitating higher

earnings, better performance of the company in the stock market and keeping the

expectations of shareholders as a core objective of the company (Le, 2019).

It allows for reaping maximum benefits out of the funds so procured at a least possible

costs.

It helps in designing appropriate capital structure for the company and ensures that the

funds has been invested in safest possible ventures.

Section: 2

Main financial statements

Financial statements are financial reports prepared with the aim to detail a company’s financial

performance through the provision of information of financial nature such as, expenses, incomes,

liabilities, assets, equities and cash flows pertaining to the specified period of time (Shapiro and

Hanouna, 2019). The three major and important financial statements of any entity are the income

INTRODUCTION

Financial management is one of the most important function that has been performed within

every businesses which involves an acquisition of finance for the business at a minimum possible

costs, utilizing the same in an optimized way in order to run the operations of the business in a

smooth way (Nso, 2018). Financial management is done in any business to ensure that the

returns derived from the acquired finance should be greater than the cost paid for the acquisition

of funds. Also, it aims to ensure that at any point of time there should be sufficient funds

available with the company, so that operations of the company should not be in any ways got

hindered.

“Financial management can be defined as the activity of business management aimed to ensure

judicious utilization of capital by selecting the correct and efficient sources of finance to raise

sufficient amount of funds to allow an entity to reach its goals and objectives.”

There are certain importance of financial management such as:

It helps in ensuring adequate and regular injection of funds in to the business.

It helps in wealth maximization of the shareholders of the company by facilitating higher

earnings, better performance of the company in the stock market and keeping the

expectations of shareholders as a core objective of the company (Le, 2019).

It allows for reaping maximum benefits out of the funds so procured at a least possible

costs.

It helps in designing appropriate capital structure for the company and ensures that the

funds has been invested in safest possible ventures.

Section: 2

Main financial statements

Financial statements are financial reports prepared with the aim to detail a company’s financial

performance through the provision of information of financial nature such as, expenses, incomes,

liabilities, assets, equities and cash flows pertaining to the specified period of time (Shapiro and

Hanouna, 2019). The three major and important financial statements of any entity are the income

statement, the balance sheet and the cash flow statement. The information obtained through

financial statements are taken as a base of corporate accounting. The brief description of these

three main financial statement are as follows:

Balance sheet: It is also known as the statement of financial position in which all the assets held

by the company, outstanding liabilities and equities of the company are stated in a structured

way. From this statement, company’s valuation can be done as per its book value of assets and

liabilities held. It gives the user of accounting information a quick view of the company’s

financial position.

Income statement: It is the proforma which indicates the income earned by the company through

its operations and related expenses incurred to facilitate business operations (Brigham and

Houston, 2021). This statement is generally referred to by the investors for identifying the

financial performance of the business during a particular time period. It indicates how much

profitable a business is for the purpose of making an investment. It indicates how revenue has

been generated by listing out all the operating and non-operating expenses.

Cash flow statement: It is another most important financial statement of a business which

indicates the movement of cash flows from and into the business by listing all the particulars of

cash inflows and cash outflows (Okanazu, 2018). It lists out all the cash transactions undertaken

by the company during the given time period and thus shows its liquidity position. And at the

end of the statement, the available cash balances with the company has also been stated.

Hence, the above mentioned all the three financial statements of a company are core to the

analysis of performance of a company from each and every different angles.

Use of ratio in financial management

Calculation of financial ratios is considered to be a very most important part of financial

management. Ratios are meant for studying the relationship between different components of

financial statements of a company (Podger and de Jong, 2019). While comparing a company’s

financial performance between two or more different periods or between the company and its

various competitors, ratios are greatly resorted to by the management and investors. Follow up

with the performance of the company and identifying signs that may cause trouble for the

company in future at an earliest possible way can be possible through ratio calculation. To study

financial statements are taken as a base of corporate accounting. The brief description of these

three main financial statement are as follows:

Balance sheet: It is also known as the statement of financial position in which all the assets held

by the company, outstanding liabilities and equities of the company are stated in a structured

way. From this statement, company’s valuation can be done as per its book value of assets and

liabilities held. It gives the user of accounting information a quick view of the company’s

financial position.

Income statement: It is the proforma which indicates the income earned by the company through

its operations and related expenses incurred to facilitate business operations (Brigham and

Houston, 2021). This statement is generally referred to by the investors for identifying the

financial performance of the business during a particular time period. It indicates how much

profitable a business is for the purpose of making an investment. It indicates how revenue has

been generated by listing out all the operating and non-operating expenses.

Cash flow statement: It is another most important financial statement of a business which

indicates the movement of cash flows from and into the business by listing all the particulars of

cash inflows and cash outflows (Okanazu, 2018). It lists out all the cash transactions undertaken

by the company during the given time period and thus shows its liquidity position. And at the

end of the statement, the available cash balances with the company has also been stated.

Hence, the above mentioned all the three financial statements of a company are core to the

analysis of performance of a company from each and every different angles.

Use of ratio in financial management

Calculation of financial ratios is considered to be a very most important part of financial

management. Ratios are meant for studying the relationship between different components of

financial statements of a company (Podger and de Jong, 2019). While comparing a company’s

financial performance between two or more different periods or between the company and its

various competitors, ratios are greatly resorted to by the management and investors. Follow up

with the performance of the company and identifying signs that may cause trouble for the

company in future at an earliest possible way can be possible through ratio calculation. To study

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the trend in the performance of the company is what is facilitated through ratios. Also, with the

help of ratios, management can be able to determine overall operational efficiency of a business

and can make policy changes and corrective measures according to it (Kanter and Siagian, 2017).

So, the concern of financial management like increasing profitability and adopting an optimum

capital structure for the company can be make sure through the use of ratio analysis which

provides guidance to the financial manager in making financial decision for the company.

Section: 3

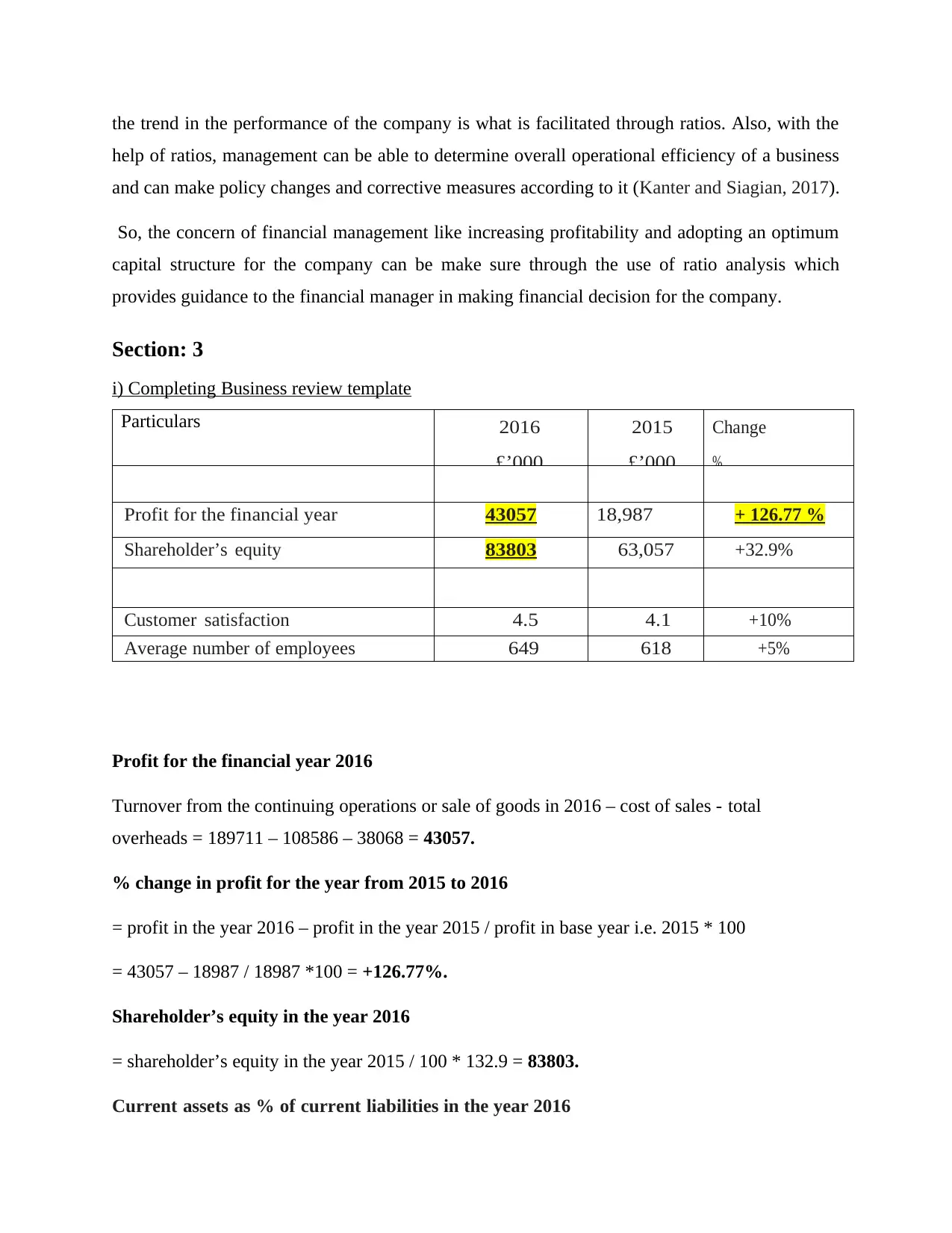

i) Completing Business review template

Particulars 2016

£’000

2015

£’000

Change

%

Profit for the financial year 43057 18,987 + 126.77 %

Shareholder’s equity 83803 63,057 +32.9%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

Profit for the financial year 2016

Turnover from the continuing operations or sale of goods in 2016 – cost of sales - total

overheads = 189711 – 108586 – 38068 = 43057.

% change in profit for the year from 2015 to 2016

= profit in the year 2016 – profit in the year 2015 / profit in base year i.e. 2015 * 100

= 43057 – 18987 / 18987 *100 = +126.77%.

Shareholder’s equity in the year 2016

= shareholder’s equity in the year 2015 / 100 * 132.9 = 83803.

Current assets as % of current liabilities in the year 2016

help of ratios, management can be able to determine overall operational efficiency of a business

and can make policy changes and corrective measures according to it (Kanter and Siagian, 2017).

So, the concern of financial management like increasing profitability and adopting an optimum

capital structure for the company can be make sure through the use of ratio analysis which

provides guidance to the financial manager in making financial decision for the company.

Section: 3

i) Completing Business review template

Particulars 2016

£’000

2015

£’000

Change

%

Profit for the financial year 43057 18,987 + 126.77 %

Shareholder’s equity 83803 63,057 +32.9%

Customer satisfaction 4.5 4.1 +10%

Average number of employees 649 618 +5%

Profit for the financial year 2016

Turnover from the continuing operations or sale of goods in 2016 – cost of sales - total

overheads = 189711 – 108586 – 38068 = 43057.

% change in profit for the year from 2015 to 2016

= profit in the year 2016 – profit in the year 2015 / profit in base year i.e. 2015 * 100

= 43057 – 18987 / 18987 *100 = +126.77%.

Shareholder’s equity in the year 2016

= shareholder’s equity in the year 2015 / 100 * 132.9 = 83803.

Current assets as % of current liabilities in the year 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

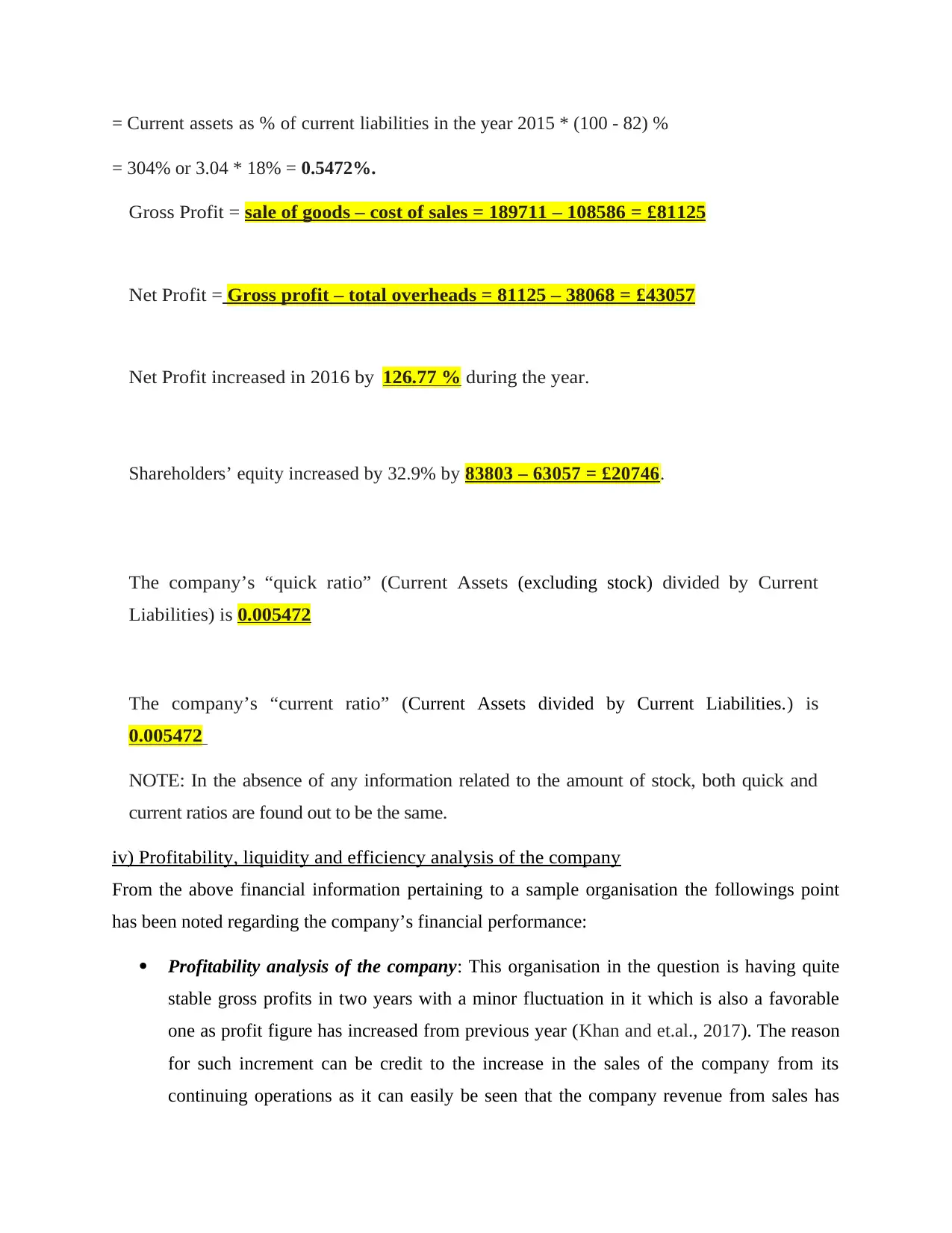

= Current assets as % of current liabilities in the year 2015 * (100 - 82) %

= 304% or 3.04 * 18% = 0.5472%.

Gross Profit = sale of goods – cost of sales = 189711 – 108586 = £ 81125

Net Profit = Gross profit – total overheads = 81125 – 38068 = £ 43057

Net Profit increased in 2016 by 126.77 % during the year.

Shareholders’ equity increased by 32.9% by 83803 – 63057 = £20746.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current

Liabilities) is 0.005472

The company’s “current ratio” (Current Assets divided by Current Liabilities. ) is

0.005472

NOTE: In the absence of any information related to the amount of stock, both quick and

current ratios are found out to be the same.

iv) Profitability, liquidity and efficiency analysis of the company

From the above financial information pertaining to a sample organisation the followings point

has been noted regarding the company’s financial performance:

Profitability analysis of the company: This organisation in the question is having quite

stable gross profits in two years with a minor fluctuation in it which is also a favorable

one as profit figure has increased from previous year (Khan and et.al., 2017). The reason

for such increment can be credit to the increase in the sales of the company from its

continuing operations as it can easily be seen that the company revenue from sales has

= 304% or 3.04 * 18% = 0.5472%.

Gross Profit = sale of goods – cost of sales = 189711 – 108586 = £ 81125

Net Profit = Gross profit – total overheads = 81125 – 38068 = £ 43057

Net Profit increased in 2016 by 126.77 % during the year.

Shareholders’ equity increased by 32.9% by 83803 – 63057 = £20746.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current

Liabilities) is 0.005472

The company’s “current ratio” (Current Assets divided by Current Liabilities. ) is

0.005472

NOTE: In the absence of any information related to the amount of stock, both quick and

current ratios are found out to be the same.

iv) Profitability, liquidity and efficiency analysis of the company

From the above financial information pertaining to a sample organisation the followings point

has been noted regarding the company’s financial performance:

Profitability analysis of the company: This organisation in the question is having quite

stable gross profits in two years with a minor fluctuation in it which is also a favorable

one as profit figure has increased from previous year (Khan and et.al., 2017). The reason

for such increment can be credit to the increase in the sales of the company from its

continuing operations as it can easily be seen that the company revenue from sales has

improved compared to previous year. But looking at the company’s net profit figure it

has been noticed that the company’s net profit has increased to a great extent from

previous in current year (Brigham and Houston, 2021). And the reason of such an

increase in profit is just due to the reduction in overhead costs or operating costs and non

– operating cost that is the interest amount of the company in the year 2016 compared

2015.

Liquidity analysis of the company: Companies liquidity can be well explained through

its current and quick ratios which indicates a severe fall from the previous year. The ratio

such as current ratio which indicates how much current assets a company have with it in

order to meet its obligations towards the business’s outstanding current liability which is

going to rise in the a small period of one year (Nso, 2018). And for the same, company

must have an enough liquidized assets to meet up the same. But here the company’s

liquidity position in the case study has got much worse than the previous year where the

company is having much higher balance in its current assets in the previous year which is

actually not required against the company’s current liabilities balance at that time. Such

situation leads to forego those income which can be earned by company by the investing

the idle current assets into some profitable avenue rather than just keeping it as a current

assets in the business. On the other hand, company’s liquidity position is very

unsatisfactory in the current year as the same has declined by 82% compared to what is

was in the previous year (Shapiro and Hanouna, 2019). And such a great declination has

results in much lower liquidity for the company in the current year as its balance of

current assets is much lower than its current liabilities. The ratio is much below 1,

indicating inability of the company in meeting its short term obligations which will be

going to arise soon or within a year.

Efficiency analysis of the company: efficiency from the given information can be seen

from reduced level of various costs of the company that is, it’s both operating and non –

operating costs (interest) has reduced to a great extent compared to the previous year

where these are quite high (Khan and et.al., 2017). The reduced cost of operations has

provided for company to earn greater profits as is happened in the case study where the

company’s net profit has been improved in a much noticeable way. So, it can be said that

the company has been successful in improving its overall efficiency than previous year.

has been noticed that the company’s net profit has increased to a great extent from

previous in current year (Brigham and Houston, 2021). And the reason of such an

increase in profit is just due to the reduction in overhead costs or operating costs and non

– operating cost that is the interest amount of the company in the year 2016 compared

2015.

Liquidity analysis of the company: Companies liquidity can be well explained through

its current and quick ratios which indicates a severe fall from the previous year. The ratio

such as current ratio which indicates how much current assets a company have with it in

order to meet its obligations towards the business’s outstanding current liability which is

going to rise in the a small period of one year (Nso, 2018). And for the same, company

must have an enough liquidized assets to meet up the same. But here the company’s

liquidity position in the case study has got much worse than the previous year where the

company is having much higher balance in its current assets in the previous year which is

actually not required against the company’s current liabilities balance at that time. Such

situation leads to forego those income which can be earned by company by the investing

the idle current assets into some profitable avenue rather than just keeping it as a current

assets in the business. On the other hand, company’s liquidity position is very

unsatisfactory in the current year as the same has declined by 82% compared to what is

was in the previous year (Shapiro and Hanouna, 2019). And such a great declination has

results in much lower liquidity for the company in the current year as its balance of

current assets is much lower than its current liabilities. The ratio is much below 1,

indicating inability of the company in meeting its short term obligations which will be

going to arise soon or within a year.

Efficiency analysis of the company: efficiency from the given information can be seen

from reduced level of various costs of the company that is, it’s both operating and non –

operating costs (interest) has reduced to a great extent compared to the previous year

where these are quite high (Khan and et.al., 2017). The reduced cost of operations has

provided for company to earn greater profits as is happened in the case study where the

company’s net profit has been improved in a much noticeable way. So, it can be said that

the company has been successful in improving its overall efficiency than previous year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Its customer satisfaction has been improved which can be said that it was due to the

reduction in the company’s costs at a considerable rate, thus indicating improvement in

efficiency of the company.

Section: 4

Process used by the business to improvise its performance

This business has much poor liquidity position which can be improved by reducing their

overhead expenses, negotiating better terms with the creditors and debtors to manage

liquidity of the business in the best possible manner (Okanazu, 2018). This is because if

creditors will give sufficient time for making payment then business will be able to

manage with less working capital and thus will require less liquid assets for any kind of

immediate payments. In the same way by allowing discounts and offers to debtors,

businesses can avail stuck liquidity in a timely manner, thus may not require to avail any

form of external support for obtaining funds for running their day to day operations of the

business. Also, cutting off of unnecessary overheads always proved to be helpful in

saving enough liquidity and therefore will lead to retention of cash balances with the

business and accordingly current and quick ratios can be improved to a great extent

(Podger and de Jong, 2019).

By selling out unnecessary assets of the business, it is possible to get more of own capital

that can be invested in the business at free of cost rather than depending upon external

sources of finance which incur costs for the business in terms of interest payments.

Through this liquidity can also be obtained if it is below the required level and also

saving of liquidity can be possible through liberation from interest charges which is

required to be paid on a regular basis.

Attracting more sales through reducing prices if there is high level of competition

prevailing in the market, so that at a reduced price more of the customers can be attracted

towards buying from a particular company over the others (Kanter and Siagian, 2017).

While on the other hand, higher prices should be charged by the business if it is facing

rising cost of operations and market price level allows for enough scope for raising the

prices of products of the company. This both of the situations will lead to more

generation of profits and accordingly financial performance of the business can be

improved to a great extent.

reduction in the company’s costs at a considerable rate, thus indicating improvement in

efficiency of the company.

Section: 4

Process used by the business to improvise its performance

This business has much poor liquidity position which can be improved by reducing their

overhead expenses, negotiating better terms with the creditors and debtors to manage

liquidity of the business in the best possible manner (Okanazu, 2018). This is because if

creditors will give sufficient time for making payment then business will be able to

manage with less working capital and thus will require less liquid assets for any kind of

immediate payments. In the same way by allowing discounts and offers to debtors,

businesses can avail stuck liquidity in a timely manner, thus may not require to avail any

form of external support for obtaining funds for running their day to day operations of the

business. Also, cutting off of unnecessary overheads always proved to be helpful in

saving enough liquidity and therefore will lead to retention of cash balances with the

business and accordingly current and quick ratios can be improved to a great extent

(Podger and de Jong, 2019).

By selling out unnecessary assets of the business, it is possible to get more of own capital

that can be invested in the business at free of cost rather than depending upon external

sources of finance which incur costs for the business in terms of interest payments.

Through this liquidity can also be obtained if it is below the required level and also

saving of liquidity can be possible through liberation from interest charges which is

required to be paid on a regular basis.

Attracting more sales through reducing prices if there is high level of competition

prevailing in the market, so that at a reduced price more of the customers can be attracted

towards buying from a particular company over the others (Kanter and Siagian, 2017).

While on the other hand, higher prices should be charged by the business if it is facing

rising cost of operations and market price level allows for enough scope for raising the

prices of products of the company. This both of the situations will lead to more

generation of profits and accordingly financial performance of the business can be

improved to a great extent.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Investing own money against debt capital will allow business to make saving of the

sufficient liquidity that is going to flow out of the business on a regular basis between

similar intervals of time (Le, 2019). Saving costs in terms of interest charges helps in

reducing financial risks and enhancing liquidity of the business.

Section: 5

REFERENCES

Nso, M. A., 2018. Cash management techniques and the relationship between cash

management and profitability of micro-finance institutions. International Journal of

Economics, Commerce and Management, 6(5), pp.468-481.

Le, B., 2019. Working capital management and firm’s valuation, profitability and

risk. International Journal of Managerial Finance.

Shapiro, A. C. and Hanouna, P., 2019. Multinational financial management. John Wiley &

Sons.

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management. Cengage

Learning.

Okanazu, O. O., 2018. Financial management decision practices for ensuring business

solvency by small and medium scale enterprises. Acta Oeconomica Universitatis

Selye, 7(2), pp.109-121.

Podger, A. and de Jong, M., 2019. The evolution of performance budgeting amidst other

public financial management reforms. Performance Budgeting Reform: Theories and

International Practices.

Kanter, A. B. and Siagian, J., 2017. The Effects of Financial Performance towards Investment

Return. Fundamental Management Journal, 2(2), pp.17-26.

Khan, M. K., and et.al., 2017. Determinants of financial performance of financial sectors (An

assessment through economic value added).

sufficient liquidity that is going to flow out of the business on a regular basis between

similar intervals of time (Le, 2019). Saving costs in terms of interest charges helps in

reducing financial risks and enhancing liquidity of the business.

Section: 5

REFERENCES

Nso, M. A., 2018. Cash management techniques and the relationship between cash

management and profitability of micro-finance institutions. International Journal of

Economics, Commerce and Management, 6(5), pp.468-481.

Le, B., 2019. Working capital management and firm’s valuation, profitability and

risk. International Journal of Managerial Finance.

Shapiro, A. C. and Hanouna, P., 2019. Multinational financial management. John Wiley &

Sons.

Brigham, E. F. and Houston, J. F., 2021. Fundamentals of financial management. Cengage

Learning.

Okanazu, O. O., 2018. Financial management decision practices for ensuring business

solvency by small and medium scale enterprises. Acta Oeconomica Universitatis

Selye, 7(2), pp.109-121.

Podger, A. and de Jong, M., 2019. The evolution of performance budgeting amidst other

public financial management reforms. Performance Budgeting Reform: Theories and

International Practices.

Kanter, A. B. and Siagian, J., 2017. The Effects of Financial Performance towards Investment

Return. Fundamental Management Journal, 2(2), pp.17-26.

Khan, M. K., and et.al., 2017. Determinants of financial performance of financial sectors (An

assessment through economic value added).

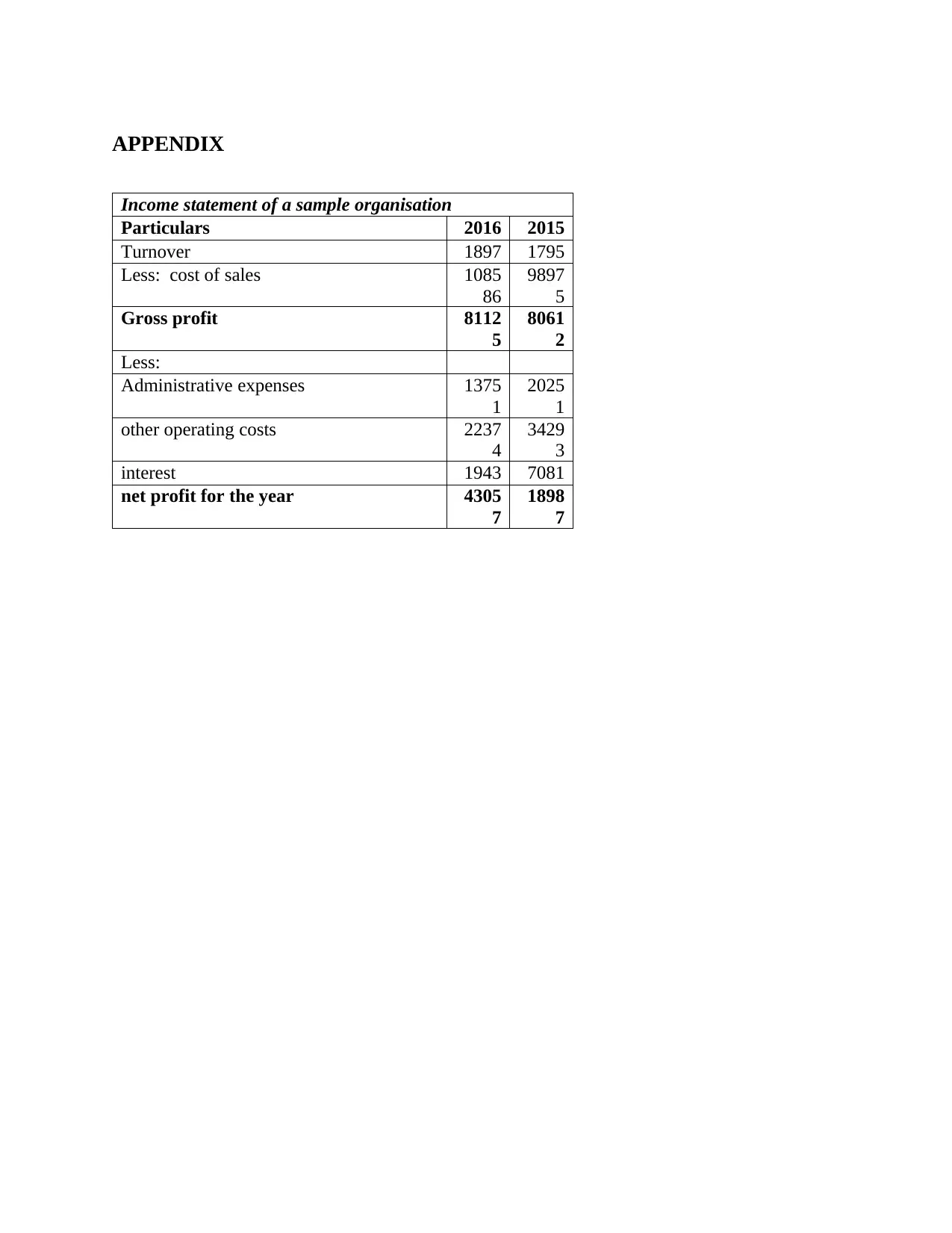

APPENDIX

Income statement of a sample organisation

Particulars 2016 2015

Turnover 1897

11

1795

87Less: cost of sales 1085

86

9897

5

Gross profit 8112

5

8061

2

Less:

Administrative expenses 1375

1

2025

1

other operating costs 2237

4

3429

3

interest 1943 7081

net profit for the year 4305

7

1898

7

Income statement of a sample organisation

Particulars 2016 2015

Turnover 1897

11

1795

87Less: cost of sales 1085

86

9897

5

Gross profit 8112

5

8061

2

Less:

Administrative expenses 1375

1

2025

1

other operating costs 2237

4

3429

3

interest 1943 7081

net profit for the year 4305

7

1898

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.