Business Finance Report: Analysis of T-shirts Ltd Performance

VerifiedAdded on 2023/01/05

|12

|3367

|411

Report

AI Summary

This report provides a comprehensive analysis of the financial performance of T-shirts Ltd. The report begins with an analysis of the company's statement of profit or loss and statement of financial position using ratio analysis to assess liquidity, profitability, and efficiency. Key financial ratios such as current ratio, quick ratio, gross profit margin, net profit margin, and return on assets are examined to evaluate the company's performance in 2019 compared to 2018. The report then delves into the understanding of financial information, differentiating between accrual and cash accounting and exploring the relationship between profit and cash flow. The report also explains the meaning and purpose of budgeting within a business context. The analysis highlights the importance of financial management and the impact of various financial decisions on the company's overall health and performance. The conclusion emphasizes the importance of strategic planning and financial management for T-shirts Ltd to overcome its current financial challenges and improve its future performance.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1: BUSINESS PERFORMANCE ANALYSIS..............................................................3

1.1 Statement of Profit or Loss..............................................................................................3

1.2 Statement of Financial Position.......................................................................................4

PART 2: UNDERSTANDING FINANCIAL INFORMATION & MANAGEMENT OF

CASH.........................................................................................................................................6

2.1 Understanding the concept of accrual accounting vs cash accounting............................6

2.2 Meaning and differences between the profit and cash flow.............................................7

PART 3.......................................................................................................................................8

Meaning and purpose of budget.............................................................................................8

Benefits of forming limited company and registering on stock exchange.............................8

REFERENCES.........................................................................................................................10

APPENDIX..............................................................................................................................11

PART 1: BUSINESS PERFORMANCE ANALYSIS..............................................................3

1.1 Statement of Profit or Loss..............................................................................................3

1.2 Statement of Financial Position.......................................................................................4

PART 2: UNDERSTANDING FINANCIAL INFORMATION & MANAGEMENT OF

CASH.........................................................................................................................................6

2.1 Understanding the concept of accrual accounting vs cash accounting............................6

2.2 Meaning and differences between the profit and cash flow.............................................7

PART 3.......................................................................................................................................8

Meaning and purpose of budget.............................................................................................8

Benefits of forming limited company and registering on stock exchange.............................8

REFERENCES.........................................................................................................................10

APPENDIX..............................................................................................................................11

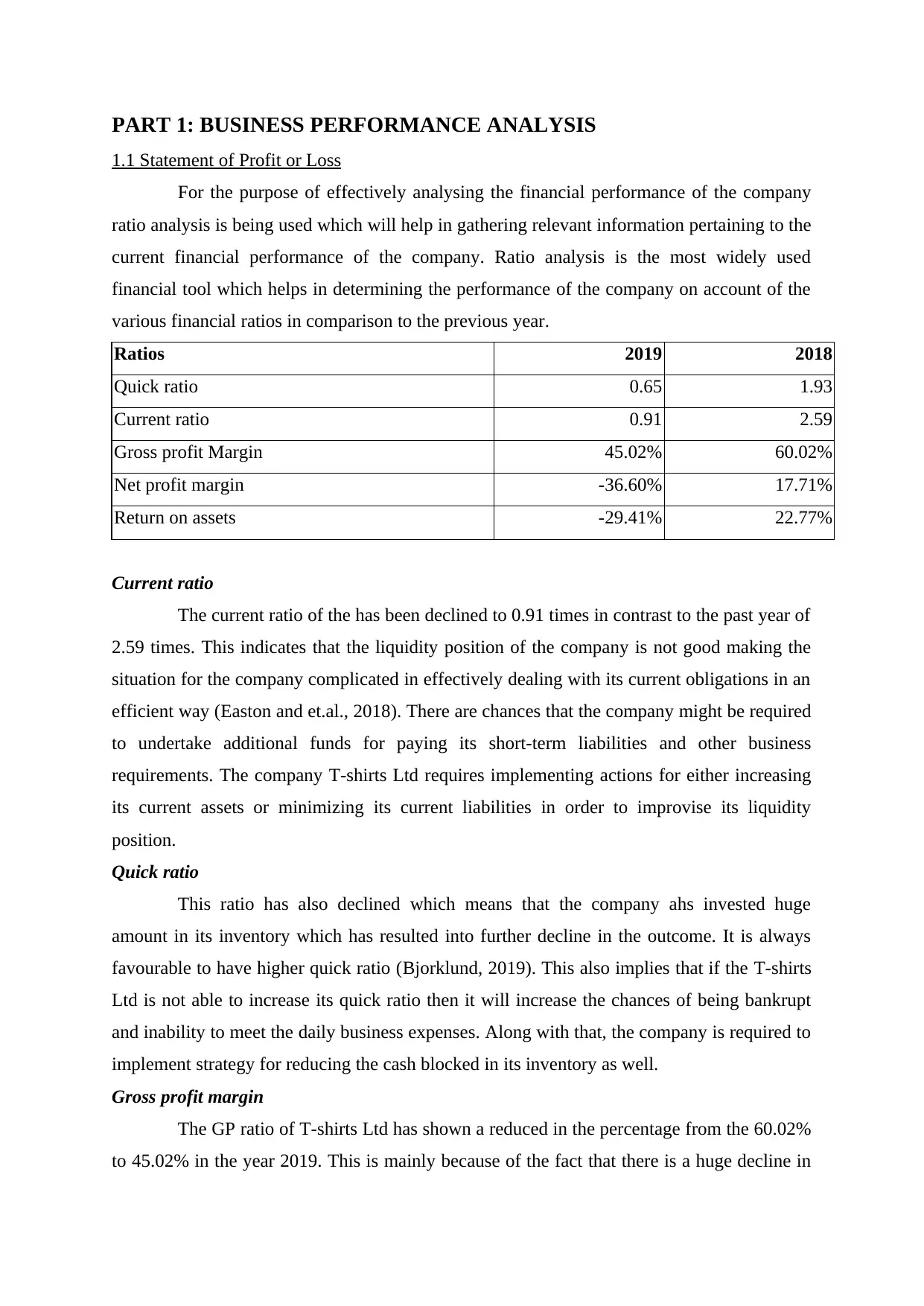

PART 1: BUSINESS PERFORMANCE ANALYSIS

1.1 Statement of Profit or Loss

For the purpose of effectively analysing the financial performance of the company

ratio analysis is being used which will help in gathering relevant information pertaining to the

current financial performance of the company. Ratio analysis is the most widely used

financial tool which helps in determining the performance of the company on account of the

various financial ratios in comparison to the previous year.

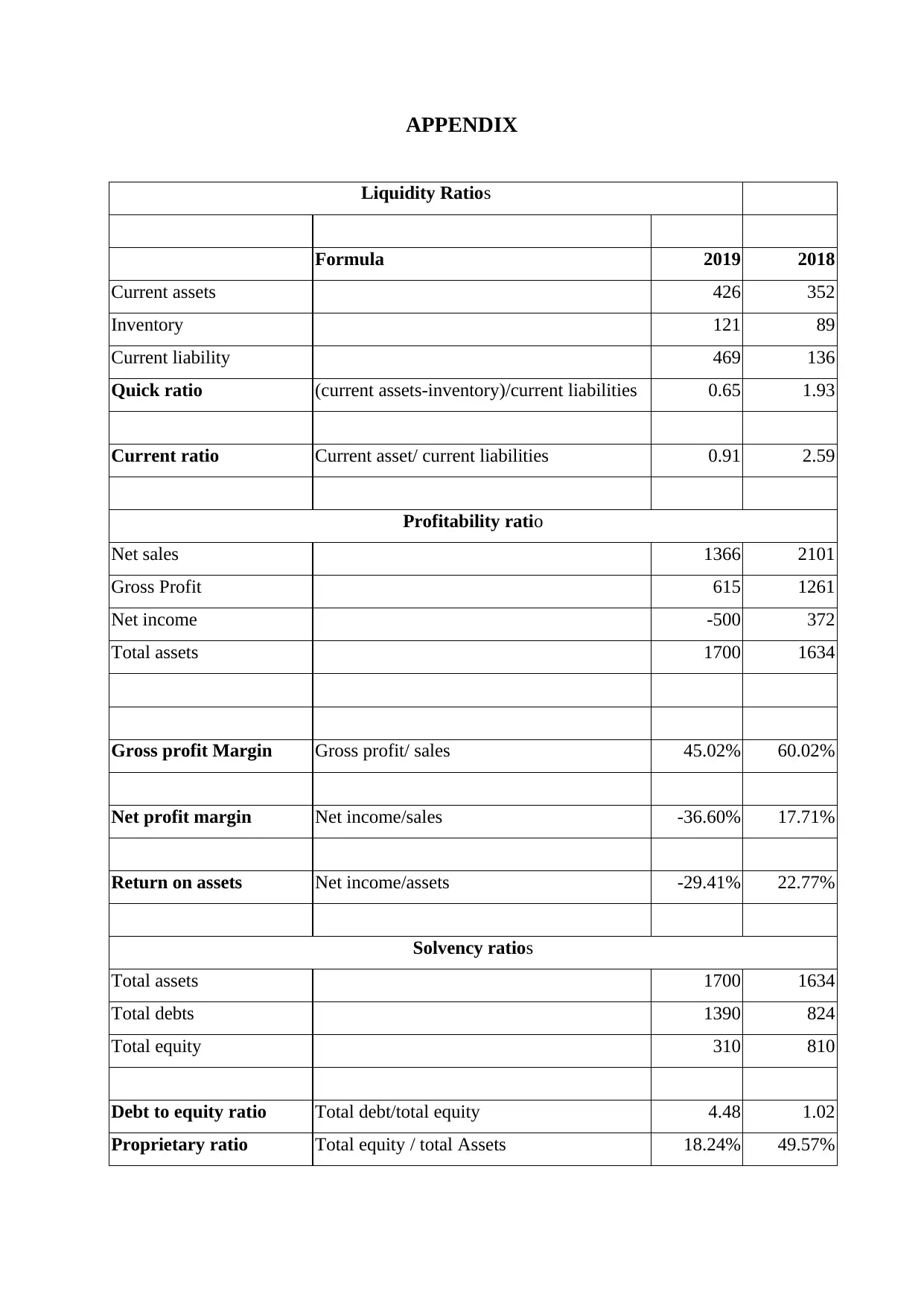

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

Gross profit Margin 45.02% 60.02%

Net profit margin -36.60% 17.71%

Return on assets -29.41% 22.77%

Current ratio

The current ratio of the has been declined to 0.91 times in contrast to the past year of

2.59 times. This indicates that the liquidity position of the company is not good making the

situation for the company complicated in effectively dealing with its current obligations in an

efficient way (Easton and et.al., 2018). There are chances that the company might be required

to undertake additional funds for paying its short-term liabilities and other business

requirements. The company T-shirts Ltd requires implementing actions for either increasing

its current assets or minimizing its current liabilities in order to improvise its liquidity

position.

Quick ratio

This ratio has also declined which means that the company ahs invested huge

amount in its inventory which has resulted into further decline in the outcome. It is always

favourable to have higher quick ratio (Bjorklund, 2019). This also implies that if the T-shirts

Ltd is not able to increase its quick ratio then it will increase the chances of being bankrupt

and inability to meet the daily business expenses. Along with that, the company is required to

implement strategy for reducing the cash blocked in its inventory as well.

Gross profit margin

The GP ratio of T-shirts Ltd has shown a reduced in the percentage from the 60.02%

to 45.02% in the year 2019. This is mainly because of the fact that there is a huge decline in

1.1 Statement of Profit or Loss

For the purpose of effectively analysing the financial performance of the company

ratio analysis is being used which will help in gathering relevant information pertaining to the

current financial performance of the company. Ratio analysis is the most widely used

financial tool which helps in determining the performance of the company on account of the

various financial ratios in comparison to the previous year.

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

Gross profit Margin 45.02% 60.02%

Net profit margin -36.60% 17.71%

Return on assets -29.41% 22.77%

Current ratio

The current ratio of the has been declined to 0.91 times in contrast to the past year of

2.59 times. This indicates that the liquidity position of the company is not good making the

situation for the company complicated in effectively dealing with its current obligations in an

efficient way (Easton and et.al., 2018). There are chances that the company might be required

to undertake additional funds for paying its short-term liabilities and other business

requirements. The company T-shirts Ltd requires implementing actions for either increasing

its current assets or minimizing its current liabilities in order to improvise its liquidity

position.

Quick ratio

This ratio has also declined which means that the company ahs invested huge

amount in its inventory which has resulted into further decline in the outcome. It is always

favourable to have higher quick ratio (Bjorklund, 2019). This also implies that if the T-shirts

Ltd is not able to increase its quick ratio then it will increase the chances of being bankrupt

and inability to meet the daily business expenses. Along with that, the company is required to

implement strategy for reducing the cash blocked in its inventory as well.

Gross profit margin

The GP ratio of T-shirts Ltd has shown a reduced in the percentage from the 60.02%

to 45.02% in the year 2019. This is mainly because of the fact that there is a huge decline in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the revenue of the company and this consequently results into decrease in the GP of T-shirts

Ltd. Therefore, the company requires come up with some new strategy in order to increase its

revenue and reducing the cost of sales as well. The company has already taken initiative for

improving its gross profit by changing its credit policy as from now on the company is

providing 60 days of credit to its debtors instead of 30 days which will result into increasing

the customer base.

Net profit margin

The ratio of NP margin has turned into negative from positive 17.71% to negative

36.60%. The core reason behind this is the decrease in GP along with increase in the

operating and non-operating expenses. Another important aspect is that there is an increase in

the interest liability of the company impacting the profits of the company. Therefore, in order

to effectively manage the business, it is important for the organization to decrease its costs

and other financial interest obligations.

Return on asset ratio

It can be clearly seen that the ROA of the company has shown a greater reduction in

the percentage. In the year 2018, it was 22.77% which decreased to -29.41%. This highlights

that the T-shirts Ltdis not effectively making use of its assets in gaining more revenue.

Therefore, the financial performance of the company is not sound enough (Firdaus and Endri,

2020). It becomes important for the company in effectively implementing the right strategy in

place as soon as possible in order to manage the business otherwise the situation can turn out

to be even worse.

1.2 Statement of Financial Position

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

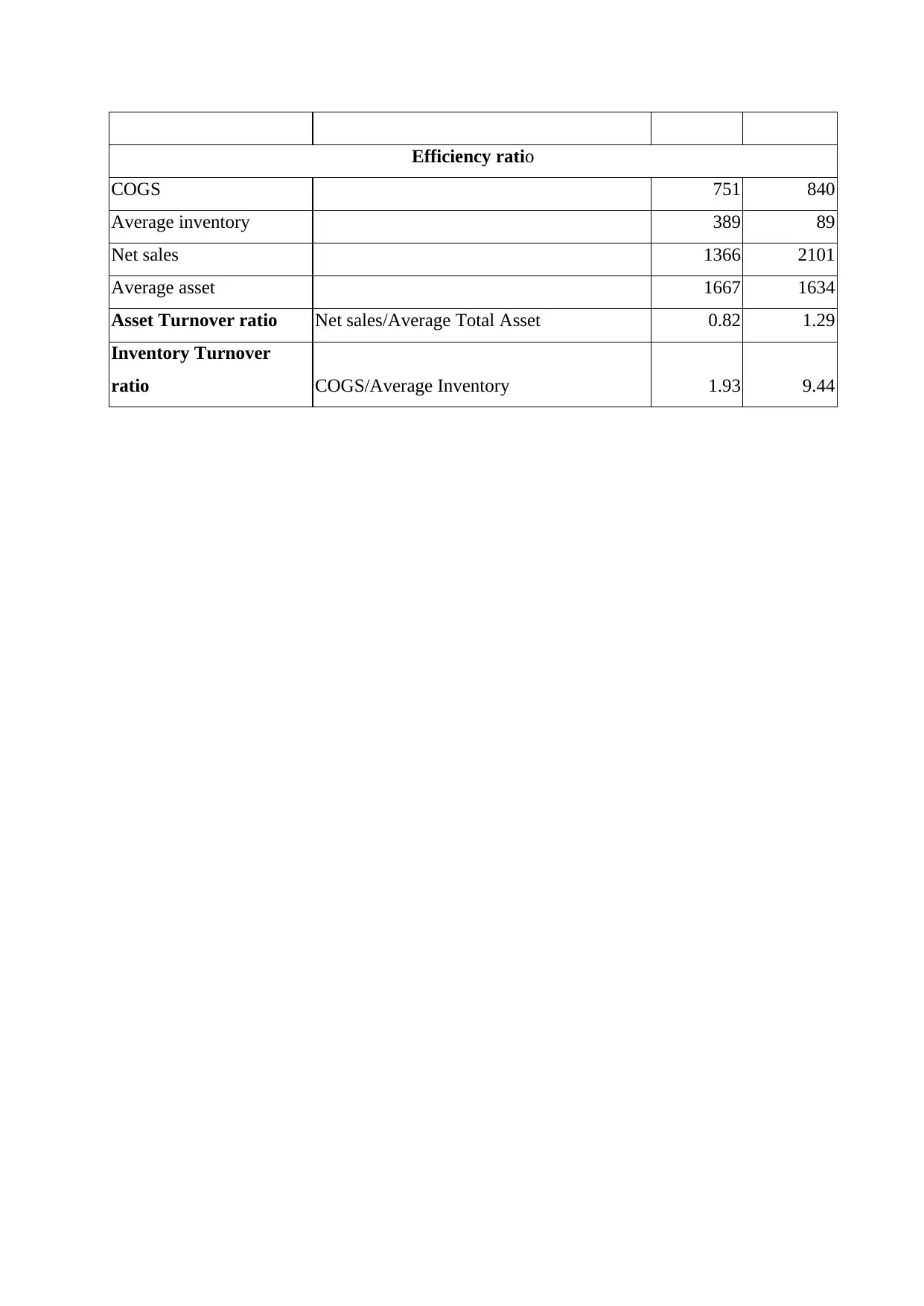

Asset Turnover ratio 0.82 1.29

Inventory Turnover ratio 1.93 9.44

Debt to equity ratio

The D/E ratio of the has been increase in the one-year time span as it was 1.02 in the

year 2018 which rise to 4.48 which means that most of the funding is done through the debt

element. This has resulted into increase in the risk factor for the business as it brings along

Ltd. Therefore, the company requires come up with some new strategy in order to increase its

revenue and reducing the cost of sales as well. The company has already taken initiative for

improving its gross profit by changing its credit policy as from now on the company is

providing 60 days of credit to its debtors instead of 30 days which will result into increasing

the customer base.

Net profit margin

The ratio of NP margin has turned into negative from positive 17.71% to negative

36.60%. The core reason behind this is the decrease in GP along with increase in the

operating and non-operating expenses. Another important aspect is that there is an increase in

the interest liability of the company impacting the profits of the company. Therefore, in order

to effectively manage the business, it is important for the organization to decrease its costs

and other financial interest obligations.

Return on asset ratio

It can be clearly seen that the ROA of the company has shown a greater reduction in

the percentage. In the year 2018, it was 22.77% which decreased to -29.41%. This highlights

that the T-shirts Ltdis not effectively making use of its assets in gaining more revenue.

Therefore, the financial performance of the company is not sound enough (Firdaus and Endri,

2020). It becomes important for the company in effectively implementing the right strategy in

place as soon as possible in order to manage the business otherwise the situation can turn out

to be even worse.

1.2 Statement of Financial Position

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

Asset Turnover ratio 0.82 1.29

Inventory Turnover ratio 1.93 9.44

Debt to equity ratio

The D/E ratio of the has been increase in the one-year time span as it was 1.02 in the

year 2018 which rise to 4.48 which means that most of the funding is done through the debt

element. This has resulted into increase in the risk factor for the business as it brings along

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

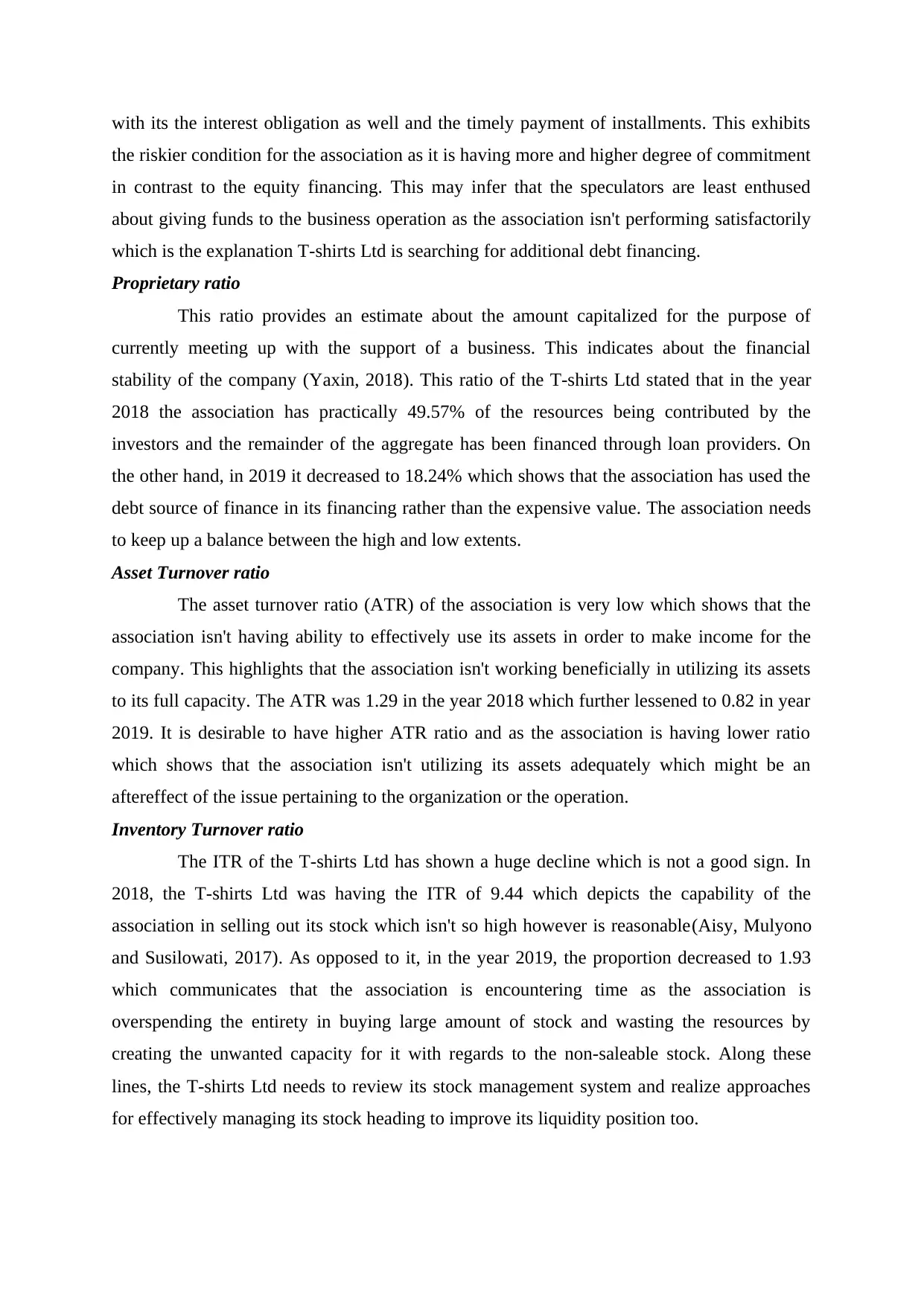

with its the interest obligation as well and the timely payment of installments. This exhibits

the riskier condition for the association as it is having more and higher degree of commitment

in contrast to the equity financing. This may infer that the speculators are least enthused

about giving funds to the business operation as the association isn't performing satisfactorily

which is the explanation T-shirts Ltd is searching for additional debt financing.

Proprietary ratio

This ratio provides an estimate about the amount capitalized for the purpose of

currently meeting up with the support of a business. This indicates about the financial

stability of the company (Yaxin, 2018). This ratio of the T-shirts Ltd stated that in the year

2018 the association has practically 49.57% of the resources being contributed by the

investors and the remainder of the aggregate has been financed through loan providers. On

the other hand, in 2019 it decreased to 18.24% which shows that the association has used the

debt source of finance in its financing rather than the expensive value. The association needs

to keep up a balance between the high and low extents.

Asset Turnover ratio

The asset turnover ratio (ATR) of the association is very low which shows that the

association isn't having ability to effectively use its assets in order to make income for the

company. This highlights that the association isn't working beneficially in utilizing its assets

to its full capacity. The ATR was 1.29 in the year 2018 which further lessened to 0.82 in year

2019. It is desirable to have higher ATR ratio and as the association is having lower ratio

which shows that the association isn't utilizing its assets adequately which might be an

aftereffect of the issue pertaining to the organization or the operation.

Inventory Turnover ratio

The ITR of the T-shirts Ltd has shown a huge decline which is not a good sign. In

2018, the T-shirts Ltd was having the ITR of 9.44 which depicts the capability of the

association in selling out its stock which isn't so high however is reasonable(Aisy, Mulyono

and Susilowati, 2017). As opposed to it, in the year 2019, the proportion decreased to 1.93

which communicates that the association is encountering time as the association is

overspending the entirety in buying large amount of stock and wasting the resources by

creating the unwanted capacity for it with regards to the non-saleable stock. Along these

lines, the T-shirts Ltd needs to review its stock management system and realize approaches

for effectively managing its stock heading to improve its liquidity position too.

the riskier condition for the association as it is having more and higher degree of commitment

in contrast to the equity financing. This may infer that the speculators are least enthused

about giving funds to the business operation as the association isn't performing satisfactorily

which is the explanation T-shirts Ltd is searching for additional debt financing.

Proprietary ratio

This ratio provides an estimate about the amount capitalized for the purpose of

currently meeting up with the support of a business. This indicates about the financial

stability of the company (Yaxin, 2018). This ratio of the T-shirts Ltd stated that in the year

2018 the association has practically 49.57% of the resources being contributed by the

investors and the remainder of the aggregate has been financed through loan providers. On

the other hand, in 2019 it decreased to 18.24% which shows that the association has used the

debt source of finance in its financing rather than the expensive value. The association needs

to keep up a balance between the high and low extents.

Asset Turnover ratio

The asset turnover ratio (ATR) of the association is very low which shows that the

association isn't having ability to effectively use its assets in order to make income for the

company. This highlights that the association isn't working beneficially in utilizing its assets

to its full capacity. The ATR was 1.29 in the year 2018 which further lessened to 0.82 in year

2019. It is desirable to have higher ATR ratio and as the association is having lower ratio

which shows that the association isn't utilizing its assets adequately which might be an

aftereffect of the issue pertaining to the organization or the operation.

Inventory Turnover ratio

The ITR of the T-shirts Ltd has shown a huge decline which is not a good sign. In

2018, the T-shirts Ltd was having the ITR of 9.44 which depicts the capability of the

association in selling out its stock which isn't so high however is reasonable(Aisy, Mulyono

and Susilowati, 2017). As opposed to it, in the year 2019, the proportion decreased to 1.93

which communicates that the association is encountering time as the association is

overspending the entirety in buying large amount of stock and wasting the resources by

creating the unwanted capacity for it with regards to the non-saleable stock. Along these

lines, the T-shirts Ltd needs to review its stock management system and realize approaches

for effectively managing its stock heading to improve its liquidity position too.

Thus, abased on the above it can be stated that the current financial position of the

T-shirts Ltd is not sound and requires to implement the strategies which will help it in

effectively managing the current situation and overcome it.

PART 2: UNDERSTANDING FINANCIAL INFORMATION &

MANAGEMENT OF CASH

2.1 Understanding the concept of accrual accounting vs cash accounting

Accrual Accounting

Under this form of accounting practice, the business transactions are recorded in the

books of accounts as and when it incurs irrespective of the fact whether cash has been

received or not (What is the difference between the cash basis and the accrual basis of

accounting? 2020.). This accounting principle follows the matching principle and in

accordance to it, the revenue and the expenditure of the business is should be recorded at the

same time.

Benefits:

This type of accounting is issued by mainly all types of business organizations.

It provides assistance to the organization in carrying out the plan for the purpose of

cost analysis and further in forecasting of revenue and along with it, accrual

accounting complies with the GAAP.

This practice is not influenced by the time factor on account of receiving cash.

Limitations:

This method might create confusion in the mind of the users resulting into the

deception in the financial statements.

Another limitation is that it is complex process in respect to recognising the revenue

and expenses and thus, requires the assistance of accountant.

Example:In the case of T-Shirts Ltd, the company has increased the credit period provided to

its customers from 30 to 60 days so even if the cash is not received, it will be presented in the

accounts book under the heading of debtors.

Cash Accounting

This method of accounting is opposite of accrual, as under this, income and

expenditure are recorded in the books when the cash is being received or the payment has

been made for the expenses. It does not take into account just the transactionsunless cash is

received or paid.

Benefits:

T-shirts Ltd is not sound and requires to implement the strategies which will help it in

effectively managing the current situation and overcome it.

PART 2: UNDERSTANDING FINANCIAL INFORMATION &

MANAGEMENT OF CASH

2.1 Understanding the concept of accrual accounting vs cash accounting

Accrual Accounting

Under this form of accounting practice, the business transactions are recorded in the

books of accounts as and when it incurs irrespective of the fact whether cash has been

received or not (What is the difference between the cash basis and the accrual basis of

accounting? 2020.). This accounting principle follows the matching principle and in

accordance to it, the revenue and the expenditure of the business is should be recorded at the

same time.

Benefits:

This type of accounting is issued by mainly all types of business organizations.

It provides assistance to the organization in carrying out the plan for the purpose of

cost analysis and further in forecasting of revenue and along with it, accrual

accounting complies with the GAAP.

This practice is not influenced by the time factor on account of receiving cash.

Limitations:

This method might create confusion in the mind of the users resulting into the

deception in the financial statements.

Another limitation is that it is complex process in respect to recognising the revenue

and expenses and thus, requires the assistance of accountant.

Example:In the case of T-Shirts Ltd, the company has increased the credit period provided to

its customers from 30 to 60 days so even if the cash is not received, it will be presented in the

accounts book under the heading of debtors.

Cash Accounting

This method of accounting is opposite of accrual, as under this, income and

expenditure are recorded in the books when the cash is being received or the payment has

been made for the expenses. It does not take into account just the transactionsunless cash is

received or paid.

Benefits:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This accounting method is very easylearn and implement and can be done single

handedly without the need of accountant.

It is effective in determining the exact amount of cash being available in hand.

Another benefit of this accounting method is that it provides help in taking advantage

of tax benefits since the transaction are recoded when the exchange of cash takes

place.

Limitations:

This method does not provide with the actual picture in respect to the performance of

the company which is because only cash transact are taken into account.

The major limitation is that it cannot be used for the businesses which provide goods

on credit to its customers.

Example:According to the given case study, if the cash accounting is implemented into it

then the transaction will be recorded only when the cash is received irrespective of credit

term provided.

2.2 Meaning and differences between the profit and cash flow

Profit:

Profit refers to the residual amount which is left behind after the business

organization effectively meets with its business expenditure (Understanding the difference

between cash flow and profit. 2018). It is shown in the income statement and is needed for

the survival of the business.

Cash flow:

The cash flow accounts for the amount the company receives or pays in a given

period. It is favourable to have positive cash flow which highlights the efficiency of the

business.

Differentiating between cash flow and profit

Cash flow Profit

It accounts for the movement of cash in and

out of the business organization.

It can be defined as the amount which is left

after meeting with all the expenses.

The cash flow shows the movement of cash

from the various sources or business activities.

Profit is the amount which is generated from

the attaining the desired sales output.

It provides information on the liquidity of the

company.

It depicts the profitable situation of the

company.

handedly without the need of accountant.

It is effective in determining the exact amount of cash being available in hand.

Another benefit of this accounting method is that it provides help in taking advantage

of tax benefits since the transaction are recoded when the exchange of cash takes

place.

Limitations:

This method does not provide with the actual picture in respect to the performance of

the company which is because only cash transact are taken into account.

The major limitation is that it cannot be used for the businesses which provide goods

on credit to its customers.

Example:According to the given case study, if the cash accounting is implemented into it

then the transaction will be recorded only when the cash is received irrespective of credit

term provided.

2.2 Meaning and differences between the profit and cash flow

Profit:

Profit refers to the residual amount which is left behind after the business

organization effectively meets with its business expenditure (Understanding the difference

between cash flow and profit. 2018). It is shown in the income statement and is needed for

the survival of the business.

Cash flow:

The cash flow accounts for the amount the company receives or pays in a given

period. It is favourable to have positive cash flow which highlights the efficiency of the

business.

Differentiating between cash flow and profit

Cash flow Profit

It accounts for the movement of cash in and

out of the business organization.

It can be defined as the amount which is left

after meeting with all the expenses.

The cash flow shows the movement of cash

from the various sources or business activities.

Profit is the amount which is generated from

the attaining the desired sales output.

It provides information on the liquidity of the

company.

It depicts the profitable situation of the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is the summation of cash from operating,

investing and financing activities.

It is difference between revenue and expenses.

PART 3

Meaning and purpose of budget

The budget is defined as the estimation of the expected income and expenses of a

company for a specific period of time. This is a type of financial plan which assist the

company in managing and planning for the operations of the company in effective manner

(Novikov, 2018). This is particularly because of the reason that when the budget is prepared

then there is estimated amount of money which can be used for expense and on basis of this

company can plan all its operations. Further the budget is a tool that ensures that there is

enough money required for the effective working of the company. This is particularly

because of the reason that company knows at the end how much money needs to be saved

and hence because of this the company plans all the activities in that manner.

The major purpose of budget is to plan and organize all the working on the basis of

the estimated amount in order to improve the financial position of the company. This is

particularly because of the reason that when the company has an advance planning then this

will assist the company in analyzing the ways in which finance can be optimally used.

Further this budget is also treated as a base for doing effective decision making. The major

reason for this is that when the company has an estimation of the income and expenses then

they can easily decide for the future working. For instance, if in budget the estimated

expenses of the company are around $4000 then company knows that they have to incur the

expenses within the range of this amount only.

Benefits of forming limited company and registering on stock exchange

The limited company is the type of company in which the limit of the liability of

every shareholder is limited. This limit can be as per the ratio approved or in accordance with

the share of shareholder within the company. There are number of benefits of forming limited

company and registering it on stock exchange. These benefits are as follows-

The most essential benefit of listing the limited company over the stock exchange is

that this increases the liquidity of the company (Lupembe, 2017). This is a benefit as when

the company registers itself on stock exchange then it can be traded by anyone hence the

liquidity of company increases and they can easily convert their shares into cash.

investing and financing activities.

It is difference between revenue and expenses.

PART 3

Meaning and purpose of budget

The budget is defined as the estimation of the expected income and expenses of a

company for a specific period of time. This is a type of financial plan which assist the

company in managing and planning for the operations of the company in effective manner

(Novikov, 2018). This is particularly because of the reason that when the budget is prepared

then there is estimated amount of money which can be used for expense and on basis of this

company can plan all its operations. Further the budget is a tool that ensures that there is

enough money required for the effective working of the company. This is particularly

because of the reason that company knows at the end how much money needs to be saved

and hence because of this the company plans all the activities in that manner.

The major purpose of budget is to plan and organize all the working on the basis of

the estimated amount in order to improve the financial position of the company. This is

particularly because of the reason that when the company has an advance planning then this

will assist the company in analyzing the ways in which finance can be optimally used.

Further this budget is also treated as a base for doing effective decision making. The major

reason for this is that when the company has an estimation of the income and expenses then

they can easily decide for the future working. For instance, if in budget the estimated

expenses of the company are around $4000 then company knows that they have to incur the

expenses within the range of this amount only.

Benefits of forming limited company and registering on stock exchange

The limited company is the type of company in which the limit of the liability of

every shareholder is limited. This limit can be as per the ratio approved or in accordance with

the share of shareholder within the company. There are number of benefits of forming limited

company and registering it on stock exchange. These benefits are as follows-

The most essential benefit of listing the limited company over the stock exchange is

that this increases the liquidity of the company (Lupembe, 2017). This is a benefit as when

the company registers itself on stock exchange then it can be traded by anyone hence the

liquidity of company increases and they can easily convert their shares into cash.

Another major benefit of listing the company is that this increases efficiency and

transparency of company and its operations. The major reason for this is that when the

company is listed then they have to maintain their working and position in market. Also the

company has to share all the details of the company with the shareholders of the company

(Briston, 2017). Thus for this they will have to publish their accounting information and this

will lead to more transparency among company and shareholders.

In addition to this another major benefit of listing the companies over stock

exchange is that the morale of the employees will increase. The major reason for this is that

with assistance of the listing over stock exchange the public perception of company will

increase. Thus, in order to meet the expectation of the public the employees will work in

more effective manner. Further, along with this if the company will perform well in the stock

market then this will yield more profit and this will result in better pay and bonus to

employees. Thus, this increases the motivation level of employees and they perform well

(Yousif and et.al, 2018).

Furthermore when the company registers itself over the stock exchanges then this

will increase the visibility of the company in the highly competitive market. The major

reason for this is that when company list itself over stock exchange then this attracts many of

the people and because of this company is motivated to increases its operations to more

higher level.

Another major benefit of listing the company over the stock exchange is that there

are unlimited sources of raising fund. The major reason for this is that when company goes in

public market then they have better result for the arranging for finance (Benefits of listing/

going public, 2017).

In addition to this another major benefit of listing the company is easy transferability

of shares. This is major benefit of listing as in this market the shares can be easily transferred

and this will assist in proper flow of money within the economy.

transparency of company and its operations. The major reason for this is that when the

company is listed then they have to maintain their working and position in market. Also the

company has to share all the details of the company with the shareholders of the company

(Briston, 2017). Thus for this they will have to publish their accounting information and this

will lead to more transparency among company and shareholders.

In addition to this another major benefit of listing the companies over stock

exchange is that the morale of the employees will increase. The major reason for this is that

with assistance of the listing over stock exchange the public perception of company will

increase. Thus, in order to meet the expectation of the public the employees will work in

more effective manner. Further, along with this if the company will perform well in the stock

market then this will yield more profit and this will result in better pay and bonus to

employees. Thus, this increases the motivation level of employees and they perform well

(Yousif and et.al, 2018).

Furthermore when the company registers itself over the stock exchanges then this

will increase the visibility of the company in the highly competitive market. The major

reason for this is that when company list itself over stock exchange then this attracts many of

the people and because of this company is motivated to increases its operations to more

higher level.

Another major benefit of listing the company over the stock exchange is that there

are unlimited sources of raising fund. The major reason for this is that when company goes in

public market then they have better result for the arranging for finance (Benefits of listing/

going public, 2017).

In addition to this another major benefit of listing the company is easy transferability

of shares. This is major benefit of listing as in this market the shares can be easily transferred

and this will assist in proper flow of money within the economy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Aisy, H.R., Mulyono, I. and Susilowati, K.D.S., 2017. Compilation of Financial Statements

and Financial Analysis for Non Profit

Organizations. JurnalMahasiswaAkuntansiManajemen. 3(1).

Bjorklund, P.R., 2019. The Financial Statements of a Property & Casualty Company. J. Legal

Econ. 25. p.101.

Briston, R.J., 2017. The stock exchange and investment analysis (Vol. 3). Routledge.

Easton, P.D. and et.al., 2018. Financial statement analysis & valuation. Boston, MA:

Cambridge Business Publishers.

Firdaus, F. and Endri, E., 2020. Financial Statement Analysis: Evidence from Indonesian

Bank BUKU IV. International Journal of Innovative Science and Research

Technology. 5(4). pp.455-461.

Lupembe, T.S., 2017. Factors hindering access of small and medium enterprises in Dar es

Salaam stock exchange in Tanzania: a case of Dar es Salaam Stock

Exchange (Doctoral dissertation, University of Dar es Salaam).

Novikov, V.M., 2018. THE BUDGET RISK: MEANING AND REGULATION IN SOCIAL

INFRASTRUCTURE. Демографія та соціальна економіка, (1), pp.73-86.

Yaxin, H., 2018. Analysis of financial statements of listed companies: a case study of Gree's

2016 annual report. Jiangsu Science & Technology Information. (15). p.4.

Yousif, K.A., and et.al, 2018. Does listing intention matter? Investigation of how earnings

forecast affects decision to list on stock exchange. INTERNATIONAL JOURNAL OF

ADVANCED AND APPLIED SCIENCES. 5(5). pp.82-91.

Online

Benefits of listing/ going public. 2017. [Online]. Available through: <

https://www.msei.in/Corporates/benefits-of-listing>

Understanding the difference between cash flow and profit. 2018. [Online]. Available

Through:<https://www.rbcroyalbank.com/business/pdf/Knowing%20the

%20difference%20between%20cash%20flow%20and%20profit.pdf>.

What is the difference between the cash basis and the accrual basis of accounting? 2020.

[Online]. Available Through:<https://www.accountingcoach.com/blog/cash-basis-

accrual-basis-of-accounting>.

Books and Journals

Aisy, H.R., Mulyono, I. and Susilowati, K.D.S., 2017. Compilation of Financial Statements

and Financial Analysis for Non Profit

Organizations. JurnalMahasiswaAkuntansiManajemen. 3(1).

Bjorklund, P.R., 2019. The Financial Statements of a Property & Casualty Company. J. Legal

Econ. 25. p.101.

Briston, R.J., 2017. The stock exchange and investment analysis (Vol. 3). Routledge.

Easton, P.D. and et.al., 2018. Financial statement analysis & valuation. Boston, MA:

Cambridge Business Publishers.

Firdaus, F. and Endri, E., 2020. Financial Statement Analysis: Evidence from Indonesian

Bank BUKU IV. International Journal of Innovative Science and Research

Technology. 5(4). pp.455-461.

Lupembe, T.S., 2017. Factors hindering access of small and medium enterprises in Dar es

Salaam stock exchange in Tanzania: a case of Dar es Salaam Stock

Exchange (Doctoral dissertation, University of Dar es Salaam).

Novikov, V.M., 2018. THE BUDGET RISK: MEANING AND REGULATION IN SOCIAL

INFRASTRUCTURE. Демографія та соціальна економіка, (1), pp.73-86.

Yaxin, H., 2018. Analysis of financial statements of listed companies: a case study of Gree's

2016 annual report. Jiangsu Science & Technology Information. (15). p.4.

Yousif, K.A., and et.al, 2018. Does listing intention matter? Investigation of how earnings

forecast affects decision to list on stock exchange. INTERNATIONAL JOURNAL OF

ADVANCED AND APPLIED SCIENCES. 5(5). pp.82-91.

Online

Benefits of listing/ going public. 2017. [Online]. Available through: <

https://www.msei.in/Corporates/benefits-of-listing>

Understanding the difference between cash flow and profit. 2018. [Online]. Available

Through:<https://www.rbcroyalbank.com/business/pdf/Knowing%20the

%20difference%20between%20cash%20flow%20and%20profit.pdf>.

What is the difference between the cash basis and the accrual basis of accounting? 2020.

[Online]. Available Through:<https://www.accountingcoach.com/blog/cash-basis-

accrual-basis-of-accounting>.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Return on assets Net income/assets -29.41% 22.77%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

Debt to equity ratio Total debt/total equity 4.48 1.02

Proprietary ratio Total equity / total Assets 18.24% 49.57%

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Return on assets Net income/assets -29.41% 22.77%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

Debt to equity ratio Total debt/total equity 4.48 1.02

Proprietary ratio Total equity / total Assets 18.24% 49.57%

Efficiency ratio

COGS 751 840

Average inventory 389 89

Net sales 1366 2101

Average asset 1667 1634

Asset Turnover ratio Net sales/Average Total Asset 0.82 1.29

Inventory Turnover

ratio COGS/Average Inventory 1.93 9.44

COGS 751 840

Average inventory 389 89

Net sales 1366 2101

Average asset 1667 1634

Asset Turnover ratio Net sales/Average Total Asset 0.82 1.29

Inventory Turnover

ratio COGS/Average Inventory 1.93 9.44

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.