Accounting Assignment: Recording Business Transactions and Analysis

VerifiedAdded on 2023/01/03

|10

|1828

|75

Homework Assignment

AI Summary

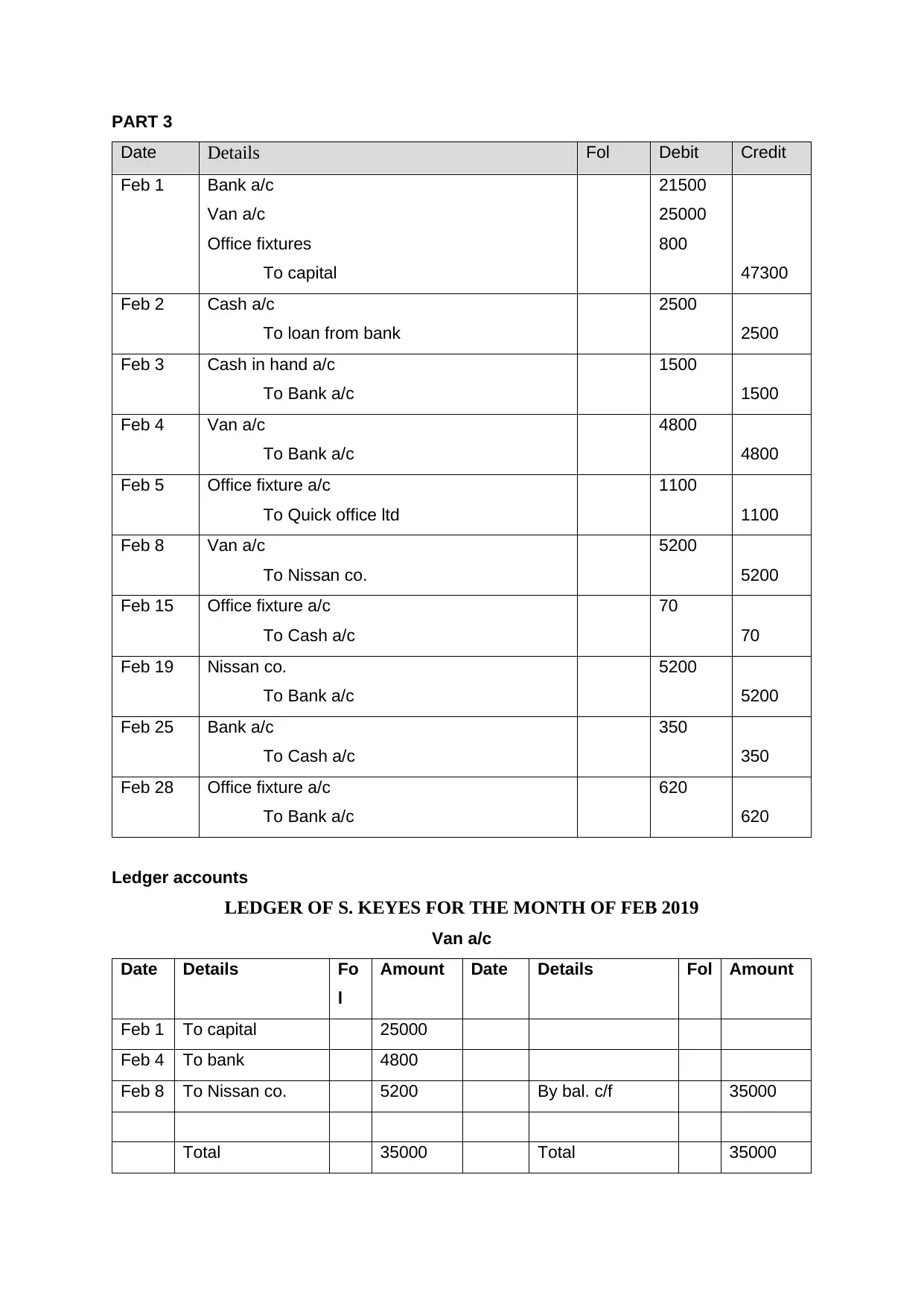

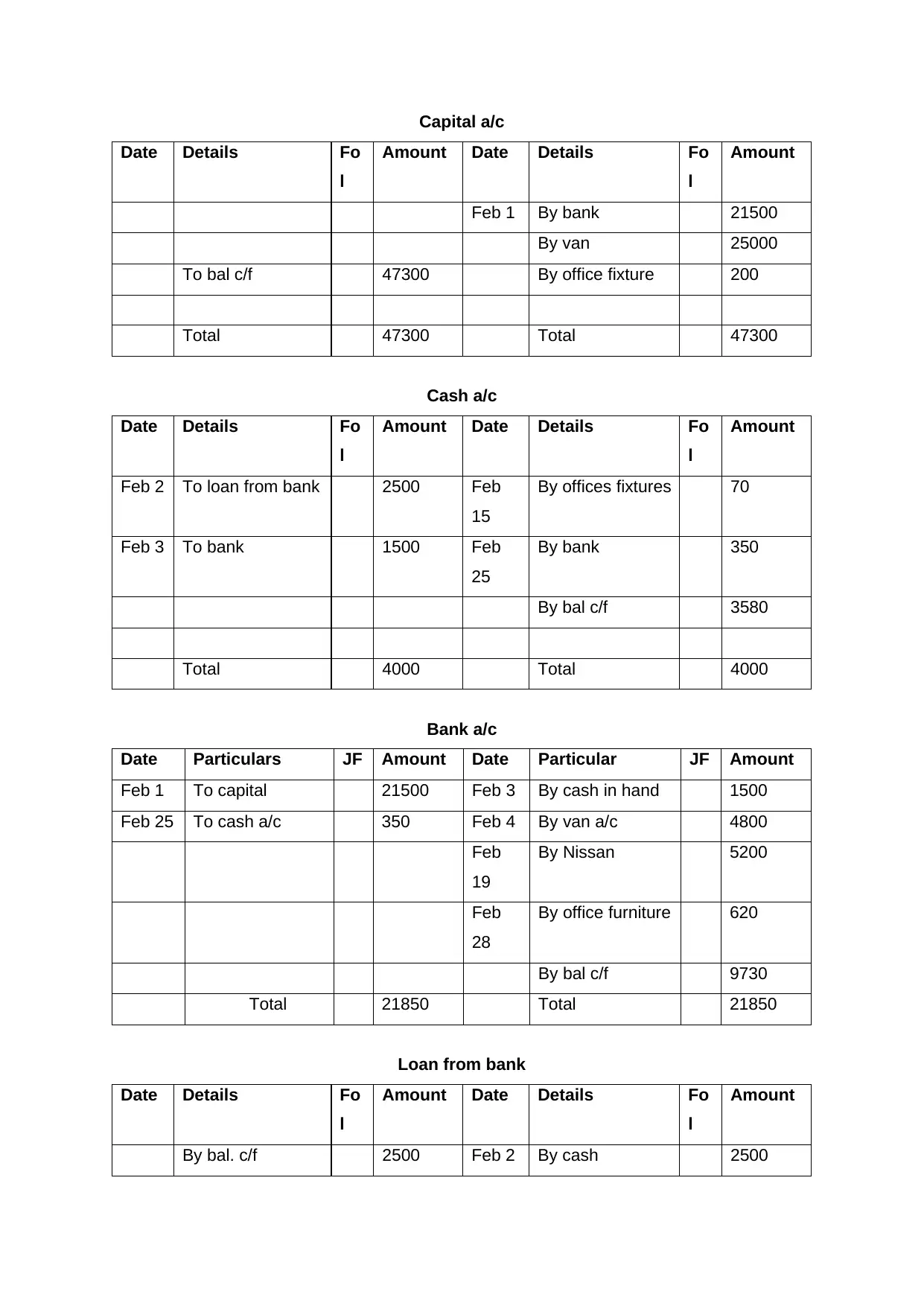

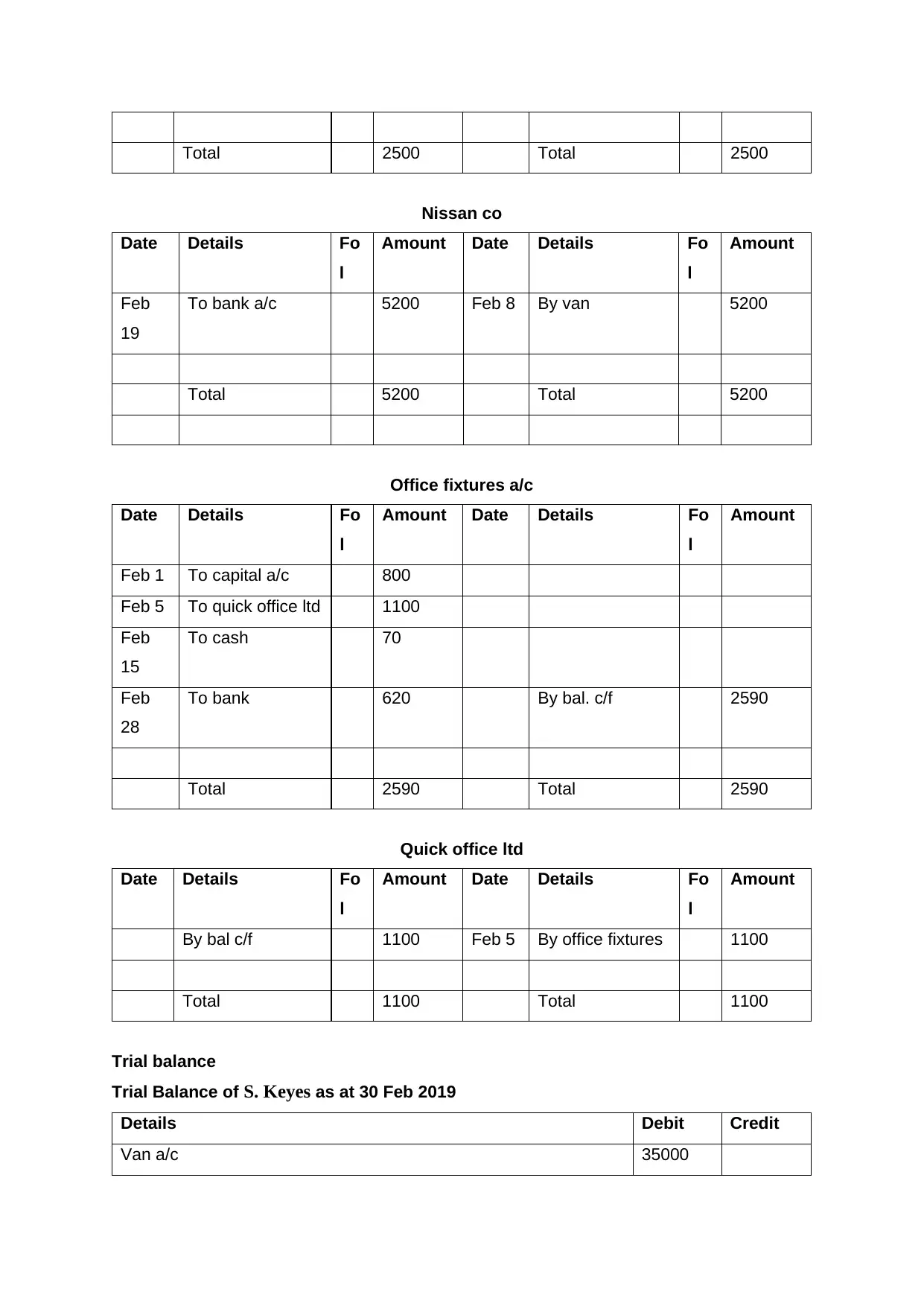

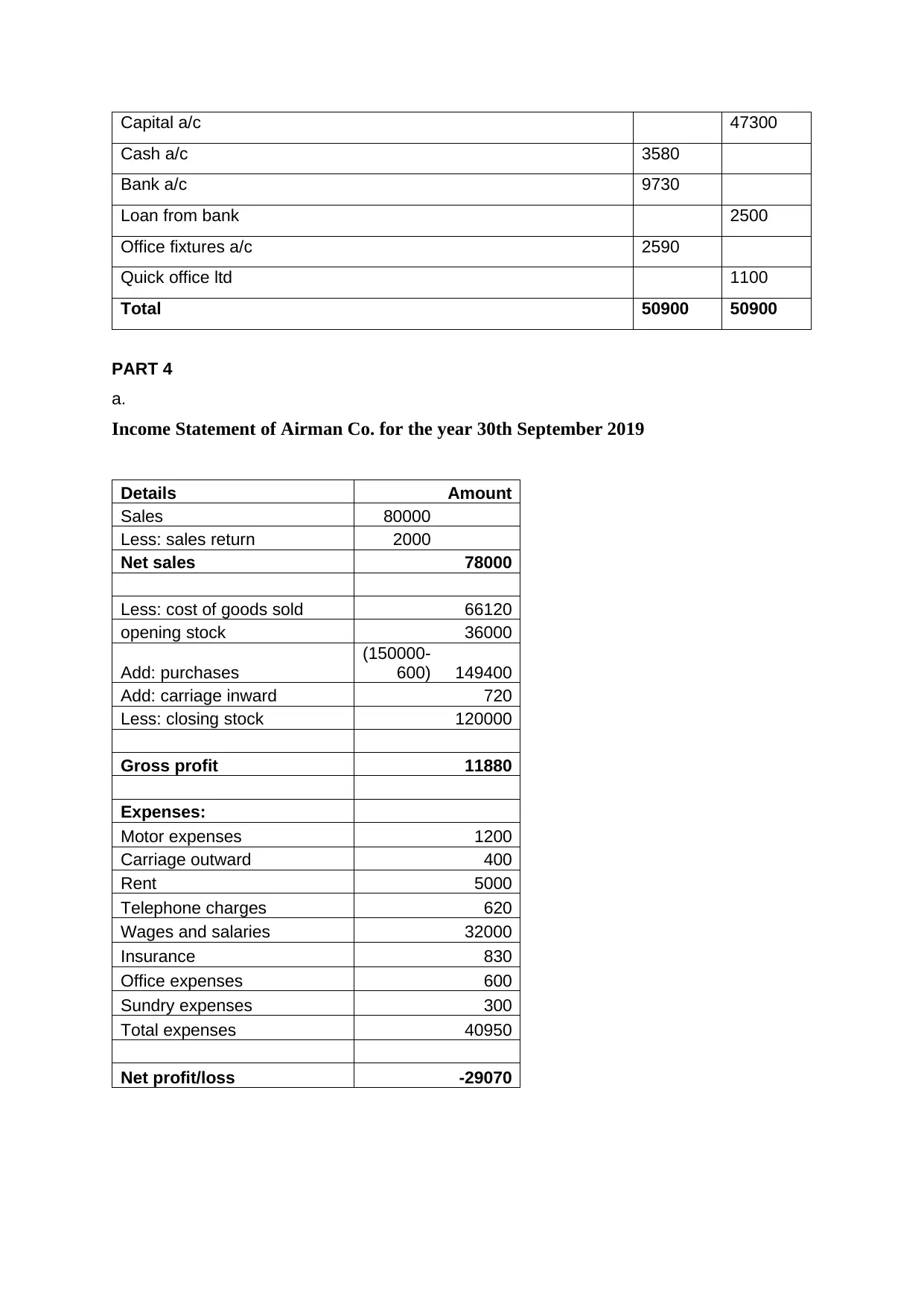

This assignment solution covers the recording of business transactions, including journal entries, ledger accounts, and the preparation of a trial balance and income statement. The solution begins with an analysis of decision-makers who use accounting information, differentiating between internal and external users. It includes journal entries for David Wise, ledger accounts for S. Keyes, and a trial balance. The solution also presents an income statement for Airman Co. and analyzes the company's financial performance. Furthermore, the solution analyzes the impact of the COVID-19 pandemic on businesses using a PESTLE analysis, examining political, economic, social, technological, legal, and environmental factors. The references section lists the sources used in the assignment.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.