Business Taxation Assignment: UK Tax Laws and Financial Analysis

VerifiedAdded on 2022/12/28

|12

|3730

|36

Homework Assignment

AI Summary

This Business Taxation assignment provides a comprehensive analysis of various aspects of UK tax law. The assignment begins with the computation of trading profit, considering allowable deductions and capital allowances. It then delves into the criteria used to distinguish between employment and self-employment, including the implications of IR35. The assignment also explores the 'badges of trade' used to determine whether an activity constitutes a business, and different VAT schemes available to VAT-registered businesses. Furthermore, it analyzes inheritance tax and capital gains tax liabilities in specific scenarios. The solution covers financial statement analysis, tax regulations, and practical applications of tax principles, providing a detailed overview of the subject matter.

BUSINESS TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION- 1.................................................................................................................................3

a) Computation of the trading profit before the deduction of the capital allowances..................3

QUESTION- 2.................................................................................................................................4

a) Criteria used for distinguishing employment from the self employment................................4

b) Why do people prefer self-employment rather than being employed, resulting in so many IR

35 cases?......................................................................................................................................6

QUESTION 3...................................................................................................................................6

a) Six Badges of trade .................................................................................................................7

b) Different VAT schemes available for VAT registered business ............................................8

QUESTION 4...................................................................................................................................9

a) Inheritance tax payable as the result of death of Peter ...........................................................9

b) Capital gain tax liability of John for the tax year 2020 /21...................................................10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

QUESTION- 1.................................................................................................................................3

a) Computation of the trading profit before the deduction of the capital allowances..................3

QUESTION- 2.................................................................................................................................4

a) Criteria used for distinguishing employment from the self employment................................4

b) Why do people prefer self-employment rather than being employed, resulting in so many IR

35 cases?......................................................................................................................................6

QUESTION 3...................................................................................................................................6

a) Six Badges of trade .................................................................................................................7

b) Different VAT schemes available for VAT registered business ............................................8

QUESTION 4...................................................................................................................................9

a) Inheritance tax payable as the result of death of Peter ...........................................................9

b) Capital gain tax liability of John for the tax year 2020 /21...................................................10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

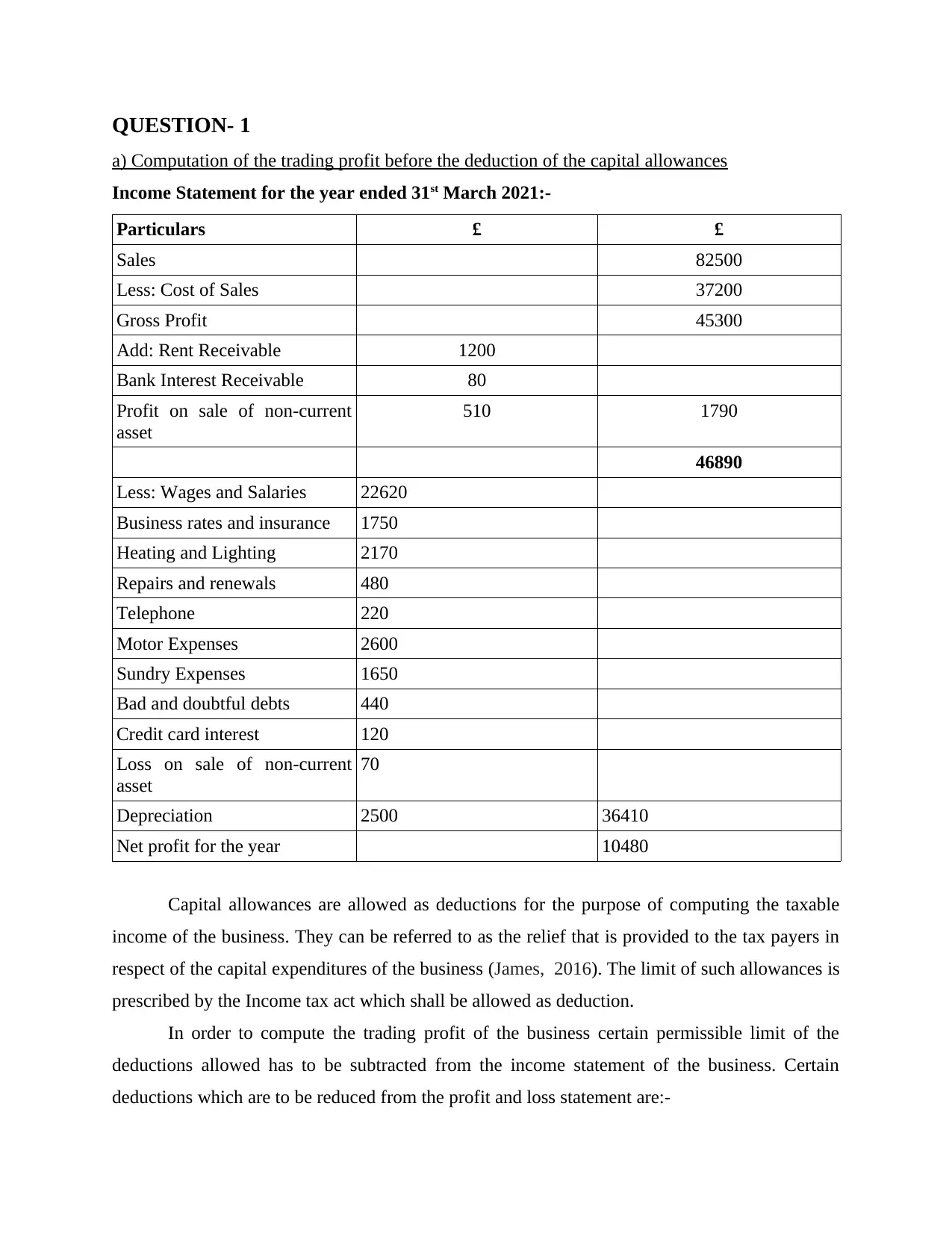

QUESTION- 1

a) Computation of the trading profit before the deduction of the capital allowances

Income Statement for the year ended 31st March 2021:-

Particulars £ £

Sales 82500

Less: Cost of Sales 37200

Gross Profit 45300

Add: Rent Receivable 1200

Bank Interest Receivable 80

Profit on sale of non-current

asset

510 1790

46890

Less: Wages and Salaries 22620

Business rates and insurance 1750

Heating and Lighting 2170

Repairs and renewals 480

Telephone 220

Motor Expenses 2600

Sundry Expenses 1650

Bad and doubtful debts 440

Credit card interest 120

Loss on sale of non-current

asset

70

Depreciation 2500 36410

Net profit for the year 10480

Capital allowances are allowed as deductions for the purpose of computing the taxable

income of the business. They can be referred to as the relief that is provided to the tax payers in

respect of the capital expenditures of the business (James, 2016). The limit of such allowances is

prescribed by the Income tax act which shall be allowed as deduction.

In order to compute the trading profit of the business certain permissible limit of the

deductions allowed has to be subtracted from the income statement of the business. Certain

deductions which are to be reduced from the profit and loss statement are:-

a) Computation of the trading profit before the deduction of the capital allowances

Income Statement for the year ended 31st March 2021:-

Particulars £ £

Sales 82500

Less: Cost of Sales 37200

Gross Profit 45300

Add: Rent Receivable 1200

Bank Interest Receivable 80

Profit on sale of non-current

asset

510 1790

46890

Less: Wages and Salaries 22620

Business rates and insurance 1750

Heating and Lighting 2170

Repairs and renewals 480

Telephone 220

Motor Expenses 2600

Sundry Expenses 1650

Bad and doubtful debts 440

Credit card interest 120

Loss on sale of non-current

asset

70

Depreciation 2500 36410

Net profit for the year 10480

Capital allowances are allowed as deductions for the purpose of computing the taxable

income of the business. They can be referred to as the relief that is provided to the tax payers in

respect of the capital expenditures of the business (James, 2016). The limit of such allowances is

prescribed by the Income tax act which shall be allowed as deduction.

In order to compute the trading profit of the business certain permissible limit of the

deductions allowed has to be subtracted from the income statement of the business. Certain

deductions which are to be reduced from the profit and loss statement are:-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a) The amount that is drawn as salary by Linda from the business is being made part of the

salaries and wages in the income statement. The salary is £200 per week which can be

£10400 approximately for the year. This does not form part of the capital allowance in

reference to tax regime so it shall remain debited in the income statement.

b) The installation of the improved heating system is a capital expenditure of the business which

has been allowed as the deduction for the purpose of computing the tax liability. This

amount shall be deducted from the statement of profit and loss to come to the trading

profit (Boadway and Tremblay, 2016). Whereas the remaining two elements shall remain

in the income statement.

c) HMRC which is the tax authority of UK has decided that one quarter of the telephone costs

and one fifth of the motor expenses are made by the business for the private use. So these

expenses cannot be considered as the business expenses for the computation of the

taxable income and neither can be made part of the trading profit of the company. And so

they are to be removed from the trading profit.

d) The sundry expenses of the business include the business entertaining expense which are

carried on by the company for entertaining their employees. The capital allowance for

such expenses is allowed up-to 50% which is £520*50%= £260. So half of the expense

shall remain in the income statement and the remaining shall be removed to ascertain the

trading profit of the business (Isabelle, 2016).

e) The provision that is set aside for the bad and doubtful debts shall not form part of the trading

profit and so the effect has to be removed from the income statement of the company.

The trade debts written off shall be included in the income statement and so no changes

are to be made in its respect.

QUESTION- 2

a) Criteria used for distinguishing employment from the self employment

Self employed- A self-employed person is one who does not work for a specific employer paying

a specific amount of salary or wages. They work for themselves and establishes a direct contact

with the clients. They are highly skilled in the work they perform like freelancers, traders,

investors, agents and the lawyers. They enjoy a degree of power but simultaneously are subject

salaries and wages in the income statement. The salary is £200 per week which can be

£10400 approximately for the year. This does not form part of the capital allowance in

reference to tax regime so it shall remain debited in the income statement.

b) The installation of the improved heating system is a capital expenditure of the business which

has been allowed as the deduction for the purpose of computing the tax liability. This

amount shall be deducted from the statement of profit and loss to come to the trading

profit (Boadway and Tremblay, 2016). Whereas the remaining two elements shall remain

in the income statement.

c) HMRC which is the tax authority of UK has decided that one quarter of the telephone costs

and one fifth of the motor expenses are made by the business for the private use. So these

expenses cannot be considered as the business expenses for the computation of the

taxable income and neither can be made part of the trading profit of the company. And so

they are to be removed from the trading profit.

d) The sundry expenses of the business include the business entertaining expense which are

carried on by the company for entertaining their employees. The capital allowance for

such expenses is allowed up-to 50% which is £520*50%= £260. So half of the expense

shall remain in the income statement and the remaining shall be removed to ascertain the

trading profit of the business (Isabelle, 2016).

e) The provision that is set aside for the bad and doubtful debts shall not form part of the trading

profit and so the effect has to be removed from the income statement of the company.

The trade debts written off shall be included in the income statement and so no changes

are to be made in its respect.

QUESTION- 2

a) Criteria used for distinguishing employment from the self employment

Self employed- A self-employed person is one who does not work for a specific employer paying

a specific amount of salary or wages. They work for themselves and establishes a direct contact

with the clients. They are highly skilled in the work they perform like freelancers, traders,

investors, agents and the lawyers. They enjoy a degree of power but simultaneously are subject

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to higher volatility and employment risk. One who earns livelihood based on an independent

economic activity are to be self-employed.

As per the tax authorities a self-employed person should file the tax returns annually and

shall be paying estimated quarterly tax. Up-to £12500 it is exempt, from £12501 to £50000 a tax

liability of 20% shall be imposed. Above £50000 till £150000 40% tax liability shall be charged

on the profits (Biddle, Fels and Sinning, 2018). Over the amount £150000 an additional rate of

45% shall be paid by the self-employed tax payers on the amount of profits that are generated in

the year.

Employed- An employee can be defined as a person who is hired under some contract or

agreement for doing specific activities and entitled to receive commission against it. An

employee who is hired in UK shall be registered under the PAYE (pay as you earn) scheme.

They shall also fall in the same tax bracket except the National Insurance of 13.8% that the

employer shall be paying for the employee. The major difference is that in case of being

employed the tax is charged on the earnings whereas in the case of self employment it is charged

on the profits.

In order to decide on the employment status of an individual that whether they are self-

employed or are employed is determined by the various agreed criteria(Maffini, Xing and

Devereux, 2019). Apart from that it also shows that an individual can be both employee and self-

employed at different point of time. The considerations for deciding the same are as follows:-

The tax authorities determine the employment status of an individual by tests which are

different from the lawful check that is undertaken. They use the CEST tool which is

“Check employment status for Tax”.

Certain important factors that are determined are the ability to substitute, lack of

mutuality of obligation and the employee's obligation to perform the work and be paid for

it.

The application of the IR 35 rules is also one such factor which helps in the assessment of

the employment status of an individual.

Those who fall under the status of being employed shall pay via PAYE scheme whereas

those who are falling under the category of being self-employed shall be paying via self

assessment regime.

economic activity are to be self-employed.

As per the tax authorities a self-employed person should file the tax returns annually and

shall be paying estimated quarterly tax. Up-to £12500 it is exempt, from £12501 to £50000 a tax

liability of 20% shall be imposed. Above £50000 till £150000 40% tax liability shall be charged

on the profits (Biddle, Fels and Sinning, 2018). Over the amount £150000 an additional rate of

45% shall be paid by the self-employed tax payers on the amount of profits that are generated in

the year.

Employed- An employee can be defined as a person who is hired under some contract or

agreement for doing specific activities and entitled to receive commission against it. An

employee who is hired in UK shall be registered under the PAYE (pay as you earn) scheme.

They shall also fall in the same tax bracket except the National Insurance of 13.8% that the

employer shall be paying for the employee. The major difference is that in case of being

employed the tax is charged on the earnings whereas in the case of self employment it is charged

on the profits.

In order to decide on the employment status of an individual that whether they are self-

employed or are employed is determined by the various agreed criteria(Maffini, Xing and

Devereux, 2019). Apart from that it also shows that an individual can be both employee and self-

employed at different point of time. The considerations for deciding the same are as follows:-

The tax authorities determine the employment status of an individual by tests which are

different from the lawful check that is undertaken. They use the CEST tool which is

“Check employment status for Tax”.

Certain important factors that are determined are the ability to substitute, lack of

mutuality of obligation and the employee's obligation to perform the work and be paid for

it.

The application of the IR 35 rules is also one such factor which helps in the assessment of

the employment status of an individual.

Those who fall under the status of being employed shall pay via PAYE scheme whereas

those who are falling under the category of being self-employed shall be paying via self

assessment regime.

The sufficient control of the party for the whom the work is to be done and the

consistency of the other provisions of the contract are the factors that are used for

evaluation of the status of an individual.

b) Why do people prefer self-employment rather than being employed, resulting in so many IR

35 cases?

Self employment was preferred over the employed status as that helped them to avoid tax

liability to an extent. The small companies and their owners in order to limit their tax liability

and their contributions in the national insurance made intermediaries or the personal service

companies. Such self-employed people used to form a small company acting as an intermediary

which was shared with a family member that is falling under the lower tax bracket. Apart from

the tax they also limited their contributions towards the national insurance (Bilicka, 2019). The

employees working under such format were disguised and so came under the IR 35 rules.

Now the IR 35 rules are being changed such that the employees which are found to be

disguised shall also be liable to the equivalent tax liability and the contribution towards the

national insurance. The percentages shall be exactly mirroring the normal employee and the

company that is paying fees for it.

Some crucial sectors that HMRC feels are more subject to the non- compliance of the tax

policies are being investigated regarding the same. Since earlier the assessment regarding

whether a particular intermediary falls under the IR 35 rules was assessed by the self-employed,

now has been shifted to the public authorities and the decision remains with them.

This was the major reason for the self employment being preferred more rather than

being employed under someone. Also, the increase in the IR 35 cases is a part of this mentality

of the self-employed people. The major advantage that was imposed while being self-employed

was that they could avoid their tax and their contributions in the insurance (Morgan, 2016).

Apart from this there are certain general benefits of the individual who are falling in the

self-employed status of employment. Some of them could be that they do not have to make

contributions in the class 1 of national insurance, tax need to be paid under the self assessment

regime and the individual may need to register for the VAT depending upon the turnover.

consistency of the other provisions of the contract are the factors that are used for

evaluation of the status of an individual.

b) Why do people prefer self-employment rather than being employed, resulting in so many IR

35 cases?

Self employment was preferred over the employed status as that helped them to avoid tax

liability to an extent. The small companies and their owners in order to limit their tax liability

and their contributions in the national insurance made intermediaries or the personal service

companies. Such self-employed people used to form a small company acting as an intermediary

which was shared with a family member that is falling under the lower tax bracket. Apart from

the tax they also limited their contributions towards the national insurance (Bilicka, 2019). The

employees working under such format were disguised and so came under the IR 35 rules.

Now the IR 35 rules are being changed such that the employees which are found to be

disguised shall also be liable to the equivalent tax liability and the contribution towards the

national insurance. The percentages shall be exactly mirroring the normal employee and the

company that is paying fees for it.

Some crucial sectors that HMRC feels are more subject to the non- compliance of the tax

policies are being investigated regarding the same. Since earlier the assessment regarding

whether a particular intermediary falls under the IR 35 rules was assessed by the self-employed,

now has been shifted to the public authorities and the decision remains with them.

This was the major reason for the self employment being preferred more rather than

being employed under someone. Also, the increase in the IR 35 cases is a part of this mentality

of the self-employed people. The major advantage that was imposed while being self-employed

was that they could avoid their tax and their contributions in the insurance (Morgan, 2016).

Apart from this there are certain general benefits of the individual who are falling in the

self-employed status of employment. Some of them could be that they do not have to make

contributions in the class 1 of national insurance, tax need to be paid under the self assessment

regime and the individual may need to register for the VAT depending upon the turnover.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 3

a) Six Badges of trade

Badges of the trade test are not conclusive and used by the HMRC for helping them to

determine whether activity is proper business or economic activity or is merely money making

line to hobby. There is careful consideration required to assess where hobby has become taxable

activity. It is clear from significant amount of the case laws on the subject that decision about

whether activity is business activity or not is not clear often. Finding of the trade could be

significant. Attributable profits will be considered as income instead of falling within capital gain

regime (Ooi, 2019). The individuals may have exposure to higher tax rate. The badges for

considering business activity are:

Profit Seeking Motive

The badge provides that an activity for constituting as trade, has to be carried out with

view of making profit. It is chink in armour exploited by the HMRC in war against the film

schemes and the other leverage loss schemes. It is platform from where HMRC could challenge

loss making ventures that appears as merely hobby to HMRC.

Number of Transactions

Though single transaction may also constitute as trade but generally where the

transactions are very few, than it is indicative of the non trading activity. In case of Pickford vs

Quirke [1927] 13 TC 250. Taxpayer here bought mill with intention of using it in trade. Mill fell

apart at seams and decided for stripping everything which was useful and then sold it bit by bit.

Profits were taxed because there were number of transactions of same nature.

Nature of Assets

It is related to nature of asset under consideration. Nature refers to factors like quantity and type

of the asset. For example buying guitar will be considered as investment activity instead of

trading activity as it is acquired for the personal enjoyment (Litchfield, Lowry and Dorrian,

2018). It can be further cleared through Rutledge vs CIR [1929] 14 TC 490.

Existence of the similar trading transaction or interests

When transaction entered by the person is similar to existing trade then it will point towards the

trading. For instance tax adviser selling car, in absence of the other badges will not be considered

as the trading transaction. But if taxpayer running garage sells car it is linked to existing trade

and likely to be considered as trading transactions.

a) Six Badges of trade

Badges of the trade test are not conclusive and used by the HMRC for helping them to

determine whether activity is proper business or economic activity or is merely money making

line to hobby. There is careful consideration required to assess where hobby has become taxable

activity. It is clear from significant amount of the case laws on the subject that decision about

whether activity is business activity or not is not clear often. Finding of the trade could be

significant. Attributable profits will be considered as income instead of falling within capital gain

regime (Ooi, 2019). The individuals may have exposure to higher tax rate. The badges for

considering business activity are:

Profit Seeking Motive

The badge provides that an activity for constituting as trade, has to be carried out with

view of making profit. It is chink in armour exploited by the HMRC in war against the film

schemes and the other leverage loss schemes. It is platform from where HMRC could challenge

loss making ventures that appears as merely hobby to HMRC.

Number of Transactions

Though single transaction may also constitute as trade but generally where the

transactions are very few, than it is indicative of the non trading activity. In case of Pickford vs

Quirke [1927] 13 TC 250. Taxpayer here bought mill with intention of using it in trade. Mill fell

apart at seams and decided for stripping everything which was useful and then sold it bit by bit.

Profits were taxed because there were number of transactions of same nature.

Nature of Assets

It is related to nature of asset under consideration. Nature refers to factors like quantity and type

of the asset. For example buying guitar will be considered as investment activity instead of

trading activity as it is acquired for the personal enjoyment (Litchfield, Lowry and Dorrian,

2018). It can be further cleared through Rutledge vs CIR [1929] 14 TC 490.

Existence of the similar trading transaction or interests

When transaction entered by the person is similar to existing trade then it will point towards the

trading. For instance tax adviser selling car, in absence of the other badges will not be considered

as the trading transaction. But if taxpayer running garage sells car it is linked to existing trade

and likely to be considered as trading transactions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Changes to asset

It is indicative of the trade, where person buys the asset and later modifies in manner

where it become more valuable. More person does for modifying the asset, more chances are

there that it will be considered as trade. However if asset does not undergo change it will not

prevent from being considered as trading transaction (Bhopal and Pitkin, 2020). In case of Cape

Brandy Syndicate vs CIR [1921] 12 TC 358 where change process undertaken for brandy was

considered as trade as it was also done for reselling

Type of Finance

Where the assets are purchased over short term finances and it is considered that

repayments will be made from proceeds then it will point towards trading venture. For instance,

in contrast situation where property purchased for 20 years interest only loan versus the 1 bought

for 6 months bridge finance loan to be repaid from sale proceeds.

b) Different VAT schemes available for VAT registered business

VAT Annual Accounting Scheme

VAT registered firm submit VAT returns & payment four times year. VAT Annual

Accounting Scheme, they are required to be done for one time in a year. The scheme is eligible

for the business who are VAT registered and have annual taxable turnover of GBP 1.35 million

or less.

VAT Cash Accounting Scheme

The scheme allows to pay the VAT over sales after the customers have paid and reclaim

VAT on stock after it is paid to the supplier. Eligibility is VAT registration and turnover within

12 months of 1.35 millions or lower. Cannot be used for VAT Flat rate scheme is being used.

VAT Margin Scheme

It is used by the sellers of second hand items, antiques, art works and collector's items.

Scheme taxes difference between cost of acquisition and sale proceeds (Pearce and Pinto, 2019).

For joining the scheme detailed record of eligible goods has to be kept and then reporting them

over the VAT return.

Capital Good Scheme

Used by the businesses for claiming VAT rebates or exemptions on the assets like

property, land or equipment that are purchased with intention of the resale but is used by owner

for the other purposes.

It is indicative of the trade, where person buys the asset and later modifies in manner

where it become more valuable. More person does for modifying the asset, more chances are

there that it will be considered as trade. However if asset does not undergo change it will not

prevent from being considered as trading transaction (Bhopal and Pitkin, 2020). In case of Cape

Brandy Syndicate vs CIR [1921] 12 TC 358 where change process undertaken for brandy was

considered as trade as it was also done for reselling

Type of Finance

Where the assets are purchased over short term finances and it is considered that

repayments will be made from proceeds then it will point towards trading venture. For instance,

in contrast situation where property purchased for 20 years interest only loan versus the 1 bought

for 6 months bridge finance loan to be repaid from sale proceeds.

b) Different VAT schemes available for VAT registered business

VAT Annual Accounting Scheme

VAT registered firm submit VAT returns & payment four times year. VAT Annual

Accounting Scheme, they are required to be done for one time in a year. The scheme is eligible

for the business who are VAT registered and have annual taxable turnover of GBP 1.35 million

or less.

VAT Cash Accounting Scheme

The scheme allows to pay the VAT over sales after the customers have paid and reclaim

VAT on stock after it is paid to the supplier. Eligibility is VAT registration and turnover within

12 months of 1.35 millions or lower. Cannot be used for VAT Flat rate scheme is being used.

VAT Margin Scheme

It is used by the sellers of second hand items, antiques, art works and collector's items.

Scheme taxes difference between cost of acquisition and sale proceeds (Pearce and Pinto, 2019).

For joining the scheme detailed record of eligible goods has to be kept and then reporting them

over the VAT return.

Capital Good Scheme

Used by the businesses for claiming VAT rebates or exemptions on the assets like

property, land or equipment that are purchased with intention of the resale but is used by owner

for the other purposes.

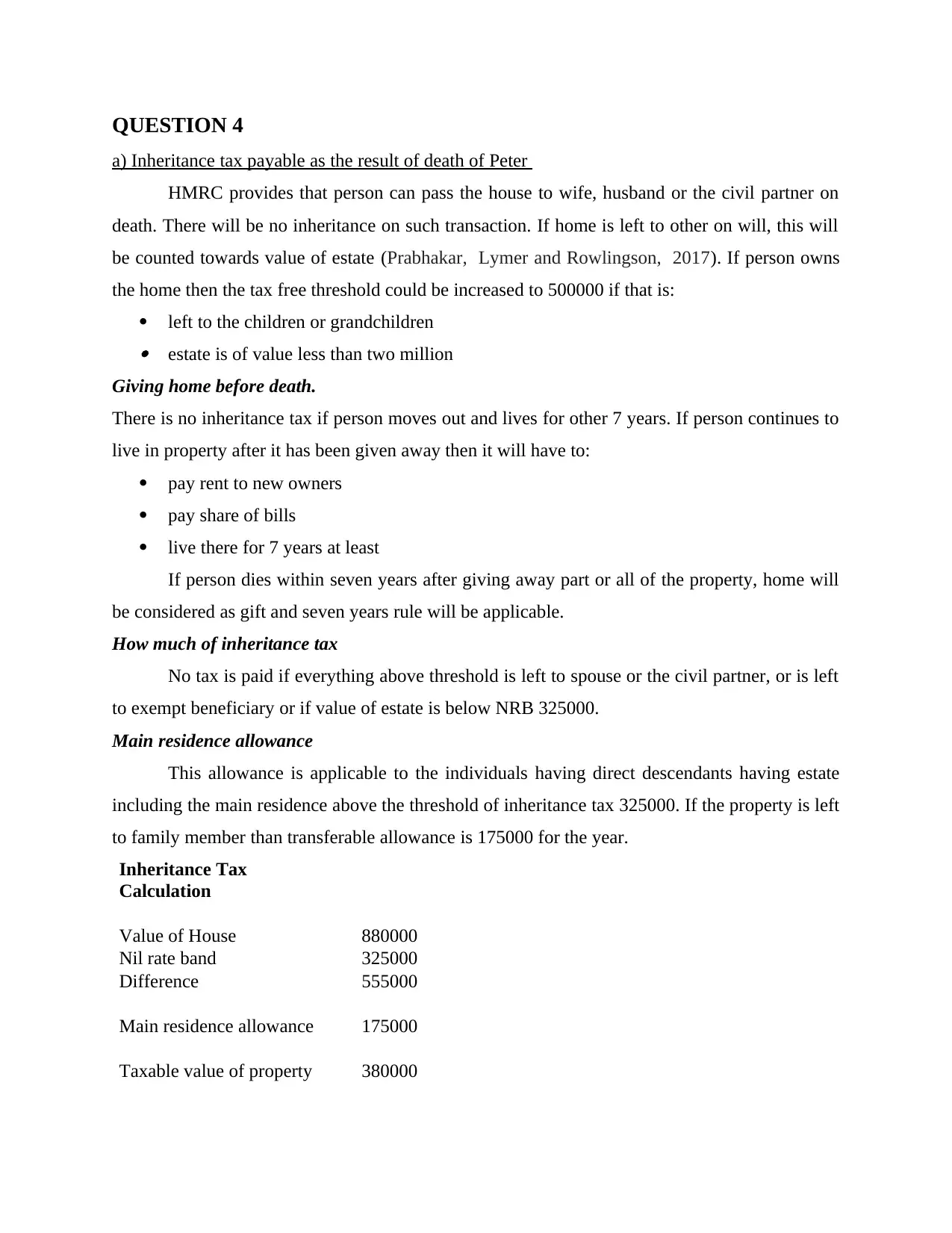

QUESTION 4

a) Inheritance tax payable as the result of death of Peter

HMRC provides that person can pass the house to wife, husband or the civil partner on

death. There will be no inheritance on such transaction. If home is left to other on will, this will

be counted towards value of estate (Prabhakar, Lymer and Rowlingson, 2017). If person owns

the home then the tax free threshold could be increased to 500000 if that is:

left to the children or grandchildren estate is of value less than two million

Giving home before death.

There is no inheritance tax if person moves out and lives for other 7 years. If person continues to

live in property after it has been given away then it will have to:

pay rent to new owners

pay share of bills

live there for 7 years at least

If person dies within seven years after giving away part or all of the property, home will

be considered as gift and seven years rule will be applicable.

How much of inheritance tax

No tax is paid if everything above threshold is left to spouse or the civil partner, or is left

to exempt beneficiary or if value of estate is below NRB 325000.

Main residence allowance

This allowance is applicable to the individuals having direct descendants having estate

including the main residence above the threshold of inheritance tax 325000. If the property is left

to family member than transferable allowance is 175000 for the year.

Inheritance Tax

Calculation

Value of House 880000

Nil rate band 325000

Difference 555000

Main residence allowance 175000

Taxable value of property 380000

a) Inheritance tax payable as the result of death of Peter

HMRC provides that person can pass the house to wife, husband or the civil partner on

death. There will be no inheritance on such transaction. If home is left to other on will, this will

be counted towards value of estate (Prabhakar, Lymer and Rowlingson, 2017). If person owns

the home then the tax free threshold could be increased to 500000 if that is:

left to the children or grandchildren estate is of value less than two million

Giving home before death.

There is no inheritance tax if person moves out and lives for other 7 years. If person continues to

live in property after it has been given away then it will have to:

pay rent to new owners

pay share of bills

live there for 7 years at least

If person dies within seven years after giving away part or all of the property, home will

be considered as gift and seven years rule will be applicable.

How much of inheritance tax

No tax is paid if everything above threshold is left to spouse or the civil partner, or is left

to exempt beneficiary or if value of estate is below NRB 325000.

Main residence allowance

This allowance is applicable to the individuals having direct descendants having estate

including the main residence above the threshold of inheritance tax 325000. If the property is left

to family member than transferable allowance is 175000 for the year.

Inheritance Tax

Calculation

Value of House 880000

Nil rate band 325000

Difference 555000

Main residence allowance 175000

Taxable value of property 380000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inheritance Tax @ 40% 152000

In the present case Peter has gifted the estate to John on wedding. The gifts made on

wedding are tax free generally. As the Peter died within six years of transferring the property it

will attract inheritance tax. The tax will be applicable on new value of property at the time it has

become taxable (Ramsey, 2019). After applying nil rate band property above threshold limit is

555000. As the property is gifted to family members they are allowed with main residence

allowance which is 175000. The inheritance tax is charged on 380000 at 40% and it has tax

liability of 152000.

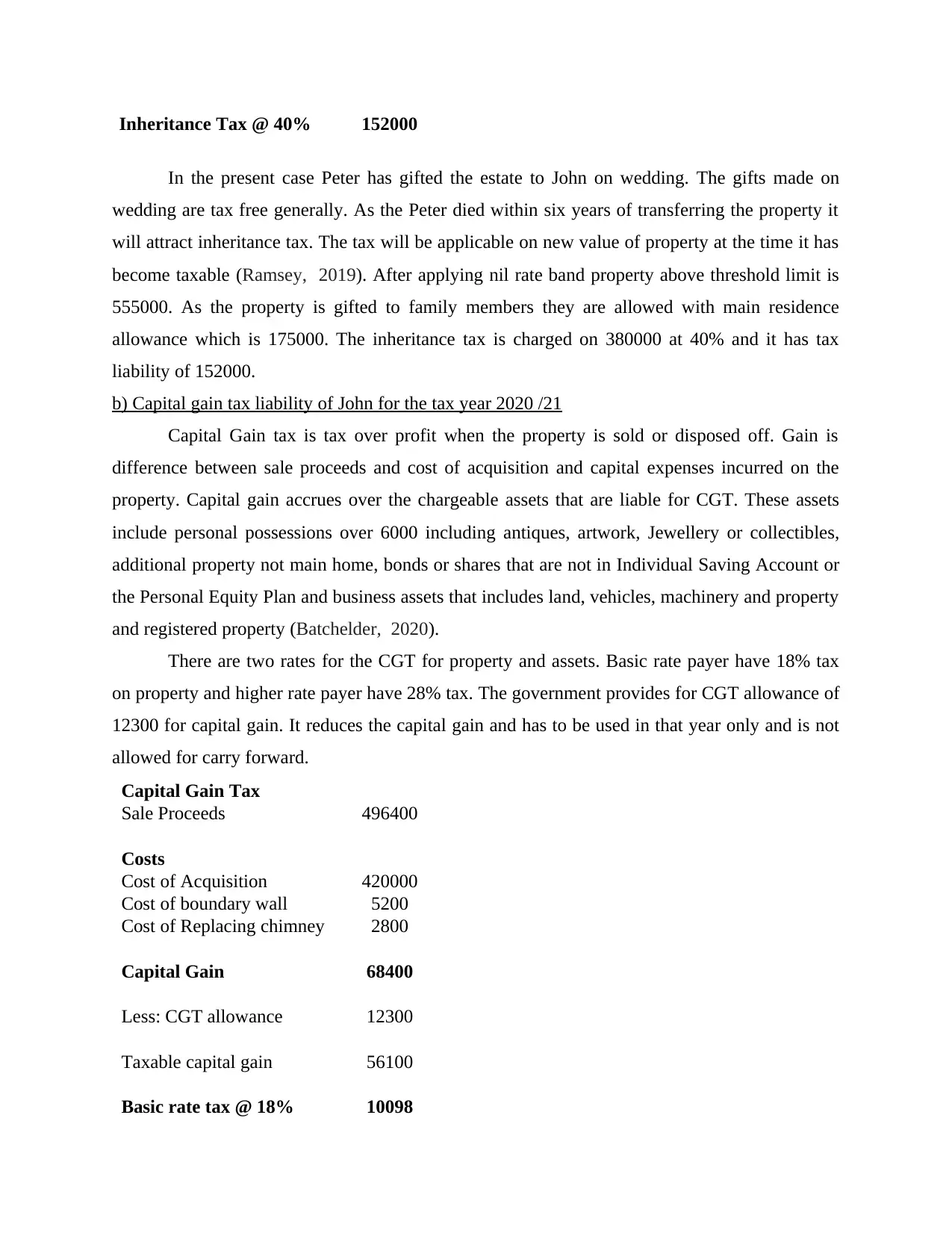

b) Capital gain tax liability of John for the tax year 2020 /21

Capital Gain tax is tax over profit when the property is sold or disposed off. Gain is

difference between sale proceeds and cost of acquisition and capital expenses incurred on the

property. Capital gain accrues over the chargeable assets that are liable for CGT. These assets

include personal possessions over 6000 including antiques, artwork, Jewellery or collectibles,

additional property not main home, bonds or shares that are not in Individual Saving Account or

the Personal Equity Plan and business assets that includes land, vehicles, machinery and property

and registered property (Batchelder, 2020).

There are two rates for the CGT for property and assets. Basic rate payer have 18% tax

on property and higher rate payer have 28% tax. The government provides for CGT allowance of

12300 for capital gain. It reduces the capital gain and has to be used in that year only and is not

allowed for carry forward.

Capital Gain Tax

Sale Proceeds 496400

Costs

Cost of Acquisition 420000

Cost of boundary wall 5200

Cost of Replacing chimney 2800

Capital Gain 68400

Less: CGT allowance 12300

Taxable capital gain 56100

Basic rate tax @ 18% 10098

In the present case Peter has gifted the estate to John on wedding. The gifts made on

wedding are tax free generally. As the Peter died within six years of transferring the property it

will attract inheritance tax. The tax will be applicable on new value of property at the time it has

become taxable (Ramsey, 2019). After applying nil rate band property above threshold limit is

555000. As the property is gifted to family members they are allowed with main residence

allowance which is 175000. The inheritance tax is charged on 380000 at 40% and it has tax

liability of 152000.

b) Capital gain tax liability of John for the tax year 2020 /21

Capital Gain tax is tax over profit when the property is sold or disposed off. Gain is

difference between sale proceeds and cost of acquisition and capital expenses incurred on the

property. Capital gain accrues over the chargeable assets that are liable for CGT. These assets

include personal possessions over 6000 including antiques, artwork, Jewellery or collectibles,

additional property not main home, bonds or shares that are not in Individual Saving Account or

the Personal Equity Plan and business assets that includes land, vehicles, machinery and property

and registered property (Batchelder, 2020).

There are two rates for the CGT for property and assets. Basic rate payer have 18% tax

on property and higher rate payer have 28% tax. The government provides for CGT allowance of

12300 for capital gain. It reduces the capital gain and has to be used in that year only and is not

allowed for carry forward.

Capital Gain Tax

Sale Proceeds 496400

Costs

Cost of Acquisition 420000

Cost of boundary wall 5200

Cost of Replacing chimney 2800

Capital Gain 68400

Less: CGT allowance 12300

Taxable capital gain 56100

Basic rate tax @ 18% 10098

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the given case John has been inherited property from father which was valued at

420000 at time of gift. For CGT purpose it will be considered as cost of property. The expenses

incurred on property are of capital nature therefore will be added to cost and will be deducted

from the sale proceeds. The total capital gain from sale of gifted property is 68400. There is

capital gain tax allowance available to everyone and it is deducted from gain reducing the gain

from 68400 to 56100. As John fall under the basic rate tax payer rate the applicable CGT rate

over property is 18%. Thus, the capital gain tax liability for the year of John is 10,098.

CONCLUSION

It could be concluded from the above report that individual has to comply with all the tax

requirements for filing the return. There are number of events and transactions that are allowed

with exemptions and other benefits. Taxpayer has to properly assess the tax requirements and

guidelines for getting the benefits and reducing the tax liability.

420000 at time of gift. For CGT purpose it will be considered as cost of property. The expenses

incurred on property are of capital nature therefore will be added to cost and will be deducted

from the sale proceeds. The total capital gain from sale of gifted property is 68400. There is

capital gain tax allowance available to everyone and it is deducted from gain reducing the gain

from 68400 to 56100. As John fall under the basic rate tax payer rate the applicable CGT rate

over property is 18%. Thus, the capital gain tax liability for the year of John is 10,098.

CONCLUSION

It could be concluded from the above report that individual has to comply with all the tax

requirements for filing the return. There are number of events and transactions that are allowed

with exemptions and other benefits. Taxpayer has to properly assess the tax requirements and

guidelines for getting the benefits and reducing the tax liability.

REFERENCES

Books and Journals

Ooi, V., 2019. Taxing ‘all other income’in Singapore and Malaysia. Oxford University

Commonwealth Law Journal. 19(2). pp.204-226.

Litchfield, C.A., Lowry, R. and Dorrian, J., 2018. Recycling 115,369 mobile phones for gorilla

conservation over a six-year period (2009-2014) at Zoos Victoria: A case study of ‘points

of influence’and mobile phone donations. PloS one. 13(12). p.e0206890.

Bhopal, K. and Pitkin, C., 2020. ‘Same old story, just a different policy’: race and policy making

in higher education in the UK. Race Ethnicity and Education. 23(4). pp.530-547.

Pearce, P. and Pinto, D., 2019. GST implications of ecommerce and goods warehousing. Tax

Specialist. 22(4). p.159.

Prabhakar, R., Lymer, A. and Rowlingson, K., 2017. Does information about wealth inequality

and inheritance tax raise public support for the wealth taxes? Evidence from a UK survey.

Ramsey, C., 2019. Inheritance Tax Considerations for Property Investors.

Batchelder, L.L., 2020. Leveling the playing field between inherited income and income from

work through an inheritance tax. Tackling the Tax Code: Efficient and Equitable Ways to

Raise Revenue. pp.48-88.

James, S. R., 2016. Accounting and Taxation: UK. Wolters Kluwer.

Boadway, R. and Tremblay, J. F., 2016. Modernizing Business Taxation. CD Howe Institute

Commentary. 452.

Isabelle, R., 2016. State aid law and business taxation. Springer.

Biddle, N., Fels, K. M. and Sinning, M., 2018. Behavioral insights on business taxation:

Evidence from two natural field experiments. Journal of Behavioral and Experimental

Finance. 18. pp.30-49.

Maffini, G., Xing, J. and Devereux, M. P., 2019. The impact of investment incentives: evidence

from UK corporation tax returns. American Economic Journal: Economic Policy. 11(3).

pp.361-89.

Bilicka, K. A., 2019. Comparing UK tax returns of foreign multinationals to matched domestic

firms. American Economic Review. 109(8). pp.2921-53.

Morgan, J., 2016. Corporation tax as a problem of MNC organisational circuits: The case for

unitary taxation. The British Journal of Politics and International Relations. 18(2).

pp.463-481.

Books and Journals

Ooi, V., 2019. Taxing ‘all other income’in Singapore and Malaysia. Oxford University

Commonwealth Law Journal. 19(2). pp.204-226.

Litchfield, C.A., Lowry, R. and Dorrian, J., 2018. Recycling 115,369 mobile phones for gorilla

conservation over a six-year period (2009-2014) at Zoos Victoria: A case study of ‘points

of influence’and mobile phone donations. PloS one. 13(12). p.e0206890.

Bhopal, K. and Pitkin, C., 2020. ‘Same old story, just a different policy’: race and policy making

in higher education in the UK. Race Ethnicity and Education. 23(4). pp.530-547.

Pearce, P. and Pinto, D., 2019. GST implications of ecommerce and goods warehousing. Tax

Specialist. 22(4). p.159.

Prabhakar, R., Lymer, A. and Rowlingson, K., 2017. Does information about wealth inequality

and inheritance tax raise public support for the wealth taxes? Evidence from a UK survey.

Ramsey, C., 2019. Inheritance Tax Considerations for Property Investors.

Batchelder, L.L., 2020. Leveling the playing field between inherited income and income from

work through an inheritance tax. Tackling the Tax Code: Efficient and Equitable Ways to

Raise Revenue. pp.48-88.

James, S. R., 2016. Accounting and Taxation: UK. Wolters Kluwer.

Boadway, R. and Tremblay, J. F., 2016. Modernizing Business Taxation. CD Howe Institute

Commentary. 452.

Isabelle, R., 2016. State aid law and business taxation. Springer.

Biddle, N., Fels, K. M. and Sinning, M., 2018. Behavioral insights on business taxation:

Evidence from two natural field experiments. Journal of Behavioral and Experimental

Finance. 18. pp.30-49.

Maffini, G., Xing, J. and Devereux, M. P., 2019. The impact of investment incentives: evidence

from UK corporation tax returns. American Economic Journal: Economic Policy. 11(3).

pp.361-89.

Bilicka, K. A., 2019. Comparing UK tax returns of foreign multinationals to matched domestic

firms. American Economic Review. 109(8). pp.2921-53.

Morgan, J., 2016. Corporation tax as a problem of MNC organisational circuits: The case for

unitary taxation. The British Journal of Politics and International Relations. 18(2).

pp.463-481.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.