Analysis of Climate Change Integration into Business Strategy Report

VerifiedAdded on 2023/06/15

|17

|3647

|203

Report

AI Summary

This report investigates the integration of climate change into business strategies, focusing on its impact on carbon disclosure scores and the role of legitimacy theory. It reviews existing literature, presents a conceptual model with independent variables like climate change integration, internal carbon pricing, and risk consideration, and a dependent variable of carbon disclosure score, controlled by firm size. The research employs descriptive and inferential statistics, analyzing data from a sample of 56 companies from the CDP survey 2015, adopting random sampling, data was collected from 28 Companies responding YES and 28 Companies responding NO. The findings reveal variations in carbon disclosure scores based on the integration of climate change into business strategy, with companies integrating climate change showing higher disclosure scores. The report also discusses the implications of legitimacy theory, suggesting that companies perceived as legitimate are more likely to integrate GHG initiatives into their business strategies.

Assigned research question: Is climate change integrated into your business

strategy.

Introduction

Climate changes have significant influences on the visions and profit maximisation strategies of

the organisation. The awareness of the climate changes is increasing day by day throughout the

world in almost every industry. Every organisation has its distinctive opportunities, challenges

and integrating climate change which plays a key role in the policy-making process. The

fundamental issue we want to address here is the incorporation of climate change in the business

strategy. Furthermore, we will relate this issue to the legitimacy theory which means an

organisation seeks to ensure that they operate within the bounds and norms according to the local

societies. To put in simple words, the business activities are perceived to be legitimate. The

bounds and norms are not static so the organisation has to be responsive and the best way is to

rely on the notion of a social contract.

Literature Review –

A plethora of research is available which deal with the issue of climate change and its

incorporation in the process of business policymaking. In this section, we will cover some

important previous studies that deal with the issue of climate change as well as with the

strategy.

Introduction

Climate changes have significant influences on the visions and profit maximisation strategies of

the organisation. The awareness of the climate changes is increasing day by day throughout the

world in almost every industry. Every organisation has its distinctive opportunities, challenges

and integrating climate change which plays a key role in the policy-making process. The

fundamental issue we want to address here is the incorporation of climate change in the business

strategy. Furthermore, we will relate this issue to the legitimacy theory which means an

organisation seeks to ensure that they operate within the bounds and norms according to the local

societies. To put in simple words, the business activities are perceived to be legitimate. The

bounds and norms are not static so the organisation has to be responsive and the best way is to

rely on the notion of a social contract.

Literature Review –

A plethora of research is available which deal with the issue of climate change and its

incorporation in the process of business policymaking. In this section, we will cover some

important previous studies that deal with the issue of climate change as well as with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

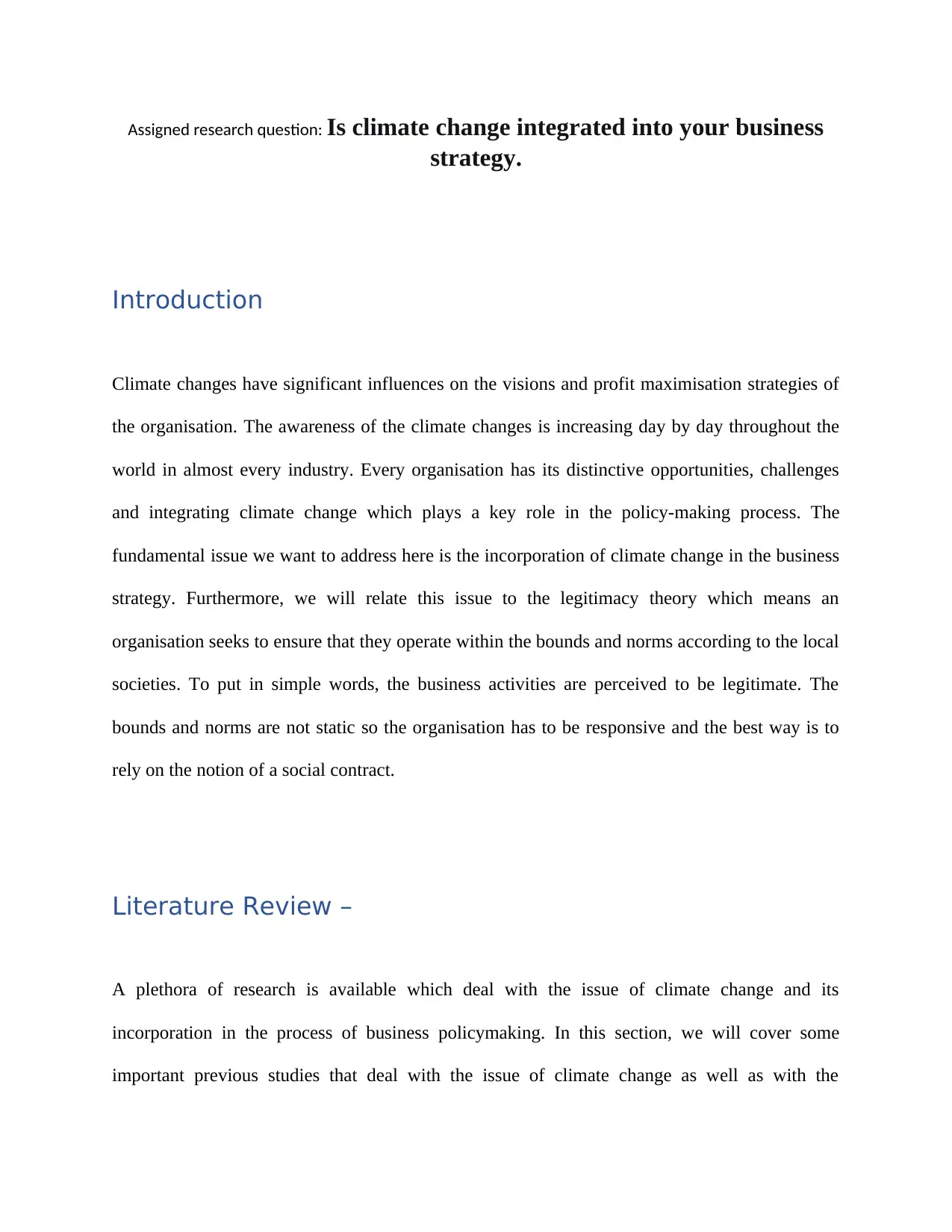

perspective of legitimacy theory. An important study conducted by the McKinsey & Company

which dealing with the generalised perspective on climate change risk that varies industry to

industry. This research is covering almost all major sectors like oil and gas, Chemicals,

agriculture, transport etc. The best way to compile that report is show with the help of the

following chart;

Figure 1. Impact of McKinsey & Co on carbon disclosure. Source: McKinsey & Company

(2017)

Legitimacy theory also aids to assess the Green House Gas emission and social performance of

the firm making it one of the best tool analyse and compare the firm’s performance with climate

change.

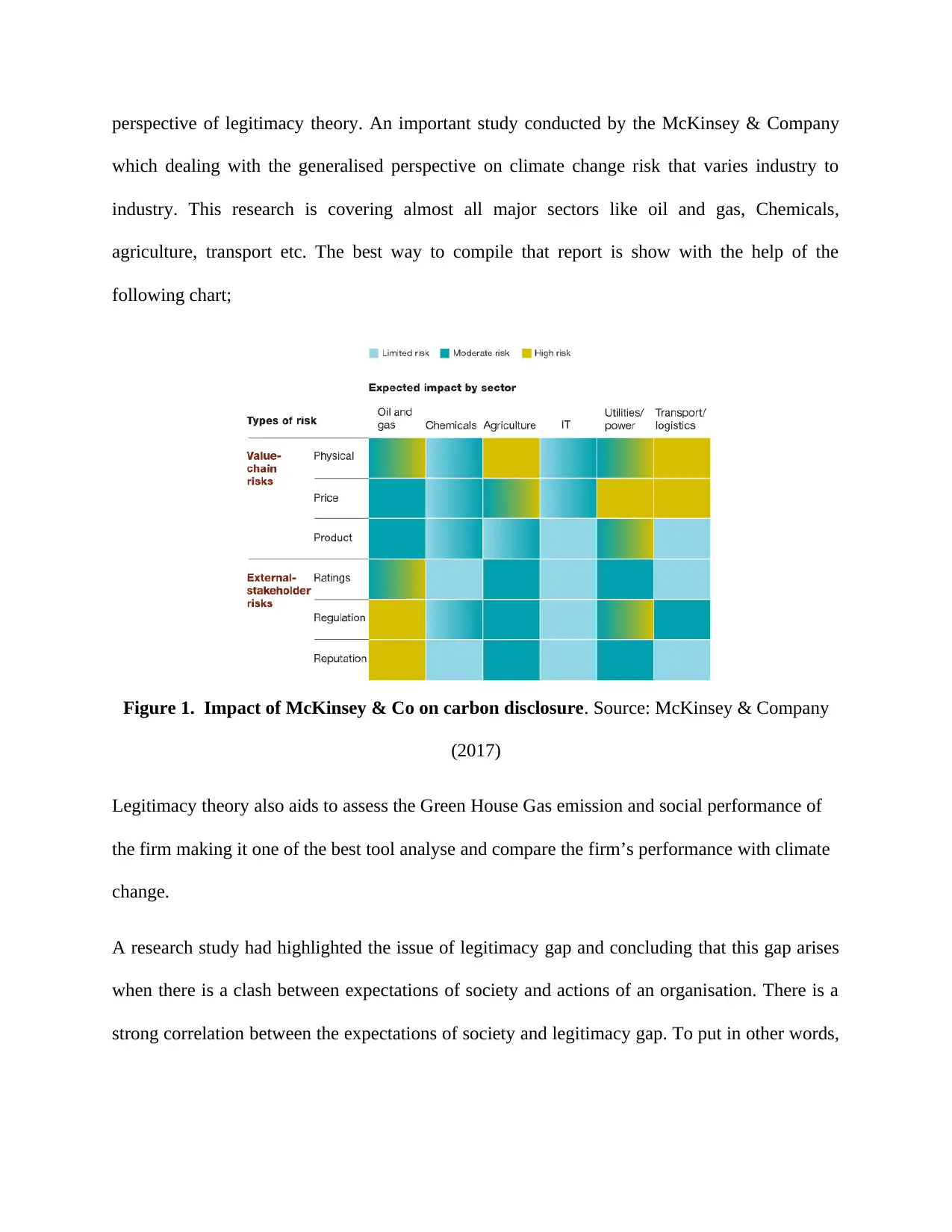

A research study had highlighted the issue of legitimacy gap and concluding that this gap arises

when there is a clash between expectations of society and actions of an organisation. There is a

strong correlation between the expectations of society and legitimacy gap. To put in other words,

which dealing with the generalised perspective on climate change risk that varies industry to

industry. This research is covering almost all major sectors like oil and gas, Chemicals,

agriculture, transport etc. The best way to compile that report is show with the help of the

following chart;

Figure 1. Impact of McKinsey & Co on carbon disclosure. Source: McKinsey & Company

(2017)

Legitimacy theory also aids to assess the Green House Gas emission and social performance of

the firm making it one of the best tool analyse and compare the firm’s performance with climate

change.

A research study had highlighted the issue of legitimacy gap and concluding that this gap arises

when there is a clash between expectations of society and actions of an organisation. There is a

strong correlation between the expectations of society and legitimacy gap. To put in other words,

it means the gap will increase when the expectations of society changes or the unknown

information become known to the society (Set

hi, 1975).

Figure 2. Legitimacy gap. Source: Sethi (1975)

Another research is suggesting the climate change action plan that can be used as a proactive

management of risk that is associated with the climate and also discussing the opportunities and

impacts. This study is based on five stages where the first stage is deal with the understanding

footprints which means mapping the emissions and improving the reporting and accuracy. The

second step is describing the implementation of suitable measures to reduce these emissions. The

next stage is dealing with the engaging externalities which mean for instance to develop methane

and shale development communication or take part in the process of global legislation and

regulations. The final stage is dealing with the building capacity which means to give proper

attention to research and development to form an action plan to incorporate the climate change in

business strategies (Mousa and Hassan, 2015).

Conceptual Model:

information become known to the society (Set

hi, 1975).

Figure 2. Legitimacy gap. Source: Sethi (1975)

Another research is suggesting the climate change action plan that can be used as a proactive

management of risk that is associated with the climate and also discussing the opportunities and

impacts. This study is based on five stages where the first stage is deal with the understanding

footprints which means mapping the emissions and improving the reporting and accuracy. The

second step is describing the implementation of suitable measures to reduce these emissions. The

next stage is dealing with the engaging externalities which mean for instance to develop methane

and shale development communication or take part in the process of global legislation and

regulations. The final stage is dealing with the building capacity which means to give proper

attention to research and development to form an action plan to incorporate the climate change in

business strategies (Mousa and Hassan, 2015).

Conceptual Model:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

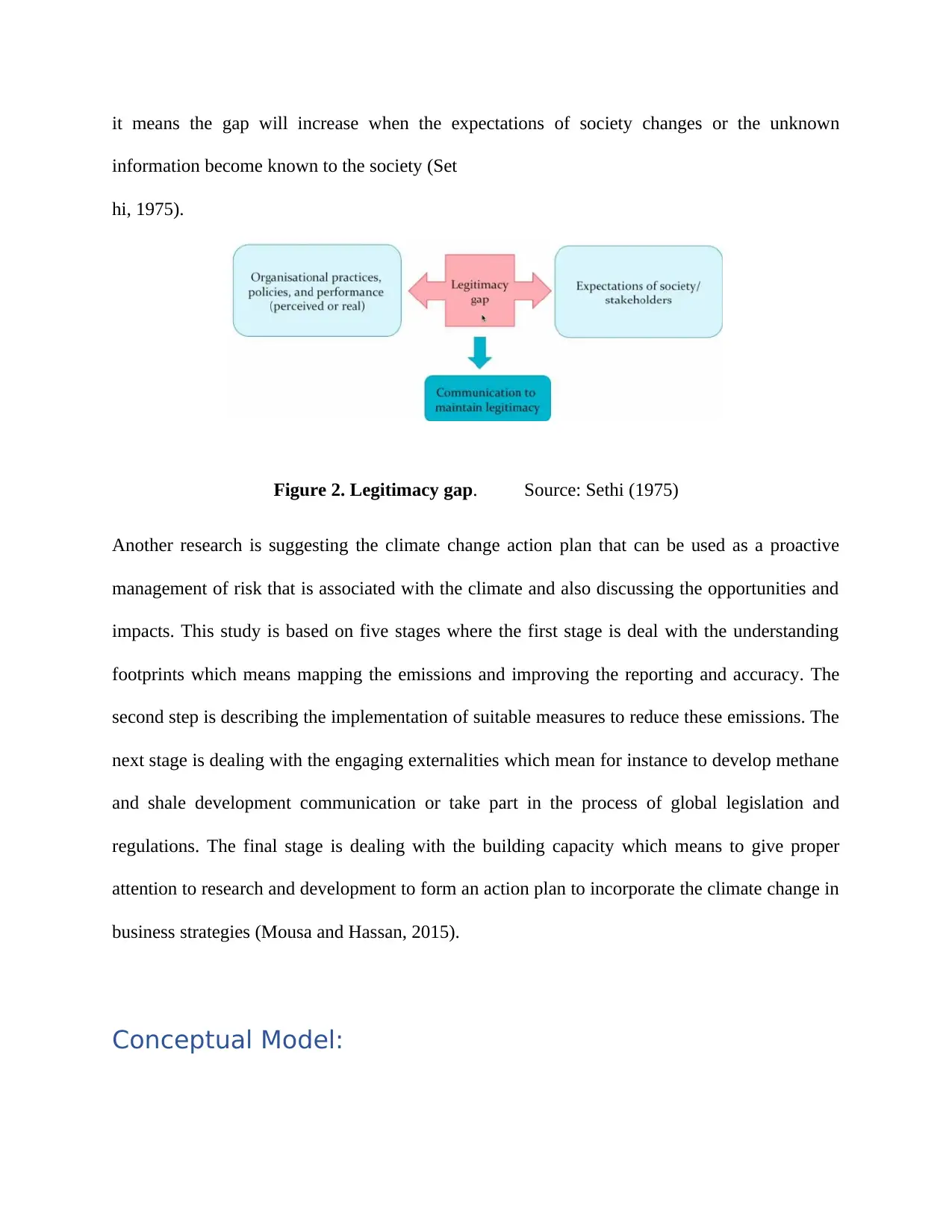

Integration of climate change in business

Internal price of carbon

Future consideration of risk

Carbon disclosure score

Independent Variables

Control variables: Size of the firm

Dependent Variables

The conceptual model of this study which is dealing with the issue of climate changes

incorporation in the business policymaking process can be presented with the help of the

following chart explicitly;

Figure 3. Conceptual model of the research.

In this research framework, there are three independent variables and one dependent variable

along with a control variable. It has been considered that carbon disclosure score is the

dependent variable, which is according to the CDP disclosure is dependent upon the integration

of climate change in business, internal price of carbon and future consideration of risk, making

them the independent variable for this research framework. This research framework considers

that size of the firm is one of the main factors that control the carbon disclosure score, this it will

be considered as the control variable.

Internal price of carbon

Future consideration of risk

Carbon disclosure score

Independent Variables

Control variables: Size of the firm

Dependent Variables

The conceptual model of this study which is dealing with the issue of climate changes

incorporation in the business policymaking process can be presented with the help of the

following chart explicitly;

Figure 3. Conceptual model of the research.

In this research framework, there are three independent variables and one dependent variable

along with a control variable. It has been considered that carbon disclosure score is the

dependent variable, which is according to the CDP disclosure is dependent upon the integration

of climate change in business, internal price of carbon and future consideration of risk, making

them the independent variable for this research framework. This research framework considers

that size of the firm is one of the main factors that control the carbon disclosure score, this it will

be considered as the control variable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

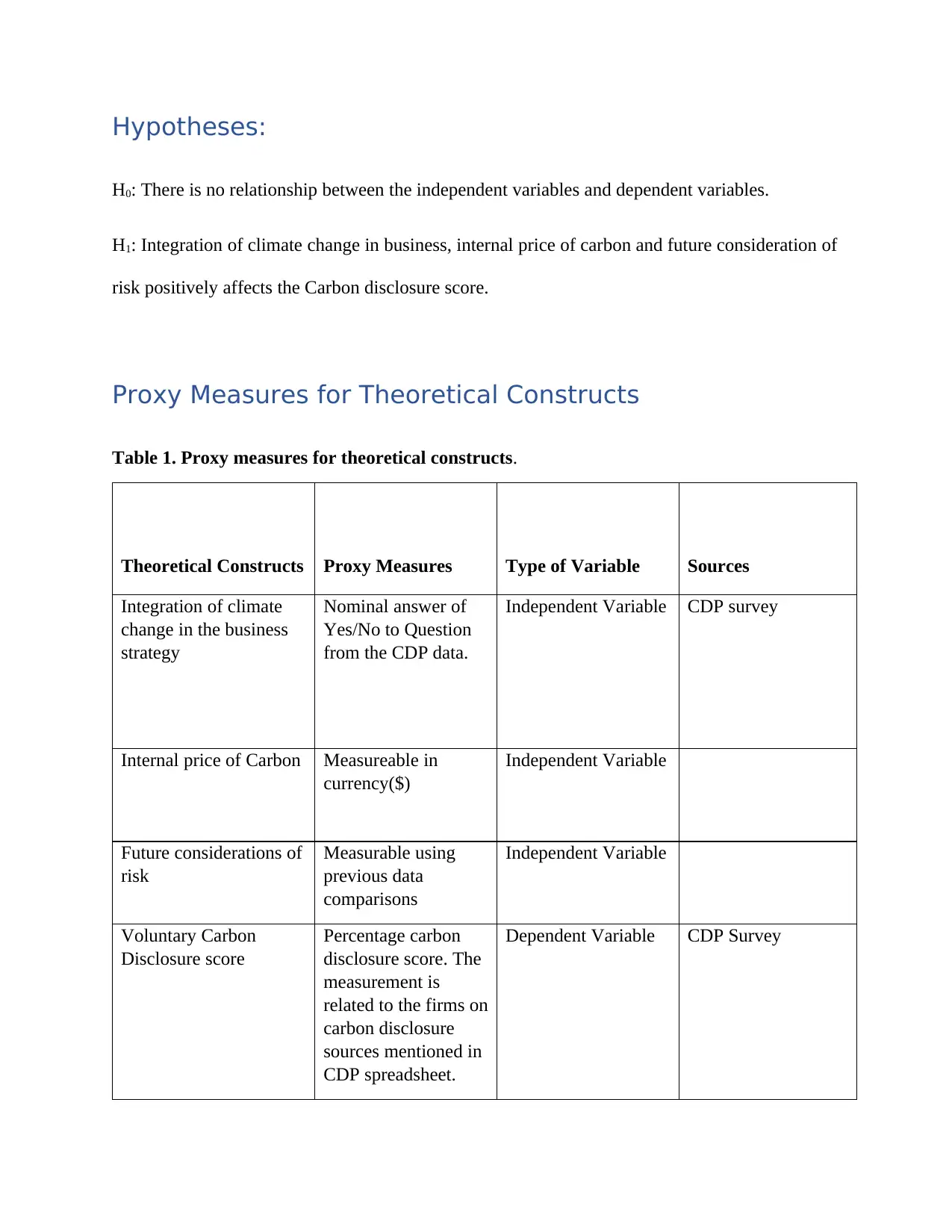

Hypotheses:

H0: There is no relationship between the independent variables and dependent variables.

H1: Integration of climate change in business, internal price of carbon and future consideration of

risk positively affects the Carbon disclosure score.

Proxy Measures for Theoretical Constructs

Table 1. Proxy measures for theoretical constructs.

Theoretical Constructs Proxy Measures Type of Variable Sources

Integration of climate

change in the business

strategy

Nominal answer of

Yes/No to Question

from the CDP data.

Independent Variable CDP survey

Internal price of Carbon Measureable in

currency($)

Independent Variable

Future considerations of

risk

Measurable using

previous data

comparisons

Independent Variable

Voluntary Carbon

Disclosure score

Percentage carbon

disclosure score. The

measurement is

related to the firms on

carbon disclosure

sources mentioned in

CDP spreadsheet.

Dependent Variable CDP Survey

H0: There is no relationship between the independent variables and dependent variables.

H1: Integration of climate change in business, internal price of carbon and future consideration of

risk positively affects the Carbon disclosure score.

Proxy Measures for Theoretical Constructs

Table 1. Proxy measures for theoretical constructs.

Theoretical Constructs Proxy Measures Type of Variable Sources

Integration of climate

change in the business

strategy

Nominal answer of

Yes/No to Question

from the CDP data.

Independent Variable CDP survey

Internal price of Carbon Measureable in

currency($)

Independent Variable

Future considerations of

risk

Measurable using

previous data

comparisons

Independent Variable

Voluntary Carbon

Disclosure score

Percentage carbon

disclosure score. The

measurement is

related to the firms on

carbon disclosure

sources mentioned in

CDP spreadsheet.

Dependent Variable CDP Survey

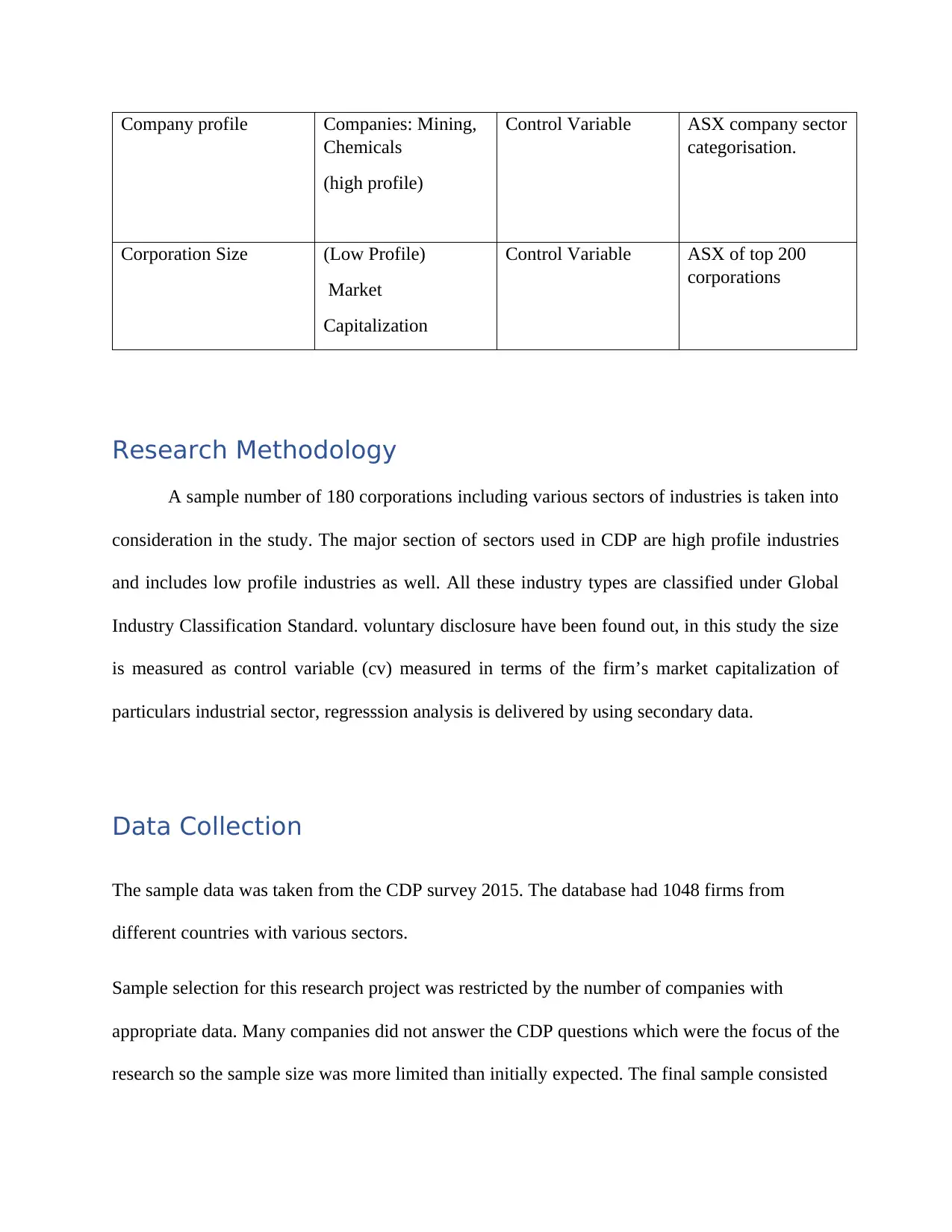

Company profile Companies: Mining,

Chemicals

(high profile)

Control Variable ASX company sector

categorisation.

Corporation Size (Low Profile)

Market

Capitalization

Control Variable ASX of top 200

corporations

Research Methodology

A sample number of 180 corporations including various sectors of industries is taken into

consideration in the study. The major section of sectors used in CDP are high profile industries

and includes low profile industries as well. All these industry types are classified under Global

Industry Classification Standard. voluntary disclosure have been found out, in this study the size

is measured as control variable (cv) measured in terms of the firm’s market capitalization of

particulars industrial sector, regresssion analysis is delivered by using secondary data.

Data Collection

The sample data was taken from the CDP survey 2015. The database had 1048 firms from

different countries with various sectors.

Sample selection for this research project was restricted by the number of companies with

appropriate data. Many companies did not answer the CDP questions which were the focus of the

research so the sample size was more limited than initially expected. The final sample consisted

Chemicals

(high profile)

Control Variable ASX company sector

categorisation.

Corporation Size (Low Profile)

Market

Capitalization

Control Variable ASX of top 200

corporations

Research Methodology

A sample number of 180 corporations including various sectors of industries is taken into

consideration in the study. The major section of sectors used in CDP are high profile industries

and includes low profile industries as well. All these industry types are classified under Global

Industry Classification Standard. voluntary disclosure have been found out, in this study the size

is measured as control variable (cv) measured in terms of the firm’s market capitalization of

particulars industrial sector, regresssion analysis is delivered by using secondary data.

Data Collection

The sample data was taken from the CDP survey 2015. The database had 1048 firms from

different countries with various sectors.

Sample selection for this research project was restricted by the number of companies with

appropriate data. Many companies did not answer the CDP questions which were the focus of the

research so the sample size was more limited than initially expected. The final sample consisted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of 56 companies from different countries and various sectors. These companies did have a

response to the identified research question. (Note that the class lecturer approved the use of 56

companies given the research question and CDP data). Adopting random sampling, data was

collected from 28 Companies responding YES and 28 Companies responding NO.

Data Analysis - Descriptive

Descriptive data analysis is being used in the research paper to analyse the data and comparison.

Descriptive data analysis is the best form to analyse and tabulate the collective data from the

samples and graphical representation as well. Mean, Median, Mode are used to measure the

central tendency results to analyse their differences from the data collection. Range, kurtosis,

skewness is used to box plot the central tendency results.

On the basis parameters, the research proceeds to explain about the analysing of data by means

of tabular representation using descriptive analysis. The two key research questions for

descriptive data analysis were the following:

1. Is climate change is integrated in the business strategy, and if so, how does it affect the

carbon disclosure score?

2. Is climate change not integrated into the business strategy and if so, how does it affect the

carbon disclosure score?

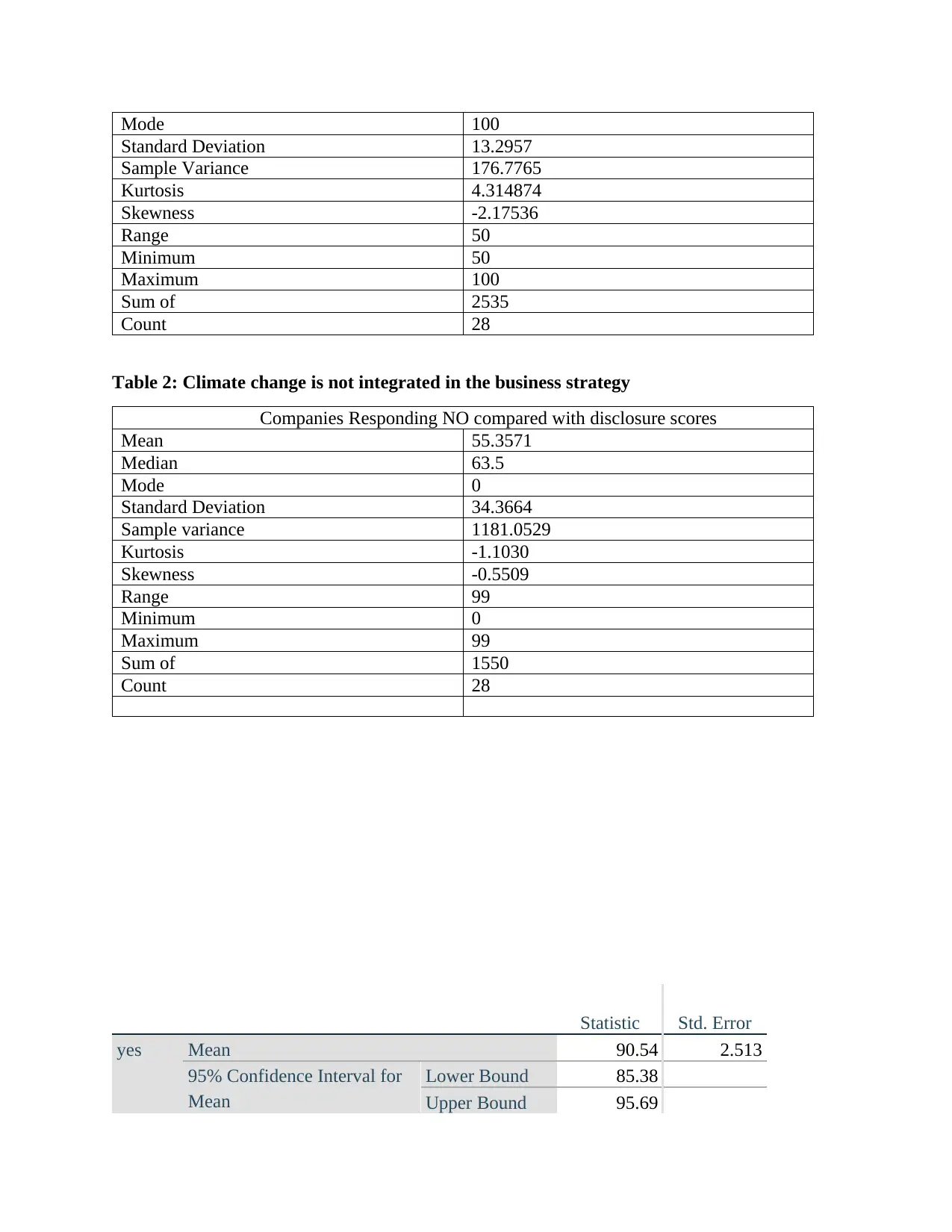

Table 1. Companies where climate change is integrated in the business strategy

Companies responding YES compared with disclosure scores

Mean 90.53571

Median 94

response to the identified research question. (Note that the class lecturer approved the use of 56

companies given the research question and CDP data). Adopting random sampling, data was

collected from 28 Companies responding YES and 28 Companies responding NO.

Data Analysis - Descriptive

Descriptive data analysis is being used in the research paper to analyse the data and comparison.

Descriptive data analysis is the best form to analyse and tabulate the collective data from the

samples and graphical representation as well. Mean, Median, Mode are used to measure the

central tendency results to analyse their differences from the data collection. Range, kurtosis,

skewness is used to box plot the central tendency results.

On the basis parameters, the research proceeds to explain about the analysing of data by means

of tabular representation using descriptive analysis. The two key research questions for

descriptive data analysis were the following:

1. Is climate change is integrated in the business strategy, and if so, how does it affect the

carbon disclosure score?

2. Is climate change not integrated into the business strategy and if so, how does it affect the

carbon disclosure score?

Table 1. Companies where climate change is integrated in the business strategy

Companies responding YES compared with disclosure scores

Mean 90.53571

Median 94

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mode 100

Standard Deviation 13.2957

Sample Variance 176.7765

Kurtosis 4.314874

Skewness -2.17536

Range 50

Minimum 50

Maximum 100

Sum of 2535

Count 28

Table 2: Climate change is not integrated in the business strategy

Companies Responding NO compared with disclosure scores

Mean 55.3571

Median 63.5

Mode 0

Standard Deviation 34.3664

Sample variance 1181.0529

Kurtosis -1.1030

Skewness -0.5509

Range 99

Minimum 0

Maximum 99

Sum of 1550

Count 28

Statistic Std. Error

yes Mean 90.54 2.513

95% Confidence Interval for

Mean

Lower Bound 85.38

Upper Bound 95.69

Standard Deviation 13.2957

Sample Variance 176.7765

Kurtosis 4.314874

Skewness -2.17536

Range 50

Minimum 50

Maximum 100

Sum of 2535

Count 28

Table 2: Climate change is not integrated in the business strategy

Companies Responding NO compared with disclosure scores

Mean 55.3571

Median 63.5

Mode 0

Standard Deviation 34.3664

Sample variance 1181.0529

Kurtosis -1.1030

Skewness -0.5509

Range 99

Minimum 0

Maximum 99

Sum of 1550

Count 28

Statistic Std. Error

yes Mean 90.54 2.513

95% Confidence Interval for

Mean

Lower Bound 85.38

Upper Bound 95.69

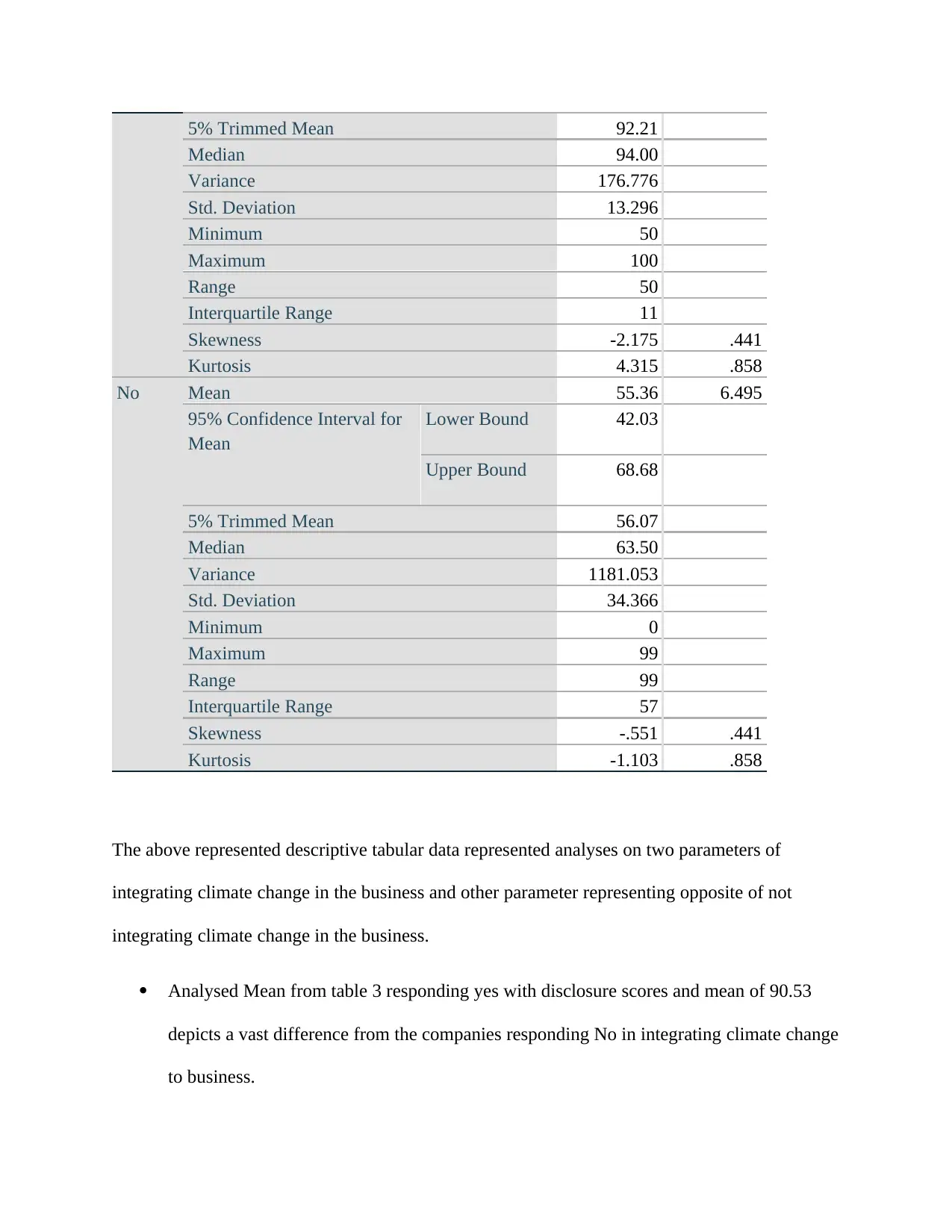

5% Trimmed Mean 92.21

Median 94.00

Variance 176.776

Std. Deviation 13.296

Minimum 50

Maximum 100

Range 50

Interquartile Range 11

Skewness -2.175 .441

Kurtosis 4.315 .858

No Mean 55.36 6.495

95% Confidence Interval for

Mean

Lower Bound 42.03

Upper Bound 68.68

5% Trimmed Mean 56.07

Median 63.50

Variance 1181.053

Std. Deviation 34.366

Minimum 0

Maximum 99

Range 99

Interquartile Range 57

Skewness -.551 .441

Kurtosis -1.103 .858

The above represented descriptive tabular data represented analyses on two parameters of

integrating climate change in the business and other parameter representing opposite of not

integrating climate change in the business.

Analysed Mean from table 3 responding yes with disclosure scores and mean of 90.53

depicts a vast difference from the companies responding No in integrating climate change

to business.

Median 94.00

Variance 176.776

Std. Deviation 13.296

Minimum 50

Maximum 100

Range 50

Interquartile Range 11

Skewness -2.175 .441

Kurtosis 4.315 .858

No Mean 55.36 6.495

95% Confidence Interval for

Mean

Lower Bound 42.03

Upper Bound 68.68

5% Trimmed Mean 56.07

Median 63.50

Variance 1181.053

Std. Deviation 34.366

Minimum 0

Maximum 99

Range 99

Interquartile Range 57

Skewness -.551 .441

Kurtosis -1.103 .858

The above represented descriptive tabular data represented analyses on two parameters of

integrating climate change in the business and other parameter representing opposite of not

integrating climate change in the business.

Analysed Mean from table 3 responding yes with disclosure scores and mean of 90.53

depicts a vast difference from the companies responding No in integrating climate change

to business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

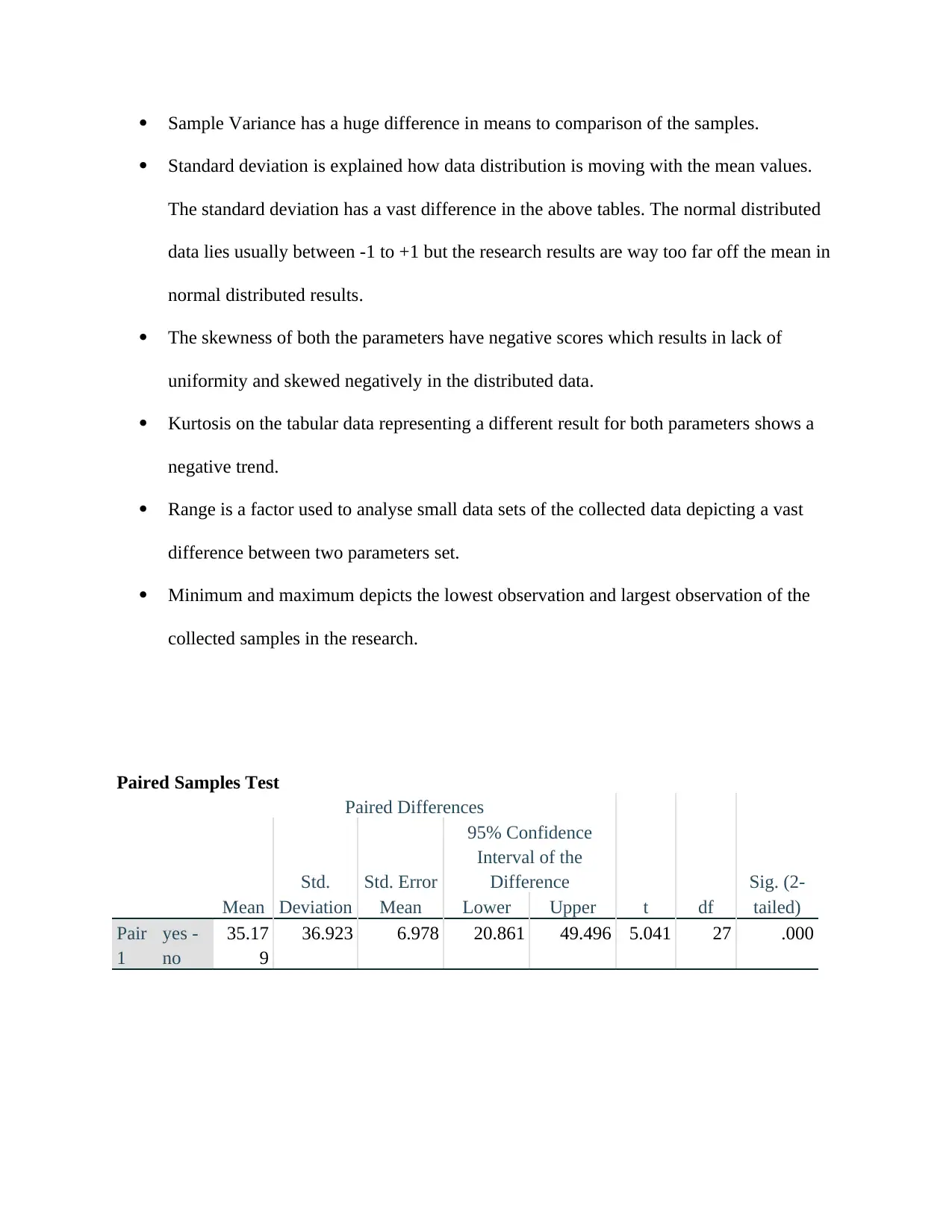

Sample Variance has a huge difference in means to comparison of the samples.

Standard deviation is explained how data distribution is moving with the mean values.

The standard deviation has a vast difference in the above tables. The normal distributed

data lies usually between -1 to +1 but the research results are way too far off the mean in

normal distributed results.

The skewness of both the parameters have negative scores which results in lack of

uniformity and skewed negatively in the distributed data.

Kurtosis on the tabular data representing a different result for both parameters shows a

negative trend.

Range is a factor used to analyse small data sets of the collected data depicting a vast

difference between two parameters set.

Minimum and maximum depicts the lowest observation and largest observation of the

collected samples in the research.

Paired Samples Test

Paired Differences

t df

Sig. (2-

tailed)Mean

Std.

Deviation

Std. Error

Mean

95% Confidence

Interval of the

Difference

Lower Upper

Pair

1

yes -

no

35.17

9

36.923 6.978 20.861 49.496 5.041 27 .000

Standard deviation is explained how data distribution is moving with the mean values.

The standard deviation has a vast difference in the above tables. The normal distributed

data lies usually between -1 to +1 but the research results are way too far off the mean in

normal distributed results.

The skewness of both the parameters have negative scores which results in lack of

uniformity and skewed negatively in the distributed data.

Kurtosis on the tabular data representing a different result for both parameters shows a

negative trend.

Range is a factor used to analyse small data sets of the collected data depicting a vast

difference between two parameters set.

Minimum and maximum depicts the lowest observation and largest observation of the

collected samples in the research.

Paired Samples Test

Paired Differences

t df

Sig. (2-

tailed)Mean

Std.

Deviation

Std. Error

Mean

95% Confidence

Interval of the

Difference

Lower Upper

Pair

1

yes -

no

35.17

9

36.923 6.978 20.861 49.496 5.041 27 .000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

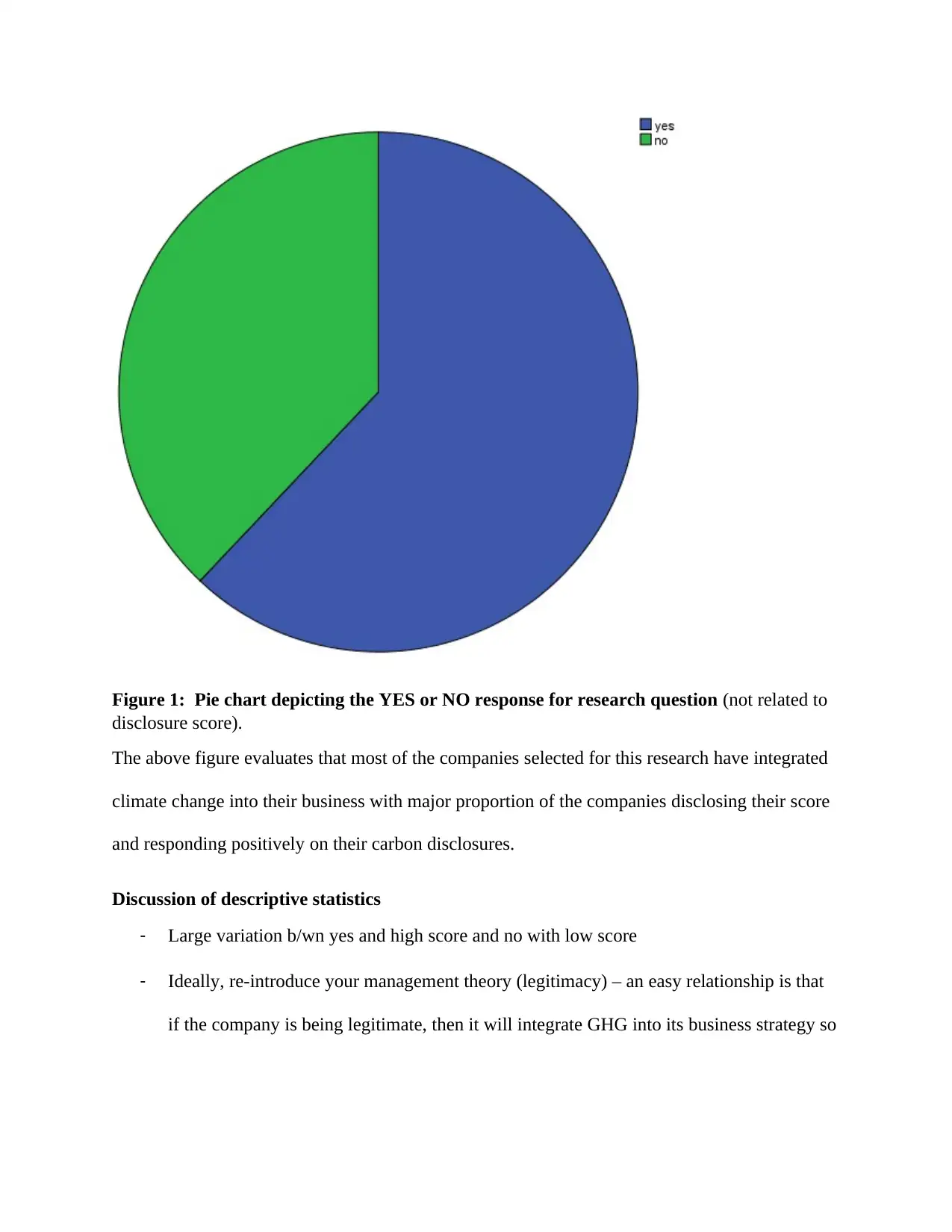

Figure 1: Pie chart depicting the YES or NO response for research question (not related to

disclosure score).

The above figure evaluates that most of the companies selected for this research have integrated

climate change into their business with major proportion of the companies disclosing their score

and responding positively on their carbon disclosures.

Discussion of descriptive statistics

- Large variation b/wn yes and high score and no with low score

- Ideally, re-introduce your management theory (legitimacy) – an easy relationship is that

if the company is being legitimate, then it will integrate GHG into its business strategy so

disclosure score).

The above figure evaluates that most of the companies selected for this research have integrated

climate change into their business with major proportion of the companies disclosing their score

and responding positively on their carbon disclosures.

Discussion of descriptive statistics

- Large variation b/wn yes and high score and no with low score

- Ideally, re-introduce your management theory (legitimacy) – an easy relationship is that

if the company is being legitimate, then it will integrate GHG into its business strategy so

that it’s higher disclosure is legitimate or makes sense. They’re not faking their GHG

initiative so could be perceived as more legit. Refs…. 1-2 paras

Research on descriptive data analysis resulted in large variation of results of the companies

responding Positive on the research question with higher values of YES disclosure scores about

the companies responding very less and negatively NO in number of disclosure scores in CDP

survey. Descriptive statistics of the research using SPSS method resulted that most of the

companies had a positive response in relation to integration climate change into business

strategy.

Reintroducing my research theory Legitimacy theory into the research. Legitimacy theory has

been more about research papers these days as there is an assumption that some proposals and

tasks of the entity are on spot to some uplifted number of norms adopted socially. The research

summarizes that companies having large variation of responding positively on research question,

which reasonably entitled to legit information on disclosure of their scores.

Data Analysis- Inferential statistics

The study is focused around the conjecture which states that, carbon disclosure score of the

company depends on a company’s act of integrating climate change as a component in its

business strategy, its internal pricing score of carbon and its consideration of future risk, where

size of the firm is the control variable (Guenther et al., 2016). The assumption on which the

study stands is that the companies belong to the same population of companies. The available

carbon disclosure score is depends on the treatment of the variable representing the integration

status of climate change to the business model, which leads to two groups of companies. The

initiative so could be perceived as more legit. Refs…. 1-2 paras

Research on descriptive data analysis resulted in large variation of results of the companies

responding Positive on the research question with higher values of YES disclosure scores about

the companies responding very less and negatively NO in number of disclosure scores in CDP

survey. Descriptive statistics of the research using SPSS method resulted that most of the

companies had a positive response in relation to integration climate change into business

strategy.

Reintroducing my research theory Legitimacy theory into the research. Legitimacy theory has

been more about research papers these days as there is an assumption that some proposals and

tasks of the entity are on spot to some uplifted number of norms adopted socially. The research

summarizes that companies having large variation of responding positively on research question,

which reasonably entitled to legit information on disclosure of their scores.

Data Analysis- Inferential statistics

The study is focused around the conjecture which states that, carbon disclosure score of the

company depends on a company’s act of integrating climate change as a component in its

business strategy, its internal pricing score of carbon and its consideration of future risk, where

size of the firm is the control variable (Guenther et al., 2016). The assumption on which the

study stands is that the companies belong to the same population of companies. The available

carbon disclosure score is depends on the treatment of the variable representing the integration

status of climate change to the business model, which leads to two groups of companies. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.