UGB 225 Business Taxation Report - Alternative Assessment 2020/21

VerifiedAdded on 2022/12/27

|12

|3469

|22

Report

AI Summary

This report analyzes various aspects of business taxation, starting with Linda's income statement and calculation of taxable income. It then delves into the distinction between employment and self-employment, discussing the advantages and disadvantages of each, along with factors to determine the correct status. The report explores different VAT schemes and the concept of the "six badges of trade" used by HMRC to determine if an activity constitutes a trade. It also examines inheritance tax and calculates John’s capital gains tax liability. Additionally, the report discusses the IR35 legislation and its implications for contractors and businesses, including the advantages of operating through a limited company. The report includes case studies and provides a thorough overview of the complexities of business taxation.

Business Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

a) Employment vs. self-employment...........................................................................................5

b) Preference for self-employment..............................................................................................6

Question 3........................................................................................................................................8

a) Six badges of trade..................................................................................................................8

b) Different VAT schemes.........................................................................................................10

Question 4......................................................................................................................................12

a) Inheritance tax.......................................................................................................................12

b) John’s capital gains tax liability............................................................................................13

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

a) Employment vs. self-employment...........................................................................................5

b) Preference for self-employment..............................................................................................6

Question 3........................................................................................................................................8

a) Six badges of trade..................................................................................................................8

b) Different VAT schemes.........................................................................................................10

Question 4......................................................................................................................................12

a) Inheritance tax.......................................................................................................................12

b) John’s capital gains tax liability............................................................................................13

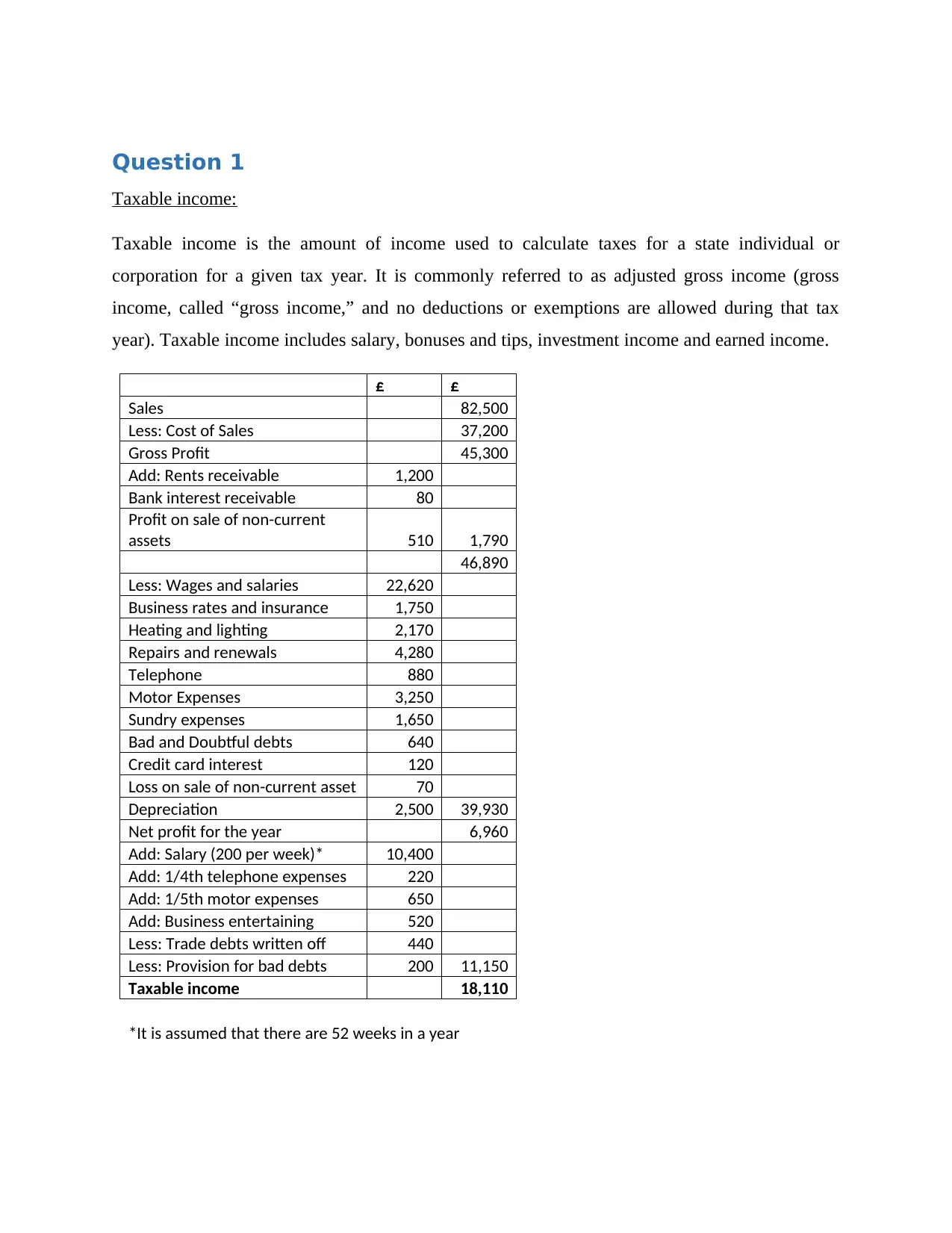

Question 1

Taxable income:

Taxable income is the amount of income used to calculate taxes for a state individual or

corporation for a given tax year. It is commonly referred to as adjusted gross income (gross

income, called “gross income,” and no deductions or exemptions are allowed during that tax

year). Taxable income includes salary, bonuses and tips, investment income and earned income.

£ £

Sales 82,500

Less: Cost of Sales 37,200

Gross Profit 45,300

Add: Rents receivable 1,200

Bank interest receivable 80

Profit on sale of non-current

assets 510 1,790

46,890

Less: Wages and salaries 22,620

Business rates and insurance 1,750

Heating and lighting 2,170

Repairs and renewals 4,280

Telephone 880

Motor Expenses 3,250

Sundry expenses 1,650

Bad and Doubtful debts 640

Credit card interest 120

Loss on sale of non-current asset 70

Depreciation 2,500 39,930

Net profit for the year 6,960

Add: Salary (200 per week)* 10,400

Add: 1/4th telephone expenses 220

Add: 1/5th motor expenses 650

Add: Business entertaining 520

Less: Trade debts written off 440

Less: Provision for bad debts 200 11,150

Taxable income 18,110

*It is assumed that there are 52 weeks in a year

Taxable income:

Taxable income is the amount of income used to calculate taxes for a state individual or

corporation for a given tax year. It is commonly referred to as adjusted gross income (gross

income, called “gross income,” and no deductions or exemptions are allowed during that tax

year). Taxable income includes salary, bonuses and tips, investment income and earned income.

£ £

Sales 82,500

Less: Cost of Sales 37,200

Gross Profit 45,300

Add: Rents receivable 1,200

Bank interest receivable 80

Profit on sale of non-current

assets 510 1,790

46,890

Less: Wages and salaries 22,620

Business rates and insurance 1,750

Heating and lighting 2,170

Repairs and renewals 4,280

Telephone 880

Motor Expenses 3,250

Sundry expenses 1,650

Bad and Doubtful debts 640

Credit card interest 120

Loss on sale of non-current asset 70

Depreciation 2,500 39,930

Net profit for the year 6,960

Add: Salary (200 per week)* 10,400

Add: 1/4th telephone expenses 220

Add: 1/5th motor expenses 650

Add: Business entertaining 520

Less: Trade debts written off 440

Less: Provision for bad debts 200 11,150

Taxable income 18,110

*It is assumed that there are 52 weeks in a year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2

a) Employment vs. self-employment

However, there are some staff members whose status is unclear. For example, you can work

from home and use your computer, but that's worse than an organization where someone controls

and manages things. In this case, you need to decide whether you are an employee or a

freelancer. The payer is not sufficient to confirm your circulation. Payers are biased because they

lack the financial costs and responsibilities of hiring staff (see explanation below). So, if you are

unsure about your condition, answering the following questions can help.

Do you have control over how your job is done, i.e. working independently without

supervision?

Do you have more than one "client"?

Can I contact other customers at any time?

Can you submit your work?

Can you refuse the job?

Do you have the tools and equipment you own? For example, do you use your own

computer, pay for a software subscription, are you responsible for repairing or updating

work equipment in the event of a breakdown?

Do you sell yourself?

Can you hire someone for work without permission?

Do you take risks and responsibilities for the work you do? Can I still pay if I can't get it

right?

Do you have a written contract outlining your working conditions?

Are you billing the customer?

Have you worked for a particular job?

Employees often have a variety of rights, including laws against unfair violations. Holiday and

severance pay and other benefits (including company contributions to health, pension and life

insurance plans). These risks and costs are borne exclusively by the self-employed.

a) Employment vs. self-employment

However, there are some staff members whose status is unclear. For example, you can work

from home and use your computer, but that's worse than an organization where someone controls

and manages things. In this case, you need to decide whether you are an employee or a

freelancer. The payer is not sufficient to confirm your circulation. Payers are biased because they

lack the financial costs and responsibilities of hiring staff (see explanation below). So, if you are

unsure about your condition, answering the following questions can help.

Do you have control over how your job is done, i.e. working independently without

supervision?

Do you have more than one "client"?

Can I contact other customers at any time?

Can you submit your work?

Can you refuse the job?

Do you have the tools and equipment you own? For example, do you use your own

computer, pay for a software subscription, are you responsible for repairing or updating

work equipment in the event of a breakdown?

Do you sell yourself?

Can you hire someone for work without permission?

Do you take risks and responsibilities for the work you do? Can I still pay if I can't get it

right?

Do you have a written contract outlining your working conditions?

Are you billing the customer?

Have you worked for a particular job?

Employees often have a variety of rights, including laws against unfair violations. Holiday and

severance pay and other benefits (including company contributions to health, pension and life

insurance plans). These risks and costs are borne exclusively by the self-employed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In addition to calculating and deducting payroll taxes, employers have to pay extra taxes to

employees. Private entrepreneurs are responsible for measuring and paying taxes.

Employees can take out employment insurance while the EI for self-employed workers is subject

to varying prices and benefits if applicable.

Self-employed people have the right to claim some work-related deductions from their income

which will reduce their income tax, including home office, car and telephone costs. Employees

can receive this type of allowance, but it is more limited.

Loans, mortgages and credit cards are often easier to obtain because employees are believed to

have a more stable income. Self-employed people often have an irregular income stream and a

high risk of liquidity recovery, which can adversely affect access to credit.

b) Preference for self-employment

The monetary law of 1972 decreased the interest for these organizations. The Ministry of

Finance has ordered laws expecting subcontractors to deduct charges from the development

business except if they work with the organization when they can get everything by doubt of far

and wide tax avoidance.

Presently, brief laborers were recruited where they were treated as "paid" office laborers, except

if the organization had an agreement with a restricted organization. Organizations in the

development and different ventures needed to abstain from stressing over numerous "specialists"

beating and leaving, and it turned out to be practically unthinkable for one individual to get a

new line of work through another office instead of through a restricted organization.

The allure was expanded by the Finance Act 2002, which set an underlying corporate expense

pace of 0% (once in the past 10%) for organizations whose benefits don't surpass £10,000. This

proceeded until 2005 when it was suspended.

Against this background, the 1999 IR35 Budget Communication gives interval measures to keep

people from avoiding government duties and protection through corporate use. It produced

results on April 6, 2000 and keeps on being known as IR35.

Be that as it may, managing organizations actually has the accompanying focal points:

employees. Private entrepreneurs are responsible for measuring and paying taxes.

Employees can take out employment insurance while the EI for self-employed workers is subject

to varying prices and benefits if applicable.

Self-employed people have the right to claim some work-related deductions from their income

which will reduce their income tax, including home office, car and telephone costs. Employees

can receive this type of allowance, but it is more limited.

Loans, mortgages and credit cards are often easier to obtain because employees are believed to

have a more stable income. Self-employed people often have an irregular income stream and a

high risk of liquidity recovery, which can adversely affect access to credit.

b) Preference for self-employment

The monetary law of 1972 decreased the interest for these organizations. The Ministry of

Finance has ordered laws expecting subcontractors to deduct charges from the development

business except if they work with the organization when they can get everything by doubt of far

and wide tax avoidance.

Presently, brief laborers were recruited where they were treated as "paid" office laborers, except

if the organization had an agreement with a restricted organization. Organizations in the

development and different ventures needed to abstain from stressing over numerous "specialists"

beating and leaving, and it turned out to be practically unthinkable for one individual to get a

new line of work through another office instead of through a restricted organization.

The allure was expanded by the Finance Act 2002, which set an underlying corporate expense

pace of 0% (once in the past 10%) for organizations whose benefits don't surpass £10,000. This

proceeded until 2005 when it was suspended.

Against this background, the 1999 IR35 Budget Communication gives interval measures to keep

people from avoiding government duties and protection through corporate use. It produced

results on April 6, 2000 and keeps on being known as IR35.

Be that as it may, managing organizations actually has the accompanying focal points:

• Entrepreneurs procure a lowest pay permitted by law and make good on a base duty and public

protection by acquiring a profit pay from the organization's benefits after expense. Circulation

expense will presently don't be collected except if the project worker is needed to pay the duty at

a higher rate.

• This saves public protection reserves (no Northern Ireland in profits) and income since profits

don't pull in PAYE.

• Corporate expense rates are fundamentally lower than personal assessment and public

protection.

• Entrepreneurs, for example, IT and different experts have the chance to telecommute. This can

prompt massive expense investment funds (see beneath).

• Contractor renting organizations save bosses' public protection costs.

IR35 intends to forestall circumvention of duty and government protection by regarding business

visionaries as representatives for charge purposes. In any case, because of laborers under the

work law, for example, ailment stipend, occasion recompense, maternity annuity, and so on, the

remittance isn't gotten.

The IR35 work test is explicit to annual duty and public protection and may give various

outcomes for a similar reason.

Case Study

1. Lime IT Ltd v. Justin, SPC2002

Applies to IR35:

The citizen organization has consented to give IT administrations to different client explicit

ventures (M) through offices. It was relied upon to require a year to finish the task.

The organization (utilizing F as a sole worker) was relied upon to work around 37 hours out of

every week, or as much as M's sensibly required, and the agreement incorporated another

statement that the organization could ship off different representatives. During the term of the

agreement, the citizen worked with 4 different clients. F. worked in one of M's workplaces and to

some extent from his home office. A stay with four PCs here was for a citizen organization.

protection by acquiring a profit pay from the organization's benefits after expense. Circulation

expense will presently don't be collected except if the project worker is needed to pay the duty at

a higher rate.

• This saves public protection reserves (no Northern Ireland in profits) and income since profits

don't pull in PAYE.

• Corporate expense rates are fundamentally lower than personal assessment and public

protection.

• Entrepreneurs, for example, IT and different experts have the chance to telecommute. This can

prompt massive expense investment funds (see beneath).

• Contractor renting organizations save bosses' public protection costs.

IR35 intends to forestall circumvention of duty and government protection by regarding business

visionaries as representatives for charge purposes. In any case, because of laborers under the

work law, for example, ailment stipend, occasion recompense, maternity annuity, and so on, the

remittance isn't gotten.

The IR35 work test is explicit to annual duty and public protection and may give various

outcomes for a similar reason.

Case Study

1. Lime IT Ltd v. Justin, SPC2002

Applies to IR35:

The citizen organization has consented to give IT administrations to different client explicit

ventures (M) through offices. It was relied upon to require a year to finish the task.

The organization (utilizing F as a sole worker) was relied upon to work around 37 hours out of

every week, or as much as M's sensibly required, and the agreement incorporated another

statement that the organization could ship off different representatives. During the term of the

agreement, the citizen worked with 4 different clients. F. worked in one of M's workplaces and to

some extent from his home office. A stay with four PCs here was for a citizen organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Deferral: It was important to "watch" the arbiter and conclude whether to recruit or

independently employed without a go between. As per the realities introduced, the relationship

will act naturally utilized.

Curiously, the complainant was disappointed with the IRS hearing, and Justin (HM Revenue and

Customs) was likewise disappointed with taking care of the case and left a long note that he gave

direction. At the point when he initially distributed his perspectives on the utilization of IR35, he

dealt with new, disliked laws and rules that were especially wrong.

Question 3

a) Six badges of trade

While brand name tests are not comprehensive, HM Revenue and Customs is utilized to decide if

a movement is an authentic monetary/business action or a coincidental action that could profit by

an interest. When choosing whether a side interest has been dependent upon tax collection, it

ought to be deliberately thought of.

Plainly in the wide case law on this matter, the choice of the organization's exhibition or not is

regularly muddled. Indeed, HMRC and the court believe it's essential to take a gander at the

10,000 foot view and not glance at every "symbol" independently or depend a lot on the

exchanging symbol. Sometimes, citizens will contend that the leisure activity is really being

exchanged for certain tax reductions identified with making exchange misfortunes.

HMRC considers the following 9 exchanging pins out of the 6 pins examined underneath as a

feature of an overall examination concerning whether a pastime is a genuine work.

1. Rationale to adapt: The goal to adapt can unmistakably demonstrate your exchanging action.

Nonetheless, this by itself isn't sufficient. Salt v. Chamberlain, Ch D 1979, 53 TC 143; [1979]

Research expert STC 750 endured a misfortune in the financial exchange in the wake of

attempting to foresee the market. The misfortune happened after numerous years and in excess of

200 exchanges. Basically it wasn't viewed as exchange and capital. We presumed that private

value exchanging would never be exchanged. Capital increases charge applies to these

independently employed without a go between. As per the realities introduced, the relationship

will act naturally utilized.

Curiously, the complainant was disappointed with the IRS hearing, and Justin (HM Revenue and

Customs) was likewise disappointed with taking care of the case and left a long note that he gave

direction. At the point when he initially distributed his perspectives on the utilization of IR35, he

dealt with new, disliked laws and rules that were especially wrong.

Question 3

a) Six badges of trade

While brand name tests are not comprehensive, HM Revenue and Customs is utilized to decide if

a movement is an authentic monetary/business action or a coincidental action that could profit by

an interest. When choosing whether a side interest has been dependent upon tax collection, it

ought to be deliberately thought of.

Plainly in the wide case law on this matter, the choice of the organization's exhibition or not is

regularly muddled. Indeed, HMRC and the court believe it's essential to take a gander at the

10,000 foot view and not glance at every "symbol" independently or depend a lot on the

exchanging symbol. Sometimes, citizens will contend that the leisure activity is really being

exchanged for certain tax reductions identified with making exchange misfortunes.

HMRC considers the following 9 exchanging pins out of the 6 pins examined underneath as a

feature of an overall examination concerning whether a pastime is a genuine work.

1. Rationale to adapt: The goal to adapt can unmistakably demonstrate your exchanging action.

Nonetheless, this by itself isn't sufficient. Salt v. Chamberlain, Ch D 1979, 53 TC 143; [1979]

Research expert STC 750 endured a misfortune in the financial exchange in the wake of

attempting to foresee the market. The misfortune happened after numerous years and in excess of

200 exchanges. Basically it wasn't viewed as exchange and capital. We presumed that private

value exchanging would never be exchanged. Capital increases charge applies to these

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

exchanges. For another situation, Rutledge v. CIR-CS 1929, 14 TC 490, the citizen was on a

work excursion to Germany, where the citizen purchased 1 million tissues. At the point when he

got back to England, a heap of tissue was offered to one individual for benefit. The benefit from

purchasing and exchanging enormous amounts of products simultaneously was "the experience

of nature." This case was taken in light of the fact that it was anything but a buy for one's own

necessities or venture purposes.

2. Number of Transactions: Transactions can be exchanging exercises. This is better on the off

chance that you have occasional and precise exchanging. This is Pickford v. Eccentricity CA

1927, 13 TC 251. Partner bought a cotton plant for business use, yet when it was bought it was in

more terrible condition than initially suspected. At that point Syndicate chose to annihilate the

processing plant and sell it individually for benefit. This was rehashed a few times with a few

factories. Because of the tedious idea of the exchange, the benefit was recognized as addressing

the exchange benefit and was liable to burden.

3. Resource Characteristics: A significant case in this field is Marson v. Morton-Ch D 1986, 59

TC 381; STC 463; [1986] 1 WLR 1343. Bought here to protect land for venture. The land was

not beneficial. Nonetheless, he got a structure license. The last was sold as an undesirable offer.

The exchange was a long way from the citizen's standard business (potato exchanging) and was

not of business premium as it resembled a speculation. The arrangement was not courageous.

Another illustration of intelligence on Chamberlain-CA 1968, 45 TC 92; 1 WLR 275; [1969] 1

All ER 332s consider the rule of "Pride in Ownership of Assets" that doesn't produce pay.

Citizens purchased two huge bars of cash to forestall the downgrading of the pound. It is smarter

to purchase and back some with an advance. Since it was bought in a brief timeframe for benefit.

Exchanging was characteristically dangerous and esteemed as exchanging benefit.

4. Presence of business or comparable interests: This is the CIR v. Fraser [1942] 24TC498. For

this situation, the citizen was a logger who purchased a lot of bourbon with gems. At that point

he sold bourbon through revenue driven office. In his choice, the appointed authority noted:

Recognition measure. In particular, the real connection among respondents and bourbon is

equivalent to by and large exchange. "

5. Changes in accessibility: It is imperative to distinguish changes or adjustments to the resource

that could make the resource more attractive. Cape Brandy Syndicate v. CIR-CA 1921, 12 TC

work excursion to Germany, where the citizen purchased 1 million tissues. At the point when he

got back to England, a heap of tissue was offered to one individual for benefit. The benefit from

purchasing and exchanging enormous amounts of products simultaneously was "the experience

of nature." This case was taken in light of the fact that it was anything but a buy for one's own

necessities or venture purposes.

2. Number of Transactions: Transactions can be exchanging exercises. This is better on the off

chance that you have occasional and precise exchanging. This is Pickford v. Eccentricity CA

1927, 13 TC 251. Partner bought a cotton plant for business use, yet when it was bought it was in

more terrible condition than initially suspected. At that point Syndicate chose to annihilate the

processing plant and sell it individually for benefit. This was rehashed a few times with a few

factories. Because of the tedious idea of the exchange, the benefit was recognized as addressing

the exchange benefit and was liable to burden.

3. Resource Characteristics: A significant case in this field is Marson v. Morton-Ch D 1986, 59

TC 381; STC 463; [1986] 1 WLR 1343. Bought here to protect land for venture. The land was

not beneficial. Nonetheless, he got a structure license. The last was sold as an undesirable offer.

The exchange was a long way from the citizen's standard business (potato exchanging) and was

not of business premium as it resembled a speculation. The arrangement was not courageous.

Another illustration of intelligence on Chamberlain-CA 1968, 45 TC 92; 1 WLR 275; [1969] 1

All ER 332s consider the rule of "Pride in Ownership of Assets" that doesn't produce pay.

Citizens purchased two huge bars of cash to forestall the downgrading of the pound. It is smarter

to purchase and back some with an advance. Since it was bought in a brief timeframe for benefit.

Exchanging was characteristically dangerous and esteemed as exchanging benefit.

4. Presence of business or comparable interests: This is the CIR v. Fraser [1942] 24TC498. For

this situation, the citizen was a logger who purchased a lot of bourbon with gems. At that point

he sold bourbon through revenue driven office. In his choice, the appointed authority noted:

Recognition measure. In particular, the real connection among respondents and bourbon is

equivalent to by and large exchange. "

5. Changes in accessibility: It is imperative to distinguish changes or adjustments to the resource

that could make the resource more attractive. Cape Brandy Syndicate v. CIR-CA 1921, 12 TC

358; [1921] 2 KB 403 individuals from the Wine Syndicate framed a different organization to

buy cognac in South Africa. Some were delivered east, others were shipped off London, blended

in with French brands, repacked and sold for benefit. Citizens attempted to demonstrate that the

exchange was basically capital because of the offer of the venture. It was believed that an

exchange or business was completed and estimated as an exchange acquire.

6. The most effective method to Sell: HM Revenue and Customs controls that an exchange is

consistently a rule on the off chance that it follows a "non-questioned exchange" exchange. CIR

v. Livingstone et al. 11TC538 methods three autonomous people who together bought a payload

transport. The boat was changed over into a liner and sold for benefit. It was the principal

transport purchased by three individuals. The exchange result has happened and the income

figuring has been affirmed

b) Different VAT schemes

Some of the different types of VAT schemes have been discussed below:

1. VAT Annual Accounting Scheme

Organizations enrolled as VAT payers regularly send VAT discounts and installments to HM

Revenue and Customs four times each year. Be that as it may, with the yearly VAT detailing

plan, you just need to do this once every year. This one-time report expects to encourage

independent venture the board. During the year, the organization's VAT is paid dependent on a

year ago's government form (or a harsh gauge if this is the first run through). After recording

your yearly government form, you will be paid or discounted the contrast between your genuine

VAT and your prepaid sum.

To partake in the program, your business should be enlisted as a VAT payer, and your yearly

VAT available turnover should be under £135 million. You are not qualified on the off chance

that you are bankrupt, have not been educated regarding VAT installments or discounts, left the

framework over the most recent a year, or have a place with a division or gathering of a VAT

paying organization. - Enrollment.

2. VAT Cash Accounting Scheme

buy cognac in South Africa. Some were delivered east, others were shipped off London, blended

in with French brands, repacked and sold for benefit. Citizens attempted to demonstrate that the

exchange was basically capital because of the offer of the venture. It was believed that an

exchange or business was completed and estimated as an exchange acquire.

6. The most effective method to Sell: HM Revenue and Customs controls that an exchange is

consistently a rule on the off chance that it follows a "non-questioned exchange" exchange. CIR

v. Livingstone et al. 11TC538 methods three autonomous people who together bought a payload

transport. The boat was changed over into a liner and sold for benefit. It was the principal

transport purchased by three individuals. The exchange result has happened and the income

figuring has been affirmed

b) Different VAT schemes

Some of the different types of VAT schemes have been discussed below:

1. VAT Annual Accounting Scheme

Organizations enrolled as VAT payers regularly send VAT discounts and installments to HM

Revenue and Customs four times each year. Be that as it may, with the yearly VAT detailing

plan, you just need to do this once every year. This one-time report expects to encourage

independent venture the board. During the year, the organization's VAT is paid dependent on a

year ago's government form (or a harsh gauge if this is the first run through). After recording

your yearly government form, you will be paid or discounted the contrast between your genuine

VAT and your prepaid sum.

To partake in the program, your business should be enlisted as a VAT payer, and your yearly

VAT available turnover should be under £135 million. You are not qualified on the off chance

that you are bankrupt, have not been educated regarding VAT installments or discounts, left the

framework over the most recent a year, or have a place with a division or gathering of a VAT

paying organization. - Enrollment.

2. VAT Cash Accounting Scheme

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This framework permits purchasers to pay VAT on deals in the wake of paying you, and VAT on

stock after installment to the provider. This is not the same as the standard method of introducing

information and paying assessments regardless of whether the receipt has not been paid.

To meet all requirements for the program, your business should be enlisted as a VAT payer and

your assessed available VAT turnover throughout the following a year should not surpass £1.35

million. Company can utilize this framework on the off chance that you utilized a single amount

installment a year ago, delayed your VAT discount, or submitted a VAT related infringement.

In the event that you are qualified, you can join toward the start of the VAT detailing period and

you don't have to report it to HM Revenue and Customs.

3. VAT Margin Scheme

The VAT edge framework is utilized by vendors of collectibles, frugality, workmanship and

different assortments. The framework demands charge on the contrast between the sum the

organization pays for the item and the sum it sells (rather than burdening the absolute deals cost).

To join the framework, you should simply keep definite records of qualified things and show

them on VAT revelation. These things should contain a receipt for everything and stock book.

There are a few exemptions for the VAT edge framework. There are special cases, particularly

for speculations, adornments and metals, just as all buys subject to VAT. There are additionally

unique conditions for utilized vehicles, barters, pawn shops, ponies and horses.

4. Capital Goods Scheme

Capital merchandise plans are utilized by organizations to apply for VAT waivers or discounts

for resources, for example, land, land or gear gained for resale yet utilized by the proprietor for

different purposes. This can be deliberate or an adjustment in the real circumstance.

Basically, this plan permits organizations to scatter their initially proclaimed VAT across their

resources throughout the long term. Everything VAT can be repaid if the resource is utilized

uniquely for business purposes. For business and individual use, you can guarantee a bit of the

VAT, which is known as a "halfway waiver".

5. Retail VAT Scheme

stock after installment to the provider. This is not the same as the standard method of introducing

information and paying assessments regardless of whether the receipt has not been paid.

To meet all requirements for the program, your business should be enlisted as a VAT payer and

your assessed available VAT turnover throughout the following a year should not surpass £1.35

million. Company can utilize this framework on the off chance that you utilized a single amount

installment a year ago, delayed your VAT discount, or submitted a VAT related infringement.

In the event that you are qualified, you can join toward the start of the VAT detailing period and

you don't have to report it to HM Revenue and Customs.

3. VAT Margin Scheme

The VAT edge framework is utilized by vendors of collectibles, frugality, workmanship and

different assortments. The framework demands charge on the contrast between the sum the

organization pays for the item and the sum it sells (rather than burdening the absolute deals cost).

To join the framework, you should simply keep definite records of qualified things and show

them on VAT revelation. These things should contain a receipt for everything and stock book.

There are a few exemptions for the VAT edge framework. There are special cases, particularly

for speculations, adornments and metals, just as all buys subject to VAT. There are additionally

unique conditions for utilized vehicles, barters, pawn shops, ponies and horses.

4. Capital Goods Scheme

Capital merchandise plans are utilized by organizations to apply for VAT waivers or discounts

for resources, for example, land, land or gear gained for resale yet utilized by the proprietor for

different purposes. This can be deliberate or an adjustment in the real circumstance.

Basically, this plan permits organizations to scatter their initially proclaimed VAT across their

resources throughout the long term. Everything VAT can be repaid if the resource is utilized

uniquely for business purposes. For business and individual use, you can guarantee a bit of the

VAT, which is known as a "halfway waiver".

5. Retail VAT Scheme

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The retail VAT plot is simply accessible to retailers and has a yearly turnover barring deals duty

of under £130 million. Organizations that blend retail and non-retail can likewise utilize the

framework; however just for retail use (non-retail stock should be accounted for consistently).

There are three regular VAT merchants utilized by various organizations.

Point of Sale Scheme -times used to ascertain and enroll VAT discounted.

Apportionment Scheme - Shared dissemination framework times used to purchase

products available to be purchased.

Direct Calculation Scheme -for organizations that sell just a modest quantity of deals at

a fixed VAT rate and sell a large portion of their deals at various rates.

Question 4

a) Inheritance tax

The British inheritance tax system is controversial and unpopular. Market Financial Solutions'

Paresh Raja explains some tax issues and discusses possible reforms. At the Conservative Party's

2019 meeting in early October 2019, British Prime Minister Sajid Javid publicly stated that the

British Inheritance Tax (IHT) law needs long-term reform. Recognizing that he saw the general

opposition of the IHT community, the minister even suggested that the so-called death tax

government could give up entirely.

IHT schemes vary according to national jurisdiction. Looking at Germany, for example, small

inheritance is tax-free and a differential scale is used that takes into account family relationships

and inheritance values before issuing the final invoice. The standard rate of inheritance tax is

40%. You are only charged for the portion of the property that exceeds the specified criteria.

Some gifts made during a lifetime may be subject to tax upon death. Depending on when the gift

was made, "cone relief" can mean that the inheritance tax on the gift is less than 40%. Other

benefits, such as Business Relief, allow you to transfer certain assets without reducing

inheritance taxes or invoices.

Total value of the estate = £880,000

Nil rate band = £325,000 (threshold free amount)

of under £130 million. Organizations that blend retail and non-retail can likewise utilize the

framework; however just for retail use (non-retail stock should be accounted for consistently).

There are three regular VAT merchants utilized by various organizations.

Point of Sale Scheme -times used to ascertain and enroll VAT discounted.

Apportionment Scheme - Shared dissemination framework times used to purchase

products available to be purchased.

Direct Calculation Scheme -for organizations that sell just a modest quantity of deals at

a fixed VAT rate and sell a large portion of their deals at various rates.

Question 4

a) Inheritance tax

The British inheritance tax system is controversial and unpopular. Market Financial Solutions'

Paresh Raja explains some tax issues and discusses possible reforms. At the Conservative Party's

2019 meeting in early October 2019, British Prime Minister Sajid Javid publicly stated that the

British Inheritance Tax (IHT) law needs long-term reform. Recognizing that he saw the general

opposition of the IHT community, the minister even suggested that the so-called death tax

government could give up entirely.

IHT schemes vary according to national jurisdiction. Looking at Germany, for example, small

inheritance is tax-free and a differential scale is used that takes into account family relationships

and inheritance values before issuing the final invoice. The standard rate of inheritance tax is

40%. You are only charged for the portion of the property that exceeds the specified criteria.

Some gifts made during a lifetime may be subject to tax upon death. Depending on when the gift

was made, "cone relief" can mean that the inheritance tax on the gift is less than 40%. Other

benefits, such as Business Relief, allow you to transfer certain assets without reducing

inheritance taxes or invoices.

Total value of the estate = £880,000

Nil rate band = £325,000 (threshold free amount)

Tax chargeable amount = £880,000 - £325,000 = £555,000

According to the UK’s tax law, inheritance tax rate is 40% of chargeable amount.

Thus, the total inheritance tax that will be payable as a result of Peter’s death is:

40% of £555,000 = £222,200

b) John’s capital gains tax liability

Value of the house gifted to John = £420,000

Profit from sale of house = (£496,400 - £5,200 - £2,800) - £420,000

= £68,000

Thus John’s capital gain tax liability = £68,000

According to the UK’s tax law, inheritance tax rate is 40% of chargeable amount.

Thus, the total inheritance tax that will be payable as a result of Peter’s death is:

40% of £555,000 = £222,200

b) John’s capital gains tax liability

Value of the house gifted to John = £420,000

Profit from sale of house = (£496,400 - £5,200 - £2,800) - £420,000

= £68,000

Thus John’s capital gain tax liability = £68,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.