Sale of Business: Comprehensive Analysis of Instructions and Contract

VerifiedAdded on 2022/08/19

|33

|15453

|20

Project

AI Summary

This assignment presents a detailed legal analysis of a business sale, beginning with client instructions and progressing through the drafting and review of a contract of sale. The scenario involves Charles John Dickenson selling 'Food Glorious Food' to Olivia Twiss, outlining the sale price, assets, deposit, settlement date, and other key terms. The analysis covers the vendor's legal obligations, including providing a vendor statement, addressing capital gains tax (CGT) and goods and services tax (GST) implications, and obtaining necessary consents for lease transfer. The assignment also examines special conditions such as rental reductions and weekly takings, as well as the transfer of a hire agreement for a neon sign. It highlights the importance of obtaining landlord and mortgagee consent, the requirements for a going concern exemption from GST, and the limitations of the legal retainer. The document includes the contract of sale and relevant attachments such as the duties form and email correspondence. Finally, the document includes a property sale scenario of 58 Melva Circuit, St Kilda, VIC 3182 involving the sale of a residential property. The file opening steps, title searches, and duties form details are provided for analysis.

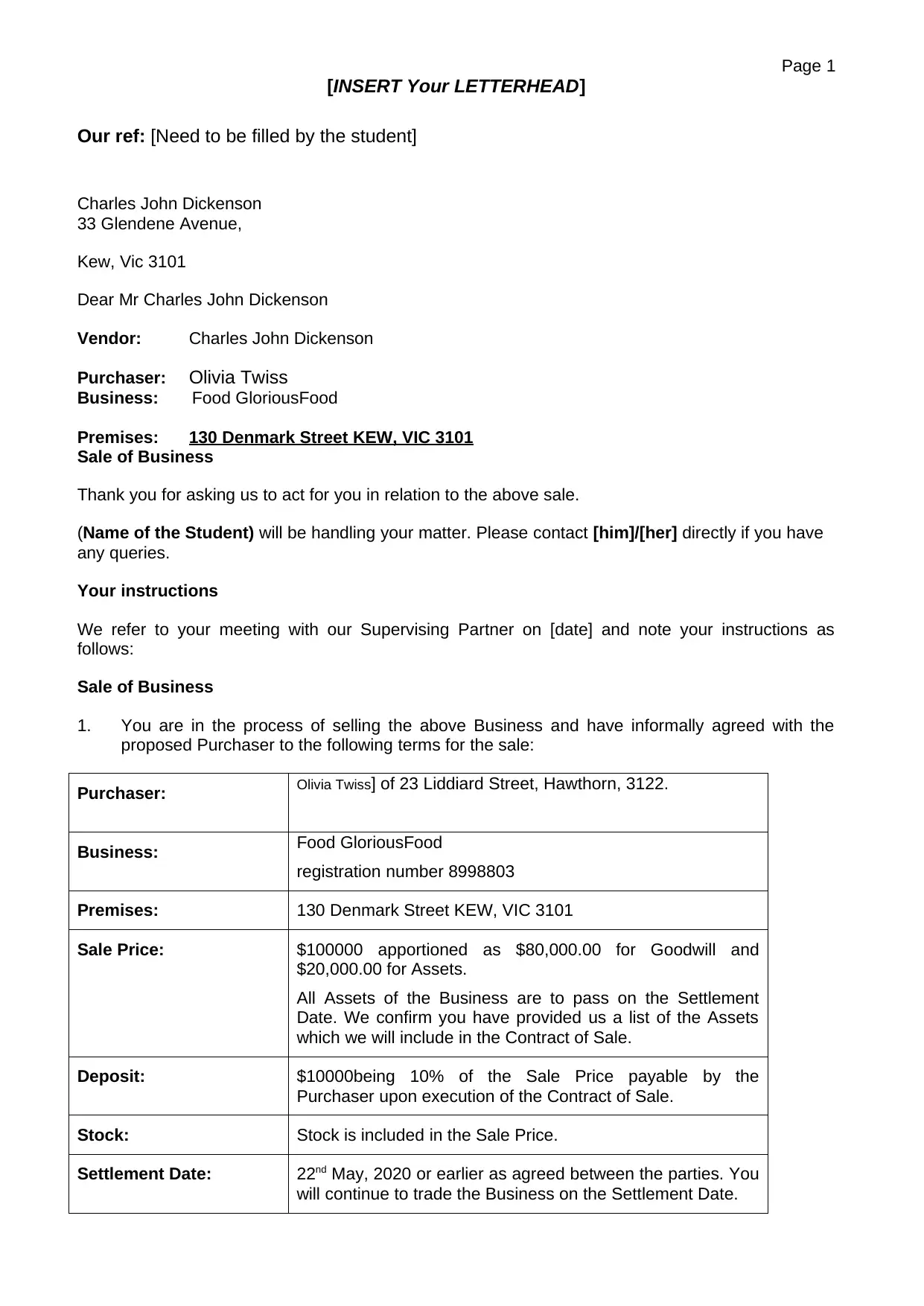

Page 1

[INSERT Your LETTERHEAD]

Our ref: [Need to be filled by the student]

Charles John Dickenson

33 Glendene Avenue,

Kew, Vic 3101

Dear Mr Charles John Dickenson

Vendor: Charles John Dickenson

Purchaser: Olivia Twiss

Business: Food GloriousFood

Premises: 130 Denmark Street KEW, VIC 3101

Sale of Business

Thank you for asking us to act for you in relation to the above sale.

(Name of the Student) will be handling your matter. Please contact [him]/[her] directly if you have

any queries.

Your instructions

We refer to your meeting with our Supervising Partner on [date] and note your instructions as

follows:

Sale of Business

1. You are in the process of selling the above Business and have informally agreed with the

proposed Purchaser to the following terms for the sale:

Purchaser: Olivia Twiss] of 23 Liddiard Street, Hawthorn, 3122.

Business: Food GloriousFood

registration number 8998803

Premises: 130 Denmark Street KEW, VIC 3101

Sale Price: $100000 apportioned as $80,000.00 for Goodwill and

$20,000.00 for Assets.

All Assets of the Business are to pass on the Settlement

Date. We confirm you have provided us a list of the Assets

which we will include in the Contract of Sale.

Deposit: $10000being 10% of the Sale Price payable by the

Purchaser upon execution of the Contract of Sale.

Stock: Stock is included in the Sale Price.

Settlement Date: 22nd May, 2020 or earlier as agreed between the parties. You

will continue to trade the Business on the Settlement Date.

[INSERT Your LETTERHEAD]

Our ref: [Need to be filled by the student]

Charles John Dickenson

33 Glendene Avenue,

Kew, Vic 3101

Dear Mr Charles John Dickenson

Vendor: Charles John Dickenson

Purchaser: Olivia Twiss

Business: Food GloriousFood

Premises: 130 Denmark Street KEW, VIC 3101

Sale of Business

Thank you for asking us to act for you in relation to the above sale.

(Name of the Student) will be handling your matter. Please contact [him]/[her] directly if you have

any queries.

Your instructions

We refer to your meeting with our Supervising Partner on [date] and note your instructions as

follows:

Sale of Business

1. You are in the process of selling the above Business and have informally agreed with the

proposed Purchaser to the following terms for the sale:

Purchaser: Olivia Twiss] of 23 Liddiard Street, Hawthorn, 3122.

Business: Food GloriousFood

registration number 8998803

Premises: 130 Denmark Street KEW, VIC 3101

Sale Price: $100000 apportioned as $80,000.00 for Goodwill and

$20,000.00 for Assets.

All Assets of the Business are to pass on the Settlement

Date. We confirm you have provided us a list of the Assets

which we will include in the Contract of Sale.

Deposit: $10000being 10% of the Sale Price payable by the

Purchaser upon execution of the Contract of Sale.

Stock: Stock is included in the Sale Price.

Settlement Date: 22nd May, 2020 or earlier as agreed between the parties. You

will continue to trade the Business on the Settlement Date.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

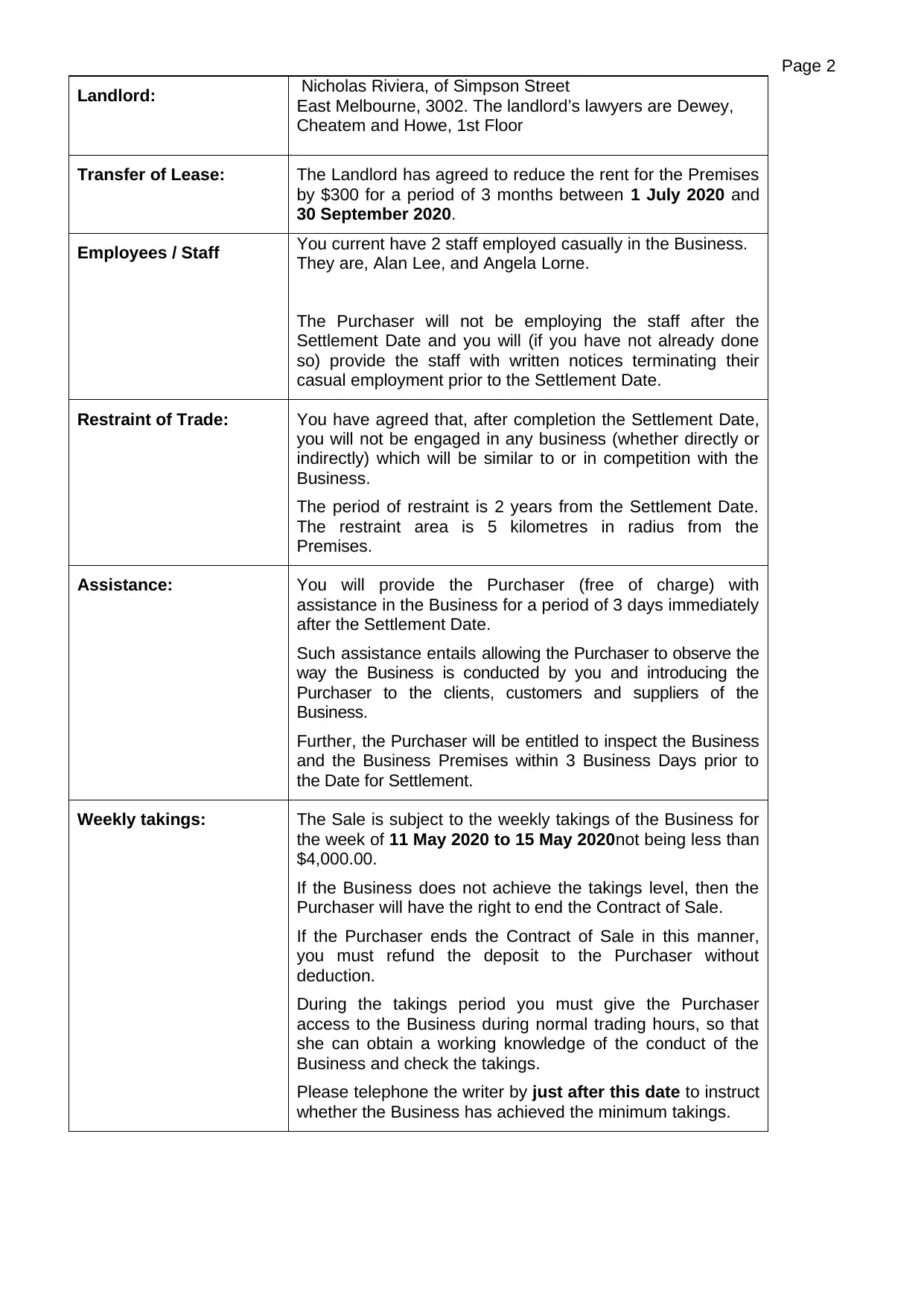

Page 2

Landlord: Nicholas Riviera, of Simpson Street

East Melbourne, 3002. The landlord’s lawyers are Dewey,

Cheatem and Howe, 1st Floor

Transfer of Lease: The Landlord has agreed to reduce the rent for the Premises

by $300 for a period of 3 months between 1 July 2020 and

30 September 2020.

Employees / Staff You current have 2 staff employed casually in the Business.

They are, Alan Lee, and Angela Lorne.

The Purchaser will not be employing the staff after the

Settlement Date and you will (if you have not already done

so) provide the staff with written notices terminating their

casual employment prior to the Settlement Date.

Restraint of Trade: You have agreed that, after completion the Settlement Date,

you will not be engaged in any business (whether directly or

indirectly) which will be similar to or in competition with the

Business.

The period of restraint is 2 years from the Settlement Date.

The restraint area is 5 kilometres in radius from the

Premises.

Assistance: You will provide the Purchaser (free of charge) with

assistance in the Business for a period of 3 days immediately

after the Settlement Date.

Such assistance entails allowing the Purchaser to observe the

way the Business is conducted by you and introducing the

Purchaser to the clients, customers and suppliers of the

Business.

Further, the Purchaser will be entitled to inspect the Business

and the Business Premises within 3 Business Days prior to

the Date for Settlement.

Weekly takings: The Sale is subject to the weekly takings of the Business for

the week of 11 May 2020 to 15 May 2020not being less than

$4,000.00.

If the Business does not achieve the takings level, then the

Purchaser will have the right to end the Contract of Sale.

If the Purchaser ends the Contract of Sale in this manner,

you must refund the deposit to the Purchaser without

deduction.

During the takings period you must give the Purchaser

access to the Business during normal trading hours, so that

she can obtain a working knowledge of the conduct of the

Business and check the takings.

Please telephone the writer by just after this date to instruct

whether the Business has achieved the minimum takings.

Landlord: Nicholas Riviera, of Simpson Street

East Melbourne, 3002. The landlord’s lawyers are Dewey,

Cheatem and Howe, 1st Floor

Transfer of Lease: The Landlord has agreed to reduce the rent for the Premises

by $300 for a period of 3 months between 1 July 2020 and

30 September 2020.

Employees / Staff You current have 2 staff employed casually in the Business.

They are, Alan Lee, and Angela Lorne.

The Purchaser will not be employing the staff after the

Settlement Date and you will (if you have not already done

so) provide the staff with written notices terminating their

casual employment prior to the Settlement Date.

Restraint of Trade: You have agreed that, after completion the Settlement Date,

you will not be engaged in any business (whether directly or

indirectly) which will be similar to or in competition with the

Business.

The period of restraint is 2 years from the Settlement Date.

The restraint area is 5 kilometres in radius from the

Premises.

Assistance: You will provide the Purchaser (free of charge) with

assistance in the Business for a period of 3 days immediately

after the Settlement Date.

Such assistance entails allowing the Purchaser to observe the

way the Business is conducted by you and introducing the

Purchaser to the clients, customers and suppliers of the

Business.

Further, the Purchaser will be entitled to inspect the Business

and the Business Premises within 3 Business Days prior to

the Date for Settlement.

Weekly takings: The Sale is subject to the weekly takings of the Business for

the week of 11 May 2020 to 15 May 2020not being less than

$4,000.00.

If the Business does not achieve the takings level, then the

Purchaser will have the right to end the Contract of Sale.

If the Purchaser ends the Contract of Sale in this manner,

you must refund the deposit to the Purchaser without

deduction.

During the takings period you must give the Purchaser

access to the Business during normal trading hours, so that

she can obtain a working knowledge of the conduct of the

Business and check the takings.

Please telephone the writer by just after this date to instruct

whether the Business has achieved the minimum takings.

Page 3

Hire Agreement: The Business has a verbal hire agreement with Beta Neon

Pty Ltd (“Beta”) for a neon sign board.

Under that agreement, you pay $[amount] per quarter in

advance as invoiced by Beta.

There are no outstanding payments. Beta has indicated, in

writing, that it will transfer the hire agreement to the

Purchaser at settlement.

You have provided the Purchaser with a copy of the letter

from Beta.

2. Under the lease you must pay for building insurance. This amount will be adjustable at

settlement. You have provided us with a letter from National Capital Insurance Ltd which

indicates that that you have paid for the current period. We note your instructions you have

provided the purchaser with a copy of this letter.

3. You want us to prepare the Contract of Sale and attend to all necessary steps in the sale of

the Business.

We confirm that you have provided us with a copy of the lease agreement over the Premises

between you and the Landlord. We will assist you to transfer this lease into the Purchaser’s name as

part of the sale. The Purchaser is responsible for preparing the Transfer of Lease form, and we will

forward this document to you when we receive it and will advise you about it in more detail.

As the Premises is subject to a lease agreement and a mortgage agreement, the consent of both

the Landlord and their mortgagee is required. This requirement protects the Purchase’s interests, as

the Landlord or mortgagor would be entitled to deny the Purchaser access from the Premises if the

business was sold without their consent. It is the Vendor’s legal responsibility to obtain this consent.

We will assist you to obtain consent from the Landlord’s legal representatives.

We note in your instructions that the landlord has agreed to a rental reduction as outlined above. We

further note that you have provided a disclosure statement by the tenant regarding an assigned

lease as required by s 61(5) of the Retail Leases Act 2003 and that the statement has been signed

by the Landlord and the Purchaser.

Section 52 Vendor Statement

We confirm that you have provided us with a statement of a vendor of a small business, as required

under s 52 of the Estate Agents Act 1980 (Vic) and note that it has been signed by the Vendor and

the Purchaser.

It is important that you are aware of your legal obligations regarding this statement. The statement

must be provided to the Purchaser, and the Purchaser must acknowledge that they have received it,

before the Purchaser agrees to the sale. If the Vendor fails to provide a statement in the correct

form and containing all the required information, then the Purchaser is entitled to cancel the

contract. The Vendor would then be obligated to repay any money paid by the Purchaser regarding

the sale. The Vendor may also be guilty of an offence under the Act and liable to pay a penalty of up

to $1652.20.

We have reviewed the statement you provided, and we confirm that it is in the correct form and

contains all information required under the law. We note that the Purchaser has signed the

statement, acknowledging that she has received it.

Capital Gains Tax (“CGT”) and Goods and Services Tax (“GST”)

CGT

Hire Agreement: The Business has a verbal hire agreement with Beta Neon

Pty Ltd (“Beta”) for a neon sign board.

Under that agreement, you pay $[amount] per quarter in

advance as invoiced by Beta.

There are no outstanding payments. Beta has indicated, in

writing, that it will transfer the hire agreement to the

Purchaser at settlement.

You have provided the Purchaser with a copy of the letter

from Beta.

2. Under the lease you must pay for building insurance. This amount will be adjustable at

settlement. You have provided us with a letter from National Capital Insurance Ltd which

indicates that that you have paid for the current period. We note your instructions you have

provided the purchaser with a copy of this letter.

3. You want us to prepare the Contract of Sale and attend to all necessary steps in the sale of

the Business.

We confirm that you have provided us with a copy of the lease agreement over the Premises

between you and the Landlord. We will assist you to transfer this lease into the Purchaser’s name as

part of the sale. The Purchaser is responsible for preparing the Transfer of Lease form, and we will

forward this document to you when we receive it and will advise you about it in more detail.

As the Premises is subject to a lease agreement and a mortgage agreement, the consent of both

the Landlord and their mortgagee is required. This requirement protects the Purchase’s interests, as

the Landlord or mortgagor would be entitled to deny the Purchaser access from the Premises if the

business was sold without their consent. It is the Vendor’s legal responsibility to obtain this consent.

We will assist you to obtain consent from the Landlord’s legal representatives.

We note in your instructions that the landlord has agreed to a rental reduction as outlined above. We

further note that you have provided a disclosure statement by the tenant regarding an assigned

lease as required by s 61(5) of the Retail Leases Act 2003 and that the statement has been signed

by the Landlord and the Purchaser.

Section 52 Vendor Statement

We confirm that you have provided us with a statement of a vendor of a small business, as required

under s 52 of the Estate Agents Act 1980 (Vic) and note that it has been signed by the Vendor and

the Purchaser.

It is important that you are aware of your legal obligations regarding this statement. The statement

must be provided to the Purchaser, and the Purchaser must acknowledge that they have received it,

before the Purchaser agrees to the sale. If the Vendor fails to provide a statement in the correct

form and containing all the required information, then the Purchaser is entitled to cancel the

contract. The Vendor would then be obligated to repay any money paid by the Purchaser regarding

the sale. The Vendor may also be guilty of an offence under the Act and liable to pay a penalty of up

to $1652.20.

We have reviewed the statement you provided, and we confirm that it is in the correct form and

contains all information required under the law. We note that the Purchaser has signed the

statement, acknowledging that she has received it.

Capital Gains Tax (“CGT”) and Goods and Services Tax (“GST”)

CGT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

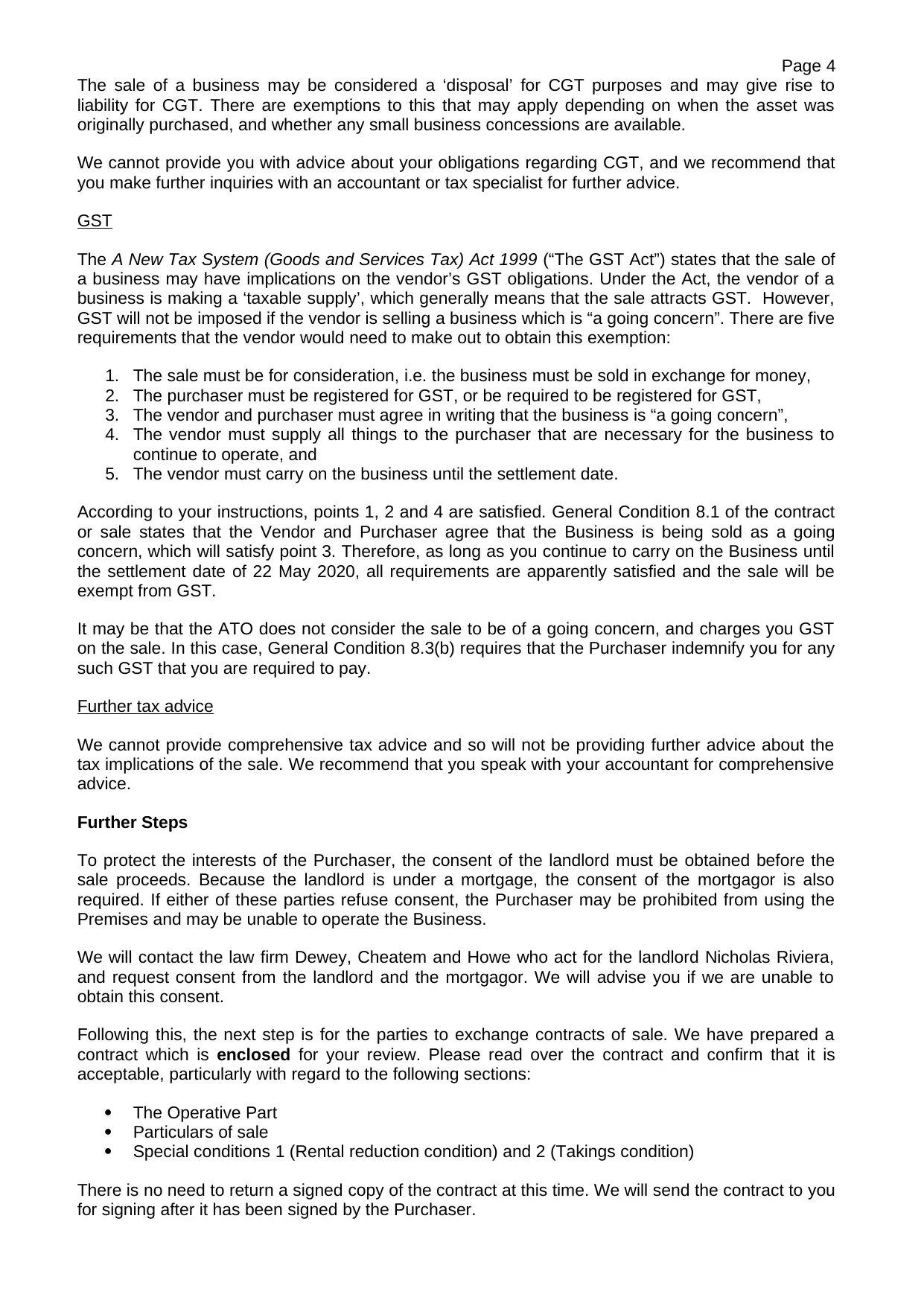

Page 4

The sale of a business may be considered a ‘disposal’ for CGT purposes and may give rise to

liability for CGT. There are exemptions to this that may apply depending on when the asset was

originally purchased, and whether any small business concessions are available.

We cannot provide you with advice about your obligations regarding CGT, and we recommend that

you make further inquiries with an accountant or tax specialist for further advice.

GST

The A New Tax System (Goods and Services Tax) Act 1999 (“The GST Act”) states that the sale of

a business may have implications on the vendor’s GST obligations. Under the Act, the vendor of a

business is making a ‘taxable supply’, which generally means that the sale attracts GST. However,

GST will not be imposed if the vendor is selling a business which is “a going concern”. There are five

requirements that the vendor would need to make out to obtain this exemption:

1. The sale must be for consideration, i.e. the business must be sold in exchange for money,

2. The purchaser must be registered for GST, or be required to be registered for GST,

3. The vendor and purchaser must agree in writing that the business is “a going concern”,

4. The vendor must supply all things to the purchaser that are necessary for the business to

continue to operate, and

5. The vendor must carry on the business until the settlement date.

According to your instructions, points 1, 2 and 4 are satisfied. General Condition 8.1 of the contract

or sale states that the Vendor and Purchaser agree that the Business is being sold as a going

concern, which will satisfy point 3. Therefore, as long as you continue to carry on the Business until

the settlement date of 22 May 2020, all requirements are apparently satisfied and the sale will be

exempt from GST.

It may be that the ATO does not consider the sale to be of a going concern, and charges you GST

on the sale. In this case, General Condition 8.3(b) requires that the Purchaser indemnify you for any

such GST that you are required to pay.

Further tax advice

We cannot provide comprehensive tax advice and so will not be providing further advice about the

tax implications of the sale. We recommend that you speak with your accountant for comprehensive

advice.

Further Steps

To protect the interests of the Purchaser, the consent of the landlord must be obtained before the

sale proceeds. Because the landlord is under a mortgage, the consent of the mortgagor is also

required. If either of these parties refuse consent, the Purchaser may be prohibited from using the

Premises and may be unable to operate the Business.

We will contact the law firm Dewey, Cheatem and Howe who act for the landlord Nicholas Riviera,

and request consent from the landlord and the mortgagor. We will advise you if we are unable to

obtain this consent.

Following this, the next step is for the parties to exchange contracts of sale. We have prepared a

contract which is enclosed for your review. Please read over the contract and confirm that it is

acceptable, particularly with regard to the following sections:

The Operative Part

Particulars of sale

Special conditions 1 (Rental reduction condition) and 2 (Takings condition)

There is no need to return a signed copy of the contract at this time. We will send the contract to you

for signing after it has been signed by the Purchaser.

The sale of a business may be considered a ‘disposal’ for CGT purposes and may give rise to

liability for CGT. There are exemptions to this that may apply depending on when the asset was

originally purchased, and whether any small business concessions are available.

We cannot provide you with advice about your obligations regarding CGT, and we recommend that

you make further inquiries with an accountant or tax specialist for further advice.

GST

The A New Tax System (Goods and Services Tax) Act 1999 (“The GST Act”) states that the sale of

a business may have implications on the vendor’s GST obligations. Under the Act, the vendor of a

business is making a ‘taxable supply’, which generally means that the sale attracts GST. However,

GST will not be imposed if the vendor is selling a business which is “a going concern”. There are five

requirements that the vendor would need to make out to obtain this exemption:

1. The sale must be for consideration, i.e. the business must be sold in exchange for money,

2. The purchaser must be registered for GST, or be required to be registered for GST,

3. The vendor and purchaser must agree in writing that the business is “a going concern”,

4. The vendor must supply all things to the purchaser that are necessary for the business to

continue to operate, and

5. The vendor must carry on the business until the settlement date.

According to your instructions, points 1, 2 and 4 are satisfied. General Condition 8.1 of the contract

or sale states that the Vendor and Purchaser agree that the Business is being sold as a going

concern, which will satisfy point 3. Therefore, as long as you continue to carry on the Business until

the settlement date of 22 May 2020, all requirements are apparently satisfied and the sale will be

exempt from GST.

It may be that the ATO does not consider the sale to be of a going concern, and charges you GST

on the sale. In this case, General Condition 8.3(b) requires that the Purchaser indemnify you for any

such GST that you are required to pay.

Further tax advice

We cannot provide comprehensive tax advice and so will not be providing further advice about the

tax implications of the sale. We recommend that you speak with your accountant for comprehensive

advice.

Further Steps

To protect the interests of the Purchaser, the consent of the landlord must be obtained before the

sale proceeds. Because the landlord is under a mortgage, the consent of the mortgagor is also

required. If either of these parties refuse consent, the Purchaser may be prohibited from using the

Premises and may be unable to operate the Business.

We will contact the law firm Dewey, Cheatem and Howe who act for the landlord Nicholas Riviera,

and request consent from the landlord and the mortgagor. We will advise you if we are unable to

obtain this consent.

Following this, the next step is for the parties to exchange contracts of sale. We have prepared a

contract which is enclosed for your review. Please read over the contract and confirm that it is

acceptable, particularly with regard to the following sections:

The Operative Part

Particulars of sale

Special conditions 1 (Rental reduction condition) and 2 (Takings condition)

There is no need to return a signed copy of the contract at this time. We will send the contract to you

for signing after it has been signed by the Purchaser.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 5

Costs

Our fee for acting for you in this matter will be $2,500.00 plus disbursements, provided that the

matter proceeds in a straightforward manner. The fee has been calculated on a lump sum basis. We

do not expect disbursements to exceed $50.00.

We have enclosed a copy of the standard-form costs disclosure agreement, as well as a statement

outlining your rights regarding these costs.

Limitations of Retainer

Our services to you in this matter will be limited to advising on and executing the sale of business

and transfer of lease. We will therefore not be advising you on:

Tax implications of the transfer (other than the CGT and GST advice provided in this letter)

Employment matters

Licensing requirements

Should you have any queries, please do not hesitate to contact Clare Manning.

Encl.

1. Costs disclosure statement

2. Statement of rights accompanying costs disclosure statement

3. Contract of sale

Should you have any queries, please do not hesitate to contact the writer.

Yours faithfully

[Name of the Student]

Attorney-at-Law

Attachment:

Costs

Our fee for acting for you in this matter will be $2,500.00 plus disbursements, provided that the

matter proceeds in a straightforward manner. The fee has been calculated on a lump sum basis. We

do not expect disbursements to exceed $50.00.

We have enclosed a copy of the standard-form costs disclosure agreement, as well as a statement

outlining your rights regarding these costs.

Limitations of Retainer

Our services to you in this matter will be limited to advising on and executing the sale of business

and transfer of lease. We will therefore not be advising you on:

Tax implications of the transfer (other than the CGT and GST advice provided in this letter)

Employment matters

Licensing requirements

Should you have any queries, please do not hesitate to contact Clare Manning.

Encl.

1. Costs disclosure statement

2. Statement of rights accompanying costs disclosure statement

3. Contract of sale

Should you have any queries, please do not hesitate to contact the writer.

Yours faithfully

[Name of the Student]

Attorney-at-Law

Attachment:

Page 6

Contract of

Sale of Business

[Ref: ]

Contract of

Sale of Business

[Ref: ]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page 7

Contents

Operative Part______________________________________3

Signing Page_______________________________________4

Particulars of sale___________________________________5

Special conditions__________________________________8

General Conditions_________________________________9

MONEY__________________________________________9

1. Payments_____________________________________9

2. Settlement____________________________________9

3. Valuing stock________________________________10

4. Apportionment of outgoings and entitlements_____10

5. Vendor’s debts_______________________________11

6. Finance______________________________________11

7. Lease _______________________________________11

8. GST________________________________________12

TRANSACTIONAL_______________________________12

9. Running the business__________________________12

10. Inspection___________________________________12

11. Employees___________________________________12

12. Warranties___________________________________13

13. Restraint of trade_____________________________13

14. Confidential information_______________________14

BREACH OF CONTRACT________________________14

15. Default______________________________________14

LEGAL AND GENERAL__________________________15

16. Service of notices_____________________________15

17. Non merger__________________________________15

18. Severance____________________________________15

19. Guarantee, indemnity and promise_______________15

20. Interpretation_________________________________16

Schedule 1: Assets included in the price_______________17

Schedule 2: Equipment hire contracts_________________18

Schedule 3: Other material contracts__________________19

Schedule 4: Terms of current or new lease_____________20

Schedule 5: Permitted encumbrances__________________22

Schedule 6: Warranties_____________________________23

Warning and Disclaimer

This document is prepared from a precedent intended solely for use by legal practitioners. The parts of the document prepared by the Law

Institute of Victoria are intended for use only by legal practitioners with the knowledge, skill and qualifications required to use the precedent

to create a document suitable for the transaction. This precedent is not a guide and it does not attempt to include all relevant issues or include

all aspects of law or changes to the law.

Legal practitioners using this document should check for any change in the law and ensure that the facts and circumstances for its intended

use are appropriately included.

The Law Institute of Victoria, its contractors and agents are not liable in any way, including, without limitation, negligence, for the use to

which the document may be put, for any errors or omissions in the precedent document, or any other changes or understanding of the law

arising from any legislative instruments or the decision of any court or tribunal, whether before or after this precedent was prepared, first

published, sold or used.

Copyright

The document is copyright. The document may only be reproduced in accordance with an agreement with the Law Institute of Victoria Limited

(ABN 32 075 475 731) for each specific transaction that is authorised. Any person who has purchased a physical copy of this precedent

document may only copy it for the purpose of providing legal services for the specific transaction or documenting the specific transaction.

“Specific transaction” means common parties entering into a legal relationship for the sale and purchase of the same subject matter.

Operative part

The vendor agrees to sell and the purchaser agrees to buy:

1. The Business for the price; and

Contents

Operative Part______________________________________3

Signing Page_______________________________________4

Particulars of sale___________________________________5

Special conditions__________________________________8

General Conditions_________________________________9

MONEY__________________________________________9

1. Payments_____________________________________9

2. Settlement____________________________________9

3. Valuing stock________________________________10

4. Apportionment of outgoings and entitlements_____10

5. Vendor’s debts_______________________________11

6. Finance______________________________________11

7. Lease _______________________________________11

8. GST________________________________________12

TRANSACTIONAL_______________________________12

9. Running the business__________________________12

10. Inspection___________________________________12

11. Employees___________________________________12

12. Warranties___________________________________13

13. Restraint of trade_____________________________13

14. Confidential information_______________________14

BREACH OF CONTRACT________________________14

15. Default______________________________________14

LEGAL AND GENERAL__________________________15

16. Service of notices_____________________________15

17. Non merger__________________________________15

18. Severance____________________________________15

19. Guarantee, indemnity and promise_______________15

20. Interpretation_________________________________16

Schedule 1: Assets included in the price_______________17

Schedule 2: Equipment hire contracts_________________18

Schedule 3: Other material contracts__________________19

Schedule 4: Terms of current or new lease_____________20

Schedule 5: Permitted encumbrances__________________22

Schedule 6: Warranties_____________________________23

Warning and Disclaimer

This document is prepared from a precedent intended solely for use by legal practitioners. The parts of the document prepared by the Law

Institute of Victoria are intended for use only by legal practitioners with the knowledge, skill and qualifications required to use the precedent

to create a document suitable for the transaction. This precedent is not a guide and it does not attempt to include all relevant issues or include

all aspects of law or changes to the law.

Legal practitioners using this document should check for any change in the law and ensure that the facts and circumstances for its intended

use are appropriately included.

The Law Institute of Victoria, its contractors and agents are not liable in any way, including, without limitation, negligence, for the use to

which the document may be put, for any errors or omissions in the precedent document, or any other changes or understanding of the law

arising from any legislative instruments or the decision of any court or tribunal, whether before or after this precedent was prepared, first

published, sold or used.

Copyright

The document is copyright. The document may only be reproduced in accordance with an agreement with the Law Institute of Victoria Limited

(ABN 32 075 475 731) for each specific transaction that is authorised. Any person who has purchased a physical copy of this precedent

document may only copy it for the purpose of providing legal services for the specific transaction or documenting the specific transaction.

“Specific transaction” means common parties entering into a legal relationship for the sale and purchase of the same subject matter.

Operative part

The vendor agrees to sell and the purchaser agrees to buy:

1. The Business for the price; and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 8

2. The Stock of the Business for the value of the Stock calculated under this contract;

as a going concern on the terms set out in this contract.

Each party agrees to promptly perform that party’s obligations contained in this contract.

The guarantor guarantees, indemnifies and promises as described in general condition 19.

All the terms of the sale and purchase are contained in this contract. This contract includes:

the particulars of sale;

any special conditions;

the general conditions; and

the schedules attached to this contract.

The particulars of sale, any special conditions and the general conditions are to be interpreted in that order of priority in the absence of

any provision to the contrary.

Each party represents and warrants to the other parties and the guarantors that the party has not altered the general conditions in this

contract from the form published by the Law Institute of Victoria dated May 2014, except to the extent that they are amended expressly

by a special condition (if any).

The authority of a person signing:

under a power of attorney;

as director of a corporation; or

as agent authorised in writing by one or more of the parties;

must be noted beneath their signature. That person represents and warrants to the other parties that the person has the power and

authority of that party to enter that party into this contract.

The vendor must provide a statement in writing to the purchaser in the prescribed form containing the prescribed particulars under

section 52 of the Estate Agents Act 1980 (Vic) if the Business is a “small business” as defined in that legislation.

2. The Stock of the Business for the value of the Stock calculated under this contract;

as a going concern on the terms set out in this contract.

Each party agrees to promptly perform that party’s obligations contained in this contract.

The guarantor guarantees, indemnifies and promises as described in general condition 19.

All the terms of the sale and purchase are contained in this contract. This contract includes:

the particulars of sale;

any special conditions;

the general conditions; and

the schedules attached to this contract.

The particulars of sale, any special conditions and the general conditions are to be interpreted in that order of priority in the absence of

any provision to the contrary.

Each party represents and warrants to the other parties and the guarantors that the party has not altered the general conditions in this

contract from the form published by the Law Institute of Victoria dated May 2014, except to the extent that they are amended expressly

by a special condition (if any).

The authority of a person signing:

under a power of attorney;

as director of a corporation; or

as agent authorised in writing by one or more of the parties;

must be noted beneath their signature. That person represents and warrants to the other parties that the person has the power and

authority of that party to enter that party into this contract.

The vendor must provide a statement in writing to the purchaser in the prescribed form containing the prescribed particulars under

section 52 of the Estate Agents Act 1980 (Vic) if the Business is a “small business” as defined in that legislation.

Page 9

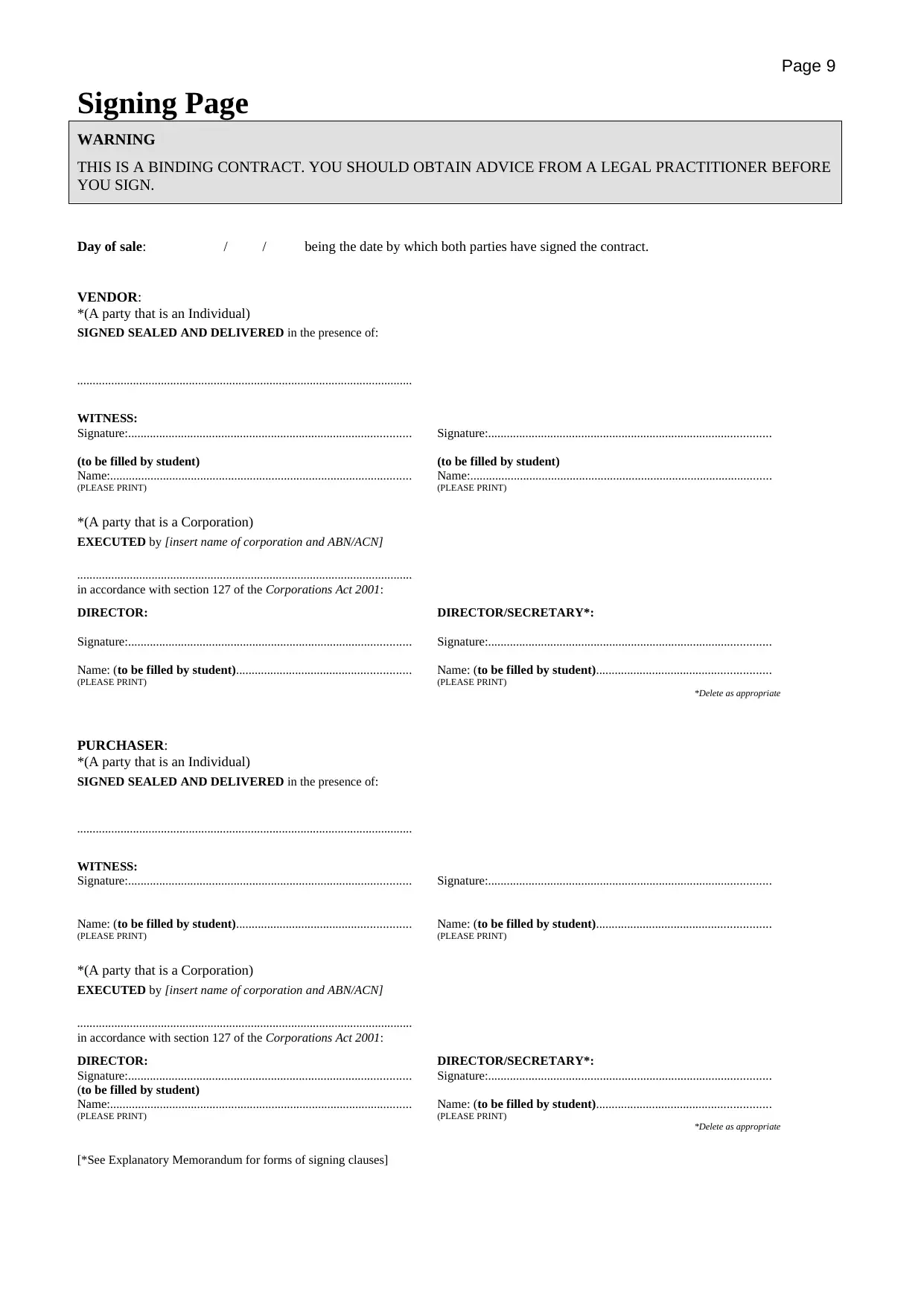

Signing Page

WARNING

THIS IS A BINDING CONTRACT. YOU SHOULD OBTAIN ADVICE FROM A LEGAL PRACTITIONER BEFORE

YOU SIGN.

Day of sale: / / being the date by which both parties have signed the contract.

VENDOR:

*(A party that is an Individual)

SIGNED SEALED AND DELIVERED in the presence of:

............................................................................................................

WITNESS:

Signature:...........................................................................................

(to be filled by student)

Name:.................................................................................................

(PLEASE PRINT)

Signature:...........................................................................................

(to be filled by student)

Name:.................................................................................................

(PLEASE PRINT)

*(A party that is a Corporation)

EXECUTED by [insert name of corporation and ABN/ACN]

............................................................................................................

in accordance with section 127 of the Corporations Act 2001:

DIRECTOR:

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

DIRECTOR/SECRETARY*:

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

*Delete as appropriate

PURCHASER:

*(A party that is an Individual)

SIGNED SEALED AND DELIVERED in the presence of:

............................................................................................................

WITNESS:

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

*(A party that is a Corporation)

EXECUTED by [insert name of corporation and ABN/ACN]

............................................................................................................

in accordance with section 127 of the Corporations Act 2001:

DIRECTOR:

Signature:...........................................................................................

(to be filled by student)

Name:.................................................................................................

(PLEASE PRINT)

DIRECTOR/SECRETARY*:

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

*Delete as appropriate

[*See Explanatory Memorandum for forms of signing clauses]

Signing Page

WARNING

THIS IS A BINDING CONTRACT. YOU SHOULD OBTAIN ADVICE FROM A LEGAL PRACTITIONER BEFORE

YOU SIGN.

Day of sale: / / being the date by which both parties have signed the contract.

VENDOR:

*(A party that is an Individual)

SIGNED SEALED AND DELIVERED in the presence of:

............................................................................................................

WITNESS:

Signature:...........................................................................................

(to be filled by student)

Name:.................................................................................................

(PLEASE PRINT)

Signature:...........................................................................................

(to be filled by student)

Name:.................................................................................................

(PLEASE PRINT)

*(A party that is a Corporation)

EXECUTED by [insert name of corporation and ABN/ACN]

............................................................................................................

in accordance with section 127 of the Corporations Act 2001:

DIRECTOR:

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

DIRECTOR/SECRETARY*:

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

*Delete as appropriate

PURCHASER:

*(A party that is an Individual)

SIGNED SEALED AND DELIVERED in the presence of:

............................................................................................................

WITNESS:

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

*(A party that is a Corporation)

EXECUTED by [insert name of corporation and ABN/ACN]

............................................................................................................

in accordance with section 127 of the Corporations Act 2001:

DIRECTOR:

Signature:...........................................................................................

(to be filled by student)

Name:.................................................................................................

(PLEASE PRINT)

DIRECTOR/SECRETARY*:

Signature:...........................................................................................

Name: (to be filled by student)........................................................

(PLEASE PRINT)

*Delete as appropriate

[*See Explanatory Memorandum for forms of signing clauses]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page 10

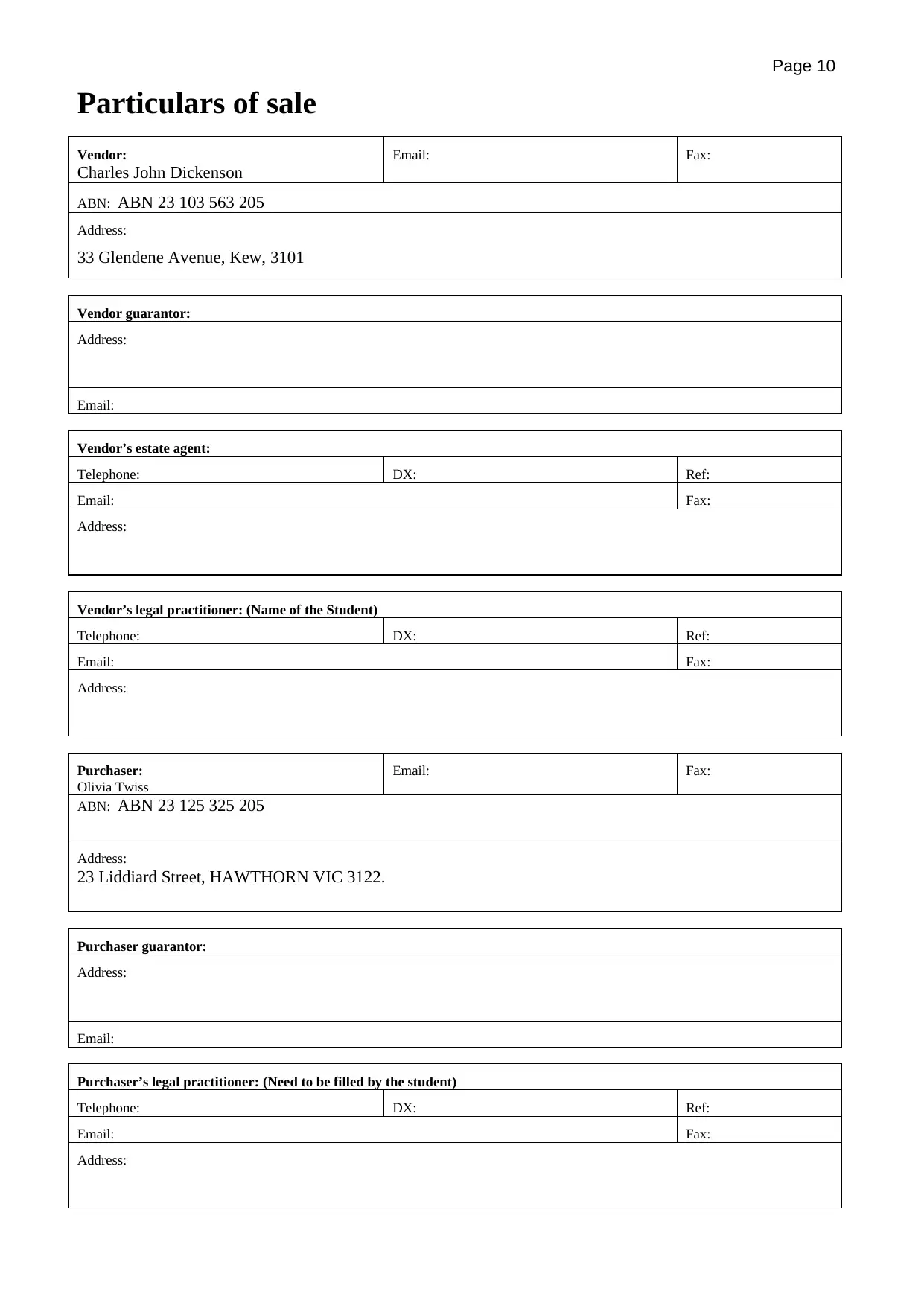

Particulars of sale

Vendor:

Charles John Dickenson

Email: Fax:

ABN: ABN 23 103 563 205

Address:

33 Glendene Avenue, Kew, 3101

Vendor guarantor:

Address:

Email:

Vendor’s estate agent:

Telephone: DX: Ref:

Email: Fax:

Address:

Vendor’s legal practitioner: (Name of the Student)

Telephone: DX: Ref:

Email: Fax:

Address:

Purchaser:

Olivia Twiss

Email: Fax:

ABN: ABN 23 125 325 205

Address:

23 Liddiard Street, HAWTHORN VIC 3122.

Purchaser guarantor:

Address:

Email:

Purchaser’s legal practitioner: (Need to be filled by the student)

Telephone: DX: Ref:

Email: Fax:

Address:

Particulars of sale

Vendor:

Charles John Dickenson

Email: Fax:

ABN: ABN 23 103 563 205

Address:

33 Glendene Avenue, Kew, 3101

Vendor guarantor:

Address:

Email:

Vendor’s estate agent:

Telephone: DX: Ref:

Email: Fax:

Address:

Vendor’s legal practitioner: (Name of the Student)

Telephone: DX: Ref:

Email: Fax:

Address:

Purchaser:

Olivia Twiss

Email: Fax:

ABN: ABN 23 125 325 205

Address:

23 Liddiard Street, HAWTHORN VIC 3122.

Purchaser guarantor:

Address:

Email:

Purchaser’s legal practitioner: (Need to be filled by the student)

Telephone: DX: Ref:

Email: Fax:

Address:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page 11

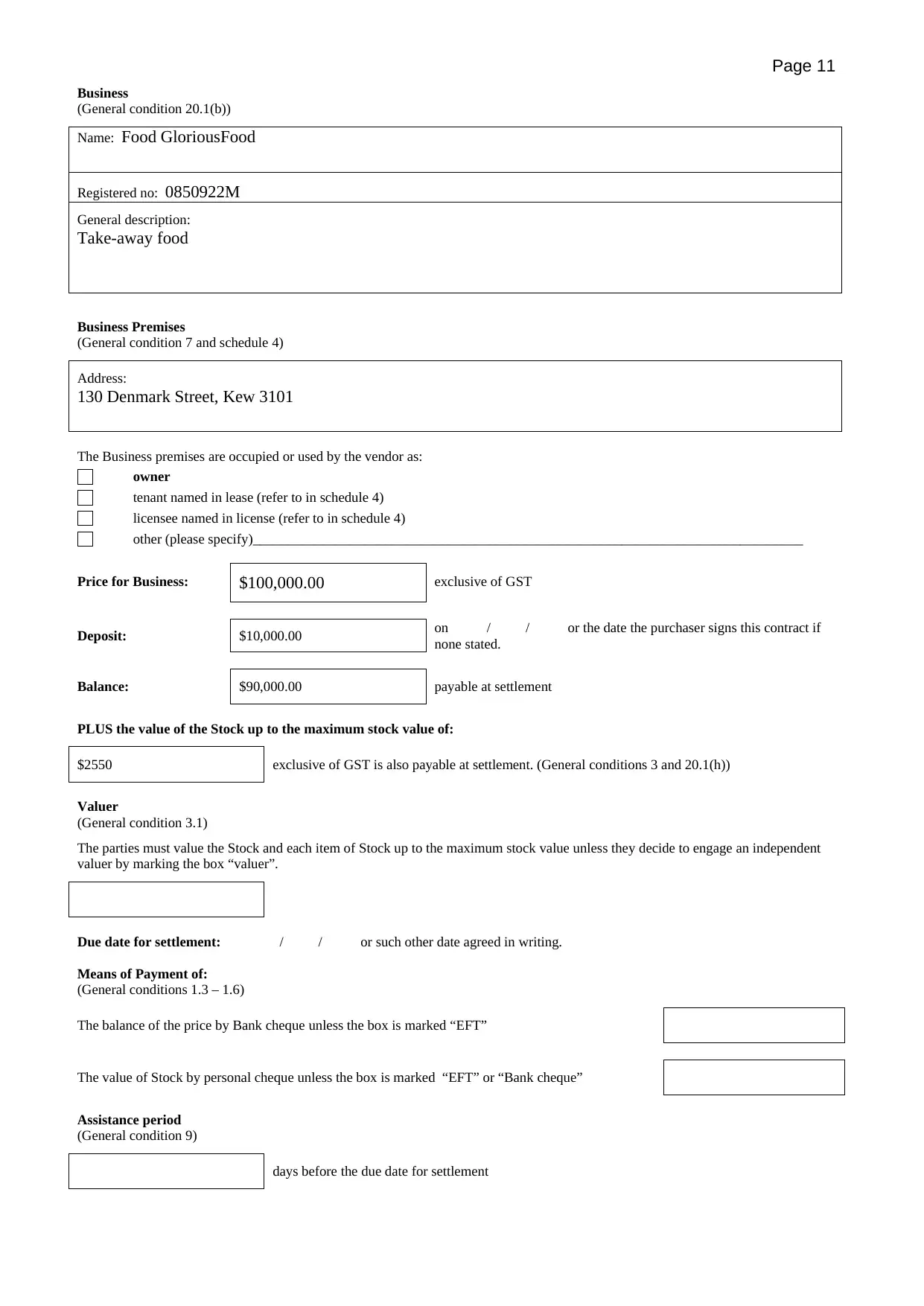

Business

(General condition 20.1(b))

Name: Food GloriousFood

Registered no: 0850922M

General description:

Take-away food

Business Premises

(General condition 7 and schedule 4)

Address:

130 Denmark Street, Kew 3101

The Business premises are occupied or used by the vendor as:

owner

tenant named in lease (refer to in schedule 4)

licensee named in license (refer to in schedule 4)

other (please specify)_______________________________________________________________________________

Price for Business: $100,000.00 exclusive of GST

Deposit: $10,000.00 on / / or the date the purchaser signs this contract if

none stated.

Balance: $90,000.00 payable at settlement

PLUS the value of the Stock up to the maximum stock value of:

$2550 exclusive of GST is also payable at settlement. (General conditions 3 and 20.1(h))

Valuer

(General condition 3.1)

The parties must value the Stock and each item of Stock up to the maximum stock value unless they decide to engage an independent

valuer by marking the box “valuer”.

Due date for settlement: / / or such other date agreed in writing.

Means of Payment of:

(General conditions 1.3 – 1.6)

The balance of the price by Bank cheque unless the box is marked “EFT”

The value of Stock by personal cheque unless the box is marked “EFT” or “Bank cheque”

Assistance period

(General condition 9)

days before the due date for settlement

Business

(General condition 20.1(b))

Name: Food GloriousFood

Registered no: 0850922M

General description:

Take-away food

Business Premises

(General condition 7 and schedule 4)

Address:

130 Denmark Street, Kew 3101

The Business premises are occupied or used by the vendor as:

owner

tenant named in lease (refer to in schedule 4)

licensee named in license (refer to in schedule 4)

other (please specify)_______________________________________________________________________________

Price for Business: $100,000.00 exclusive of GST

Deposit: $10,000.00 on / / or the date the purchaser signs this contract if

none stated.

Balance: $90,000.00 payable at settlement

PLUS the value of the Stock up to the maximum stock value of:

$2550 exclusive of GST is also payable at settlement. (General conditions 3 and 20.1(h))

Valuer

(General condition 3.1)

The parties must value the Stock and each item of Stock up to the maximum stock value unless they decide to engage an independent

valuer by marking the box “valuer”.

Due date for settlement: / / or such other date agreed in writing.

Means of Payment of:

(General conditions 1.3 – 1.6)

The balance of the price by Bank cheque unless the box is marked “EFT”

The value of Stock by personal cheque unless the box is marked “EFT” or “Bank cheque”

Assistance period

(General condition 9)

days before the due date for settlement

Page 12

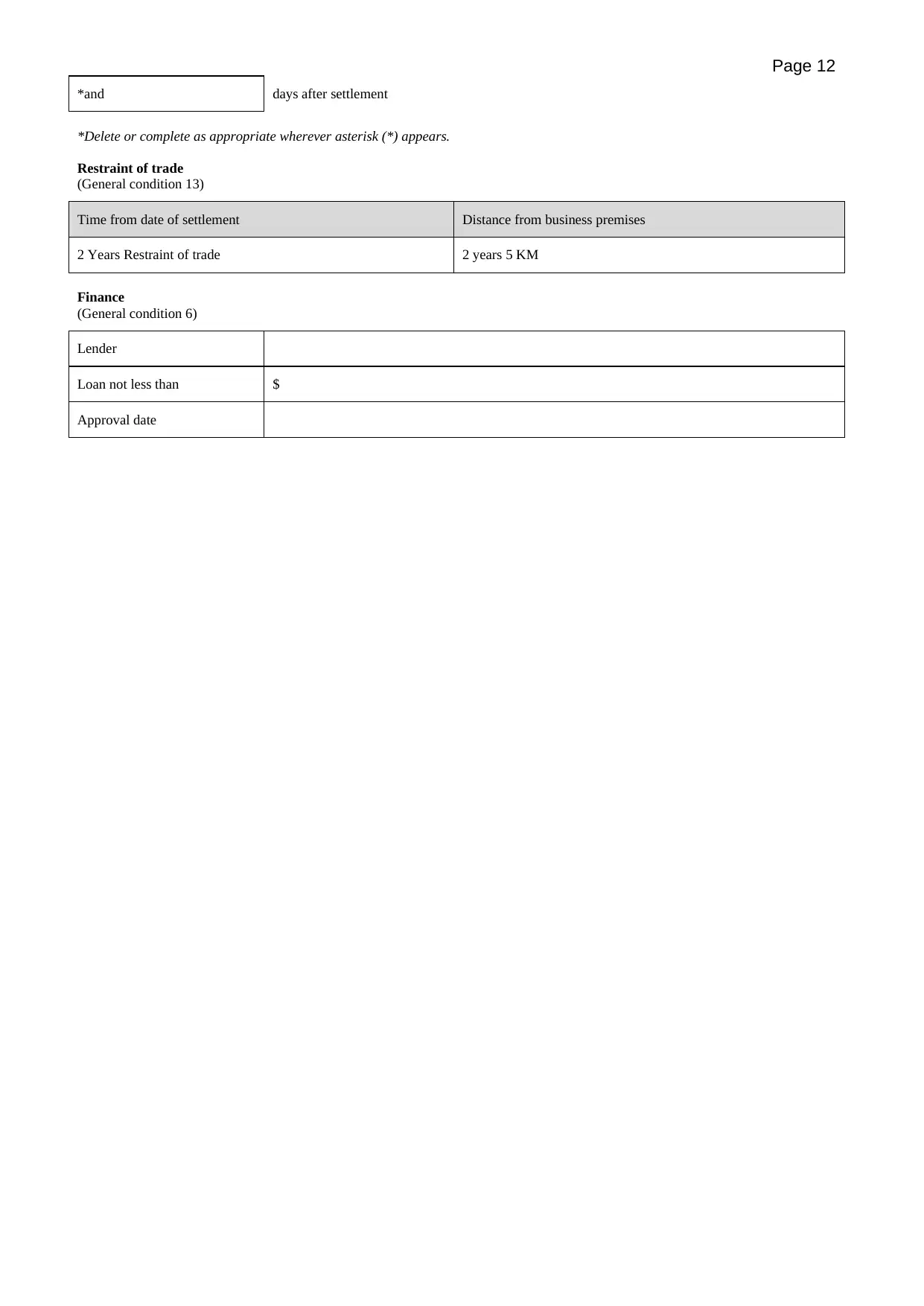

*and days after settlement

*Delete or complete as appropriate wherever asterisk (*) appears.

Restraint of trade

(General condition 13)

Time from date of settlement Distance from business premises

2 Years Restraint of trade 2 years 5 KM

Finance

(General condition 6)

Lender

Loan not less than $

Approval date

*and days after settlement

*Delete or complete as appropriate wherever asterisk (*) appears.

Restraint of trade

(General condition 13)

Time from date of settlement Distance from business premises

2 Years Restraint of trade 2 years 5 KM

Finance

(General condition 6)

Lender

Loan not less than $

Approval date

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.