Business Taxation: Comprehensive Report on Tax Regulations and Schemes

VerifiedAdded on 2022/12/29

|12

|3689

|97

Report

AI Summary

This report provides a comprehensive analysis of business taxation, covering various aspects such as the assessment of trading profits with a practical example calculating Linda's trading profits for the year, criteria for employment versus self-employment and the reasons individuals prefer self-employment, a discussion of the six badges of trade used to determine if an activity constitutes trading, an overview of different VAT schemes for VAT-registered companies, and practical calculations of inheritance tax and capital gains tax liabilities. The report delves into the nuances of tax regulations and provides insights into how businesses and individuals can navigate the complexities of the tax system, highlighting the importance of understanding and complying with taxation requirements. Desklib offers a range of study tools, including solved assignments and past papers, to support students in their academic endeavors.

Business Taxation Alternative

Assessment

Assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Linda's trading profits for the year 31st march 2121: .................................................................3

QUESTION 2...................................................................................................................................4

Criteria for the use for employment for self employment, why people prefer self employment:

......................................................................................................................................................4

Why prefer self-employment rather than being employed, resulting in so many IR 35 cases:...6

QUESTION 3...................................................................................................................................7

Discussion Six badges for trade:..................................................................................................7

Different VAT schemes for the various VAT registered companies:..........................................9

QUESTION 4.................................................................................................................................10

Inheritance tax arising when the death:.....................................................................................10

Capital gain tax liability:............................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Linda's trading profits for the year 31st march 2121: .................................................................3

QUESTION 2...................................................................................................................................4

Criteria for the use for employment for self employment, why people prefer self employment:

......................................................................................................................................................4

Why prefer self-employment rather than being employed, resulting in so many IR 35 cases:...6

QUESTION 3...................................................................................................................................7

Discussion Six badges for trade:..................................................................................................7

Different VAT schemes for the various VAT registered companies:..........................................9

QUESTION 4.................................................................................................................................10

Inheritance tax arising when the death:.....................................................................................10

Capital gain tax liability:............................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Business taxation alludes to the tax contributions that companies are obliged to incur as

part of their periodic business operational processes Whether in business there is a sole owner,

associate, limited company or corporate entity, LLP etc. each entity shall be accountable for

complying with the taxation requirements (Blakeley, 2018). The study-assessment discusses

different facets of the business taxation. The report covers aspects like practical sum

on assessment of trading profits, key 6 trade badges, multiple VAT schemes with respect to

different approved VAT enterprises etc. In addition, it consists of practical sum of inheritance tax

as well as capital gain tax requirements.

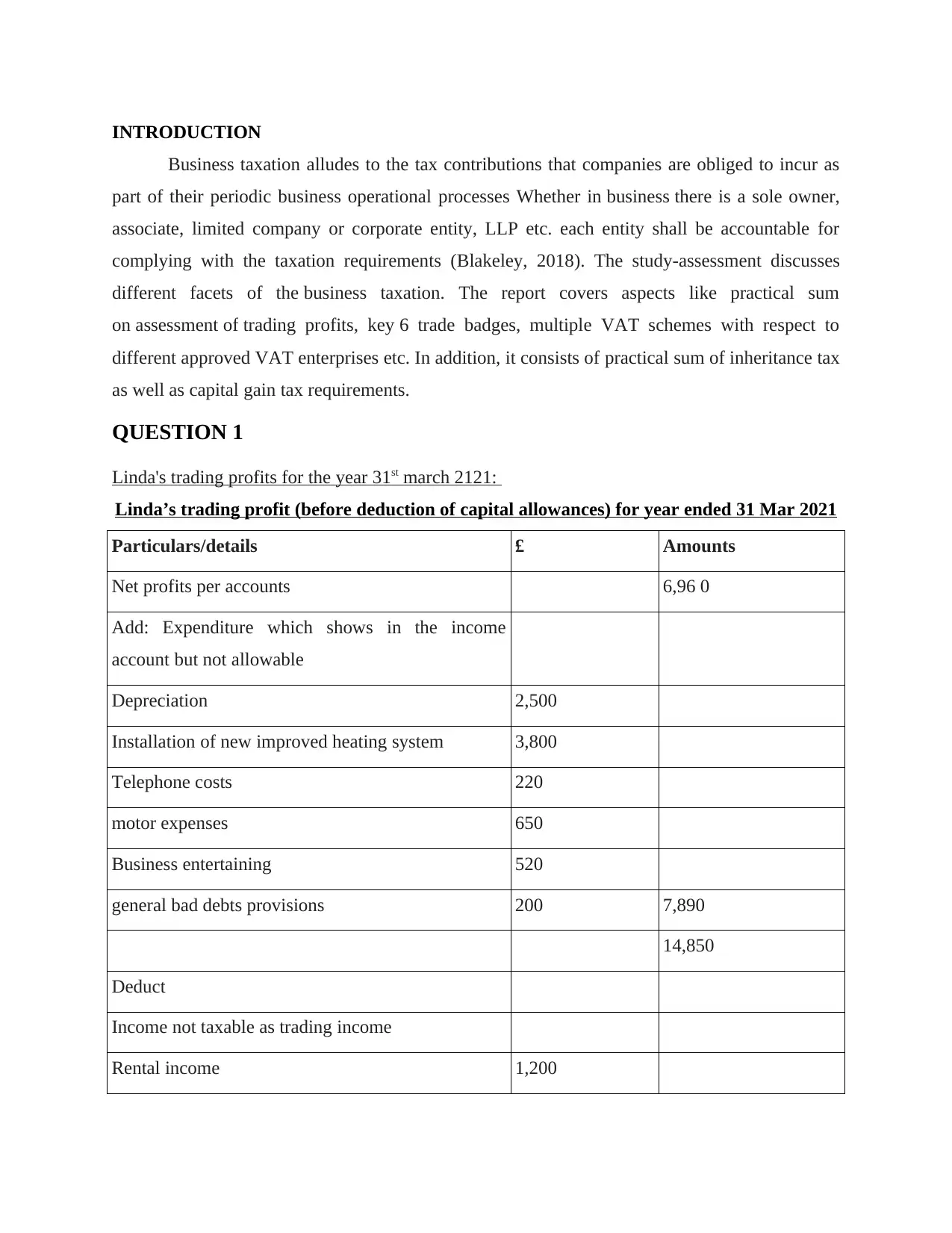

QUESTION 1

Linda's trading profits for the year 31st march 2121:

Linda’s trading profit (before deduction of capital allowances) for year ended 31 Mar 2021

Particulars/details £ Amounts

Net profits per accounts 6,96 0

Add: Expenditure which shows in the income

account but not allowable

Depreciation 2,500

Installation of new improved heating system 3,800

Telephone costs 220

motor expenses 650

Business entertaining 520

general bad debts provisions 200 7,890

14,850

Deduct

Income not taxable as trading income

Rental income 1,200

Business taxation alludes to the tax contributions that companies are obliged to incur as

part of their periodic business operational processes Whether in business there is a sole owner,

associate, limited company or corporate entity, LLP etc. each entity shall be accountable for

complying with the taxation requirements (Blakeley, 2018). The study-assessment discusses

different facets of the business taxation. The report covers aspects like practical sum

on assessment of trading profits, key 6 trade badges, multiple VAT schemes with respect to

different approved VAT enterprises etc. In addition, it consists of practical sum of inheritance tax

as well as capital gain tax requirements.

QUESTION 1

Linda's trading profits for the year 31st march 2121:

Linda’s trading profit (before deduction of capital allowances) for year ended 31 Mar 2021

Particulars/details £ Amounts

Net profits per accounts 6,96 0

Add: Expenditure which shows in the income

account but not allowable

Depreciation 2,500

Installation of new improved heating system 3,800

Telephone costs 220

motor expenses 650

Business entertaining 520

general bad debts provisions 200 7,890

14,850

Deduct

Income not taxable as trading income

Rental income 1,200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank interest receives 80 1,280

Trading profits 13,570

QUESTION 2

Criteria for the use for employment for self employment, why people prefer self employment:

Employment implies to contract of employment agreed by both employers and

employees. Normally, the employer controls what his/her employee does, including where

their employees work. Employment is indeed an agreement between the employer

and employees to give certain remuneration to the employee. In order, the employee should be

given a salary/wage or even a regular salary. Although employee personnel may begin

negotiations certain matters in the employment contract the provisions are determined entirely

by employer. Both sides may also cancel such contract (Milanez, 2017). An employment

contract with an individual employee can require a verbal confrontation, written

correspondences or even letter of confirmation. The United Kingdom outlines employment as

'service contract.' There is a contract under which there are shared commitments among

employers and their employees. The employment contract gives the employer power over where

and how job can be done. In general, in order to render matters much more complex, there's also

no formal acknowledgement as to how term 'work rules' can be defined.

Employers deduct federal as well as state taxation and pay expenses like Medicare, Welfare

Benefits and disability taxes on salaries and wages paid by workers. That's one of factors which

puts employment other than working for independent contractor. Employment often allows

employee personnel to control more facets of their job, such as the place of work, infrastructure,

tasks, hours and salaries. Employee feedback, self-reliance and self-reliance differ greatly based

on employer. Some enable considerable autonomy in way employees operate while others decide

how employees use each minute; all circumstances are employment. When the employee

disagrees with employer in private sector, employee has range of choices (Kudrle, 2019). They

can carry the matter to their supervisor, go to HR, speak to senior leadership or even offer notice.

Employers aren't allowed to discrimination on the grounds of colour, nationality, faith, sex (such

as pregnancy), personal preference, sexual preference, political orientation, aged, disabilities or

genetic details. Employees have right to lodge a Discrimination Complaint with relevant

authorities, which enforces fair employment regulations.

Trading profits 13,570

QUESTION 2

Criteria for the use for employment for self employment, why people prefer self employment:

Employment implies to contract of employment agreed by both employers and

employees. Normally, the employer controls what his/her employee does, including where

their employees work. Employment is indeed an agreement between the employer

and employees to give certain remuneration to the employee. In order, the employee should be

given a salary/wage or even a regular salary. Although employee personnel may begin

negotiations certain matters in the employment contract the provisions are determined entirely

by employer. Both sides may also cancel such contract (Milanez, 2017). An employment

contract with an individual employee can require a verbal confrontation, written

correspondences or even letter of confirmation. The United Kingdom outlines employment as

'service contract.' There is a contract under which there are shared commitments among

employers and their employees. The employment contract gives the employer power over where

and how job can be done. In general, in order to render matters much more complex, there's also

no formal acknowledgement as to how term 'work rules' can be defined.

Employers deduct federal as well as state taxation and pay expenses like Medicare, Welfare

Benefits and disability taxes on salaries and wages paid by workers. That's one of factors which

puts employment other than working for independent contractor. Employment often allows

employee personnel to control more facets of their job, such as the place of work, infrastructure,

tasks, hours and salaries. Employee feedback, self-reliance and self-reliance differ greatly based

on employer. Some enable considerable autonomy in way employees operate while others decide

how employees use each minute; all circumstances are employment. When the employee

disagrees with employer in private sector, employee has range of choices (Kudrle, 2019). They

can carry the matter to their supervisor, go to HR, speak to senior leadership or even offer notice.

Employers aren't allowed to discrimination on the grounds of colour, nationality, faith, sex (such

as pregnancy), personal preference, sexual preference, political orientation, aged, disabilities or

genetic details. Employees have right to lodge a Discrimination Complaint with relevant

authorities, which enforces fair employment regulations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

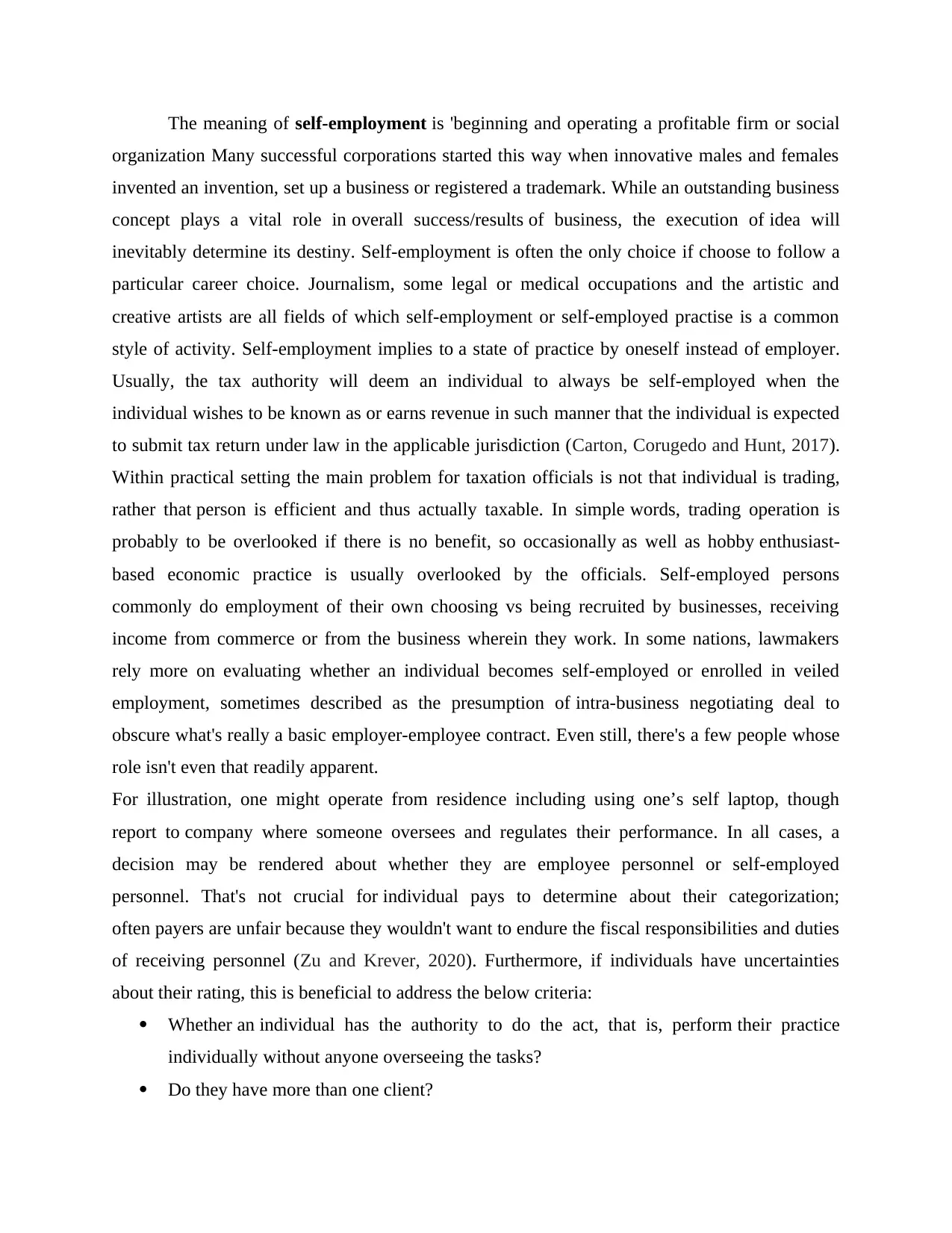

The meaning of self-employment is 'beginning and operating a profitable firm or social

organization Many successful corporations started this way when innovative males and females

invented an invention, set up a business or registered a trademark. While an outstanding business

concept plays a vital role in overall success/results of business, the execution of idea will

inevitably determine its destiny. Self-employment is often the only choice if choose to follow a

particular career choice. Journalism, some legal or medical occupations and the artistic and

creative artists are all fields of which self-employment or self-employed practise is a common

style of activity. Self-employment implies to a state of practice by oneself instead of employer.

Usually, the tax authority will deem an individual to always be self-employed when the

individual wishes to be known as or earns revenue in such manner that the individual is expected

to submit tax return under law in the applicable jurisdiction (Carton, Corugedo and Hunt, 2017).

Within practical setting the main problem for taxation officials is not that individual is trading,

rather that person is efficient and thus actually taxable. In simple words, trading operation is

probably to be overlooked if there is no benefit, so occasionally as well as hobby enthusiast-

based economic practice is usually overlooked by the officials. Self-employed persons

commonly do employment of their own choosing vs being recruited by businesses, receiving

income from commerce or from the business wherein they work. In some nations, lawmakers

rely more on evaluating whether an individual becomes self-employed or enrolled in veiled

employment, sometimes described as the presumption of intra-business negotiating deal to

obscure what's really a basic employer-employee contract. Even still, there's a few people whose

role isn't even that readily apparent.

For illustration, one might operate from residence including using one’s self laptop, though

report to company where someone oversees and regulates their performance. In all cases, a

decision may be rendered about whether they are employee personnel or self-employed

personnel. That's not crucial for individual pays to determine about their categorization;

often payers are unfair because they wouldn't want to endure the fiscal responsibilities and duties

of receiving personnel (Zu and Krever, 2020). Furthermore, if individuals have uncertainties

about their rating, this is beneficial to address the below criteria:

Whether an individual has the authority to do the act, that is, perform their practice

individually without anyone overseeing the tasks?

Do they have more than one client?

organization Many successful corporations started this way when innovative males and females

invented an invention, set up a business or registered a trademark. While an outstanding business

concept plays a vital role in overall success/results of business, the execution of idea will

inevitably determine its destiny. Self-employment is often the only choice if choose to follow a

particular career choice. Journalism, some legal or medical occupations and the artistic and

creative artists are all fields of which self-employment or self-employed practise is a common

style of activity. Self-employment implies to a state of practice by oneself instead of employer.

Usually, the tax authority will deem an individual to always be self-employed when the

individual wishes to be known as or earns revenue in such manner that the individual is expected

to submit tax return under law in the applicable jurisdiction (Carton, Corugedo and Hunt, 2017).

Within practical setting the main problem for taxation officials is not that individual is trading,

rather that person is efficient and thus actually taxable. In simple words, trading operation is

probably to be overlooked if there is no benefit, so occasionally as well as hobby enthusiast-

based economic practice is usually overlooked by the officials. Self-employed persons

commonly do employment of their own choosing vs being recruited by businesses, receiving

income from commerce or from the business wherein they work. In some nations, lawmakers

rely more on evaluating whether an individual becomes self-employed or enrolled in veiled

employment, sometimes described as the presumption of intra-business negotiating deal to

obscure what's really a basic employer-employee contract. Even still, there's a few people whose

role isn't even that readily apparent.

For illustration, one might operate from residence including using one’s self laptop, though

report to company where someone oversees and regulates their performance. In all cases, a

decision may be rendered about whether they are employee personnel or self-employed

personnel. That's not crucial for individual pays to determine about their categorization;

often payers are unfair because they wouldn't want to endure the fiscal responsibilities and duties

of receiving personnel (Zu and Krever, 2020). Furthermore, if individuals have uncertainties

about their rating, this is beneficial to address the below criteria:

Whether an individual has the authority to do the act, that is, perform their practice

individually without anyone overseeing the tasks?

Do they have more than one client?

Are persons able to bring clients with thru if they prefer?

Can they be able to distribute/assign their tasks?

Can they not be able? to perform that duties?

Would they get their own funds and resources Instance, When something crashes, do they

have private computers, are they culpable for paying software rentals, are they

accountable for restoring or improving their task instruments?

Do you have offered yourself/your skills?

Should anyone else be hired to operate without anyone else's authorisation?

Do they share the burden of obligation for the job performed instance, if these are not

done properly, will they also be fined?

Is there really a written contract outlining work situations and specifications

Are they going to have a customer invoiced?

Have you ever been employed to do any predefined employment?

Why prefer self-employment rather than being employed, resulting in so many IR 35 cases:

Control across all areas of business: Executive control over any aspect of the organisation is the

major benefit of being in self-employment. Individuals assess what to have for business.

Individuals should select the target demographic. They have selected the marketing

characteristics that render their company distinctive. Becoming self-employed therefore means

that one could set ones-self-priorities, business agenda and priorities. They are culpable

for quality level of the items or services that business offer. They choose all the bosses they

employed, but rather than getting stuck with their co-workers they can't tolerate, they tend to

pick ones they interact with every day (Kaledin and et.al., 2018).

Tax Benefits: Individuals could exempt those costs relevant to the operations of the commercial

enterprise digital, telephone and fax bills shall apply if the individual uses same wireless and

network facilities inside the organisation that they do for personal use, just a portion of the

expense would be deducted. Flight and commercial usage of vehicle shall be liable for cutting

taxes. They would also exempt foods and entertainment expenditures since they are related to

employment. If people return to college and otherwise expand their business-related capabilities,

they will be able to deduct those expenses.

Can they be able to distribute/assign their tasks?

Can they not be able? to perform that duties?

Would they get their own funds and resources Instance, When something crashes, do they

have private computers, are they culpable for paying software rentals, are they

accountable for restoring or improving their task instruments?

Do you have offered yourself/your skills?

Should anyone else be hired to operate without anyone else's authorisation?

Do they share the burden of obligation for the job performed instance, if these are not

done properly, will they also be fined?

Is there really a written contract outlining work situations and specifications

Are they going to have a customer invoiced?

Have you ever been employed to do any predefined employment?

Why prefer self-employment rather than being employed, resulting in so many IR 35 cases:

Control across all areas of business: Executive control over any aspect of the organisation is the

major benefit of being in self-employment. Individuals assess what to have for business.

Individuals should select the target demographic. They have selected the marketing

characteristics that render their company distinctive. Becoming self-employed therefore means

that one could set ones-self-priorities, business agenda and priorities. They are culpable

for quality level of the items or services that business offer. They choose all the bosses they

employed, but rather than getting stuck with their co-workers they can't tolerate, they tend to

pick ones they interact with every day (Kaledin and et.al., 2018).

Tax Benefits: Individuals could exempt those costs relevant to the operations of the commercial

enterprise digital, telephone and fax bills shall apply if the individual uses same wireless and

network facilities inside the organisation that they do for personal use, just a portion of the

expense would be deducted. Flight and commercial usage of vehicle shall be liable for cutting

taxes. They would also exempt foods and entertainment expenditures since they are related to

employment. If people return to college and otherwise expand their business-related capabilities,

they will be able to deduct those expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Potential for Growth: Self-employment enables anyone with rational knowledge in all aspects of

running business Functioning for themselves has to be effective and will require conducting a

great deal of research concerning the different dimensions of business. This corresponds to areas

such as purchasing online, management of staff, advertising and payroll These talents remain

with them but since they broaden the company and start a fresh business as well as they also

aspire to go back to collaborating with others (Al Karaawy and Al Baaj., 2018).

Customer Interactions: If individuals become self-employed, individuals often do what they can,

especially at the beginnings This means that one can build successful connections with their

customers. They work specifically with any consumer who uses their facilities or buys their

products. They have a remarkable opportunity of continuing to learn consumers, which gives

them perspectives into what they want. This relation would also continue to develop customer

satisfaction and serve them to contribute to their corporation in the long term.

QUESTION 3

Discussion Six badges for trade:

In 1955, the study of the Royal Commissions on the Taxation of Profits and Income reviewed the

case laws and created six trade badges. That was starting point because, as one would

understand, some improvements being made in the area, supplemented by case-laws. Here are 6

major trade badges mainly applied, as described below:

Profit Seeking Motive: This is evident that a motivation for making profits may entail a

trading function although this not so much adequate on own. In the particular instance of

Salt v Chamberlain case law [1979] STC 750, analysis consultant incurred losses on the

share exchange upon failing to forecast the sector. The failure occurred after multiple

periods of greater than two hundred transactions. This doesn't seem like a matter of trade

and wealth in life. It has been formed that selling of securities by private citizen could

never be followed by an exchanging of badges. All revenues are prone to taxation on

capital gains (Clarke and Kopczuk, 2017).

Number of transactions: The term determines an unethical practice being conducted by

businesses, which deals in goods or services and once they sell an assets and gain some

profits. Then they engage in the activity of several realization of the same asset in a

specific period of time. The gain of profit from that asset will be anticipated as taxable

running business Functioning for themselves has to be effective and will require conducting a

great deal of research concerning the different dimensions of business. This corresponds to areas

such as purchasing online, management of staff, advertising and payroll These talents remain

with them but since they broaden the company and start a fresh business as well as they also

aspire to go back to collaborating with others (Al Karaawy and Al Baaj., 2018).

Customer Interactions: If individuals become self-employed, individuals often do what they can,

especially at the beginnings This means that one can build successful connections with their

customers. They work specifically with any consumer who uses their facilities or buys their

products. They have a remarkable opportunity of continuing to learn consumers, which gives

them perspectives into what they want. This relation would also continue to develop customer

satisfaction and serve them to contribute to their corporation in the long term.

QUESTION 3

Discussion Six badges for trade:

In 1955, the study of the Royal Commissions on the Taxation of Profits and Income reviewed the

case laws and created six trade badges. That was starting point because, as one would

understand, some improvements being made in the area, supplemented by case-laws. Here are 6

major trade badges mainly applied, as described below:

Profit Seeking Motive: This is evident that a motivation for making profits may entail a

trading function although this not so much adequate on own. In the particular instance of

Salt v Chamberlain case law [1979] STC 750, analysis consultant incurred losses on the

share exchange upon failing to forecast the sector. The failure occurred after multiple

periods of greater than two hundred transactions. This doesn't seem like a matter of trade

and wealth in life. It has been formed that selling of securities by private citizen could

never be followed by an exchanging of badges. All revenues are prone to taxation on

capital gains (Clarke and Kopczuk, 2017).

Number of transactions: The term determines an unethical practice being conducted by

businesses, which deals in goods or services and once they sell an assets and gain some

profits. Then they engage in the activity of several realization of the same asset in a

specific period of time. The gain of profit from that asset will be anticipated as taxable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

value. Initially it is not consider as trading activity but series of purchase and sale

transaction for that asset is considered as trading activity. If such transactions are going

at natural time interval and showing the habitual and regular activity which make it a

weak case of trading and that won't be considered in trading activity.

Changes to the asset-Any changes or modifications made to properties that will make

them even more important need to be remembered. For Cape Brandy Syndicate v CIR-

CA 1921, 12 TC 358; [1921] wine syndicate members formed a new trade union in

African Countries to purchase brandy. Several have been sent to the South, the others

were sent to England to be blended, re-engineered and sold at a profit with French

brandy. The investor tried to argue that, as a result of the transfer of the investment, the

transaction was financially available. This was held to have been carried out by exchange

or a corporation and may be measured as a business advantage.

Way sale carried out- HMRC states in its guidance that that's always a sign if the

contract follows those in 'unquestionable markets.' Scenario CIR v Barton and Others

involved three unrelated persons who had bought cargo vessels together. The ship was

converted into a steam drifter and then sold for profit. The purchase was the first vessel

bought by the three people. The value, which was defined as trading profit, was

calculated. In the decision, the judge claimed that the test to be taken to ascertain whether

or not the activity now being investigated is of a 'deal' type is that the dealings in question

are from the same nature and are carried out in the same way as is characteristic of

ordinary trading on the business line (Timoshenkov and Nashchekina, 2018).

Source of finance: the root of the financing must be ascertained before deciding whether

the operation is carried out. In the first case, the financing drawn up to purchase an asset

would mean that the asset will have to be sold in necessary to protect the debt. It is

essential to consider financial needs from those resources which are less time and cost

consuming. It is so because a business can succeed in long time period only if they take

financial assistance from right sources.

Interval of period between selling and acquisition- The duration of asset possession is

an important indicator of exchange. The longer the duration of ownership, the more

probable it was to be a transaction rather than a purchase. HMRC is also intentionally

exploring whether an aim that would suggest tax status can be seen. The time period

transaction for that asset is considered as trading activity. If such transactions are going

at natural time interval and showing the habitual and regular activity which make it a

weak case of trading and that won't be considered in trading activity.

Changes to the asset-Any changes or modifications made to properties that will make

them even more important need to be remembered. For Cape Brandy Syndicate v CIR-

CA 1921, 12 TC 358; [1921] wine syndicate members formed a new trade union in

African Countries to purchase brandy. Several have been sent to the South, the others

were sent to England to be blended, re-engineered and sold at a profit with French

brandy. The investor tried to argue that, as a result of the transfer of the investment, the

transaction was financially available. This was held to have been carried out by exchange

or a corporation and may be measured as a business advantage.

Way sale carried out- HMRC states in its guidance that that's always a sign if the

contract follows those in 'unquestionable markets.' Scenario CIR v Barton and Others

involved three unrelated persons who had bought cargo vessels together. The ship was

converted into a steam drifter and then sold for profit. The purchase was the first vessel

bought by the three people. The value, which was defined as trading profit, was

calculated. In the decision, the judge claimed that the test to be taken to ascertain whether

or not the activity now being investigated is of a 'deal' type is that the dealings in question

are from the same nature and are carried out in the same way as is characteristic of

ordinary trading on the business line (Timoshenkov and Nashchekina, 2018).

Source of finance: the root of the financing must be ascertained before deciding whether

the operation is carried out. In the first case, the financing drawn up to purchase an asset

would mean that the asset will have to be sold in necessary to protect the debt. It is

essential to consider financial needs from those resources which are less time and cost

consuming. It is so because a business can succeed in long time period only if they take

financial assistance from right sources.

Interval of period between selling and acquisition- The duration of asset possession is

an important indicator of exchange. The longer the duration of ownership, the more

probable it was to be a transaction rather than a purchase. HMRC is also intentionally

exploring whether an aim that would suggest tax status can be seen. The time period

between these two aspects need to be assessed before determining the tax value in an

effective manner. This is so because there should be a distinct amount of time between

selling and acquiring so that both parties can be satisfied (Biddle, Fels and Sinning,

2018).

Different VAT schemes for the various VAT registered companies:

VAT full form is value added tax and by name it specifies itself that add a tax on value

of goods and service and that has to be submitted to Her Majesty's Revenues and Customs and it

is consumption based tax. Value added tax is charged on sale of goods, service like selling an

assets, commission based things and etc. Some goods which are being exported out of the United

Kingdom are kept out of the VAT system and are not charged under the certain scheme. VAT

comes under indirect tax because it is charged by the business in when a sell is made to

customer. VAT is not equal at all level of business it depend on business to business and there

are some exception for the certain industry. Their are many VAT scheme in UK which are

mentioned below.

VAT annual accounting scheme

In this accounting scheme companies file their VAT returns single times a year. This

scheme usually applied on small scale businesses. To become eligible for this scheme businesses

must have VAT taxable turnover less the or equal to 1.35 million. Pros for this scheme are

business have to file VAT return once in a year rather then four times a year. Business get

enough time to file VAT returns and make remaining payments (Shvets and Synooka, 2020).

Cons for the scheme is when businesses made advance payments they are likely to get refunded

once a year this scheme doesn't provide the facility of reclaiming the balance amount at regular

period of time.

Flat rate scheme

In flat rate scheme businesses have to pay a percentage of sales to Her Majesty's

Revenues and Customs and that percentage may change according to the business to business. In

this business VAT is charged on invoices from customer but don't have to give every purchase

and sale details for every transaction. For being eligible for this scheme business turnover must

be up to 150000. Pros for this scheme are it easily compiled with the norms and save cost in

compiling process. Less number of rules are followed in this scheme. Cons for this scheme is,

effective manner. This is so because there should be a distinct amount of time between

selling and acquiring so that both parties can be satisfied (Biddle, Fels and Sinning,

2018).

Different VAT schemes for the various VAT registered companies:

VAT full form is value added tax and by name it specifies itself that add a tax on value

of goods and service and that has to be submitted to Her Majesty's Revenues and Customs and it

is consumption based tax. Value added tax is charged on sale of goods, service like selling an

assets, commission based things and etc. Some goods which are being exported out of the United

Kingdom are kept out of the VAT system and are not charged under the certain scheme. VAT

comes under indirect tax because it is charged by the business in when a sell is made to

customer. VAT is not equal at all level of business it depend on business to business and there

are some exception for the certain industry. Their are many VAT scheme in UK which are

mentioned below.

VAT annual accounting scheme

In this accounting scheme companies file their VAT returns single times a year. This

scheme usually applied on small scale businesses. To become eligible for this scheme businesses

must have VAT taxable turnover less the or equal to 1.35 million. Pros for this scheme are

business have to file VAT return once in a year rather then four times a year. Business get

enough time to file VAT returns and make remaining payments (Shvets and Synooka, 2020).

Cons for the scheme is when businesses made advance payments they are likely to get refunded

once a year this scheme doesn't provide the facility of reclaiming the balance amount at regular

period of time.

Flat rate scheme

In flat rate scheme businesses have to pay a percentage of sales to Her Majesty's

Revenues and Customs and that percentage may change according to the business to business. In

this business VAT is charged on invoices from customer but don't have to give every purchase

and sale details for every transaction. For being eligible for this scheme business turnover must

be up to 150000. Pros for this scheme are it easily compiled with the norms and save cost in

compiling process. Less number of rules are followed in this scheme. Cons for this scheme is,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business which are charged by higher rate they have to pay more VAT in comparison with

normal VAT return which affect the profitability of their business.

VAT margin scheme

VAT margin scheme is mostly used by the business deals the antiques item, goods which

are already being used or repaired and up for resale or work on art and other collectors. In this

scheme business pay the tax on difference between what the business have purchased the product

and for what value it is being sold to customers (Habu, 2017). In this scheme business have to

keep a clear record for all eligible transaction which are made during the year and track the

record while filing the VAT return. In this scheme there are some exceptions for dealing in

investment gold, precious stone and metals for the business.

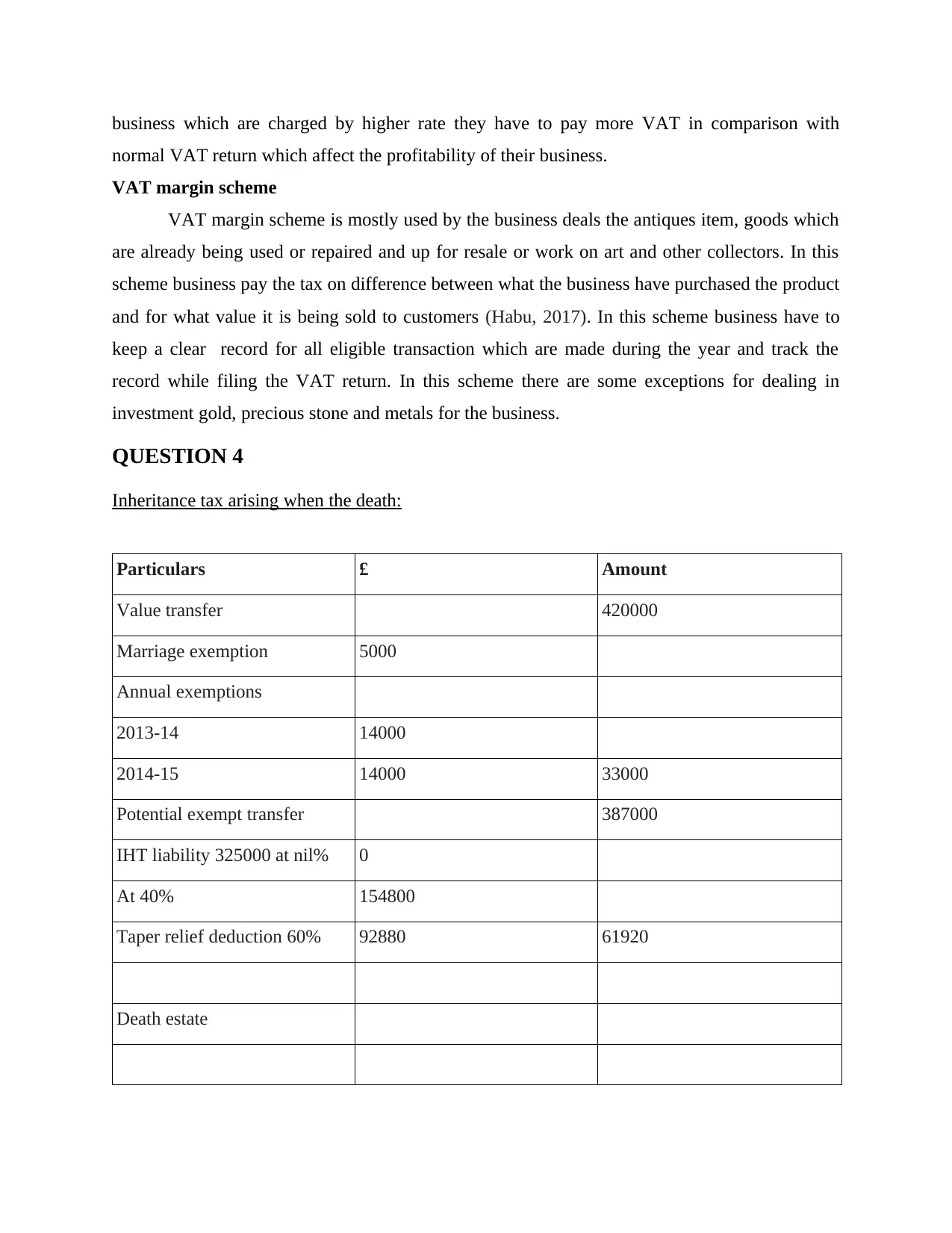

QUESTION 4

Inheritance tax arising when the death:

Particulars £ Amount

Value transfer 420000

Marriage exemption 5000

Annual exemptions

2013-14 14000

2014-15 14000 33000

Potential exempt transfer 387000

IHT liability 325000 at nil% 0

At 40% 154800

Taper relief deduction 60% 92880 61920

Death estate

normal VAT return which affect the profitability of their business.

VAT margin scheme

VAT margin scheme is mostly used by the business deals the antiques item, goods which

are already being used or repaired and up for resale or work on art and other collectors. In this

scheme business pay the tax on difference between what the business have purchased the product

and for what value it is being sold to customers (Habu, 2017). In this scheme business have to

keep a clear record for all eligible transaction which are made during the year and track the

record while filing the VAT return. In this scheme there are some exceptions for dealing in

investment gold, precious stone and metals for the business.

QUESTION 4

Inheritance tax arising when the death:

Particulars £ Amount

Value transfer 420000

Marriage exemption 5000

Annual exemptions

2013-14 14000

2014-15 14000 33000

Potential exempt transfer 387000

IHT liability 325000 at nil% 0

At 40% 154800

Taper relief deduction 60% 92880 61920

Death estate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Value for estate 880000

Spouse exemption (880000/2 ) 440000

Chargeable estate 440000

IHT liability 440000 at 40% 176000

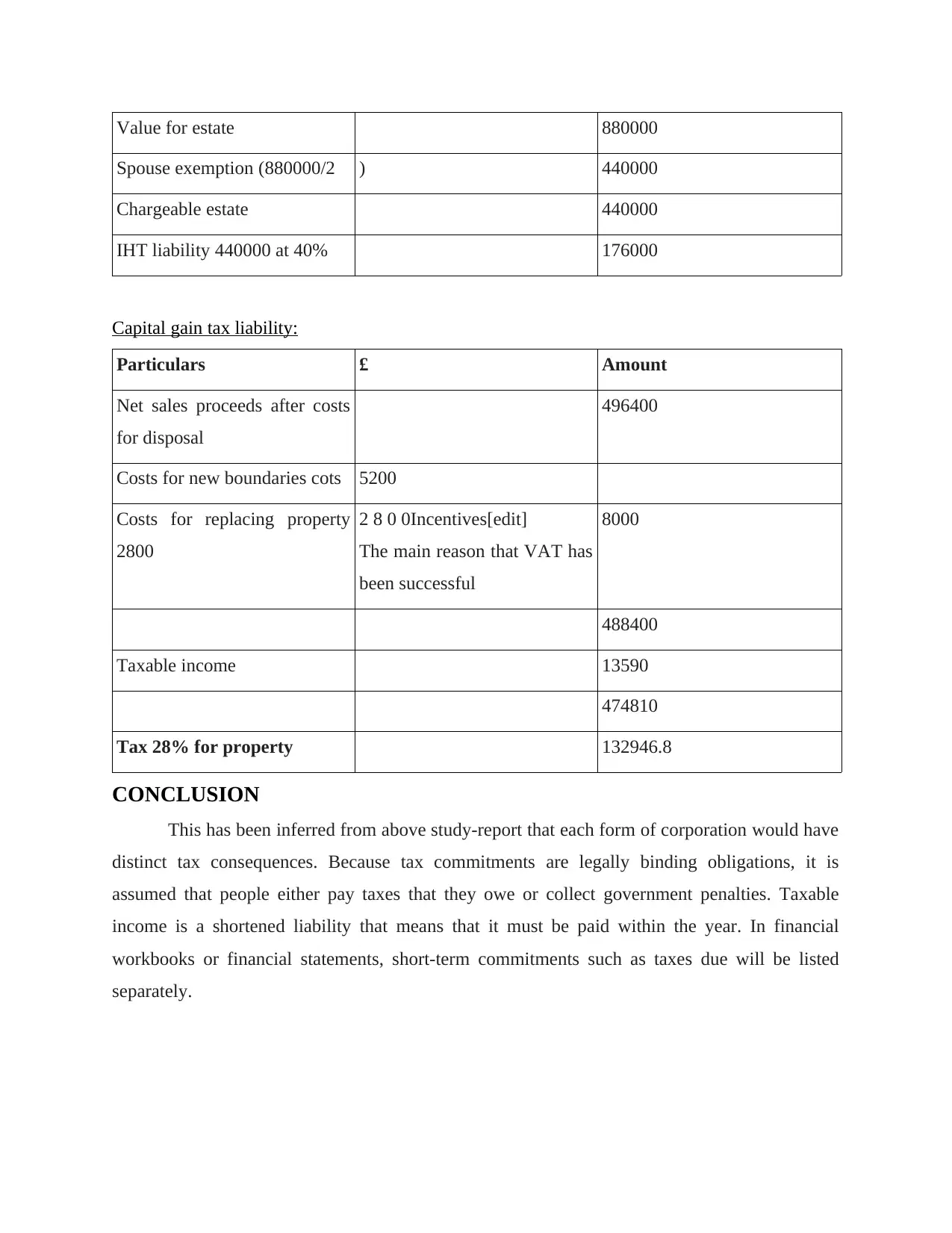

Capital gain tax liability:

Particulars £ Amount

Net sales proceeds after costs

for disposal

496400

Costs for new boundaries cots 5200

Costs for replacing property

2800

2 8 0 0Incentives[edit]

The main reason that VAT has

been successful

8000

488400

Taxable income 13590

474810

Tax 28% for property 132946.8

CONCLUSION

This has been inferred from above study-report that each form of corporation would have

distinct tax consequences. Because tax commitments are legally binding obligations, it is

assumed that people either pay taxes that they owe or collect government penalties. Taxable

income is a shortened liability that means that it must be paid within the year. In financial

workbooks or financial statements, short-term commitments such as taxes due will be listed

separately.

Spouse exemption (880000/2 ) 440000

Chargeable estate 440000

IHT liability 440000 at 40% 176000

Capital gain tax liability:

Particulars £ Amount

Net sales proceeds after costs

for disposal

496400

Costs for new boundaries cots 5200

Costs for replacing property

2800

2 8 0 0Incentives[edit]

The main reason that VAT has

been successful

8000

488400

Taxable income 13590

474810

Tax 28% for property 132946.8

CONCLUSION

This has been inferred from above study-report that each form of corporation would have

distinct tax consequences. Because tax commitments are legally binding obligations, it is

assumed that people either pay taxes that they owe or collect government penalties. Taxable

income is a shortened liability that means that it must be paid within the year. In financial

workbooks or financial statements, short-term commitments such as taxes due will be listed

separately.

REFERENCES

Books and Journals:

Al Karaawy, N.A.A. and Al Baaj, Q.M.A., 2018. Taxation of international business

organizations. Academy of Accounting and Financial Studies Journal, 22(1), pp.1-16.

Biddle, N., Fels, K.M. and Sinning, M., 2018. Behavioral insights on business taxation: Evidence

from two natural field experiments. Journal of Behavioral and Experimental

Finance, 18, pp.30-49.

Blakeley, G., 2018. Fair dues: Rebalancing business taxation in the UK.

Carton, B., Corugedo, E.F. and Hunt, M.B.L., 2017. No business taxation without model

representation: Adding corporate income and cash flow taxes to GIMF. International

Monetary Fund.

Clarke, C. and Kopczuk, W., 2017. Business income and business taxation in the United States

since the 1950s. Tax Policy and the Economy, 31(1), pp.121-159.

Habu, K., 2017. Centre for Business Taxation Tax Database 2017.

Kaledin, S.V., Barkhatov, V.I., Kapkaev, Y. and Shestakova, E.V., 2018. SMALL BUSINESS

TAXATION IN EUROPEAN COUNTRIES: CRUCIAL POINTS, SPECIFIC

FEATURES AND POTENTIAL ADAPTATION OF ADVANTAGEOUS

OPTIONS. Journal of Fundamental and Applied Sciences, 10(6S), pp.1611-1629.

Kudrle, R., 2019. The Continuing Turmoil in International Business Taxation. Available at SSRN

3597720.

Milanez, A., 2017. Legal tax liability, legal remittance responsibility and tax incidence: Three

dimensions of business taxation.

Shvets, Y.O. and Synooka, D.V., 2020. FEATURES OF TAXATION OF SMALL BUSINESS

ENTITIES IN UKRAINE: PROBLEMS AND DIRECTIONS OF

IMPROVEMENT. Bulletin of Zaporizhzhia National University. Economic Sciences, (3

(47)), pp.95-100.

Timoshenkov, I.V. and Nashchekina, O.N., 2018. Business taxation: a transaction cost theory

perspective.

Zu, Y. and Krever, R., 2020. The United Kingdom has spoken: The receding impact of European

jurisprudence on the UK interpretation of the common VAT system. Common Law

World Review, 49(1), pp.75-91.

Books and Journals:

Al Karaawy, N.A.A. and Al Baaj, Q.M.A., 2018. Taxation of international business

organizations. Academy of Accounting and Financial Studies Journal, 22(1), pp.1-16.

Biddle, N., Fels, K.M. and Sinning, M., 2018. Behavioral insights on business taxation: Evidence

from two natural field experiments. Journal of Behavioral and Experimental

Finance, 18, pp.30-49.

Blakeley, G., 2018. Fair dues: Rebalancing business taxation in the UK.

Carton, B., Corugedo, E.F. and Hunt, M.B.L., 2017. No business taxation without model

representation: Adding corporate income and cash flow taxes to GIMF. International

Monetary Fund.

Clarke, C. and Kopczuk, W., 2017. Business income and business taxation in the United States

since the 1950s. Tax Policy and the Economy, 31(1), pp.121-159.

Habu, K., 2017. Centre for Business Taxation Tax Database 2017.

Kaledin, S.V., Barkhatov, V.I., Kapkaev, Y. and Shestakova, E.V., 2018. SMALL BUSINESS

TAXATION IN EUROPEAN COUNTRIES: CRUCIAL POINTS, SPECIFIC

FEATURES AND POTENTIAL ADAPTATION OF ADVANTAGEOUS

OPTIONS. Journal of Fundamental and Applied Sciences, 10(6S), pp.1611-1629.

Kudrle, R., 2019. The Continuing Turmoil in International Business Taxation. Available at SSRN

3597720.

Milanez, A., 2017. Legal tax liability, legal remittance responsibility and tax incidence: Three

dimensions of business taxation.

Shvets, Y.O. and Synooka, D.V., 2020. FEATURES OF TAXATION OF SMALL BUSINESS

ENTITIES IN UKRAINE: PROBLEMS AND DIRECTIONS OF

IMPROVEMENT. Bulletin of Zaporizhzhia National University. Economic Sciences, (3

(47)), pp.95-100.

Timoshenkov, I.V. and Nashchekina, O.N., 2018. Business taxation: a transaction cost theory

perspective.

Zu, Y. and Krever, R., 2020. The United Kingdom has spoken: The receding impact of European

jurisprudence on the UK interpretation of the common VAT system. Common Law

World Review, 49(1), pp.75-91.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.