Business Decision Making Essay: Project Selection and Analysis

VerifiedAdded on 2022/08/31

|10

|1861

|27

Essay

AI Summary

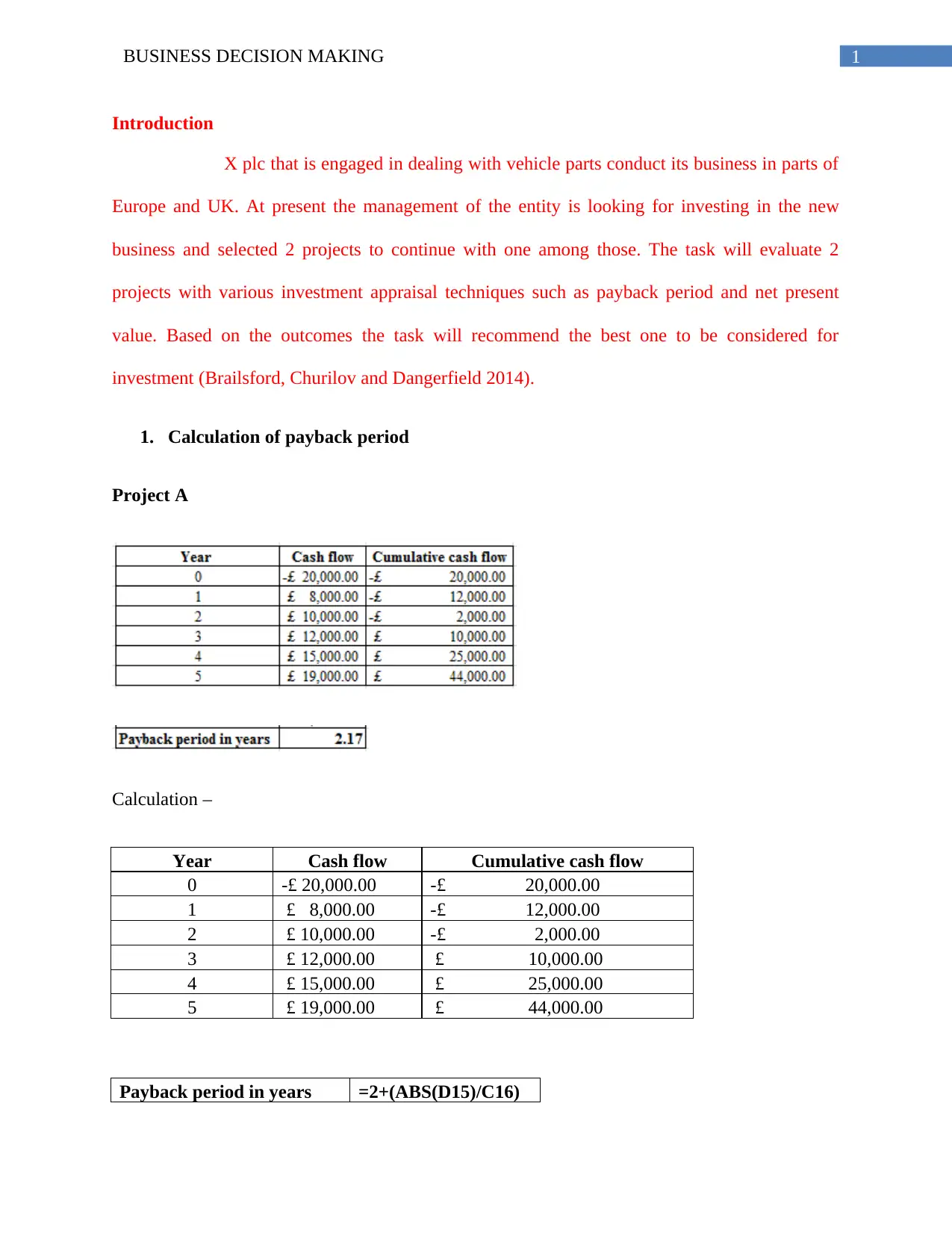

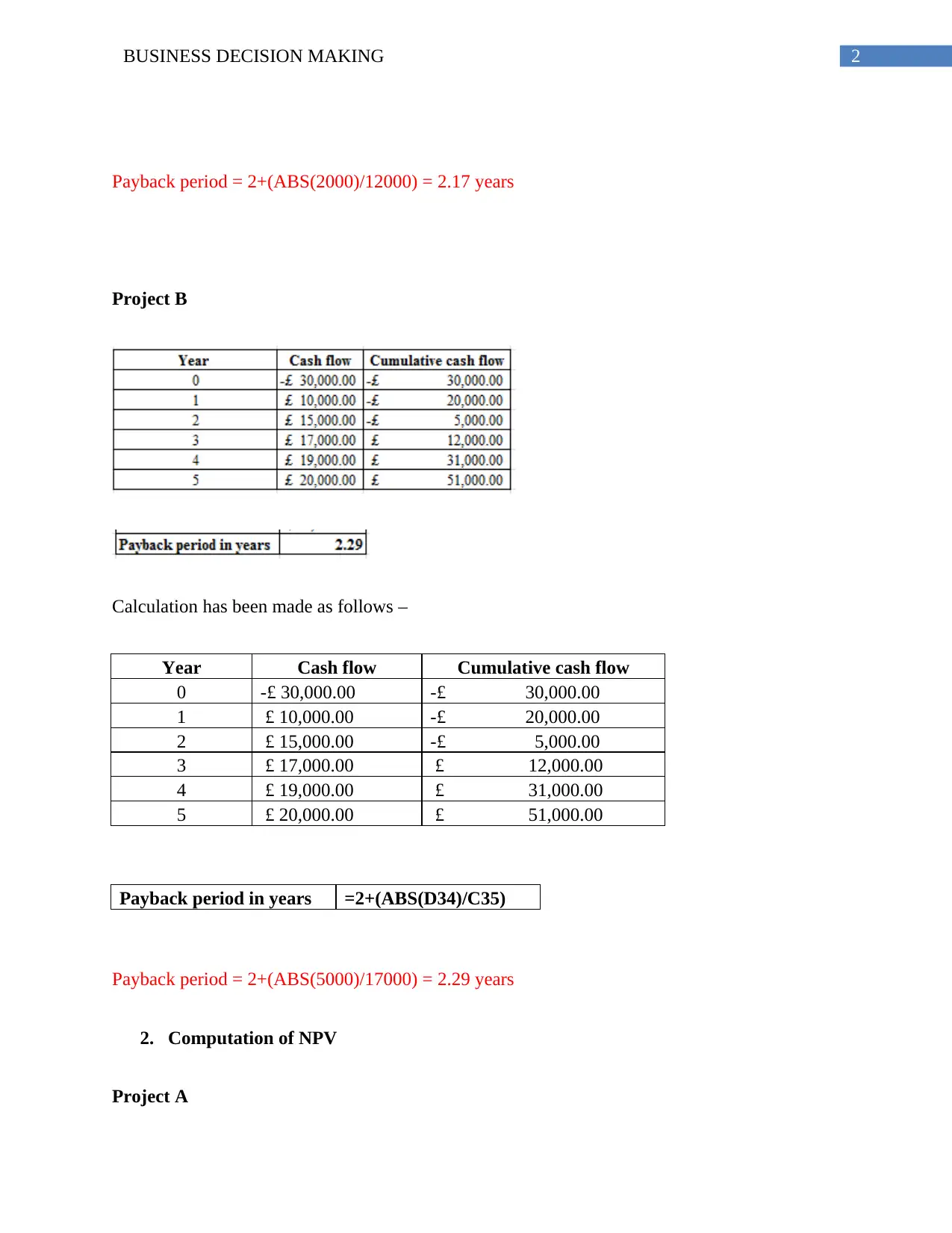

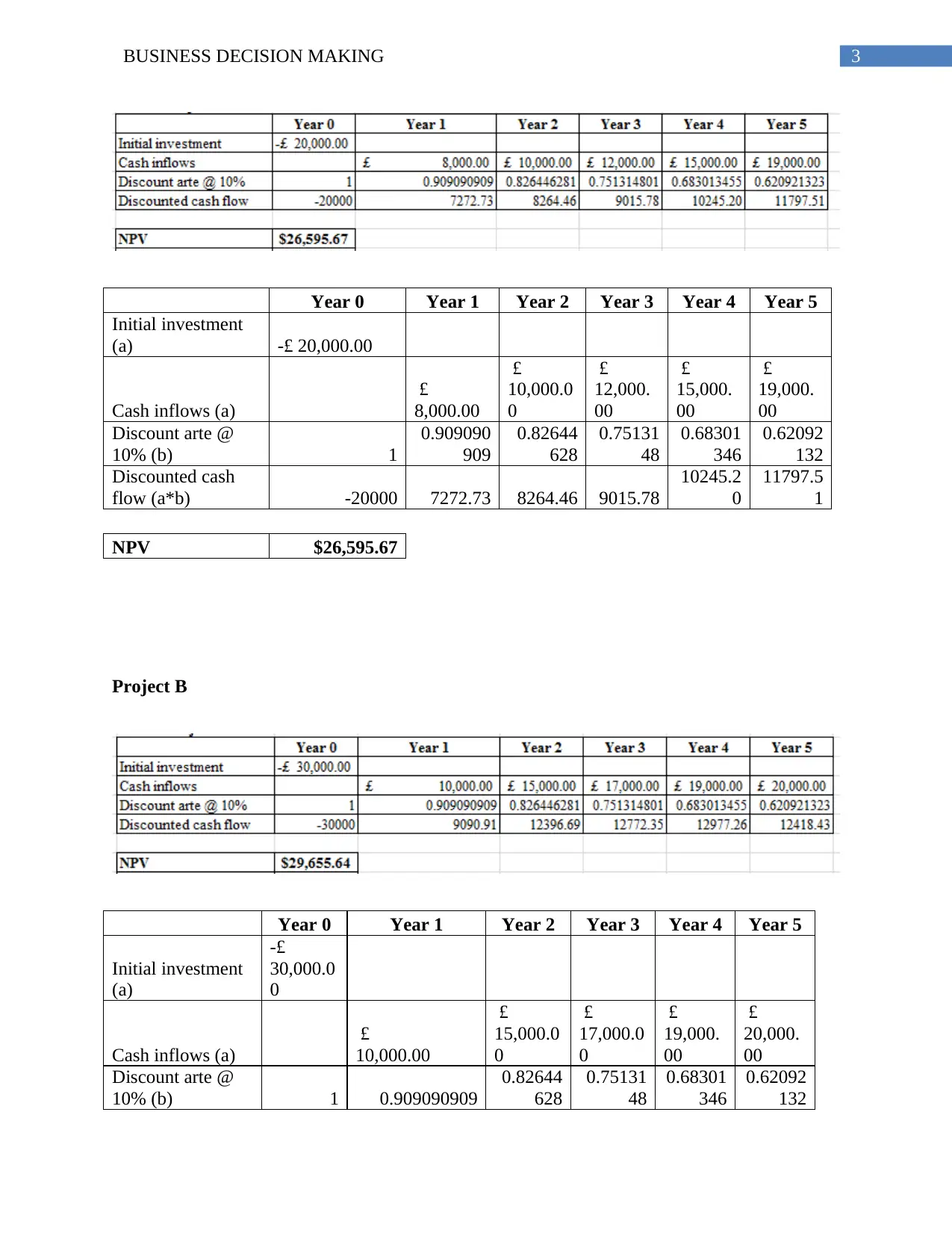

This essay analyzes business decision-making processes, focusing on project appraisal techniques used by X plc, a vehicle parts company. The essay evaluates two potential investment projects using the payback period and net present value (NPV) methods. Calculations and analyses are provided for both projects, leading to a recommendation on which project to invest in. The essay highlights the advantages and disadvantages of each technique, emphasizing the importance of considering the time value of money. Financial factors like return on investment and opportunity cost, along with non-financial factors such as employee morale and legislative requirements, are also discussed. The practical implications of management decisions and the importance of considering shareholder preferences are also included. The essay concludes by recommending project B, which has a higher NPV, as the more profitable investment for X plc.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.