Business Taxation Report: Trading Profits, Self-Employment, and VAT

VerifiedAdded on 2022/12/29

|12

|3481

|479

Report

AI Summary

This report delves into the intricacies of business taxation, commencing with an analysis of Linda's trading profits, detailing permissible and non-permissible expenses, and explaining key financial accounting terminologies such as trading accounts, income statements, and balance sheets. It then transitions to a discussion on the criteria for employment versus self-employment, highlighting the advantages of self-employment such as flexible schedules and financial incentives. The report explores the six badges of trade used by HMRC to determine economic activity, including the profit motive, volume of transactions, and character of properties. Finally, it examines different VAT schemes for VAT-registered companies, explaining the calculation methods and the role of VAT in the supply chain. The report provides an in-depth understanding of corporation tax, VAT, and other relevant aspects of business taxation.

Business

Taxation

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

QUESTION 2..................................................................................................................................5

QUESTION 3..................................................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

QUESTION 1..................................................................................................................................3

QUESTION 2..................................................................................................................................5

QUESTION 3..................................................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Company taxation is the taxation system that corporations pay for regular business operations.

Business tax is seen in the corporate tax that businesses pay on their operations. As per the tax

rules, businesses pay taxes (Blakeley, 2018). The corporate tax government can make pay tax

laws accountable for sole trader, partnership, limited partnership, enterprise, companies. The

direct tax that applies to the company's net income is the corporate tax. These tax companies pay

the state for their sales. Businesses, for instance, pay any taxes under the tax rules. This report

provides the basis for corporation taxes. This article discusses subjects such as trading earnings,

peer, six trade codes, and VAT schemes for separate VAT firms, etc. In addition, it encompasses

issues such as inheritance tax, capital benefit tax obligation, etc.

QUESTION 1

Linda's trading profits for the year 31st march 2121:

Trading gains are equal to the revenue from the operations. It does not require income-related

funding, costs for earnings for the properties. In order to maximize the profitability, it appears to

be a higher predictor of the potential for the key operations of corporations. Sales for the shares,

the benefit that an investor drives for the acquisition (Martins, 2019). For the investor who

understands the risks involved in the deals for the firm, trade gains are important. Such revenues

are for acquisitions, product distribution, utilities. This argument indicates that firms that report

trade earnings do not have permissible trades. Trading gains are revenue-producing company

profits, costs that are not allowable for companies. These sales help corporations raise money for

their operations, helping firms meet goals.

There are various terminology in accounting that assist managers in making financial decisions.

The finance department documents transactions that help businesses meet their targets. Different

financial accounts are prepared by the accounting department to help them maintain records.

These documents aid them in the organization of financing, handling funds for the operations

that are carried out to meet goals of industry. Trading, income statement, balance sheet and

transactions included with company were included in the financial report.

The trading account reveals direct costs, even that the firm conducts its operations. Trading

account which is structured for choice managers to make company transactions. For the taxable

pay, net profits the company receives, selling, sales statement is valuable. It reflects the

Company taxation is the taxation system that corporations pay for regular business operations.

Business tax is seen in the corporate tax that businesses pay on their operations. As per the tax

rules, businesses pay taxes (Blakeley, 2018). The corporate tax government can make pay tax

laws accountable for sole trader, partnership, limited partnership, enterprise, companies. The

direct tax that applies to the company's net income is the corporate tax. These tax companies pay

the state for their sales. Businesses, for instance, pay any taxes under the tax rules. This report

provides the basis for corporation taxes. This article discusses subjects such as trading earnings,

peer, six trade codes, and VAT schemes for separate VAT firms, etc. In addition, it encompasses

issues such as inheritance tax, capital benefit tax obligation, etc.

QUESTION 1

Linda's trading profits for the year 31st march 2121:

Trading gains are equal to the revenue from the operations. It does not require income-related

funding, costs for earnings for the properties. In order to maximize the profitability, it appears to

be a higher predictor of the potential for the key operations of corporations. Sales for the shares,

the benefit that an investor drives for the acquisition (Martins, 2019). For the investor who

understands the risks involved in the deals for the firm, trade gains are important. Such revenues

are for acquisitions, product distribution, utilities. This argument indicates that firms that report

trade earnings do not have permissible trades. Trading gains are revenue-producing company

profits, costs that are not allowable for companies. These sales help corporations raise money for

their operations, helping firms meet goals.

There are various terminology in accounting that assist managers in making financial decisions.

The finance department documents transactions that help businesses meet their targets. Different

financial accounts are prepared by the accounting department to help them maintain records.

These documents aid them in the organization of financing, handling funds for the operations

that are carried out to meet goals of industry. Trading, income statement, balance sheet and

transactions included with company were included in the financial report.

The trading account reveals direct costs, even that the firm conducts its operations. Trading

account which is structured for choice managers to make company transactions. For the taxable

pay, net profits the company receives, selling, sales statement is valuable. It reflects the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

relationship between revenue and gross income, which allows the organization to determine

productivity. It indicates the relationships between the expenses of the product sold and gross

income. The Trade Account contains details pertaining to trading operations. The benefit trading

account displays numerous terms, including costs and group profits.

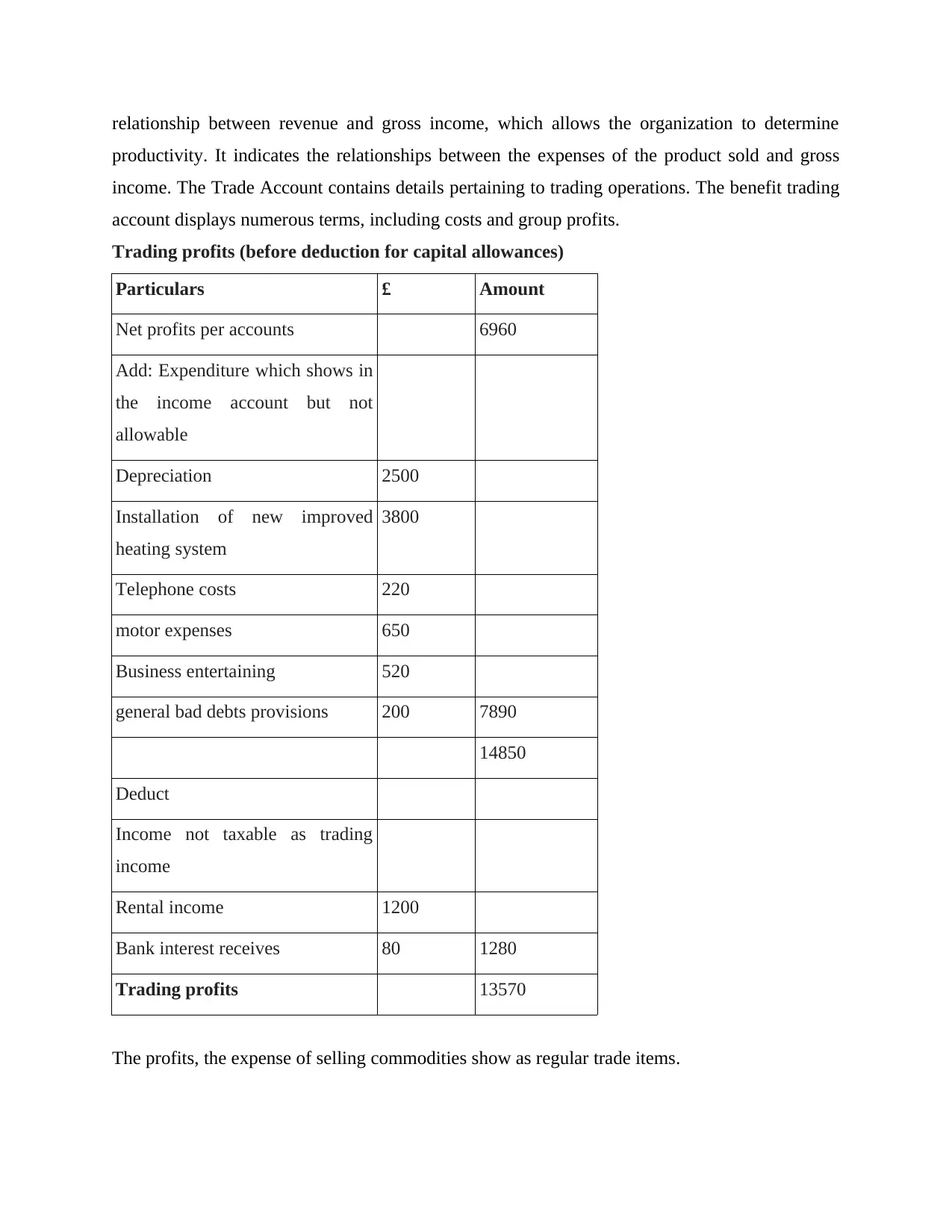

Trading profits (before deduction for capital allowances)

Particulars £ Amount

Net profits per accounts 6960

Add: Expenditure which shows in

the income account but not

allowable

Depreciation 2500

Installation of new improved

heating system

3800

Telephone costs 220

motor expenses 650

Business entertaining 520

general bad debts provisions 200 7890

14850

Deduct

Income not taxable as trading

income

Rental income 1200

Bank interest receives 80 1280

Trading profits 13570

The profits, the expense of selling commodities show as regular trade items.

productivity. It indicates the relationships between the expenses of the product sold and gross

income. The Trade Account contains details pertaining to trading operations. The benefit trading

account displays numerous terms, including costs and group profits.

Trading profits (before deduction for capital allowances)

Particulars £ Amount

Net profits per accounts 6960

Add: Expenditure which shows in

the income account but not

allowable

Depreciation 2500

Installation of new improved

heating system

3800

Telephone costs 220

motor expenses 650

Business entertaining 520

general bad debts provisions 200 7890

14850

Deduct

Income not taxable as trading

income

Rental income 1200

Bank interest receives 80 1280

Trading profits 13570

The profits, the expense of selling commodities show as regular trade items.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The rental income for the purchase of a business as property income for the primary Corporate

Tax estimate.

The interest earned by the bank is not subject to income tax.

Wages and compensation (including NICs for employers) are permissible.

Devaluation is never admissible (Biddle, Fels and Sinning, 2018).

Fees for directors are handled in the same manner as all compensation for workers.

Administrative costs are solely and primarily for the company.

Installation costs and engine costs are for personal consumption, and are not for commercial

purposes.

Company hospitality expenses are permitted, but it is never permissible to entertain clients.

Changes in the general rules for bad debts must still be changed, although it is appropriate to

raise particular provisions and to write off bad debts.

QUESTION 2

Criteria for the use for employment for self employment, why people prefer self employment:

Employment is from whether the workers work for the company who pays them wages.

Employment is just work for employers, paying salaries for workers (Giroud and Rauh, 2019).

Jobs for people who do not work for themselves are a sector that works with workers.

Self-employment is the jobs that persons perform for themselves and not for employers. This

offers people the benefits of what they want to do with their careers. It is the mechanism that

demonstrates that people don't work for the employer that pays their salaries. It indicates

accountability for self-employment in situations where the payer does not have taxes. Different

professions, highly specialized for unique forms of jobs, involve self-employed individuals.

Self-employees are responsible for the fees they collect. Self-employment gives workplace

flexibility deals; individuals are not liable for work hours for the employers. Companies who

earn net income all divide the profits with workers in these kinds of jobs. The bulk of self-

employed business people go to the organization when they want to fix issues for clients. They

value people for their products, resources, for society. They build jobs, pay taxes to fund schools,

towns, neighbours, etc. To achieve their goals, people enhance their lifestyle in this way.

Self-employment offers a greater work time balance; people pick their own clients, etc. Self-

employment draws as it helps people to inspire, helps to create new ideas, etc. Self-employment

gives the organization the ability for fresh ideas that help customers meet their need. Self-

Tax estimate.

The interest earned by the bank is not subject to income tax.

Wages and compensation (including NICs for employers) are permissible.

Devaluation is never admissible (Biddle, Fels and Sinning, 2018).

Fees for directors are handled in the same manner as all compensation for workers.

Administrative costs are solely and primarily for the company.

Installation costs and engine costs are for personal consumption, and are not for commercial

purposes.

Company hospitality expenses are permitted, but it is never permissible to entertain clients.

Changes in the general rules for bad debts must still be changed, although it is appropriate to

raise particular provisions and to write off bad debts.

QUESTION 2

Criteria for the use for employment for self employment, why people prefer self employment:

Employment is from whether the workers work for the company who pays them wages.

Employment is just work for employers, paying salaries for workers (Giroud and Rauh, 2019).

Jobs for people who do not work for themselves are a sector that works with workers.

Self-employment is the jobs that persons perform for themselves and not for employers. This

offers people the benefits of what they want to do with their careers. It is the mechanism that

demonstrates that people don't work for the employer that pays their salaries. It indicates

accountability for self-employment in situations where the payer does not have taxes. Different

professions, highly specialized for unique forms of jobs, involve self-employed individuals.

Self-employees are responsible for the fees they collect. Self-employment gives workplace

flexibility deals; individuals are not liable for work hours for the employers. Companies who

earn net income all divide the profits with workers in these kinds of jobs. The bulk of self-

employed business people go to the organization when they want to fix issues for clients. They

value people for their products, resources, for society. They build jobs, pay taxes to fund schools,

towns, neighbours, etc. To achieve their goals, people enhance their lifestyle in this way.

Self-employment offers a greater work time balance; people pick their own clients, etc. Self-

employment draws as it helps people to inspire, helps to create new ideas, etc. Self-employment

gives the organization the ability for fresh ideas that help customers meet their need. Self-

employed individuals build demand for consumers and encourage consumers to purchase

products and services. They give people a job from their earnings for their work. People who

earn profitability for economic activity, which helps to change their lifestyle, are self-employees.

As the entrepreneur manages numerous ventures with his own money, that gives their rewards as

they gain profits (Todtenhaupt, 2018).

They have their very own rules for pacing as they needs to run. They submit their innovative

ideas for submit for the company for the new products, facilities that helps consumers for

fulfilling the requirements which satisfies them.

Self-employed timetable: Self-employed employees work for themselves because they work on

their own schedule. It's about employees doing their own careers.

Be your own boss: Self-employment ensures that you build a boss of your own. It's about

building a self-empire, how consumers will make offers.

Take account of tax incentives for self-employment: self-employment is a tax deductible from

employer expenses from corporate profits.

Keep the income you make: as it raises efficiency, self-employed workers earn money. Self-

employees maintain the money they receive from their company.

Enjoy a job with artistic freedom: this is the draw for creative employees when they work for

their own innovation process as they operate for their own company.

QUESTION 3

Discussion Six badges for trade:

Trade badges are used by HMRC to determine whether an activity can be called a decent

economic behaviour or economic activity or whether it is just an economically active section for

an individual's hobby. To decide whether a hobby is reshaped into a subject to tax exercise,

careful discussion is needed. Trade codes also include components that take purchases into

account, the sequence of transactions (Al Karaawy and Al Baaj, 2018). In June 1955, the Royal

Profit Taxation Committee used court rulings to propose a method for the identification of trade

badges, including the subject matter for realization, the duration of the holding period, the

frequency percentage for transaction costs, the additional works, the situations responsible for

realization, etc.

products and services. They give people a job from their earnings for their work. People who

earn profitability for economic activity, which helps to change their lifestyle, are self-employees.

As the entrepreneur manages numerous ventures with his own money, that gives their rewards as

they gain profits (Todtenhaupt, 2018).

They have their very own rules for pacing as they needs to run. They submit their innovative

ideas for submit for the company for the new products, facilities that helps consumers for

fulfilling the requirements which satisfies them.

Self-employed timetable: Self-employed employees work for themselves because they work on

their own schedule. It's about employees doing their own careers.

Be your own boss: Self-employment ensures that you build a boss of your own. It's about

building a self-empire, how consumers will make offers.

Take account of tax incentives for self-employment: self-employment is a tax deductible from

employer expenses from corporate profits.

Keep the income you make: as it raises efficiency, self-employed workers earn money. Self-

employees maintain the money they receive from their company.

Enjoy a job with artistic freedom: this is the draw for creative employees when they work for

their own innovation process as they operate for their own company.

QUESTION 3

Discussion Six badges for trade:

Trade badges are used by HMRC to determine whether an activity can be called a decent

economic behaviour or economic activity or whether it is just an economically active section for

an individual's hobby. To decide whether a hobby is reshaped into a subject to tax exercise,

careful discussion is needed. Trade codes also include components that take purchases into

account, the sequence of transactions (Al Karaawy and Al Baaj, 2018). In June 1955, the Royal

Profit Taxation Committee used court rulings to propose a method for the identification of trade

badges, including the subject matter for realization, the duration of the holding period, the

frequency percentage for transaction costs, the additional works, the situations responsible for

realization, etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benefit motive: It is important for the creation of an enterprise in a market that such practices

contain a profit-making motive. In many other terms, it may also be claimed that an action that

involves the purpose of revenue is considered a trading activity. Resale goods are an adventure

with the essence of trade in money seeking with the major purchase of content. This indicates

that the purchase is not produced for private use, but for company productive investments.

Volume of transactions: the volume of transactions with a trading operation is larger than the

number of predictive activities for regular, systemic transactions. This indicates that gains are

trade profits, deductible on frequent contract undertakings, for also include (Beckers, 2018). This

is the case with the property in question. The resource which involves the source material of the

transaction. Possible options for treating assets as stock of exchange include an equity

acquisition for returns of investment, appreciation of assets needed for personal use, pleasure. In

the case of Murray v IRC, the timber trader buys the rights for the two sales of plantation.

Character of properties: these views on assets, issues emerge as assets are acquired as

investments capable of growing profits, personal assets, investments for plant and equipment

exchange. Marson v Morton was a significant case in this field. This was where property with the

intention of holding it as an estate was bought. The land produced no revenue, but it did have

planning application. Following an unsolicited bid, the property was later sold. As the trade was

well away from the usual operation of the investor (potato merchant) and was equivalent to an

acquisition, it was not a benefit from selling.

Life, interest, for related business activities: this is the case seen in CIR v Fraser. In this scenario,

the taxpayer reveals the woodcutter who buys the whiskey shipment for the securities for the

transactions going out in his business.

Changes in assets: It is necessary for an asset to shift, making it more valuable. In this scenario,

members of the wine cartel buy brandy from South Africa. This illustrates that the investor

argues that the transactions arising from the selling of an investment are money (Cnossen, 2018).

The manner in which the deal is made: HMRC is the guideline that often shows the exchange

that accompanies the undisputed exchange. This comprises three unrelated people that have

acquired the Freight vessel together. For the steam drifter that sold for the earnings, this ship is

transformed. Next, the sale of the vessel that purchased three citizens. The appraisal accounts for

the benefits that are maintained from the profits from the exchange.

contain a profit-making motive. In many other terms, it may also be claimed that an action that

involves the purpose of revenue is considered a trading activity. Resale goods are an adventure

with the essence of trade in money seeking with the major purchase of content. This indicates

that the purchase is not produced for private use, but for company productive investments.

Volume of transactions: the volume of transactions with a trading operation is larger than the

number of predictive activities for regular, systemic transactions. This indicates that gains are

trade profits, deductible on frequent contract undertakings, for also include (Beckers, 2018). This

is the case with the property in question. The resource which involves the source material of the

transaction. Possible options for treating assets as stock of exchange include an equity

acquisition for returns of investment, appreciation of assets needed for personal use, pleasure. In

the case of Murray v IRC, the timber trader buys the rights for the two sales of plantation.

Character of properties: these views on assets, issues emerge as assets are acquired as

investments capable of growing profits, personal assets, investments for plant and equipment

exchange. Marson v Morton was a significant case in this field. This was where property with the

intention of holding it as an estate was bought. The land produced no revenue, but it did have

planning application. Following an unsolicited bid, the property was later sold. As the trade was

well away from the usual operation of the investor (potato merchant) and was equivalent to an

acquisition, it was not a benefit from selling.

Life, interest, for related business activities: this is the case seen in CIR v Fraser. In this scenario,

the taxpayer reveals the woodcutter who buys the whiskey shipment for the securities for the

transactions going out in his business.

Changes in assets: It is necessary for an asset to shift, making it more valuable. In this scenario,

members of the wine cartel buy brandy from South Africa. This illustrates that the investor

argues that the transactions arising from the selling of an investment are money (Cnossen, 2018).

The manner in which the deal is made: HMRC is the guideline that often shows the exchange

that accompanies the undisputed exchange. This comprises three unrelated people that have

acquired the Freight vessel together. For the steam drifter that sold for the earnings, this ship is

transformed. Next, the sale of the vessel that purchased three citizens. The appraisal accounts for

the benefits that are maintained from the profits from the exchange.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Source of finance: Where the trade held for the undertakings, the source of finance is significant.

Fund takes the acquisition of an asset and indicates the redemption of asset debts.

Purchase interval periods, sales: The length of the assets retained is an accurate determinant for

trading. The longer the span of possession, the greater the expenditure.

Different VAT schemes for the various VAT registered companies:

Value added tax is the position of consumption tax on goods where the value added by each

supply chain system, from manufacturing to sales for consumers, is applied. The amount of VAT

charged by consumers for the cost of the goods is the cost of material use for goods previously

taxed (Agarwal and Chakraborty, 2019). VAT is the mechanism for which the value-added tax

for the products supply chain, the services produced by the organization, is used in order to meet

its goals. Economic value tax helps pay for the shared network that supplies the states, taxpayers

that use the products, facilities for the supply of the same locality. Not all localities need VAT

charges, but exports are excluded. VAT is the levy on locations, where the corporate taxes are

the basis for the position of the buyers who have registered for the purchase price of the goods

and services. The terms VAT, GST, tax on sales are used by each other. A sixth increase in VAT

on gross tax receipts. There are VAT calculation methods that include the method of credit bill,

balance bases. Sales purchases are taxed in the credit-invoice process, with the buyer advised of

the VAT on the sale, and companies may earn VAT compensation paid on input products,

services. With the exception of Japan, it is the highest employee base system that is used by

national VATs. The design of accounts base, which involves a company, measures the amount of

all taxable transactions by subtracting the amount of all taxable expenditures in respect to which

the VAT rates are added at the benefit of the variance. This approach is only used for Japan, but

it still includes the Flat Tax terms, which are the tax elements for US legislators to make

proposals (Bushnyakova and Kashirina, 2019). The accounting principles have different

accounting techniques. Accrual accounting compares earnings with the time in that they are

received and matches costs with the period during that they are paid. Although it is more difficult

than paying for the cash base, it provides effective information. The Generic VAT Budgetary

Requirements is a form of recording VAT where VAT is reported and charged on the grounds of

when receipts are given. Underneath the VAT Standard Accounting Scheme, companies accept a

VAT Return four times per year.

Fund takes the acquisition of an asset and indicates the redemption of asset debts.

Purchase interval periods, sales: The length of the assets retained is an accurate determinant for

trading. The longer the span of possession, the greater the expenditure.

Different VAT schemes for the various VAT registered companies:

Value added tax is the position of consumption tax on goods where the value added by each

supply chain system, from manufacturing to sales for consumers, is applied. The amount of VAT

charged by consumers for the cost of the goods is the cost of material use for goods previously

taxed (Agarwal and Chakraborty, 2019). VAT is the mechanism for which the value-added tax

for the products supply chain, the services produced by the organization, is used in order to meet

its goals. Economic value tax helps pay for the shared network that supplies the states, taxpayers

that use the products, facilities for the supply of the same locality. Not all localities need VAT

charges, but exports are excluded. VAT is the levy on locations, where the corporate taxes are

the basis for the position of the buyers who have registered for the purchase price of the goods

and services. The terms VAT, GST, tax on sales are used by each other. A sixth increase in VAT

on gross tax receipts. There are VAT calculation methods that include the method of credit bill,

balance bases. Sales purchases are taxed in the credit-invoice process, with the buyer advised of

the VAT on the sale, and companies may earn VAT compensation paid on input products,

services. With the exception of Japan, it is the highest employee base system that is used by

national VATs. The design of accounts base, which involves a company, measures the amount of

all taxable transactions by subtracting the amount of all taxable expenditures in respect to which

the VAT rates are added at the benefit of the variance. This approach is only used for Japan, but

it still includes the Flat Tax terms, which are the tax elements for US legislators to make

proposals (Bushnyakova and Kashirina, 2019). The accounting principles have different

accounting techniques. Accrual accounting compares earnings with the time in that they are

received and matches costs with the period during that they are paid. Although it is more difficult

than paying for the cash base, it provides effective information. The Generic VAT Budgetary

Requirements is a form of recording VAT where VAT is reported and charged on the grounds of

when receipts are given. Underneath the VAT Standard Accounting Scheme, companies accept a

VAT Return four times per year.

Accrual accounting foundation lets companies manage receivables, payables, etc. The

accounting period lets firms balance sales with their earnings costs, which allows corporations to

achieve greater productivity.

Annual accounting strategies for VAT: Annual financial statements scheme for VAT for HMRC

VAT returns for VAT. The operating budget return for small firms makes management simpler

for them. Advance charges for the corporation's VAT, depending on the corporation's prior

returns.

VAT Cash Accounting Strategies: the VAT system for revenue after payment to consumers, as

opposed to the return of stock after sale to vendors by the corporation.

VAT Margin Schemes: VAT Margin Strategies are applications for vendors. For the firms

paying for the products, the system taxes reflect the variations.

Capital goods strategies: for companies, capital goods show deductions from VAT for properties

that include land, buildings, appliances bought for resale purposes. Such schemes encourage

firms to distribute the initial VAT on properties (Awasthi and Engelschalk, 2018).

VAT retail schemes: VAT strategies for retail transactions are used by corporations for resale

purposes.

Point of Sale System: This is for those firms who, as sales are made, quantify and report VAT.

Apportionment Scheme: And is for all businesses who buy items for the purpose of resale.

Direct Estimation Scheme: This is much of their revenue displays with different VAT prices for

those companies who have the limited sum for the sales for VAT volume.

VAT is the levy on locations, where the corporate taxes are the basis for the position of the

buyers who have applied for the purchase quality of the product and services. The terms VAT,

GST, tax on sales are used by each other. A sixth increase in VAT on gross tax receipts. There

are VAT calculation methods that include the system of credit invoice, account balances

(Timoshenkov and Nashchekina, 2018). Sales purchases are taxed in the credit-invoice process,

with the buyer advised of the VAT on the sale, and companies may earn VAT credit charged on

input products, services.

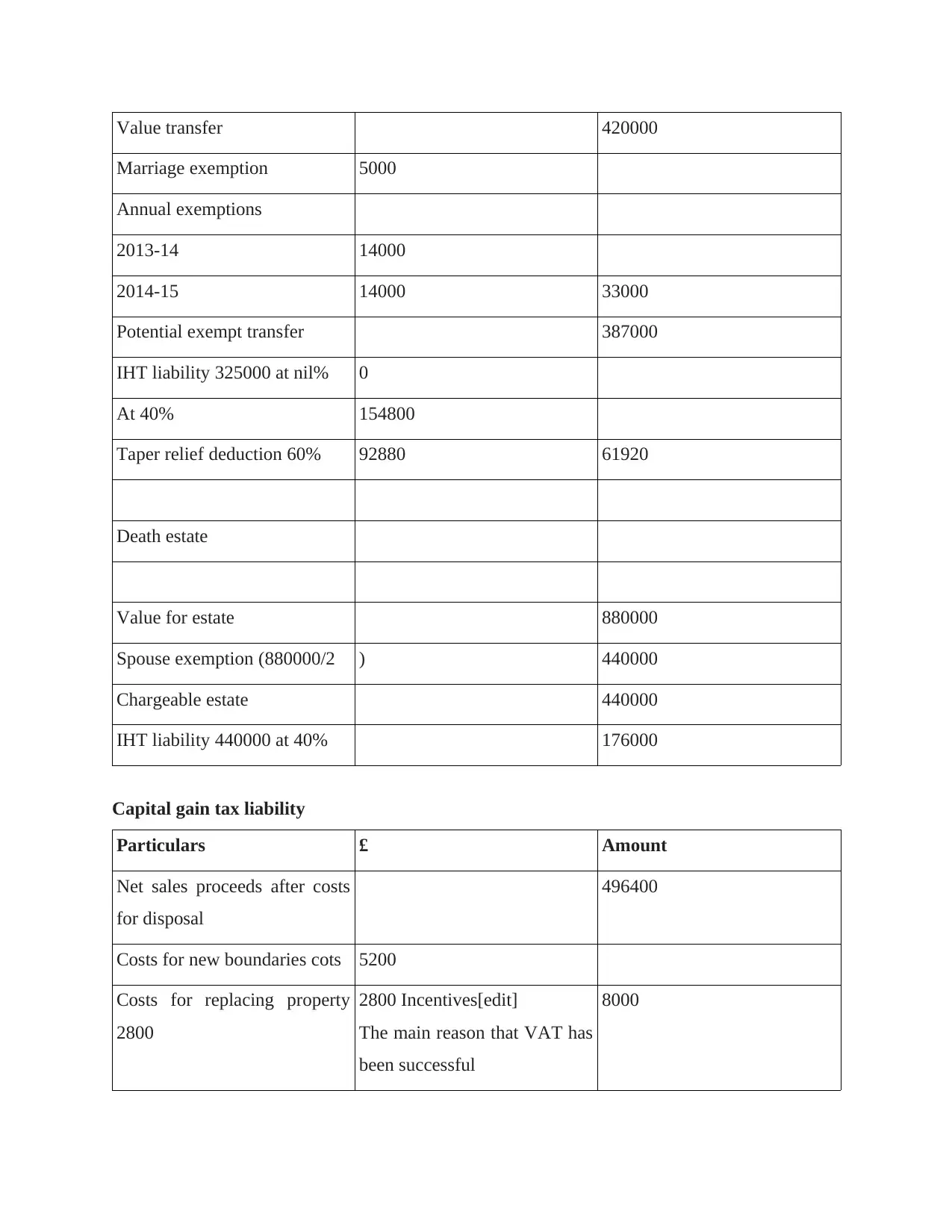

Inheritance tax arising when the death

Particulars £ Amount

accounting period lets firms balance sales with their earnings costs, which allows corporations to

achieve greater productivity.

Annual accounting strategies for VAT: Annual financial statements scheme for VAT for HMRC

VAT returns for VAT. The operating budget return for small firms makes management simpler

for them. Advance charges for the corporation's VAT, depending on the corporation's prior

returns.

VAT Cash Accounting Strategies: the VAT system for revenue after payment to consumers, as

opposed to the return of stock after sale to vendors by the corporation.

VAT Margin Schemes: VAT Margin Strategies are applications for vendors. For the firms

paying for the products, the system taxes reflect the variations.

Capital goods strategies: for companies, capital goods show deductions from VAT for properties

that include land, buildings, appliances bought for resale purposes. Such schemes encourage

firms to distribute the initial VAT on properties (Awasthi and Engelschalk, 2018).

VAT retail schemes: VAT strategies for retail transactions are used by corporations for resale

purposes.

Point of Sale System: This is for those firms who, as sales are made, quantify and report VAT.

Apportionment Scheme: And is for all businesses who buy items for the purpose of resale.

Direct Estimation Scheme: This is much of their revenue displays with different VAT prices for

those companies who have the limited sum for the sales for VAT volume.

VAT is the levy on locations, where the corporate taxes are the basis for the position of the

buyers who have applied for the purchase quality of the product and services. The terms VAT,

GST, tax on sales are used by each other. A sixth increase in VAT on gross tax receipts. There

are VAT calculation methods that include the system of credit invoice, account balances

(Timoshenkov and Nashchekina, 2018). Sales purchases are taxed in the credit-invoice process,

with the buyer advised of the VAT on the sale, and companies may earn VAT credit charged on

input products, services.

Inheritance tax arising when the death

Particulars £ Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Value transfer 420000

Marriage exemption 5000

Annual exemptions

2013-14 14000

2014-15 14000 33000

Potential exempt transfer 387000

IHT liability 325000 at nil% 0

At 40% 154800

Taper relief deduction 60% 92880 61920

Death estate

Value for estate 880000

Spouse exemption (880000/2 ) 440000

Chargeable estate 440000

IHT liability 440000 at 40% 176000

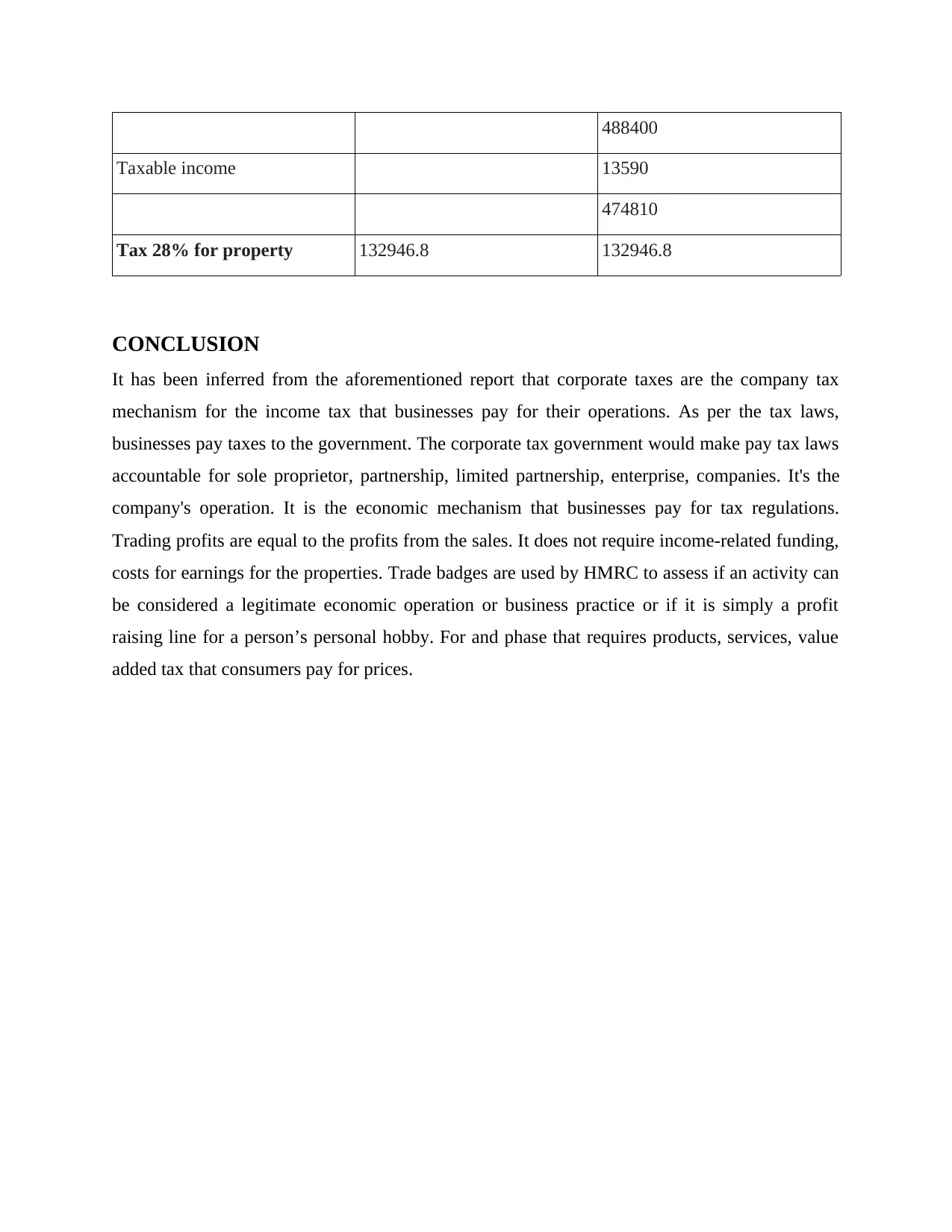

Capital gain tax liability

Particulars £ Amount

Net sales proceeds after costs

for disposal

496400

Costs for new boundaries cots 5200

Costs for replacing property

2800

2800 Incentives[edit]

The main reason that VAT has

been successful

8000

Marriage exemption 5000

Annual exemptions

2013-14 14000

2014-15 14000 33000

Potential exempt transfer 387000

IHT liability 325000 at nil% 0

At 40% 154800

Taper relief deduction 60% 92880 61920

Death estate

Value for estate 880000

Spouse exemption (880000/2 ) 440000

Chargeable estate 440000

IHT liability 440000 at 40% 176000

Capital gain tax liability

Particulars £ Amount

Net sales proceeds after costs

for disposal

496400

Costs for new boundaries cots 5200

Costs for replacing property

2800

2800 Incentives[edit]

The main reason that VAT has

been successful

8000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

488400

Taxable income 13590

474810

Tax 28% for property 132946.8 132946.8

CONCLUSION

It has been inferred from the aforementioned report that corporate taxes are the company tax

mechanism for the income tax that businesses pay for their operations. As per the tax laws,

businesses pay taxes to the government. The corporate tax government would make pay tax laws

accountable for sole proprietor, partnership, limited partnership, enterprise, companies. It's the

company's operation. It is the economic mechanism that businesses pay for tax regulations.

Trading profits are equal to the profits from the sales. It does not require income-related funding,

costs for earnings for the properties. Trade badges are used by HMRC to assess if an activity can

be considered a legitimate economic operation or business practice or if it is simply a profit

raising line for a person’s personal hobby. For and phase that requires products, services, value

added tax that consumers pay for prices.

Taxable income 13590

474810

Tax 28% for property 132946.8 132946.8

CONCLUSION

It has been inferred from the aforementioned report that corporate taxes are the company tax

mechanism for the income tax that businesses pay for their operations. As per the tax laws,

businesses pay taxes to the government. The corporate tax government would make pay tax laws

accountable for sole proprietor, partnership, limited partnership, enterprise, companies. It's the

company's operation. It is the economic mechanism that businesses pay for tax regulations.

Trading profits are equal to the profits from the sales. It does not require income-related funding,

costs for earnings for the properties. Trade badges are used by HMRC to assess if an activity can

be considered a legitimate economic operation or business practice or if it is simply a profit

raising line for a person’s personal hobby. For and phase that requires products, services, value

added tax that consumers pay for prices.

REFERENCES

Books and journals:

Blakeley, G., 2018. Fair dues: Rebalancing business taxation in the UK.

Martins, A., 2019. Country Note: Three Emblematic Measures in Portuguese Business Taxation:

A Preliminary Quantitative Appraisal. Intertax, 47(6/7).

Biddle, N., Fels, K.M. and Sinning, M., 2018. Behavioral insights on business taxation: Evidence

from two natural field experiments. Journal of Behavioral and Experimental Finance, 18,

pp.30-49.

Giroud, X. and Rauh, J., 2019. State taxation and the reallocation of business activity: Evidence

from establishment-level data. Journal of Political Economy, 127(3), pp.1262-1316.

Todtenhaupt, M., 2018. Essays in business taxation (Doctoral dissertation).

Al Karaawy, N.A.A. and Al Baaj, Q.M.A., 2018. Taxation of international business

organizations. Academy of Accounting and Financial Studies Journal, 22(1), pp.1-16.

Beckers, A., 2018. The Creeping Juridification of the Code of Conduct for Business Taxation:

How EU Codes of Conduct Become Hard Law. Yearbook of European Law, 37, pp.569-

596.

Cnossen, S., 2018. Corporation taxes in the European Union: Slowly moving toward

comprehensive business income taxation?. International Tax and Public Finance, 25(3),

pp.808-840.

Agarwal, S. and Chakraborty, L., 2019. Business Taxation in an Emerging Economy: Analysing

Corporate Tax Incidence. Rev. Eur. Stud., 11, p.8.

Bushnyakova, A.I. and Kashirina, M.V., 2019. Some features of small business taxation (on the

example of construction). In Наука и образование в социокультурном пространстве

современного общества (pp. 60-64).

Awasthi, R. and Engelschalk, M., 2018. Taxation and the shadow economy: how the tax system

can stimulate and enforce the formalization of business activities. The World Bank.

Timoshenkov, I.V. and Nashchekina, O.N., 2018. Business taxation: a transaction

Books and journals:

Blakeley, G., 2018. Fair dues: Rebalancing business taxation in the UK.

Martins, A., 2019. Country Note: Three Emblematic Measures in Portuguese Business Taxation:

A Preliminary Quantitative Appraisal. Intertax, 47(6/7).

Biddle, N., Fels, K.M. and Sinning, M., 2018. Behavioral insights on business taxation: Evidence

from two natural field experiments. Journal of Behavioral and Experimental Finance, 18,

pp.30-49.

Giroud, X. and Rauh, J., 2019. State taxation and the reallocation of business activity: Evidence

from establishment-level data. Journal of Political Economy, 127(3), pp.1262-1316.

Todtenhaupt, M., 2018. Essays in business taxation (Doctoral dissertation).

Al Karaawy, N.A.A. and Al Baaj, Q.M.A., 2018. Taxation of international business

organizations. Academy of Accounting and Financial Studies Journal, 22(1), pp.1-16.

Beckers, A., 2018. The Creeping Juridification of the Code of Conduct for Business Taxation:

How EU Codes of Conduct Become Hard Law. Yearbook of European Law, 37, pp.569-

596.

Cnossen, S., 2018. Corporation taxes in the European Union: Slowly moving toward

comprehensive business income taxation?. International Tax and Public Finance, 25(3),

pp.808-840.

Agarwal, S. and Chakraborty, L., 2019. Business Taxation in an Emerging Economy: Analysing

Corporate Tax Incidence. Rev. Eur. Stud., 11, p.8.

Bushnyakova, A.I. and Kashirina, M.V., 2019. Some features of small business taxation (on the

example of construction). In Наука и образование в социокультурном пространстве

современного общества (pp. 60-64).

Awasthi, R. and Engelschalk, M., 2018. Taxation and the shadow economy: how the tax system

can stimulate and enforce the formalization of business activities. The World Bank.

Timoshenkov, I.V. and Nashchekina, O.N., 2018. Business taxation: a transaction

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.