Analysis of Business Performance, Accounting, and Financial Ratios

VerifiedAdded on 2022/12/09

|11

|3536

|272

Report

AI Summary

This comprehensive report delves into various aspects of business finance and economics. It begins with an introduction to business finance, covering topics such as the allocation of capital and economic forecasting. The main body outlines the major determinants of business performance, distinguishing between microeconomic and macroeconomic factors, and discusses how these factors influence an organization's competitive environment. The report explains the role of accounting in an organization, emphasizing its significance in terms of reporting and decision-making, and differentiates between the main financial statements, describing their structure and key terms. It includes a practical section where financial ratios for XYZ Plc are calculated and interpreted for the years ended March 31, 2019, and 2020. Furthermore, the report defines management accounting and explains its vital role in organizational planning, monitoring, and decision-making, concluding with a summary of key findings and insights. The report is a valuable resource for students studying business finance, offering a blend of theoretical concepts and practical application.

Business Finance and Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Outline the major determinants that influence business performance as well as

distinguish whether they are microeconomic or macroeconomic. Discussion on the economic

factors which influence an organization's competitive environment:..........................................3

Explain role of the accounting in an organization and emphasize its significance in terms of

reporting as well as decision-making:.........................................................................................5

Differentiate from the main financial statements as well as describe the structure and terms

included in each:..........................................................................................................................6

Calculate and interpret the following ratios for XYZ Plc for the years ended March 31 2019

and 2020, respectively:................................................................................................................7

Define the management accounting and explain why it is vital for organizational planning,

monitoring, and decision-making:...............................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Contents...........................................................................................................................................2

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Outline the major determinants that influence business performance as well as

distinguish whether they are microeconomic or macroeconomic. Discussion on the economic

factors which influence an organization's competitive environment:..........................................3

Explain role of the accounting in an organization and emphasize its significance in terms of

reporting as well as decision-making:.........................................................................................5

Differentiate from the main financial statements as well as describe the structure and terms

included in each:..........................................................................................................................6

Calculate and interpret the following ratios for XYZ Plc for the years ended March 31 2019

and 2020, respectively:................................................................................................................7

Define the management accounting and explain why it is vital for organizational planning,

monitoring, and decision-making:...............................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Introduction

Business finance known as the corporate finance in business world, relates to allocating

capital, developing economic forecasts, evaluating equity as well as debt funding options, and

performing other operations within the company (Melé, Rosanas and Fontrodona, 2017). Small

companies, on the whole, do not have large finance team, but these roles may be present in the

organization. The study covers different tasks covering multiple aspects of business finance like

role of accounting, micro and macro factors affecting business environment, ratio analysis as

well as through discussion on concept of management accounting.

Main Body

Outline the major determinants that influence business performance as well as

distinguish whether they are microeconomic or macroeconomic. Discussion on the

economic factors which influence an organization's competitive environment:

In external business environment, there're two types of components: micro as well as macro.

These external forces are beyond businesses' power, but they do have an impact on decisions

taken while developing a tactical business model.

Factors in the Microenvironment

Suppliers: If suppliers have power, they will influence the company's performance.

When supplier is the sole or main distributor to their products; the customer is not critical

to supplier's operation; and supplier's inventory is an integral part of purchaser's end product

and business, supplier possesses control.

Resellers: Whether a company's product is sold by third-party resellers or industry intermediaries

like retailers, wholesalers, including distributors, those resellers have an effect on the company 's

business performance. If retail vendor has a good reputation, for instance, this could be used to

advertise the product.

Customers: How business sell their items / products/services to them will be heavily influenced

by who are their customers (B2B or Business to customer, regional or foreign, etc.) as well

as their motives for purchasing the product (Pendley, 2018).

The competition: The business competition consists of those that offer the same or even similar

goods and services as corporation, as well as the manner they sell must be considered. What

Business finance known as the corporate finance in business world, relates to allocating

capital, developing economic forecasts, evaluating equity as well as debt funding options, and

performing other operations within the company (Melé, Rosanas and Fontrodona, 2017). Small

companies, on the whole, do not have large finance team, but these roles may be present in the

organization. The study covers different tasks covering multiple aspects of business finance like

role of accounting, micro and macro factors affecting business environment, ratio analysis as

well as through discussion on concept of management accounting.

Main Body

Outline the major determinants that influence business performance as well as

distinguish whether they are microeconomic or macroeconomic. Discussion on the

economic factors which influence an organization's competitive environment:

In external business environment, there're two types of components: micro as well as macro.

These external forces are beyond businesses' power, but they do have an impact on decisions

taken while developing a tactical business model.

Factors in the Microenvironment

Suppliers: If suppliers have power, they will influence the company's performance.

When supplier is the sole or main distributor to their products; the customer is not critical

to supplier's operation; and supplier's inventory is an integral part of purchaser's end product

and business, supplier possesses control.

Resellers: Whether a company's product is sold by third-party resellers or industry intermediaries

like retailers, wholesalers, including distributors, those resellers have an effect on the company 's

business performance. If retail vendor has a good reputation, for instance, this could be used to

advertise the product.

Customers: How business sell their items / products/services to them will be heavily influenced

by who are their customers (B2B or Business to customer, regional or foreign, etc.) as well

as their motives for purchasing the product (Pendley, 2018).

The competition: The business competition consists of those that offer the same or even similar

goods and services as corporation, as well as the manner they sell must be considered. What

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

influence do price differences and products differentiation have on business? How

does business use this to improve your performance and also get ahead of competition?

The public at large: company has a responsibility to the general public. Every action taken by the

organization must be seen through the eyes of general public as well as how it affects them. The

general populace has the ability to assist business in achieving thier objectives as well as to

discourage from doing so.

Macro Environment Factors

Demographic forces: Popular demographic forces, such as country/region; age group; ethnicity;

educational attainment; family lifestyle; cultural factors and trends, all have an effect on different

consumer segments.

Economic: factors Both organization's efficiency and the customer's decision-making processes

are affected by the economic climate.

Natural/physical forces: This is essential to consider the Earth's regeneration of environmental

resource base like trees, farm commodities, marine products, and so on. Traditional non -

renewable resources including such oil, coals, minerals, and others can also have an effect on the

organization's production.

Technological factors: The expertise and experience used in manufacturing, as well as the

technologies and materials used for production of goods and services, may all have an effect on

the corporation's smooth operation and should be taken into account.

Political and regulatory forces: When making marketing decisions, that's crucial to keep in mind

the organization's and marketplaces' political and legal changes (Fields, 2016).

Social and cultural forces: Social as well as cultural influence of the goods and services company

brings to marketplace should be addressed. To demonstrate that the company is socially

responsible, all aspects of the manufacturing process or products lines which are detrimental to

societies should be removed. The environment is recent instance of this, with many industries

being compelled to rethink their products/services in attempt to become environmentally

sustainable.

Environmental factors like micro as well as macro variables have a direct effect on the

performance of marketing campaigns, so they must be carefully considered during development

of strategic marketing strategy. These considerations would boost the long-term effectiveness of

your company's marketing strategy as well as the brand's credibility.

does business use this to improve your performance and also get ahead of competition?

The public at large: company has a responsibility to the general public. Every action taken by the

organization must be seen through the eyes of general public as well as how it affects them. The

general populace has the ability to assist business in achieving thier objectives as well as to

discourage from doing so.

Macro Environment Factors

Demographic forces: Popular demographic forces, such as country/region; age group; ethnicity;

educational attainment; family lifestyle; cultural factors and trends, all have an effect on different

consumer segments.

Economic: factors Both organization's efficiency and the customer's decision-making processes

are affected by the economic climate.

Natural/physical forces: This is essential to consider the Earth's regeneration of environmental

resource base like trees, farm commodities, marine products, and so on. Traditional non -

renewable resources including such oil, coals, minerals, and others can also have an effect on the

organization's production.

Technological factors: The expertise and experience used in manufacturing, as well as the

technologies and materials used for production of goods and services, may all have an effect on

the corporation's smooth operation and should be taken into account.

Political and regulatory forces: When making marketing decisions, that's crucial to keep in mind

the organization's and marketplaces' political and legal changes (Fields, 2016).

Social and cultural forces: Social as well as cultural influence of the goods and services company

brings to marketplace should be addressed. To demonstrate that the company is socially

responsible, all aspects of the manufacturing process or products lines which are detrimental to

societies should be removed. The environment is recent instance of this, with many industries

being compelled to rethink their products/services in attempt to become environmentally

sustainable.

Environmental factors like micro as well as macro variables have a direct effect on the

performance of marketing campaigns, so they must be carefully considered during development

of strategic marketing strategy. These considerations would boost the long-term effectiveness of

your company's marketing strategy as well as the brand's credibility.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Explain role of the accounting in an organization and emphasize its significance in terms of

reporting as well as decision-making:

Accounting assists a company in achieving its goals and objectives by collecting, arranging, and

sharing data about its operations. As a result, it is important in today's business world. Apart

from accounting, the position of individual accountant or reporting professionals in modern

organization is critical because this employee, or division, is responsible for two different

accounting concepts: financial accounting and the managerial accounting. Recognizing what

such 2 categories of accounting would help to clarify and justify role of accounting in today's

world (Hertz and Friedman, 2015).

Accounting's goal is to offer financial reports to the corporation's stakeholders: management,

customers, and lenders. Accounting tracks and describes the corporation 's activities and reports

the findings to executives and other stakeholder groups.

Management teams need reliable and timely accounting data in order to make informed

decisions, and accounting professionals provide this data. As the accounting phase gathers data

and describes it in variety of reports, accounting professionals assist in interpreting the reports'

implications and suggesting ways to use information to solve enterprise issues.

Management as well as fiscal accounting are the two types of accounting. Accounting reports

about how well company is going, whereas management accounting assists in its operation.

Importance with respect to both reporting and decision-making:

Accurate data regarding the corporation 's assets, liabilities, income, and cash position is required

to run a corporation. Accounting is the source of this vital data. Accounting is important in

determining the feasibility of investments made. An investment's adequate consideration

necessitates a thorough examination of expenses and estimates of expected potential cash flows

Some conditions must, be achieved such as identifying barriers to returns on investment.

Consider problem that many managers face when deciding whether to build a new factory or

extend existing ones. Investing $1 million in new manufacturing facility or spending $300,000 to

extend production line could be an option. Each option would have distinct cash outflows

in beginning and distinct cash inflows in future. The return on the investment for each strategy

would be distinct. So, which of the two should management pick? The company's accounting

professionals will examine the numbers with each investment, measure rate of return, and report

their results to management (Galarza, 2017). This is situation in which accounting procedures

reporting as well as decision-making:

Accounting assists a company in achieving its goals and objectives by collecting, arranging, and

sharing data about its operations. As a result, it is important in today's business world. Apart

from accounting, the position of individual accountant or reporting professionals in modern

organization is critical because this employee, or division, is responsible for two different

accounting concepts: financial accounting and the managerial accounting. Recognizing what

such 2 categories of accounting would help to clarify and justify role of accounting in today's

world (Hertz and Friedman, 2015).

Accounting's goal is to offer financial reports to the corporation's stakeholders: management,

customers, and lenders. Accounting tracks and describes the corporation 's activities and reports

the findings to executives and other stakeholder groups.

Management teams need reliable and timely accounting data in order to make informed

decisions, and accounting professionals provide this data. As the accounting phase gathers data

and describes it in variety of reports, accounting professionals assist in interpreting the reports'

implications and suggesting ways to use information to solve enterprise issues.

Management as well as fiscal accounting are the two types of accounting. Accounting reports

about how well company is going, whereas management accounting assists in its operation.

Importance with respect to both reporting and decision-making:

Accurate data regarding the corporation 's assets, liabilities, income, and cash position is required

to run a corporation. Accounting is the source of this vital data. Accounting is important in

determining the feasibility of investments made. An investment's adequate consideration

necessitates a thorough examination of expenses and estimates of expected potential cash flows

Some conditions must, be achieved such as identifying barriers to returns on investment.

Consider problem that many managers face when deciding whether to build a new factory or

extend existing ones. Investing $1 million in new manufacturing facility or spending $300,000 to

extend production line could be an option. Each option would have distinct cash outflows

in beginning and distinct cash inflows in future. The return on the investment for each strategy

would be distinct. So, which of the two should management pick? The company's accounting

professionals will examine the numbers with each investment, measure rate of return, and report

their results to management (Galarza, 2017). This is situation in which accounting procedures

generate the necessary financial data for management to take informed decisions They must also

investigate different financing options for these investments. Relevant facts and data should

always be used to support decisions.

Differentiate from the main financial statements as well as describe the structure and terms

included in each:

Balance sheet or the statement of financial position, income statement, cash flows statement, as

well as statement of changes in shareholders' equity are the four fundamental financial

statements used by an organization. Balance sheet is an overview of an organization at a certain

point in time. On a given date, it lists entity's assets, different liabilities, and, in case of a

company, stockholders' equity.

Income statement summarizes a corporation's sales, earnings, costs, losses, and net incomes or

loss over a given time span. This statement resembles moving picture of corporation's activities

over the course of this time span. During a given timeframe, the cash flows statement outlines an

entity's cash collections and cash pay-outs related to its working, spending, and funding

activities. The start of the time equity of enterprise is reconciled with ending balance in statement

showing changes in shareholders' equity or the stockholders' equity (Fabozzi, 2016).

Elements of Financial Statement:

Assets are the probable outcome economic benefits that a single individual will receive or

manage as a consequence of previous transactions or events.

Comprehensive income is shift in a corporation's equity (overall net assets) over time as a result

of sales as well as certain non-owner occurrences and situations. Except for changes in equity

arising from owner contributions and dividends to owners, this covers all improvements in equity

over a timeframe.

Distributions to company owners are reductions in a company's net assets as result of selling

assets, rendering facilities, or levying liabilities to the company's owners. Ownership stake or

equity in company is reduced as a result of dividends to owners.

After subtracting a corporation's liabilities, equity is remaining interest in assets. Ownership

interest in corporate company is referred to as equity.

Expenses implies outflows or other utilizes of assets or occurring of liabilities resulting

from entity's continuing main or core activity, such as shipping or processing products, rendering

facilities, or carry out some other operations.

investigate different financing options for these investments. Relevant facts and data should

always be used to support decisions.

Differentiate from the main financial statements as well as describe the structure and terms

included in each:

Balance sheet or the statement of financial position, income statement, cash flows statement, as

well as statement of changes in shareholders' equity are the four fundamental financial

statements used by an organization. Balance sheet is an overview of an organization at a certain

point in time. On a given date, it lists entity's assets, different liabilities, and, in case of a

company, stockholders' equity.

Income statement summarizes a corporation's sales, earnings, costs, losses, and net incomes or

loss over a given time span. This statement resembles moving picture of corporation's activities

over the course of this time span. During a given timeframe, the cash flows statement outlines an

entity's cash collections and cash pay-outs related to its working, spending, and funding

activities. The start of the time equity of enterprise is reconciled with ending balance in statement

showing changes in shareholders' equity or the stockholders' equity (Fabozzi, 2016).

Elements of Financial Statement:

Assets are the probable outcome economic benefits that a single individual will receive or

manage as a consequence of previous transactions or events.

Comprehensive income is shift in a corporation's equity (overall net assets) over time as a result

of sales as well as certain non-owner occurrences and situations. Except for changes in equity

arising from owner contributions and dividends to owners, this covers all improvements in equity

over a timeframe.

Distributions to company owners are reductions in a company's net assets as result of selling

assets, rendering facilities, or levying liabilities to the company's owners. Ownership stake or

equity in company is reduced as a result of dividends to owners.

After subtracting a corporation's liabilities, equity is remaining interest in assets. Ownership

interest in corporate company is referred to as equity.

Expenses implies outflows or other utilizes of assets or occurring of liabilities resulting

from entity's continuing main or core activity, such as shipping or processing products, rendering

facilities, or carry out some other operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

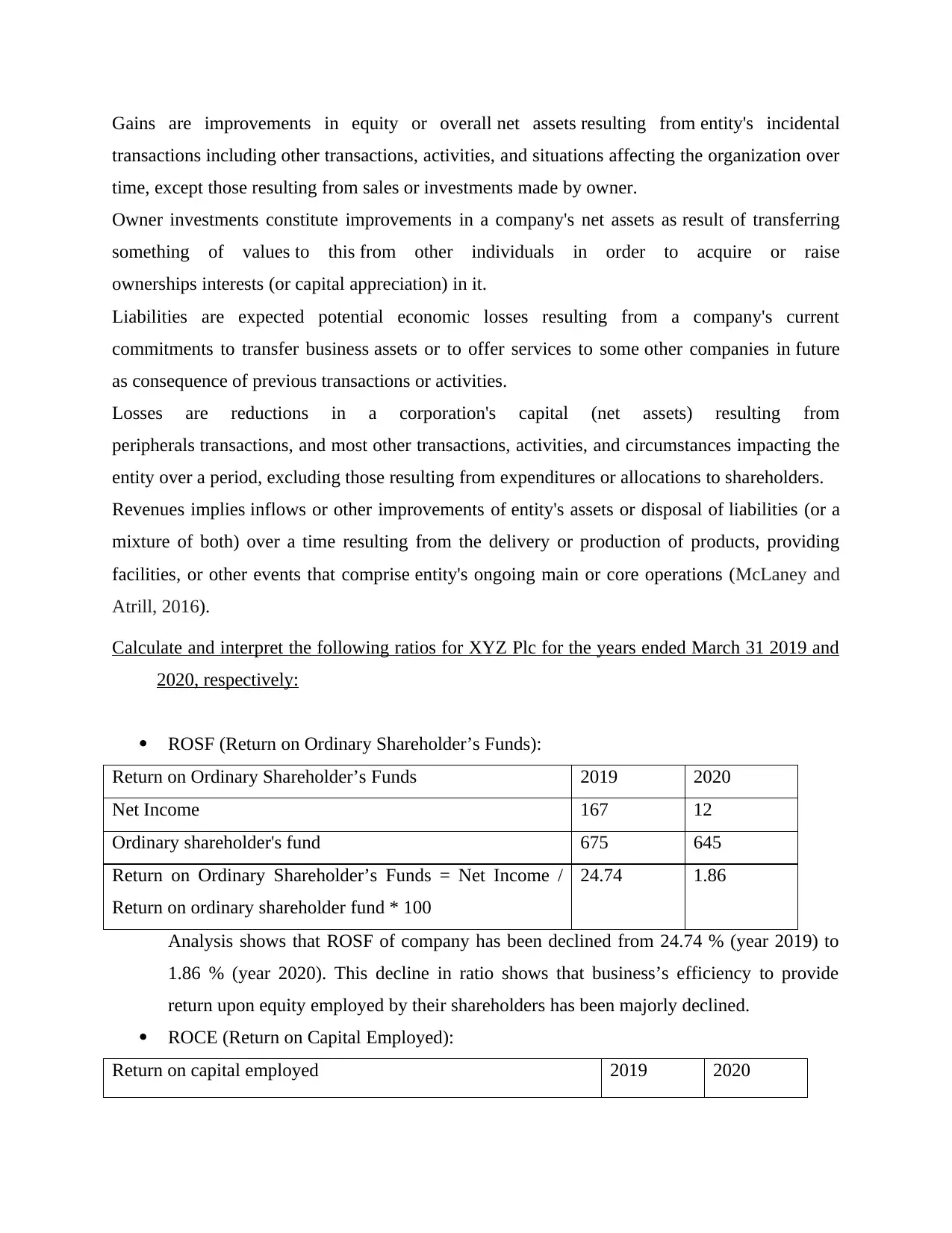

Gains are improvements in equity or overall net assets resulting from entity's incidental

transactions including other transactions, activities, and situations affecting the organization over

time, except those resulting from sales or investments made by owner.

Owner investments constitute improvements in a company's net assets as result of transferring

something of values to this from other individuals in order to acquire or raise

ownerships interests (or capital appreciation) in it.

Liabilities are expected potential economic losses resulting from a company's current

commitments to transfer business assets or to offer services to some other companies in future

as consequence of previous transactions or activities.

Losses are reductions in a corporation's capital (net assets) resulting from

peripherals transactions, and most other transactions, activities, and circumstances impacting the

entity over a period, excluding those resulting from expenditures or allocations to shareholders.

Revenues implies inflows or other improvements of entity's assets or disposal of liabilities (or a

mixture of both) over a time resulting from the delivery or production of products, providing

facilities, or other events that comprise entity's ongoing main or core operations (McLaney and

Atrill, 2016).

Calculate and interpret the following ratios for XYZ Plc for the years ended March 31 2019 and

2020, respectively:

ROSF (Return on Ordinary Shareholder’s Funds):

Return on Ordinary Shareholder’s Funds 2019 2020

Net Income 167 12

Ordinary shareholder's fund 675 645

Return on Ordinary Shareholder’s Funds = Net Income /

Return on ordinary shareholder fund * 100

24.74 1.86

Analysis shows that ROSF of company has been declined from 24.74 % (year 2019) to

1.86 % (year 2020). This decline in ratio shows that business’s efficiency to provide

return upon equity employed by their shareholders has been majorly declined.

ROCE (Return on Capital Employed):

Return on capital employed 2019 2020

transactions including other transactions, activities, and situations affecting the organization over

time, except those resulting from sales or investments made by owner.

Owner investments constitute improvements in a company's net assets as result of transferring

something of values to this from other individuals in order to acquire or raise

ownerships interests (or capital appreciation) in it.

Liabilities are expected potential economic losses resulting from a company's current

commitments to transfer business assets or to offer services to some other companies in future

as consequence of previous transactions or activities.

Losses are reductions in a corporation's capital (net assets) resulting from

peripherals transactions, and most other transactions, activities, and circumstances impacting the

entity over a period, excluding those resulting from expenditures or allocations to shareholders.

Revenues implies inflows or other improvements of entity's assets or disposal of liabilities (or a

mixture of both) over a time resulting from the delivery or production of products, providing

facilities, or other events that comprise entity's ongoing main or core operations (McLaney and

Atrill, 2016).

Calculate and interpret the following ratios for XYZ Plc for the years ended March 31 2019 and

2020, respectively:

ROSF (Return on Ordinary Shareholder’s Funds):

Return on Ordinary Shareholder’s Funds 2019 2020

Net Income 167 12

Ordinary shareholder's fund 675 645

Return on Ordinary Shareholder’s Funds = Net Income /

Return on ordinary shareholder fund * 100

24.74 1.86

Analysis shows that ROSF of company has been declined from 24.74 % (year 2019) to

1.86 % (year 2020). This decline in ratio shows that business’s efficiency to provide

return upon equity employed by their shareholders has been majorly declined.

ROCE (Return on Capital Employed):

Return on capital employed 2019 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

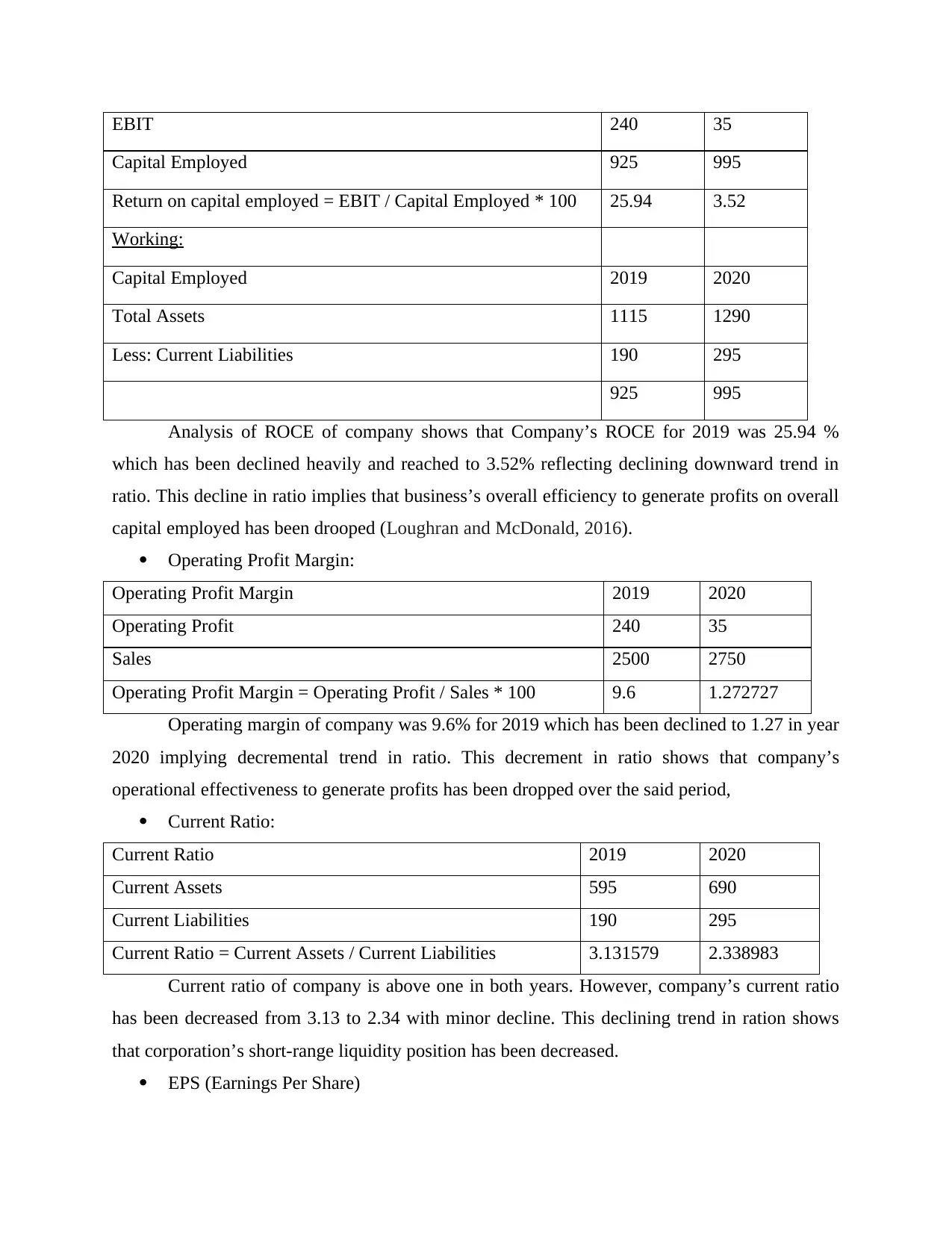

EBIT 240 35

Capital Employed 925 995

Return on capital employed = EBIT / Capital Employed * 100 25.94 3.52

Working:

Capital Employed 2019 2020

Total Assets 1115 1290

Less: Current Liabilities 190 295

925 995

Analysis of ROCE of company shows that Company’s ROCE for 2019 was 25.94 %

which has been declined heavily and reached to 3.52% reflecting declining downward trend in

ratio. This decline in ratio implies that business’s overall efficiency to generate profits on overall

capital employed has been drooped (Loughran and McDonald, 2016).

Operating Profit Margin:

Operating Profit Margin 2019 2020

Operating Profit 240 35

Sales 2500 2750

Operating Profit Margin = Operating Profit / Sales * 100 9.6 1.272727

Operating margin of company was 9.6% for 2019 which has been declined to 1.27 in year

2020 implying decremental trend in ratio. This decrement in ratio shows that company’s

operational effectiveness to generate profits has been dropped over the said period,

Current Ratio:

Current Ratio 2019 2020

Current Assets 595 690

Current Liabilities 190 295

Current Ratio = Current Assets / Current Liabilities 3.131579 2.338983

Current ratio of company is above one in both years. However, company’s current ratio

has been decreased from 3.13 to 2.34 with minor decline. This declining trend in ration shows

that corporation’s short-range liquidity position has been decreased.

EPS (Earnings Per Share)

Capital Employed 925 995

Return on capital employed = EBIT / Capital Employed * 100 25.94 3.52

Working:

Capital Employed 2019 2020

Total Assets 1115 1290

Less: Current Liabilities 190 295

925 995

Analysis of ROCE of company shows that Company’s ROCE for 2019 was 25.94 %

which has been declined heavily and reached to 3.52% reflecting declining downward trend in

ratio. This decline in ratio implies that business’s overall efficiency to generate profits on overall

capital employed has been drooped (Loughran and McDonald, 2016).

Operating Profit Margin:

Operating Profit Margin 2019 2020

Operating Profit 240 35

Sales 2500 2750

Operating Profit Margin = Operating Profit / Sales * 100 9.6 1.272727

Operating margin of company was 9.6% for 2019 which has been declined to 1.27 in year

2020 implying decremental trend in ratio. This decrement in ratio shows that company’s

operational effectiveness to generate profits has been dropped over the said period,

Current Ratio:

Current Ratio 2019 2020

Current Assets 595 690

Current Liabilities 190 295

Current Ratio = Current Assets / Current Liabilities 3.131579 2.338983

Current ratio of company is above one in both years. However, company’s current ratio

has been decreased from 3.13 to 2.34 with minor decline. This declining trend in ration shows

that corporation’s short-range liquidity position has been decreased.

EPS (Earnings Per Share)

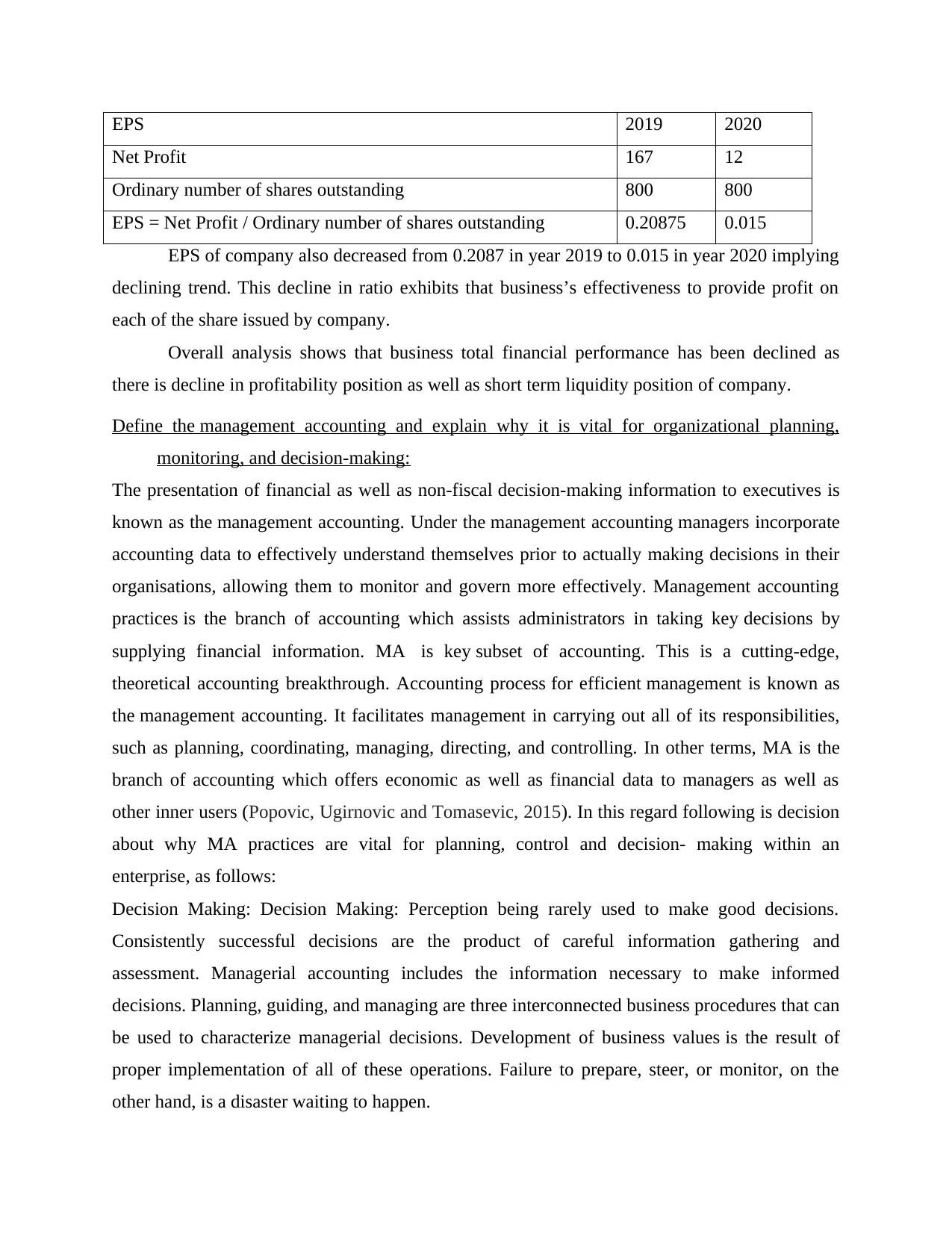

EPS 2019 2020

Net Profit 167 12

Ordinary number of shares outstanding 800 800

EPS = Net Profit / Ordinary number of shares outstanding 0.20875 0.015

EPS of company also decreased from 0.2087 in year 2019 to 0.015 in year 2020 implying

declining trend. This decline in ratio exhibits that business’s effectiveness to provide profit on

each of the share issued by company.

Overall analysis shows that business total financial performance has been declined as

there is decline in profitability position as well as short term liquidity position of company.

Define the management accounting and explain why it is vital for organizational planning,

monitoring, and decision-making:

The presentation of financial as well as non-fiscal decision-making information to executives is

known as the management accounting. Under the management accounting managers incorporate

accounting data to effectively understand themselves prior to actually making decisions in their

organisations, allowing them to monitor and govern more effectively. Management accounting

practices is the branch of accounting which assists administrators in taking key decisions by

supplying financial information. MA is key subset of accounting. This is a cutting-edge,

theoretical accounting breakthrough. Accounting process for efficient management is known as

the management accounting. It facilitates management in carrying out all of its responsibilities,

such as planning, coordinating, managing, directing, and controlling. In other terms, MA is the

branch of accounting which offers economic as well as financial data to managers as well as

other inner users (Popovic, Ugirnovic and Tomasevic, 2015). In this regard following is decision

about why MA practices are vital for planning, control and decision- making within an

enterprise, as follows:

Decision Making: Decision Making: Perception being rarely used to make good decisions.

Consistently successful decisions are the product of careful information gathering and

assessment. Managerial accounting includes the information necessary to make informed

decisions. Planning, guiding, and managing are three interconnected business procedures that can

be used to characterize managerial decisions. Development of business values is the result of

proper implementation of all of these operations. Failure to prepare, steer, or monitor, on the

other hand, is a disaster waiting to happen.

Net Profit 167 12

Ordinary number of shares outstanding 800 800

EPS = Net Profit / Ordinary number of shares outstanding 0.20875 0.015

EPS of company also decreased from 0.2087 in year 2019 to 0.015 in year 2020 implying

declining trend. This decline in ratio exhibits that business’s effectiveness to provide profit on

each of the share issued by company.

Overall analysis shows that business total financial performance has been declined as

there is decline in profitability position as well as short term liquidity position of company.

Define the management accounting and explain why it is vital for organizational planning,

monitoring, and decision-making:

The presentation of financial as well as non-fiscal decision-making information to executives is

known as the management accounting. Under the management accounting managers incorporate

accounting data to effectively understand themselves prior to actually making decisions in their

organisations, allowing them to monitor and govern more effectively. Management accounting

practices is the branch of accounting which assists administrators in taking key decisions by

supplying financial information. MA is key subset of accounting. This is a cutting-edge,

theoretical accounting breakthrough. Accounting process for efficient management is known as

the management accounting. It facilitates management in carrying out all of its responsibilities,

such as planning, coordinating, managing, directing, and controlling. In other terms, MA is the

branch of accounting which offers economic as well as financial data to managers as well as

other inner users (Popovic, Ugirnovic and Tomasevic, 2015). In this regard following is decision

about why MA practices are vital for planning, control and decision- making within an

enterprise, as follows:

Decision Making: Decision Making: Perception being rarely used to make good decisions.

Consistently successful decisions are the product of careful information gathering and

assessment. Managerial accounting includes the information necessary to make informed

decisions. Planning, guiding, and managing are three interconnected business procedures that can

be used to characterize managerial decisions. Development of business values is the result of

proper implementation of all of these operations. Failure to prepare, steer, or monitor, on the

other hand, is a disaster waiting to happen.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The core concept is that (1) good decisions resulting in value proposition, (2) decisions should

happen across a continuum of planning, guiding, and regulating operations, and (3) quality

decisions making could only be reliably achieved through knowledge reliance.

Planning: A company must prepare for its success. What is the concept of planning? It's all about

agreeing on course of actions to achieve a specific goal. All stages of planning are required.

First, it happens at the very top of setting key strategy hierarchy. It then goes on to more broad-

based discussion of how to find the best “position” to increase the likelihood of achieving goals.

Eventually, planning must take into account fiscal realities/constraints as well as expected

monetary results (budgets). A company enterprise may be formed of a large number of people.

Such individuals should be brought together to function in unison.

It's crucial that they communicate and comprehend the church's plans. In nutshell, "everyone

must be on same page." As a result, consistent communication is critical.

Monitoring: There are lot of positive plans which never come to fruition. A plan's realization

necessitates the start and course of various acts. These acts must frequently be well-

coordinated and scheduled. Resources should be, available and approvals has to be within order

to allow people to carry out the plan. The managerial accountant, plays a critical role in putting

business strategies into motion. To enable management to manoeuvre the company, information

structures must be created. Management should be confident that stock will be accessible when

required that efficient resources (individuals and industrial equipment) will be accessible when

necessary and also that transportations networks will be accessible to produce production, among

other things. In addition, administration must be prepared to show that contracts and legislation

are being followed. These are difficult tasks that can only be accomplished with the help of good

information tools offered by management accounting professionals (Macve, 2015).

Conclusion

Form above study this has been articulated that Every company has bottom line that

stems from organization's objectives. Company can define fiscal targets and decide what

performance looks like in terms of bottom line through using the business finance. Financial

targets tell about approaching sustainability or whether company is stuck in a rut despite best

efforts.

happen across a continuum of planning, guiding, and regulating operations, and (3) quality

decisions making could only be reliably achieved through knowledge reliance.

Planning: A company must prepare for its success. What is the concept of planning? It's all about

agreeing on course of actions to achieve a specific goal. All stages of planning are required.

First, it happens at the very top of setting key strategy hierarchy. It then goes on to more broad-

based discussion of how to find the best “position” to increase the likelihood of achieving goals.

Eventually, planning must take into account fiscal realities/constraints as well as expected

monetary results (budgets). A company enterprise may be formed of a large number of people.

Such individuals should be brought together to function in unison.

It's crucial that they communicate and comprehend the church's plans. In nutshell, "everyone

must be on same page." As a result, consistent communication is critical.

Monitoring: There are lot of positive plans which never come to fruition. A plan's realization

necessitates the start and course of various acts. These acts must frequently be well-

coordinated and scheduled. Resources should be, available and approvals has to be within order

to allow people to carry out the plan. The managerial accountant, plays a critical role in putting

business strategies into motion. To enable management to manoeuvre the company, information

structures must be created. Management should be confident that stock will be accessible when

required that efficient resources (individuals and industrial equipment) will be accessible when

necessary and also that transportations networks will be accessible to produce production, among

other things. In addition, administration must be prepared to show that contracts and legislation

are being followed. These are difficult tasks that can only be accomplished with the help of good

information tools offered by management accounting professionals (Macve, 2015).

Conclusion

Form above study this has been articulated that Every company has bottom line that

stems from organization's objectives. Company can define fiscal targets and decide what

performance looks like in terms of bottom line through using the business finance. Financial

targets tell about approaching sustainability or whether company is stuck in a rut despite best

efforts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and Journals:

Melé, D., Rosanas, J.M. and Fontrodona, J., 2017. Ethics in finance and accounting: Editorial

introduction. Journal of Business Ethics, 140(4), pp.609-613.

Pendley, J.A., 2018. Finance and accounting professionals and cybersecurity awareness. Journal

of Corporate Accounting & Finance, 29(1), pp.53-58.

Fields, E., 2016. The essentials of finance and accounting for nonfinancial managers. Amacom.

Hertz, S. and Friedman, H.H., 2015. Why Spirituality Belongs in the Finance and Accounting

Curricula. Journal of Accounting & Finance (2158-3625), 15(5).

Galarza, M., 2017. The changing nature of accounting. Strategic Finance, 98(8), p.50.

Fabozzi, F.J., 2016. Entrepreneurial Finance and Accounting for High-Tech Companies. MIT

Press.

McLaney, E. and Atrill, P., 2016. Accounting and finance: an introduction. Prentice Hill.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Macve, R.H., 2015. Fair value vs conservatism? Aspects of the history of accounting, auditing,

business and finance from ancient Mesopotamia to modern China. The British

Accounting Review, 47(2), pp.124-141.

Popovic, S., Ugirnovic, M. and Tomasevic, S., 2015. Management of agricultural enterprises by

means of fair financial reporting in accordance with international standards of the

finance and accounting reporting. Communications in Dependability and Quality

Management, 18(3), pp.24-30.

Books and Journals:

Melé, D., Rosanas, J.M. and Fontrodona, J., 2017. Ethics in finance and accounting: Editorial

introduction. Journal of Business Ethics, 140(4), pp.609-613.

Pendley, J.A., 2018. Finance and accounting professionals and cybersecurity awareness. Journal

of Corporate Accounting & Finance, 29(1), pp.53-58.

Fields, E., 2016. The essentials of finance and accounting for nonfinancial managers. Amacom.

Hertz, S. and Friedman, H.H., 2015. Why Spirituality Belongs in the Finance and Accounting

Curricula. Journal of Accounting & Finance (2158-3625), 15(5).

Galarza, M., 2017. The changing nature of accounting. Strategic Finance, 98(8), p.50.

Fabozzi, F.J., 2016. Entrepreneurial Finance and Accounting for High-Tech Companies. MIT

Press.

McLaney, E. and Atrill, P., 2016. Accounting and finance: an introduction. Prentice Hill.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Macve, R.H., 2015. Fair value vs conservatism? Aspects of the history of accounting, auditing,

business and finance from ancient Mesopotamia to modern China. The British

Accounting Review, 47(2), pp.124-141.

Popovic, S., Ugirnovic, M. and Tomasevic, S., 2015. Management of agricultural enterprises by

means of fair financial reporting in accordance with international standards of the

finance and accounting reporting. Communications in Dependability and Quality

Management, 18(3), pp.24-30.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.