Business Strategy Report: Business Strategy in Financial Industry

VerifiedAdded on 2023/01/05

|11

|3246

|37

Report

AI Summary

This report provides a comprehensive analysis of business strategy within the financial industry, focusing on Deloitte as a case study. It begins with an introduction to strategic planning, emphasizing its importance in achieving organizational objectives. The report then identifies key challenges faced by financial institutions in the UK, including consumer expectations, competition, investor expectations, and regulatory conditions. Furthermore, it differentiates between wholesale and retail banking, highlighting their distinct characteristics, products, profitability, and operational structures. The report also evaluates the effectiveness of strategic options using the Ansoff matrix, exploring market penetration and market development strategies. The analysis provides valuable insights into strategic planning and implementation within the financial sector.

Business strategy

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

1.Strategic planning in context of the financial industry:............................................................3

2.Challenges faced by the financial industries in UK:................................................................4

3. Strategic implementation and differentiation between wholesale and retail organisation......5

4.Evaluate the effectiveness and application of strategic option.................................................6

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................1

1

INTRODUCTION...........................................................................................................................3

1.Strategic planning in context of the financial industry:............................................................3

2.Challenges faced by the financial industries in UK:................................................................4

3. Strategic implementation and differentiation between wholesale and retail organisation......5

4.Evaluate the effectiveness and application of strategic option.................................................6

CONCLUSION................................................................................................................................9

REFERENCES................................................................................................................................1

1

INTRODUCTION

Business strategy is basically a long-term planning executed by the management personals

in order to acquire futuristic objectives and targets of the organisation. This strategy includes the

products and services company planning to offer, short- term and long-term objectives, the kind

of target market or customers they wanted to cater. This report will conduct a detailed study on

Deloitte. The Deloitte TT limited was founded in 1845 with its origin in London, UNITED

KINGDOM. It is a multinational company dealing in specialised service sector. They provide

various services like auditing, risk and financial advisory, consultation, tax and lawful services.

This following report will define the strategic planning’s followed in a financial industry. Further

it will also identify various challenges which a monetary institution in UK have to face. It will

also describe the different strategies implemented in wholesale and retail banking and

differentiate them on that basis. Lastly the research will critically evaluate the applications of

tactical models to the retail industry.

1.Strategic planning in context of the financial industry:

Business planning is the procedure of development a direction for business and will help to

identify the long term and short-term objectives. This planning process also helps to monitor the

mission and objectives of the enterprise and identifying the tools and techniques to achieve them.

Managing budget statement, assets sheet and bankbook planning is a complex process but it has

to be carried out to manage risk management of interest rates and wealth management

(Alstadheim, 2020). Technological advancement preparation is very essential for banks varies

from small scale to large scale as mobile banking and safety & security of data is becoming

important. Lastly, the merger and amalgamation planning prioritised by the management of

financial enterprises. Different activities will be implanted in the organization like, tactical,

technological, Mergers and acquisition and finance planning.

Mergers and acquisitions planning: The M&A planning prove is important for every scale size

firms and plays a key role in financing strategic plans. The financial services have experienced

significant integration. Through this process the biggest companies like Deloitte have grown

bigger. The association is very obvious in city areas and small size market. Banks with high asset

values take part in attainments, in most of the acquisitions, such banks will act as buyers.

2

Business strategy is basically a long-term planning executed by the management personals

in order to acquire futuristic objectives and targets of the organisation. This strategy includes the

products and services company planning to offer, short- term and long-term objectives, the kind

of target market or customers they wanted to cater. This report will conduct a detailed study on

Deloitte. The Deloitte TT limited was founded in 1845 with its origin in London, UNITED

KINGDOM. It is a multinational company dealing in specialised service sector. They provide

various services like auditing, risk and financial advisory, consultation, tax and lawful services.

This following report will define the strategic planning’s followed in a financial industry. Further

it will also identify various challenges which a monetary institution in UK have to face. It will

also describe the different strategies implemented in wholesale and retail banking and

differentiate them on that basis. Lastly the research will critically evaluate the applications of

tactical models to the retail industry.

1.Strategic planning in context of the financial industry:

Business planning is the procedure of development a direction for business and will help to

identify the long term and short-term objectives. This planning process also helps to monitor the

mission and objectives of the enterprise and identifying the tools and techniques to achieve them.

Managing budget statement, assets sheet and bankbook planning is a complex process but it has

to be carried out to manage risk management of interest rates and wealth management

(Alstadheim, 2020). Technological advancement preparation is very essential for banks varies

from small scale to large scale as mobile banking and safety & security of data is becoming

important. Lastly, the merger and amalgamation planning prioritised by the management of

financial enterprises. Different activities will be implanted in the organization like, tactical,

technological, Mergers and acquisition and finance planning.

Mergers and acquisitions planning: The M&A planning prove is important for every scale size

firms and plays a key role in financing strategic plans. The financial services have experienced

significant integration. Through this process the biggest companies like Deloitte have grown

bigger. The association is very obvious in city areas and small size market. Banks with high asset

values take part in attainments, in most of the acquisitions, such banks will act as buyers.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Amalgamation planning should essentially be the part of tactical development progression. This

will determine Who can merge with you? Who can acquire you?

Technology planning: It does not matter whether the bank is private or corporate adapting

technological advancement is necessary. Technology will provide an insight of how a company

uses or utilize technological support in corporation activities (Fernandes and Pinto, 2019). It

includes, what are the needs of customers in mobile and internet banking services? Protection

and safety of customers personal data?

Capital Planning: This planning process will determine how a firm can manage their annual

report. In Deloitte they emphasise on investment plan which is required to be updated on a

timely basis to acquiescence with fresh aimed wealth stages and fulfil organisational needs.

Understanding of these guidelines are essential to have a better understanding of the asset and

liabilities and commercial plan, for the clienteles and shareholders companies cater to (Steiner,

2010).

Strategic planning: An efficient Strategic Plan will result in overall success. The Mission and

Vision are more permanent, but the strategy will be modified and revised on continue basis. The

exact thing will be implicated for the long term and short-term goals as well. Through this

planning procedure it will enable to identify the major initiatives to be taken (Gertler, Kiyotaki

and Prestipino, 2016).

2.Challenges faced by the financial industries in UK:

The banking industries are facing extraordinary revolution as it moving or growing

forward. Most of the financial firms have adapted the high-tech uprising, but there are still many

challenges present in the market which need to overcome. The banking establishments will need

new and innovative ideas and methods for accomplishment. Now a day’s customer expects faster

accessibility and better results (Bryson, Edwards and Van Slyke, 2018). Financial institutions

which fails or left behind to maintain the pace with the ever-changing environment and

competition will suffer in the long run. The banking industry facing challenges in numerous

ways, they are discussed below.

Consumer expectations: Deloitte TT are finding it hard to maintain balance with the client’s

expectations. Traditional banking institutions are struggling really hard to deliver the services

which were demanded by the customers specifically in regards with technology. For example, A

3

will determine Who can merge with you? Who can acquire you?

Technology planning: It does not matter whether the bank is private or corporate adapting

technological advancement is necessary. Technology will provide an insight of how a company

uses or utilize technological support in corporation activities (Fernandes and Pinto, 2019). It

includes, what are the needs of customers in mobile and internet banking services? Protection

and safety of customers personal data?

Capital Planning: This planning process will determine how a firm can manage their annual

report. In Deloitte they emphasise on investment plan which is required to be updated on a

timely basis to acquiescence with fresh aimed wealth stages and fulfil organisational needs.

Understanding of these guidelines are essential to have a better understanding of the asset and

liabilities and commercial plan, for the clienteles and shareholders companies cater to (Steiner,

2010).

Strategic planning: An efficient Strategic Plan will result in overall success. The Mission and

Vision are more permanent, but the strategy will be modified and revised on continue basis. The

exact thing will be implicated for the long term and short-term goals as well. Through this

planning procedure it will enable to identify the major initiatives to be taken (Gertler, Kiyotaki

and Prestipino, 2016).

2.Challenges faced by the financial industries in UK:

The banking industries are facing extraordinary revolution as it moving or growing

forward. Most of the financial firms have adapted the high-tech uprising, but there are still many

challenges present in the market which need to overcome. The banking establishments will need

new and innovative ideas and methods for accomplishment. Now a day’s customer expects faster

accessibility and better results (Bryson, Edwards and Van Slyke, 2018). Financial institutions

which fails or left behind to maintain the pace with the ever-changing environment and

competition will suffer in the long run. The banking industry facing challenges in numerous

ways, they are discussed below.

Consumer expectations: Deloitte TT are finding it hard to maintain balance with the client’s

expectations. Traditional banking institutions are struggling really hard to deliver the services

which were demanded by the customers specifically in regards with technology. For example, A

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

large percentage of customers are using mobile banking and internet banking for transactions. A

research was conducted and it was found that banking clienteles use smartphones or other

electronic devices for banking, but they also expect good personal customer handling when they

physically visit their bank branches.

Increasing pressure from competition: Consumers are ready to experiment or make changes

with their monetary facilities provider. Currently there are many firms entering in the finance

market and people are switching to them as they brink new technologically advanced and

innovative ideas (Melecky and Podpiera, 2018). Deloitte have less complicated procedures and

good return on investment or interest rates. This is the main reason people deviate from

traditional banking facilities to these modern monetary firms.

Investor expectations: As mentioned in the above point entering of new competition in the

market, investors’ expectations are fluctuating rapidly. This will make it difficult for the

conventional establishments, which leads to lowering down the participation of new investors

and preventing the turnover of existing shareholders (Okpebholo and Sheikh, 2020).

Regulatory conditions: Protocols in the financial service area are deteriorating, which compels

the banks to invest a large ratio of their personal budget. Establishing and efficient system which

is eligible to maintain a balance with the guidelines and standards necessitate resources.

Traditional banks were facing such kind of extreme challenges, which leads them to push harder

to evolve, modify and improve their functions to keep up the leap with the continuously

changing buyer and investor outlooks. Financial companies are struggling to identify the aspects

which ensure them to acquire sustainable progress (Visco, 2018). Investment and economic

service area enterprises are required to develop an efficient tactic which help them to enhance the

cliental involvement.

3. Strategic implementation and differentiation between wholesale and retail organisation

Traditionally banking referred to a place where people can withdraw and deposit their cash

and take credit when they need capital. Nowadays financial services have completed change

from what they were before. Retail and wholesale banking are biggest example of that, the

differences between retail and wholesale banking are mentioned below:

Characteristics of retail banking: They have numerous networks of distribution which include

branches, through online websites, portals and mobile applications, customer service call centers

4

research was conducted and it was found that banking clienteles use smartphones or other

electronic devices for banking, but they also expect good personal customer handling when they

physically visit their bank branches.

Increasing pressure from competition: Consumers are ready to experiment or make changes

with their monetary facilities provider. Currently there are many firms entering in the finance

market and people are switching to them as they brink new technologically advanced and

innovative ideas (Melecky and Podpiera, 2018). Deloitte have less complicated procedures and

good return on investment or interest rates. This is the main reason people deviate from

traditional banking facilities to these modern monetary firms.

Investor expectations: As mentioned in the above point entering of new competition in the

market, investors’ expectations are fluctuating rapidly. This will make it difficult for the

conventional establishments, which leads to lowering down the participation of new investors

and preventing the turnover of existing shareholders (Okpebholo and Sheikh, 2020).

Regulatory conditions: Protocols in the financial service area are deteriorating, which compels

the banks to invest a large ratio of their personal budget. Establishing and efficient system which

is eligible to maintain a balance with the guidelines and standards necessitate resources.

Traditional banks were facing such kind of extreme challenges, which leads them to push harder

to evolve, modify and improve their functions to keep up the leap with the continuously

changing buyer and investor outlooks. Financial companies are struggling to identify the aspects

which ensure them to acquire sustainable progress (Visco, 2018). Investment and economic

service area enterprises are required to develop an efficient tactic which help them to enhance the

cliental involvement.

3. Strategic implementation and differentiation between wholesale and retail organisation

Traditionally banking referred to a place where people can withdraw and deposit their cash

and take credit when they need capital. Nowadays financial services have completed change

from what they were before. Retail and wholesale banking are biggest example of that, the

differences between retail and wholesale banking are mentioned below:

Characteristics of retail banking: They have numerous networks of distribution which include

branches, through online websites, portals and mobile applications, customer service call centers

4

and kiosks etc. They also have a large no. of customers groups like, individual customers,

household or domestic customers, SME’s etc.

Characteristics of corporate banking: The services provided by such banking institutions are

facilitating deposits, credit facilities, email banking, trading and investing financing and loaning,

term lending’s and guarantees of bank. They also provide customised services for large

institutions and multinational companies. Some of those services are, capital and investment

management, international dealings, stakeholder’s management, financing large scale projects,

consultation services etc.

Definition: Retail banks refers to the type of banking services which caters to individuals and

their main concern is acquiring retail consumers. On the other side wholesale banking targets big

or high-profile business customers and providing efficient services to commercial consumers.

Products: Private customer banks provide a wide range of services which includes, deposit

accounts, vehicle, housing loans, loans against property, insurances, credit facilities and

stockholding services etc. products and services offered by commercial banks are trading,

industry, import, business, equipment funding loans (Gomera, Chinyamurindi and Mishi, 2018).

In Private banking, standardized services and products are presented to their potential consumers

these commodities and services are also termed as off-the-shelf. On the contrary commercial

banking, tends to modify and tailor their products and facilities, in accordance with the

preferences of the clients.

Profitability: In terms of profit corporate banks turn out to be more profitable in contrast the

private cliental banks.

Ticket Size of Loan: The size tickets provided for loans is low due the effect of Non-performing

assets in retail banking in comparison with wholesale banking whose ticket size is high and due

to distinct influence of NPA. For example: Car loans, education, personal, housing loans are

provided by retail banks whereas big loans like industry, equipment, import and export loans

were offered by corporate banks.

5

household or domestic customers, SME’s etc.

Characteristics of corporate banking: The services provided by such banking institutions are

facilitating deposits, credit facilities, email banking, trading and investing financing and loaning,

term lending’s and guarantees of bank. They also provide customised services for large

institutions and multinational companies. Some of those services are, capital and investment

management, international dealings, stakeholder’s management, financing large scale projects,

consultation services etc.

Definition: Retail banks refers to the type of banking services which caters to individuals and

their main concern is acquiring retail consumers. On the other side wholesale banking targets big

or high-profile business customers and providing efficient services to commercial consumers.

Products: Private customer banks provide a wide range of services which includes, deposit

accounts, vehicle, housing loans, loans against property, insurances, credit facilities and

stockholding services etc. products and services offered by commercial banks are trading,

industry, import, business, equipment funding loans (Gomera, Chinyamurindi and Mishi, 2018).

In Private banking, standardized services and products are presented to their potential consumers

these commodities and services are also termed as off-the-shelf. On the contrary commercial

banking, tends to modify and tailor their products and facilities, in accordance with the

preferences of the clients.

Profitability: In terms of profit corporate banks turn out to be more profitable in contrast the

private cliental banks.

Ticket Size of Loan: The size tickets provided for loans is low due the effect of Non-performing

assets in retail banking in comparison with wholesale banking whose ticket size is high and due

to distinct influence of NPA. For example: Car loans, education, personal, housing loans are

provided by retail banks whereas big loans like industry, equipment, import and export loans

were offered by corporate banks.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Monitoring and Recovery: It is quite difficult to do recovery and observation in private banking

sector as their customer base is very wide but as corporate banks caters to only commercial and

business people their client ratio is comparatively small so this makes it easy for them to do

recovery and monitoring procedures efficiently (Kosiba, J.P.B., and et. al., 2018).

Interest Rates: The depository cost is minimum because their consumers don’t have to liberty or

to bargain as they have less deposits in banks but the customer base of wholesale banks have

opportunity to ask for high interest rates as they deposit very large amount of capitals and funds.

Operational Costs: The overall operational cost incurred in the establishment of private

financing firms is very high as they have to set up various branches in distinct location to acquire

and to reach large number of clients. It is totally opposite in the case of commercial financers as

they operate from their main branches and those are sufficient to supply services to their cliental

base.

As this is clearly evaluated from the above detailed implementation that there is a vast difference

between retail and wholesale banking which is the reason banks are establishing separate

branches in accordance with their business.

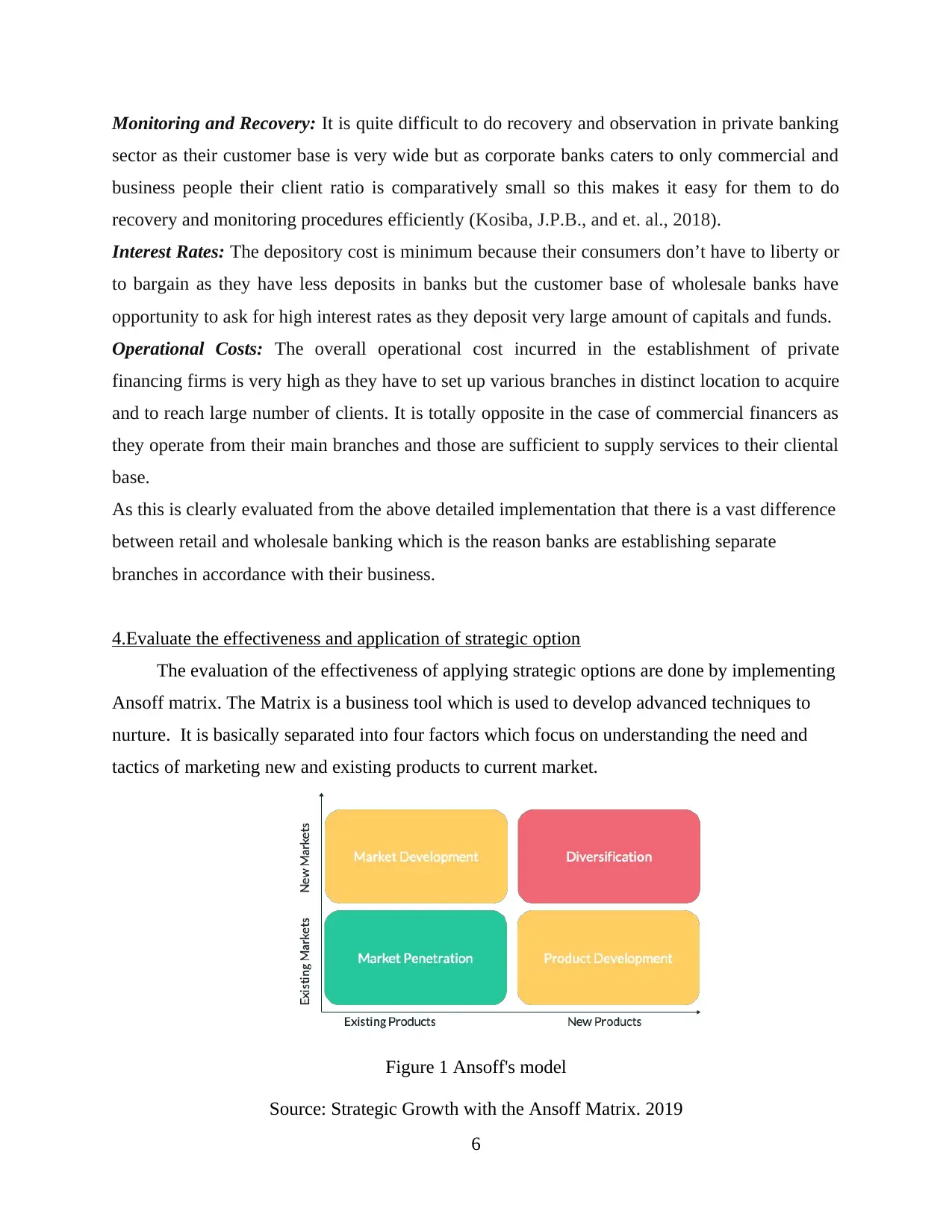

4.Evaluate the effectiveness and application of strategic option

The evaluation of the effectiveness of applying strategic options are done by implementing

Ansoff matrix. The Matrix is a business tool which is used to develop advanced techniques to

nurture. It is basically separated into four factors which focus on understanding the need and

tactics of marketing new and existing products to current market.

Figure 1 Ansoff's model

Source: Strategic Growth with the Ansoff Matrix. 2019

6

sector as their customer base is very wide but as corporate banks caters to only commercial and

business people their client ratio is comparatively small so this makes it easy for them to do

recovery and monitoring procedures efficiently (Kosiba, J.P.B., and et. al., 2018).

Interest Rates: The depository cost is minimum because their consumers don’t have to liberty or

to bargain as they have less deposits in banks but the customer base of wholesale banks have

opportunity to ask for high interest rates as they deposit very large amount of capitals and funds.

Operational Costs: The overall operational cost incurred in the establishment of private

financing firms is very high as they have to set up various branches in distinct location to acquire

and to reach large number of clients. It is totally opposite in the case of commercial financers as

they operate from their main branches and those are sufficient to supply services to their cliental

base.

As this is clearly evaluated from the above detailed implementation that there is a vast difference

between retail and wholesale banking which is the reason banks are establishing separate

branches in accordance with their business.

4.Evaluate the effectiveness and application of strategic option

The evaluation of the effectiveness of applying strategic options are done by implementing

Ansoff matrix. The Matrix is a business tool which is used to develop advanced techniques to

nurture. It is basically separated into four factors which focus on understanding the need and

tactics of marketing new and existing products to current market.

Figure 1 Ansoff's model

Source: Strategic Growth with the Ansoff Matrix. 2019

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Market Penetration: This strategy is proved to be less risky for financial sector. The products

offered by this industry are ranging from mutual funds, investments, insurance, sip and

retirement plans etc. It is identified that the customers are ignorant about the variety of products

and services this institution is offering (Le, 2017). It is beneficial for the enterprise to get in

contact with their existing customer base and identify if there is anything which company can

offer them for good and also turn out to be beneficial for the clients. Penetrating in the market

basically involves meeting with their already retained potential customers and collect feedback

from them, on the basis of their queries company can also suggest them new offerings or services

which will be helpful. One of the basic approaches in banking is to upsurge shareholders on the

other hand the available products were presented to potential and present clienteles for buyers’

market and for collective customer share. Current markets are also known as domestic markets.

It is a comparatively near to the ground risk approach as the demographic and psychographic

features of consumers are well understood by the financial personals (Ojha, Patel and Sridharan,

2020).

Market Development: This is comparatively dicier policy than developing a new product.

Marketers finds it more difficult to launch existing product to new customer than developing new

products and services for current market. This is a skilful progress plan, that effectively

established on market segment. This corporation have two choices in terms of market

development which are, establishing or opening new offices in different locations or cities, or

they can target a particular age group of people most probably the youngsters. Enterprises need

to target young generation because they are technologically advanced and are more adaptable to

change. They also want services which are time efficient and equipped with latest modifications

(Pousttchi and Dehnert, 2018). This will helpful for the organisations because if they succeed in

convincing the youth, they automatically influence their parents and elders into it.

Product Development: This particular strategy objective is to offer new products to possessed

market sectors. It is proved to be good when the clients kept a long-term relation with banks, it

will be beneficial for both the financial personals and the customers to understand the changing

needs at different stages and fulfilling those wants as per their demands. This tactic has medium

risk because the main focus is on current marketplace. They can also make some changes and

modify their current product to compete in the competitive market and also meet the needs of

7

offered by this industry are ranging from mutual funds, investments, insurance, sip and

retirement plans etc. It is identified that the customers are ignorant about the variety of products

and services this institution is offering (Le, 2017). It is beneficial for the enterprise to get in

contact with their existing customer base and identify if there is anything which company can

offer them for good and also turn out to be beneficial for the clients. Penetrating in the market

basically involves meeting with their already retained potential customers and collect feedback

from them, on the basis of their queries company can also suggest them new offerings or services

which will be helpful. One of the basic approaches in banking is to upsurge shareholders on the

other hand the available products were presented to potential and present clienteles for buyers’

market and for collective customer share. Current markets are also known as domestic markets.

It is a comparatively near to the ground risk approach as the demographic and psychographic

features of consumers are well understood by the financial personals (Ojha, Patel and Sridharan,

2020).

Market Development: This is comparatively dicier policy than developing a new product.

Marketers finds it more difficult to launch existing product to new customer than developing new

products and services for current market. This is a skilful progress plan, that effectively

established on market segment. This corporation have two choices in terms of market

development which are, establishing or opening new offices in different locations or cities, or

they can target a particular age group of people most probably the youngsters. Enterprises need

to target young generation because they are technologically advanced and are more adaptable to

change. They also want services which are time efficient and equipped with latest modifications

(Pousttchi and Dehnert, 2018). This will helpful for the organisations because if they succeed in

convincing the youth, they automatically influence their parents and elders into it.

Product Development: This particular strategy objective is to offer new products to possessed

market sectors. It is proved to be good when the clients kept a long-term relation with banks, it

will be beneficial for both the financial personals and the customers to understand the changing

needs at different stages and fulfilling those wants as per their demands. This tactic has medium

risk because the main focus is on current marketplace. They can also make some changes and

modify their current product to compete in the competitive market and also meet the needs of

7

their consumers (Rushchyshyn, Nikonenko and Kostak, 2017). Deloitte introduced a latest

benefit for their clients which include paid consultation services and also offer house finances

etc.

Diversification: This strategy is considered the riskiest, because diversification refers to offering

new latest services and products in the fresh and completely new market. This will consist a high

percentage of risk that weather or not that product will be welcomed or does it fulfil the need of

the consumers. It is clearly dangerous than the market development process. One of the positive

sides of this approach is that companies have an opportunity to acquire new customers those who

are not familiar with their firm so the marketers can attract them by acknowledge them with all

the benefits, facilities and products provided (Sapir, Schoenmaker and Véron, 2017). For

example, if some person wanted to take housing or car loan and approach their office to get

information, so it will be an advantage for the officials to provide them good customer service

and while in the process can also offer them or advise them the other financial products offered

by the company as well.

CONCLUSION

The above report examines the strategic planning procedures implementation on the banking

sector industry, it is understood by the report that the financial performance is the base of any

organisations success and this gave a different level of meaning to the role of strategic planning

in the business. It has also identified the challenges which Deloitte have faced while establishing

as a banking firm. Further it analysed the various difference between the private banking and

wholesale banking industries. Lastly the research evaluated the strategic option through Ansoff’s

model and also explains its effectiveness and applications.

8

benefit for their clients which include paid consultation services and also offer house finances

etc.

Diversification: This strategy is considered the riskiest, because diversification refers to offering

new latest services and products in the fresh and completely new market. This will consist a high

percentage of risk that weather or not that product will be welcomed or does it fulfil the need of

the consumers. It is clearly dangerous than the market development process. One of the positive

sides of this approach is that companies have an opportunity to acquire new customers those who

are not familiar with their firm so the marketers can attract them by acknowledge them with all

the benefits, facilities and products provided (Sapir, Schoenmaker and Véron, 2017). For

example, if some person wanted to take housing or car loan and approach their office to get

information, so it will be an advantage for the officials to provide them good customer service

and while in the process can also offer them or advise them the other financial products offered

by the company as well.

CONCLUSION

The above report examines the strategic planning procedures implementation on the banking

sector industry, it is understood by the report that the financial performance is the base of any

organisations success and this gave a different level of meaning to the role of strategic planning

in the business. It has also identified the challenges which Deloitte have faced while establishing

as a banking firm. Further it analysed the various difference between the private banking and

wholesale banking industries. Lastly the research evaluated the strategic option through Ansoff’s

model and also explains its effectiveness and applications.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Alstadheim, R., 2020. Banks’ wholesale funding share as an indicator of financial vulnerability.

Bryson, J.M., Edwards, L.H. and Van Slyke, D.M., 2018. Getting strategic about strategic

planning research.

Fernandes, T. and Pinto, T., 2019. Relationship quality determinants and outcomes in retail

banking services: The role of customer experience. Journal of Retailing and

Consumer Services. 50. pp.30-41.

Gertler, M., Kiyotaki, N. and Prestipino, A., 2016. Wholesale banking and bank runs in

macroeconomic modeling of financial crises. In Handbook of

Macroeconomics (Vol. 2. pp. 1345-1425). Elsevier.

Gomera, S., Chinyamurindi, W.T. and Mishi, S., 2018. Relationship between strategic planning

and financial performance: The case of small, micro-and medium-scale businesses

in the Buffalo City Metropolitan. South African Journal of Economic and

Management Sciences. 21(1). pp.1-9.

Kosiba, J.P.B., and et. al., 2018. Examining customer engagement and brand loyalty in retail

banking. International Journal of Retail & Distribution Management.

Le, T., 2017. Developing Service Quality Measurement Approach for Wholesale Banking

Operation Unit of a Bank.

Melecky, M. and Podpiera, A.M., 2018. Financial sector strategies and financial sector outcomes:

do the strategies perform?. The World Bank.

Ojha, D., Patel, P.C. and Sridharan, S.V., 2020. Dynamic strategic planning and firm competitive

performance: A conceptualization and an empirical test. International Journal of

Production Economics. 222. p.107509.

Okpebholo, E. and Sheikh, A.Z., 2020. Optimization of non-monetary reward provisions:

Evidence from the UK banking sector. IBA Business Review. 15(1).

Pousttchi, K. and Dehnert, M., 2018. Exploring the digitalization impact on consumer decision-

making in retail banking. Electronic Markets. 28(3). pp.265-286.

Rushchyshyn, N., Nikonenko, U. and Kostak, Z., 2017. Formation of financial security of the

enterprise based on strategic planning. Baltic Journal of Economic Studies. 3(4).

Sapir, A., Schoenmaker, D. and Véron, N., 2017. Making the best of Brexit for the EU27.

financial system.

Steiner, G.A., 2010. Strategic planning. Simon and Schuster.

Visco, I., 2018. Banks and finance after the crisis: Lessons and challenges. PSL Quarterly

Review. 71(286).

9

Books and journals

Alstadheim, R., 2020. Banks’ wholesale funding share as an indicator of financial vulnerability.

Bryson, J.M., Edwards, L.H. and Van Slyke, D.M., 2018. Getting strategic about strategic

planning research.

Fernandes, T. and Pinto, T., 2019. Relationship quality determinants and outcomes in retail

banking services: The role of customer experience. Journal of Retailing and

Consumer Services. 50. pp.30-41.

Gertler, M., Kiyotaki, N. and Prestipino, A., 2016. Wholesale banking and bank runs in

macroeconomic modeling of financial crises. In Handbook of

Macroeconomics (Vol. 2. pp. 1345-1425). Elsevier.

Gomera, S., Chinyamurindi, W.T. and Mishi, S., 2018. Relationship between strategic planning

and financial performance: The case of small, micro-and medium-scale businesses

in the Buffalo City Metropolitan. South African Journal of Economic and

Management Sciences. 21(1). pp.1-9.

Kosiba, J.P.B., and et. al., 2018. Examining customer engagement and brand loyalty in retail

banking. International Journal of Retail & Distribution Management.

Le, T., 2017. Developing Service Quality Measurement Approach for Wholesale Banking

Operation Unit of a Bank.

Melecky, M. and Podpiera, A.M., 2018. Financial sector strategies and financial sector outcomes:

do the strategies perform?. The World Bank.

Ojha, D., Patel, P.C. and Sridharan, S.V., 2020. Dynamic strategic planning and firm competitive

performance: A conceptualization and an empirical test. International Journal of

Production Economics. 222. p.107509.

Okpebholo, E. and Sheikh, A.Z., 2020. Optimization of non-monetary reward provisions:

Evidence from the UK banking sector. IBA Business Review. 15(1).

Pousttchi, K. and Dehnert, M., 2018. Exploring the digitalization impact on consumer decision-

making in retail banking. Electronic Markets. 28(3). pp.265-286.

Rushchyshyn, N., Nikonenko, U. and Kostak, Z., 2017. Formation of financial security of the

enterprise based on strategic planning. Baltic Journal of Economic Studies. 3(4).

Sapir, A., Schoenmaker, D. and Véron, N., 2017. Making the best of Brexit for the EU27.

financial system.

Steiner, G.A., 2010. Strategic planning. Simon and Schuster.

Visco, I., 2018. Banks and finance after the crisis: Lessons and challenges. PSL Quarterly

Review. 71(286).

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Online

Strategic Growth with the Ansoff Matrix, 2019 [Online]. Available through:

< https://www.tractionwise.com/en/magazine/ansoff-matrix-growth/ >

10

Strategic Growth with the Ansoff Matrix, 2019 [Online]. Available through:

< https://www.tractionwise.com/en/magazine/ansoff-matrix-growth/ >

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.