AYB200 S1 2019 Financial Accounting: Business Report Analysis

VerifiedAdded on 2023/01/16

|10

|1604

|59

Report

AI Summary

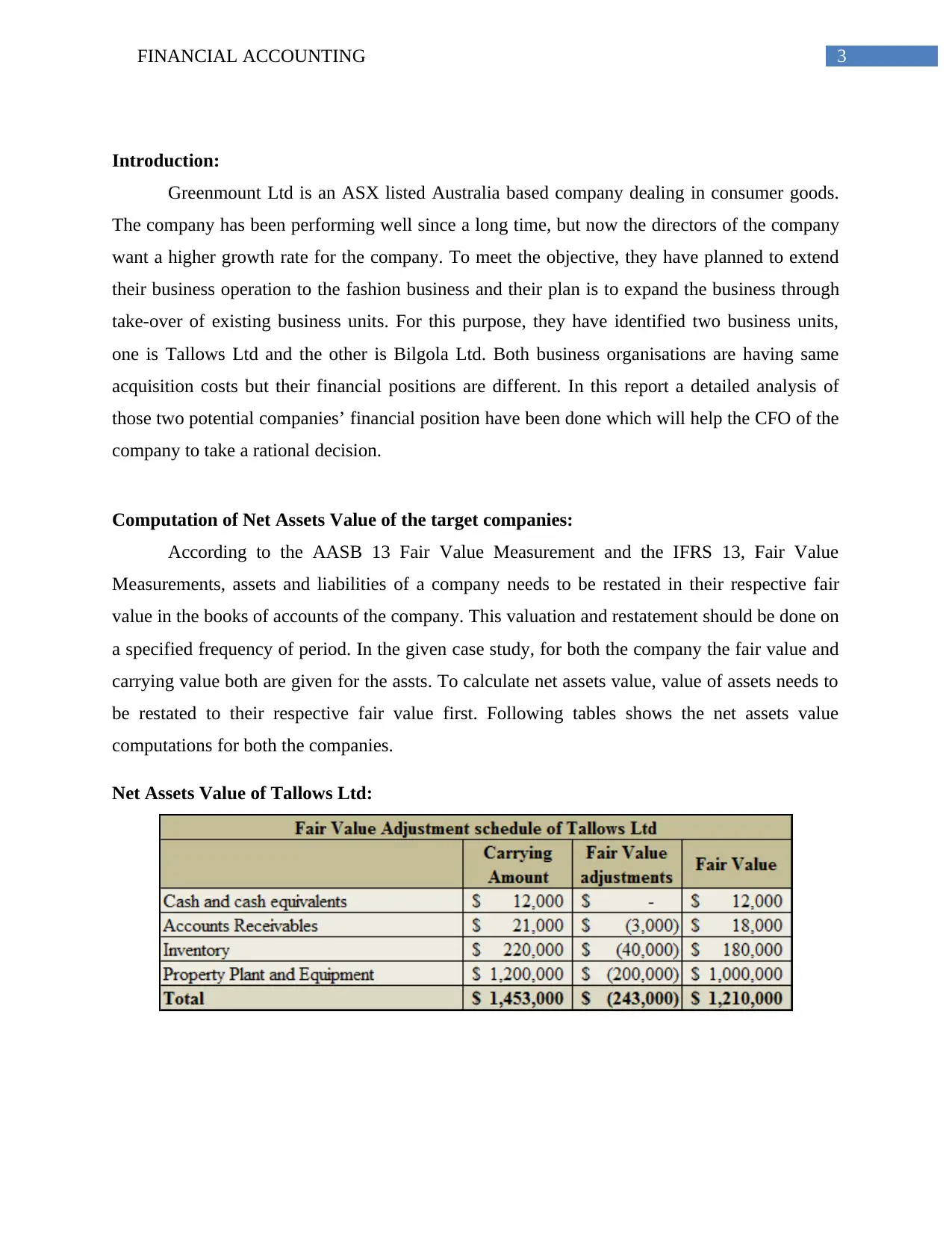

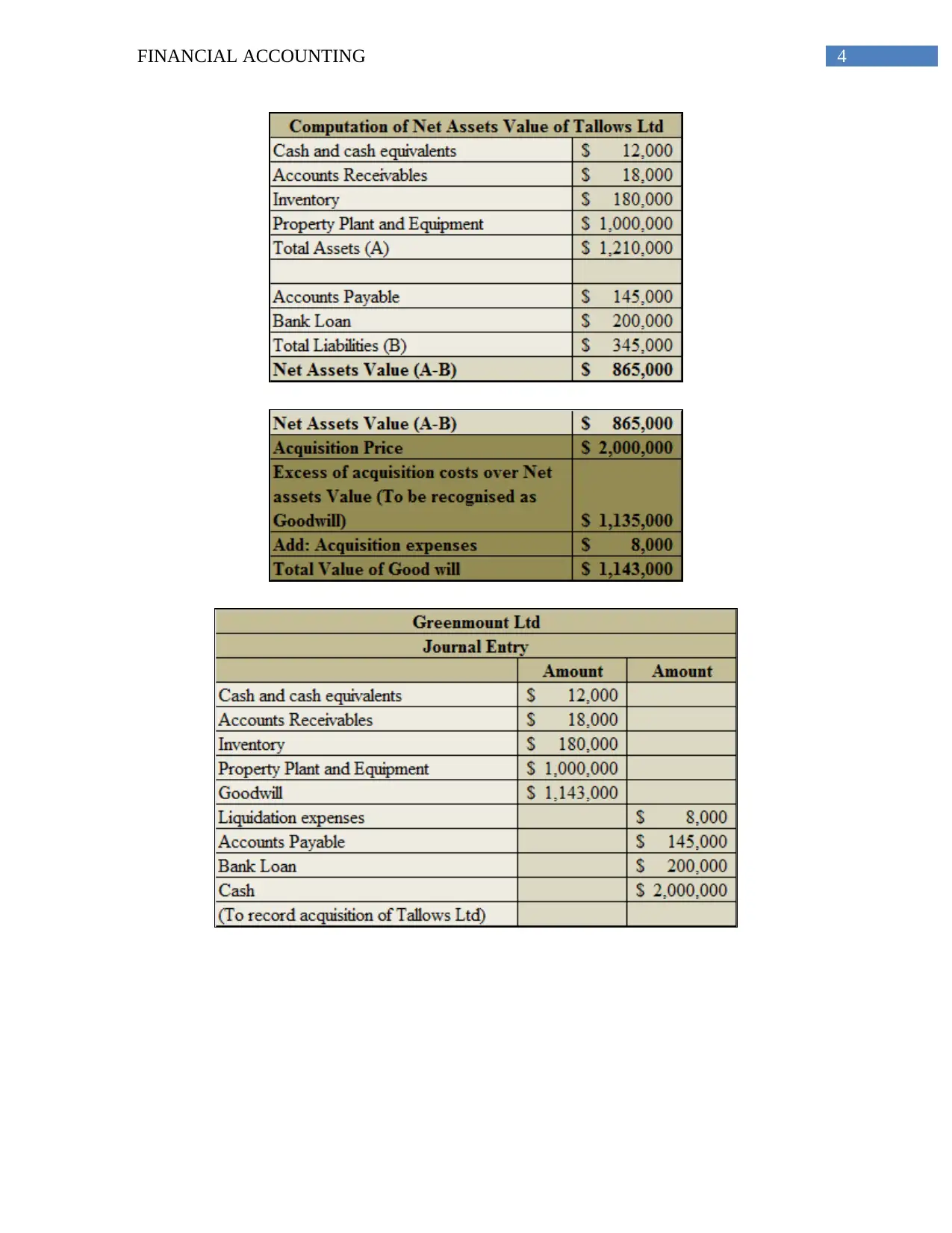

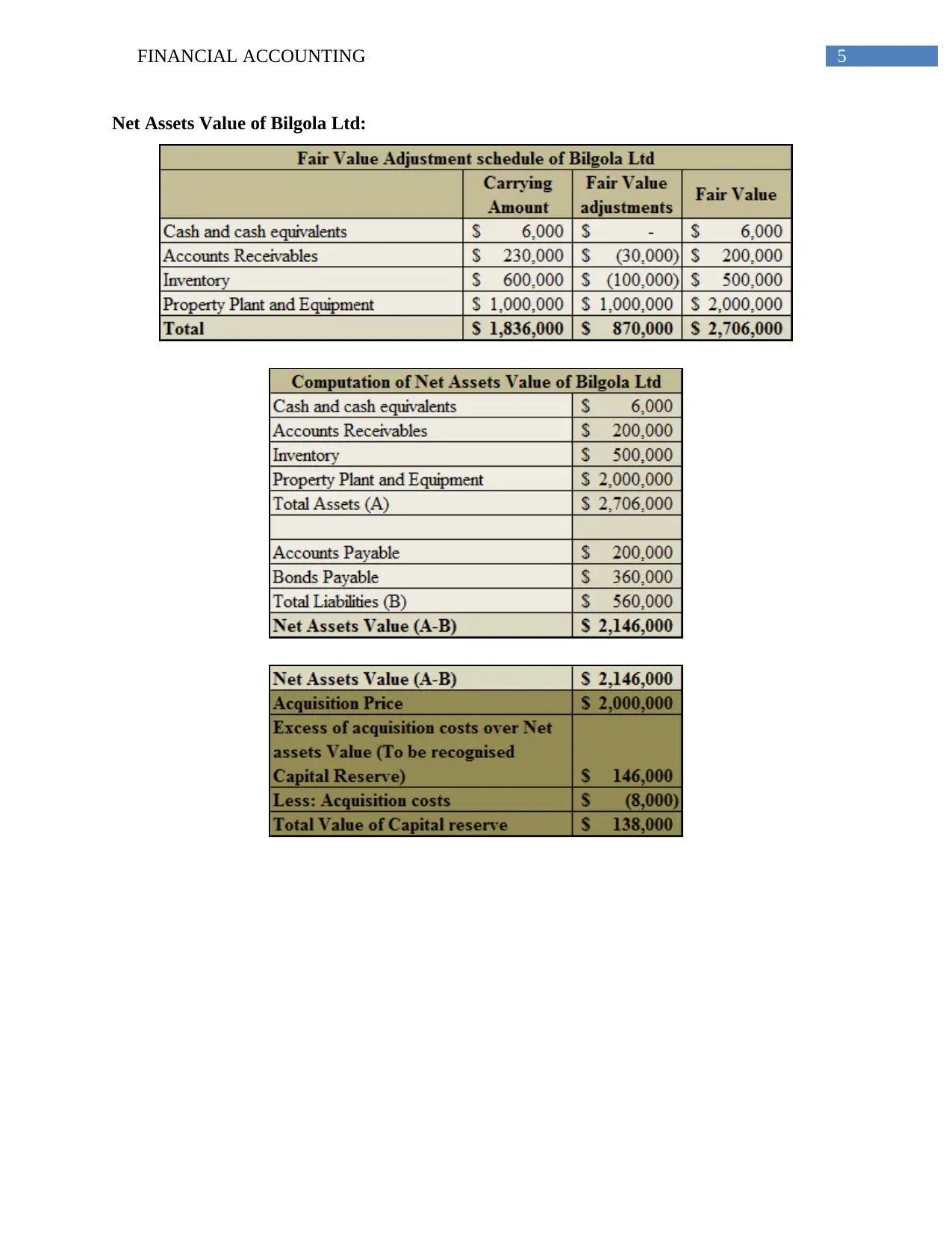

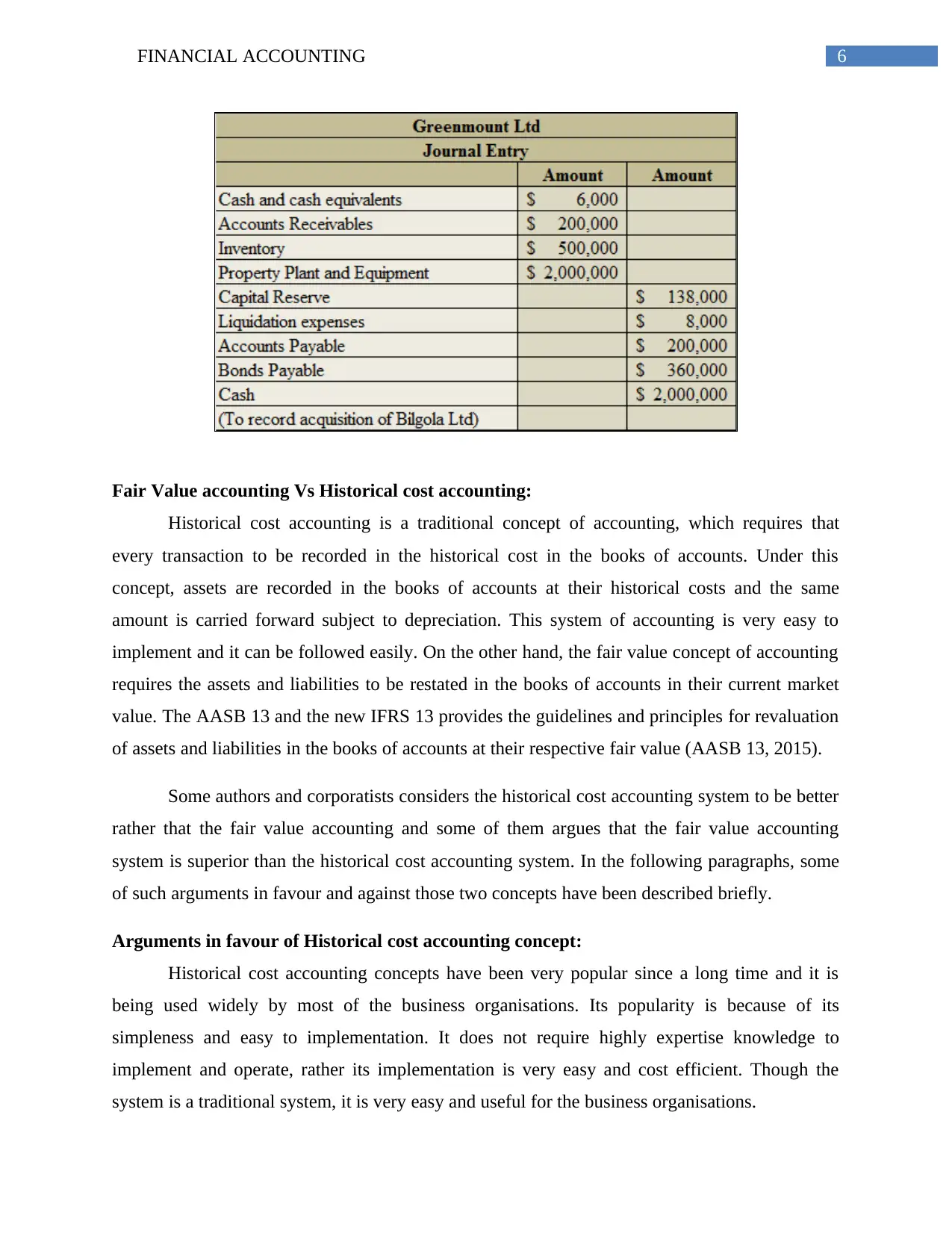

This report provides a detailed financial analysis of Greenmount Ltd, an ASX-listed company considering expanding into the fashion business through acquisitions. The report begins with an executive summary and table of contents, followed by an introduction outlining Greenmount Ltd's goals and the identification of two potential acquisition targets: Tallows Ltd and Bilgola Ltd. The core of the analysis involves computing the net asset value of both target companies, using fair value accounting principles as outlined in AASB 13 and IFRS 13. The report then contrasts fair value accounting with historical cost accounting, presenting arguments for and against each method. The conclusion synthesizes the findings and recommends that Greenmount Ltd acquire Bilgola Ltd based on its higher net asset value and favorable plant, property, and equipment life. The report references relevant accounting standards and academic literature to support its analysis and recommendations.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.