Business Statistics: Bitcoin, Stock Market Descriptive Analysis Report

VerifiedAdded on 2023/01/23

|12

|2383

|65

Report

AI Summary

This business statistics report analyzes the weekly closing prices and returns of Bitcoin, NAB, Wesfarmers, and Woodside. It includes a trend line analysis of Bitcoin's closing price and histograms of weekly returns for all assets, along with descriptive statistics (mean, standard deviation, skewness, kurtosis, etc.) to assess the distribution and volatility. The report examines the probability of loss for each investment and compares their performance. The analysis covers the period from 2013 to 2020, providing insights into market trends and investment risks. The report uses scatter diagrams and descriptive statistics to evaluate the performance of each asset and determine whether they follow a trend line. The report also focuses on the descriptive analysis of the data to provide insights into the data and the probability of loss in investing in the stocks. The report concludes with an overview of the findings and their implications for investment strategies. It uses data analysis to assist in the decision-making process of investing in financial markets.

Running head: BUSINESS STATISTICS

Business Statistics

Name of the Student:

Name of the University:

Author Note:

Business Statistics

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS STATISTICS

Table of Contents

Introduction................................................................................................................................3

Trend line for weekly closing price...........................................................................................3

Histogram of weekly return.......................................................................................................4

Three aspects of descriptive analysis.........................................................................................4

Analysis of NAB, Wesfarmers and Woodside...........................................................................5

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

Table of Contents

Introduction................................................................................................................................3

Trend line for weekly closing price...........................................................................................3

Histogram of weekly return.......................................................................................................4

Three aspects of descriptive analysis.........................................................................................4

Analysis of NAB, Wesfarmers and Woodside...........................................................................5

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

2BUSINESS STATISTICS

Executive Summary

Bitcoin is a payment network which is very well-known as a cryptocurrency that uses

the block chain technology. Some says, Bitcoin as a secure, global and digital currency

represents the future of finance and some are not optimistic about it. A statistical analysis is

needed to judge that whether it is recommendable or not to invest in Bitcoin. Data on the

closing price and the return of Bitcoin on weekly basis can be used to get the best results

from the analysis. The trend and the statistics can suggest the better option between investin

and not investing on Bitcoins.

Executive Summary

Bitcoin is a payment network which is very well-known as a cryptocurrency that uses

the block chain technology. Some says, Bitcoin as a secure, global and digital currency

represents the future of finance and some are not optimistic about it. A statistical analysis is

needed to judge that whether it is recommendable or not to invest in Bitcoin. Data on the

closing price and the return of Bitcoin on weekly basis can be used to get the best results

from the analysis. The trend and the statistics can suggest the better option between investin

and not investing on Bitcoins.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS STATISTICS

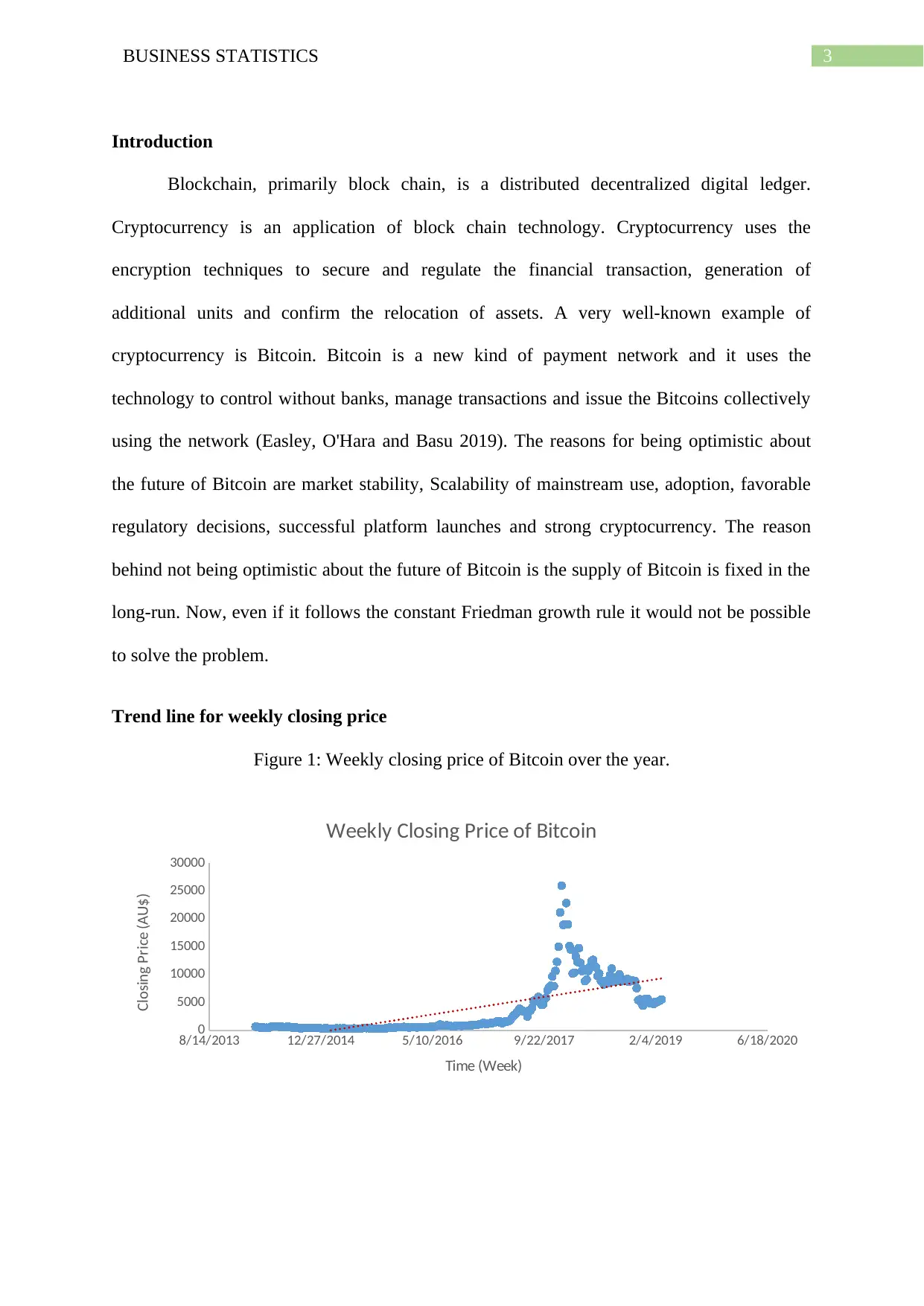

Introduction

Blockchain, primarily block chain, is a distributed decentralized digital ledger.

Cryptocurrency is an application of block chain technology. Cryptocurrency uses the

encryption techniques to secure and regulate the financial transaction, generation of

additional units and confirm the relocation of assets. A very well-known example of

cryptocurrency is Bitcoin. Bitcoin is a new kind of payment network and it uses the

technology to control without banks, manage transactions and issue the Bitcoins collectively

using the network (Easley, O'Hara and Basu 2019). The reasons for being optimistic about

the future of Bitcoin are market stability, Scalability of mainstream use, adoption, favorable

regulatory decisions, successful platform launches and strong cryptocurrency. The reason

behind not being optimistic about the future of Bitcoin is the supply of Bitcoin is fixed in the

long-run. Now, even if it follows the constant Friedman growth rule it would not be possible

to solve the problem.

Trend line for weekly closing price

Figure 1: Weekly closing price of Bitcoin over the year.

8/14/2013 12/27/2014 5/10/2016 9/22/2017 2/4/2019 6/18/2020

0

5000

10000

15000

20000

25000

30000

Weekly Closing Price of Bitcoin

Time (Week)

Closing Price (AU$)

Introduction

Blockchain, primarily block chain, is a distributed decentralized digital ledger.

Cryptocurrency is an application of block chain technology. Cryptocurrency uses the

encryption techniques to secure and regulate the financial transaction, generation of

additional units and confirm the relocation of assets. A very well-known example of

cryptocurrency is Bitcoin. Bitcoin is a new kind of payment network and it uses the

technology to control without banks, manage transactions and issue the Bitcoins collectively

using the network (Easley, O'Hara and Basu 2019). The reasons for being optimistic about

the future of Bitcoin are market stability, Scalability of mainstream use, adoption, favorable

regulatory decisions, successful platform launches and strong cryptocurrency. The reason

behind not being optimistic about the future of Bitcoin is the supply of Bitcoin is fixed in the

long-run. Now, even if it follows the constant Friedman growth rule it would not be possible

to solve the problem.

Trend line for weekly closing price

Figure 1: Weekly closing price of Bitcoin over the year.

8/14/2013 12/27/2014 5/10/2016 9/22/2017 2/4/2019 6/18/2020

0

5000

10000

15000

20000

25000

30000

Weekly Closing Price of Bitcoin

Time (Week)

Closing Price (AU$)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS STATISTICS

The above figure is scatter diagram presenting the weekly closing price of the Bitcoin.

The scatter diagram is helpful to determine the relationship between two variables. To do so,

it presents the dependent variable on the vertical axis and the independent variable on the

horizontal axis. Then it presents the data of dependent variable against each value of

independent variable. In the figure above the closing price of Bitcoin is presented on the

vertical axis and the dots are presenting the closing price of Bitcoin against each week from

2014 to 2019. A trend line is presented which does not match with the scatter diagram of

close price of Bitcoins. Therefore, it can be said that the price does not follow the trend line

(Güçlü 2018).

Histogram of weekly return

Figure 2: Weekly return on Bitcoin over the year

3/9/2014

5/18/2014

7/27/2014

10/5/2014

12/14/2014

2/22/2015

5/3/2015

7/12/2015

9/20/2015

11/29/2015

2/7/2016

4/17/2016

6/26/2016

9/4/2016

11/13/2016

1/22/2017

4/2/2017

6/11/2017

8/20/2017

10/29/2017

1/7/2018

3/18/2018

5/27/2018

8/5/2018

10/14/2018

12/23/2018

3/3/2019

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

Weekly Return on Bitcoin

Time (Week)

Weekly Return (AU $)

For normal distributions the top point of bars of histogram makes a shape of bell. But

the above figure does not appear as a bell shaped and there are too many peaks that implies

that the closing price is not normally distributed. The peak and bottom values of the return on

Bitcoin are the evidence of the outliers. There are a number of peaks and bottoms that are

shown by the longest bars of the histogram.

Three aspects of descriptive analysis

Return on Bitcoin

The above figure is scatter diagram presenting the weekly closing price of the Bitcoin.

The scatter diagram is helpful to determine the relationship between two variables. To do so,

it presents the dependent variable on the vertical axis and the independent variable on the

horizontal axis. Then it presents the data of dependent variable against each value of

independent variable. In the figure above the closing price of Bitcoin is presented on the

vertical axis and the dots are presenting the closing price of Bitcoin against each week from

2014 to 2019. A trend line is presented which does not match with the scatter diagram of

close price of Bitcoins. Therefore, it can be said that the price does not follow the trend line

(Güçlü 2018).

Histogram of weekly return

Figure 2: Weekly return on Bitcoin over the year

3/9/2014

5/18/2014

7/27/2014

10/5/2014

12/14/2014

2/22/2015

5/3/2015

7/12/2015

9/20/2015

11/29/2015

2/7/2016

4/17/2016

6/26/2016

9/4/2016

11/13/2016

1/22/2017

4/2/2017

6/11/2017

8/20/2017

10/29/2017

1/7/2018

3/18/2018

5/27/2018

8/5/2018

10/14/2018

12/23/2018

3/3/2019

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

Weekly Return on Bitcoin

Time (Week)

Weekly Return (AU $)

For normal distributions the top point of bars of histogram makes a shape of bell. But

the above figure does not appear as a bell shaped and there are too many peaks that implies

that the closing price is not normally distributed. The peak and bottom values of the return on

Bitcoin are the evidence of the outliers. There are a number of peaks and bottoms that are

shown by the longest bars of the histogram.

Three aspects of descriptive analysis

Return on Bitcoin

5BUSINESS STATISTICS

Mean 0.016

Standard Error 0.008

Median 0.012

Standard Deviation 0.126

Sample Variance 0.016

Kurtosis 3.006

Skewness 0.606

Range 1.054

Minimum -0.398

Maximum 0.657

Sum 4.124

Count 260

Table 1: Descriptive statistics of weekly return on Bitcoin

Three points of descriptive analysis (location, shape and spread) of the weekly return

on Bitcoin is presented by the above table. The location is presented by the mean value that

equals to 0.016% of the variable around which the closing prices are stabilized. The shape is

measured by the number of mode values, skewness and kurtosis. The distribution of weekly

return on Bitcoin is multimodal distribution. The value of skewness is positive which

indicates that the distribution is positively skewed that means most of the values are on the

right side of the median. Kurtosis is 3.006 that indicates that the tail of the distribution is

normal. The spread of a data set is described by the standard deviation of the data (Chambers

2017). The standard deviation of the weekly closing price is 0.126 that the return on Bitcoin

varies between -0.11 and 0.142. The higher the value of SD, the higher the spread is.

The probability of loss in inviting on Bitcoins is (114/260) or 43.85%.

Analysis of NAB, Wesfarmers and Woodside

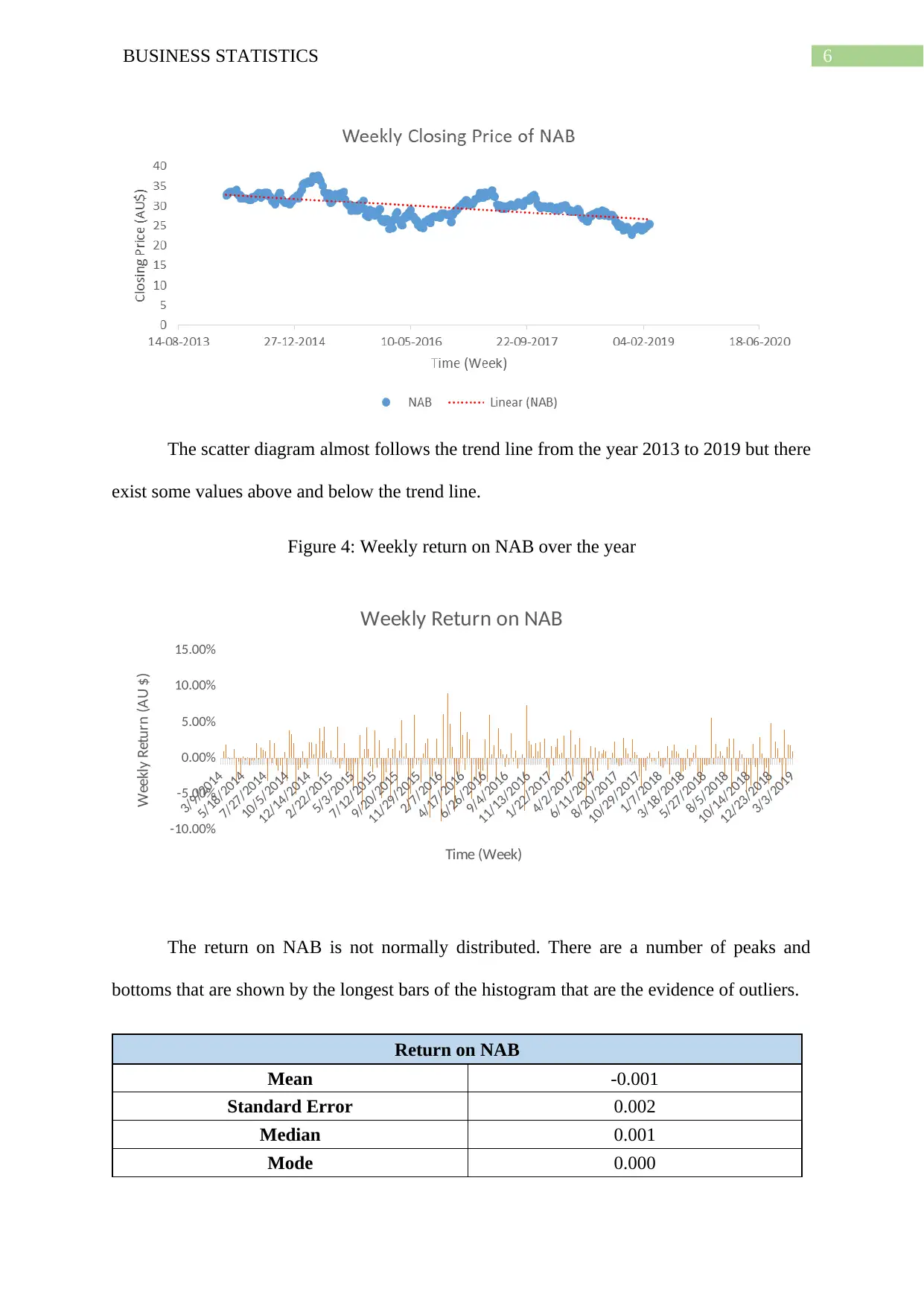

Figure 3: Weekly closing price of NAB over the year

Mean 0.016

Standard Error 0.008

Median 0.012

Standard Deviation 0.126

Sample Variance 0.016

Kurtosis 3.006

Skewness 0.606

Range 1.054

Minimum -0.398

Maximum 0.657

Sum 4.124

Count 260

Table 1: Descriptive statistics of weekly return on Bitcoin

Three points of descriptive analysis (location, shape and spread) of the weekly return

on Bitcoin is presented by the above table. The location is presented by the mean value that

equals to 0.016% of the variable around which the closing prices are stabilized. The shape is

measured by the number of mode values, skewness and kurtosis. The distribution of weekly

return on Bitcoin is multimodal distribution. The value of skewness is positive which

indicates that the distribution is positively skewed that means most of the values are on the

right side of the median. Kurtosis is 3.006 that indicates that the tail of the distribution is

normal. The spread of a data set is described by the standard deviation of the data (Chambers

2017). The standard deviation of the weekly closing price is 0.126 that the return on Bitcoin

varies between -0.11 and 0.142. The higher the value of SD, the higher the spread is.

The probability of loss in inviting on Bitcoins is (114/260) or 43.85%.

Analysis of NAB, Wesfarmers and Woodside

Figure 3: Weekly closing price of NAB over the year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS STATISTICS

The scatter diagram almost follows the trend line from the year 2013 to 2019 but there

exist some values above and below the trend line.

Figure 4: Weekly return on NAB over the year

3/9/2014

5/18/2014

7/27/2014

10/5/2014

12/14/2014

2/22/2015

5/3/2015

7/12/2015

9/20/2015

11/29/2015

2/7/2016

4/17/2016

6/26/2016

9/4/2016

11/13/2016

1/22/2017

4/2/2017

6/11/2017

8/20/2017

10/29/2017

1/7/2018

3/18/2018

5/27/2018

8/5/2018

10/14/2018

12/23/2018

3/3/2019

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Weekly Return on NAB

Time (Week)

Weekly Return (AU $)

The return on NAB is not normally distributed. There are a number of peaks and

bottoms that are shown by the longest bars of the histogram that are the evidence of outliers.

Return on NAB

Mean -0.001

Standard Error 0.002

Median 0.001

Mode 0.000

The scatter diagram almost follows the trend line from the year 2013 to 2019 but there

exist some values above and below the trend line.

Figure 4: Weekly return on NAB over the year

3/9/2014

5/18/2014

7/27/2014

10/5/2014

12/14/2014

2/22/2015

5/3/2015

7/12/2015

9/20/2015

11/29/2015

2/7/2016

4/17/2016

6/26/2016

9/4/2016

11/13/2016

1/22/2017

4/2/2017

6/11/2017

8/20/2017

10/29/2017

1/7/2018

3/18/2018

5/27/2018

8/5/2018

10/14/2018

12/23/2018

3/3/2019

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Weekly Return on NAB

Time (Week)

Weekly Return (AU $)

The return on NAB is not normally distributed. There are a number of peaks and

bottoms that are shown by the longest bars of the histogram that are the evidence of outliers.

Return on NAB

Mean -0.001

Standard Error 0.002

Median 0.001

Mode 0.000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS STATISTICS

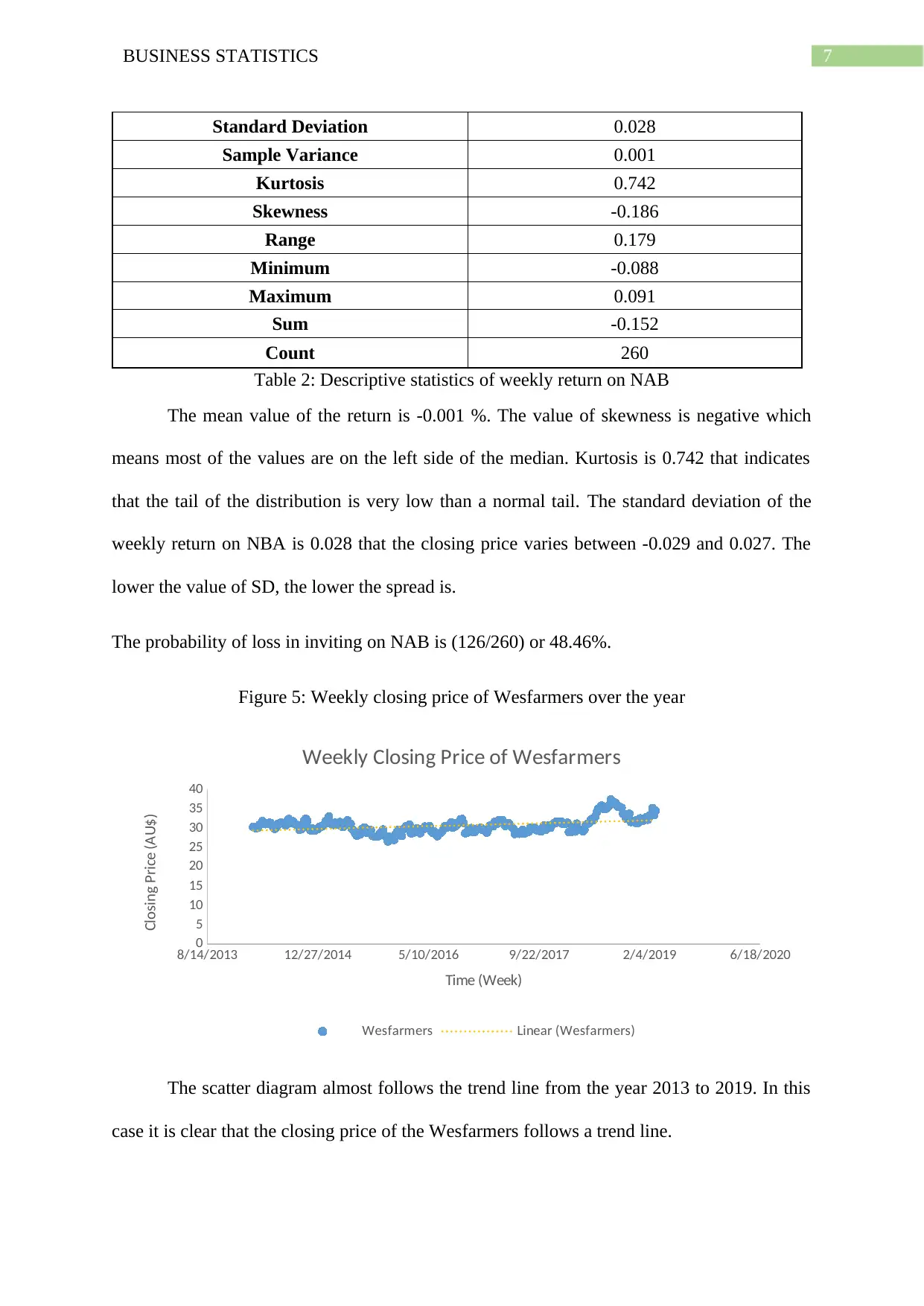

Standard Deviation 0.028

Sample Variance 0.001

Kurtosis 0.742

Skewness -0.186

Range 0.179

Minimum -0.088

Maximum 0.091

Sum -0.152

Count 260

Table 2: Descriptive statistics of weekly return on NAB

The mean value of the return is -0.001 %. The value of skewness is negative which

means most of the values are on the left side of the median. Kurtosis is 0.742 that indicates

that the tail of the distribution is very low than a normal tail. The standard deviation of the

weekly return on NBA is 0.028 that the closing price varies between -0.029 and 0.027. The

lower the value of SD, the lower the spread is.

The probability of loss in inviting on NAB is (126/260) or 48.46%.

Figure 5: Weekly closing price of Wesfarmers over the year

8/14/2013 12/27/2014 5/10/2016 9/22/2017 2/4/2019 6/18/2020

0

5

10

15

20

25

30

35

40

Weekly Closing Price of Wesfarmers

Wesfarmers Linear (Wesfarmers)

Time (Week)

Closing Price (AU$)

The scatter diagram almost follows the trend line from the year 2013 to 2019. In this

case it is clear that the closing price of the Wesfarmers follows a trend line.

Standard Deviation 0.028

Sample Variance 0.001

Kurtosis 0.742

Skewness -0.186

Range 0.179

Minimum -0.088

Maximum 0.091

Sum -0.152

Count 260

Table 2: Descriptive statistics of weekly return on NAB

The mean value of the return is -0.001 %. The value of skewness is negative which

means most of the values are on the left side of the median. Kurtosis is 0.742 that indicates

that the tail of the distribution is very low than a normal tail. The standard deviation of the

weekly return on NBA is 0.028 that the closing price varies between -0.029 and 0.027. The

lower the value of SD, the lower the spread is.

The probability of loss in inviting on NAB is (126/260) or 48.46%.

Figure 5: Weekly closing price of Wesfarmers over the year

8/14/2013 12/27/2014 5/10/2016 9/22/2017 2/4/2019 6/18/2020

0

5

10

15

20

25

30

35

40

Weekly Closing Price of Wesfarmers

Wesfarmers Linear (Wesfarmers)

Time (Week)

Closing Price (AU$)

The scatter diagram almost follows the trend line from the year 2013 to 2019. In this

case it is clear that the closing price of the Wesfarmers follows a trend line.

8BUSINESS STATISTICS

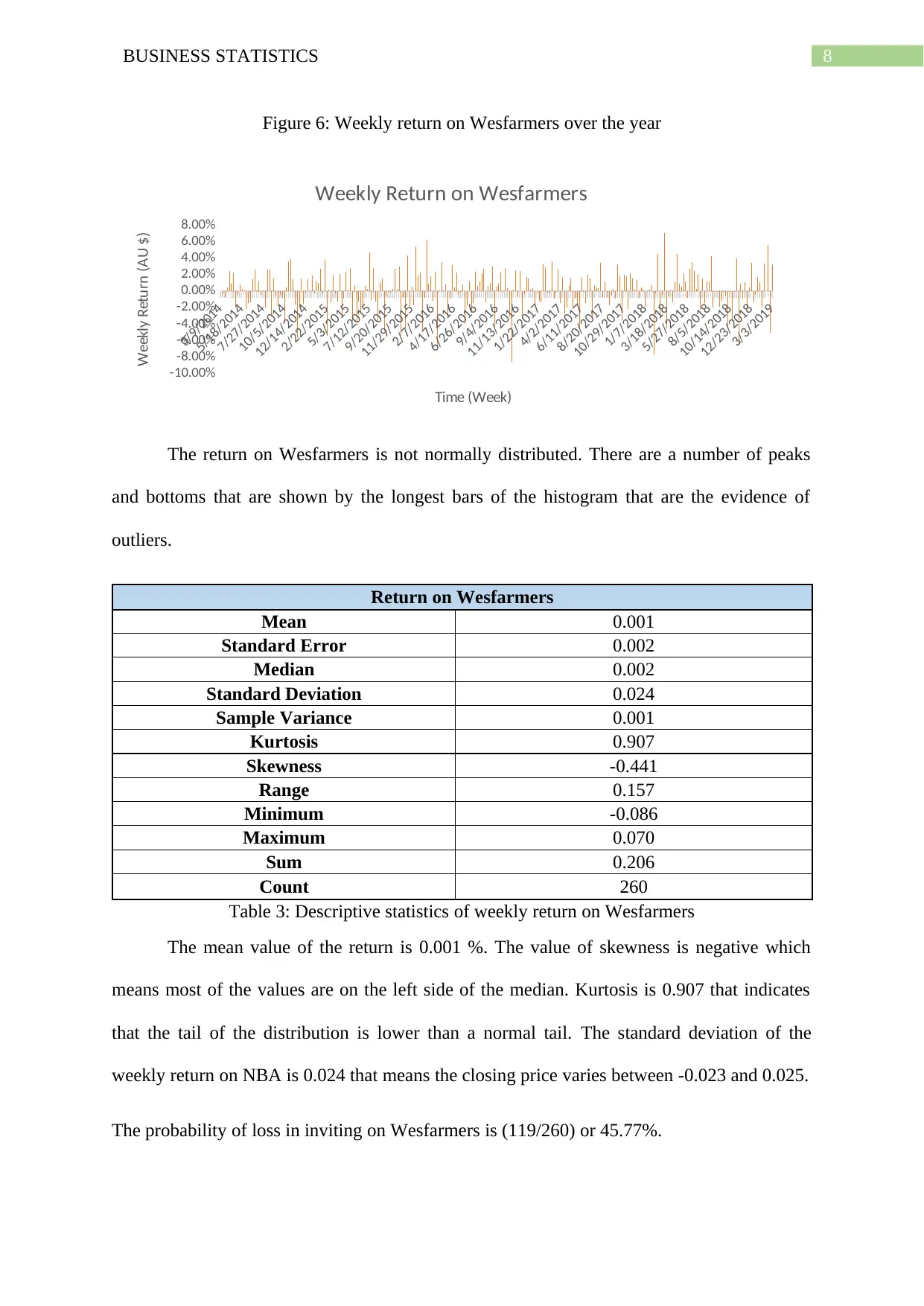

Figure 6: Weekly return on Wesfarmers over the year

3/9/2014

5/18/2014

7/27/2014

10/5/2014

12/14/2014

2/22/2015

5/3/2015

7/12/2015

9/20/2015

11/29/2015

2/7/2016

4/17/2016

6/26/2016

9/4/2016

11/13/2016

1/22/2017

4/2/2017

6/11/2017

8/20/2017

10/29/2017

1/7/2018

3/18/2018

5/27/2018

8/5/2018

10/14/2018

12/23/2018

3/3/2019

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Weekly Return on Wesfarmers

Time (Week)

Weekly Return (AU $)

The return on Wesfarmers is not normally distributed. There are a number of peaks

and bottoms that are shown by the longest bars of the histogram that are the evidence of

outliers.

Return on Wesfarmers

Mean 0.001

Standard Error 0.002

Median 0.002

Standard Deviation 0.024

Sample Variance 0.001

Kurtosis 0.907

Skewness -0.441

Range 0.157

Minimum -0.086

Maximum 0.070

Sum 0.206

Count 260

Table 3: Descriptive statistics of weekly return on Wesfarmers

The mean value of the return is 0.001 %. The value of skewness is negative which

means most of the values are on the left side of the median. Kurtosis is 0.907 that indicates

that the tail of the distribution is lower than a normal tail. The standard deviation of the

weekly return on NBA is 0.024 that means the closing price varies between -0.023 and 0.025.

The probability of loss in inviting on Wesfarmers is (119/260) or 45.77%.

Figure 6: Weekly return on Wesfarmers over the year

3/9/2014

5/18/2014

7/27/2014

10/5/2014

12/14/2014

2/22/2015

5/3/2015

7/12/2015

9/20/2015

11/29/2015

2/7/2016

4/17/2016

6/26/2016

9/4/2016

11/13/2016

1/22/2017

4/2/2017

6/11/2017

8/20/2017

10/29/2017

1/7/2018

3/18/2018

5/27/2018

8/5/2018

10/14/2018

12/23/2018

3/3/2019

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Weekly Return on Wesfarmers

Time (Week)

Weekly Return (AU $)

The return on Wesfarmers is not normally distributed. There are a number of peaks

and bottoms that are shown by the longest bars of the histogram that are the evidence of

outliers.

Return on Wesfarmers

Mean 0.001

Standard Error 0.002

Median 0.002

Standard Deviation 0.024

Sample Variance 0.001

Kurtosis 0.907

Skewness -0.441

Range 0.157

Minimum -0.086

Maximum 0.070

Sum 0.206

Count 260

Table 3: Descriptive statistics of weekly return on Wesfarmers

The mean value of the return is 0.001 %. The value of skewness is negative which

means most of the values are on the left side of the median. Kurtosis is 0.907 that indicates

that the tail of the distribution is lower than a normal tail. The standard deviation of the

weekly return on NBA is 0.024 that means the closing price varies between -0.023 and 0.025.

The probability of loss in inviting on Wesfarmers is (119/260) or 45.77%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS STATISTICS

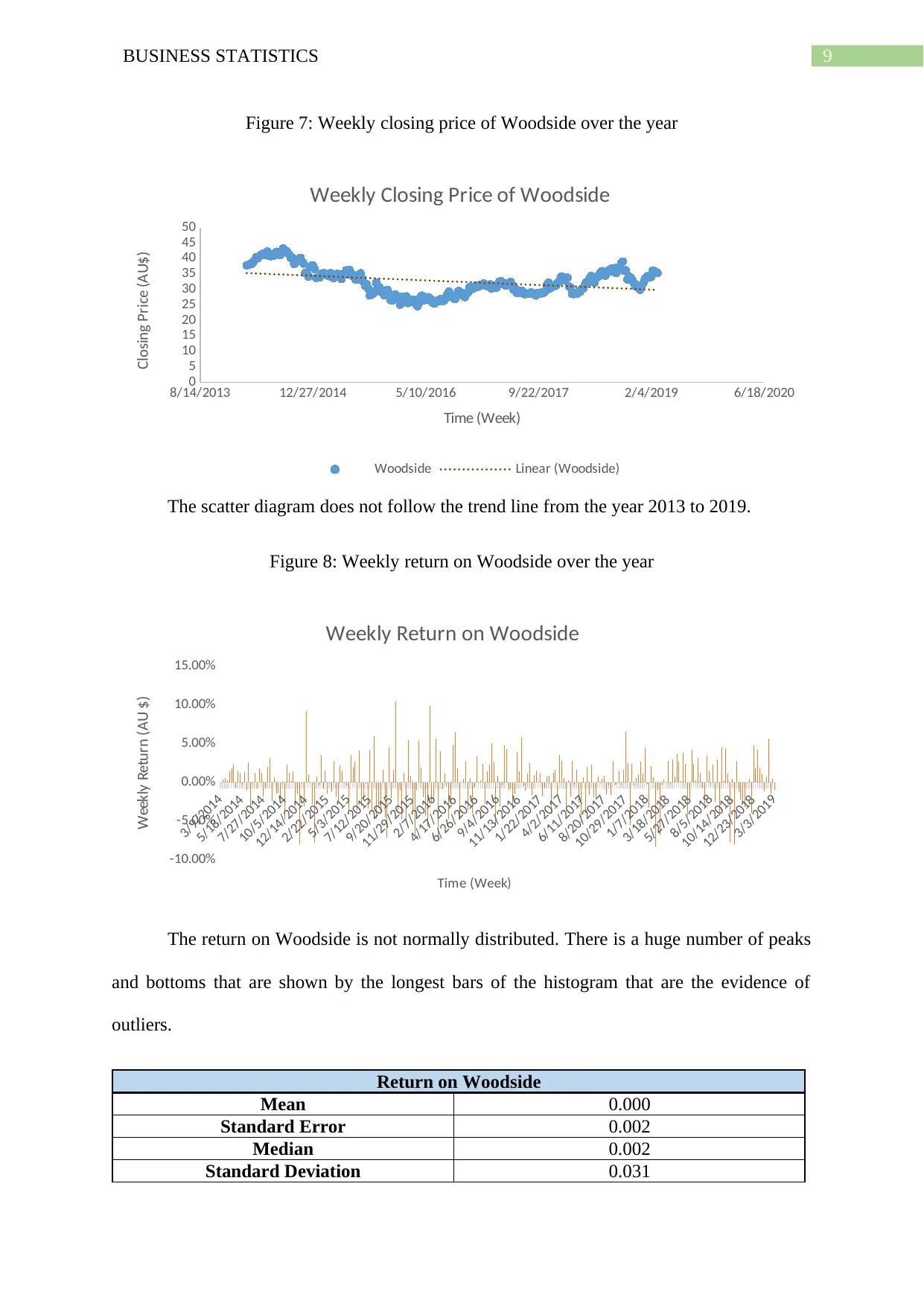

Figure 7: Weekly closing price of Woodside over the year

8/14/2013 12/27/2014 5/10/2016 9/22/2017 2/4/2019 6/18/2020

0

5

10

15

20

25

30

35

40

45

50

Weekly Closing Price of Woodside

Woodside Linear (Woodside)

Time (Week)

Closing Price (AU$)

The scatter diagram does not follow the trend line from the year 2013 to 2019.

Figure 8: Weekly return on Woodside over the year

3/9/2014

5/18/2014

7/27/2014

10/5/2014

12/14/2014

2/22/2015

5/3/2015

7/12/2015

9/20/2015

11/29/2015

2/7/2016

4/17/2016

6/26/2016

9/4/2016

11/13/2016

1/22/2017

4/2/2017

6/11/2017

8/20/2017

10/29/2017

1/7/2018

3/18/2018

5/27/2018

8/5/2018

10/14/2018

12/23/2018

3/3/2019

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Weekly Return on Woodside

Time (Week)

Weekly Return (AU $)

The return on Woodside is not normally distributed. There is a huge number of peaks

and bottoms that are shown by the longest bars of the histogram that are the evidence of

outliers.

Return on Woodside

Mean 0.000

Standard Error 0.002

Median 0.002

Standard Deviation 0.031

Figure 7: Weekly closing price of Woodside over the year

8/14/2013 12/27/2014 5/10/2016 9/22/2017 2/4/2019 6/18/2020

0

5

10

15

20

25

30

35

40

45

50

Weekly Closing Price of Woodside

Woodside Linear (Woodside)

Time (Week)

Closing Price (AU$)

The scatter diagram does not follow the trend line from the year 2013 to 2019.

Figure 8: Weekly return on Woodside over the year

3/9/2014

5/18/2014

7/27/2014

10/5/2014

12/14/2014

2/22/2015

5/3/2015

7/12/2015

9/20/2015

11/29/2015

2/7/2016

4/17/2016

6/26/2016

9/4/2016

11/13/2016

1/22/2017

4/2/2017

6/11/2017

8/20/2017

10/29/2017

1/7/2018

3/18/2018

5/27/2018

8/5/2018

10/14/2018

12/23/2018

3/3/2019

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Weekly Return on Woodside

Time (Week)

Weekly Return (AU $)

The return on Woodside is not normally distributed. There is a huge number of peaks

and bottoms that are shown by the longest bars of the histogram that are the evidence of

outliers.

Return on Woodside

Mean 0.000

Standard Error 0.002

Median 0.002

Standard Deviation 0.031

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

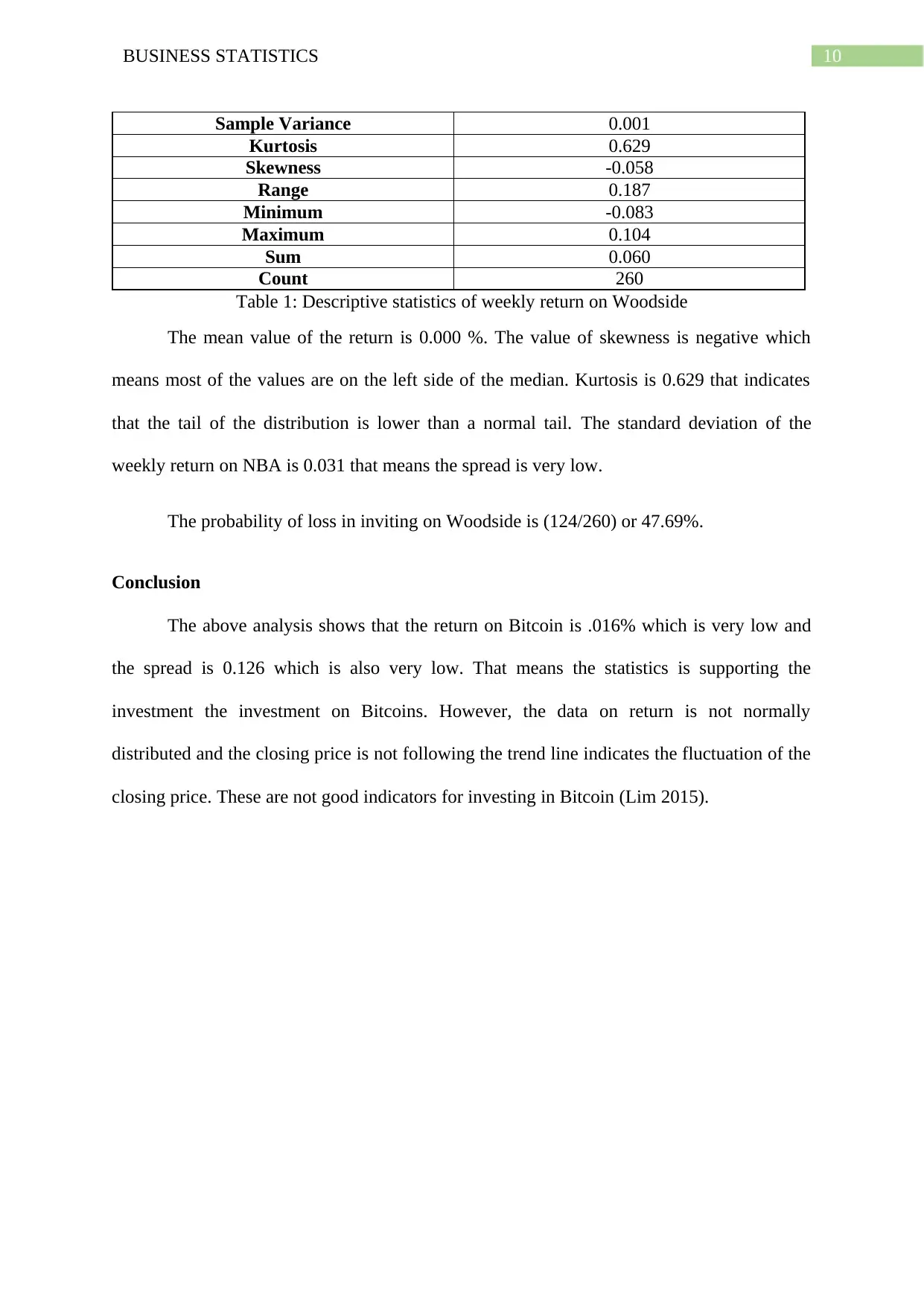

10BUSINESS STATISTICS

Sample Variance 0.001

Kurtosis 0.629

Skewness -0.058

Range 0.187

Minimum -0.083

Maximum 0.104

Sum 0.060

Count 260

Table 1: Descriptive statistics of weekly return on Woodside

The mean value of the return is 0.000 %. The value of skewness is negative which

means most of the values are on the left side of the median. Kurtosis is 0.629 that indicates

that the tail of the distribution is lower than a normal tail. The standard deviation of the

weekly return on NBA is 0.031 that means the spread is very low.

The probability of loss in inviting on Woodside is (124/260) or 47.69%.

Conclusion

The above analysis shows that the return on Bitcoin is .016% which is very low and

the spread is 0.126 which is also very low. That means the statistics is supporting the

investment the investment on Bitcoins. However, the data on return is not normally

distributed and the closing price is not following the trend line indicates the fluctuation of the

closing price. These are not good indicators for investing in Bitcoin (Lim 2015).

Sample Variance 0.001

Kurtosis 0.629

Skewness -0.058

Range 0.187

Minimum -0.083

Maximum 0.104

Sum 0.060

Count 260

Table 1: Descriptive statistics of weekly return on Woodside

The mean value of the return is 0.000 %. The value of skewness is negative which

means most of the values are on the left side of the median. Kurtosis is 0.629 that indicates

that the tail of the distribution is lower than a normal tail. The standard deviation of the

weekly return on NBA is 0.031 that means the spread is very low.

The probability of loss in inviting on Woodside is (124/260) or 47.69%.

Conclusion

The above analysis shows that the return on Bitcoin is .016% which is very low and

the spread is 0.126 which is also very low. That means the statistics is supporting the

investment the investment on Bitcoins. However, the data on return is not normally

distributed and the closing price is not following the trend line indicates the fluctuation of the

closing price. These are not good indicators for investing in Bitcoin (Lim 2015).

11BUSINESS STATISTICS

Reference

Chambers, J.M., 2017. Graphical Methods for Data Analysis: 0. Chapman and Hall/CRC.

Easley, D., O'Hara, M. and Basu, S., 2019. From mining to markets: The evolution of bitcoin

transaction fees. Journal of Financial Economics.

Güçlü, Y.S., 2018. Multiple Şen-innovative trend analyses and partial Mann-Kendall

test. Journal of Hydrology, 566, pp.685-704.

Lim, K.G., 2015. Financial valuation and econometrics.

Reference

Chambers, J.M., 2017. Graphical Methods for Data Analysis: 0. Chapman and Hall/CRC.

Easley, D., O'Hara, M. and Basu, S., 2019. From mining to markets: The evolution of bitcoin

transaction fees. Journal of Financial Economics.

Güçlü, Y.S., 2018. Multiple Şen-innovative trend analyses and partial Mann-Kendall

test. Journal of Hydrology, 566, pp.685-704.

Lim, K.G., 2015. Financial valuation and econometrics.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.