Statistics of Business and Finance: Stock Returns Analysis & CAPM

VerifiedAdded on 2023/06/03

|9

|1388

|439

Homework Assignment

AI Summary

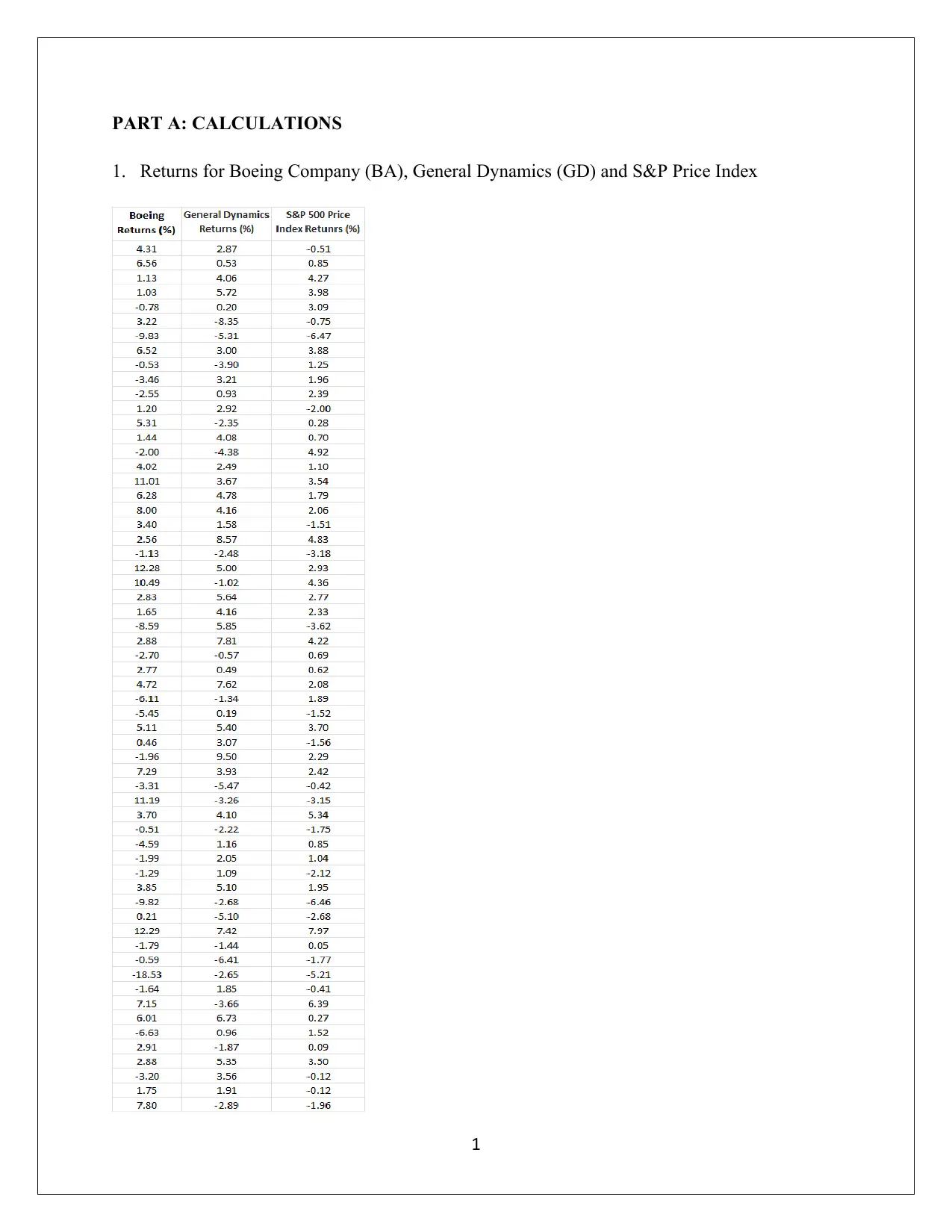

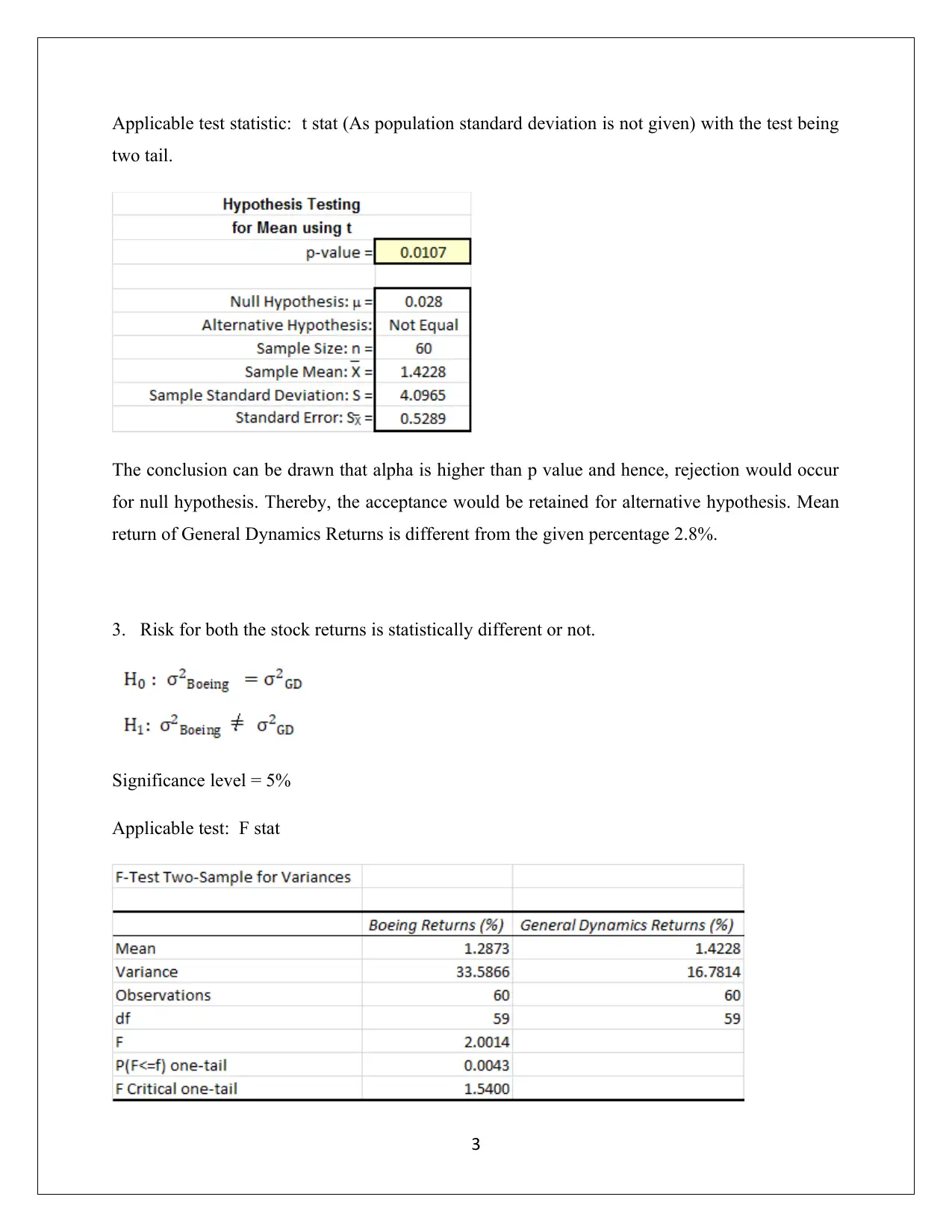

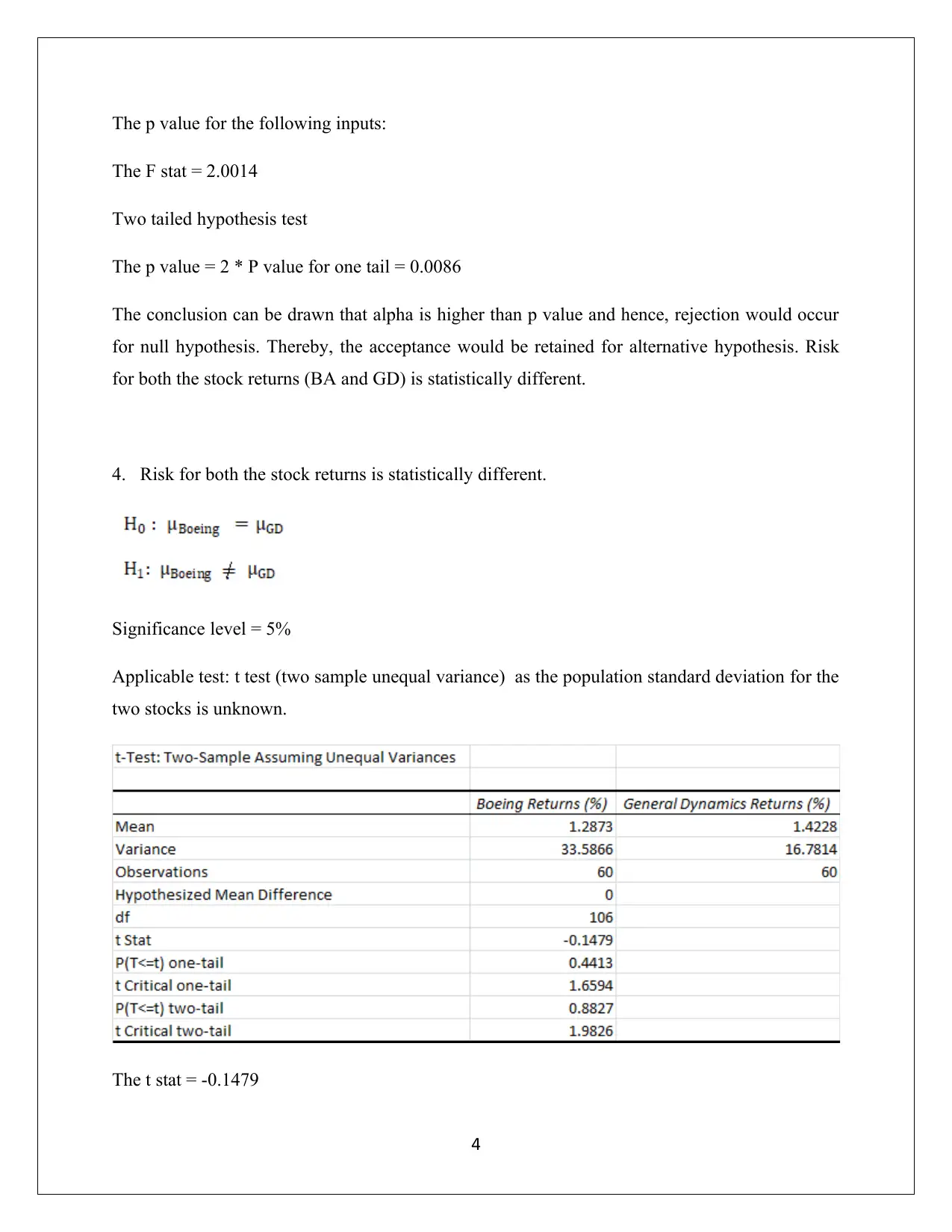

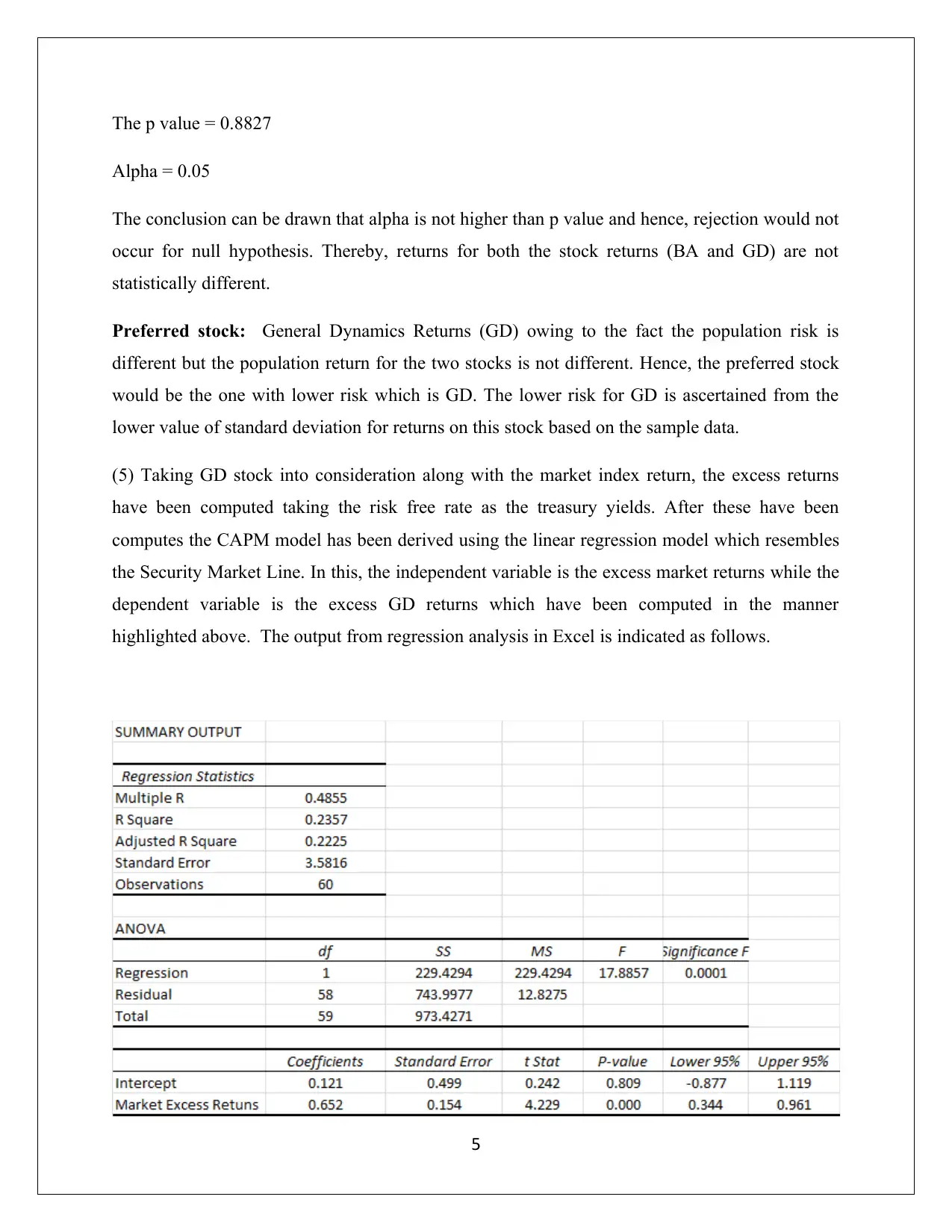

This assignment focuses on the statistical analysis of stock returns for Boeing (BA) and General Dynamics (GD), utilizing hypothesis testing and the Capital Asset Pricing Model (CAPM). The analysis includes Jarque-Bera tests for normality, t-tests for mean return comparison, and F-tests for risk assessment. The study determines that neither Boeing nor General Dynamics returns are normally distributed. Further analysis reveals a statistically significant difference in risk between the two stocks, favoring General Dynamics due to its lower risk profile. The CAPM model is applied to General Dynamics, revealing a beta of 0.652, but the model's explanatory power is limited, as indicated by a low coefficient of determination. The assignment concludes that while General Dynamics may be considered a neutral stock, the residuals of the CAPM model do not satisfy the assumption of normality, suggesting limitations in the model's applicability. Desklib offers more solved assignments and past papers for students.

1 out of 9

Related Documents

![Statistical Analysis of Business and Finance Data - [Semester]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fbusiness-finance-statistics-hypothesis-interpretation_page_2.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.